Sportswear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

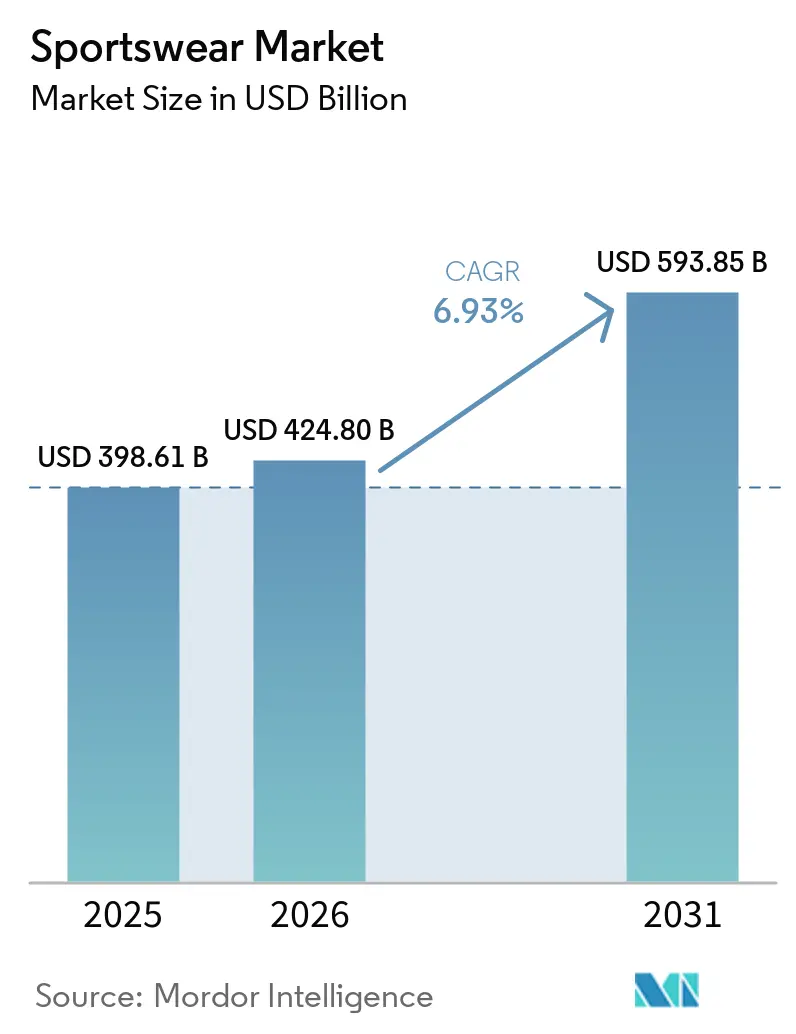

| Market Size (2026) | USD 424.80 Billion |

| Market Size (2031) | USD 593.85 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

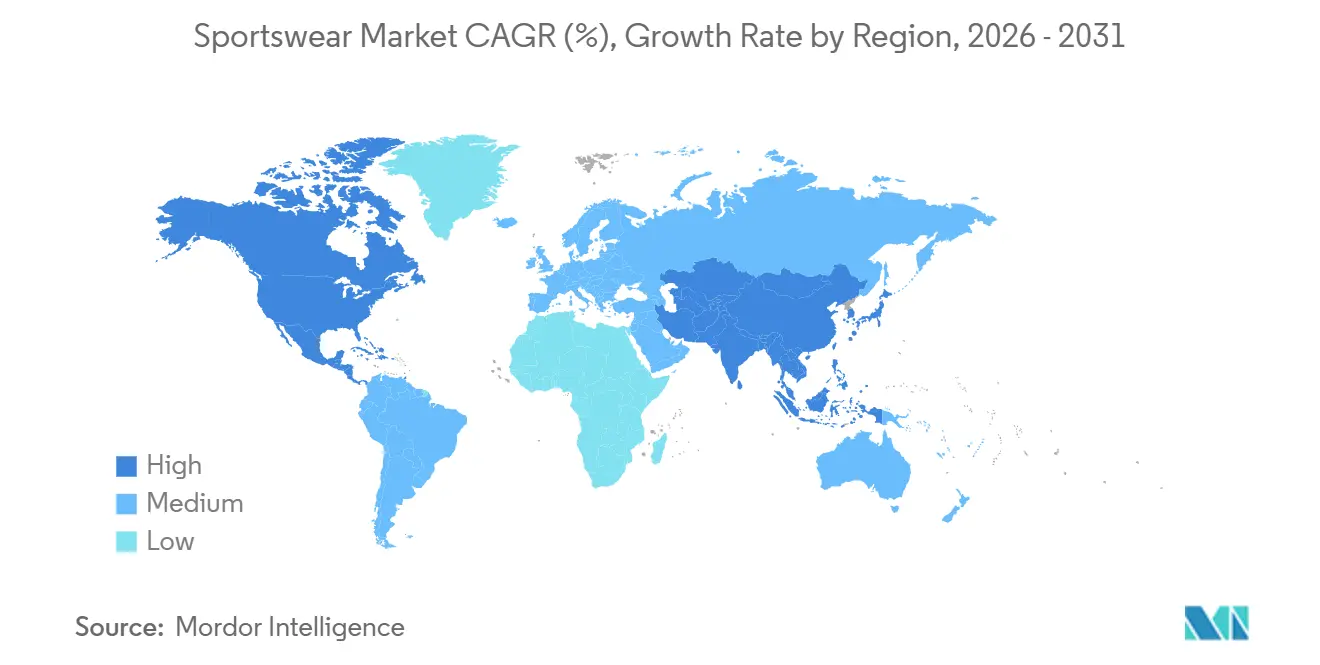

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sportswear Market Analysis by Mordor Intelligence

The sportswear market size is expected to increase from USD 398.61 billion in 2025 to USD 424.80 billion in 2026 and reach USD 593.85 billion by 2031, growing at a CAGR of 6.93% over 2026-2031. Sportswear has transitioned from a discretionary purchase to a core wardrobe category, supported by a structural shift in global consumer lifestyle priorities toward health and fitness. According to the Sports & Fitness Industry Association's (SFIA) 2026 Topline Participation Report, 250 million Americans participated in at least one sport or fitness activity in 2025, a historic high, reflecting the broader demand backdrop across the world's largest sportswear consumer market [1]Source: Sports & Fitness Industry Association, "Team Sports Lead Year-Over-Year Growth While Teen Inactivity Rises and the Gap Between Gender Activity Widens", sfia.org . Participation rates in team sports exceeded 90 million in the US alone, while global mass participation events reported 7.8% like-for-like growth in 2025, pointing to a sustained participation-driven demand cycle that underpins multi-year market expansion [2]Source: Eventrac, "THE MASS PARTICIPATION REPORT 2025", eventrac.co.uk. Brands that can combine supply chain diversification with credible anti-counterfeiting technology will be positioned to convert participation-driven demand into sustainable revenue growth through 2031.

Key Report Takeaways

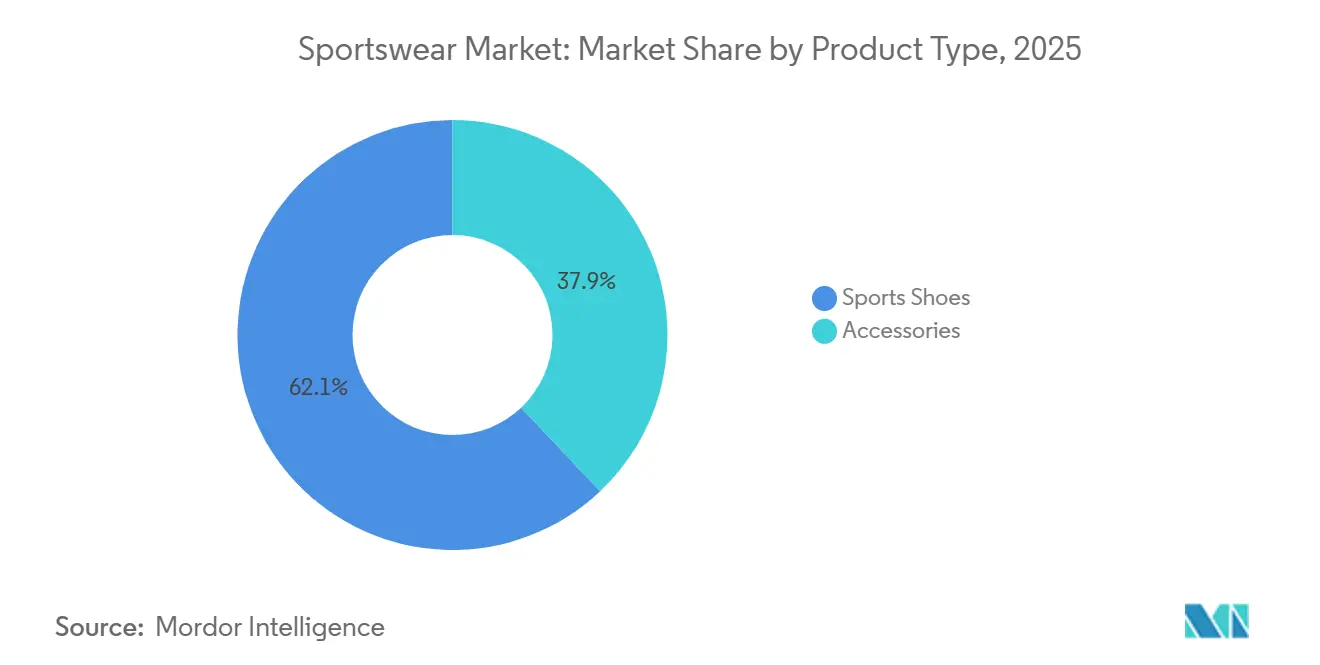

- By product type, sports shoes held 62.0% of the sportswear market share in 2025, while accessories are projected to grow at a 8.0% CAGR through 2031.

- By sports type, running accounted for 38.6% of the sportswear market size in 2025 and is also forecast to expand at a 8.4% CAGR through 2031.

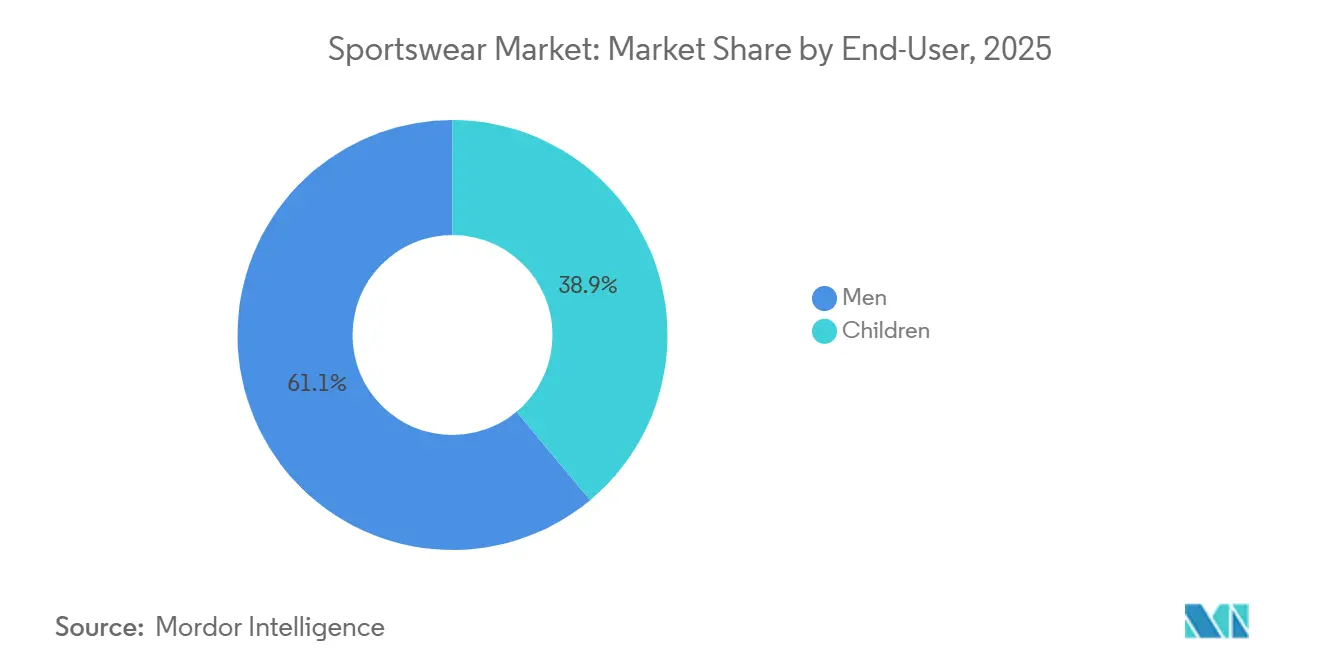

- By end-user, men represented 61.0% of the sportswear market size in 2025, while children are set to record the highest CAGR at 9.2% through 2031.

- By distribution channel, offline retail stores captured 67.8% of the sportswear market share in 2025, while online retail stores are advancing at a 9.4% CAGR through 2031.

- By geography, North America held 42.2% of the sportswear market size in 2025, while Asia-Pacific is expected to post the fastest CAGR at 8.6% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sportswear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in fitness and sports activities | +1.5% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Celebrity endorsements and sports sponsorships boosting demand | +0.9% | Global, particularly North America, Europe, and urban APAC (Asia-Pacific) markets | Short term (≤ 2 years) |

| Product innovation in performance fabrics and design | +1.3% | Global, R&D concentrated in North America, Japan, and Germany | Medium term (2-4 years) |

| Growing popularity of athleisure fashion trends | +1.1% | Global, strongest in North America and urban APAC cities | Medium term (2-4 years) |

| Expansion of organized sports and fitness clubs | +0.7% | Global, early gains in APAC and MEA (Middle East and Africa) | Long term (≥ 4 years) |

| Growing female participation in sports activities | +0.8% | Global, with accelerating gains in South Asia, Middle East, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Fitness Participation Broadens the Consumer Base

The sportswear market is drawing support from historically high sports and fitness participation across mature and developing regions. The Sports & Fitness Industry Association reported that 250 million Americans joined at least 1 sport or fitness activity in 2025, while team sports participation moved past 90 million. The same report showed that only 32% of Americans met the federal guideline for weekly moderate activity, which leaves a large participation gap that can still convert into future apparel demand. This matters for the sportswear market because participation now extends beyond dedicated athletes and into everyday wellness routines. That wider user base supports repeat demand across shoes, apparel, and accessories instead of relying only on event-driven purchases.

Product Innovation in Performance Fabrics Repositions Quality Benchmarks

The sportswear market is also being shaped by a stronger product cycle centered on technical fabrics and material science. Nike introduced Aero-FIT for 2026 football kits with higher airflow and a construction made from 100% textile waste through advanced chemical recycling. In February 2026, Lululemon launched PowerLu, a new proprietary fabric designed for strength training with targeted support and motion range. These launches show that better cooling, support, and recycled inputs are becoming core buying factors instead of optional upgrades. In the sportswear market, brands that connect performance and sustainability in the same product are in a better position to support premium pricing and stronger brand loyalty.

Athleisure Expansion Converts Casual Consumers into Regular Buyers

The sportswear market continues to gain from athleisure demand because consumers now use active products across exercise, travel, and daily wear. That crossover effect is strengthening demand for sportswear and sports shoes beyond strictly performance-led occasions. It is also helping brands sell technical products to a broader audience that values comfort, appearance, and easy reuse across settings. This shift supports more frequent purchases because the same consumer can buy for training, casual use, and light outdoor activity. The sportswear market, therefore, benefits from a wider usage pattern that keeps demand active even when formal sports participation varies by season.

Celebrity Endorsements and Major Sporting Events Spike Near-Term Demand

The sportswear market still responds quickly to athlete partnerships and major sports events. In June 2026, PUMA announced a multi-year partnership with McLaren Racing that covers team kit and lifestyle apparel across Formula 1, IndyCar, F1 Academy, and sim racing. In March 2026, Lululemon extended its performance story through ShowZero technology and linked the launch to professional tennis player Frances Tiafoe. These moves show how endorsements and event alignment can lift visibility and drive faster product sell-through in a short window. They also raise execution pressure because brands need fresh product pipelines to avoid weak post-event demand once the initial surge fades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of counterfeit sportswear products | -0.8% | Global, concentrated in APAC and MEA, major re-export hubs in China, Türkiye, Hong Kong | Short term (≤ 2 years) |

| Supply chain disruptions affecting product availability | -0.7% | Global, polyester-intensive and Middle East-dependent sourcing chains most exposed | Short term (≤ 2 years) |

| Seasonal demand fluctuations across regions | -0.3% | Temperate climate markets in North America and Northern Europe | Short term (≤ 2 years) |

| Fast-changing fashion trends increasing inventory risks | -0.5% | Global, most acute in urban markets of North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Sportswear Products Erode Brand Revenue and Consumer Trust

Counterfeit supply remains a direct challenge for the sportswear market, especially around high-visibility tournament periods. In April 2025, OLAF and Spanish customs seized 1.5 tonnes of counterfeit sportswear that was headed for a major football event. The European Union Intellectual Property Office reported that counterfeiting continues to damage legitimate clothing sales and employment across the region. The International Trademark Association also noted that mobile-first shopping and deceptive websites are making it harder for consumers to identify genuine sellers [3]Source: International Trademark Association, "Exploring the Growing Problem of Counterfeits in Sports Apparel & Merchandise", inta.org. In the sportswear market, brands with stronger authentication tools and better channel control are more likely to protect pricing power and trust through major event cycles.

Supply Chain Disruptions Drive Up Input Costs and Constrain Availability

Supply pressure remains a near-term limit on the sportswear market because many product lines still depend heavily on synthetic materials and complex sourcing routes. The current disruption around the Strait of Hormuz has been described as the most severe garments and textiles supply shock since the pandemic, with textile production costs at risk of rising by 10% to 15%. Under Armour said supply chain pressure reduced gross margin by 315 basis points in fiscal 2026, and the company responded by cutting 25% of its SKUs. Columbia Sportswear also disclosed that it paid USD 80 million in tariffs during Q1 2026 while waiting for refunds, which shows how trade policy is adding direct cost pressure. For the sportswear market, the companies in the strongest position are those that have already diversified sourcing and started reducing exposure to volatile input channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Footwear Dominates, Accessories Gain Ground

Sports shoes held a 62.0% share in 2025, which made them the largest product category in the sportswear market. Their lead reflects higher average selling prices and steady demand across performance, casual, and sport-casual use. Sports apparel remained the second-largest product type and continued to benefit from the same athleisure crossover that supports broader category demand. This pattern shows that the sportswear industry is still anchored by footwear economics, even as apparel narratives become more product-led.

Accessories are projected to grow at an 8.0% CAGR through 2031, making them the fastest-expanding product type in the sportswear market. Growth is being supported by compression gear, sports bags, hydration products, and other performance-adjacent purchases that consumers now treat as part of a full activity setup. PUMA strengthened this part of the innovation chain in March 2026 when it partnered with Shincell New Materials to co-develop the next generation of NITRO foam and opened a joint laboratory in Suzhou. Nike also reported 16% equipment growth in North America in fiscal 2025, which supports the view that accessories are becoming a repeat purchase category rather than an occasional add-on

By Sports Type: Running Commands Market Share, Other Sports Accelerate

Running accounted for 38.6% of the sportswear market size in 2025, and it is forecast to expand at an 8.4% CAGR through 2031. That makes running both the largest and fastest-growing sports type in the sportswear market. The segment benefits from recurring demand because runners replace shoes and technical apparel more frequently than many other user groups. Running also sets the tone for fabric innovation, fit, and comfort across the wider portfolio.

Other sports types continue to create focused opportunities in soccer, basketball, golf, and baseball within the sportswear market. Soccer lines are receiving a lift from the 2026 World Cup cycle, which is raising demand in host and participant markets. Basketball remains commercially important in North America and China, while golf keeps high value per unit because of dress codes and premium buyers. The sportswear industry also benefits when technical credibility in running carries over into lifestyle and multi-sport collections, which helps brands stretch one area of strength across a broader product mix.

By End-User: Men Lead, Children Drive Future Growth

Men generated 61.0% of revenue in 2025, which kept them as the largest end-user group in the sportswear market. The segment benefits from stronger spending in performance categories and a larger base of team sports participants. This scale still gives men a central role in product launch planning, retail placement, and brand campaigns. At the same time, the sportswear market is expanding beyond that core base as participation spreads more evenly across age groups and formats.

Children are projected to record a 9.2% CAGR through 2031, making them the fastest-growing end-user segment in the sportswear market. The National Federation of State High School Associations reported 8.26 million high school sports participants in the 2024-25 school year, the highest level on record. The same release showed strong gains in girls' flag football and wrestling, which is widening product demand across youth categories. This gives the sportswear market a longer demand runway because youth participation today can translate into adult brand loyalty in later years.

By Distribution Channel: Offline Retail Anchors, Digital Channels Accelerate

Offline retail stores held 67.8% share in 2025, which kept them as the largest channel in the sportswear market. Physical stores still matter because consumers often want to check fit, feel, and comfort before buying performance shoes and technical apparel. They also remain important for branded storytelling and event-linked merchandising. This means stores continue to support both conversion and brand visibility even as digital gains speed.

Online retail stores are expected to grow at a 9.4% CAGR through 2031, making them the fastest-growing channel in the sportswear market. Adidas reported that direct-to-consumer sales rose 22% on a currency-neutral basis in Q1 2026, with own retail up 19% and e-commerce up 25%. This shows that digital growth is strongest when brands combine their own platforms with strong store networks and brand control. In the sportswear market, that mix gives companies better pricing discipline, richer customer data, and a stronger base for repeat purchases across categories.

Geography Analysis

North America held 42.2% of the sportswear market size in 2025, which made it the largest regional contributor. The region benefits from high fitness spending, strong brand penetration, and a wide retail base across stores and direct digital channels. The 2026 World Cup is adding another layer of demand across the United States, Canada, and Mexico as brands push team kits and event-led collections. Columbia Sportswear disclosed that it paid USD 80 million in tariffs during Q1 2026 while awaiting refunds, which shows that cost pressure is still affecting operators in the region. Even with those pressures, North America remains a key anchor for the sportswear market because participation habits are keeping demand more resilient than broad apparel spending.

Europe remained the second-largest regional block in the sportswear market, with Germany leading demand and the UK set to record the fastest growth in the region through 2031. The region benefits from strong consumer attention to technical quality and from the presence of major brands such as Adidas and PUMA. Adidas reported record revenue of EUR 24,811 million, or USD 27.2 billion, in 2025, with apparel up 15% and footwear up 12% on a currency-neutral basis. That result shows that Europe still matters as both a demand center and a base for global product and brand development.

Asia Pacific is forecast to grow at an 8.6% CAGR through 2031, which makes it the fastest-growing geography in the sportswear market. China and India are the main demand engines as urbanization, younger consumers, and expanding gym culture increase category reach. The region is also becoming more important in competitive terms because Asian brands are pushing beyond their home bases and building larger international ambitions. The Middle East and Africa remain smaller in current value, but government-backed sports development and football visibility are gradually widening the accessible customer base for the sportswear market.

Competitive Landscape

The sportswear market remains moderately fragmented, with Nike and Adidas forming the leading global pair while several regional and category-focused brands continue to narrow the gap. Nike reported revenue of USD 46.3 billion for fiscal 2025, down 10% from the prior year, which reflected weaker momentum in parts of its business. Adidas moved in the opposite direction and reported record 2025 revenue, with strong growth in both apparel and footwear. That contrast shows that leadership in the sportswear market is still meaningful, but it is not fixed. Brand momentum, category execution, and direct retail strength are now changing competitive positions more quickly than before.

Strategic moves in 2026 show that the sportswear market is being contested through product technology, partnerships, and selective expansion. PUMA signed a multi-year global partnership with McLaren Racing in January 2026 to supply team kit and lifestyle apparel across multiple motorsport properties. Lululemon announced entry into 6 new markets in 2026 through franchise partnerships, which shows a deliberate push into earlier-stage demand centers. Adidas also launched a EUR 1 billion share buyback backed by expected 2026 cash flows, which signals management confidence in continued operating strength.

Materials innovation is becoming one of the clearest ways to stand apart in the sportswear market. Nike used Aero-FIT to raise its performance and recycled-material story in elite apparel. Lululemon extended its technical platform through PowerLu and ShowZero, which shows how fabric ownership can support both function and brand identity. In the sportswear market, brands that control fabric development, direct channels, and strong event visibility are better placed to defend price realization against smaller rivals and private-label pressure.

Sportswear Industry Leaders

-

Nike Inc.

-

Adidas Group

-

Puma SE

-

Under Armour Inc.

-

Lululemon Athletica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Under Armour launched The Bouncy Tee featuring NEOLAST™, an advanced fiber co-developed with Pima cotton to deliver engineered stretch, shape retention, and rapid-dry moisture management, expanding the brand's premium performance basics line as it executes a portfolio reset following significant SKU rationalization

- March 2026: Lululemon introduced ShowZero™ sweat-concealing technology for high-sweat activities, developed with professional tennis player Frances Tiafoe, as the first major extension of the ShowZero platform beyond golf. The technology uses a novel yarn structure that alters light interaction with fabric to conceal perspiration during intense exertion

- January 2026: PUMA announced a multi-year global partnership with McLaren Racing covering team kit and lifestyle apparel across the McLaren Formula 1 Team, Arrow McLaren IndyCar Team, F1 Academy, and McLaren F1 Sim Racing, extending PUMA's motorsport brand equity into one of the sport's most commercially valuable team franchises

Global Sportswear Market Report Scope

The sportswear market comprises apparel, footwear, and accessories specifically designed for sports, fitness, athletic activities, and active lifestyles. The Sportswear Market Report is Segmented by Product Type (Sports Apparel, Sports Shoes, and Accessories), Sports Type (Golf, Soccer, Basketball, and More), End-User (Men, Women, Children), Distribution Channel (Online Retail Stores and Offline Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Sports Apparel |

| Sports Shoes |

| Accessories |

| Golf |

| Soccer |

| Basketball |

| Baseball |

| Running |

| Other Sport Types |

| Men |

| Women |

| Children |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Sports Apparel | |

| Sports Shoes | ||

| Accessories | ||

| Sports Type | Golf | |

| Soccer | ||

| Basketball | ||

| Baseball | ||

| Running | ||

| Other Sport Types | ||

| End-User | Men | |

| Women | ||

| Children | ||

| Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the sportswear market by 2031?

The sportswear market is forecast to reach USD 593.9 billion by 2031, rising from USD 424.8 billion in 2026 at a 6.9% CAGR.

Which product category leads sportswear sales?

Sports shoes led product demand with a 62.0% share in 2025, supported by premium pricing and broad use across performance and casual wear.

Which sports category is growing fastest in sportswear?

Running is both the largest and the fastest-growing sports type, with 38.6% share in 2025 and an 8.4% CAGR through 2031.

Why do offline stores still matter for sportswear sales?

Offline stores still led with 67.8% share in 2025 because many buyers want to test fit, comfort, and fabric feel before purchasing.

Page last updated on: