Boutique Fitness Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

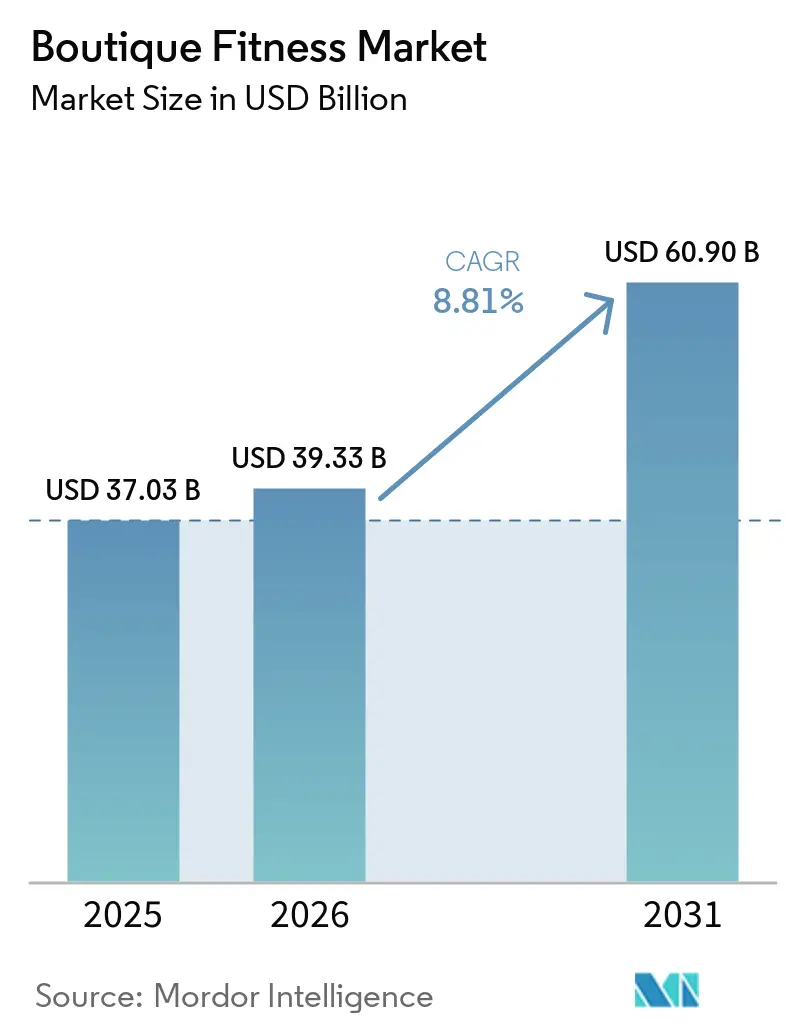

| Market Size (2026) | USD 39.33 Billion |

| Market Size (2031) | USD 60.90 Billion |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

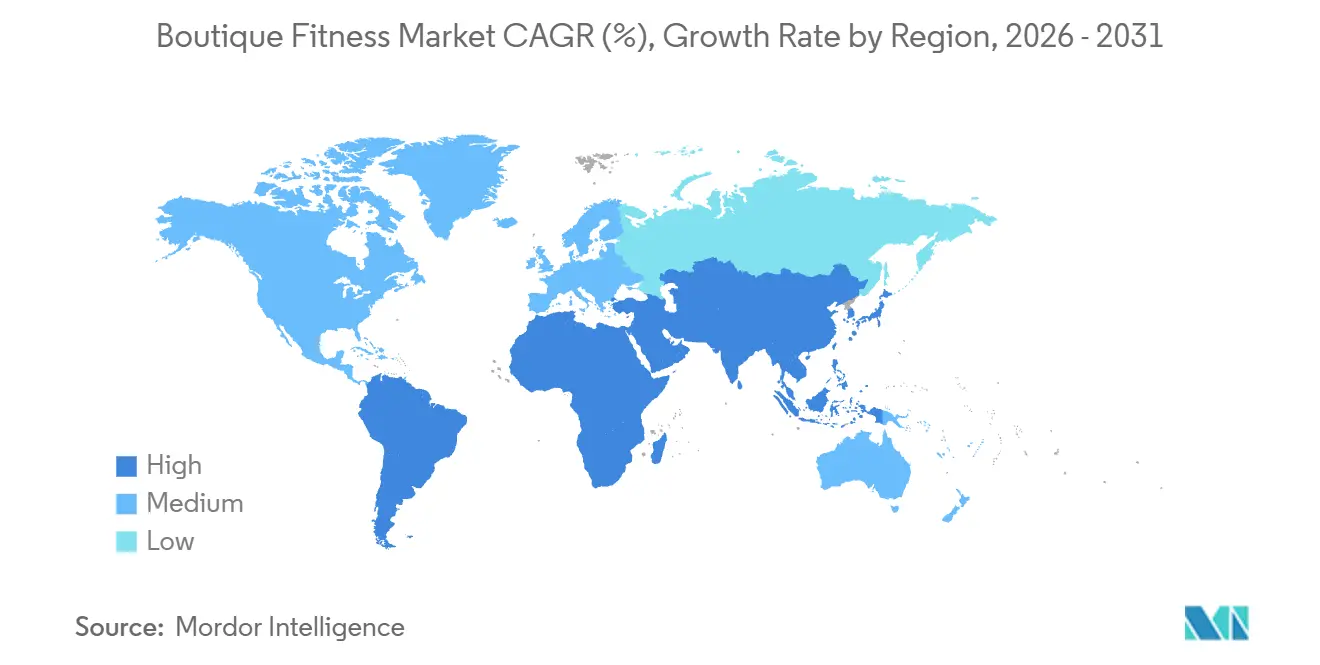

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Boutique Fitness Market Analysis by Mordor Intelligence

The boutique fitness market is projected to grow from USD 37.03 billion in 2025 to USD 39.93 billion in 2026 and reach USD 60.90 billion by 2031, with an 8.81% CAGR from 2026 to 2031. This growth is driven by consumer demand for specialized classes offering expert guidance, visible results, and better accountability than traditional gym memberships. In 2025, the U.S. recorded 81 million fitness facility memberships and nearly 7 billion visits, highlighting strong demand for structured exercise. Studio participation has become more active, with the member non-utilization rate dropping to 4.6%, improving attendance and ensuring stable recurring revenue. The market benefits from hybrid fitness trends, rising demand for personalized sessions, and increased participation from youth and women in urban areas. Competitive strategies focus on franchise expansion, wellness add-ons, digital coaching, and AI integration. Key opportunities lie in the Asia-Pacific region, youth-focused programs, and adaptable local formats.

Key Report Takeaways

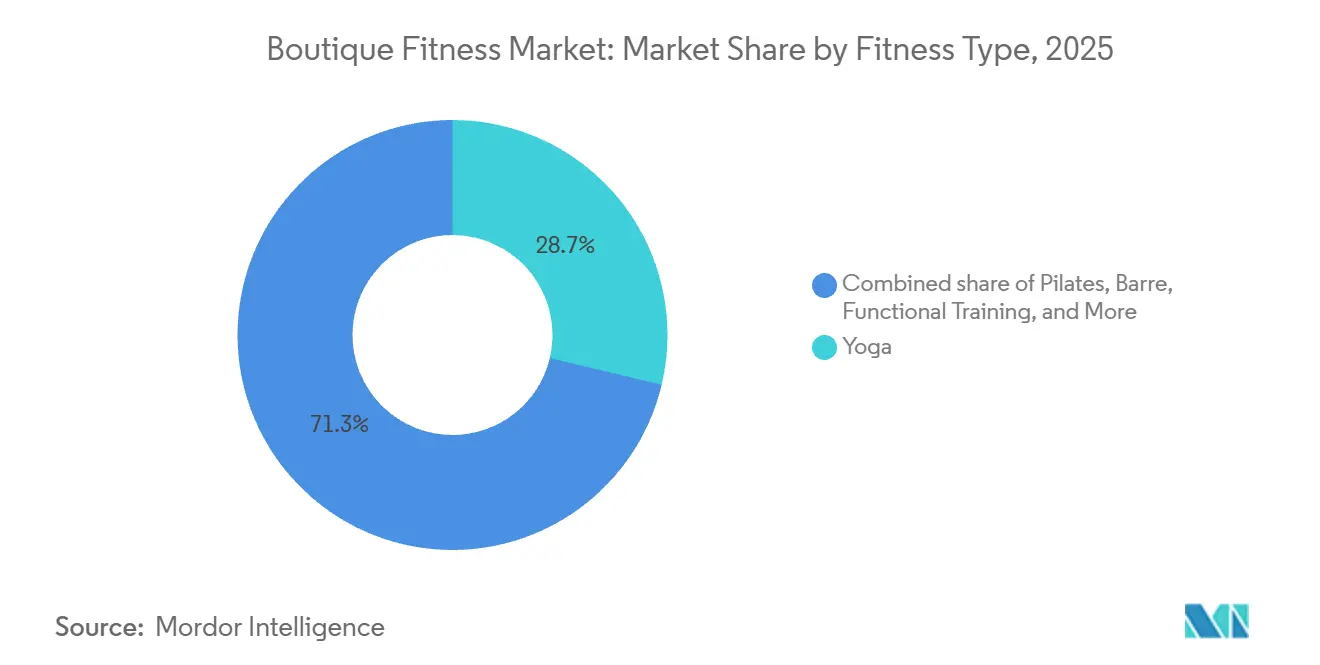

- By fitness type, yoga held 28.71% of boutique fitness market share in 2025, while dance fitness is forecast to expand at a 9.76% CAGR through 2031.

- By end user, women accounted for 65.23% of the segment in 2025, while children recorded the highest projected CAGR at 10.22% through 2031.

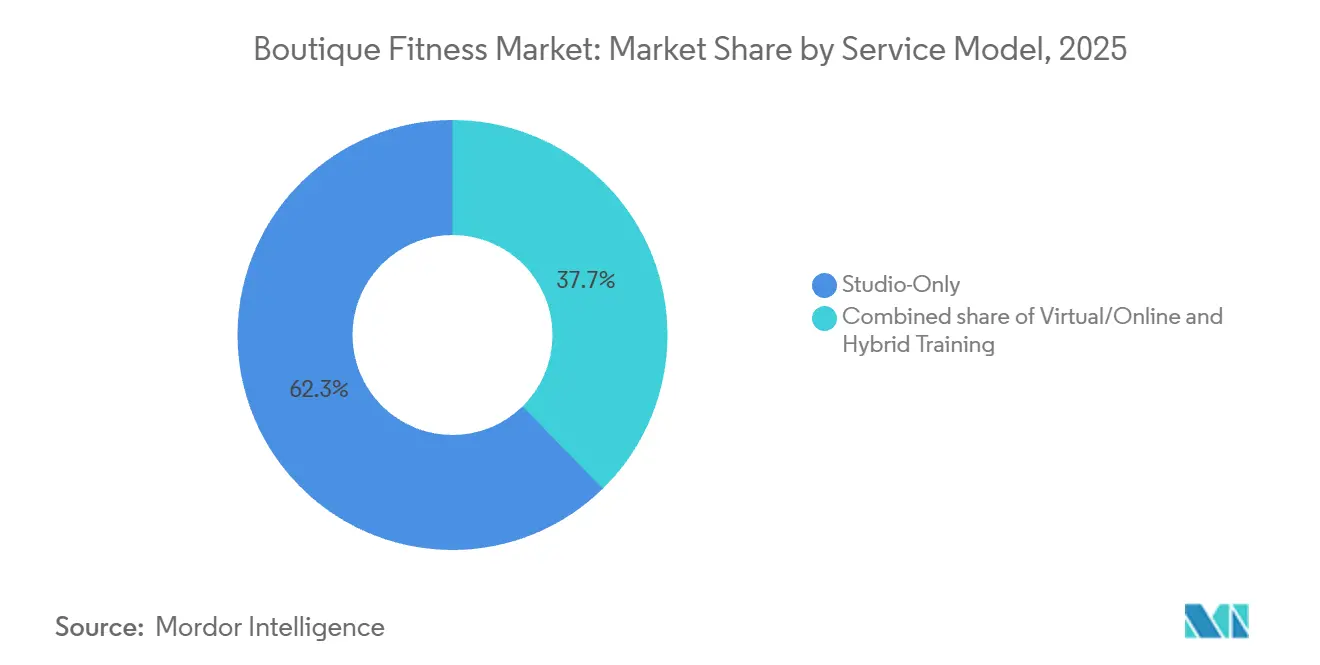

- By service model, studio-only accounted for 62.33% of the boutique fitness market size in 2025, while virtual or online is advancing at a 10.87% CAGR through 2031.

- By ownership model, the franchise model held 58.99% of the segment in 2025, while independently owned studios are projected to grow at a 9.82% CAGR through 2031.

- By geography, North America captured 42.92% of the boutique fitness market size in 2025, while Asia-Pacific is expected to expand at an 11.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Boutique Fitness Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Consciousness and Wellness Prioritization | +2.1% | Global | Long term (≥ 4 years) |

| Social Media Influence and Digital Fitness Trends | +1.6% | Global, with highest intensity in North America & APAC | Short term (≤ 2 years) |

| Growing Demand for Personalized and Specialized Workout Experiences | +1.8% | Global | Medium term (2-4 years) |

| Increasing Prevalence of Obesity and Sedentary Lifestyles | +1.4% | Global, Americas and APAC intensifying | Long term (≥ 4 years) |

| Millennial Demand for Holistic Wellness and Premium Amenities | +1.5% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Integration of AI Technologies and Smart Equipment | +1.2% | North America and Europe, rapid diffusion to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Wellness Prioritization

Preventive wellness is driving growth in the boutique fitness market. In 2025, 81 million Americans held fitness facility memberships, representing 26.1% of the population, one of the highest global rates[1]Source: Health & Fitness Association, “India Fitness Market Report 2025”, healthandfitness.org. Members were seven times less likely to report no weekly physical activity compared to non-members, with inactivity rates at 4.7% versus 33.1%. This highlights how structured participation builds lasting exercise habits rather than short-term efforts. Boutique fitness studios benefit from this trend by focusing on frequent attendance, instructor accountability, and community engagement, aligning with preventive health goals. Younger adults, especially Gen Z, led U.S. membership penetration at 35.5% in 2025, showing fitness is tied to social identity and daily routines. As a result, the boutique fitness market is thriving not only from increased health awareness but also from a shift in how consumers prioritize wellness spending.

Social Media Influence and Digital Fitness Trends

Social media is accelerating the adoption of new workout formats, enabling the boutique fitness market to swiftly elevate these concepts to mainstream prominence. In 2025, Gen Z made up 47% of all new gym memberships. This is significant, as this demographic leans heavily on digital platforms, peer visibility, and shareable experiences to decide where to work out. Visually appealing formats like Pilates, barre, yoga, and dance classes seamlessly align with this discovery trend, granting the boutique fitness market an edge over traditional gyms. Pricing remains robust in these socially prominent categories. For instance, average per-class prices climbed from USD 20.10 to USD 21.32 in the latest period. This uptick indicates that members are willing to pay a premium when they perceive the experience as unique and contemporary. Such pricing dynamics are crucial. They enable the boutique fitness market to counterbalance rising costs in rent, labor, and technology without a dip in demand. Furthermore, this trend underscores that digital visibility has evolved beyond mere marketing; it now plays a pivotal role in trial, brand relevance, pricing strategies, and member retention within the boutique fitness landscape.

Growing Demand for Personalized and Specialized Workout Experiences

As consumers move away from generic programming, the boutique fitness market is focusing on deeper specialization and better member-level customization. In early 2025, nearly 49% of fitness and wellness consumers used AI-powered apps or coaching tools daily. Additionally, 38% of Millennials and 33% of Gen Z stated that AI significantly supported their health goals, highlighting strong demand for personalized guidance. This demand is influencing operators' decisions. In April 2026, Technogym and Google Cloud announced a multi-year collaboration to integrate Gemini generative AI models into connected equipment and studio systems. This integration could reduce trainer program design time by up to 80%, raising service standards in digitally enhanced studios. Such advancements are vital for the boutique fitness market, where formats like yoga, HIIT, and Pilates already compete on instructor expertise and visible outcomes. Enhanced personalization strengthens this value proposition. The boutique fitness market is benefiting from rising interest in specialized formats and growing expectations for individualized relevance in every class, coach, and plan.

Increasing Prevalence of Obesity and Sedentary Lifestyles

The global obesity crisis is driving demand for structured exercise, boosting the boutique fitness market. In 2022, the World Health Organization reported over 1 billion people worldwide were living with obesity. By 2025, the WHO's Childhood Obesity Surveillance Initiative revealed that 25% of children aged 7-9 in 37 European countries were overweight or obese, with rates ranging from 9% to 42%. A 2024 WHO report also highlighted that adult physical inactivity levels remain off track for 2030 targets, with the Americas and Eastern Mediterranean showing the highest inactivity rates[2]Source: World Health Organization, “The WHO Acceleration Plan to Stop Obesity”, who.int. These trends are expanding the boutique fitness market, especially for low-impact, community-focused, and beginner-friendly formats that lower entry barriers for guided participation. Additionally, growing health risk awareness is increasing demand for fitness options that feel supervised, measurable, and sustainable over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Traditional Gyms and Big-Box Chains | -1.0% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| High Operational Costs and Premium Pricing | -0.8% | Global, worst in high-cost urban markets | Long term (≥ 4 years) |

| Dependence on Expert Trainers and Staff Quality | -0.5% | Global | Medium term (2-4 years) |

| Regulatory Compliance and Zoning Restrictions | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Traditional Gyms and Big-Box Chains

Competition from large-format gym operators is narrowing the original service gap that helped the boutique fitness market justify premium pricing. Bigger operators can add small-group formats, digital coaching, recovery services, and entry-level AI tools on top of a broader amenity base, while boutique studios cannot easily match the same breadth of offer at the same price point. This creates a structural pressure on the boutique fitness market, especially in cities where premium members compare value across multiple formats rather than staying loyal to a single class concept. At the same time, the boutique fitness market still retains a meaningful advantage in accountability, specialist instruction, and group identity, which helps protect attendance quality and annual retention. The pressure is therefore real, but it does not remove the core appeal of the category. The brands that are most exposed are usually the single-format concepts with limited programming flexibility, narrow audience reach, and heavy dependence on expensive urban locations.

High Operational Costs and Premium Pricing

High operating costs continue to challenge the boutique fitness market. This model relies on premium locations, trained instructors, smaller class sizes, and consistent technology investments. While average boutique class pricing rose from USD 20.10 to USD 21.32 in the latest reporting period, this increase falls short of fully countering inflation in rent, labor, and studio systems. Compliance costs are becoming increasingly evident for franchised operators. In March 2026, the Federal Trade Commission secured a USD 17 million settlement against Xponential Fitness for Franchise Rule violations. This action underscores heightened scrutiny on disclosure, governance, and operational practices within larger networks. Such scrutiny can lead to increased due diligence and legal costs for the entire boutique fitness market. The pressure is particularly pronounced in the middle tier. Studios here are too large to operate leanly, yet not big enough to distribute overhead costs efficiently across a wider member base. Consequently, while the boutique fitness market enjoys robust demand, maintaining margin stability proves more challenging than achieving topline growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fitness Type: Yoga’s Scale Advantage Meets Dance Fitness’s Acceleration

In 2025, yoga held a 28.71% share of the boutique fitness market, making it the leading format. Its wide demographic appeal, strong consumer familiarity, and adaptability to both dedicated studios and mixed programming schedules contributed to this dominance. The Health & Fitness Association ranked yoga as the top activity in U.S. fitness facilities in 2025, with 17.7 million members, highlighting its role in regular fitness routines. Yoga’s combination of exercise, recovery, stress management, and community engagement broadens its appeal, making it more resilient than niche fitness concepts targeting performance-focused audiences.In May 2026, CorePower Yoga strengthened yoga’s position by launching red light classes with HigherDOSE in select markets. This move reflects how leading operators are adding wellness features to boost revenue and stand out.

Dance fitness is the fastest-growing segment in the boutique fitness market, with a projected 9.76% CAGR from 2026 to 2031. It attracts beginners, older adults, and socially motivated individuals who avoid traditional gyms. Zumba celebrated its 25th anniversary in April 2026, reporting over 465 million classes globally across 200,000+ locations in 185 countries. This milestone highlights dance fitness’s global scale and appeal. In the boutique fitness market, dance fitness is an expansion category, bringing in new participants rather than shifting members from other formats.

By End User: Women Lead Market Participation, Children Drive Fastest Expansion

In 2025, women made up 65.23% of the end-user base, dominating the boutique fitness market. The market's focus on instructor-led sessions, smaller groups, and community engagement has consistently appealed to female participants. Data from the Health & Fitness Association in 2024 showed women drove a 16% year-over-year increase in personal training participation in the U.S., reaching 7.3 million users, while also leading growth in small-group formats. These trends are crucial for the boutique fitness market, as its core offerings, expert coaching, regular class attendance, and community engagement, align closely with women's preferences. Women's leadership stems not only from their participation size but also from their alignment with boutique operators' strengths.

Children are the fastest-growing demographic in the boutique fitness market, with a projected 10.22% CAGR from 2026 to 2031. This growth is driven by increased parental spending on children's physical development and rising awareness of childhood inactivity and obesity. The WHO Childhood Obesity Surveillance Initiative reported in 2025 that 25% of European children aged 7-9 were overweight or obese, emphasizing the need for structured physical activity. This has created opportunities in the boutique fitness market for youth-focused programs like conditioning, skill-building, and science-based development, bridging the gap between recreation and organized sports. These formats attract operators and investments as they address health, skill growth, and family spending needs.

By Service Model: In-Studio Attendance Holds Premium Share While Hybrid Formats Accelerate

In 2025, studio-only sessions accounted for 62.33% of the segment, highlighting the continued preference for in-person attendance in the boutique fitness market. Members value live coaching, scheduled sessions, and the social connections built through group participation. The Health & Fitness Association reported nearly 7 billion visits to U.S. fitness facilities in 2025, with only 4.6% of members not using their memberships, reflecting strong attendance. This trend supports the boutique fitness model, where frequent visits integrate studios into members' routines and boost sales in retail, recovery, and premium class packages.

Virtual and online services are the fastest-growing segment in boutique fitness, with a projected CAGR of 10.87% from 2026 to 2031. This growth reflects a hybrid approach rather than a shift away from studios. Digital platforms enhance scheduling flexibility, coaching continuity, and reach, helping operators engage members between visits, retain travelers, and serve areas with fewer studios. In May 2026, Xponential Fitness reported Club Pilates had 189 international studios across 14 countries and over 499 more under committed licenses, showing the importance of scalable digital options. While hybrid delivery expands reach and continuity, in-studio experiences remain central to premium engagement.

By Ownership Model: Franchises Command Share, Independent Studios Drive Growth

In 2025, the franchise model dominated the boutique fitness market, commanding a 58.99% share. This advantage stems from franchise systems leveraging stronger brand recognition, centralized marketing, operational playbooks, and shared technology, enabling new units to scale more rapidly than standalone studios. In April 2026, Xponential Fitness underscored the franchise model's strength by inked its most significant development pact with Riser Fitness, rolling out 127 new Club Pilates studios across six U.S. states over five years. This deal highlighted the confidence of capital-backed multi-unit operators in the boutique fitness market, even amidst heightened governance scrutiny and rising cost pressures. In a landscape where technology systems, lead generation, and instructor consistency play pivotal roles in member retention, the scale of franchises becomes paramount.

Independently owned studios are emerging as the fastest-growing segment in the boutique fitness arena, eyeing a robust 9.82% CAGR from 2026 to 2031. Their allure lies in lower entry barriers, adaptable pricing, localized positioning, and the agility to pivot based on neighborhood demands, sidestepping a one-size-fits-all brand approach. This flexibility is crucial, as certain smaller cities, suburban areas, and underserved urban locales may not warrant a full franchise rollout yet can thrive with tailored local concepts. Moreover, independent studios' nimbleness in adjusting to local preferences, be it scheduling, wellness offerings, or community collaborations, bolsters their loyalty in regions where larger operators are sparse. Given this trajectory, the boutique fitness landscape appears poised for a dual structure: expansive franchise systems will amplify their network scale, while local independents will adeptly seize niche demands.

Geography Analysis

In 2025, North America led the boutique fitness market, holding 42.92% of its size. This dominance is driven by a strong franchise network, consumer preference for premium fitness formats, and willingness to invest in specialized exercise experiences. U.S. fitness membership penetration reached 26.1%, with Gen Z adults at 35.5%. Adults aged 65 and above were the fastest-growing group, with an 8.6% year-over-year increase, showing the market's appeal across age groups. The combination of youth engagement, older adult growth, and a developed franchise system secures North America's leading position.

Europe remains a key region for boutique fitness, with membership growth driving the fitness base to record levels. EuropeActive reported 75.5 million fitness memberships in 2025, the highest ever, alongside EUR 39.1 billion in revenue, reflecting rising consumer spending. Boutique fitness benefits from this expanding active member base rather than relying solely on new adopters. With fitness penetration still below North American levels, Europe offers significant growth potential for premium studios.

Asia-Pacific is the fastest-growing boutique fitness market, with an 11.5% CAGR projected from 2026 to 2031. India presents a major opportunity, with boutique studios expected to grow at an 18.8% CAGR by 2030. As of 2024, 820 million Indians aged 18-62 were inactive, highlighting a vast untapped market. In China, urban centers are adopting yoga, cycling, and HIIT, driven by health awareness and digital fitness trends. South America and the Middle East & Africa are smaller markets but are growing due to urban demand, franchise expansion, and rising acceptance of structured fitness spending. Growth in these regions is concentrated in metropolitan areas with strong income levels and brand visibility.

Competitive Landscape

The boutique fitness market is moderately fragmented. It includes specialized brands focusing on unique workout formats, personalized coaching, and community engagement. Leading players like Xponential Fitness, Orangetheory Fitness, F45 Training Holdings Inc., CorePower Yoga LLC, and Equinox Holdings, Inc. offer tailored fitness experiences such as functional training, yoga, cycling, strength training, and high-intensity interval workouts. Growing demand for personalized wellness and experiential fitness allows regional and niche players to thrive alongside established brands.

Competition centers on brand loyalty, membership retention, instructor quality, and engaging in-studio and digital experiences. Major players invest in technology-driven platforms, mobile apps, performance tracking tools, and hybrid models combining physical and virtual classes. Franchise expansion helps operators like Xponential Fitness, Orangetheory Fitness, and F45 Training grow geographically while maintaining asset-light business models.

As interest in health, wellness, and community-based fitness rises, companies focus on service diversification, premium experiences, and partnerships to strengthen their positions. Luxury providers like Equinox stand out with integrated wellness ecosystems, while CorePower Yoga benefits from the growing popularity of mind-body fitness. Low entry barriers for independent studios and constant innovation in workout formats keep the market dynamic, pushing established and emerging players to enhance customer engagement and expand offerings.

Boutique Fitness Industry Leaders

Xponential Fitness

Orangetheory Fitness

F45 Training Holdings Inc.

CorePower Yoga LLC

Equinox Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CorePower Yoga, the largest US yoga studio brand with 220+ locations, launched "Red Light Classes" in partnership with wellness brand HigherDOSE, integrating full-body red (660nm) and near-infrared LED panels into select studio environments across New York, Los Angeles, Miami, and other major markets, creating a wellness-technology overlay that directly monetizes recovery demand within the yoga format.

- April 2026: Xponential Fitness signed the largest development agreement in its history with Riser Fitness, committing to 127 new Club Pilates studios across California, Idaho, Minnesota, Nevada, Oregon, and Washington over 5 years; Riser operates 110+ studios in 8 states, holds 340+ global development licenses, and is funded by over USD 140 million from Fortress Investment Group.

- April 2026: Technogym and Google Cloud announced a multi-year collaboration to integrate Google’s Gemini generative AI models into the Technogym AI Ecosystem, enabling AI-powered coaching programs and studio management tools that reduce trainer program design time by up to 80% and provide predictive member engagement analytics.

Global Boutique Fitness Market Report Scope

| Yoga |

| Pilates |

| Cycling/Spinning |

| Barre |

| High-Intensity Interval Training (HIIT) |

| Functional Training |

| Dance Fitness |

| Boxing & Martial Arts |

| Cross-Training |

| Others |

| Men |

| Women |

| Children |

| Studio-Only |

| Hybrid Training (In-Studio and Virtual) |

| Virtual/Online |

| Franchise Model |

| Independently Owned |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Fitness Type | Yoga | |

| Pilates | ||

| Cycling/Spinning | ||

| Barre | ||

| High-Intensity Interval Training (HIIT) | ||

| Functional Training | ||

| Dance Fitness | ||

| Boxing & Martial Arts | ||

| Cross-Training | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Service Model | Studio-Only | |

| Hybrid Training (In-Studio and Virtual) | ||

| Virtual/Online | ||

| By Ownership Model | Franchise Model | |

| Independently Owned | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving boutique fitness demand through 2031?

Growth is being supported by higher health awareness, stronger demand for specialized instruction, durable hybrid habits, and wider participation across women, youth, and urban professionals.

How large is boutique fitness expected to become by 2031?

The boutique fitness market is forecast to reach USD 60.90 billion by 2031, rising from USD 39.93 billion in 2026 at an 8.81% CAGR over 2026-2031.

Which workout format leads current revenue contribution?

Yoga led the fitness type segment with 28.71% share in 2025 because it has broad demographic reach and works well across dedicated and mixed studio schedules.

Why is Asia-Pacific important for future expansion?

Asia-Pacific is projected to grow at an 11.5% CAGR through 2031, with India standing out because boutique studios are the fastest-growing sub-segment within its broader fitness economy.

Page last updated on: