Golf Gloves Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

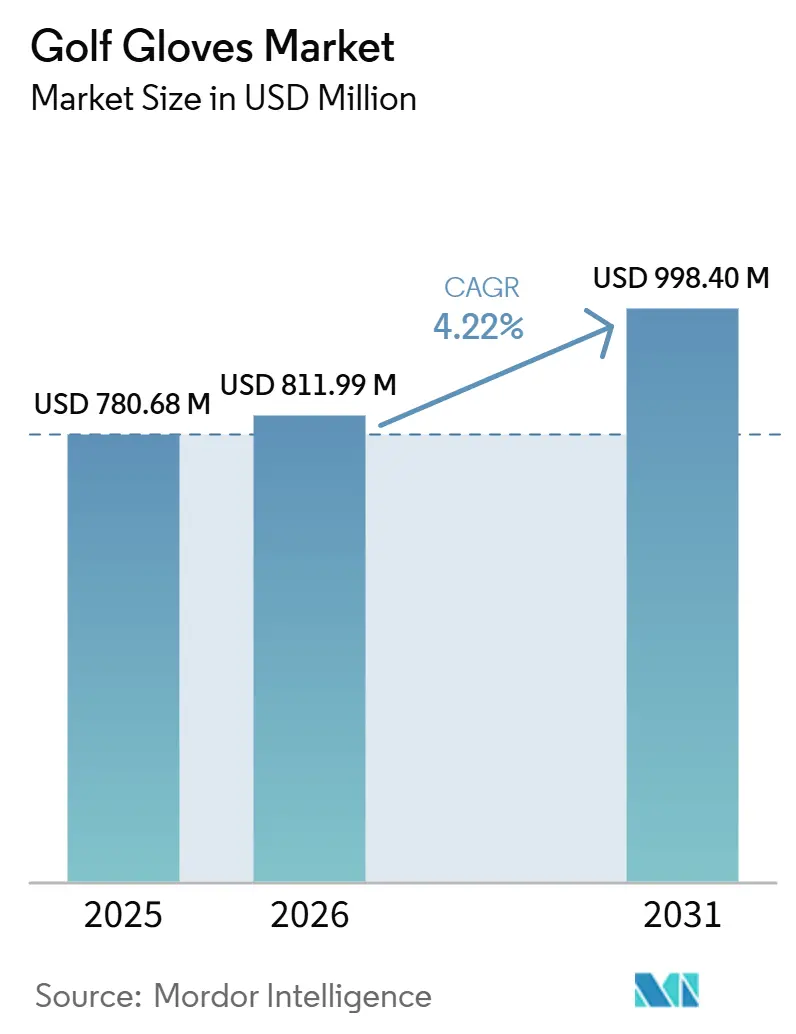

| Market Size (2026) | USD 811.99 Million |

| Market Size (2031) | USD 998.40 Million |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

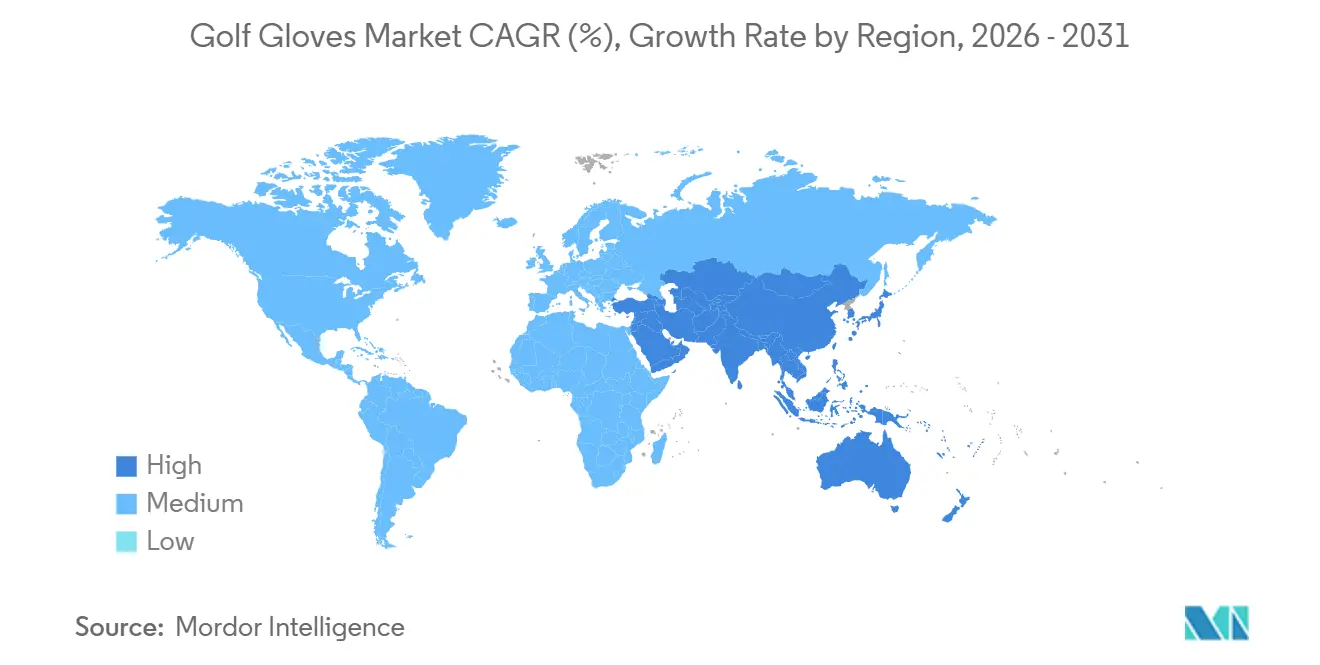

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Golf Gloves Market Analysis by Mordor Intelligence

The golf gloves market size was valued at USD 780.68 million in 2025 and estimated to grow from USD 811.99 million in 2026 to reach USD 998.40 million by 2031, at a CAGR of 4.22% during the forecast period 2026-2031. This growth is influenced by evolving demographics and advancements in material science, which are reshaping demand across both established and emerging golf markets. Insights from organizations such as the National Golf Foundation, The R&A, and the United States Golf Association reveal a steady increase in golf participation, with female players driving a significant portion of this momentum. Over the last decade, the share of female golfers in the U.S. has grown substantially, rising from a smaller proportion to a more prominent percentage today. Material innovation has become a critical factor for differentiation in the market. Companies are focusing on developing products that cater to performance and comfort. For example, Callaway's Syntech 2025 glove incorporates FUSETECH synthetic material with moisture-wicking panels to enhance usability, while Vice Golf's Duro 2025 glove is designed for all-weather performance at competitive price points. These innovations reflect the market's focus on addressing diverse consumer needs and preferences.

Key Report Takeaways

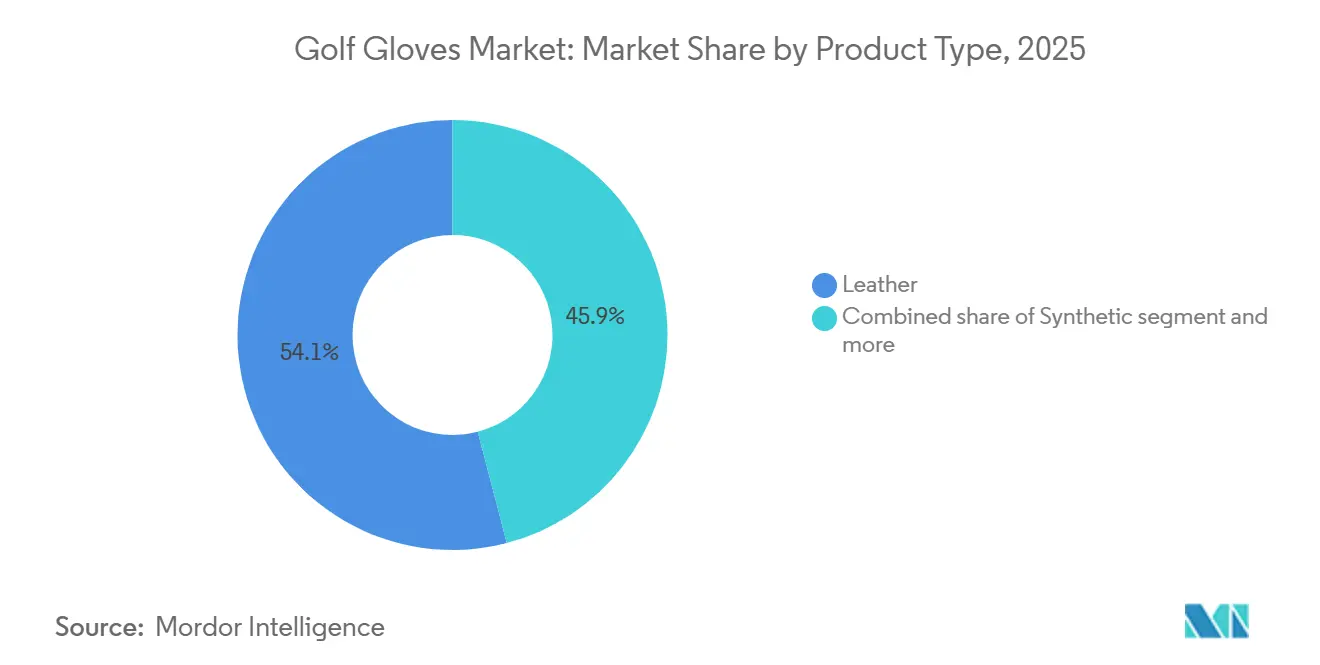

- By product type, leather gloves held 54.01% of the golf gloves market share in 2025; synthetic gloves are projected to advance at a 4.84% CAGR from 2026 to 2031, driven by humid-climate golfers seeking moisture-wicking durability.

- By end user, men accounted for 72.68% of the golf gloves market share in 2025; the women’s segment is forecast to grow at a 5.77% CAGR from 2026 to 2031, supported by rising female participation in the United States, Saudi Arabia, and Germany.

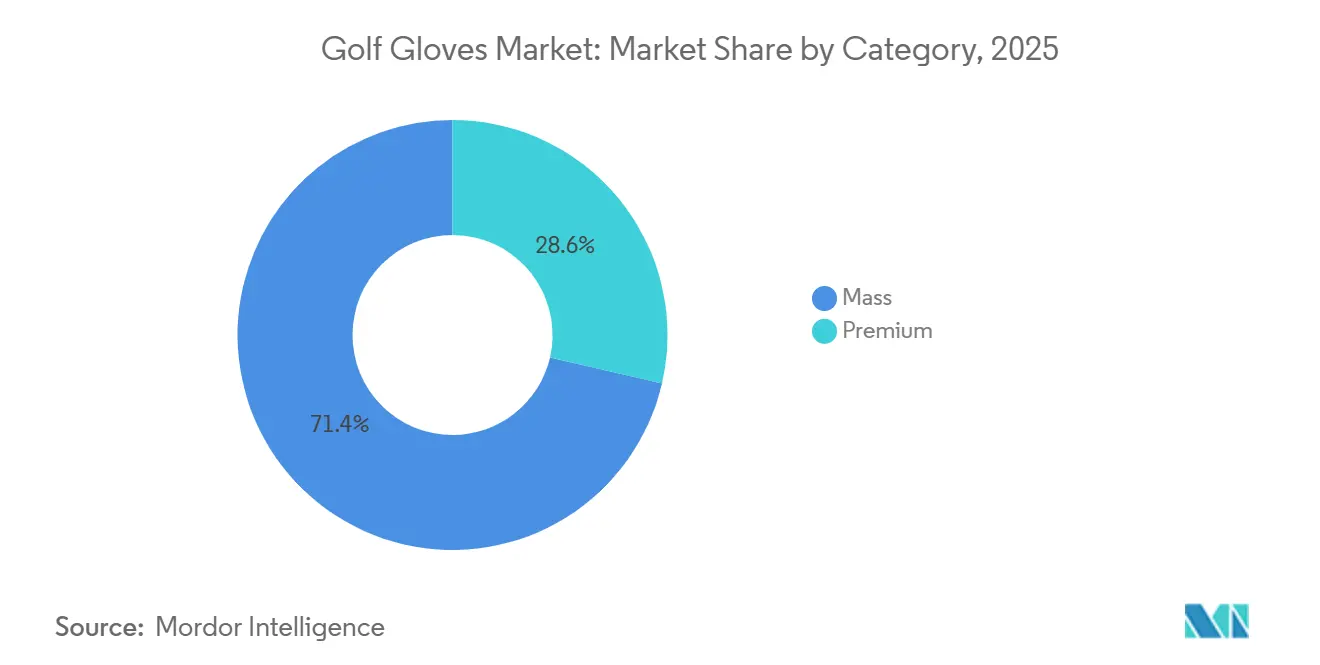

- By category, the mass tier held 71.37% of the golf gloves market share in 2025; the premium tier is projected to grow at a 6.03% CAGR from 2026 to 2031, as anatomical grip pads and hybrid materials justify higher price points.

- By distribution channel, offline retail retained 63.44% of the golf gloves market share in 2025; online channels are expected to climb at a 5.01% CAGR from 2026 to 2031, driven by direct-to-consumer brands and omnichannel upgrades at golf shops.

- By geography, North America captured 46.93% of the golf gloves market share in 2025; Asia-Pacific is anticipated to be the fastest-growing region, with a projected 5.26% CAGR from 2026 to 2031, fueled by infrastructure pipelines in India and Saudi Arabia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing recreational and leisure golf demand | +0.8% | Global, with strongest gains in North America, Middle East, India | Medium term (2-4 years) |

| Innovations in breathable and moisture-wicking materials | +0.7% | APAC core (humid climates), spill-over to North America and Europe | Short term (≤ 2 years) |

| Technological enhancements improving grip and comfort | +0.6% | North America & EU (premium segments), emerging in APAC | Medium term (2-4 years) |

| Rising global golf participation among all ages | +0.9% | Global, with early gains in India, Saudi Arabia, UAE, and Germany | Long term (≥ 4 years) |

| Growth in golf tournaments and competitive play worldwide | +0.5% | North America, Europe, Asia-Pacific (Japan, South Korea, Australia) | Medium term (2-4 years) |

| Enhanced marketing and brand visibility by key players | +0.4% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing recreational and leisure golf demand

Increasing recreational and leisure golf participation is a key driver for the global golf gloves market. In 2025, the National Golf Foundation reported 29.1 million on-course golfers in the United States, highlighting the growing popularity of golf as a recreational activity. The shift in consumer spending toward experiences over material goods has positioned golf as a favored outdoor activity that integrates fitness and social interaction. Initiatives such as the 'PIF Future Fairways' by the Public Investment Fund (PIF) and Golf Saudi further emphasize the sport's expanding appeal in regions like Saudi Arabia [1]Source: Public Investment Fund, "PIF and Golf Saudi launch PIF Future Fairways, showcasing the future of golf in Saudi Arabia", pif.gov.sa. The limited lifespan of golf gloves, 60-90 rounds for leather and 120-180 hours for synthetic materials, ensures recurring purchases as participation increases, supporting market growth. Additionally, government-backed entertainment complexes in the UAE reinforce golf's role as a lifestyle activity, sustaining demand even during economic uncertainties.

Innovations in breathable and moisture‑wicking materials

Innovations in breathable and moisture-wicking materials are significantly driving the growth of the global golf gloves market. Manufacturers are increasingly focusing on developing advanced materials that enhance player comfort and performance under varying environmental conditions. For instance, Callaway's Syntech 2025 utilizes FUSETECH synthetic layers with hydrophobic panels, providing a tactile experience comparable to cabretta leather while repelling moisture. Similarly, FootJoy's ProFLX integrates perforated mesh backs with leather palms, ensuring improved airflow without compromising grip, which is crucial for maintaining control during play. Vice Golf's Duro, designed specifically for tropical climates, becomes tackier when exposed to moisture, addressing the challenges posed by high humidity. These material innovations not only improve functionality but also cater to the growing demand for durable, high-performance golf gloves, making them a key driver in the market's expansion.

Rising global golf participation among all ages

Rising global golf participation across all age groups is a key driver for the growth of the global golf gloves market. In the United States, female on-course participation has reached unprecedented levels, with nearly eight million women actively playing golf. Women now account for a significant share of all on-course golfers in the U.S., a significant rise from around one-fifth a decade ago [2] Source: National Golf Foundation, "Golf Participation: Growing & Diversifying", ngf.org. This increasing participation among women highlights the need for product diversification, as manufacturers must address specific requirements such as tailored sizing and fit profiles for women. Furthermore, younger players are increasingly drawn to golf, with many showing a preference for gloves featuring fashion-forward designs and sustainable materials. These trends underscore the importance of innovation and customization in golf glove manufacturing to cater to the evolving demands of a diverse and expanding consumer base.

Technological enhancements improving grip and comfort

The integration of advanced technologies into golf gloves is emerging as a significant driver for the golf gloves market. Products like Umbrella Sports’ SmartGrip Pro, which incorporates sensors to monitor grip pressure and swing tempo, are enhancing user experience by providing actionable insights for performance improvement. Similarly, Bionic Gloves’ anatomical pad system, designed to redistribute pressure and extend product lifespan, reflects the growing demand for durability and functionality. The introduction of G-GRIP Pro at CES 2026, capable of analyzing ten swings to recommend grip-strength adjustments, further underscores the shift towards data-driven performance optimization. Additionally, the adoption of silicone micro-dot patterns and compression wrist zones to reduce fatigue and slippage highlights the market's transition from basic hand protection to solutions that offer measurable performance benefits. This trend is expected to drive innovation and growth in the market during the forecast period.

High pricing of premium leather gloves limits adoption

The high pricing of premium leather golf gloves limits their adoption, posing a restraint on the growth of the global golf gloves market. Cabretta leather gloves are widely recognized for their superior softness, fit, and grip, which cater to the preferences of professional and advanced players. However, these gloves are significantly more expensive compared to synthetic alternatives, making them less accessible to a broader consumer base. For example, Callaway Golf's Tour Authentic glove, crafted from ultra-soft cabretta leather, is positioned as a premium product and is priced considerably higher than standard gloves. Furthermore, premium leather gloves tend to wear out more quickly, especially in humid or wet conditions, necessitating frequent replacements. This increases the overall cost of ownership, further deterring price-sensitive consumers. As a result, beginners and casual golfers often prefer more affordable and durable synthetic options, which impacts the adoption rate of premium leather gloves in the market.

Seasonal demand fluctuations reduce year‑round sales

Seasonal demand fluctuations act as a restraint on the global golf gloves market by limiting consistent year-round sales. Golf, being an outdoor sport, is heavily influenced by weather conditions, with demand peaking during spring and summer in regions like North America and Europe. In colder months or during adverse weather conditions, the frequency of play declines, reducing the consumption of golf accessories, including gloves. Leading brands such as Callaway Golf and FootJoy typically experience higher sales during tournament seasons and favorable weather, while off-season demand remains subdued. This cyclical demand pattern creates challenges in inventory management, production planning, and revenue stability for manufacturers and retailers. Additionally, in regions with shorter golfing seasons, consumers purchase gloves less frequently, further impacting market growth. As a result, the seasonal nature of golf participation leads to uneven demand patterns, constraining the market's annual sales potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetic Materials Challenge Leather Dominance

Leather continues to dominate the golf gloves market, holding a significant 54.01% share in 2025. This segment remains the largest due to its strong preference among tour professionals who value the superior tactile feedback it provides. Leather gloves are often associated with premium quality and performance, making them a staple choice for serious golfers. However, their susceptibility to wear and tear in humid conditions limits their appeal in certain regions. Despite this, advancements in leather processing and treatments have helped maintain its relevance, ensuring its position as the leading segment in the market.

On the other hand, synthetic golf gloves are emerging as the fastest-growing segment, with a projected CAGR of 4.84% through 2031. This growth is particularly pronounced in regions like Southeast Asia, where high humidity accelerates the degradation of leather gloves. Synthetic gloves have gained traction due to innovations such as hydrophobic coatings and suede-microfiber blends, which enhance durability and mimic the feel of leather. Additionally, hybrid constructions, like Cobra’s Pur Tech 2026, combine cabretta leather palms with breathable synthetic backs, offering a balance of performance and affordability. These advancements have positioned synthetic gloves as a practical and increasingly popular choice among golfers, driving their rapid expansion in the market.

By End User: Women’s Uptick Outpaces Men’s Base

In 2025, men represented the largest segment in the golf gloves market, accounting for a substantial 72.68% share. This dominance can be attributed to the higher participation rates among male golfers globally, coupled with a wide range of product offerings tailored to their needs. The segment benefits from consistent demand, driven by both professional and recreational players, ensuring its continued prominence in the market. Additionally, established brands have maintained a strong foothold by catering to male preferences with durable materials and performance-enhancing features, further solidifying their market position.

Meanwhile, the women’s segment is projected to be the fastest-growing, with a CAGR of 5.77% during the forecast period. This growth is fueled by increasing female participation in golf across key regions such as the United States, Germany, India, and Saudi Arabia. Brands are actively addressing the unique preferences of female consumers by introducing products with customized sizing, pastel color options, and sustainable materials. For instance, companies like Bionic have launched women-specific SKUs featuring anatomical padding to reduce grip pressure, enhancing comfort and performance. These targeted innovations are expected to drive significant growth in the women’s segment, making it a key area of focus for market players.

By Category: Premium Tier Commands Growing Wallet Share

The mass-market gloves segment continues to lead the golf gloves market, holding a dominant 71.37% share. This segment's prominence stems from its ability to cater to a diverse group of golfers, particularly those who value affordability and functionality. These gloves are designed to provide reliable performance at accessible price points, making them a go-to choice for amateur and recreational players. Their widespread availability across retail channels and consistent demand ensure that the mass-market segment remains the backbone of the industry. This segment's stability and broad appeal make it a critical driver of the overall market's performance.

On the other hand, the premium-tier segment is emerging as the fastest-growing category, recording a strong CAGR of 6.03%, outpacing the overall market's growth rate. This growth is fueled by a noticeable shift in consumer preferences, with players increasingly seeking gloves that deliver measurable performance enhancements, such as better pressure relief and improved grip consistency. Additionally, the rise of golf tourism, a billion-dollar ecosystem, has introduced travelers to premium pro-shop assortments, further driving interest in high-end gloves. As the pricing of smart gloves becomes more competitive, the premium segment is poised for substantial revenue growth. Importantly, this expansion is expected to occur without cannibalizing the mass-market segment, highlighting the premium category's potential to carve out a larger share of the market while complementing existing offerings.

By Distribution Channel: Online Growth Challenges Offline Dominance

Offline retail continues to dominate as the largest distribution channel, accounting for 63.44% of the market share. These physical retail outlets serve as vital community hubs, where PGA professionals significantly influence consumer purchasing decisions. The tactile shopping experience, combined with expert guidance, makes offline retail a preferred choice for many customers. This channel remains essential for brands aiming to build trust and foster long-term relationships with their consumer base, particularly for products requiring fit validation or personalized recommendations.

Meanwhile, the online segment is the fastest-growing distribution channel, with a compound annual growth rate (CAGR) of 5.01%. This growth is propelled by the increasing popularity of direct-to-consumer models, seamless omnichannel fulfillment strategies, and the growing trust in micro-influencers. Online platforms are becoming increasingly sophisticated, with features like virtual sizing tools and flexible in-store pickup options. These innovations cater to first-time buyers seeking confidence in their purchases and loyal customers looking for convenient replenishment solutions. As a result, brands that effectively integrate these capabilities are well-positioned to capitalize on the expanding online market.

Geography Analysis

North America remains the largest segment in the golf gloves market, expected to account for 46.93% of the revenue by 2025. The region's leadership is driven by its affluent consumer base and a strong appetite for innovation. While Canada's shorter golf season limits overall market volume, Mexico's resort courses experience notable seasonal demand, primarily fueled by U.S. tourists. Manufacturers are leveraging North America as a strategic hub to introduce advanced products, such as smart gloves and recycled hybrids, aligning with the region's preference for premium and sustainable solutions. This combination of high purchasing power and openness to innovation solidifies North America's position as the commercial epicenter of the market.

Asia-Pacific is projected to be the fastest-growing segment, with a robust CAGR of 5.26% forecasted through 2031. The region's growth is underpinned by increasing golf participation, particularly in humid ASEAN markets, where demand for lightweight and breathable gloves is on the rise. Manufacturers who tailor their products to suit these climatic conditions are well-positioned to capture significant market share. Additionally, the expanding middle-class population and growing interest in golf as a recreational activity are key factors driving this growth. The region's dynamic economic development and rising disposable incomes further enhance its potential as a high-growth market for golf gloves.

Other regions, including Southern Europe, the Middle East and Africa, and South America, present diverse market dynamics. Southern Europe's mild winters attract Northern tourists, creating consistent demand for all-weather synthetic gloves. However, challenges such as fragmented languages and distribution networks necessitate localized marketing and packaging strategies. In the Middle East and Africa, South Africa's established golfing community supports steady replacement demand, while emerging markets like Nigeria and Egypt show promise due to their growing affluent urban populations. South America, meanwhile, faces structural constraints, with limited public golf courses restricting broader participation. In countries like Brazil and Argentina, golf remains an elite activity, and the market is expected to rely on affordable synthetic gloves until investments in public-sector or private-equity initiatives improve course accessibility and drive higher volumes.

Competitive Landscape

The golf gloves market exhibits high concentration with established players leveraging brand loyalty and performance differentiation to maintain market positions, though direct-to-consumer disruption and technological innovation create opportunities for smaller contenders to capture niche segments. Legacy leaders, such as Acushnet (FootJoy) and Callaway, utilize tour visibility, extensive fitting networks, and multi-channel distribution to protect their market share. Acushnet's 2023 revenue of USD 2.38 billion underscores the robust spending power of dedicated golfers.

Private capital is reshaping the landscape: L. Catterton's investment in L.A.B. Golf and Oakley Capital's stake in Vice Sporting Goods highlight a pronounced interest in scalable niche innovators. These investments reflect a growing trend of financial backing for companies that cater to specific consumer needs, enabling them to expand their market presence. Direct-to-consumer specialists, capitalizing on social media economics, sidestep costly endorsements and traditional retail rents, but sustaining this edge requires relentless digital storytelling. Effective use of digital platforms allows these companies to engage directly with consumers, build brand loyalty, and reduce overhead costs, giving them a competitive advantage in a crowded market.

Technological hurdles, from smart-sensor integration to the demand for PFAS-free synthetics, call for hefty research and development investments. These advancements are crucial for meeting evolving consumer preferences and regulatory requirements. Yet, navigating the complexities of regulatory compliance can act as a protective shield, deterring new entrants and safeguarding established players. TaylorMade's new plant in South Korea showcases a move towards vertical integration, bolstering its manufacturing capabilities, securing its supply chain, and cutting lead times. This strategic move ensures greater control over production processes and enhances responsiveness to market demands. With the industry's cyclical demand, adept inventory control becomes crucial, offering global players a significant operational edge. Efficient inventory management allows companies to minimize waste, optimize resources, and meet seasonal demand fluctuations effectively.

Golf Gloves Industry Leaders

-

FootJoy

-

Callaway Golf Company

-

TaylorMade Golf Company

-

Srixon / Cleveland Golf

-

Mizuno Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Exo Golf launched the EXO Patented Golf Glove, incorporating Zyntech's nanocell technology. The glove was designed to improve the hand-to-club connection, enhance control and consistency, and optimize energy transfer upon impact. This product established a new benchmark in modern performance golf gloves.

- March 2026: Golfvante launched the 804 Edition, a premium golf glove designed for players seeking maximum feel, stylish design, and a strong identity. Made from ultra-thin AAA-grade cabretta leather, the 804 Edition featured a slim fit and a tastefully standout design, catering to golfers who valued both precision and character in their game.

- March 2026: Golfvante launched one of Sweden's most comprehensive collections of golf gloves designed for children and juniors. The five new models addressed various needs, ranging from budget-friendly training gloves to premium options made from cabretta leather.

Global Golf Gloves Market Report Scope

Golf gloves are essential sports accessories designed to improve grip, provide comfort, and enhance performance for golfers by ensuring better club control and reducing slippage during play. The global golf gloves market is segmented by product type, end user, category, distribution channel, and geography. By product type, the market is categorized into leather, synthetic, and other materials. By end user, it is divided into men, women, and kids. By category, the market is classified into mass and premium segments. By distribution channel, it is segmented into online retail stores and offline retail stores. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. Market sizing and forecasts for each segment are provided in terms of value (USD).

| Leather |

| Synthetic |

| Others |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Leather | |

| Synthetic | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Kids | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will women’s demand for gloves grow through 2031?

The women’s segment is forecast to register a 5.77% CAGR, outpacing the overall Golf Gloves market as female participation expands in North America, Europe, and the Middle East.

Which material type will add the most absolute revenue?

Advanced synthetic gloves will add the most, posting a 4.84% CAGR on top of leather’s larger base, thanks to durability and humidity resistance.

What is driving premium glove uptake?

Verified performance gains, such as 40% pressure reduction, sensor-based swing data, and recycled hybrid fabrics—justify higher prices and fuel a 6.03% premium-tier CAGR.

Why is Asia-Pacific considered the growth engine?

An expanding middle class and government-funded golf entertainment venues push the region to a projected 5.26% CAGR through 2031.

Page last updated on: