Golf Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

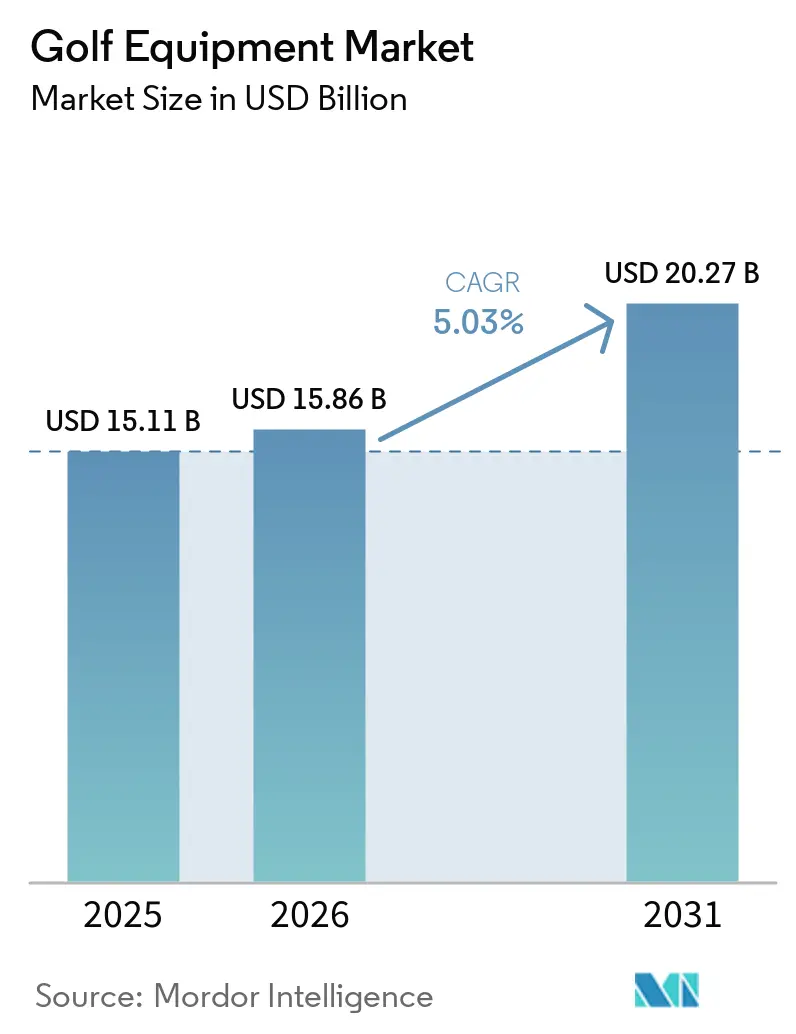

| Market Size (2026) | USD 15.86 Billion |

| Market Size (2031) | USD 20.27 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

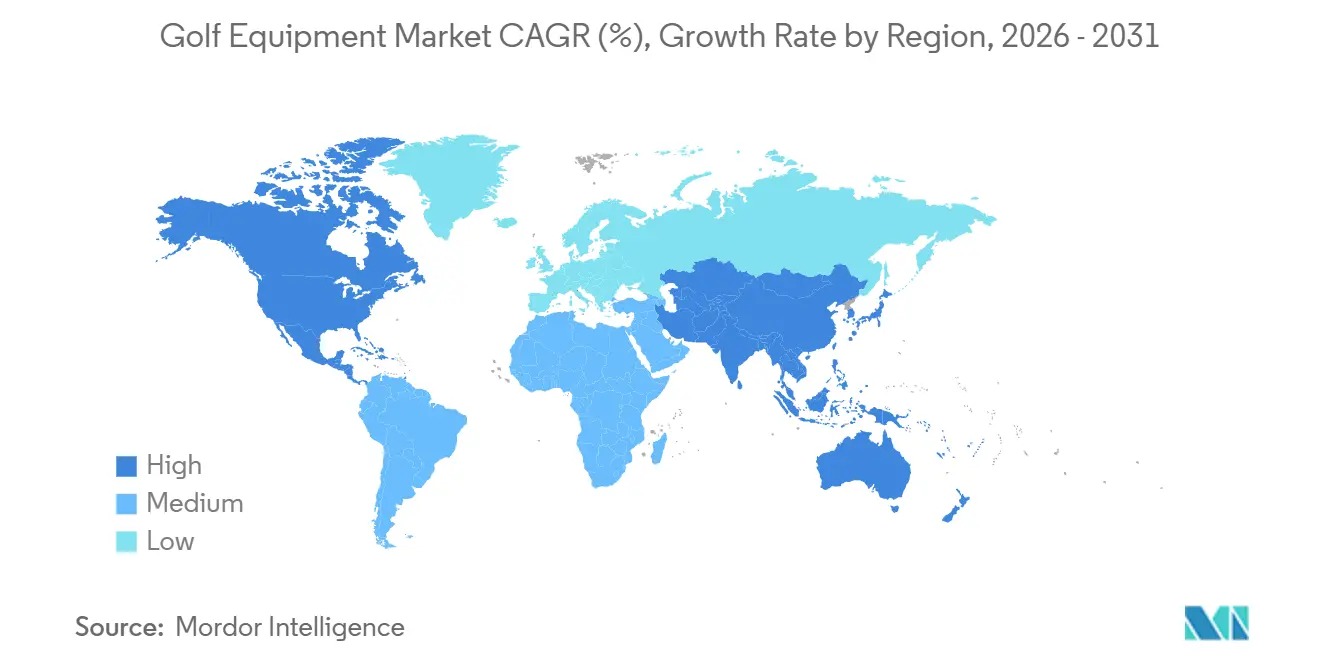

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

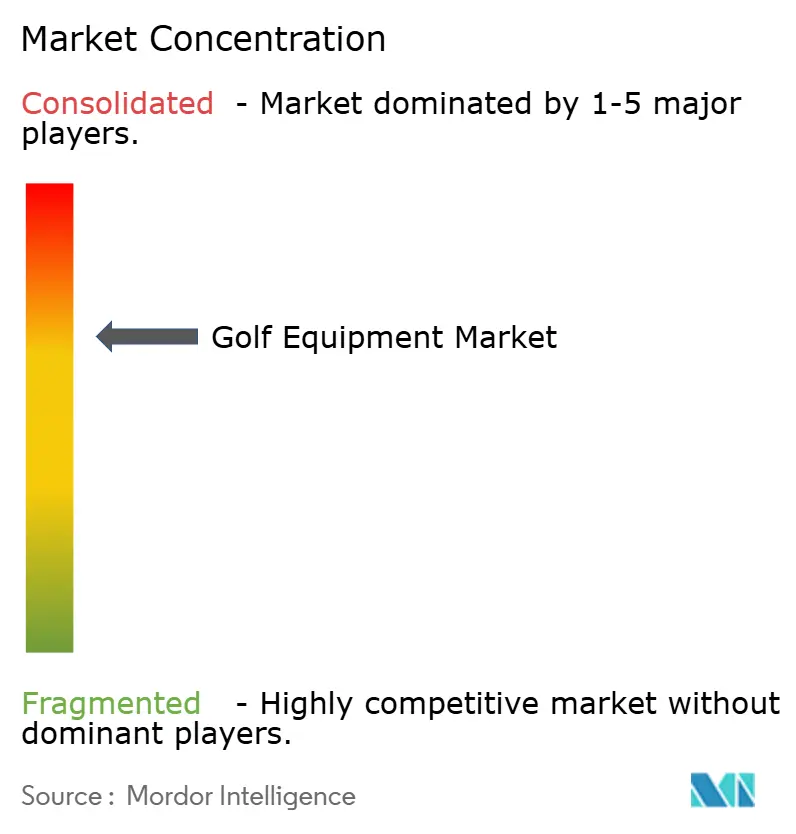

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Golf Equipment Market Analysis by Mordor Intelligence

The golf equipment market size is expected to grow from USD 15.11 billion in 2025 to USD 15.86 billion in 2026 and is forecast to reach USD 20.27 billion by 2031 at 5.03% CAGR over 2026-2031. The market growth is being supported by increasing participation in recreational and professional golf, rising demand for technologically advanced clubs and golf balls, and the growing popularity of golf tourism worldwide. Equipment manufacturers are focusing on product innovation, including lightweight materials, enhanced club designs, and performance-improving technologies to attract both amateur and experienced players. The expansion of golf facilities, driving ranges, and simulator-based golf experiences is further contributing to equipment sales. Additionally, growing interest among younger demographics and women golfers is broadening the consumer base, creating sustained demand across multiple golf equipment categories.

Key Report Takeaways

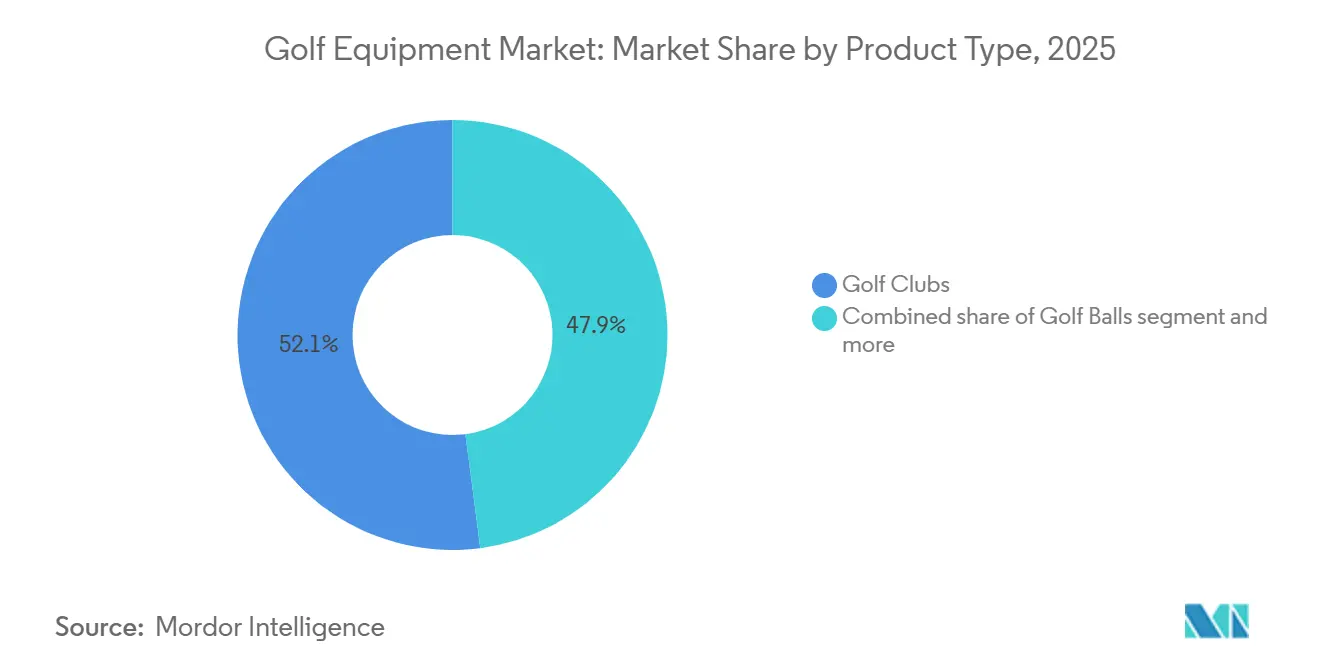

- By product type, golf clubs led with 52.06% revenue share in 2025, while golf balls are projected to expand at a 5.39% CAGR through 2031.

- By category, the mass segment held 63.89% share in 2025, while the premium segment is forecast to grow at a 5.61% CAGR through 2031.

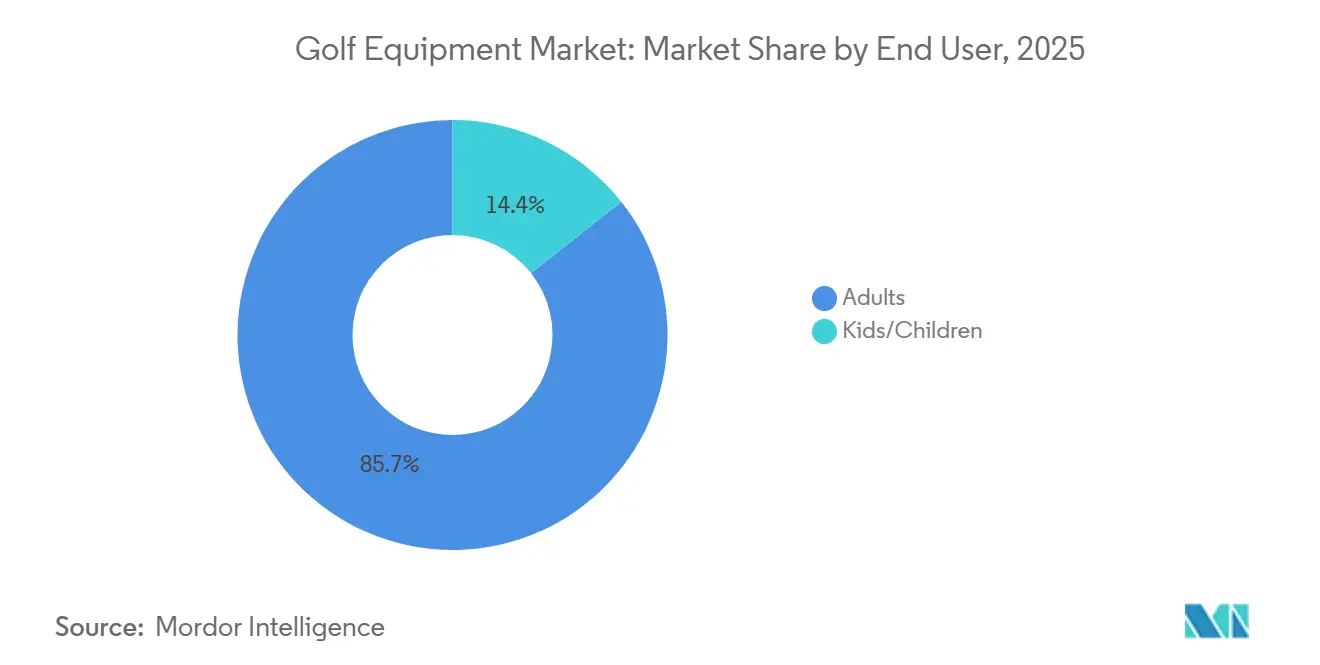

- By end user, adults accounted for 85.65% share in 2025, while kids and children are projected to grow at a 5.49% CAGR through 2031.

- By distribution channel, offline retail stores held 75.81% share in 2025, while online retail stores are expected to advance at a 6.14% CAGR through 2031.

- By geography, North America accounted for 47.68% of the golf equipment market size in 2025, while Asia-Pacific is projected to grow at a 5.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Golf Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing participation in golf across emerging markets | +1.2% | Global, strongest in Asia-Pacific, the Middle East, and Central and South America | Medium term (2-4 years) |

| Increasing investment in golf course development and expansion | +0.8% | Asia-Pacific core, with spillover to the Middle East and South America | Long term (≥ 4 years) |

| Rising demand for technologically advanced golf clubs | +0.9% | North America and Europe, with early uptake in Japan and South Korea | Short term (≤ 2 years) |

| Growing popularity of custom-fitted golf equipment | +0.6% | North America and Europe, with selective uptake in Japan and Australia | Medium term (2-4 years) |

| Expansion of indoor golf simulators driving equipment purchases | +0.5% | Asia-Pacific core, followed by North America and Europe | Medium term (2-4 years) |

| Increasing number of junior golf development programs | +0.4% | United States, United Kingdom, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing participation in golf across emerging markets

Increasing participation in previously smaller markets is driving growth in the golf equipment market. The Royal and Ancient Golf Club of St Andrews reported in its June 2026 update that 112.2 million adults and juniors actively played golf outside the U.S. and Mexico, reflecting an annual increase of 4.2 million players[1]Source: Asian Golf Industry Federation, “Sustained Increase in Golf’s Global Participation”, agif.asia. Junior participation experienced a 6% rise, reaching 47.1 million. This growth is crucial for the golf equipment market, as younger players often begin with affordable equipment and progress through multiple replacement cycles as their skills improve and their purchasing power increases. Asia recorded 26.2 million adult golfers, while Central and South America achieved an impressive 20% year-over-year growth in participation[2]Source: Asian Golf Industry Federation, “Sustained Increase in Golf’s Global Participation”, agif.asia. These developments highlight a shift in demand, which is no longer concentrated solely in traditional, mature golf economies. This diversification supports both entry-level sales and future trade-ups, strengthening the market's foundation for repeat purchases over the next several years.

Increasing investment in golf course development and expansion

Increasing investment in golf course development and expansion is a significant driver of the golf equipment market, as improved infrastructure enhances access to the sport and attracts new participants. Governments, private developers, and golf resort operators are investing in new courses, practice facilities, and technology-enabled golf venues to meet growing consumer interest. The expansion of golf infrastructure encourages higher participation rates, which directly increases demand for golf clubs, balls, bags, and related equipment. According to the National Golf Foundation, a record 48.1 million Americans aged 6 and above participated in golf activities in 2025, including 29.1 million on-course golfers and 19 million individuals engaged exclusively in off-course formats such as driving ranges, indoor simulators, and golf entertainment venues[3]Source: National Golf Federation, “Golf Industry Facts”, ngf.org. The growing popularity of these facilities creates more opportunities for equipment purchases by both new and experienced players. Additionally, investments in golf tourism destinations and premium golf resorts further stimulate equipment sales by encouraging frequent play and equipment upgrades.

Rising demand for technologically advanced golf clubs

Rising demand for technologically advanced golf clubs is a key driver of growth in the golf equipment market. Golfers are increasingly seeking clubs that enhance distance, accuracy, forgiveness, and overall performance, encouraging manufacturers to invest heavily in innovation. Advanced technologies such as artificial intelligence-assisted club design, adjustable weighting systems, carbon composite materials, and aerodynamic club heads are transforming the performance capabilities of modern golf clubs. These innovations help players of varying skill levels optimize their game, making premium and technologically sophisticated products more attractive. Equipment manufacturers are also offering personalized fitting solutions that enable golfers to customize clubs based on swing characteristics and playing style. Professional endorsements and product launches featuring cutting-edge technologies further accelerate consumer adoption.

Growing popularity of custom-fitted golf equipment

The growing popularity of custom-fitted golf equipment is emerging as a significant driver of the golf equipment market. Golfers are increasingly recognizing that clubs tailored to their swing speed, height, posture, and playing style can improve accuracy, distance, consistency, and overall performance. As a result, demand for personalized fitting services has increased across specialty golf retailers, pro shops, and dedicated fitting centers. Equipment manufacturers are investing in advanced fitting technologies, including launch monitors, swing analysis software, and data-driven customization tools, to provide more precise recommendations. Custom fitting also encourages consumers to purchase premium clubs and upgrade existing equipment, contributing to higher average selling prices. Professional golfers and coaches frequently advocate the benefits of fitted equipment, further increasing consumer awareness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium golf clubs and equipment | -0.5% | Global, strongest in price-sensitive emerging markets | Medium term (2-4 years) |

| Limited accessibility to golf courses in many regions | -0.3% | South America, Africa, the Middle East, and rural parts of mature markets | Long term (≥ 4 years) |

| High maintenance and storage requirements for equipment | -0.2% | Global, with stronger effect in dense urban markets in Asia | Short term (≤ 2 years) |

| Economic downturns reducing discretionary spending on golf gear | -0.6% | Global, with added sensitivity in debt-heavy consumer markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of premium golf clubs and equipment

The high cost of premium golf clubs and equipment remains a significant restraint on the growth of the golf equipment market. Advanced golf clubs incorporating technologies such as carbon composite materials, adjustable weighting systems, and custom-fitting features often carry premium price tags that can be prohibitive for many consumers. A complete set of high-end clubs, along with golf balls, bags, and accessories, represents a substantial financial investment, particularly for beginners and occasional players. This cost barrier can discourage new participants from entering the sport and limit equipment upgrades among budget-conscious golfers. The challenge is especially pronounced in emerging markets, where disposable incomes and golf participation rates are comparatively lower. Additionally, recurring expenses related to course fees, memberships, and lessons further increase the overall cost of engagement.

Limited accessibility to golf courses in many regions

Limited accessibility to golf courses in many regions remains a key restraint for the golf equipment market. Golf participation is heavily dependent on the availability of courses, driving ranges, and practice facilities, which are unevenly distributed across countries and regions. In many developing markets, the number of golf courses remains limited due to high land requirements, significant development costs, and competing land-use priorities. This lack of infrastructure restricts opportunities for individuals to learn and regularly participate in the sport, thereby reducing demand for golf equipment. Long travel distances to golf facilities and limited public access to private clubs can further discourage participation among potential players. The challenge is particularly evident in rural and emerging urban areas where golf infrastructure is underdeveloped. As a result, constrained access to playing facilities continues to limit player growth and slows the expansion of the golf equipment market in several regions worldwide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Golf Balls Drive Volume as Clubs Define Margin

Golf clubs represented the largest product segment in the golf equipment market, accounting for 52.06% of total revenue in 2025. The segment’s dominance is primarily attributed to the high average selling price of clubs compared to other equipment categories and the frequent introduction of technologically advanced products. Manufacturers continuously invest in innovations such as lightweight composite materials, adjustable club heads, enhanced aerodynamics, and custom-fitting solutions to improve player performance. Professional endorsements and equipment upgrades by both amateur and experienced golfers further support demand. The replacement cycle for drivers, irons, wedges, and putters also contributes significantly to recurring sales.

Golf balls are projected to be the fastest-growing product segment, expanding at a CAGR of 5.39% through 2031. Growth is driven by the consumable nature of golf balls, which require frequent replacement due to wear, loss, and regular usage. Rising participation in golf across both mature and emerging markets is increasing the volume of balls purchased by recreational and professional players alike. Manufacturers are introducing advanced ball technologies designed to improve spin control, distance, durability, and overall performance, encouraging product upgrades. The expansion of golf courses, driving ranges, and simulator-based golf activities is also contributing to higher consumption rates.

By Category: Premium Segment Gains Share as Mass Tier Sustains Scale

The mass category dominated the golf equipment market in 2025, accounting for 63.89% of total revenue. The segment's leadership is primarily driven by its broad accessibility and affordability, making golf equipment available to a larger base of recreational and entry-level golfers. Mass-market products are widely distributed through sporting goods retailers, specialty golf stores, and online platforms, ensuring strong market penetration across developed and emerging regions. Manufacturers continue to focus on offering reliable performance, durability, and value-oriented pricing to attract cost-conscious consumers. The growing popularity of golf as a recreational activity has further expanded demand for equipment within this category.

The premium category is anticipated to be the fastest-growing segment, registering a CAGR of 5.61% through 2031. Growth is being driven by increasing consumer willingness to invest in high-performance equipment featuring advanced materials, precision engineering, and customized fitting options. Experienced golfers and enthusiasts are increasingly seeking premium clubs, balls, and accessories designed to enhance distance, accuracy, and overall gameplay. Leading manufacturers are continuously introducing technologically sophisticated products that command higher price points and appeal to performance-focused consumers. The expansion of golf tourism, rising disposable incomes, and growing participation among affluent demographics are also supporting demand for premium equipment.

By End User: Kids and Juniors Represent a Long-Dated Revenue Pipeline

Adults represented the largest end-user segment in the golf equipment market, accounting for 85.65% of total revenue in 2025. The segment’s dominance is driven by the substantial participation of adult recreational golfers, club members, and professional players across major golfing regions. Adults typically have greater purchasing power and are more likely to invest in premium clubs, golf balls, bags, and accessories to enhance their performance. The popularity of golf as a leisure, networking, and competitive sport among working professionals further contributes to strong equipment demand. In addition, frequent equipment upgrades, custom fitting services, and increasing participation in golf tourism support sustained spending within this demographic.

The kids and children segment is projected to be the fastest-growing end-user category, registering a CAGR of 5.49% through 2031. Growth is being supported by rising efforts from golf associations, schools, and sports organizations to introduce the sport to younger age groups. Junior golf development programs, youth tournaments, and beginner-focused training initiatives are increasing participation among children worldwide. Equipment manufacturers are also expanding their portfolios with lightweight clubs, junior golf sets, and age-specific products designed to improve accessibility and enjoyment for young players. Parents are increasingly encouraging participation in golf due to its physical, social, and developmental benefits, further boosting demand for youth equipment.

By Distribution Channel: Online Retail Disrupts the Fitting-First Model

Offline retail stores accounted for the largest share of the golf equipment market in 2025, representing 75.81% of total revenue. The segment’s dominance is largely attributed to consumers’ preference for physically evaluating golf clubs, balls, bags, and accessories before making a purchase. Specialty golf stores, sporting goods retailers, and pro shops provide customers with access to expert guidance, club-fitting services, and product demonstrations that enhance purchasing confidence. Many golfers prefer in-store experiences to assess factors such as club weight, grip comfort, and overall product feel. Established retail networks and strong relationships between manufacturers and golf retailers further support the segment’s leadership position.

Online retail stores are expected to be the fastest-growing distribution channel, advancing at a CAGR of 6.14% through 2031. Growth is being driven by increasing digital adoption, expanding e-commerce infrastructure, and the convenience of purchasing golf equipment from home. Online platforms provide consumers with access to a wider range of products, competitive pricing, customer reviews, and direct-to-consumer offerings from leading manufacturers. The growing use of digital fitting technologies and virtual consultation services is also helping reduce barriers to online equipment purchases. In addition, smartphone penetration and improved logistics networks are enabling faster and more efficient product delivery across key markets.

Geography Analysis

North America dominated the golf equipment market in 2025, accounting for 47.68% of global revenue. The region benefits from a well-established golfing culture, a large base of recreational and professional players, and extensive golf course infrastructure. The United States remains the largest contributor, supported by strong consumer spending on premium golf clubs, balls, and accessories. High participation rates across various age groups, combined with widespread adoption of custom-fitting services and advanced equipment technologies, continue to drive demand. The presence of leading equipment manufacturers and strong retail distribution networks further reinforces the region’s leadership position. Additionally, growing interest in simulator golf and year-round training facilities supports sustained equipment sales across North America.

Asia-Pacific is projected to be the fastest-growing regional market, registering a CAGR of 5.39% through 2031. Growth is being fueled by rising disposable incomes, expanding middle-class populations, and increasing participation in golf across countries such as Japan, South Korea, China, and Australia. Governments and private investors are supporting the development of golf courses, resorts, and training facilities, improving access to the sport. Younger consumers are increasingly engaging with golf through technology-enabled experiences, including indoor simulators and driving ranges. The growing popularity of golf tourism and international tournaments is also enhancing awareness and equipment demand. As a result, manufacturers are strengthening their presence in the region through localized product offerings and distribution partnerships.

Europe, South America, and the Middle East and Africa collectively represent important growth opportunities within the golf equipment market. Europe benefits from a mature golfing tradition, particularly in the United Kingdom, Germany, Spain, and Scandinavia, where participation rates remain stable and demand for premium equipment remains strong. South America is witnessing gradual growth, supported by increasing golf tourism and rising interest in the sport among affluent consumers. In the Middle East and Africa, investments in luxury golf resorts, international tournaments, and tourism-focused developments are contributing to market expansion. Countries such as the United Arab Emirates and South Africa continue to attract both local and international golfers.

Competitive Landscape

The golf equipment market exhibits a moderately concentrated competitive structure, with a limited number of established manufacturers accounting for a significant share of global revenues. Leading companies such as The Callaway Golf Company, Acushnet Holdings Corp., and TaylorMade Golf Company, Inc. maintain strong market positions through extensive product portfolios, global distribution networks, and continuous investment in research and development. These companies benefit from high brand recognition among both professional and recreational golfers, enabling them to sustain premium pricing and customer loyalty. Their longstanding relationships with golf retailers, courses, and professional tours further strengthen their competitive advantage across key regional markets.

Competition in the market is primarily driven by technological innovation, product performance, and brand endorsement strategies. Manufacturers continuously introduce advanced club designs, high-performance golf balls, and custom-fitting solutions to improve distance, accuracy, forgiveness, and overall player experience. Partnerships with professional golfers and sponsorship of major tournaments remain important marketing tools for enhancing brand visibility and consumer trust. Companies are also leveraging digital fitting technologies, simulation platforms, and direct-to-consumer sales channels to expand customer engagement and differentiate their offerings in an increasingly competitive environment.

Despite the dominance of major brands, the market continues to witness competition from specialized and emerging equipment manufacturers targeting niche customer segments. Companies focusing on premium handcrafted clubs, training aids, putters, and customized equipment are gaining traction among enthusiasts seeking personalized performance solutions. Regional players are also strengthening their presence through localized distribution strategies and competitive pricing. As participation in golf expands across emerging markets and younger demographics, manufacturers are expected to intensify investments in innovation, sustainability initiatives, and product diversification to capture additional market share and maintain long-term growth.

Golf Equipment Industry Leaders

The Callaway Golf Company

Acushnet Holdings Corp.

Sumitomo Rubber Industries, Ltd.

Taylor Made Golf Company, Inc.

Mizuno Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Acushnet's Scotty Cameron brand expanded its 2026 Phantom lineup with the launch of the Phantom 3.2 and Phantom 12 putter models. Both mid-mallet and high-MOI designs had been validated on professional tours in prototype form before their consumer release.

- June 2026: HONMA and Bugatti unveiled a limited-edition golf equipment collection, the HONMA × BUGATTI: Icons. This collection marries HONMA’s precision club-making with Bugatti’s luxury performance and design. Developed from a mutual dedication to craftsmanship and engineering excellence, the collection offers three product lines: the BERES Super Premium Collection, Tour World Premium Collection, and the Super Premium Bugatti Putter.

- January 2026: Titleist rolled out its new AVX golf ball, boasting a revamped three-piece construction. This design enhances short-game control while retaining the AVX franchise's hallmark features: low long-game spin, impressive distance, and a soft feel. The revamped model features a softer urethane cover for heightened greenside spin, a quicker core formulation for consistent ball speed and distance, and a newly engineered high-flex casing layer to fine-tune spin performance across all clubs.

Global Golf Equipment Market Report Scope

The golf equipment comprises the production, distribution, and sale of products specifically designed for playing and practicing golf. The golf equipment market is segmented by product type, category, end user, distribution channel, and geography. Based on the product type, the market is segmented into golf clubs, golf balls, and golf bags and accessories. Based on category, the market is segmented into mass and premium. Based on end user, the market is segmented into adults, and kids/children. Based on the distribution channel, the market is segmented into offline and online retail stores. The market also covers the global-level analysis of major regions, such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts were made based on value (USD million).

| Golf Clubs |

| Golf Balls |

| Golf Bags and Accessories |

| Mass |

| Premium |

| Adults |

| Kids/Children |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Sweden | |

| Ireland | |

| Austria | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| New Zealand | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Golf Clubs | |

| Golf Balls | ||

| Golf Bags and Accessories | ||

| By Category | Mass | |

| Premium | ||

| By End User | Adults | |

| Kids/Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Sweden | ||

| Ireland | ||

| Austria | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| New Zealand | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value forecast for golf equipment?

The golf equipment market is forecast to reach USD 20.27 billion by 2031, rising from USD 15.86 billion in 2026 at a 5.03% CAGR over 2026-2031.

Which product segment leads current revenue in golf equipment?

Golf clubs held 52.06% of revenue in 2025, making them the largest product segment because of their higher selling prices and strong upgrade cycle.

Which product segment is growing the fastest through 2031?

Golf balls are projected to grow at a 5.39% CAGR through 2031, helped by repeat purchases and rising participation among beginners and juniors.

Why is Asia-Pacific important for future growth?

Asia-Pacific is the fastest-growing region at a 5.39% CAGR, supported by rising player numbers and major golf infrastructure projects in markets such as China and Vietnam.

What is driving premium equipment demand?

Premium demand is being lifted by material innovation, fitting-led purchases, and connected performance tools that make upgrade decisions easier to justify.

Page last updated on: