Golf Shoes Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

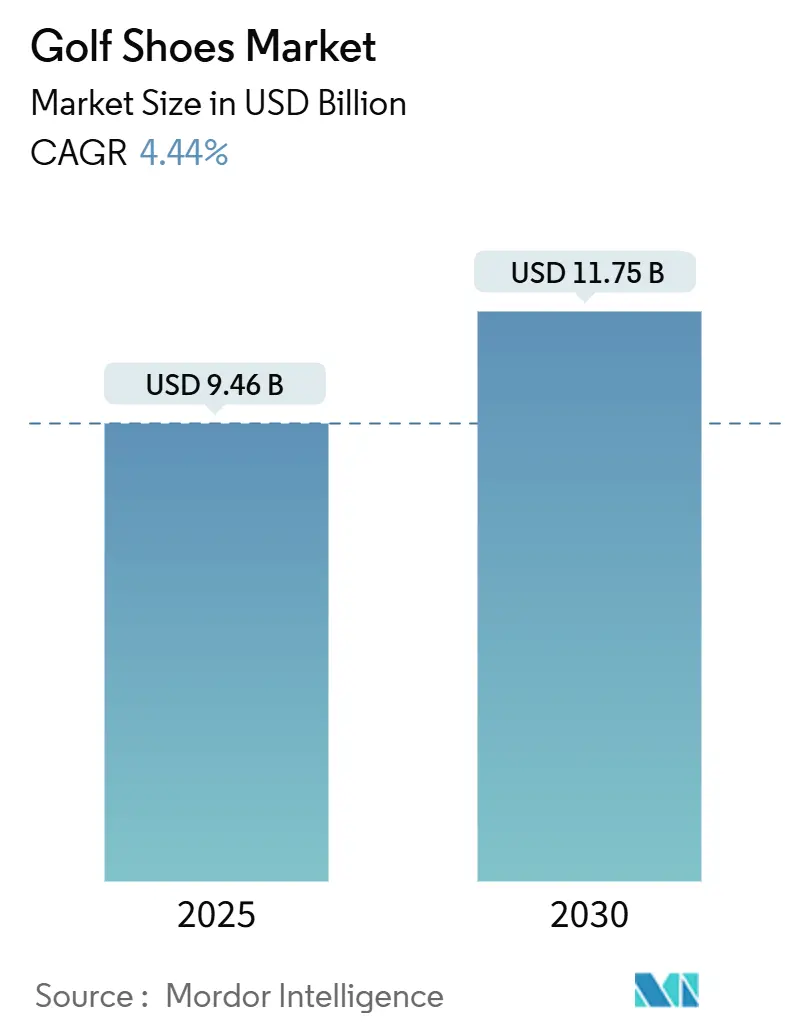

| Market Size (2025) | USD 9.46 Billion |

| Market Size (2030) | USD 11.75 Billion |

| Growth Rate (2025 - 2030) | 4.44% CAGR |

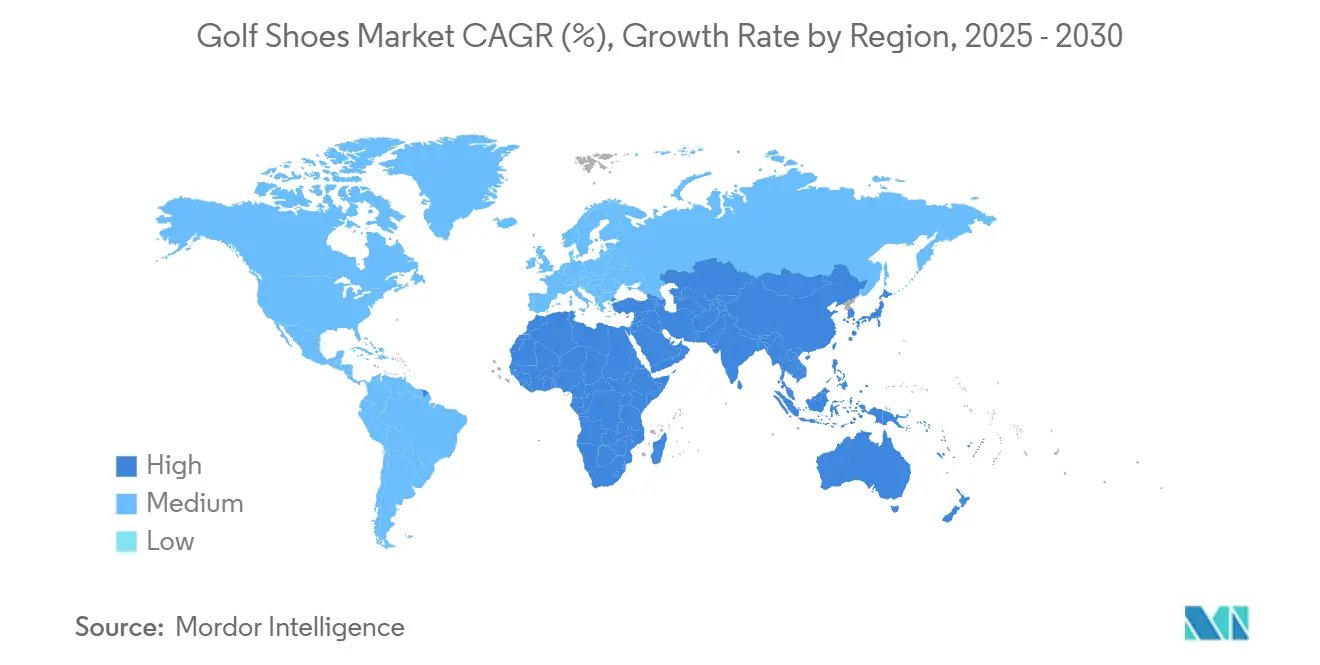

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Golf Shoes Market Analysis by Mordor Intelligence

The golf shoes market size stands at USD 9.46 billion in 2025 and is forecast to reach USD 11.75 billion by 2030, advancing at a 4.44% CAGR. Global participation is surging, athletic performance is blending with lifestyle aesthetics, and rapid innovations in lightweight waterproof materials are driving this expansion. North America's 45 million players bolster current demand, providing a stable foundation for market growth[1]Source: PGA of America,"By the Numbers: Golf in 2024", www.pga.com. Meanwhile, Asia-Pacific's burgeoning middle class, coupled with the increasing popularity of golf as a recreational activity, fuels the most pronounced growth in the market. The rise of spikeless designs, which offer enhanced comfort and versatility, upgrades to premium categories that cater to high-end consumers, and omni-channel retail strategies that integrate online and offline sales channels, enhance revenue prospects for brands catering to both recreational and performance-focused golfers. While competitive intensity is moderate, it allows established athletic giants and emerging specialists to carve out distinctions in sustainability initiatives, advanced fit systems tailored to individual needs, and endorsement portfolios featuring prominent athletes and influencers.

Key Report Takeaways

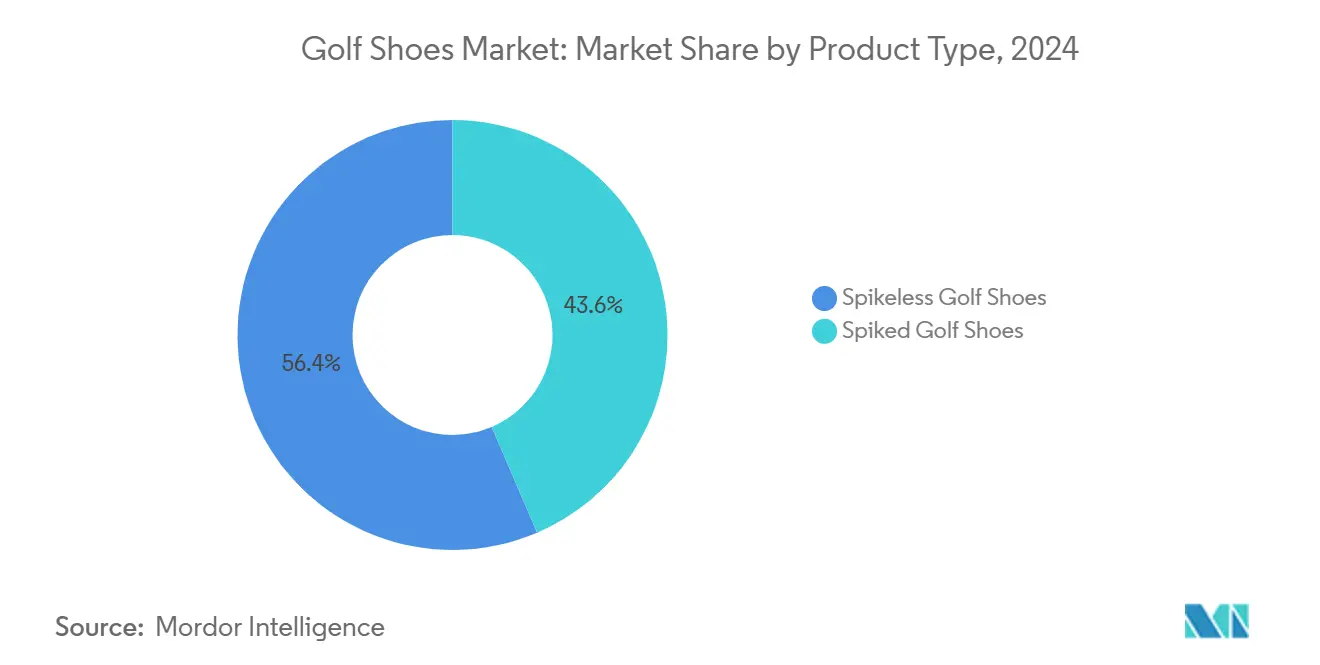

- By product type, spikeless footwear led with 56.44% revenue share in 2024, while spiked footwear is projected to expand at a 5.23% CAGR between 2025-2030.

- By end user, men accounted for 72.64% of the 2024 base, yet women are forecast to grow at a 5.93% CAGR through 2030.

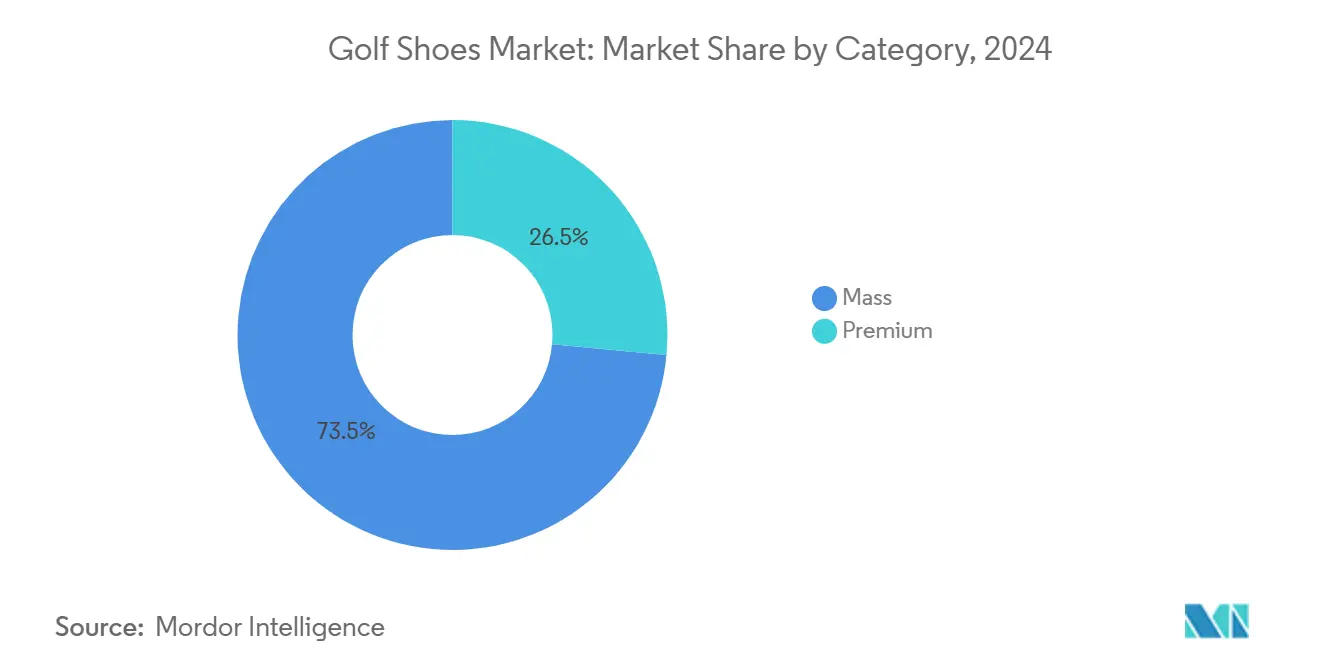

- By category, mass-market lines held 73.51% of the 2024 value, whereas premium lines are set to compound at a 4.93% CAGR in the out-years.

- By distribution channel, offline stores captured 60.84% share in 2024; online channels are on track for a 5.48% CAGR across the forecast.

- By geography, North America held 49.17% in 2024, while Asia-Pacific is positioned to deliver the fastest 5.78% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Golf Shoes Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global participation in golf | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Shift toward athleisure and spikeless footwear | +0.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Technological advances in lightweight waterproof materials | +0.7% | Global | Long term (≥ 4 years) |

| Liberalization of golf-course dress codes | +0.5% | North America, Europe | Medium term (2-4 years) |

| Corporate wellness programs adopting golf events | +0.4% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of 9-hole urban golf formats | +0.3% | Urban centers worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising global participation in golf

In 2023, research and development-affiliated countries saw a historic surge in on-course golfers, rising by 3.1 million to reach a total of 42.7 million. This growth reflects the increasing popularity of golf as a recreational activity and its appeal to a broader audience. In 2024, the United States Golf Association reported an 8% increase in 9-hole rounds compared to the previous year, indicating a trend of deeper engagement and repeat participation among golfers. Since 2020, women and girls have made up 63% of the newly added golfers, significantly shifting the demographic landscape and highlighting the sport's growing inclusivity[2]Source: United States Golf Association,"Golf Scorecard Provides a 2024 Snapshot of the Recreational Game", www.usga.org. Furthermore, corporate wellness initiatives, often spotlighting tournament days, are accelerating footwear replacement cycles among professionals, as these events encourage active participation and frequent use of golf equipment. As this consumer base broadens, there's a pronounced demand for golf shoes that seamlessly blend recreational comfort with stability during swings, underscoring the growing fusion of sport and athleisure. This trend reflects the evolving preferences of modern golfers who seek performance-oriented yet stylish footwear that caters to both functionality and lifestyle needs.

Shift toward athleisure and spikeless footwear

As users increasingly prefer footwear that transitions seamlessly from the fairway to daily life, the versatility of athleisure has driven a surge in spikeless adoption. In 2024, spikeless designs accounted for a notable 56.44% of the total volume, highlighting their growing dominance in the market. A prime example of this trend is Jordan Brand’s Air Rev model, which combines Flight Lock containment with a flexible Air Zoom unit, ensuring on-course torque control while maintaining urban style elements. This design not only caters to performance needs but also aligns with the evolving consumer preference for multi-functional footwear. Recent dress-code updates endorsing "recognized golf attire" have further supported the adoption of lifestyle silhouettes that meet the standards of private clubs, bridging the gap between traditional golf norms and modern fashion trends. Given the ongoing blend of sporty functionality with casual aesthetics, spikeless formats are poised to remain at the forefront throughout the forecast period, driven by their ability to cater to both performance and lifestyle demands.

Technological advances in lightweight waterproof materials

Material research and development drives growth in the premium segment. ECCO Golf's BIOM H5 combines recycled-content uppers with FLUIDFORM direct-comfort tooling, ensuring a watertight construction without the use of adhesives. This innovation not only enhances durability but also reduces the environmental impact by minimizing the use of synthetic materials and adhesives. ASICS' GEL-KAYANO ACE 2 utilizes FlyteFoam for shock absorption and features tailored flex grooves that enhance energy return during swings. The FlyteFoam technology, made from organic fibers, provides a lightweight yet resilient cushioning system, while the flex grooves are designed to optimize rotational movement, improving performance and comfort. These advancements address consumer preferences for lightweight, weather-resistant footwear that performs well in variable conditions. Additionally, they align with the increasing demand for sustainable practices in mature markets, where stricter environmental expectations are shaping product development strategies. By integrating cutting-edge material technologies with eco-conscious design, these brands are setting new benchmarks in the premium footwear market.

Liberalization of golf-course dress codes

Clubs in North America and Europe have revised their dress codes to attract a wider audience and reduce barriers to participation. By adopting a performance-oriented approach to attire guidelines, clubs are now embracing more athletic styles, such as streamlined silhouettes, moisture-wicking fabrics, and designs that prioritize mobility and comfort. This shift has created opportunities for mainstream sportswear brands to market lifestyle icons that combine style and functionality, featuring outsoles specifically designed to protect greens while ensuring durability, grip, and performance. By making the dress code feel less exclusive, clubs are experiencing an increase in participation, particularly among younger demographics, casual players, and those previously deterred by traditional attire norms. These new entrants are driving demand for footwear that not only reflects their style but also complies with course requirements, effectively merging fashion, performance, and practicality. Additionally, this evolution in dress codes aligns with broader trends in the sportswear market, where versatility and inclusivity are becoming key drivers of consumer preferences, further encouraging innovation in golf apparel and footwear.

Restraints Impact Analysis of Golf Shoes Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality and weather dependence | -0.8% | Temperate regions | Short term (≤ 2 years) |

| High average selling price | -0.6% | Price-sensitive and emerging economies | Medium term (2-4 years) |

| Sustainability scrutiny of synthetic materials | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Supply-chain disruption for specialty cleats | -0.3% | Asia manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Seasonality and weather dependence

In northern climates, about 94.5% of rounds take place in recreational settings, often at the mercy of unpredictable weather[3]Source: United States Golf Association,"Golf Scorecard Provides a 2024 Snapshot of the Recreational Game", www.usga.org. This volatility compresses play into the spring-summer months, creating a highly seasonal demand pattern. As a result, retailers face challenges in managing sharp inventory peaks and implementing discounts, which can significantly erode profit margins during less-than-ideal summers. Additionally, storms and heat events, which are becoming more frequent and severe due to climate change, further exacerbate this unpredictability. These weather-related disruptions not only impact the timing and frequency of play but also influence consumer purchasing behavior, as players may delay or avoid buying equipment and apparel during uncertain conditions. While covered ranges and simulators provide some relief by offering alternative play options, they cannot fully offset the dependency on outdoor conditions. Consequently, sales of full-price shoes remain closely tied to favorable weather, limiting overall demand during seasons affected by adverse conditions and creating additional challenges for retailers in maintaining consistent revenue streams.

High average selling price

Golf shoes, typically priced above USD 150, incorporate features like waterproof membranes, advanced cleat systems, and swing-stability engineering, which contribute to their premium pricing. For example, ASICS’ GEL-KAYANO ACE 2 is priced at USD 169.99, reflecting the inclusion of such advanced technologies. These high price points are particularly challenging in developing markets, where income elasticity is higher, and inflationary pressures on discretionary spending further exacerbate the issue. Newcomers and casual players in these regions often prioritize affordability over premium features, limiting their willingness to invest in high-priced golf shoes. To address this, brands have introduced entry-level SKUs and bundle promotions aimed at attracting price-sensitive buyers. However, these measures have only partially mitigated the issue, as the high average selling prices (ASPs) continue to act as a structural barrier. This persistent challenge significantly restricts volume growth in the market, particularly in regions where affordability is a key factor influencing consumer behavior.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Golf Shoes Market Segment Analysis

By Product Type:

Versatile Spikeless Footwear Heads Revenue While Spiked Lines Drive Performance GrowthIn 2024, spikeless golf shoes dominate the market, capturing about 56.44% of market share. This trend highlights a pronounced consumer inclination towards footwear that effortlessly shifts from the golf course to urban locales, all while maintaining traction. Players with a lifestyle focus are particularly drawn to spikeless designs, valuing their blend of versatility, style, and performance. Premium spikeless offerings boast cutting-edge multi-density outsoles, mimicking the grip of traditional spikes on dry turf, and are paired with EVA or PU midsoles for enhanced comfort. Furthermore, manufacturers are crafting resilient nubs, designed to withstand the rigors of avid golfers, effectively bridging the traction gap between spikeless shoes and their cleated counterparts. Consequently, the spikeless segment appeals to those prioritizing both functionality and lifestyle in their golf footwear.

Conversely, spiked golf shoes are the market's fastest-growing segment, with projections indicating a 5.23% compound annual growth rate through 2030. Competitive athletes and tour professionals remain loyal to cleated designs, drawn by their superior traction and ground reaction force across diverse course conditions. Today's cleated shoes boast advancements like lighter chassis, replaceable low-profile spikes, and hybrid lug layouts, all designed to reduce turf damage and enhance performance. To navigate market challenges and appeal to a broader audience, brands are rolling out convertible footwear with twist-in cleats. This innovation lets golfers toggle between spiked and spikeless configurations, adapting to course demands or weather changes. Such a versatile product strategy not only appeals to a diverse range of players but also cultivates brand loyalty as golfers evolve in their preferences and skills. The rising popularity of the spiked segment underscores a sustained demand for specialized features among dedicated golfers.

By End User:

Female Participation Catalyzes New Design ImperativesIn 2024, men command a significant 72.64% share of the golf shoe market, underscoring the sport's historical male-centric participation and buying habits. The men's segment boasts a diverse array of styles, technologies, and performance features, catering to varying skill levels and preferences. Leading brands are prioritizing innovations that bolster fit, durability, and specialized features like traction and comfort, addressing the needs of both serious and casual male golfers. While men maintain a stronghold in the market, evolving social and sporting dynamics are nudging brands towards inclusivity. This includes offering broader sizing and a wider range of colors to resonate with changing consumer preferences. To retain dominance, brands must harmonize traditional performance attributes with subtle innovations that appeal to a diverse male golfer demographic.

On the other hand, the women's segment is emerging as the fastest-growing sector in golf shoe consumption, with projections indicating a robust 5.93% CAGR. This surge can be attributed to the rising prominence of elite female golfers and focused initiatives aimed at nurturing young talent for sustained engagement. Today's product development delves deeper than mere aesthetic tweaks; considerations like accommodating wider forefeet, lower insteps, and a richer color spectrum underscore a commitment to designs that genuinely cater to female biomechanics. Brands are harnessing female foot-scan data to craft lasts that not only enhance comfort but also minimize break-in durations, marking a pivot towards authentic performance-driven solutions over mere cosmetic adjustments. Meanwhile, while children's footwear occupies a smaller niche, it showcases notable growth as families increasingly embrace golf as a collective outdoor pursuit. Junior shoe lines are now integrating advanced adult features, such as waterproof knit uppers and BOA® dial closures, to cultivate early brand allegiance. With extended sizing options and the incorporation of golf into educational and community programs, there's a consistent demand for budget-friendly junior shoes, setting the stage for continued volume growth.

By Category:

Premium Innovation Trickle-Down Supports Mass-Market BreadthIn 2024, value-tier golf shoes command the market, raking in a notable 73.51% of total revenue. Their popularity stems from attracting first-time buyers and casual players who prioritize affordability and reliability. Brands are leveraging modular tooling for swift color updates, sidestepping hefty research and development expenses. Additionally, promotional pricing during major golf tournaments and bundled starter kits, complete with accessories like gloves and spikes, boost accessibility, drawing in new players. These mass-market portfolios are vital for maintaining a broad market presence, especially in economically uncertain times. Consequently, value-tier models are instrumental in both introducing and retaining new golfers, striking a balance between cost and quality.

Conversely, premium golf shoes are on the fast track, boasting a projected compound annual growth rate of 4.93%. This surge is fueled by consumers increasingly willing to invest in biomechanically optimized designs as they transition to regular players. Premium shoes boast next-gen features like recycled midsoles, solvent-free bonding, and bio-based textiles, elevating both performance and sustainability. Such eco-friendly advancements not only bolster brand narratives but also rationalize premium pricing in mature, eco-conscious markets. The premium tier acts as a testing ground for cutting-edge technologies, which often find their way into mass-market lines. Overall, the premium segment's growth underscores a consumer trend prioritizing durability, performance, and environmental consciousness in golf footwear.

By Distribution Channel:

Omni-Channel Execution Becomes Table StakesIn 2024, brick-and-mortar retail commands a dominant 60.84% share of the golf footwear market. This stronghold is primarily attributed to the pivotal role of fit validation in purchasing technical golf shoes. Consumers prioritize confidence in their choices, a sentiment bolstered by specialty golf retailers and major sporting goods stores. These outlets offer services like gait analysis and expert in-person fittings, guiding players to the most comfortable and performance-enhanced footwear. The tactile experience of trying on shoes, gauging comfort, and receiving tailored advice is a unique advantage of physical stores. Moreover, these outlets ensure instant product availability, a boon for last-minute weekend purchases. Retailers are also adopting hybrid strategies, such as click-and-collect, merging the convenience of online shopping with the tactile benefits of in-store experiences.

On the flip side, online sales are the market's fastest-growing segment, boasting a 5.48% compound annual growth rate. As digital capabilities advance, features like enhanced product visualizations, interactive size-and-fit quizzes, and lenient return policies are alleviating purchase hesitations. Direct-to-consumer (DTC) platforms are not just selling; they're building loyalty through programs and exclusive product drops. The click-and-collect model bridges the gap between online and offline shopping, letting consumers check stock online and conveniently pick up items before heading to the store. Innovative partnerships, such as Golf Genius’ MyShop, are weaving e-commerce into pro-shop ecosystems, extending sales opportunities beyond traditional hours. As consumer demand for seamless shopping experiences grows, brands are harmonizing inventory visibility, pricing, and marketing across platforms, reducing conflicts and enhancing customer loyalty.

Geography Analysis

North America Golf Shoes Market

North America, with a commanding 49.17% share, underscores its deep-rooted golf culture and significant spending power. The U.S. alone drives a staggering USD 101.7 billion in golf-related economic activity, fueling brisk shoe replacement cycles and a dynamic retail landscape. This robust economic contribution is supported by a well-established network of golf courses, retail outlets, and training facilities, which cater to both professional and amateur players. To capture the attention of both veteran and novice players, manufacturers strategically leverage athlete endorsements and sponsor college golf events, ensuring sustained brand visibility and consumer engagement.

APAC Golf Shoes Market

Asia-Pacific emerges as the fastest-growing region, boasting a 5.78% CAGR. This surge is fueled by rising disposable incomes and a notable shift from screen time to outdoor activities. South Korea's impressive jump in participation from 2% to 34% over three decades highlights the region's vibrancy and growing interest in golf as a recreational activity. Meanwhile, China and India stand poised for growth, provided their infrastructure keeps pace. China's increasing investment in golf courses and training facilities, coupled with India's burgeoning local manufacturing hubs, not only reduces lead times but also buffers against freight volatility. These developments position the region as a key player for both volume and margin growth, with significant opportunities for market penetration and product diversification.

EMEA and South America Golf Shoes Market

Europe experiences steady, albeit slower, growth, largely driven by eco-conscious consumers emphasizing circular-economy principles. Scandinavian countries spearhead the movement, championing recycled-content designs and pushing brands to authenticate their supply chains. The region's focus on sustainability has led to innovations in product design and material sourcing, encouraging brands to adopt environmentally friendly practices. In South America and the Middle East, and Africa, burgeoning golf tourism and the development of resort courses hint at untapped potential. While currency fluctuations and sparse retail presence pose challenges, partnerships between brands and hospitality entities signal a promising, gradual expansion. These collaborations aim to enhance the golfing experience for tourists and locals alike, fostering long-term growth in these emerging markets.

Competitive Landscape

The global golf shoes market exhibits moderate concentration. Legacy specialists like FootJoy, with their long-standing tour validation and bespoke fitting services, safeguard their core franchises. Meanwhile, athletic giants Nike, Adidas, and Puma introduce innovations, think knit uppers and energy-return foams, across categories. Their expansive marketing boosts awareness of new products, broadening the market for both entry-level and premium golf shoes.

Emerging players like PAYNTR Golf, leveraging biomechanics research, design outsoles that enhance vertical ground force. They've secured shelf space through collaborations with Dick’s Sporting Goods and Golf Galaxy. Brands prioritizing sustainability attract eco-conscious consumers with transparent supply chains. At the same time, luxury brands are crafting limited-run leather designs, appealing to the fashion-savvy golfer.

Research and development focus on personalized fits, with innovations like BOA® dials and heat-moldable inserts gaining popularity. Strategic investments, such as L. Catterton acquiring a majority stake in L.A.B. Golf, highlight the market's appetite for performance niches that can expand across equipment categories. Footwear brands, like SQAIRZ, are broadening their horizons, extending endorsement deals into sports beyond golf, such as baseball. This move underscores a quest for multi-sport validation, aiming to diversify revenue streams and reduce seasonality risks.

Golf Shoes Industry Leaders

-

FootJoy (Acushnet Company)

-

Adidas AG

-

Nike Inc.

-

PUMA SE

-

Goatlane Sports AB

- *Disclaimer: Major Players sorted in no particular order

Golf Shoes Market Companies Covered in this Report

- Goatlane Sports AB

- Acushnet Company (FootJoy)

- Adidas AG

- Nike Inc.

- PUMA SE

- ECCO Sko A/S

- Under Armour Inc.

- Skechers USA Inc.

- Topgolf Callaway Brands Corp.

- New Balance Athletics Inc.

- ASICS Corporation

- Duca del Cosma B.V.

- Nebuloni Golf

- Mizuno Corporation

- Peter Millar LLC

- Genesco Inc.

- Royal Albartross

- PAYNTR Golf

- Kankura Golf

- Decathlon

Recent Industry Developments in Golf Shoes Market

- July 2025: FootJoy, in collaboration with Harris Tweed Shoes, unveiled a limited edition of golf shoes during the 153rd British Open at Royal Portrush. The Premiere Series Packard and Field models boast authentic Harris Tweed wool, adorned in a unique plaid pattern that pays homage to the culture and traditions of Northern Ireland’s Antrim coast.

- July 2025: Nike Inc. debuted its latest golf-inspired sneakers during the PGA Championship. The lineup includes the Nike Victory Tour 4, Air Zoom Infinity Tour 2, and Air Max 90 Golf. The performance golf shoe's base is crafted from faux ostrich leather, complemented by a mudguard showcasing a textured, spotted metallic gold pattern.

- April 2025: Adidas introduced its golf shoe collection, featuring the Coursecup and Gazelle Golf, timed with the prestigious Master's Tournament.

- March 2025: Under Armour rolled out a limited-edition golf shoe, celebrating its growing accolades. This model boasts the Swing Support System for a 360-degree lockdown, along with HOVR and Charged Cushioning for enhanced comfort and impact protection.

Global Golf Shoes Market Report Scope

Segmentation Overview

| Spiked Golf Shoes |

| Spikeless Golf Shoes |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Austria | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| New Zealand | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Spiked Golf Shoes | |

| Spikeless Golf Shoes | ||

| By End User | Men | |

| Women | ||

| Kids | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Austria | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| New Zealand | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global golf shoes market?

It is valued at USD 9.46 billion in 2025 and is projected to reach USD 11.75 billion by 2030.

Which region holds the largest share of golf footwear sales?

North America leads with 49.17% of 2024 revenue, supported by 45 million active golfers.

How fast is the women’s golf footwear segment growing?

Women’s shoes are forecast to expand at a 5.93% CAGR between 2025-2030 due to rising participation.

How does online retail contribute to golf shoe sales?

E-commerce channels are growing at a 5.48% CAGR thanks to rich product imagery, fit tools and flexible returns that build shopper confidence.

Page last updated on: