Fishing Apparel and Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

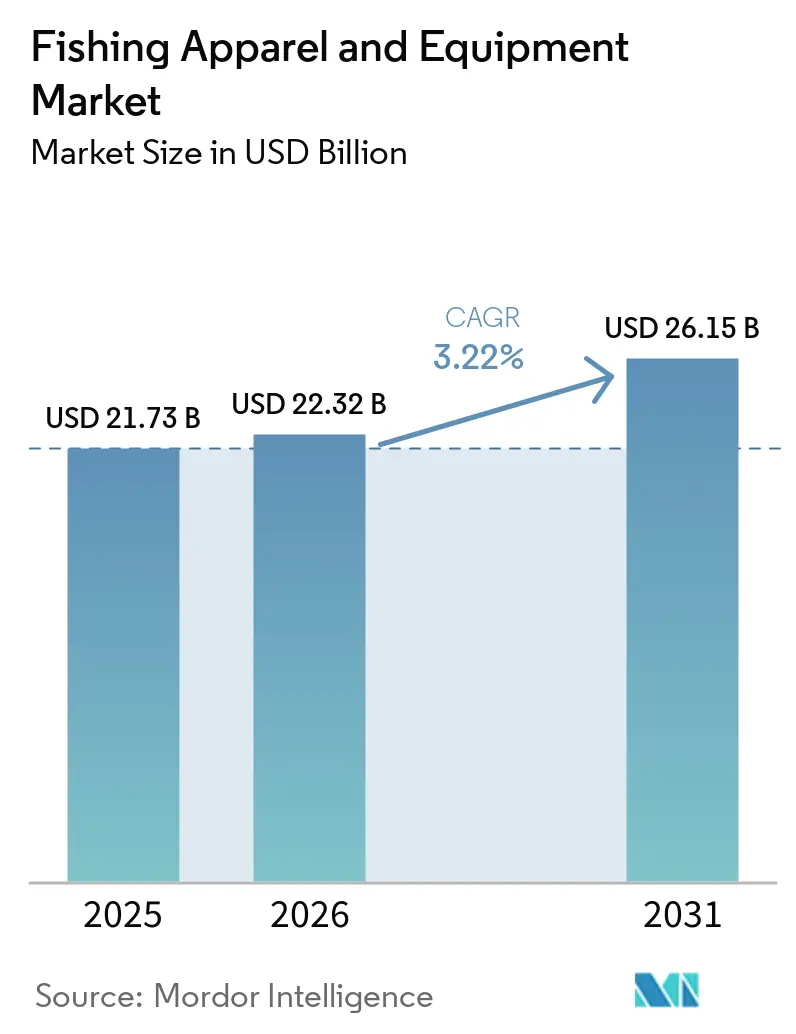

| Market Size (2026) | USD 22.32 Billion |

| Market Size (2031) | USD 26.15 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

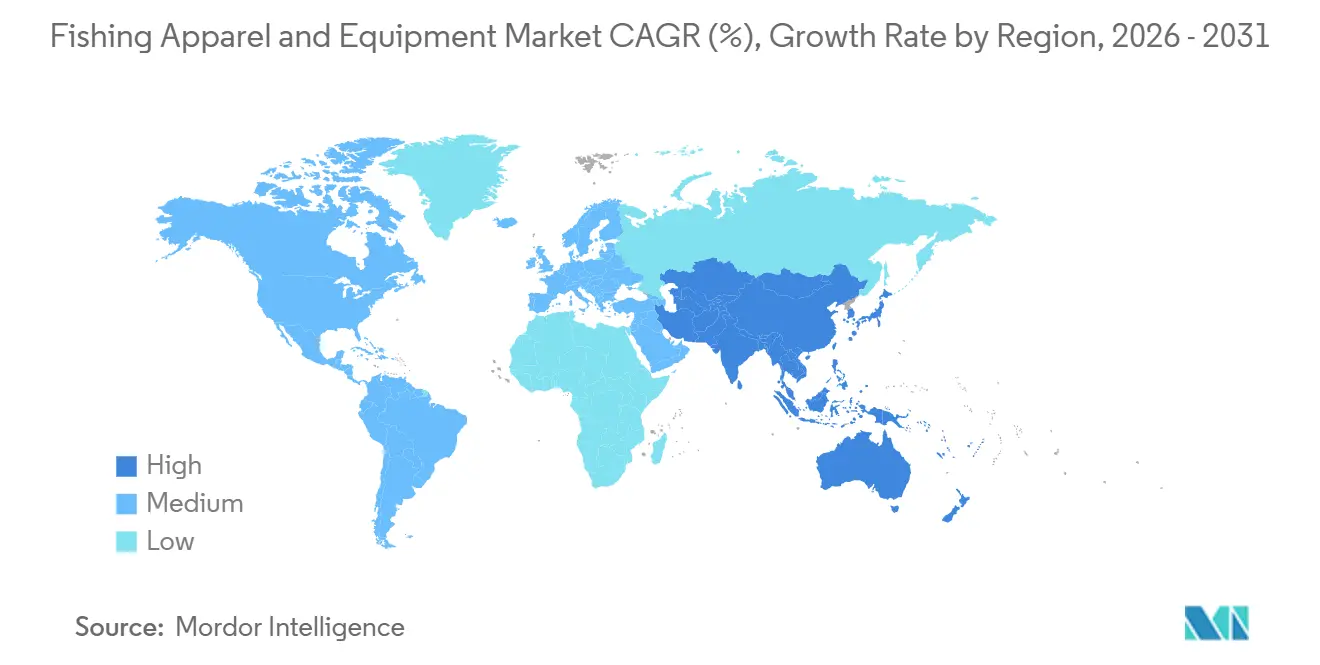

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fishing Apparel and Equipment Market Analysis by Mordor Intelligence

The fishing apparel and equipment market size is expected to grow from USD 21.73 billion in 2025 to USD 22.32 billion in 2026 and is forecast to reach USD 26.15 billion by 2031 at 3.22% CAGR over 2026-2031. The steady growth of the fishing apparel and equipment market is supported by rising participation in recreational and sport fishing activities across both developed and emerging economies. Increasing consumer interest in outdoor leisure pursuits, coupled with growing awareness of specialized fishing gear, continues to drive product demand. Manufacturers are introducing advanced apparel featuring UV protection, waterproof materials, and enhanced comfort, while equipment innovations improve performance and durability. The expansion of e-commerce platforms has also increased product accessibility, enabling brands to reach a broader customer base. Additionally, fishing tourism, competitive angling events, and government initiatives promoting outdoor recreation are contributing to market expansion.

Key Report Takeaways

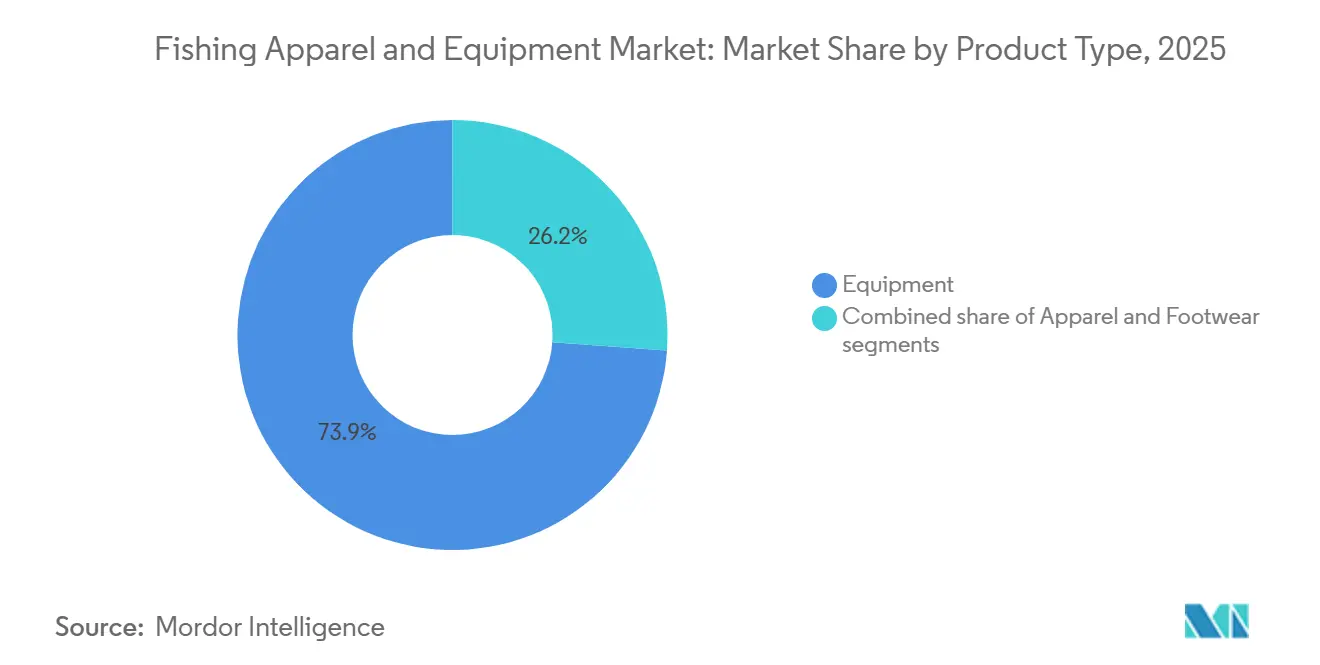

- By product type, equipment held 73.85% of the fishing apparel and equipment market share in 2025, while apparel is forecast to expand at a 3.82% CAGR through 2031.

- By end user, adults accounted for 89.21% of the fishing apparel and equipment market size in 2025, while kids and children recorded the highest projected CAGR at 4.08% through 2031.

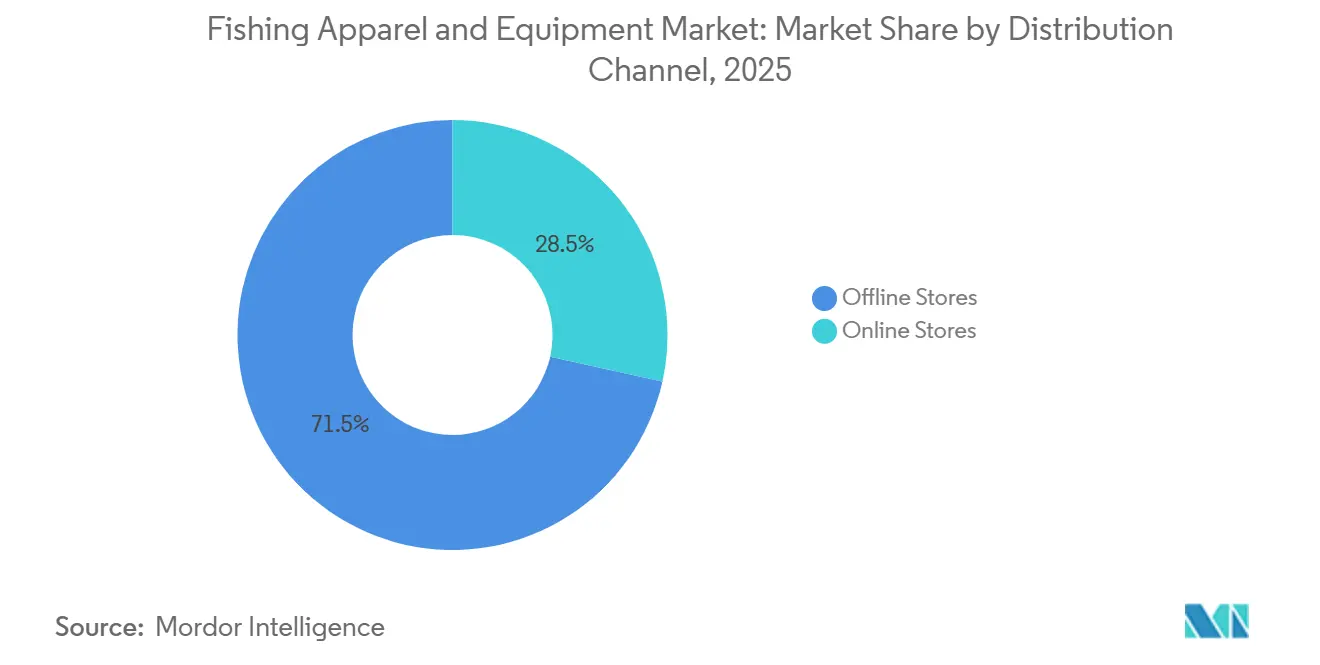

- By distribution channel, offline stores captured 71.53% of the fishing apparel and equipment market size in 2025, while online stores are advancing at a 4.46% CAGR through 2031.

- By geography, North America led with 35.01% of the fishing apparel and equipment market share in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 4.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fishing Apparel and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing participation in recreational and sport fishing activities | +0.8% | Global, with concentrated upside in North America and Western Europe | Short term (≤ 2 years) |

| Increasing popularity of fishing tourism and guided fishing expeditions | +0.5% | North America, Europe, and Asia-Pacific coastal areas, with spillover into South America | Medium term (2-4 years) |

| Technological advancements in fishing rods, reels, fish finders, and tackle | +0.7% | Global, with strongest adoption in North America, Japan, and China | Medium term (2-4 years) |

| Growth of competitive fishing tournaments and angling events | +0.4% | North America core, with expansion into Europe and East Asia | Medium term (2-4 years) |

| Rising interest in outdoor recreation and nature-based leisure activities | +0.4% | Global, especially Asia-Pacific emerging markets and younger consumers | Medium term (2-4 years) |

| Expansion of e-commerce channels for fishing gear and apparel sales | +0.5% | Global, with fast movement in China, the United Kingdom, and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing participation in recreational and sport fishing activities

Growing participation in recreational and sport fishing activities is a key factor shaping the fishing apparel and equipment market. Increasing consumer interest in outdoor recreation, nature-based experiences, and competitive angling is creating sustained demand for fishing gear, apparel, and accessories. The market is benefiting from a broad expansion in participation rather than a temporary surge in activity. According to the Recreational Boating & Fishing Foundation, 57.9 million Americans participated in fishing in 2024, surpassing the previous record of 57.7 million in 2023, while the national participation rate remained strong at 19%[1]Source: National Marine Manufacturers Association, “Record High Fishing Participation Reached in 2024”, nmma.org. Participation is also becoming more diverse, with 21.3 million women engaging in fishing activities in the United States during 2024. As more individuals take up recreational and sport fishing, demand for rods, reels, tackle, performance apparel, and protective gear continues to rise. This expanding participant base is encouraging manufacturers to introduce innovative products and supporting long-term growth across the fishing apparel and equipment market.

Increasing popularity of fishing tourism and guided fishing expeditions

Rising popularity of fishing tourism and guided fishing expeditions is emerging as a significant driver of the fishing apparel and equipment market. Anglers are increasingly traveling to renowned fishing destinations and participating in professionally guided fishing experiences, creating demand for specialized gear, apparel, and accessories. These trips often require high-performance equipment suited to specific environments, encouraging higher consumer spending on premium products. The market is benefiting from destination-based angling activities that extend beyond routine local fishing and promote greater equipment purchases. Europe provides a strong example of this trend, with approximately 25 million recreational anglers fishing with rod and line across the region in 2024. In addition, recreational sea anglers in Europe collectively spend around EUR 10.5 billion annually on fishing activities and equipment, highlighting the sector's substantial economic impact [2]Source: CBI Ministry of Foreign Affairs, “The European market potential for fishing tourism”, cbi.eu. As fishing tourism continues to expand globally, demand for advanced fishing equipment, protective apparel, and travel-oriented gear is expected to grow steadily, supporting market expansion.

Technological advancements in fishing rods, reels, fish finders, and tackle

Technological advancements in fishing rods, reels, fish finders, and tackle are significantly enhancing the appeal and performance of modern fishing equipment. Manufacturers are increasingly incorporating lightweight composite materials, precision-engineered reel systems, and improved rod designs to enhance durability, casting accuracy, and user comfort. The integration of advanced electronics, including GPS-enabled fish finders, sonar technology, and real-time navigation features, is helping anglers locate fish more efficiently and improve overall fishing success. Innovations in lures, hooks, and terminal tackle are also contributing to better performance across different fishing environments. These developments are encouraging both recreational and professional anglers to upgrade existing equipment and invest in premium products. Continuous product innovation is expanding the range of specialized fishing solutions available in the market while improving the overall fishing experience. As technology continues to evolve, demand for advanced fishing equipment is expected to remain strong across global markets.Technological advancements in fishing rods, reels, fish finders, and tackle

Growth of competitive fishing tournaments and angling events

The growth of competitive fishing tournaments and angling events is contributing significantly to demand for fishing apparel and equipment worldwide. Organized competitions encourage participants to invest in high-performance rods, reels, tackle, electronics, and specialized apparel that can improve efficiency and overall results. As tournament fishing gains greater visibility through media coverage, sponsorships, and digital platforms, more recreational anglers are becoming interested in competitive participation. This trend is increasing spending on premium and technologically advanced fishing products designed for specific fishing techniques and environments. Event organizers, sponsors, and equipment manufacturers also play a role in promoting new products and innovations to a broader audience. In addition, competitive fishing events often attract spectators and enthusiasts who subsequently purchase fishing gear for personal use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal dependence of fishing activities in many regions | -0.4% | North America northern states, Northern Europe, and Northern Asia-Pacific | Short term (≤ 2 years) |

| Stringent fishing regulations and catch limits restricting participation | -0.3% | North America, the European Union, Australia, and New Zealand | Medium term (2-4 years) |

| High costs of premium fishing equipment and technical apparel | -0.3% | Global, with sharper pressure in price-sensitive South America and Middle East and Africa markets | Long term (≥ 4 years) |

| Environmental degradation affecting fish populations and fishing locations | -0.3% | Global, with stronger pressure in coastal Asia, the Mediterranean, and Asia-Pacific fisheries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal dependence of fishing activities in many regions

Seasonal dependence of fishing activities remains a significant challenge for the fishing apparel and equipment market, particularly in northern freshwater and mixed-climate regions. Weather conditions, ice coverage, and limited fishing seasons restrict participation opportunities in many parts of the northern United States, Canada, and Scandinavia. As a result, sales of fishing gear are often concentrated within a relatively short spring and summer period, while demand for apparel is compressed into even narrower seasonal windows. This concentration increases business exposure to unfavorable weather patterns, delayed thaw conditions, and fluctuations in consumer activity. Retailers and manufacturers may face inventory management challenges when peak purchasing periods are disrupted. Additionally, the OECD’s Review of Fisheries 2025 highlighted that the increasing frequency of extreme weather events is affecting fishing-related livelihoods and access to fishing locations[3]Source: Organisation for Economic Co-operation and Development, “OECD Review of Fisheries 2025”, oecd.org. These factors create uncertainty in participation levels and purchasing behavior, limiting consistent year-round demand for fishing apparel and equipment.

Stringent fishing regulations and catch limits restricting participation

Stringent fishing regulations and catch limits present a notable challenge for the fishing apparel and equipment market by limiting fishing activity in certain regions and seasons. Governments and fisheries management authorities increasingly implement quotas, catch restrictions, size limits, licensing requirements, and seasonal closures to protect fish populations and maintain sustainable ecosystems. While these measures support long-term conservation goals, they can reduce fishing opportunities for recreational and commercial anglers. Restrictions on specific species or fishing locations may discourage participation and lower the frequency of fishing trips. As a result, consumers may delay or reduce spending on fishing rods, reels, tackle, apparel, and related accessories. Regulatory complexity can also create uncertainty among anglers regarding permitted fishing activities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Scale Anchors Market While Apparel Accelerates

The equipment segment dominated the fishing apparel and equipment market in 2025, accounting for 73.85% of total revenue. Its leading position is attributed to the essential role that fishing rods, reels, lines, lures, tackle, fish finders, and related accessories play in recreational, sport, and commercial fishing activities. Anglers typically allocate a larger portion of their spending toward equipment due to its direct impact on fishing performance, efficiency, and success rates. Continuous technological advancements, including improved materials, lightweight designs, smart electronics, and enhanced durability, have further strengthened demand for fishing equipment. The segment also benefits from frequent replacement purchases and ongoing product upgrades among enthusiasts and professional users.

The apparel segment is projected to register the fastest CAGR of 3.82% through 2031, reflecting increasing consumer awareness of comfort, safety, and performance during fishing activities. Demand for specialized fishing apparel is rising as anglers seek products that offer UV protection, moisture management, waterproofing, and protection against varying weather conditions. Manufacturers are introducing innovative fabrics and functional designs that enhance comfort during extended outdoor use. The growing popularity of sport fishing and fishing tourism is also encouraging consumers to invest in premium apparel products, including fishing shirts, jackets, bibs, waders, gloves, and footwear. In addition, the influence of outdoor lifestyle trends and social media marketing has expanded the appeal of fishing apparel beyond dedicated anglers.

By End User: Adult Dominance Stable, Children Segment Gaining Structural Velocity

The adult segment dominated the fishing apparel and equipment market in 2025, accounting for 89.21% of total market revenue. Adults represent the largest consumer group due to their high participation in recreational, sport, and professional fishing activities across freshwater and saltwater environments. This segment benefits from greater purchasing power, enabling consumers to invest in premium fishing rods, reels, electronics, tackle, and specialized apparel. Many adult anglers also engage in competitive fishing events and fishing tourism, which further increases spending on high-performance equipment and protective clothing. The growing popularity of outdoor recreation and nature-based leisure activities has continued to strengthen demand among adult consumers.

The kids and children segment is expected to record the fastest CAGR of 4.08% through 2031, driven by increasing efforts to introduce younger generations to fishing and outdoor activities. Families are increasingly participating in recreational fishing trips, creating demand for age-appropriate fishing gear, apparel, and accessories designed specifically for children. Manufacturers are responding by launching lightweight, easy-to-use equipment and protective clothing tailored to younger users. Educational fishing programs, youth angling competitions, and outdoor recreation initiatives are also encouraging greater participation among children.

By Distribution Channel: Offline Stores Hold Majority Share While Online Accelerates

The offline stores segment dominated the fishing apparel and equipment market in 2025, accounting for 71.53% of total revenue. Its strong market position is driven by consumers’ preference to physically inspect fishing gear, apparel, and accessories before making purchasing decisions. Fishing equipment often requires hands-on evaluation of factors such as weight, durability, comfort, and functionality, making brick-and-mortar stores an important sales channel. Specialty fishing stores, sporting goods retailers, and outdoor recreation outlets also provide expert guidance, product demonstrations, and personalized recommendations that enhance the customer experience. In addition, immediate product availability and after-sales support contribute to the continued popularity of offline channels.

The online retail stores segment is projected to register the fastest CAGR of 4.46% through 2031, supported by the rapid expansion of e-commerce and digital shopping platforms. Consumers are increasingly turning to online channels due to the convenience of browsing a wide range of products, comparing prices, and accessing customer reviews from any location. Online retailers also offer access to international brands and specialized fishing products that may not be readily available through local stores. Improvements in logistics, faster delivery services, and secure payment systems have further strengthened consumer confidence in online purchases. As internet penetration and smartphone usage continue to rise globally, online retail is expected to gain a larger share of the fishing apparel and equipment market over the forecast period.

Geography Analysis

North America accounted for 35.01% of the global fishing apparel and equipment market in 2025, making it the largest regional market. The region benefits from a strong culture of recreational fishing, high consumer spending on outdoor activities, and widespread participation in sport fishing tournaments. The United States and Canada represent the primary revenue-generating countries, supported by extensive freshwater and coastal fishing opportunities. Consumers in the region show strong demand for premium fishing gear, advanced electronics, and performance-oriented apparel. Well-established distribution networks and the presence of leading manufacturers further strengthen market growth. Continuous product innovation and increasing adoption of technologically advanced fishing equipment are expected to sustain the region’s leadership position.

Asia-Pacific is projected to register the fastest CAGR of 4.38% through 2031, driven by rising interest in recreational fishing and outdoor leisure activities. Countries such as China, Japan, Australia, South Korea, and India are witnessing growing participation in both freshwater and saltwater fishing. Increasing disposable incomes and expanding middle-class populations are encouraging consumers to spend more on specialized fishing apparel and equipment. The region is also benefiting from the rapid growth of e-commerce platforms, which improve access to international and premium fishing brands. Government initiatives promoting tourism and outdoor recreation further support market expansion.

Europe, South America, and the Middle East and Africa collectively represent a significant share of the global fishing apparel and equipment market. Europe benefits from a well-established angling culture, particularly in countries such as the United Kingdom, Germany, France, and the Nordic nations, where recreational fishing remains highly popular. South America is experiencing gradual growth due to expanding fishing tourism and increasing participation in sport fishing activities. Meanwhile, the Middle East and Africa market is supported by coastal fishing traditions, growing tourism sectors, and rising interest in outdoor recreational pursuits.

Competitive Landscape

The Fishing Apparel and Equipment Market exhibits a moderately fragmented competitive structure, with several global manufacturers maintaining strong positions across different product categories. Major participants such as Shimano, Rapala VMC, Pure Fishing, and Johnson Outdoors have established extensive distribution networks, strong brand recognition, and broad product portfolios. However, no single company dominates the entire market, as demand is spread across diverse fishing disciplines and equipment types. The presence of numerous regional and niche manufacturers further intensifies competition. As a result, market leadership is distributed among companies specializing in specific segments rather than concentrated in the hands of a few dominant players.

Shimano and Rapala VMC are among the most influential competitors due to their extensive international presence and comprehensive offerings in rods, reels, lures, and fishing accessories. Pure Fishing strengthens its market position through a portfolio of well-known brands that cater to multiple customer segments, price points, and fishing styles. This multi-brand strategy enables the company to address varying consumer preferences across recreational, sport, and professional fishing activities. Continuous product innovation, sponsorship of fishing events, and investments in distribution expansion have helped these companies maintain strong visibility and customer loyalty in key regional markets.

Johnson Outdoors occupies a distinct position within the market through its focus on advanced fishing technologies and premium equipment solutions. Its brands, including Humminbird and Minn Kota, have gained significant recognition in fish-finding electronics, trolling motors, and navigation systems, particularly among serious anglers. At the same time, numerous specialized brands continue to hold strong credibility in categories such as fly fishing equipment, commercial fishing apparel, waterproof outerwear, saltwater gear, and terminal tackle products. This diversity of competitors fosters innovation and product differentiation, ensuring that the market remains highly competitive while offering consumers a wide range of specialized and performance-oriented fishing solutions.

Fishing Apparel and Equipment Industry Leaders

Shimano Inc.

Rapala VMC Corporation

Pure Fishing, Inc.

Johnson Outdoors Inc.

Globeride, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Abu Garcia entered the realm of digital cast-control technology by launching its Revo VoltiQ Series baitcasting reels. These reels featured the proprietary VoltiQ electronic casting system, which continuously monitored spool rotation and automatically adjusted braking in real-time, enhancing casting distance, accuracy, and control. The company offered two variants: the Revo SX VoltiQ with an alloy frame and the Revo X VoltiQ with a carbon-composite frame, targeting both premium enthusiasts and budget-conscious users.

- March 2026: Garmin pushed the boundaries of sonar technology by introducing a 360-degree scanning sonar system. This system, equipped with the motorised Spy Pole transducer, allowed anglers to view fish and underwater structures in a comprehensive 2D/3D bird's-eye perspective, eliminating the need for rescanning. This innovation elevated consumer-grade sonar capabilities and solidified Garmin's position at the forefront of advanced fishing electronics.

- January 2026: Shimano North America Fishing unveiled two new products: the Vanquish, the lightest in Shimano's MagnumLite spinning reel line, and the Stella 25000 SW D, a fresh offshore saltwater spinning reel. Each product catered to specific performance tiers, and their launch underscored Shimano's dedication to leading technological advancements in both ultralight freshwater and robust saltwater fishing segments.

Global Fishing Apparel and Equipment Market Report Scope

Fishing Apparel and Equipment refers to specialized clothing, footwear, accessories, and gear designed to enhance comfort, safety, protection, and efficiency during recreational, commercial, and sport fishing activities. The fishing apparel and equipment market is segmented by product type, end user, distribution channel, and geography. Based on the product type, the market is segmented into apparel, footwear, and equipment. Based on end user, the market is segmented into adults and kids/children. Based on the distribution channel, the market is segmented into offline and online stores. The market also covers the global-level analysis of major regions, such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts were made based on value (USD million).

| Apparel | |

| Footwear | |

| Equipment | Rods |

| Reels | |

| Hooks | |

| Others |

| Kids/Children |

| Adults |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Norway | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Rest of Middle East and Africa |

| By Product Type | Apparel | |

| Footwear | ||

| Equipment | Rods | |

| Reels | ||

| Hooks | ||

| Others | ||

| By End User | Kids/Children | |

| Adults | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the fishing apparel and equipment market by 2031?

The fishing apparel and equipment market is forecast to reach USD 26.15 billion by 2031, up from USD 22.32 billion in 2026, at a 3.22% CAGR over 2026-2031.

Which product type leads spending in fishing apparel and equipment?

Equipment remains the largest product type, accounting for 73.85% of value in 2025, supported by broad demand for rods, reels, tackle, and electronics.

Which product category is growing the fastest through 2031?

Apparel is the fastest-growing product type, with a projected 3.82% CAGR through 2031, driven by technical fabrics, UV protection, and performance wear adoption.

Why does North America lead this category?

North America held 35.01% of value in 2025 because it combines a large active angler base, strong tournament culture, mature retail access, and conservation-backed fishing infrastructure.

What is driving online sales of fishing gear and apparel?

Online stores are projected to grow at a 4.46% CAGR through 2031 as buyers become more comfortable purchasing repeat items and branded equipment through digital platforms.

Page last updated on: