Golf Bags Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

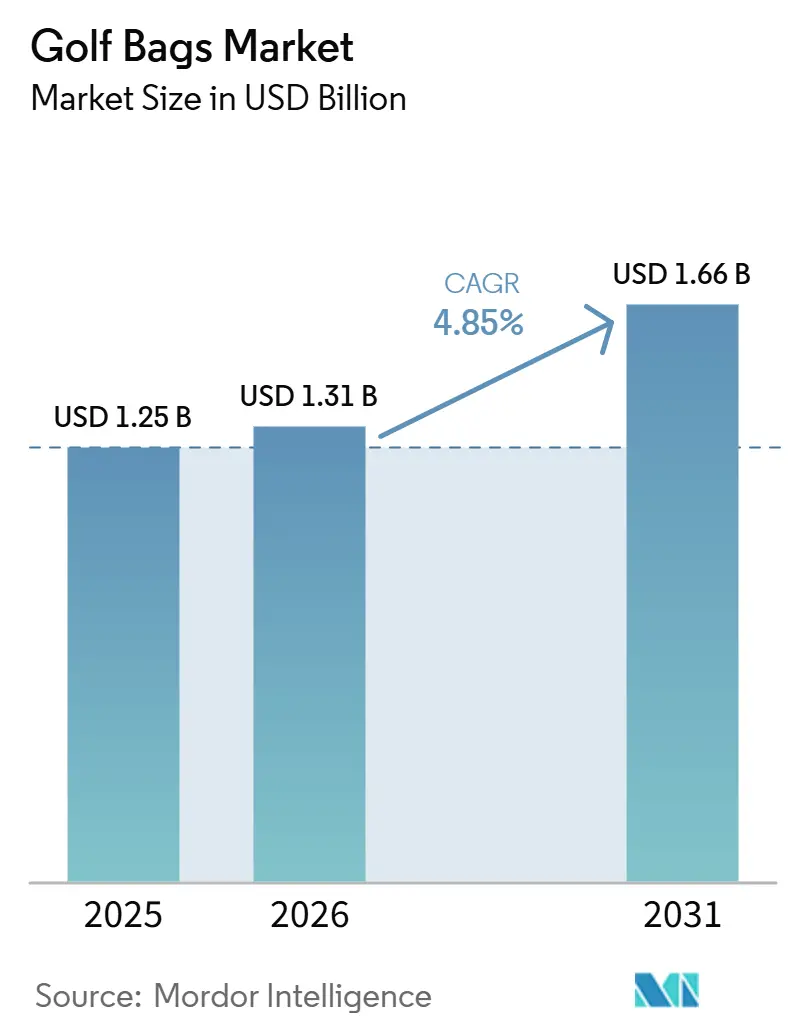

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Golf Bags Market Analysis by Mordor Intelligence

The golf bags market size is expected to grow from USD 1.25 billion in 2025 to USD 1.31 billion in 2026 and is forecast to reach USD 1.66 billion by 2031 at a 4.85% CAGR over 2026-2031. The market is growing due to an expanding and increasingly diverse golfer base. Participation now extends beyond traditional on-course players to include off-course users, women, and a rising number of first-time entrants compared to earlier cycles. Many of these newer players are first-time buyers, generating demand that goes beyond replacement purchases. The market is further supported by increased travel activity among golfers, with many purchasing bags for both regular play and travel, raising the likelihood of households owning multiple bags. Ongoing product design innovations are also narrowing the gap between premium and standard formats, making upgrades more justifiable and sustaining market activity across a wider range of price segments. Collectively, these factors support the continued expansion of the golf bags market.

Key Report Takeaways

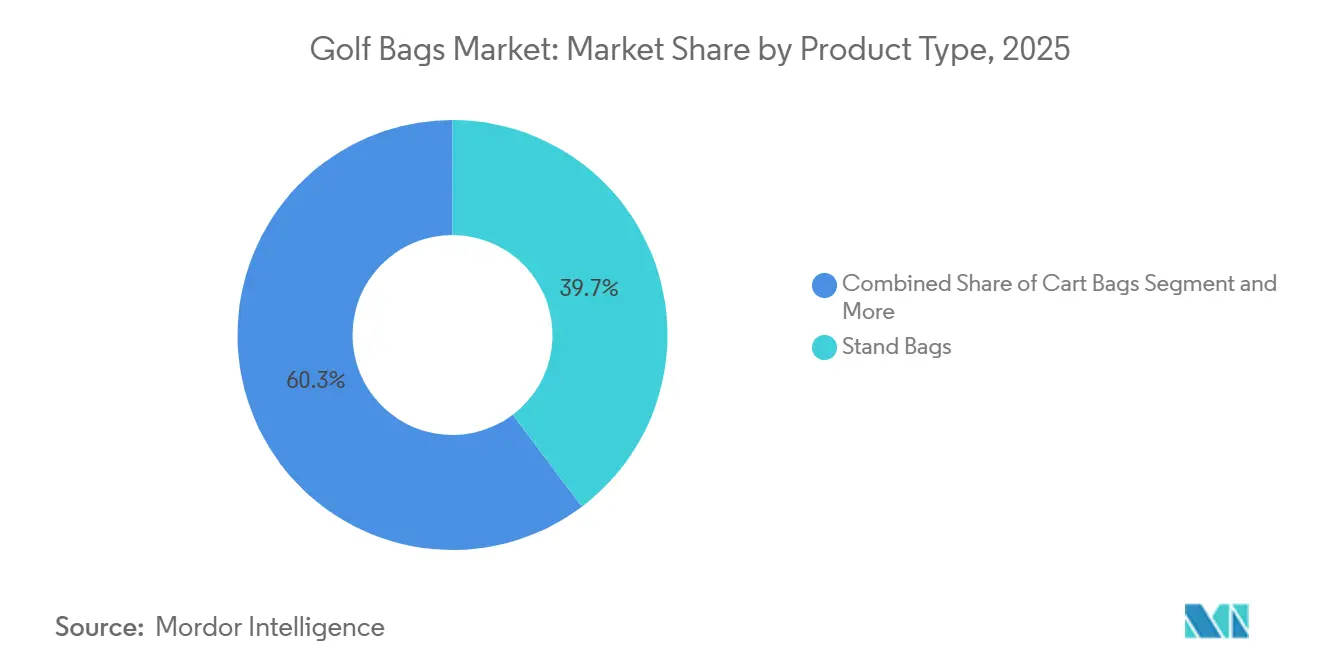

- By product type, stand bags held 39.72% of the golf bags market share in 2025; cart bags are projected to expand at a 5.91% CAGR through 2031.

- By material type, nylon commanded 47.53% of the golf bags market size in 2025, while polyester is set to grow at 6.01% CAGR by 2031.

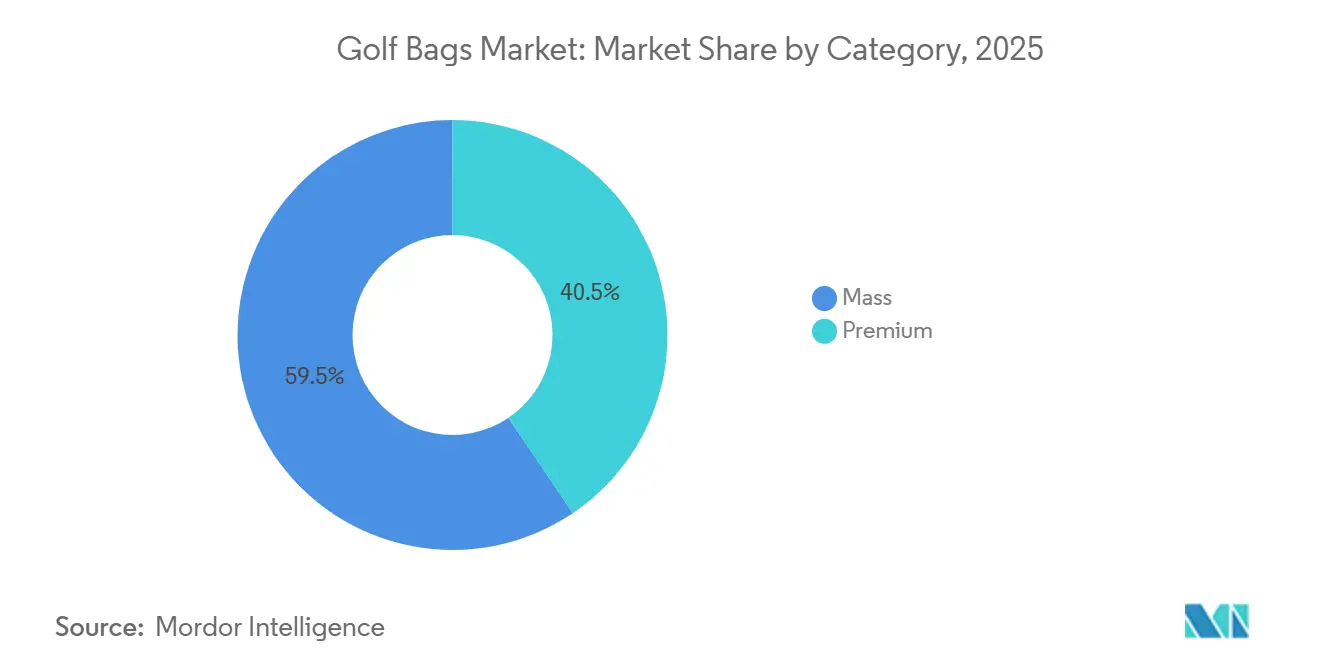

- By category, mass-market offerings accounted for 59.46% share of the golf bags market size in 2025; premium models are poised to accelerate at a 6.22% CAGR through 2031.

- By distribution channel, offline retail captured 65.59% of the golf bags market share in 2025, whereas online retail is forecast to advance at a 6.73% CAGR to 2031.

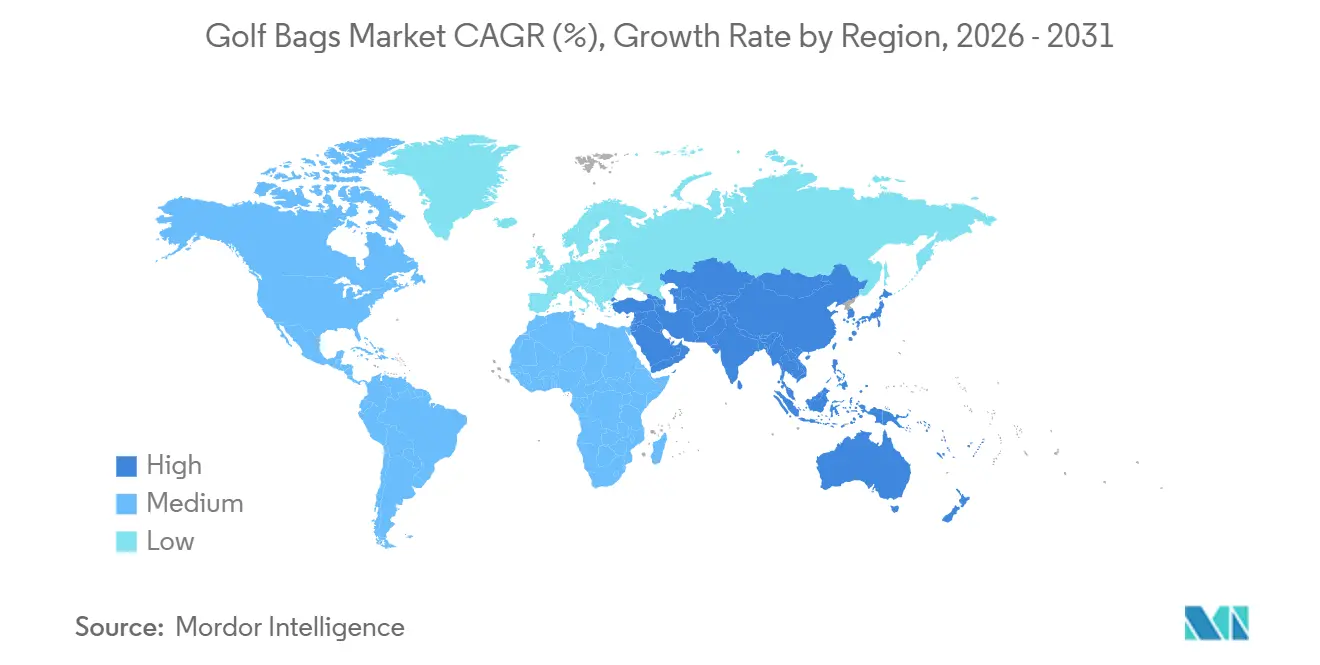

- By geography, North America led with 47.28% of the golf bags market share in 2025; Asia-Pacific represents the fastest-growing region and is projected to record a 6.68% CAGR through 203.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in golf | +1.4% | Global, with concentrated impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Growth in golf tourism and travel-ready equipment | +1.0% | North America and Europe core; spill-over to Asia-Pacific and Middle East and Africa | Medium term (2–4 years) |

| Advances in design and materials technology | +0.8% | Global, led by North America and Asia-Pacific manufacturing hubs | Medium term (2–4 years) |

| Expansion of golf courses and practice infrastructure | +0.5% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Sustainability-led materials and eco-friendly products | +0.4% | North America and Europe primary; early Asia-Pacific growth | Long term (≥ 4 years) |

| Customization demand from club fitting, branding, and team identity | +0.6% | North America and Europe primary; early Asia-Pacific growth | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising participation in golf

Rising participation in golf serves as a significant growth driver for the golf bags market. As reported by the National Golf Foundation (March 2026), the sport’s participant base has increased by 41% over the past six years (2019-2025), bringing it close to 50 million players for the first time[1]Source: National Golf Foundation, "Golf’s Growth Era – The Road to 50 Million Golfers", ngf.org. Last year alone, over 48 million Americans played golf at traditional courses or off-course facilities that are making the game more accessible and engaging. With an average annual growth rate of 6% for past 6 years, the United States golf market is projected to exceed 50 million participants by the end of 2026[2]Source: National Golf Foundation, "Golf’s Growth Era – The Road to 50 Million Golfers", ngf.org. This upward trend is fueled by expanded access to golf, the emergence of new facilities, and a growing awareness of the sport’s physical, mental, and social benefits, which continue to attract a broader and more diverse audience.

Growth in golf tourism and travel-ready equipment

According to National Golf Foundation (NGF) data published in April 2026, from 2022 through 2025, more than 12 million Americans traveled to play golf each year, with each of those four years recording either the highest or among the highest participation levels on record, reflecting increased consumer interest in experiential travel. The market has rebounded post-pandemic, generating more than USD 31 billion in travel-related expenditures in the United States and benefiting from new course openings at destinations such as Pinehurst and Bandon Dunes[3]Source: National Golf Foundation, "New Heights for Golf Tourism?", ngf.org. Rising airport travel numbers further indicate expanding demand for destination golf experiences. Additionally, growth in travel-ready golf equipment, focused on convenience and portability, has made it easier for golfers to take spontaneous and multi-day trips, supporting continued expansion in golf tourism.

Advances in design and materials technology

Advances in design and materials technology have contributed to growth in the golf bags market by enabling the production of lighter, more durable, and more functional bags. Innovations such as high-performance fabrics, water-resistant materials, and impact-resistant shells improve the overall quality and longevity of golf bags. Ergonomic design features, including padded straps, multiple compartments, and specialized storage solutions, enhance convenience and comfort during travel and on-course use. These improvements address the evolving needs of golfers by making it easier to carry equipment securely and efficiently. Continuous innovation in design and materials supports consumer interest and expands market opportunities within the golf bags segment.

Expansion of golf courses and practice infrastructure

The expansion and modernization of golf facilities continue to drive the golf bags market. According to the NGF's January 2026 industry overview, the United States has approximately 16,000 courses across nearly 14,000 facilities, with notable growth in recent years[4]Source: National Golf Foundation, "Golf’s State-of-Industry In 3 Minutes", ngf.org. As of 2025, these facilities are spread across various states, supporting high usage rates and sustained demand for golf equipment. Facility utilization remains high as operators continue to develop and upgrade golf courses and practice areas. Infrastructure investments enhance the playing experience and encourage greater participation in the sport. This modernization trend directly supports the golf bags market by increasing demand for quality equipment tailored to a growing and diverse golfer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and grey-market bags eroding brand trust | -0.7% | Global; most acute in Asia-Pacific and via cross-border e-commerce platforms | Short term (≤ 2 years) |

| Competition from substitute leisure sports | -0.4% | Global, with highest intensity in North America and Western Europe | Medium term (2–4 years) |

| Increasing interest in virtual golfing | -0.5% | North America and Europe; early-stage in Asia-Pacific | Medium term (2–4 years) |

| High product durability limiting replacement cycles | -0.6% | Global; most acute in premium and mid-market segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and grey-market bags eroding brand trust

Counterfeit golf bags represent a significant concern within the broader fake golf products market, affecting brand reputation and consumer trust. These counterfeit bags often imitate genuine designs but use inferior materials and construction, creating safety risks and causing customer dissatisfaction. Brands must protect these high-visibility products to maintain brand integrity and customer loyalty.

In May 2026, the U.S. Golf Manufacturers Anti-Counterfeiting Working Group conducted four raids in China and seized more than 109,569 counterfeit clubs, components, tools, labels, headcovers, and other golf products bearing the trademarks of all Golf Group members. Authorities detained eleven suspects. This action follows additional raids conducted by police earlier in the year, bringing the total number of counterfeit golf products confiscated in 2026 to 214,780. The seized products included golf bags, clubs, and accessories, underscoring the ongoing threat of counterfeit products in the golf industry.

Competition from substitute leisure sports

Competition from substitute leisure sports presents a significant challenge to the golf bag market, as consumers increasingly explore alternative activities such as pickleball, disc golf, and outdoor fitness pursuits, which typically do not require specialized or expensive equipment. These emerging sports attract participants due to their lower costs, greater accessibility, and broader appeal among younger demographics seeking quick, social, and easy-to-learn recreational options. As a result, demand for traditional golf gear, including golf bags, may decline. Furthermore, the growing popularity of these alternative activities can shift consumer spending and leisure time away from golf and its associated products. This trend highlights the need for the golf industry to innovate and adapt to changing consumer preferences to maintain market relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stand Bags Anchor Volume, Cart Bags Accelerating

Stand bags accounted for 39.72% of the golf bags market in 2025, driven by their alignment with the largest and fastest-growing participant cohort, recreational walking golfers who prioritize weight and portability over storage capacity. The post-pandemic normalization of on-course walking, combined with material innovations that have reduced premium stand bag weights to under 3 pounds, has reinforced stand bag dominance with no meaningful near-term threat from other formats.

Cart bags register the fastest product-type growth at a 5.91% CAGR through 2031, supported by an aging North American and European core golfer demographic that increasingly prefers motorized cart use, as well as the rising adoption of personal push-cart and electric caddy systems across Asia-Pacific markets. Staff/tour bags and other product types serve distinct but smaller niches: staff bags are primarily driven by pro tour branding cycles and team outfit programs, while travel bags represent a structurally growing sub-segment tied to the golf tourism surge, despite remaining a modest share of overall market.

By Material Type: Nylon Holds Structural Lead, Polyester Closes the Innovation Gap

Nylon held the largest material share, at 47.53%, in 2025, supported by years of proven performance in durability, water resistance, and weight efficiency, which have made it the default specification for mainstream and premium bag construction. Manufacturers are increasingly using ballistic and reinforced nylon grades while exploring emerging composite materials, including carbon fiber-reinforced polymer leg frames and structural biodegradable components. Although these innovations remain in the early stages of commercial application, they indicate the next cycle of material differentiation.

Polyester is the fastest-growing material segment at a 6.01% CAGR through 2031, driven by lower input costs that support price-competitive mass-market products in Asia-Pacific manufacturing chains, and by its compatibility with recycled fiber integration, which aligns with sustainability-oriented procurement among younger golfers. Recycled polyester now appears in an expanding range of golf bag constructions. Major equipment brands are establishing recycled synthetics as a viable performance material rather than a compromise specification.

By Category: Mass Segment Holds Majority Position, Premium Conversion Accelerating

The mass category accounted for 59.46% of the market value in 2025, primarily driven by recreational golfers worldwide. These consumers tend to prioritize functionality and price over brand prestige or advanced materials, making affordability a key factor in their purchasing decisions. This segment is particularly dominant in Asia-Pacific markets, where golf participation is growing at the entry level, and in price-sensitive regions such as South America and the Middle East. In these markets, golf is often viewed as an aspirational activity rather than an established leisure pursuit, reinforcing demand for accessible, value-driven products.

The premium category is growing at the fastest rate, with a compound annual growth rate (CAGR) of 6.22% projected through 2031. This growth is driven by the increasing influence of the custom-fitting ecosystem, which improves consumer experience and product personalization. The broader outdoor sports market is also shifting toward premiumization, as consumers seek higher-quality equipment that offers better performance and exclusivity. This reflects a shift in consumer preference toward more specialized, high-end golf products, even within a market traditionally dominated by mass-market offerings.

By Distribution Channel: Offline Retail Remains Dominant, Digital Channels Reorder Competitive Dynamics

Offline retail held the largest share of the golf bags market in 2025, accounting for 65.59%. Golfers often prefer to physically evaluate products, checking strap ergonomics, pocket configurations, and material feel, before making higher-priced purchases. Specialty golf retailers and pro shops maintain a competitive edge by offering personalized fitting assistance and same-day availability, which online channels cannot easily replicate. Competition among offline retailers is strongest in pro shops, where original equipment manufacturer brands benefit from established relationships with club professionals. Bag brands also use green-grass retail education programs and demo days to boost visibility and compete against larger incumbents with greater resources.

Online retail is the fastest-growing distribution channel, with a projected CAGR of 6.73% through 2031. This growth is driven by factors including user reviews, detailed specification comparisons, and direct-to-consumer (DTC) platforms that build trust among informed buyers. DTC brands continue to see increasing success as consumers favor direct engagement with manufacturers. The online channel also offers margin advantages by eliminating markdown pressure and enabling manufacturers to collect customer data for targeted lifecycle marketing.

Geography Analysis

North America held 47.28% of the golf bags market share in 2025, making it the clear regional leader. The region benefits from dense golf infrastructure, strong equipment spending, and a large active player base. According to national golf federation, as of February 2026, United States golfers played more than 500 million rounds in 2025 for the sixth consecutive year, keeping equipment usage and replacement demand elevated. Golf travel also remains significant in the region, with more than 12 million Americans traveling to play golf each year between 2022 and 2025 according to national golf federation. This creates simultaneous demand for regular play bags and travel-oriented formats.

Asia-Pacific is forecast to grow at a 6.68% CAGR through 2031, making it the fastest-growing region in the golf bags market. Japan remains the most mature market within the region, while China offers the strongest growth potential as registered golfer numbers continue to rise. South Korea contributes a design-conscious buyer base, and Southeast Asia is gaining ground through both domestic participation and golf tourism. South America and the Middle East and Africa remain smaller markets currently, but both present long-term opportunity as course investment and premium leisure spending increase.

Europe remains a significant part of the golf bags market, combining established golf traditions with active tourism demand and steady participation across several countries. The United Kingdom, Germany, Ireland, and Scandinavia remain important consumption centers, while Southern and Eastern Europe continue to broaden the playing base. Waterproof construction is particularly relevant in Europe, as playing conditions frequently make weather resistance a practical priority. This sustains demand for premium materials and specialized finishes even when unit growth is moderate. France and the United Kingdom are also projected to post strong growth rates through 2031, indicating uneven but favorable momentum across the region.

Competitive Landscape

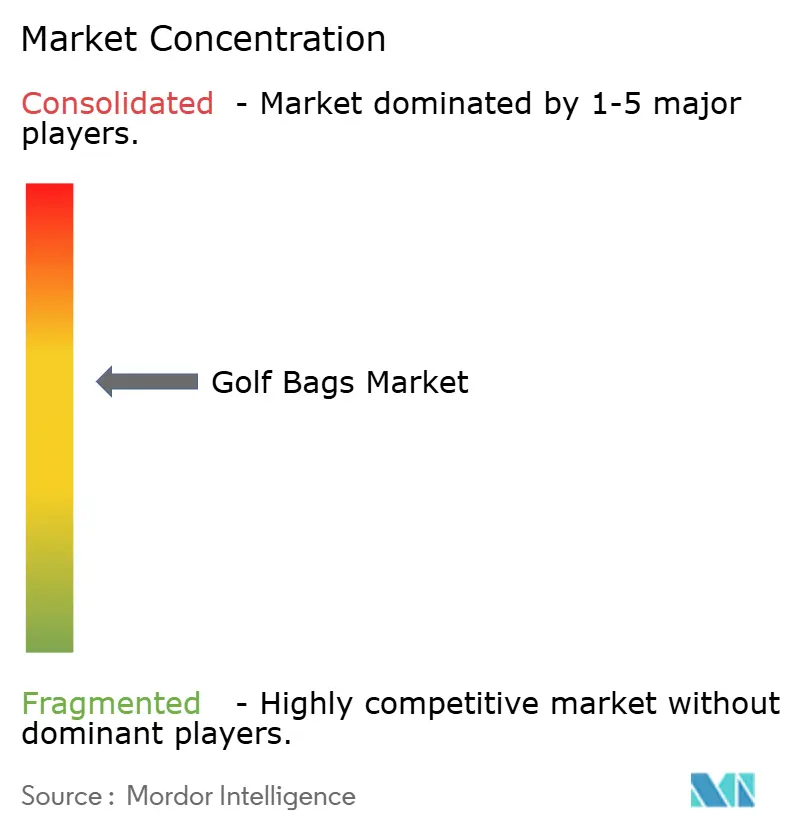

The golf bags market is moderately fragmented, with a diverse mix of established equipment manufacturers, specialist bag brands, and newer direct-to-consumer (DTC) players competing across overlapping price segments. No single player dominates the entire category, as the market spans various product types, materials, channels, and regional markets. Major brands such as Acushnet Holdings Corp. (Titleist), Callaway Golf Company, PING, Inc., TaylorMade Golf Company, and Sun Mountain Sports benefit from long-standing trust built through their golf clubs, balls, and equipment, which supports their bag sales. Specialist brands like VESSEL, Club Glove, Jones Sports, and BIG MAX compete by focusing on design innovation, weight reduction, organization, and format, keeping the competitive landscape active.

Leading players are refining their product lines and strategic positioning. Acushnet Holdings Corp. (Titleist) launched new premium stand bags in March 2025, featuring redesigned leg systems, advanced materials, and waterproof options to strengthen its premium carry lineup. Callaway Golf Company shifted its strategic focus by selling a majority stake in Topgolf in January 2026, aiming to streamline its core golf equipment business and invest further in clubs, balls, bags, and the OGIO brand. PING, Inc. expanded its product offerings in 2025 as well by introducing lightweight bags to appeal to a broader audience. TaylorMade Golf Company focused on integrating premium materials into its latest bag collections in June 2026. Sun Mountain Sports continued expanding its range of high-performance, durable bags tailored for serious golfers as of June 2026. Across these players, product innovation, ecosystem expansion, and strategic focus are central to maintaining competitive advantage.

Emerging players are identifying niche opportunities by addressing gaps in sustainability, technology integration, and demographic-specific designs. Growth potential exists in sustainable materials, particularly at accessible price points, as consumer expectations shift toward eco-friendly products. Technology integration remains uneven, with high-end models adopting smart features more rapidly than mainstream options. Women-specific designs represent another area of opportunity, as many brands rely on cosmetic updates, superficial styling changes that do not enhance ergonomics or functionality, rather than substantive ergonomic and organizational improvements, despite a growing female golf participation base. Established players such as Sun Mountain Sports, Titleist, Callaway, PING, and TaylorMade hold advantages in brand protection, as anti-counterfeit measures are more effective when coordinated among major players, helping to safeguard premium segments amid ongoing market fragmentation.

Golf Bags Industry Leaders

-

Sun Mountain Sports

-

Acushnet Holdings Corp.

-

Callaway Golf Company

-

PING, Inc.

-

TaylorMade Golf Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sun Mountain Sports, in collaboration with Realtree, announced the launch of its limited edition Major Collection, featuring two products: the Matchplay 4-Way Stand Bag and the ClubGlider Meridian Travel Bag. The Matchplay 4-Way Stand Bag features a Realtree camo design with eight purpose-built pockets, including an apparel pocket, valuables pocket, and insulated cooler pouch, and four full-length dividers for club organization. Built with ballistic nylon and equipped with the X-Fit Dual Strap System, this bag retails at USD 435. The ClubGlider Meridian Travel Bag, priced at USD 450, is designed for travel with a patented kickstand, reinforced ballistic-style construction, and heavy-duty two-way zippers. Both products are available for a limited time through select retailers.

- April 2026: TaylorMade launched its 2026 Season Opener Collection, featuring a range of accessories tied to golf's most recognized tournament. The centerpiece is a limited-edition TaylorMade Staff Bag in an emerald green and white color palette with gold hardware. The bag includes azalea embroidery on the side panels, referencing the tournament's floral emblem, along with a detachable numbered patch representing the tournament's edition this year.

- February 2026: Titleist announced the launch of its latest Players S Stand Bags lineup, featuring a comprehensive redesign based on golfer testing and insights. The new models, Players S4, Players S4 StaDry, and Players S5, offer improved durability, lightweight performance, and enhanced organization. Key features include redesigned stand systems for reliable leg deployment and stability, new top cuff designs for easier club access, and upgraded materials with greater UV and water resistance. The Players S4 and S4 StaDry models feature a lightweight construction, with the StaDry version offering seam-sealed waterproof protection suited for damp conditions. The Players S5 offers greater storage capacity with a 5-way top cuff and additional pockets. All models include double straps, full-length dividers, magnetic tee pockets, and YKK zippers. These stand bags are now available worldwide.

Global Golf Bags Market Report Scope

The report covers various product types in the golf bags market, including stand bags, cart bags, staff/tour bags, and other product types. This segmentation supports analysis of consumer preferences and demand patterns across different styles and functionalities, providing insights into market trends and growth opportunities for each category.

In terms of material type, the report examines nylon, polyester, leather, and other materials used in manufacturing golf bags. Understanding material composition provides insights into durability, cost, and premium positioning, helping stakeholders identify key material developments and consumer preferences.

The market is also segmented by category into mass and premium segments. This division highlights the differences in consumer bases, price sensitivities, and brand strategies, allowing for a better understanding of how premium offerings compete with mass-market products across various regions.

Distribution channels are analyzed through offline retail and online retail segments. This segmentation clarifies how consumers access golf bags, highlighting the importance of multi-channel strategies, e-commerce trends, and the evolving retail landscape within the industry.

Geographically, the report segments the market into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. Each region is further divided into key countries and the rest of the area, enabling a comprehensive understanding of regional dynamics, market size, and growth drivers across different parts of the world.

| Stand Bags |

| Cart Bags |

| Staff/Tour Bags |

| Other Product Types |

| Nylon |

| Polyester |

| Leather |

| Other Material Types |

| Mass |

| Premium |

| Offline Retail |

| Online Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Stand Bags | |

| Cart Bags | ||

| Staff/Tour Bags | ||

| Other Product Types | ||

| By Material Type | Nylon | |

| Polyester | ||

| Leather | ||

| Other Material Types | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail | |

| Online Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the golf bags business and where is it heading by 2031?

The golf bags market was valued at USD 1.25 billion in 2025, reached USD 1.31 billion in 2026, and is forecast to reach USD 1.66 billion by 2031 at a 4.85% CAGR.

Which product type leads demand in golf bags?

Stand bags led in 2025 with 39.72% share because they fit recreational and walking golfers who want portability and lighter carry weight.

Which sales channel is growing the fastest for golf bags?

Online retail is growing the fastest at a 6.73% CAGR through 2031, although offline retail still held the larger 65.59% share in 2025.

Why is the premium side of golf bags growing faster than the mass segment?

Premium bags are benefiting from stronger upgrade demand, brand-led purchases, and buyers who see the bag as part of a broader equipment identity, lifting premium CAGR to 6.22%.

What are the main risks affecting golf bag demand?

The biggest pressures come from counterfeit products, long replacement cycles for premium bags, and growing simulator-based golf activity that reduces on-course equipment wear.

Page last updated on: