Sports Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

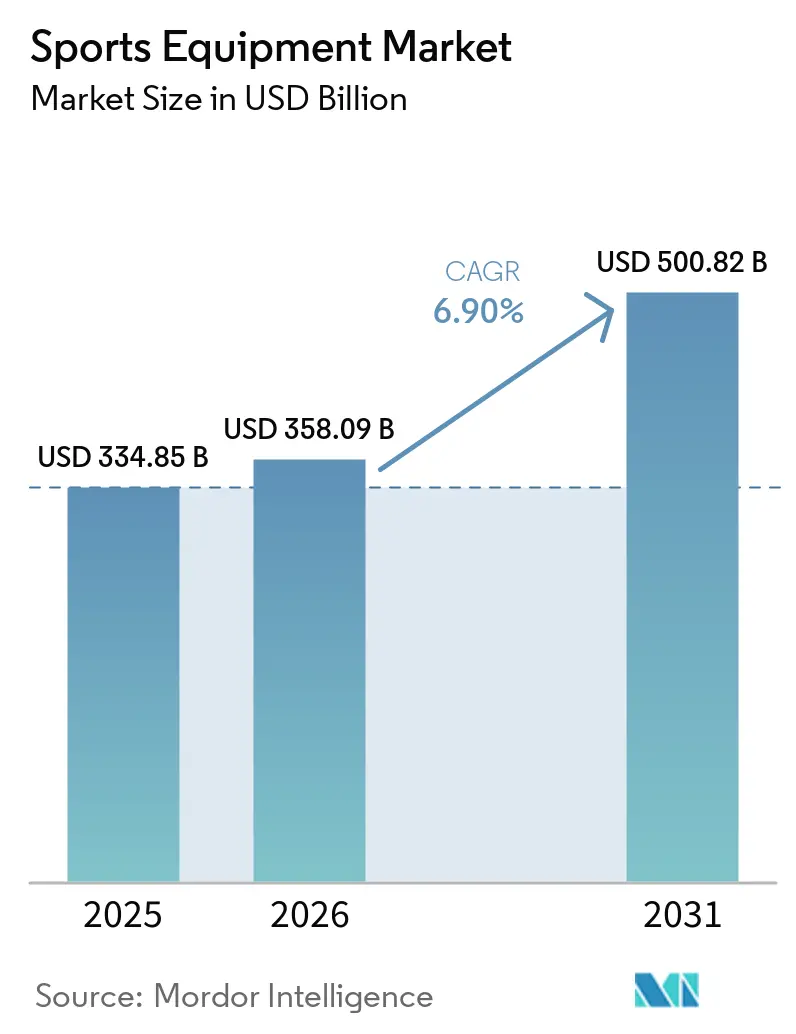

| Market Size (2026) | USD 358.09 Billion |

| Market Size (2031) | USD 500.82 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

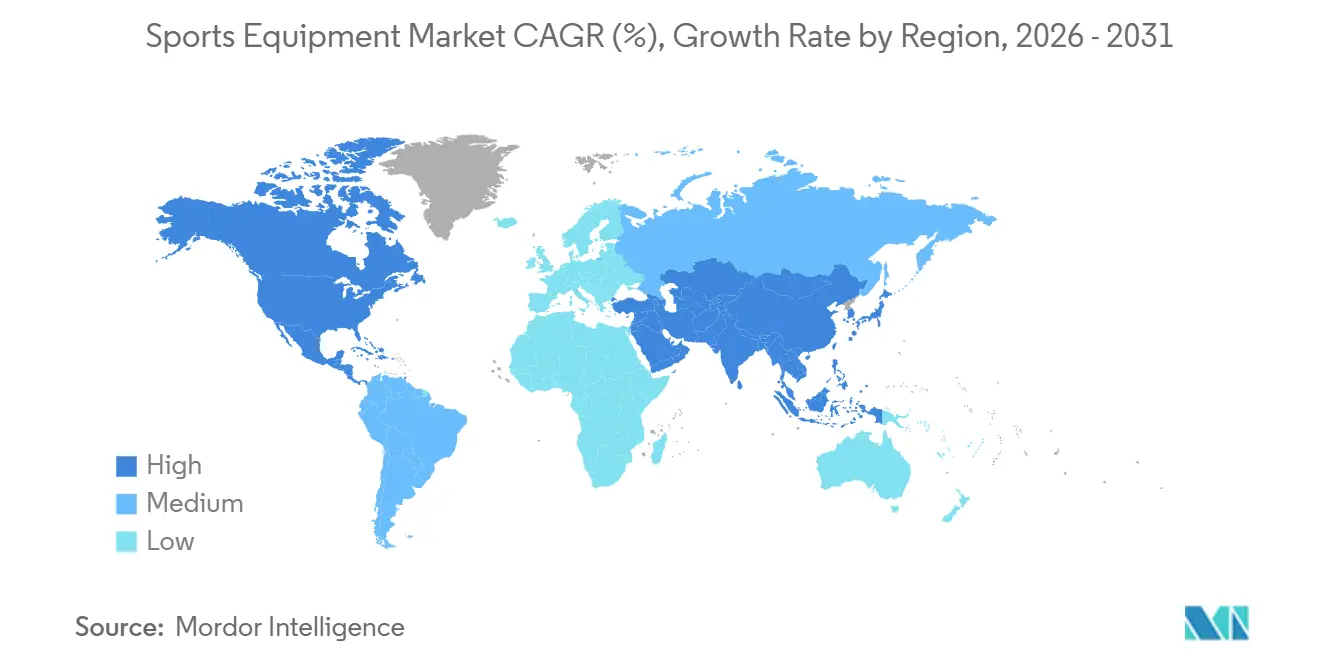

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sports Equipment Market Analysis by Mordor Intelligence

The Sports Equipment Market is projected to grow from USD 334.85 billion in 2025 to USD 358.09 billion in 2026, reaching USD 500.82 billion by 2031, with a CAGR of 6.90% during 2026–2031. This growth is primarily attributed to the increasing global emphasis on physical fitness, active lifestyles, and participation in both recreational and professional sports activities. Rising consumer awareness about health, wellness, obesity management, and mental well-being is driving greater engagement in fitness routines, outdoor recreation, athletic training, and sports-based leisure activities. This trend is significantly boosting the demand for sporting goods and exercise equipment. Additionally, the growing popularity of gym memberships, home fitness programs, adventure sports, cycling, running, and team-based recreational activities is sustaining strong long-term demand across various equipment categories.

Key Report Takeaways

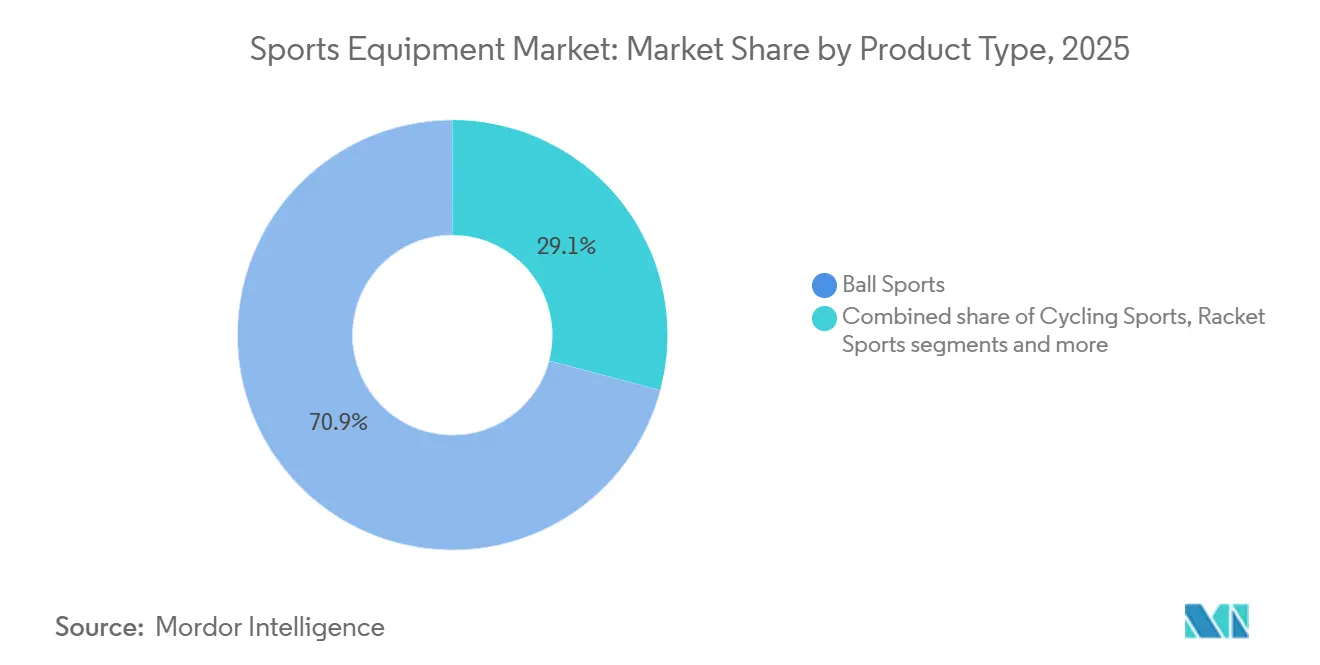

- By product type, ball sports held 70.89% of market revenues in 2025, while water sports is projected to grow at 7.56% through 2031.

- By end user, male consumers accounted for 66.87% of revenues in 2025, while the female segment is forecast to expand at 8.34% through 2031.

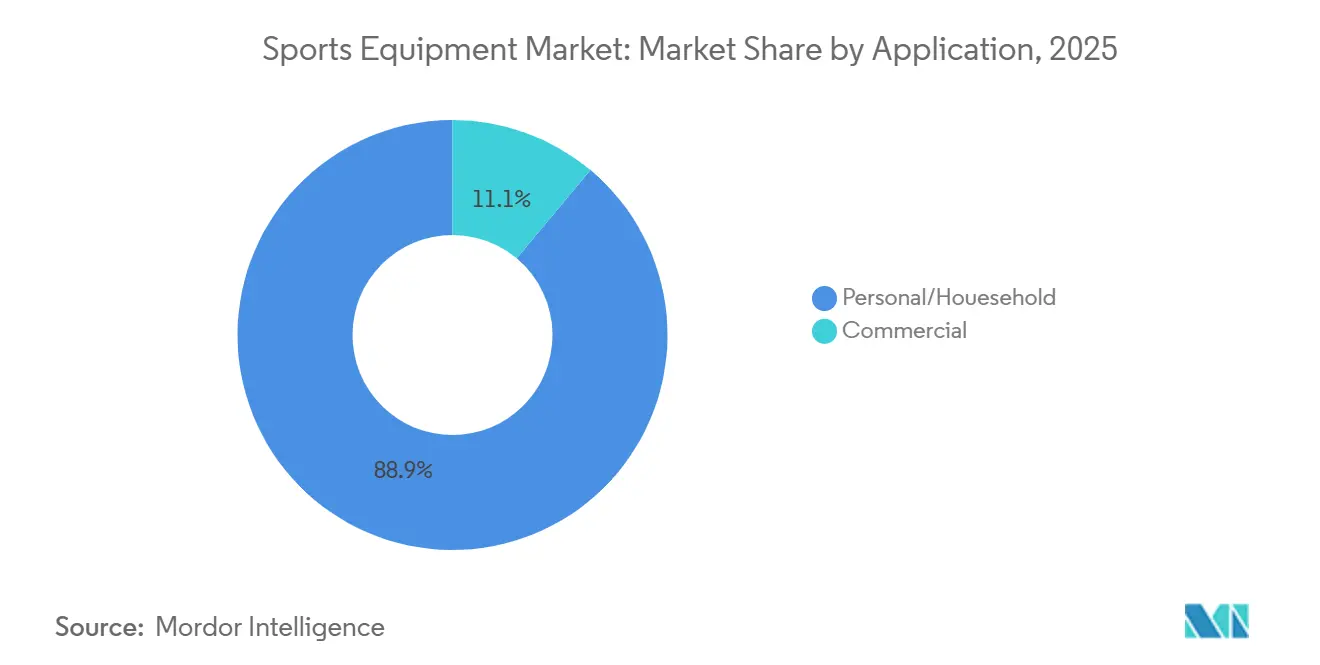

- By application, personal and household use represented 88.91% of revenues in 2025, while the commercial segment is projected to grow at 7.12% through 2031.

- By distribution channel, offline retail stores held 69.31% of revenues in 2025, while online retail stores are forecast to advance at 9.11% through 2031.

- By geography, North America accounted for 38.01% of revenues in 2025, while Asia-Pacific is projected to grow at 8.09% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sports Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in recreational and professional sports | +1.8% | Global; strongest in North America and urban Asia-Pacific | Short term (≤2 years) |

| Growing health and wellness awareness | +1.4% | Global; North America and Europe; urban Asia-Pacific | Long term (≥4 years) |

| Rising popularity of outdoor and adventure sports | +1.0% | North America, Western Europe, premium urban Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in sports equipment | +0.9% | North America and Europe (early adoption), premium Asia-Pacific | Long term (≥4 years) |

| Rising influence of international sporting events | +0.7% | Global; near-term peak in Americas and Europe (FIFA WC 2026) | Short term (≤2 years) |

| Growth in youth sports programs and school athletics | +0.5% | North America (strongest); spill-over to South America America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising participation in recreational and professional sports

Rising involvement in fitness activities, competitive sports, and outdoor recreational programs is fueling strong demand for sporting goods, training accessories, and protective equipment. Growing awareness of physical health, active lifestyles, mental wellness, and athletic performance is motivating consumers across various age groups to engage more actively in sports and recreational activities. This trend is leading to consistent purchases of equipment for team sports, individual fitness training, adventure sports, racquet sports, and outdoor recreational activities. For example, according to Statistics Poland, approximately 43.7% of people in Poland participated in sports or recreational activities in 2025, underscoring the increasing consumer engagement in physical and recreational fitness activities [1]Source: Statistics Poland, "Participation in sport and recreational activities in 2025", stat.gov.pl. Additionally, the rising popularity of organized tournaments, school athletics, gym memberships, and outdoor recreational participation is driving higher spending on performance-enhancing sports products and fitness equipment.

Growing health and wellness awareness

Increasing health and wellness awareness is driving the growth of the global sports equipment market, as consumers prioritize physical fitness, active lifestyles, and preventive healthcare to enhance overall well-being. Concerns about obesity, cardiovascular diseases, stress management, and sedentary lifestyles are motivating individuals to adopt regular exercise routines, recreational sports, gym training, yoga, cycling, and outdoor fitness activities. This emphasis on physical and mental health is boosting demand for fitness equipment, training accessories, sports gear, and wearable performance products for both household and commercial use. Additionally, awareness campaigns promoting healthy living and participation in physical activities are supporting sustained market growth. The rising adoption of home workouts, digital fitness programs, wellness applications, and sports-based recreational activities is further driving equipment purchases among consumers aiming for healthier lifestyles.

Rising popularity of outdoor and adventure sports

The increasing popularity of outdoor and adventure sports is a significant driver for the global sports equipment market. Growing consumer interest in recreational travel, nature-based activities, and fitness-oriented outdoor experiences is fueling the demand for specialized sporting gear and protective equipment. Activities such as hiking, trekking, camping, cycling, climbing, kayaking, surfing, and mountain sports are becoming increasingly popular among consumers pursuing active and experience-driven lifestyles. Additionally, rising awareness of physical wellness, stress reduction, and adventure tourism is encouraging participation in outdoor recreational activities across various age groups. For example, the Outdoor Industry Association's 2026 Hiking Report indicated that approximately 63.4 million Americans actively participated in hiking, underscoring the growing consumer engagement in outdoor recreational sports [2]Source: Outdoor Industry Association, "The Hiking Boom Isn't Slowing Down", outdoorindustry.org.

Technological advancements in sports equipment

Technological advancements in sports equipment, including innovations in materials, connectivity features, and performance-enhancing designs, are improving user experience, safety, and athletic efficiency. Manufacturers are increasingly incorporating technologies such as smart sensors, wearable tracking systems, lightweight composite materials, shock absorption systems, and connected fitness devices into sports products to enhance training accuracy and performance monitoring. These developments are driving adoption among both professional athletes and recreational users, as they offer improved durability, comfort, injury prevention, and real-time performance analysis. Furthermore, the rising popularity of data-driven fitness training and personalized athletic programs is boosting demand for smart sports equipment across various sports categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium sports equipment | -1.1% | Developing markets; lower-income cohorts globally | Long term (≥4 years) |

| Seasonal demand fluctuations | -0.8% | North America and Europe (winter sports, water sports) | Short term (≤2 years) |

| Risk of injuries associated with sports activities | -0.5% | Global; regulatory response strongest in North America | Medium term (2-4 years) |

| Availability of low-cost counterfeit products | -0.7% | Global; concentrated in e-commerce-heavy and developing markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High cost of premium sports equipment

The high cost of premium sports equipment serves as a significant restraint for the global sports equipment market. Advanced sporting goods and high-performance training products are often inaccessible to price-sensitive consumers due to their elevated prices. Equipment made with lightweight composites, smart tracking technologies, impact-resistant materials, and performance-enhancing features typically comes at a higher cost, limiting adoption among recreational users and amateur athletes. Additionally, consumers involved in multiple sports activities may incur substantial expenses for protective gear, accessories, footwear, and maintenance equipment, which can deter frequent product upgrades and replacements. Furthermore, the substantial initial investment required for advanced fitness machines, professional-grade sporting goods, and specialized adventure sports equipment restricts market penetration in cost-conscious consumer segments.

Seasonal demand fluctuations

Seasonal demand fluctuations present a notable challenge for the global sports equipment market, as the demand for various sporting products is significantly affected by weather conditions, tournament schedules, and seasonal recreational activities. Products related to winter sports, water sports, outdoor adventure activities, and certain field sports often experience irregular sales patterns throughout the year, resulting in periods of both high and low consumer demand. This reliance on seasonality can create difficulties in inventory management, lead to excess stock accumulation, and cause inconsistent revenue streams for manufacturers and retailers. Additionally, unfavorable weather conditions, shorter activity seasons, and shifts in consumer recreational preferences may reduce participation in specific sports activities, further impacting equipment sales during off-peak periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ball Sports Dominate, Water Sports Sets the Growth Pace

Ball sports accounted for 70.89% of market revenues in 2025, driven by widespread participation in organized and recreational sports activities that require consistent use of sporting equipment, accessories, and protective gear. This category benefits from strong engagement across schools, colleges, sports clubs, training academies, and professional competitions, ensuring stable year-round demand for equipment associated with field and court-based games. For example, according to the National Federation of State High School Associations (NFHS), over 921,000 high school students in the United States participated in basketball during 2024–25, underscoring the large-scale participation base supporting equipment demand. The growing emphasis on fitness, teamwork, athletic performance, and youth sports development continues to drive equipment consumption globally at both amateur and professional levels.

Water sports represent the fastest-growing segment in product categorization, with a projected CAGR of 7.56% through 2031. This growth is fueled by increasing global interest in recreational marine activities, adventure tourism, and outdoor fitness participation. Consumer preference for experiential leisure activities such as surfing, kayaking, paddleboarding, jet skiing, snorkeling, and scuba diving is significantly boosting demand for specialized sports equipment and safety gear. Additionally, growing awareness of physical wellness and active lifestyles has encouraged participation in water-based fitness and recreational activities across various age groups. The expansion of water sports training centers, coastal recreational facilities, and organized sporting events further drives demand for equipment such as boards, wetsuits, flotation devices, paddles, and protective accessories.

By End User: Male Segment Anchors Revenue, Female Participation Accelerates

Male consumers accounted for 66.87% of market revenues in 2025, primarily due to higher participation rates in organized sports, professional athletic competitions, gym-based fitness training, and outdoor recreational activities. Significant engagement in sports such as football, cricket, basketball, cycling, bodybuilding, combat sports, and adventure sports continues to drive demand for sporting goods, protective gear, training accessories, and fitness equipment. This segment benefits from frequent product replacement cycles linked to intensive training routines, competitive sports participation, and the use of performance-focused equipment. Additionally, the growing adoption of fitness-oriented lifestyles, strength training programs, and endurance sports has notably increased demand for technologically advanced and performance-enhancing sports equipment among male consumers.

The female segment is expected to grow at a CAGR of 8.34% during 2026–2031, fueled by rising participation in fitness activities, organized sports, recreational athletics, and outdoor adventure programs. Increased awareness of health, wellness, physical fitness, and active lifestyles has encouraged women to engage in activities such as running, yoga, cycling, gym training, swimming, tennis, and team sports. Enhanced support for women’s sports through school programs, professional leagues, fitness communities, and social campaigns is further driving demand for sports equipment, protective gear, and training accessories designed for female consumers. Moreover, improved access to sports facilities, fitness centers, and recreational programs is bolstering long-term participation trends across various age groups.

By Application: Household Use Dominates, Commercial Segment Outpaces

The personal and household application segment accounted for 88.91% of market revenues in 2025. This dominance is primarily attributed to the increasing adoption of sports, fitness, and recreational activities by individual consumers for health maintenance, physical fitness, and lifestyle enhancement. The growing preference for home-based workouts, participation in recreational sports, and personal fitness routines has significantly driven demand for sporting goods, exercise equipment, and training accessories tailored for non-commercial use. The segment benefits from the accessibility of fitness programs, digital workout platforms, and sports training content, which encourage consumers to engage independently in athletic and recreational activities. Key product categories contributing to this segment's dominance include fitness equipment, ball sports gear, cycling products, yoga accessories, and outdoor recreational equipment, supported by a high volume of direct consumer purchases.

The commercial segment is projected to grow at the fastest application rate of 7.12% through 2031. This growth is driven by the rapid expansion of gyms, fitness centers, sports academies, training facilities, recreational clubs, and institutional sports infrastructure. Increased investment in professional athletic training, wellness programs, and organized sports activities is fueling demand for durable, high-performance sports equipment in commercial establishments. Additionally, the rising consumer preference for structured fitness programs, professional coaching, and specialized training environments has prompted commercial facilities to upgrade and expand their equipment offerings. The growing popularity of group fitness classes, indoor sports complexes, and recreational activity centers further contributes to the increased procurement of sports and fitness equipment for commercial use.

By Distribution Channel: Physical Retail Retains Scale, Digital Channels Accelerate

Offline retail stores accounted for 69.31% of distribution in 2025, driven by strong consumer preference for physically evaluating sports equipment before purchase. This allows consumers to assess product quality, durability, comfort, size, grip, and performance suitability. The segment benefits from the widespread presence of specialty sports stores, brand outlets, department stores, and large-format retail chains, which offer extensive product assortments, expert guidance, and personalized customer assistance. Additionally, immediate product availability and after-sales support continue to reinforce consumer reliance on offline purchasing channels. The dominance of this segment is further supported by in-store demonstrations, professional fitting services, equipment customization, and direct interaction with trained sales personnel, enabling consumers to make informed purchasing decisions.

Online retail stores are forecast to grow at 9.11% through 2031, fueled by increasing consumer preference for convenient digital shopping platforms. These platforms provide extensive product variety, competitive pricing, and easy access to global sports equipment brands. The rapid expansion of e-commerce platforms, mobile shopping applications, and direct-to-consumer sales channels has significantly enhanced product accessibility for consumers seeking sports gear, fitness equipment, and training accessories. This segment is also benefiting from rising internet penetration, growing adoption of digital payment systems, and increased reliance on online product research, reviews, and comparisons before purchase. Furthermore, the availability of detailed product specifications, virtual demonstrations, personalized recommendations, and flexible return policies is boosting consumer confidence in online sports equipment purchases.

Geography Analysis

North America is projected to retain its position as the largest regional market with a 38.01% share in 2025. This dominance is attributed to the strong presence of an organized sports culture, widespread participation in both recreational and professional athletic activities, and high consumer engagement in fitness and outdoor sports. The region benefits from extensive sports infrastructure, including stadiums, gyms, training academies, fitness clubs, and educational athletic programs, which consistently drive demand for sporting goods and exercise equipment. Additionally, the strong adoption of technologically advanced fitness products, smart sports equipment, and high-performance training accessories further supports market growth. Increasing participation in school athletics, professional leagues, adventure sports, and home fitness activities continues to bolster equipment consumption across various categories.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 8.09% over the period 2026–2031. This growth is driven by rapidly increasing participation in sports and fitness activities, the expansion of urban recreational culture, and rising investments in sports infrastructure development. The growing popularity of gym memberships, outdoor sports, cycling, water sports, racquet sports, and fitness training among younger consumers is significantly boosting demand for sports equipment in the region. Government initiatives promoting physical fitness, school sports participation, and international sporting events are further encouraging equipment adoption. Additionally, the region is benefiting from the rapid growth of e-commerce platforms, improved accessibility to international sports brands, and rising consumer interest in health and wellness activities.

Europe continues to exhibit strong demand for winter sports equipment, cycling gear, football-related products, and fitness accessories, supported by its well-established sports culture and organized recreational infrastructure. For example, according to Sport England, approximately 298,500 people participated in winter sports activities in England in 2024, reflecting sustained engagement in specialized sports categories that drive equipment demand [3]Source: Sport England, "Number of people participating in winter sports in England ", sportengland.org. South America is witnessing increasing sports participation, driven by its strong football culture, community recreation activities, and expanding fitness awareness. Meanwhile, the Middle East and Africa region is benefiting from growing investments in sports facilities, wellness tourism, and large-scale sporting events, which are encouraging broader adoption of sports equipment and training products.

Competitive Landscape

The sports equipment market is fragmented, with numerous international, regional, and niche manufacturers competing across diverse product categories, athletic activities, and consumer segments. Major players in the market include adidas AG, Puma SE, Decathlon S.A., Amer Sports, Inc., and Mizuno Corporation. Market participants compete based on product innovation, technological integration, pricing strategies, brand visibility, distribution networks, product durability, and performance-enhancing features. The industry is characterized by continuous product launches, the expansion of sports-specific equipment portfolios, and growing investments in smart and connected fitness technologies to strengthen competitive positioning.

Companies are increasingly focusing on technological advancements and digital ecosystem partnerships to improve consumer engagement and enhance brand loyalty. The integration of wearable fitness technologies, smart sensors, AI-enabled training systems, and connected fitness platforms is becoming a key competitive strategy among manufacturers seeking to differentiate their product offerings. Additionally, partnerships with digital fitness applications, online coaching platforms, sports analytics providers, and e-commerce marketplaces are enabling companies to strengthen customer interaction and create personalized training experiences. The growing importance of omnichannel retail strategies, direct-to-consumer platforms, and digital marketing campaigns is also intensifying competition, as brands aim to improve accessibility, customer retention, and online sales performance.

Competitive intensity within the market is further increasing due to rising consumer demand for lightweight materials, sustainable manufacturing practices, ergonomic product designs, and performance-oriented sports equipment. Manufacturers are actively investing in research and development activities to introduce technologically advanced, environmentally sustainable, and sport-specific products that meet evolving consumer expectations. Strategic collaborations with professional athletes, sports leagues, fitness influencers, and recreational sports organizations continue to play a significant role in strengthening brand recognition and expanding global market reach.

Sports Equipment Industry Leaders

-

adidas AG

-

Puma SE

-

Decathlon S.A.

-

Mizuno Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Peloton launched its new Commercial Series Bike and Tread, designed specifically for high-traffic gym environments. This initiative signifies the company's entry into the commercial fitness market, combining Peloton's digital content with Precor's industrial-grade engineering.

- November 2025: Sena Technologies Inc. introduced the Latitude S2 Snow Communication Helmet. Designed for snow sports enthusiasts, the Latitude S2 integrates Mesh and Bluetooth technology with advanced comfort and safety features to enhance communication and performance on the slopes.

- September 2025: Decathlon introduced the 'Explore Series,' a new range of multi-purpose bicycles specifically designed for Indian riders and conditions. These bicycles are tailored to suit local riding styles and rider morphology, combining the touring comfort of a hybrid bike with the durability of a mountain bike.

Global Sports Equipment Market Report Scope

The sports equipment market is the global industry that manufactures and sells gear, apparel, and machinery used for physical exercise, recreation, and competitive sports. The sports equipment market is segmented by product type, end-user, application, distribution channel, and geography. Based on product type, the market is segmented into ball sports, cycling sports, racket sports, water sports, winter sports, and other sports types. Based on end-user, the market is segmented into male and female. Based on application, the market is segmented into personal/household and commercial. Based on distribution channel, the market is segmented into offline retail stores and online retail stores. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Ball Sports |

| Cycling Sports |

| Racket Sports |

| Water Sports |

| Winter Sports |

| Other Sports Type |

| Male |

| Female |

| Personal/Houesehold |

| Commercial |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Ball Sports | |

| Cycling Sports | ||

| Racket Sports | ||

| Water Sports | ||

| Winter Sports | ||

| Other Sports Type | ||

| By End-User | Male | |

| Female | ||

| By Application | Personal/Houesehold | |

| Commercial | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the global sports equipment market?

The global sports equipment market reached USD 358.09 billion in 2026 and is projected to rise to USD 500.82 billion by 2031 at a 6.9% CAGR.

Which product category leads worldwide demand?

Ball sports remained the largest product group with 70.89% of revenue in 2025, supported by the global scale of football, basketball, baseball, and newer growth areas such as pickleball.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region with an 8.09% CAGR over 2026-2031, supported by strong brand growth in Greater China and broader urban demand across the region.

Why are online channels growing faster than stores?

Online retail is forecast to grow at 9.11% through 2031 because brands are using direct digital channels for data, margin control, premium assortment, and customization, even though stores still lead overall share.

Page last updated on: