Hospital Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 65.47 Billion |

| Market Size (2031) | USD 89.75 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

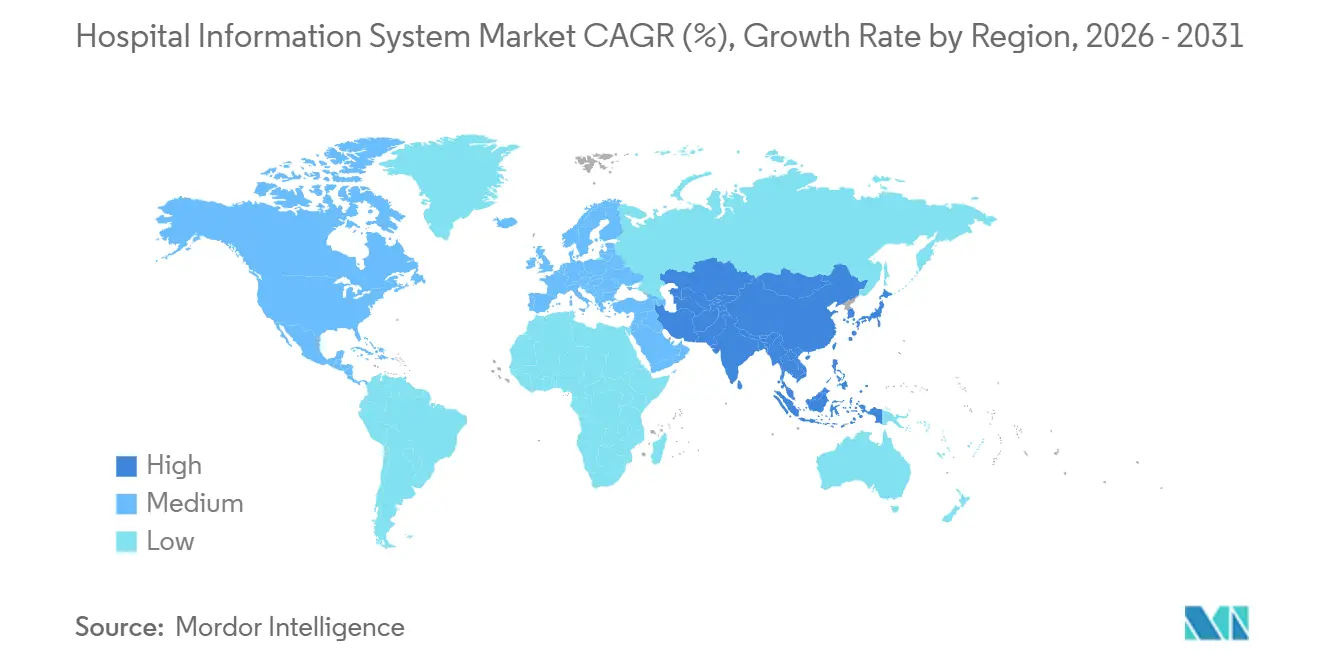

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

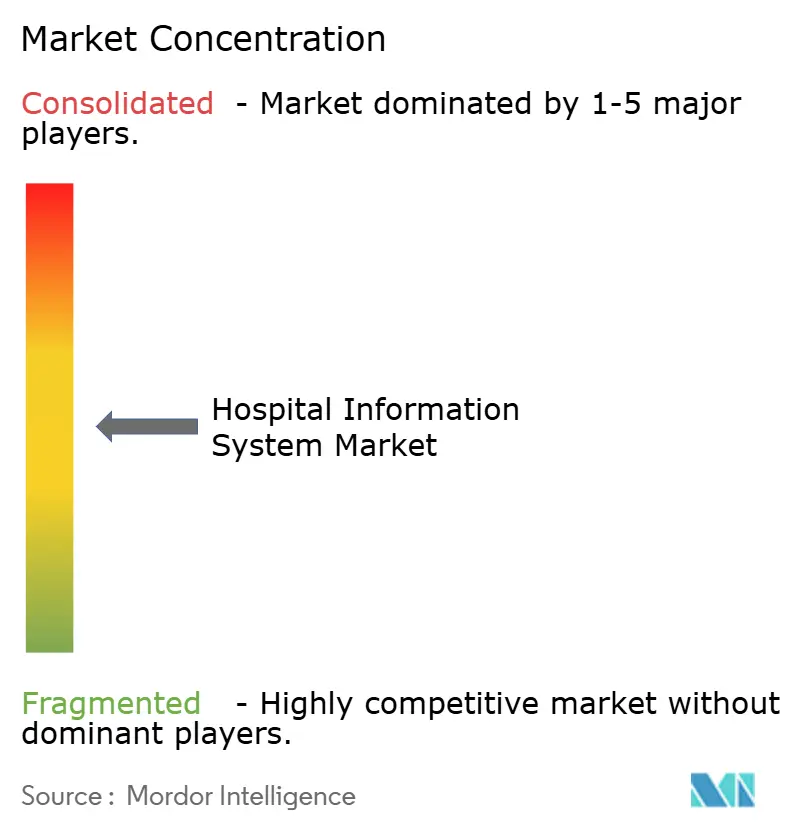

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Information System Market Analysis by Mordor Intelligence

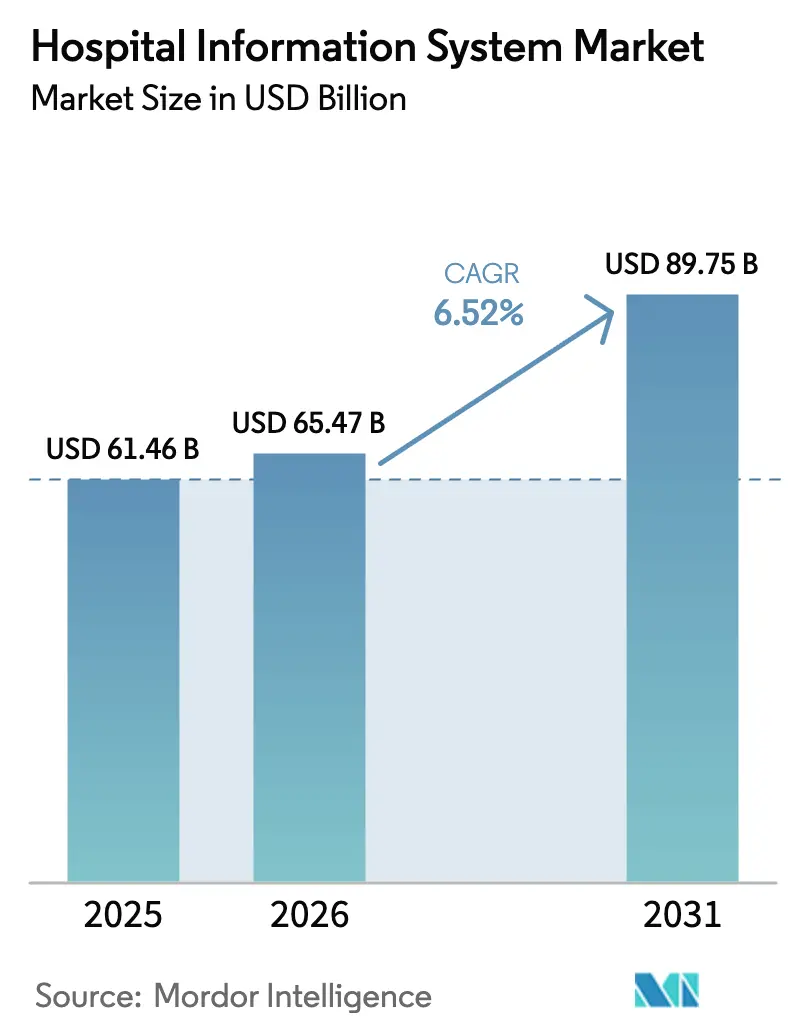

The Hospital Information System Market size is expected to grow from USD 61.46 billion in 2025 to USD 65.47 billion in 2026 and is forecast to reach USD 89.75 billion by 2031 at 6.52% CAGR over 2026-2031.

A growing consensus that integrated digital platforms are no longer optional but foundational infrastructure is reshaping procurement agendas. Buyers now focus on lifetime total cost of ownership, measurable clinical outcomes and vendor support for modular cloud upgrades. These priorities have pushed decision-making from siloed departments to enterprise-level digital steering committees that blend financial and clinical oversight. Competition is intensifying as suppliers bundle analytics, cybersecurity, and managed services, positioning themselves as partners in multi-year “digital modernization” programs rather than one-time software vendors.

Key Report Takeaways

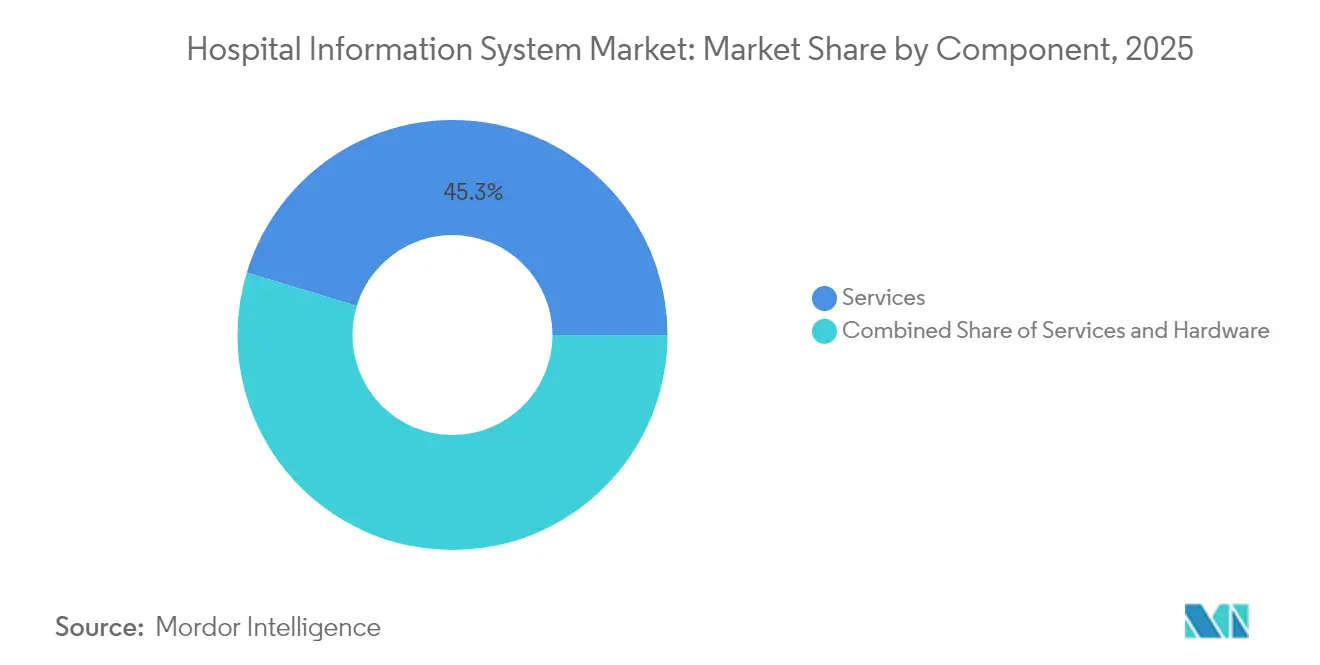

- By component, services captured 45.30% of the hospital information system market share in 2025, while software is projected to grow at an 7.6% CAGR to 2031.

- By mode of delivery, on-premises deployments accounted for 54.20% of the hospital information system market size in 2025; cloud models are poised to grow at an 8.55% CAGR through 2031.

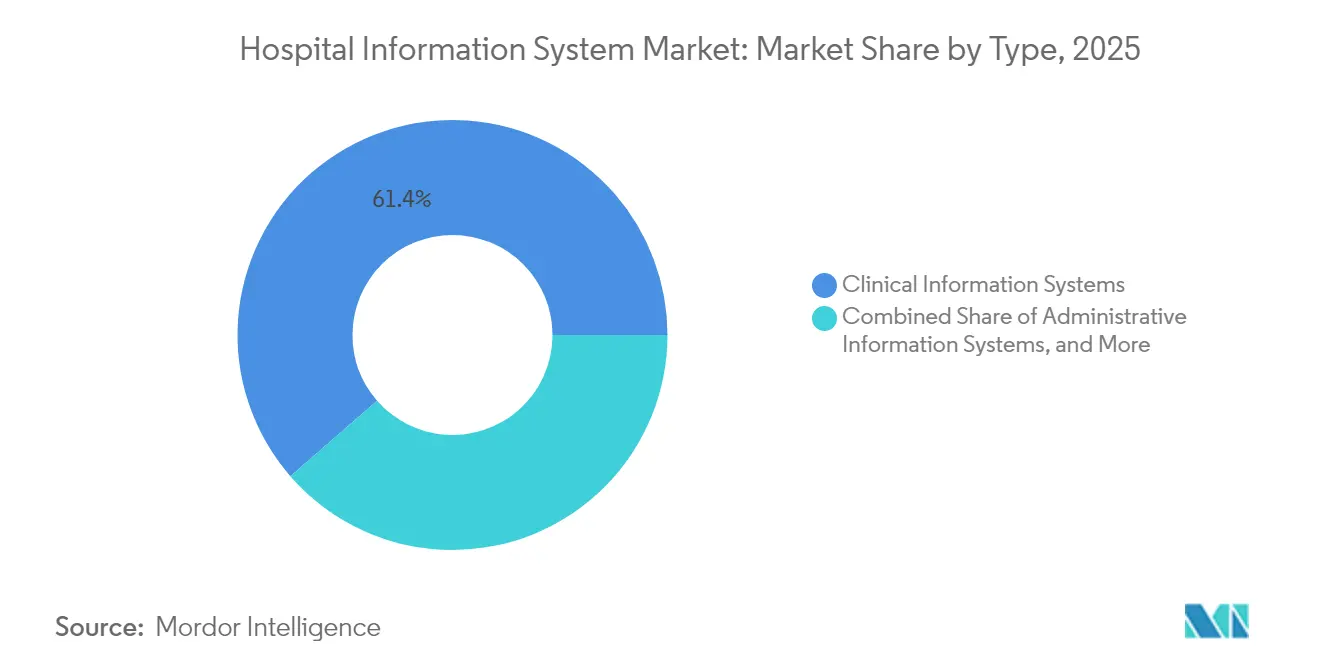

- By system type, clinical information systems accounted for 61.40% of the hospital information system market in 2025 and will likely retain leadership even as administrative systems expand at a 7.3% CAGR.

- By end user, multi-specialty hospitals led revenue generation in 2025, while small community hospitals show the fastest adoption of subscription platforms.

- By geography, North America held a 41.60% share of the hospital information system market in 2025, yet Asia-Pacific is predicted to record the highest CAGR of 9.1% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hospital Information System Market Trends and Insights

Driver Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven analytics & clinical decision support | +1.2% | Global | Medium term (2-4 years) |

| Large-scale hospital builds in emerging markets | +1.0% | Asia-Pacific & GCC | Long term (≥4 years) |

| US ONC Cures Act & other interoperability mandates | +0.8% | North America & Europe | Short term (≤2 years) |

| AI-powered CDS modules for CIS | +0.7% | Global | Medium term (2-4 years) |

| Rising demand for quality healthcare delivery | +0.6% | Global | Long term (≥4 years) |

| Rapid technology advancement in healthcare | +0.5% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Use of AI-Driven Analytics and Clinical Decision Support

Hospitals now embed machine-learning models to flag sepsis, optimise antibiotics and predict discharge readiness in near real time. Epic lists more than 100 AI features on its roadmap, signalling how deeply analytics is being woven into core platforms [1]Epic Systems, “Connecting 600+ Hospitals to TEFCA,” epic.com. Duke Health shortened bed-assignment intervals after implementing GE HealthCare’s Command Center Software, demonstrating tangible throughput gains [2]Duke Health, “Command Center Improves Bed Assignment,” dukehealth.org. Boards increasingly demand model-explainability statements, and governance teams work with data scientists to calibrate algorithms that reflect local care pathways. As these practices become mainstream, AI functionality is shifting from pilots to default requirements, enlarging addressable spend in the hospital information system market.

Large-Scale Hospital Infrastructure Investments in Emerging Markets

Gulf Cooperation Council states and multiple Southeast Asian countries now budget digital platforms alongside construction, allowing new tertiary centres to leapfrog legacy architectures. Projects in the United Arab Emirates allocate substantial funds to EHR, imaging archives and command-centre analytics, ensuring that digital maturity grows in lockstep with physical capacity [3]Ministry of Health and Prevention, “Ministry of Health and Prevention Official Website,” MOHAP, mohap.gov.ae. Vendors providing multilingual interfaces gain first-mover advantage. These dynamics redirect revenue pools toward fast-growing, infrastructure-rich regions, reinforcing Asia-Pacific’s role as the quickest-expanding hospital information system market.

Interoperability mandates such as the US ONC Cures Act driving digital consolidation

The Trusted Exchange Framework and Common Agreement (TEFCA) accelerated cross-vendor health-information sharing, prompting suppliers to acquire niche analytics firms to protect installed bases [4]Office of the National Coordinator for Health Information Technology, “HealthIT.gov Home,” U.S. Department of Health and Human Services, healthit.gov. Interoperability frameworks shrink switching costs for hospitals, encouraging consolidation of disparate systems into single-vendor estates. As a result, long-term contracts now combine hardware refresh, data migration and staff skilling, turning the hospital information system market into a hybrid of subscription software and outcome-based services.

AI-powered clinical decision support adoption boosting CIS modules

Ambient listening and generative documentation tools reduce clinician typing time, improving staff satisfaction while preserving data quality. Mayo Clinic’s pilot with Epic and Abridge shows early evidence of nursing-workflow gains. As health systems witness these benefits, budgets shift toward AI-ready clinical information system modules, lifting software revenue faster than traditional service revenue in the hospital information system market.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership | -1.1% | Global | Medium term (2-4 years) |

| Rising cybersecurity & compliance risks | -1.0% | Global | Short term (≤2 years) |

| Physician resistance due to workflow disruption | -0.6% | Global | Short term (≤2 years) |

| Lack of IT infrastructure in emerging nations | -0.5% | Sub-Saharan Africa & parts of South Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership

Comprehensive EHR deployments can cost hundreds of millions of USD when hardware, data migration, workflow redesign and multi-year maintenance are included. Northwell Health’s board approved a USD 1.2 billion initiative after leadership demonstrated a credible payback horizon through reduced duplicative testing and improved population-health management. Smaller hospitals lack the balance sheets to absorb such capital outlays, pushing them toward subscription pricing or shared-services models. Innovative financing mechanisms—ranging from managed-service concessions to public-private partnerships—are therefore gaining traction. Vendors respond by bundling optimisation services within contracts, recognising that clients judge value over the full life cycle. This evolving economics is nudging the Hospital Information System industry toward outcome-based pricing structures that reward measurable improvements rather than mere software installation.

Increasing Cybersecurity and Compliance Risks

Healthcare topped all sectors for reported breaches in 2024, according to the American Hospital Association, highlighting a widening attack surface that spans on-premise servers, cloud connectors and medical IoT devices. The February 2024 ransomware assault on Change Healthcare disrupted claims clearing for nearly every United States hospital, proving that third-party dependencies can paralyse entire ecosystems. Ascension’s subsequent downtime further illustrated how cyber-incidents rapidly escalate into clinical risk when medication dispensing and imaging archives go offline. Regulators responded by tightening breach-notification timelines and mandating zero-trust frameworks, which in turn elevate compliance spending within IT budgets. Hospitals are therefore embedding security orchestration and automated incident response directly into their information systems rather than treating them as bolt-on appliances. This integration is reshaping vendor selection criteria, with chief information security officers gaining a stronger voice in Hospital Information System market procurements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Component: Services Lead While Software Accelerates

Services accounted for the largest Hospital Information System market share, representing 45.30% of 2025 revenue, while the software component is forecast to record an 7.6% CAGR between 2026 and 2031. Complex data-conversion projects and multi-site rollouts continue to drive demand for consultative and managed services, particularly among health systems consolidating multiple legacy platforms. Meanwhile, the rising popularity of AI-enabled modules is fuelling software licence growth, especially for decision-support and ambient documentation. Epic’s partnership with Mayo Clinic and Abridge to pilot generative AI for nursing workflows typifies how vendors are deepening service wrap-arounds to accelerate time-to-value. An observable consequence is that implementation timelines are shortening as repeatable, cloud-native templates replace bespoke coding. Providers that align service engagements to measurable clinical and financial objectives tend to realise faster benefit realisation, reinforcing the strategic role of professional services in the Hospital Information System industry.

Mode of Delivery: On-Premise Dominance Faces Cloud Challenge

On-premise deployments retained the largest hospital information system market size in 2025, with an estimated 54.20% share, yet cloud-based models are projected to expand at close to a 8.55 % CAGR through 2031. Chief technology officers cite scalability and business-continuity features as primary cloud motivators, but many still keep core EHR databases on local servers for latency and sovereignty reasons. Progressive organisations adopt hybrid architectures, hosting analytics sandboxes in the cloud while maintaining high-transaction modules in dedicated data centres. Epic’s success stories from early public-cloud adopters demonstrate operational elasticity, though cost efficiencies remain contingent on rigorous instance-rightsizing. A practical implication is that network-bandwidth planning and identity-access management become as critical as application logic in project roadmaps. Consequently, mode-of-delivery decisions now involve multidisciplinary reviews that balance resilience, cost, data-residency and innovation goals.

Type: Clinical Systems Expand Beyond Traditional Boundaries

Clinical Information Systems represented roughly 61.40% of the hospital information system market share in 2025, forming the digital spine for inpatient and ambulatory workflows. AI-powered ambient listening tools are trimming clinician documentation time, thereby freeing capacity for more direct patient interaction. Administrative systems, while smaller today, exhibit a forecast 7.3% CAGR, driven by rising recognition that revenue-cycle precision underpins financial sustainability. The line separating clinical and administrative domains is fading as integrated suites now carry scheduling, inventory and claims modules alongside order entry and results reporting.

End-User: Multi-Specialty Hospitals Drive Innovation Adoption

Multi-specialty hospitals command the largest Hospital Information System market size, reflecting their complex caseloads and requirement for deeply integrated records across departments. Specialty facilities—for example, oncology-only centres—often opt for narrower but highly specialised modules that interface with broader national health networks. Smaller community hospitals increasingly leverage vendor-hosted platforms to access enterprise-grade functionality without extensive capital expenditure. Variation in digital maturity among end-users pushes suppliers to offer flexible deployment topologies and modular licensing that scale with organisational sophistication. The implication is a more segmented selling approach, where value propositions are tailored to the clinical complexity and financial profile of each provider category within the Hospital Information System industry.

Geography Analysis

North America recorded a 41.60% hospital information system market share in 2025, buoyed by mandated EHR adoption and sizeable budgets. After the Change Healthcare cyber incident, US hospitals tightened vendor risk assessments and embedded real-time threat-intelligence clauses in contracts. A BMC Digital Health review noted that 84% of US systems deploy AI predictive models, though governance teams remain under-resourced. Providers therefore seek managed services for model validation, fostering a service-rich hospital information system market.

Asia-Pacific is poised for the fastest 9.1% CAGR to 2031, fuelled by rising health expenditure and cloud-first policies. India’s federal health budget increased double digits in 2024, and Thailand’s ministry pilots tele-medicine kiosks interfacing with AI triage engines. Singapore’s smart-ward initiatives emphasise IoT-enabled vital-sign tracking, raising interoperability expectations. Vendors offering language localisation gain headroom, especially as personal-data-protection acts proliferate. Leapfrogging older infrastructure, hospitals adopt cloud EHR platforms that align with regional broadband upgrades, fortifying Asia-Pacific’s role in the hospital information system market.

Europe, the Middle East and Africa present a spectrum of digital maturity. Germany’s Krankenhauszukunftsgesetz (KHZG) fund compels hospitals to certify digital-medication management, spurring suppliers to expand ecosystem services. GCC nations report more than three-quarters of public hospitals already on EHRs, amplified by Saudi Arabia’s Vision 2030 tele-consultation targets. Regulatory convergence on data-interchange standards eases multi-national implementations, while talent flows from Europe to Gulf megaprojects accelerate skill-mix evolution. Collectively, the region remains a heterogeneous but strategically important theatre for the hospital information system market.

Competitive Landscape

Epic Systems remains the Hospital Information System market leader, holding close to 40% domestic share and expanding into selected European contracts. Oracle Health is investing in a next-generation EHR platform that integrates analytics and voice-driven interfaces, scheduled for release in 2025. GE HealthCare’s partnership with Amazon Web Services targets generative AI solutions that embed within imaging chains and command centres, highlighting the strategic importance of cloud hyperscalers. Collectively, these moves signal a shift toward platform-plus-ecosystem strategies, where core EHR functionalities anchor a marketplace of niche applications and developer toolkits.

Mid-size hospital groups present a lucrative white-space that incumbent mega-suite vendors historically underserviced due to cost and complexity. Epic’s Garden Plot programme lowers entry barriers by offering a pre-configured, cloud-hosted environment aimed at community hospitals and large physician groups. Parallelly, Innovaccer secured significant late-stage funding to scale its cloud-native data platform, aspiring to bridge payer, provider and patient data flows with AI analytics. As these challengers reach scale, price transparency and rapid deployment are becoming differentiators, pressuring legacy vendors to streamline professional-service overhead. An emerging consequence is that competitive advantage may hinge on the ability to deliver outcome guarantees rather than technology feature lists.

Artificial intelligence now represents the most active battleground, with firms like Veradigm leveraging generative language models to mine de-identified clinical notes for population-health insights. Oracle Health embeds machine-learning accelerators within its upcoming platform, while small-cap specialists develop single-purpose solutions for oncology or cardiology decision support. Strategic acquisitions of algorithm start-ups by EHR giants underscore how analytic intellectual property is becoming indispensable table stakes. The clear takeaway is that future Hospital Information System market share will correlate with a vendor’s capacity to operationalise AI responsibly at scale, integrating cybersecurity, governance and clinician trust from the outset.

Hospital Information System Industry Leaders

Oracle Health (Cerner)

Epic Systems Corporation

Dedalus Group

Koninklijke Philips NV

GE HealthCare Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: RailTel Corporation of India Limited secured a ₹12.85 crore contract from Mahatma Gandhi Institute of Medical Sciences to implement a comprehensive hospital management system. This includes HIMS, fire safety, academic activity systems, accounts, campus management, and website development signaling RailTel’s strategic diversification into healthcare IT beyond its railway telecom roots.

- October 2025: The U.S. Cybersecurity and Infrastructure Security Agency (CISA) issued alerts highlighting vulnerabilities in Vertikal Systems’ hospital management information system. Exploitation of these low-complexity flaws could expose sensitive patient data, underscoring the growing importance of cybersecurity in HIS adoption.

- May 2025: Delhi announced plans to roll out a centralized health information system across all hospitals. The initiative includes a real-time dashboard for monitoring bed availability, medicine stocks, diagnostic trends, and resource utilization, supported by a central healthcare control room — a major step toward integrated digital health infrastructure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hospital information system market as all integrated and modular digital platforms deployed inside acute-care hospitals that capture, store, secure, and exchange clinical, administrative, and financial data. The boundary spans electronic health and medical records, laboratory, radiology, pharmacy, billing, scheduling, analytics, and interoperability engines delivered through on-premise, cloud, and hybrid architectures.

Scope Exclusion: Stand-alone telehealth services for outpatient clinics, non-hospital practice-management software, and physical medical devices lie outside this boundary.

Segmentation Overview

- By Component

- Software

- Services

- Hardware

- By Mode of Delivery

- On-premise

- Cloud-based

- Hybrid (Hosted)

- By Type

- Clinical Information Systems

- Electronic Health/Medical Records

- Computerized Physician Order Entry

- Laboratory Information System

- Radiology Information System

- Pharmacy Information System

- Picture Archiving & Communication Systems

- Others (ICU, Anesthesia, etc.)

- Administrative Information Systems

- Patient Registration & Scheduling

- Revenue Cycle Management

- Workforce Management

- Supply Chain & Inventory Management

- Ancillary Information Systems

- Clinical Information Systems

- By End-user

- Multi-specialty Hospitals

- Specialty Hospitals

- Academic Medical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Afterward, we interview hospital CIOs, clinical informatics leads, and implementation partners across North America, Europe, Asia-Pacific, Latin America, and the Middle East. Their feedback refines average selling prices, deployment timelines, and module attachment rates that documents seldom disclose, enabling us to lock assumption ranges.

Desk Research

Mordor analysts begin with authoritative public datasets from the WHO Global eHealth Observatory, OECD digital-health statistics, and HIMSS ICT adoption surveys, which outline baseline penetration by region. We enrich these inputs with government procurement portals, national eHealth budgets, patent filings accessed via Questel, shipment insights from Volza, and vendor financials drawn through D&B Hoovers and Dow Jones Factiva, shaping an initial country matrix. The sources named illustrate breadth only; many additional repositories informed the desk phase.

Market-Sizing & Forecasting

We build the 2024 baseline via a top-down spend pool that multiplies licensed bed counts by average IT outlay per bed and adjusts for public-private mix, service complexity, and currency effects. Selective bottom-up supplier roll-ups and channel checks validate totals. Key variables like mandatory EHR deadlines, cloud-infrastructure pricing, replacement-cycle length, healthcare spend per capita, and inpatient admission growth capture volume and price movement. A multivariate regression links these drivers to yearly spend, while scenario analysis probes upside and downside cases. Data gaps in emerging regions are bridged with occupancy proxies confirmed during interviews.

Data Validation & Update Cycle

Outputs undergo anomaly checks, peer review, and a variance threshold that triggers re-contact with sources. Mordor refreshes every twelve months and issues interim updates when policy shifts or mergers materially alter the outlook.

Why Mordor's Hospital Information System Baseline Earns Boardroom Trust

Published estimates often diverge because firms select different product mixes, deployment cut-offs, and forecast cadences.

Key Gap Drivers include the addition of broader healthcare IT segments, aggressive cloud migration assumptions without regional adoption filters, and less frequent model refreshes compared with our annual cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 61.46 B | Mordor Intelligence | |

| USD 63.80 B | Global Consultancy A | Wider scope adds ambulatory and home-care IT spend |

| USD 177.52 B | Industry Journal B | Assumes uniform cloud conversion and uses 2023 price points without currency normalization |

These comparisons show how Mordor's disciplined scope selection, annually updated variables, and transparent assumption book deliver a balanced baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current Hospital Information System market size?

The market is valued at USD 65.47 billion in 2026 and is projected to grow to USD 89.75 billion by 2031.

Which region holds the highest Hospital Information System market share?

North America leads with roughly 41.60 % share, driven by established EHR mandates and sustained IT budgets.

What is the expected CAGR for cloud-based Hospital Information Systems?

Cloud-delivered solutions are forecast to expand at close to a 8.55 % CAGR between 2026 and 2031.

How are cybersecurity concerns influencing purchasing decisions?

Rising breach incidents push hospitals to prioritise vendors that integrate zero-trust architectures and real-time threat detection into their core platforms.

Page last updated on: