Golf Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

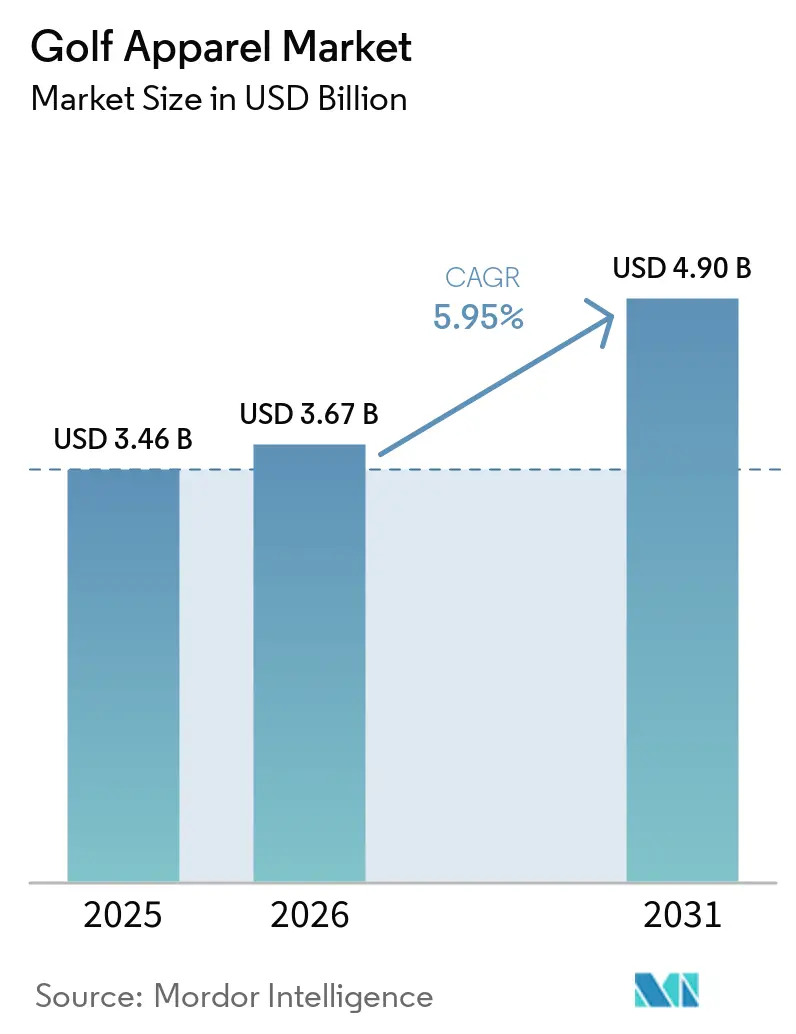

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 4.90 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

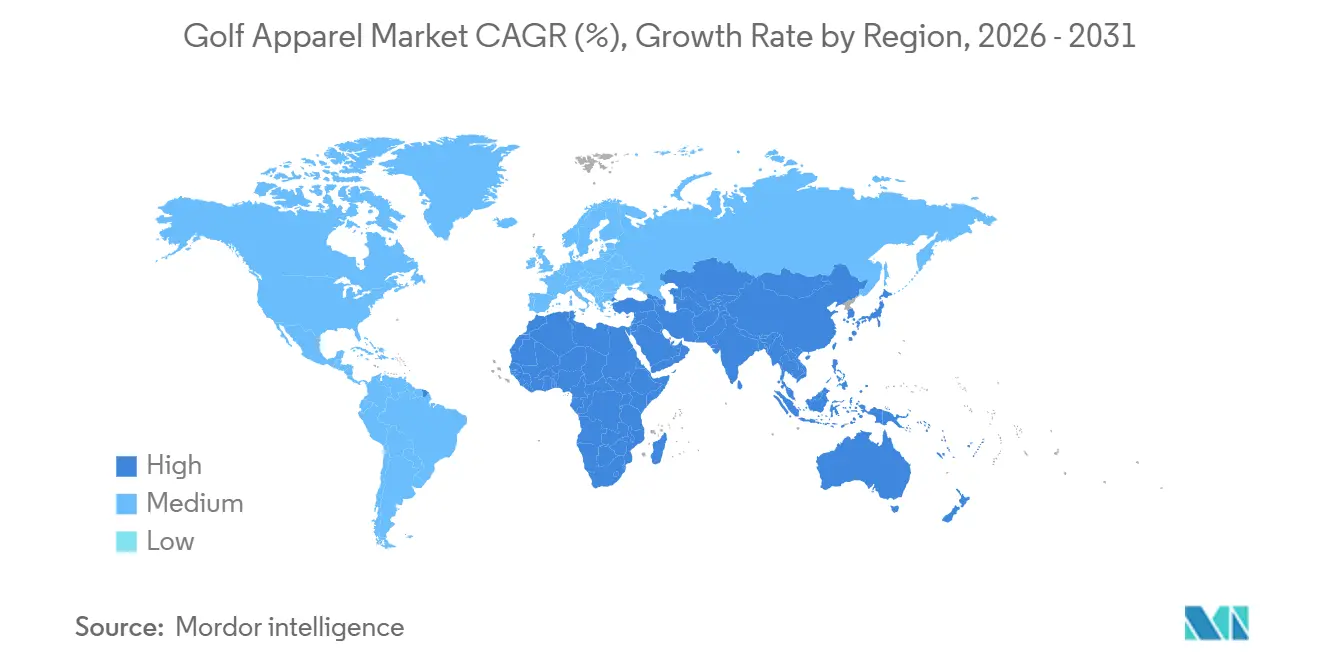

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Golf Apparel Market Analysis by Mordor Intelligence

The golf apparel market size is expected to increase from USD 3.46 billion in 2025 to USD 3.67 billion in 2026 and reach USD 4.90 billion by 2031, growing at a CAGR of 5.95% over 2026-2031. High-income baby boomers are driving solid demand, while athleisure-inspired designs and a booming e-commerce sector are bolstering the golf apparel market's growth. Lightweight, four-way-stretch laminates in performance outerwear are setting new premium price benchmarks by offering enhanced comfort and mobility, appealing to both amateur and professional golfers. Meanwhile, in sun-soaked Asia-Pacific, UV-protective smart fabrics are sparking a surge in demand as consumers prioritize skin protection alongside performance. Direct-to-consumer brands, leveraging influencer-led drops and limited-edition collections, are carving out market share from established players by creating a sense of exclusivity and urgency. Notably, women's golf apparel lines are outpacing men's, coinciding with heightened media attention on professional women's golf, which is inspiring more women to take up the sport. While input-cost fluctuations, counterfeit challenges, and lenient country-club dress codes are tempering the momentum, they haven't halted it in the golf apparel market, which continues to evolve and adapt to changing consumer preferences.

Key Report Takeaways

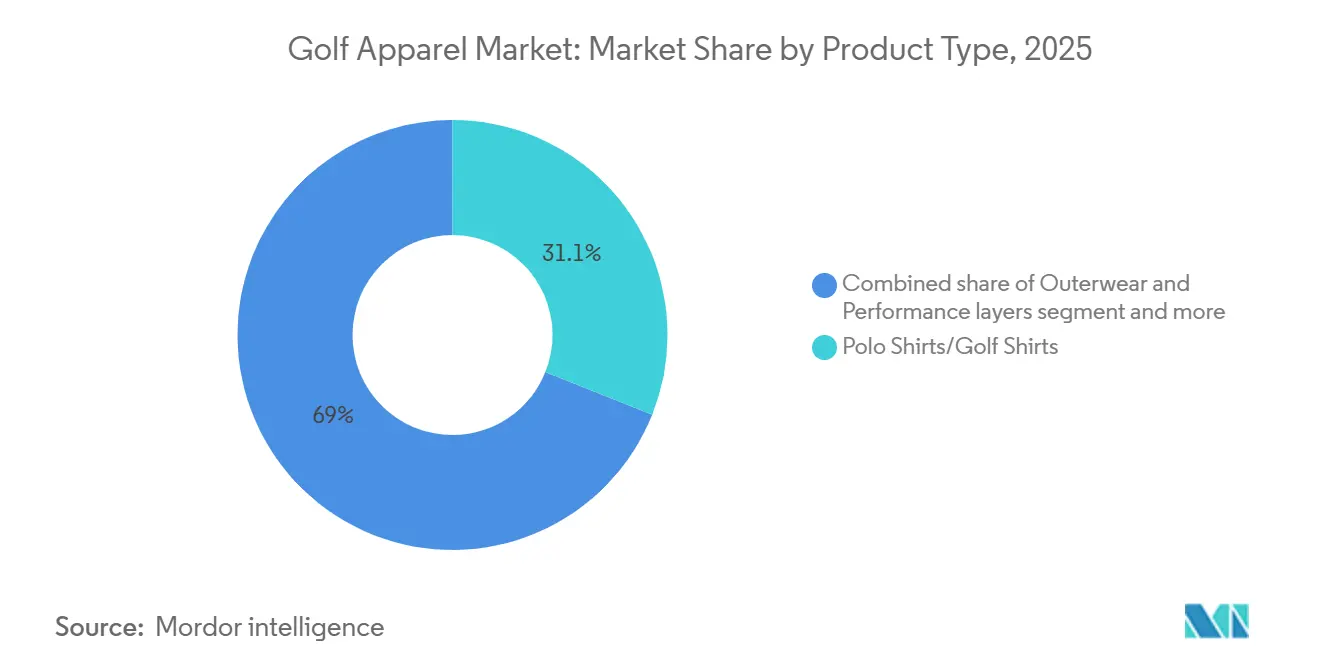

- By product type, polo and golf shirts led with 31.05% of 2025 revenue, while outerwear and performance layers are projected to grow at an 8.15% CAGR through 2031.

- By end user, men held 63.71% of the 2025 demand, yet women’s apparel is forecast to expand at a 7.68% CAGR over 2026-2031.

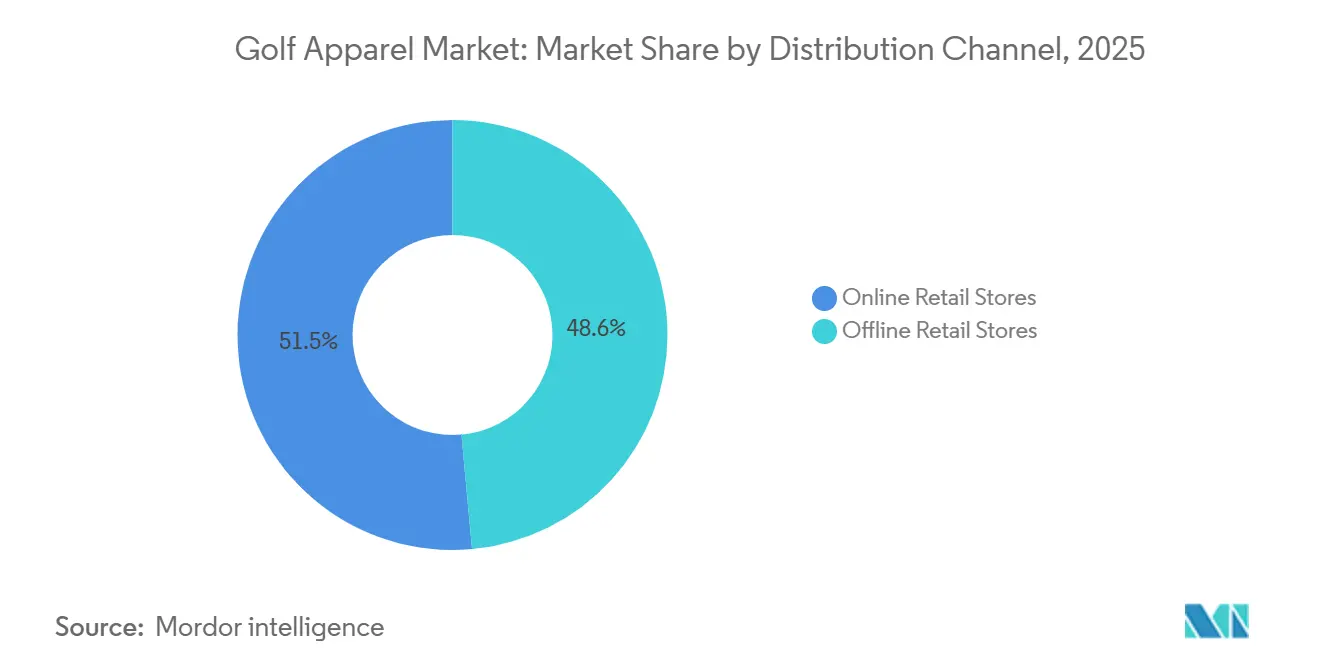

- By distribution channel, offline retail captured 48.55% of 2025 sales, whereas online platforms are advancing at a 13.22% CAGR through 2031.

- By geography, North America commanded 36.48% of 2025 revenue, and Asia-Pacific is on track for a 7.98% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global golf participation among millennials | +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Influence of athleisure crossover trends | +0.9% | Global, led by North America and Europe | Short term (≤ 2 years) |

| High disposable income of core golf demographics | +0.8% | North America, Europe, select Asia-Pacific markets (Japan, South Korea) | Long term (≥ 4 years) |

| Accelerating women's pro-golf media coverage | +0.7% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rise of golf-centric micro-influencers boosting DTC brands | +1.0% | Global, digitally native markets (North America, Asia-Pacific urban centers) | Short term (≤ 2 years) |

| Adoption of UV-protective smart fabrics in Asia-Pacific | +0.6% | Asia-Pacific core, spillover to Middle East and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising global golf participation among millennials

In 2024, Millennials emerged as the dominant age group among U.S. golfers, numbering 6.3 million out of a total of 47.2 million[1]Source: National Golf Foundation, "A New Age in Golf", ngf.org. Their quicker turnover in apparel purchases is driving volume growth, as they tend to replace items more frequently compared to older cohorts. Technical fabrics that seamlessly blend workout functionality with urban style are gaining traction, especially since 51% of Gen Z golfers prioritize wellness over competition, reflecting a shift in consumer preferences toward health-conscious and lifestyle-oriented products. Brands that market polos and outerwear as versatile staples, rather than specialized gear, are successfully attracting younger buyers at rates surpassing the market average. This demographic's heightened engagement on social media has empowered direct-to-consumer brands to expand without relying on traditional tour endorsements, enabling these brands to connect directly with their target audience and build loyalty. Collectively, these dynamics are fueling a consistent uptick in spending within the golf apparel market, creating opportunities for innovation and growth in this segment.

Influence of athleisure crossover trends

Lululemon's foray into golf apparel demonstrated that its signature four-way stretch, moisture-wicking knits, originally crafted for yoga, adapt effortlessly to the golf course. This move not only showcased the versatility of its products but also set a new standard for performance-driven golf apparel. In response, competitors have integrated these features into their standard offerings, resulting in heightened average selling prices and accelerated product lifecycles, as brands strive to keep up with evolving consumer expectations. In 2025, PUMA, in collaboration with Show Me Your Mumu, launched a women-centric capsule that married stylish silhouettes with high-performance fibers, highlighting a trend towards fashion-forward designs that cater to both functionality and aesthetics. With minimalist color palettes and tapered fits suitable for both on and off the course, the appeal of golf apparel is expanding, attracting a broader consumer base. This shift is amplifying the presence of lifestyle-centric disruptors in the market, as they continue to challenge traditional players by blending style and performance seamlessly.

High disposable income of core golf demographics

Golfers aged 50 and above consistently lead in apparel spending, a trend fueled by their established playing habits and unwavering brand loyalty. This demographic refreshes its wardrobe each season, gravitating towards heritage labels like Peter Millar and FootJoy, which are known for their premium quality and classic designs. While they traditionally favor pro shops and specialty retailers for the tactile shopping experience and personalized service, there's a noticeable shift towards curated e-commerce platforms offering convenience and tailored recommendations. This evolution compels brands to strike a balance between their brick-and-mortar presence and direct online channels to cater to this segment effectively. Even as younger demographics gain momentum with their growing interest in golf apparel, the spending of this older cohort remains pivotal, underpinning baseline unit volumes and profit margins, and providing a stable revenue stream for the market.

Accelerating women’s pro-golf media coverage

According to the Asia-Pacific Golf Confederation, women now make up almost 25% of the global pool of registered golfers, which equates to a notable 7.9 million female golfers in the U.S. alone[2]Asia-Pacific Golf Confederation," Golf Participation is Growing and Diversifying", apgc.online. This uptick has led to a notable rise in apparel adoption among recreational female golfers, as increased visibility of the sport encourages participation and demand for specialized clothing. Instead of merely resizing men's cuts, brands are now establishing dedicated design teams to cater specifically to women’s preferences and performance needs. PUMA and Nike, for instance, have rolled out women-centric lines, championed by star athletes such as Nelly Korda, which further drive consumer interest. These initiatives not only enhance brand loyalty but also set a new standard for inclusivity and innovation in the golf apparel market. With this heightened visibility, retailers are increasingly allocating shelf space to women's collections, thereby expanding the overall golf apparel market and creating new growth opportunities for industry players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in performance-textile raw-material prices | -0.5% | Global, with acute impact in manufacturing hubs (Vietnam, China, Cambodia) | Short term (≤ 2 years) |

| Counterfeit and grey-market golf apparel | -0.4% | Global, concentrated in Asia-Pacific and online marketplaces | Medium term (2-4 years) |

| Seasonal demand fluctuations in temperate regions | -0.3% | North America, Europe, temperate Asia-Pacific markets | Short term (≤ 2 years) |

| Country-club dress-code liberalization reducing premium-apparel turnover | -0.2% | North America, Europe (private clubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in performance-textile raw-material prices

Brands reliant on oil-derived inputs, like polyester and elastane, find themselves at the mercy of crude price fluctuations. These fluctuations can significantly impact production costs, leading to potential pricing adjustments or margin pressures. Nike's FY2025 report highlighted that 61% of its apparel volume comes from Vietnam, China, and Cambodia. Any currency or energy shocks in these regions could dent Nike's gross margins, as these factors directly influence manufacturing and logistics expenses. While industry giants employ vertical integration and multi-year hedging to buffer against such risks, smaller direct-to-consumer labels lack this luxury. Without similar risk mitigation strategies, these smaller players face heightened exposure to cost volatility. As a result, when input costs surge, the competitive edge leans heavily towards the larger players, who can better absorb or offset these fluctuations.

Counterfeit and grey-market golf apparel

In January 2026, Chinese authorities confiscated over 105,000 counterfeit golf garments, bringing the total lifetime seizures to over 3 million units. According to a report, counterfeiting costs Europe's clothing, cosmetics, and toy sectors a staggering EUR 16 billion each year. This figure represents 5.2% of their combined total revenue and translates to the loss of nearly 200,000 jobs annually[3]European Union Intellectual Property Office," Economic impact of counterfeiting in the clothing, cosmetics, and toy sectors in the EU", euipo.europa.eu. This underscores the ongoing battle against counterfeit goods, which continues to undermine brand reputation and erode consumer confidence. The rise of digital marketplaces has further exacerbated the issue, enabling unauthorized sales and turning brand protection into a significant and recurring cost center for companies. To address this, measures such as blockchain tagging and serialized QR codes are being introduced to improve product authenticity and traceability. However, cross-border enforcement remains inconsistent, posing a substantial challenge, particularly for mid-tier brands with constrained legal budgets, which limits their ability to effectively combat counterfeit operations on a global scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Outerwear Guides Innovation Spending

Polo and golf shirts, accounting for 31.05% of total revenue in 2025, dominate the market. Their frequent replacement and everyday usability, both on and off the course, bolster this position. Consistent demand from both amateur and professional golfers cements their status as staples in apparel rotations. Innovations like adidas's TWISTKNIT, emphasizing lightweight and performance-oriented fabrics, have notably enhanced comfort and breathability, bringing them closer to technical outerwear. The segment's broad price accessibility attracts a diverse consumer base globally. Furthermore, categories like headwear serve as entry-level purchases, bolstering the overall demand for apparel.

Outerwear and performance layers, the fastest-growing segment, are set to expand at a CAGR of 8.15%. This growth is fueled by breakthroughs in waterproof and breathable technologies. Products boasting waterproof ratings of up to 20,000 mm are particularly popular among consumers prioritizing all-weather functionality. Brands like Galvin Green and PING are at the forefront, introducing high-performance shells and jackets that command premium prices. Sustainability trends also favor this segment, exemplified by Nike's Aero-FIT line, which melds recycled materials with a design for better airflow. As the pace of innovation quickens, mid-tier brands find themselves at a crossroads: invest in R&D or compete on price, altering the competitive dynamics.

By End User: Women Outpace Men From a Smaller Base

In 2025, men's apparel is set to dominate, making up 63.71% of total spending. This stronghold is bolstered by a loyal consumer base and a deep-rooted affinity for traditional golf brands. The segment enjoys scale advantages, with steady demand for staples like polos, trousers, and outerwear. Yet, growth is slowing as younger male consumers gravitate towards versatile athleisure styles that extend beyond the golf course. Brands are now re-evaluating their designs and positioning to stay relevant with these shifting demographics. Nevertheless, men's apparel remains the cornerstone of market revenue, thanks to its established foothold and robust purchasing power.

Women's apparel is on a rapid ascent, with projections showing a CAGR of 7.68%. This surge is fueled by increasing participation and heightened visibility, notably through platforms like LPGA coverage. Brands are pivoting towards tailored designs that emphasize fit, comfort, and style, rather than merely adapting men's templates. Such a shift is broadening the consumer base and spurring more frequent purchases. Moreover, a rising interest in coordinated collections and trendier golfwear is amplifying the segment's allure. While still smaller in scale, women's apparel is carving out a significant growth trajectory, driven by innovation and a deeper engagement in the sport.

By Distribution Channel: Online Acceleration Reshapes Economics

In 2025, offline retail is set to dominate, making up 48.55% of total sales. This is largely thanks to a dedicated group of affluent, older golfers who value the in-store experience. Physical stores not only allow for fit checks and fabric assessments but also offer personalized services that sway purchasing choices. Pro shops and specialty outlets are pivotal in bolstering brand trust and pushing premium product sales. Even with the digital wave, the in-store experience holds its ground, thanks to its unique advantages. To further engage customers and curb potential sales losses, retailers are adopting tech innovations like virtual mirrors and endless-aisle kiosks.

E-commerce is on a rapid ascent, with projections indicating a CAGR of 13.22%. This surge is fueled by the swift emergence of direct-to-consumer brands and a digital-first approach. Online avenues empower brands to secure better margins, which they often reinvest in influencer marketing, social media, and regular product launches. The allure of digital convenience is drawing in younger consumers, broadening the market's reach. Concurrently, omnichannel strategies are becoming more prevalent. A case in point is Good Good Golf, which is branching out into U.S. pro shops to bolster its online demand efforts. Yet, the journey to achieve a flawless blend of online and offline channels is ongoing, presenting both hurdles and prospects for retailers.

Geography Analysis

In 2025, North America accounted for 36.48% of total revenue, buoyed by affluent golfers aged 50 and above and bolstered by the region's extensive course infrastructure. While rising youth participation offers potential growth, Q2 sell-throughs often falter with adverse spring weather, leading to deeper markdowns and stricter inventory controls. Additionally, brands in this market enjoy a robust premium positioning, particularly in the performance and lifestyle segments.

Asia-Pacific, led by consumers in China, Japan, and South Korea, is the region witnessing the fastest growth, boasting a 7.98% CAGR. These consumers are increasingly gravitating towards UV-protective textiles and lifestyle apparel tailored for the golf course. Furthermore, social media is playing a pivotal role in amplifying golf culture. For instance, localized content, like subtitled Good Good Golf videos, is effectively raising awareness among younger, middle-class shoppers. This blend of climate-conscious product demand and heightened digital engagement is propelling the category's expansion.

Europe maintains steady volume generation, particularly in the United Kingdom, Germany, and the Nordics. However, macroeconomic pressures are curbing discretionary spending. Meanwhile, smaller yet strategically vital markets in the Middle East and South America offer brands a chance to diversify, mitigating weather-related sales fluctuations and extending their sales window throughout the year. Collectively, these regions provide the golf apparel market with a wider geographic footprint and a more resilient growth trajectory.

Competitive Landscape

In the golf apparel market, moderate fragmentation is evident. While giants like Nike, Adidas, PUMA, and Under Armour command a significant share, it's not a majority. These brands leverage their global presence and marketing budgets to maintain relevance, but they face increasing competition from niche players. Meanwhile, specialists such as FootJoy and TravisMathew maintain their credibility, driven by tour endorsements. Their focus on performance-driven designs and strong ties to professional golfers help them retain a loyal customer base. Lululemon's foray into the market with a 2025 launch underscored the rising demand for crossover items, heightening the competition for stretch-knit polos and tapered joggers. This move highlights the growing intersection between athletic and lifestyle apparel in the golf sector.

Material science plays a pivotal role: Nike's Aero-FIT mesh and Under Armour's auxetic Clone upper showcase how R&D investments translate into enhanced pricing power. These innovations not only improve performance but also allow brands to differentiate themselves in a crowded market. By focusing on advanced materials, companies can cater to consumers seeking both functionality and comfort. Meanwhile, direct-to-consumer brands like Malbon Golf, Bad Birdie, and Eastside Golf are making waves. By leveraging micro-influencer communities and limited product drops, they're successfully appealing to younger consumers and challenging established players in the golf apparel sector. Their ability to create a sense of exclusivity and community engagement has disrupted traditional retail models.

Sustainability and customization are becoming key focus areas. Brands are in a race to roll out features like recycled yarns and on-demand color options, aiming to connect with environmentally-conscious buyers. These initiatives align with the growing consumer demand for eco-friendly and personalized products. Companies that prioritize these trends are likely to gain a competitive edge in the forecast period.

Golf Apparel Industry Leaders

-

Nike, Inc.

-

Adidas AG

-

PUMA SE

-

Acushnet Holdings Corp. (FootJoy)

-

Callaway Brands Corp. (TravisMathew)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cole Haan plans to launch its first golf apparel line in Spring 2026, marking its expansion beyond footwear into performance clothing. In partnership with Catapult Group, the men's collection combines refined design with innovative fabrics, offering stretchability, moisture management, temperature regulation, and weather resistance.

- July 2025: Honma Golf has launched a new apparel line, drawing inspiration from urban aesthetics, specifically designed for golfers in the city. This collection features sleek, minimalist designs crafted from advanced fabrics. These fabrics offer a range of benefits: moisture-wicking capabilities, UV protection, stretchability, and water repellency. The shirts in this collection are priced at around ¥10,000, and the pants come with a retail tag of ¥12,100.

- July 2025: In a nod to the esteemed legacy of The Open Championship, Nike Golf unveiled a trio of sneakers: the Victory Tour 4, Air Zoom Infinity Tour 2, and Air Max 90 Golf. Each sneaker, adorned in a striking white and accented with metallic gold, embodies the spirit of the prestigious event.

- June 2025: Centroid has completed its acquisition of TaylorMade from KPS, signaling a bold move into the premium golf equipment and apparel market. This acquisition allows Centroid to strengthen its position in the sports industry by leveraging TaylorMade's established brand reputation and extensive product portfolio.

- May 2025: Jordan Brand unveiled the Air Rev golf shoe, featuring the innovative Flight Lock containment. In addition, the brand hinted at a Summer 2025 apparel collection, showcasing stylish cargo pants and mock-neck tops designed for golf lovers.

Global Golf Apparel Market Report Scope

Golf Apparel refers to clothing specifically designed for golf. The market is segmented into various product types, end users, distribution channels, and geography. Based on the product type, the market is segmented into polo shirts/golf shirts, golf trousers/pants, shorts, golf skirts/skorts dresses, outerwear and performance layers, and headwear, and accessories. Based on end user, the market is segmented into female, male and kids. Based on the distribution channel, the market is segmented into online retail stores and offline retail stores. The market provides a detailed analysis for the major economies across North America, Europe, Asia-Pacific, South America and Middle East and Africa.

| Polo Shirts/Golf Shirts |

| Golf Trousers/Pants and Shorts |

| Golf Skirts/Skorts Dresses |

| Outerwear and Performance Layers |

| Headwear and Accessories |

| Female |

| Male |

| Kids |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Sweden | |

| Ireland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Polo Shirts/Golf Shirts | |

| Golf Trousers/Pants and Shorts | ||

| Golf Skirts/Skorts Dresses | ||

| Outerwear and Performance Layers | ||

| Headwear and Accessories | ||

| End User | Female | |

| Male | ||

| Kids | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Sweden | ||

| Ireland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the golf apparel market expected to grow between 2026 and 2031?

It is projected to register a 5.95% CAGR over 2026-2031, reaching USD 4.90 billion by the end of the forecast period.

Which region will add the most incremental revenue?

Asia-Pacific is forecast to post the fastest 7.98% CAGR, driven by UV-protective smart fabrics and rising player numbers.

What product category is expanding quickest?

Outerwear and performance layers are on track for an 8.15% CAGR as brands invest in breathable, waterproof shell systems.

Why is women’s golf apparel a priority for brands?

Media visibility, such as USD 132 million in LPGA prize money for 2026, is expanding participation, lifting women’s apparel at a 7.68% CAGR.

Page last updated on: