AI In Hospital Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 18.02 Billion |

| Growth Rate (2026 - 2031) | 22.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Hospital Asset Management Market Analysis by Mordor Intelligence

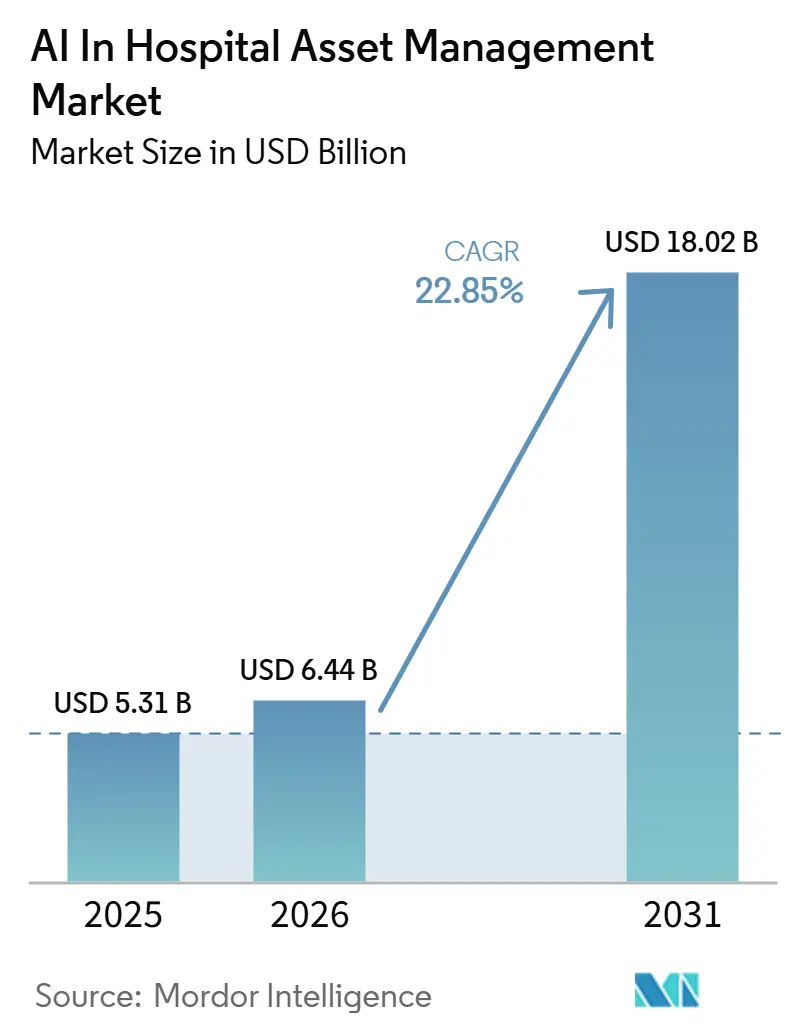

The AI In Hospital Asset Management Market size was valued at USD 5.31 billion in 2025 and is estimated to grow from USD 6.44 billion in 2026 to reach USD 18.02 billion by 2031, at a CAGR of 22.85% during the forecast period (2026-2031).

The AI in hospital asset management market is moving beyond basic equipment location and toward a broader operating model that combines tracking, predictive maintenance, workflow coordination, and audit readiness. Hospitals are giving more weight to platforms that turn location and usage data into actions on redeployment, service scheduling, and uptime control, which is widening the software layer in the AI in hospital asset management market. Regulation is also shaping purchasing decisions because providers need stronger records on device traceability, maintenance discipline, and technology inventories, which raises the value of compliance-ready tools in the AI in hospital asset management market. Smart hospital programs, digital twin projects, and subscription-led delivery models are reducing deployment friction in some settings, while cybersecurity, interoperability, and implementation cost still slow full-scale rollouts across the AI in hospital asset management market. Competition remains active between diversified healthcare technology suppliers, RTLS specialists, and workflow software vendors, and the firms that combine tracking accuracy with usable analytics and service support are improving their position in the AI in hospital asset management market.

Key Report Takeaways

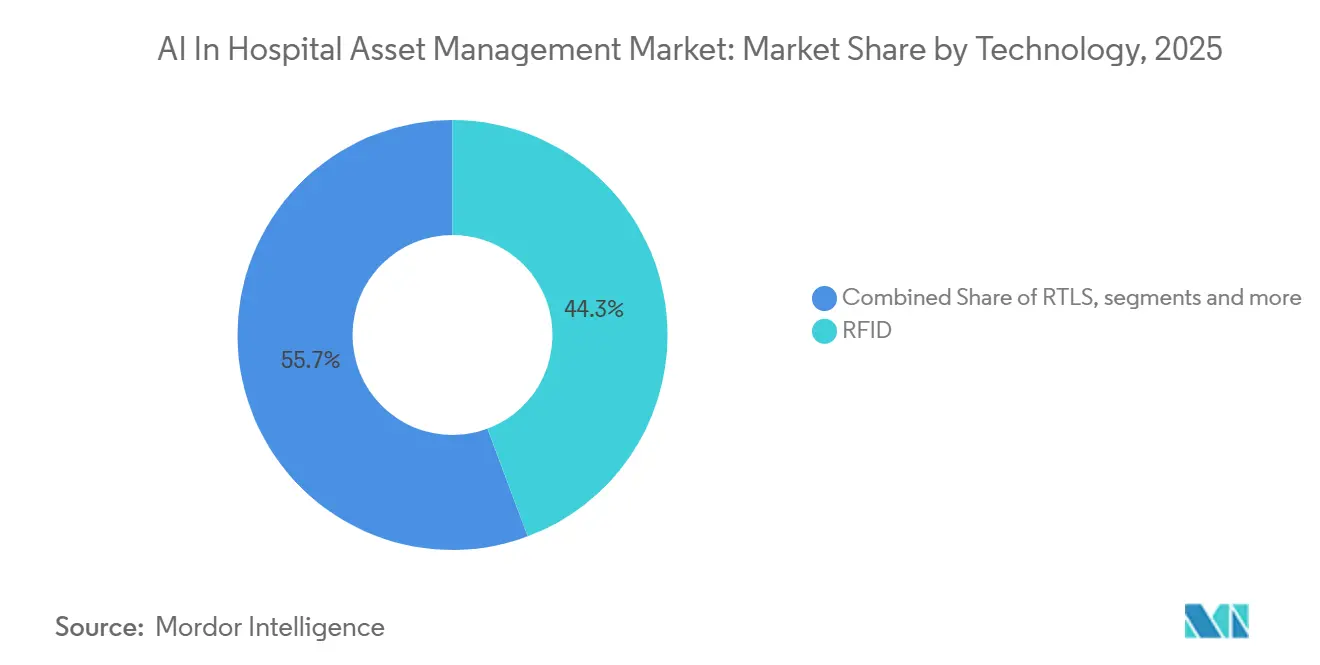

- By technology, RFID held 44.27% of revenue in 2025, while RTLS is projected to expand at 23.13% CAGR through 2031.

- By component, software and analytics led with 56.11% revenue share in 2025, while services are forecasted to grow at 23.72% CAGR through 2031.

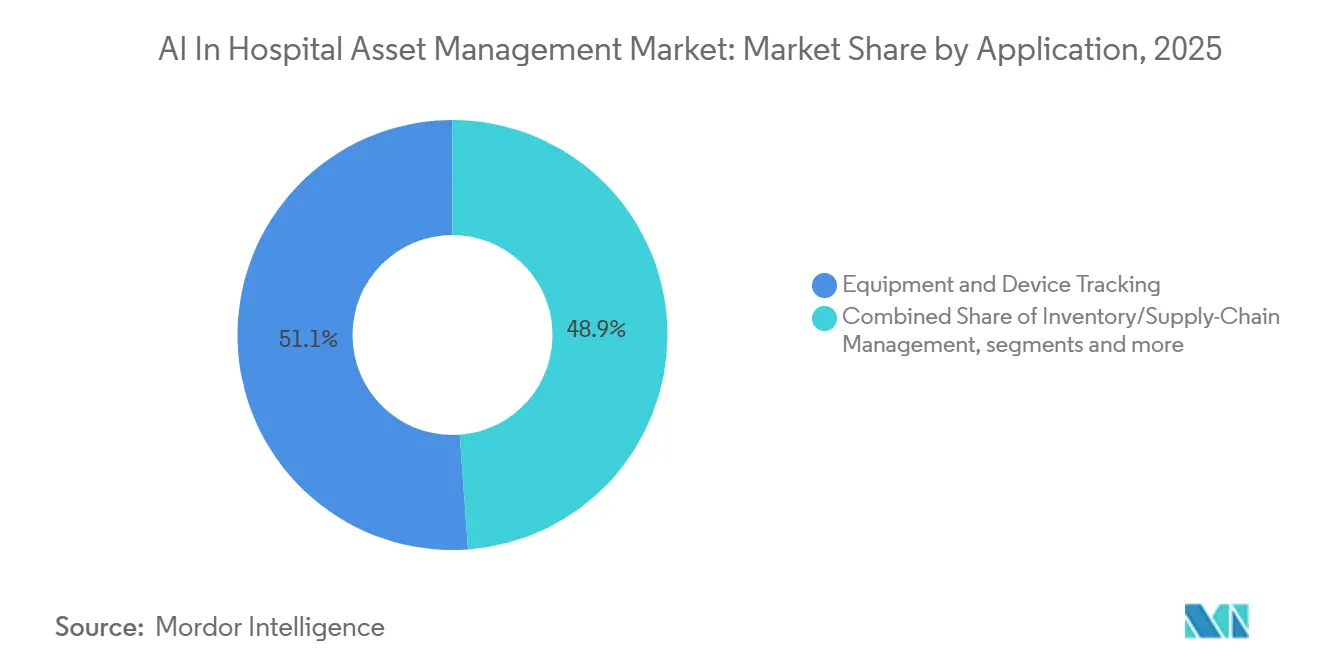

- By application, equipment and device tracking accounted for 51.15% of revenue in 2025, while bed and capacity management is projected to advance at 24.71% CAGR through 2031.

- By end-user, hospitals held 40.28% revenue share in 2025, while ambulatory surgical centers are expected to grow at 25.22% CAGR through 2031.

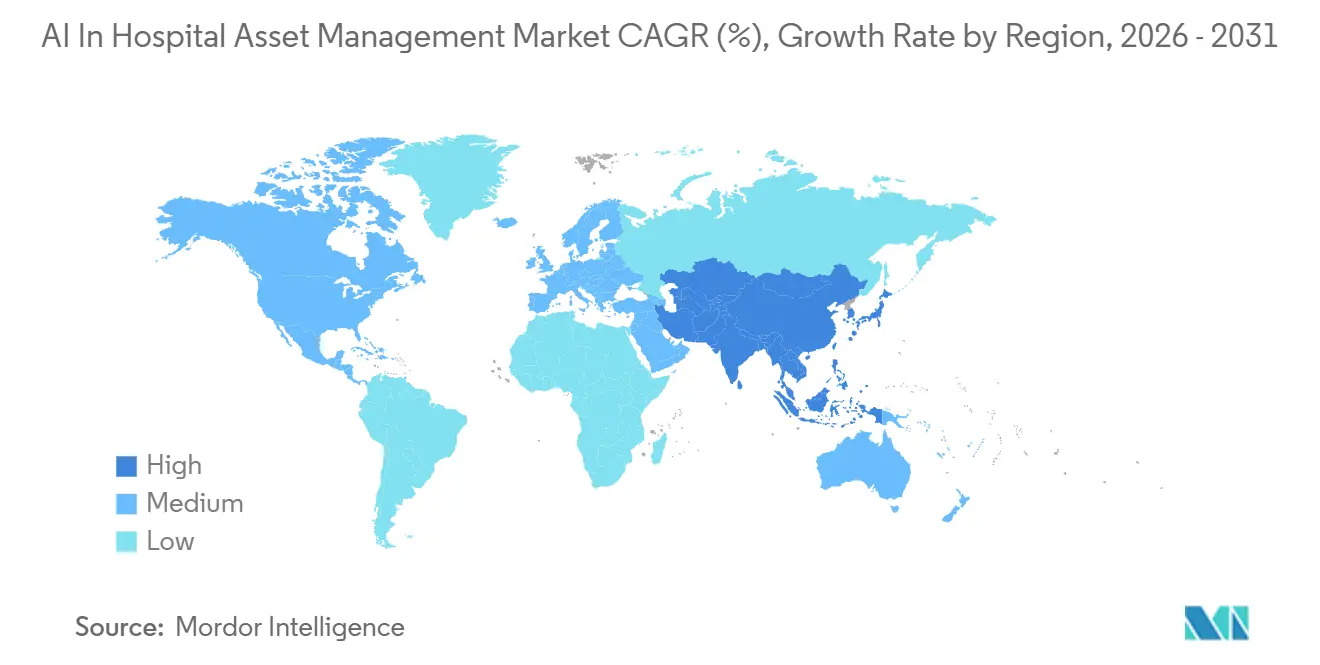

- By geography, North America led with 43.12% revenue share in 2025, while Asia-Pacific is projected to record 27.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Hospital Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of AI-Powered Real-Time Asset Tracking and Monitoring | +4.8% | Global, concentrated in North America and APAC | Short term (≤ 2 years) |

| Increasing Need to Optimize Asset Utilization and Reduce Equipment Downtime | +3.7% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Expansion of Smart Hospitals and AI-Enabled Connected Healthcare Infrastructure | +2.9% | APAC core, China, South Korea, India, with spillover to MEA and South America | Medium term (2-4 years) |

| Rising Demand for Predictive Maintenance of Critical Medical Equipment | +3.2% | North America and EU, with early adoption in Australia and Japan | Medium term (2-4 years) |

| Integration of AI, IoT, And Digital Twin Technologies for Intelligent Asset Management | +3.5% | Global, with accelerating deployments in China, Germany, and Singapore | Long term (≥ 4 years) |

| Increasing Focus on Operational Efficiency, Cost Optimization, and Workflow Automation | +2.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of AI-Powered Real-Time Asset Tracking and Monitoring

The AI in hospital asset management market is gaining from a clear shift in buyer expectations, because hospitals now want systems that do more than show where equipment is located. Real-time tracking has become more valuable when it feeds AI models that connect movement data with staffing pressure, room demand, and equipment availability. This allows hospitals to move from reactive search and dispatch activity to earlier decisions on where devices should be positioned before shortages appear. The return profile also improves when providers can build on existing RFID and RTLS infrastructure instead of replacing earlier investments, which lowers switching friction in the AI in hospital asset management market. A 2025 peer-reviewed hospital case study showed that an IoT and Random Forest maintenance model across 150 vital equipment units reduced unplanned downtime by 27% and improved maintenance cost efficiency by 20%.[1]Dhruv Rawal et al., “Optimizing Hospital Resource Management with IoT and Machine Learning: A Case Study in Predictive Maintenance,” Journal of Nephrology Studies, doi.org. The same pattern supports stronger buying interest because hospitals can connect location visibility with measurable uptime and service gains in the AI in hospital asset management market.

Increasing Need to Optimize Asset Utilization and Reduce Equipment Downtime

The AI in hospital asset management market is also supported by the need to use existing equipment more effectively before new capital is approved. Large hospitals often maintain equipment pools that exceed actual utilization needs because planners prepare for peak demand, and that cushions service risk but ties up capital. The issue is more serious when assets are misplaced, underused, or unavailable during care peaks, because clinical workflow slows while procurement costs remain high. Impinj states that 15% of hospital assets are lost or stolen each year, which shows why utilization analytics and continuous tracking remain practical priorities for provider organizations.[2]Impinj, “RAIN RFID Solutions for Hospitals and the Healthcare Industry,” impinj.com.AI-driven redeployment logic helps hospitals identify idle devices, shift them across departments, and delay avoidable purchases, which improves the economic case for the AI in hospital asset management market. This is also pulling decision making upward from technical teams to executive leadership, because utilization and downtime are now linked more directly with margin discipline and service continuity.

Expansion of Smart Hospitals and AI-Enabled Connected Healthcare Infrastructure

The AI in hospital asset management market is benefiting from new hospital builds and digital modernization programs that can embed asset intelligence at the design stage. Pre-wired environments and integrated digital backbones reduce the burden of retrofits and make it easier to connect equipment data, facility systems, and operational dashboards. A 2025 peer-reviewed German analysis also placed AI-led hospital logistics, including asset tracking and resource scheduling, within core operational infrastructure rather than optional digital tooling.[3]Florian Decker et al., “Künstliche Intelligenz in der Krankenhauslogistik und in betrieblichen Prozessen,” Bundesgesundheitsblatt – Gesundheitsforschung – Gesundheitsschutz, springer.com.As that view spreads, the AI in hospital asset management market gains a longer planning horizon and access to larger institutional budgets.

Rising Demand for Predictive Maintenance of Critical Medical Equipment

The AI in hospital asset management market is seeing strong demand from predictive maintenance because it raises the value of location systems beyond search and retrieval. When hospitals combine runtime, vibration, temperature, and usage data with machine learning, they can identify pre-failure conditions before a critical device drops out of service. That shift reduces emergency repair activity and also lowers the clinical risk tied to equipment failure during active care. Hospitals also gain better lifecycle records when service actions, utilization intensity, and maintenance compliance are captured digitally inside the AI in hospital asset management market. This supports procurement planning, total cost control, and easier adherence to manufacturer maintenance schedules and medical device quality systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Implementation and Ongoing Maintenance Costs | -2.1% | Global, most acute in South America and MEA | Medium term (2-4 years) |

| Data Privacy, Cybersecurity, and Interoperability Challenges | -1.8% | North America and EU, with growing concern in APAC | Short term (≤ 2 years) |

| Accuracy Limitations Due to Signal Interference and Complex Clinical Environments | -1.2% | Global, especially dense clinical environments | Short term (≤ 2 years) |

| Challenges In Legacy System Integration and AI Model Deployment | -1.4% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Implementation and Ongoing Maintenance Costs

The AI in hospital asset management market still faces a real barrier from enterprise-wide deployment cost, especially in community hospitals and mid-sized health systems. Even when newer BLE-ready networks reduce hardware needs, providers still face spending on tags, software, integration, staff training, and change management. The cost picture becomes heavier when hospitals want data from asset platforms to flow into EHRs, CMMS environments, nurse call systems, and internal reporting tools. Professional services can therefore remain as important as license fees, which slows wider adoption in parts of the AI in hospital asset management market where budgets are tightly controlled. This challenge is less severe when vendors offer phased rollouts, cloud subscriptions, or managed services that spread costs over time. Those delivery models are gaining importance because they let providers expand coverage without reopening large capital approval cycles.

Data Privacy, Cybersecurity, and Interoperability Challenges

The AI in hospital asset management market also faces pressure from privacy, cybersecurity, and interoperability requirements that make implementation more complex. The proposed HIPAA Security Rule update published by the U.S. Department of Health and Human Services in December 2024 requires a documented technology asset inventory for systems that create, receive, maintain, or transmit electronic protected health information, including connected devices and related infrastructure. HHS.GOV That requirement supports adoption, but it also raises the standard because hospitals must keep inventories current and defensible rather than static and occasional. In parallel, automated flow and tracking features must be designed carefully where consent, privacy, and data use rules are stricter, which can narrow feature scope or delay deployment choices. The result is that buyers in the AI in hospital asset management market increasingly expect secure architecture, clean integration layers, and audit-ready reporting as part of the core offer. Vendors that cannot show those controls clearly are more likely to face delayed purchases and narrower rollout phases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RFID Anchors the Present, RTLS Defines the Future

RFID held 44.27% of AI in hospital asset management market share in 2025, while RTLS is expected to expand at 23.13% CAGR through 2031. RFID remains deeply embedded in hospital workflows because it supports fast item reads, stable performance in sterile processing, and strong fit with supply chain and medication control routines. The American Hospital Association highlighted RFID solutions for medication inventory management in early 2025, which reflects the practical role of high-volume non-line-of-sight scanning in hospital operations. Hospitals also continue to value RFID because it works well in controlled environments where inventory accuracy and audit speed matter more than continuous movement mapping. This keeps RFID central to the installed base of the AI in hospital asset management market even as other technologies gain attention.

RTLS is growing faster because hospitals increasingly need continuous location streams for bed turns, patient movement, staff safety workflows, and live equipment dispatch. In the AI in hospital asset management industry, that shift does not remove RFID from the stack, but it does move more budget toward platforms that support ongoing spatial awareness rather than point-in-time confirmation. The broader result for the AI in hospital asset management market is a layered technology model where buyers want interoperability across RFID, RTLS, and software dashboards rather than isolated tools.

By Component: Software Intelligence Leads Value Creation

Software and analytics accounted for 56.11% of AI in hospital asset management market size in 2025, while services are projected to grow at 23.72% CAGR through 2031. This reflects a clear transition in which value is being created less by tags, readers, and gateways and more by the intelligence layer that interprets hospital activity. Buyers are paying for dashboards, predictive rules, workflow automation, and integration connectors because those features determine whether visibility data changes clinical operations. As a result, the AI in hospital asset management market is rewarding vendors that can connect maintenance logic, alerts, utilization analytics, and reporting into one usable software environment.

Services are growing faster because many provider organizations prefer bundled support that covers onboarding, integration, training, updates, and operational tuning. Managed-service structures also reduce the burden on internal IT and biomedical engineering teams, which makes scaling easier across multiple facilities. Hardware remains essential, especially in greenfield projects and settings where legacy infrastructure is limited, but its commercial role is becoming more standardized in the AI in hospital asset management market. This makes recurring software and services revenue more strategic than one-time hardware deployment revenue across the AI in hospital asset management market.

By Application: Equipment Tracking Dominates, Bed Management Accelerates

Equipment and device tracking represented 51.15% of AI in hospital asset management market size in 2025, and bed and capacity management is forecasted to rise at 24.71% CAGR through 2031. Equipment tracking still leads because it supports the most immediate operational need, which is locating mobile devices quickly and keeping them available where care is delivered. Hospitals can see direct labor gains when staff spend less time searching, and that makes equipment visibility the entry point for many deployments in the AI in hospital asset management market.

Bed and capacity management is growing faster because hospitals are using the same real-time data layer to improve room assignment, discharge timing, turnover visibility, and throughput coordination. That growth shows a broadening role for the AI in hospital asset management market from device visibility toward operational flow management across departments. Inventory and supply chain management is also gaining traction, especially in pharmacy automation and sterile processing, where simultaneous reads can compress count cycles and improve traceability discipline. Patient and staff tracking continue to expand where workplace safety, response speed, and supervision needs are becoming more formalized. Together, these patterns show that the AI in hospital asset management market is moving from a single use case toward a wider workflow platform.

By End-User: Hospitals hold the largest base while ASCs post the fastest growth

Hospitals held 39.89% of end-user revenue in 2025, which kept them in the lead across the AI in hospital asset tracking market because large inpatient networks carry the widest mix of device management, sterilization, redistribution, compliance, and maintenance workflows. Their scale also means that asset movement across departments and campuses can create hidden idle time and duplicate purchasing when visibility is weak. Ambulatory surgical centers are the expected to be the fastest-growing end-user group, with a projected 26.82% CAGR from 2026 to 2031, because same-day procedural volume is rising while these facilities still need precise control over leaner asset pools and limited storage footprints. In the AI in hospital asset tracking market size, ASC demand stands out because a misplaced device in a compact, high-throughput center can cancel a case rather than merely delay it.

Long-term care facilities are adopting more selectively, with demand centered on wandering protection, staff duress, and medication control rather than on broad equipment fleets. Diagnostic centers and rehabilitation facilities are also showing interest in modular SaaS-led deployments that can scale over time without the same capital burden as a full hospital campus build. Within the AI in hospital asset tracking industry, hospitals therefore remain the main revenue base while ASCs provide a strong growth engine tied to fast implementation and clear operational payback.

Geography Analysis

North America held 43.12% of AI in hospital asset management market share in 2025. The region leads because it combines a mature base of RFID and RTLS infrastructure with strong hospital technology spending and heavier regulatory pressure on traceability and documentation. The FDA’s Quality Management System Regulation is now in force in 2026, which strengthens expectations around device quality systems and reinforces the need for structured asset-related processes. The proposed HIPAA Security Rule update also raises the importance of current technology asset inventories, which makes compliance and cybersecurity part of the same purchase discussion in the AI in hospital asset management market.

Europe remains the second-largest regional block in the AI in hospital asset management market. Germany, the United Kingdom, and France account for much of the institutional adoption because they have stronger hospital digitization programs and clearer traceability needs than smaller markets. The region is also shaped by item-level control expectations for medical devices and implant-related workflows, which supports demand for interoperable tracking systems. Italy and Spain are also progressing as hospital digitization programs advance, while adoption in the Middle East and Africa remains earlier but is moving through smart hospital construction in GCC countries.

Asia-Pacific is the fastest-growing region in the AI in hospital asset management market, with a projected 27.11% CAGR expected through 2031. Growth in the region is tied to hospital modernization, new infrastructure, and a stronger willingness to embed operational intelligence during construction rather than after commissioning. China is moving quickly through large hospital digitization programs, while South Korea and Japan are also adding momentum through AI-led care models and connected asset workflows. India and Southeast Asia still trail the most advanced markets in penetration, but their growth path remains strong because modernization, outpatient expansion, and smart facility investment are improving the fit for scalable cloud and hybrid deployments. This keeps Asia-Pacific central to future expansion in the AI in hospital asset management market.

Competitive Landscape

The AI in hospital asset management market remains moderately concentrated, with broad healthcare technology groups and focused RTLS specialists competing across the same provider budgets. Large healthcare vendors benefit from existing hospital relationships, field service networks, and the ability to connect asset tools with imaging, maintenance, and enterprise workflows. Specialist suppliers still matter because they often offer deeper location precision, stronger workflow tailoring, and healthcare-specific deployment experience. This creates a market where buying decisions depend less on one product feature and more on how well vendors combine data capture, analytics, service support, and integration readiness. The competitive pattern in the AI in hospital asset management market therefore favors providers that can move from device visibility to operational intelligence without forcing hospitals into fragmented point solutions.

GE HealthCare has been active in expanding its operating footprint in this space. In February 2026, the company launched ReadyFix, a remote fleet management solution that extends its position in connected device oversight and service orchestration. In June 2026, GE HealthCare also expanded its collaboration with Carilion Clinic by deploying its Advanced Asset Management Program and Encompass RTLS platform across the Virginia network. These moves show a strategy built around long-term service relationships rather than stand-alone software sales, and that is a meaningful position inside the AI in hospital asset management market.

Mid-sized hospitals and multi-site outpatient groups remain less fully served, which keeps room open for vendors with lighter deployment models and lower operating complexity. PartsSource’s Asset Uptime launch in 2025 also points to a software-led approach that ties device monitoring, maintenance coordination, and supply chain visibility together. At the technology layer, Impinj remains important because its RAIN RFID platform supports partner ecosystems and recurring value capture through readers, tags, and enablement of larger solution stacks. That combination of platform vendors, service-led medtech firms, and workflow specialists keeps the AI in hospital asset management market competitive without showing a single dominant leader.

AI In Hospital Asset Management Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Siemens Healthineers AG

Zebra Technologies Corporation

Securitas Healthcare LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: GE HealthCare expanded its clinical engineering services relationship with Carilion Clinic, deploying its Advanced Asset Management Program (AAMP) and Encompass RTLS platform across Carilion's Virginia network. The agreement is designed to optimize medical equipment across its full lifecycle and reduce operational variability across the health system.

- June 2026: TeleTracking Technologies launched Operations IQ Ambulatory, the company's most significant strategic expansion in 35 years, extending its real-time operational intelligence platform from acute-care hospitals to outpatient access and referral management. The product is purpose-built for health systems managing patient flow across hospital and ASC settings.

- April 2026: Zebra Technologies announced a partnership with Aiva Health to power hands-free nurse workflows using Aiva's AI-powered Nurse Assistant on Zebra's healthcare mobile computers and WS101-H wearable badge, integrating asset and workflow intelligence at the point of care.

Global AI In Hospital Asset Management Market Report Scope

According to the report’s scope, the AI in hospital asset management market comprises AI-powered software, platforms, and services that enable real-time tracking, utilization optimization, predictive maintenance, and lifecycle management of hospital assets. These solutions leverage artificial intelligence, IoT, and analytics to improve operational efficiency, reduce equipment downtime, and enhance resource allocation across healthcare facilities.

The AI in hospital asset management market is segmented into technology, component, application, end-user, and geography. By technology, the market is segmented into RFID, RTLS, barcode scanners, Bluetooth low energy, and other technologies. By component, the market is segmented into hardware, software and analytics, and services. By application, the market is segmented into equipment and device tracking, inventory/supply-chain management, patient and staff tracking, bed and capacity management, environmental and condition monitoring, and other applications. By end-user, the market is segmented into hospitals, ambulatory surgical centers, long-term care facilities, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| RFID |

| RTLS |

| Barcode Scanners |

| Bluetooth Low Energy |

| Other Technologies |

| Hardware |

| Software and Analytics |

| Services |

| Equipment and Device Tracking |

| Inventory/Supply-Chain Management |

| Patient and Staff Tracking |

| Bed and Capacity Management |

| Environmental and Condition Monitoring |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Long-Term Care Facilities |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | RFID | |

| RTLS | ||

| Barcode Scanners | ||

| Bluetooth Low Energy | ||

| Other Technologies | ||

| By Component | Hardware | |

| Software and Analytics | ||

| Services | ||

| By Application | Equipment and Device Tracking | |

| Inventory/Supply-Chain Management | ||

| Patient and Staff Tracking | ||

| Bed and Capacity Management | ||

| Environmental and Condition Monitoring | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Long-Term Care Facilities | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for AI in hospital asset management through 2031?

The AI in hospital asset management market is at USD 5.31 billion in 2025 to USD 6.44 billion by 2026 and is forecasted to reach USD 18.02 billion by 2031 at 22.85% CAGR, which reflects strong demand for tracking, maintenance, and workflow intelligence.

Which technology is leading hospital deployments today?

RFID led with 44.27% share in 2025 because it fits medication, inventory, and sterile processing workflows well, while RTLS is expected to grow faster at 23.13% CAGR through 2031.

Which application area is growing the fastest in this space?

Bed and capacity management is anticipated to be the fastest-growing application at 24.71% CAGR through 2031, showing that hospitals are using the same data layer for throughput and room management, not only equipment search.

Which region is expected to expand the fastest over the forecast period?

Asia-Pacific is forecasted to grow at 27.11% CAGR through 2031, supported by smart hospital projects, digital twin infrastructure, and broader modernization across major healthcare systems.

Page last updated on: