Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.87 Billion |

| Market Size (2026) | USD 9.25 Billion |

| Market Size (2031) | USD 11.41 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Home Furniture Market Analysis by Mordor Intelligence

The Mexico home furniture market size was valued at USD 8.87 billion in 2025 and estimated to grow from USD 9.25 billion in 2026 to reach USD 11.41 billion by 2031, at a CAGR of 4.29% during the forecast period (2026-2031). Rising household formation, a government pledge to build 1 million new homes with zero-interest mortgages and accelerating near-shoring investment all converge to lift demand across every price tier of residential furnishings. Rapid digital adoption, e-commerce already equals 23% of total retail sales, reshapes distribution economics and forces even legacy furniture chains to double down on omnichannel capabilities. At the same time, temporary tariffs of 5%-50% on 544 HS codes shield local producers from low-cost Asian imports, balancing consumer price sensitivity with industrial policy aims[1]Source: Office of Textiles & Apparel, “Temporary Tariffs on Furniture HS Codes,” trade.gov. Sustainability considerations—from FSC certification uptake to modular designs that suit compact apartments—are now mainstream purchase criteria, especially among millennials and Gen Z. Supply-side consolidation, exemplified by La-Z-Boy’s production streamlining and Man Wah’s 2.5 million-square-foot facility, further tightens value-chain control and improves lead-time reliability.

Key Report Takeaways

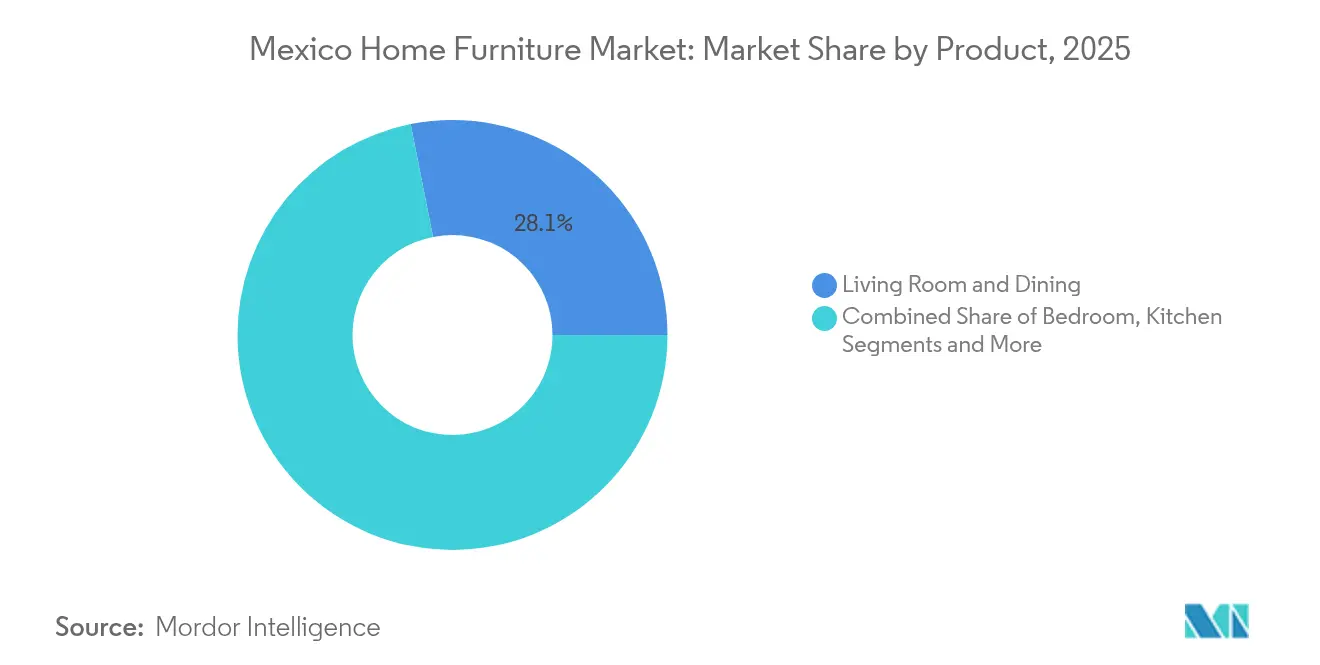

- By product category, Living Room & Dining Furniture captured 28.12% of Mexico home furniture market share in 2025, while Bedroom Furniture is projected to post the fastest 6.85% CAGR through 2031.

- By material, wood commanded 57.10% share of the Mexico home furniture market size in 2025, whereas Plastic & Polymer solutions are forecast to lead growth at an 7.75% CAGR to 2031.

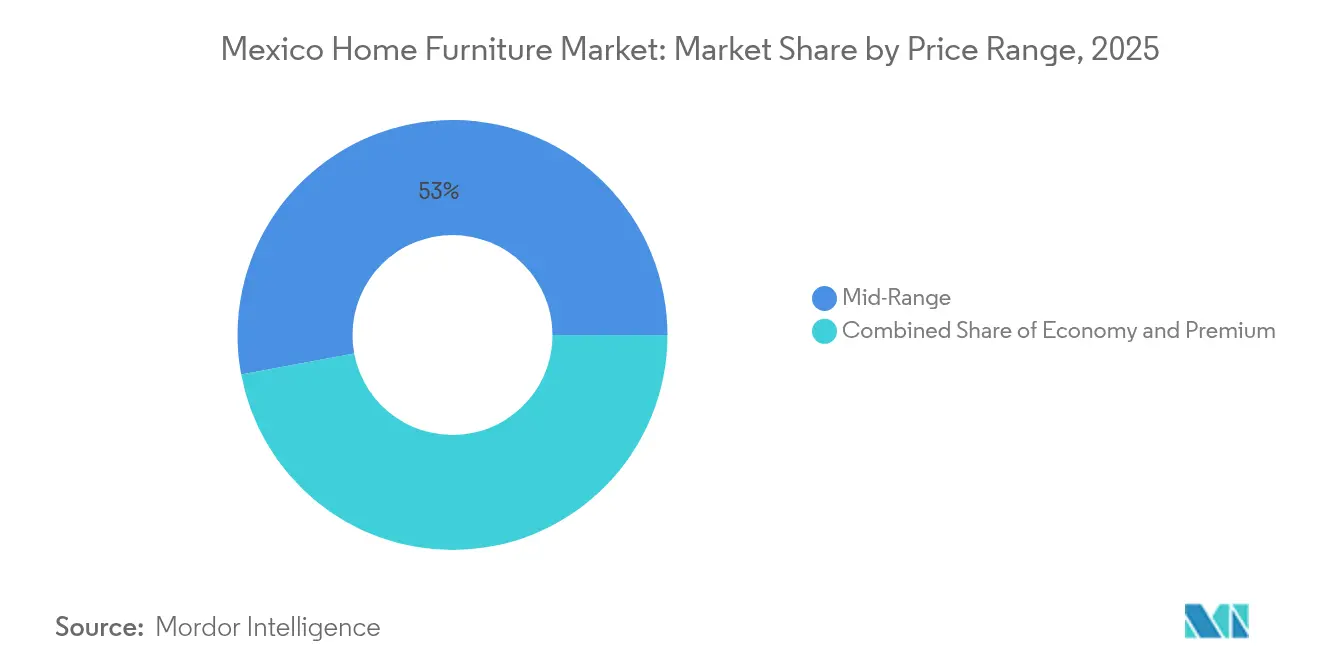

- By price band, mid-range products accounted for 52.95% revenue share in 2025, while premium furniture is set to expand at a 6.15% CAGR over the forecast horizon.

- By distribution channel, specialty furniture stores retained 43.85% share of the Mexico home furniture market size in 2025, yet online channels are advancing at an 8.35% CAGR through 2031.

- By geography, Central Mexico held 39.10% of 2025 revenue, whereas the Mexico City Metro area is projected to record a 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing middle-class disposable income | +1.2% | National, strongest in Central Mexico and Mexico City Metro | Medium term (2-4 years) |

| Housing construction & renovation boom | +1.8% | National, with concentration in Central and Northern Mexico | Short term (≤ 2 years) |

| E-commerce and omni-channel expansion | +0.9% | National, led by Mexico City Metro and urban centers | Medium term (2-4 years) |

| Remote-work driven demand for ergonomic home-office furniture | +0.7% | Central Mexico, Mexico City Metro, Northern industrial centers | Short term (≤ 2 years) |

| Near-shoring-led inflow of expatriates boosting furnished rentals | +0.5% | Northern Mexico, Central Mexico industrial corridors | Medium term (2-4 years) |

| INFONAVIT credit programs enabling furniture purchases | +0.8% | National, with higher impact in Central and Southern Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Middle-Class Disposable Income

Household net-adjusted disposable income reached USD 16,269 in 2024 and continues to climb, positioning the emerging middle class as the core customer cohort for the Mexico home furniture market[2]Source: Mexico Desk, “Middle-Class Income Trends,” Santander Trade, santandertrade.com. Urbanization stands at 80% and reinforces an appetite for stylish yet functional pieces that fit smaller dwellings without sacrificing quality. Cash still dominates payment preferences, but expanding consumer credit, from retailer cards to fintech loans, broadens financing access for mid-range and premium purchases. Younger demographics, reflected in a median age of 29.8 years, look for products that solve space constraints and resonate with sustainability ideals. Combined, these factors underpin sustained demand growth across virtually every product category and price tier.

Housing Construction & Renovation Boom

President Claudia Sheinbaum’s plan to add 1 million homes financed by MXN 600 billion creates a direct furniture-multiplication effect. Government-backed pipelines totaling 55,000 projects scheduled for completion by March 2025 let manufacturers forecast volumes with more precision. Real-estate GDP growth of 15.6% in 2023 confirms sector momentum that spills into furnishings, appliances, and décor demand. Existing homeowners are also upgrading interiors as Mexico City property prices jumped 30% over five years, feeding a renovation wave. A structural housing deficit of 2.8 million units means this driver will sustain well beyond the current administration’s term.

E-commerce and Omni-channel Expansion

Digital channels produced USD 45 billion in gross merchandise value during 2023 and already cover the full national territory thanks to improved last-mile logistics. IKEA logged 42% online sales growth and now ships to all 32 states from a single distribution center, setting a performance benchmark. Liverpool multiplied online sales 5.1 times during the pandemic and captured 80% of total revenue via digital touchpoints at peak, proving omnichannel is no longer optional. Gen Z and Millennial Buyers prioritize convenience, transparent delivery windows, and easy returns, pressuring legacy retailers to revamp tech stacks. Cash-on-delivery and Oxxo-store payment codes bridge Mexico’s unbanked segments, enabling a broader audience to participate in online furniture purchasing.

Remote-Work Driven Demand for Ergonomic Home-Office Furniture

Work-from-home remains sticky even after pandemic restrictions, and multinational near-shoring brings thousands of knowledge workers who expect enterprise-grade desks, chairs, and storage solutions. Suburban migration trends enlarge floor plans and allow consumers to dedicate full rooms to office setups, lifting average ticket sizes. Condos with coworking amenity floors inspire purchases of modular or mobile furniture that toggles between living and working modes. Corporate procurement divisions are furnishing distributed employees’ homes, opening new B2B revenue streams for manufacturers. Given Mexico’s advantage in time-zone alignment with the United States, remote work adoption is likely to intensify, keeping this demand driver active in the short term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile lumber & input costs | -0.8% | National, with higher impact in Northern Mexico manufacturing centers | Short term (≤ 2 years) |

| Influx of low-cost Asian imports | -1.1% | National, particularly affecting Central and Southern Mexico price-sensitive segments | Medium term (2-4 years) |

| Freight & border-crossing bottlenecks | -0.6% | Northern Mexico border regions, with spillover effects to Central Mexico distribution hubs | Short term (≤ 2 years) |

| Fragmented domestic manufacturing productivity | -0.9% | National, with concentration in traditional furniture clusters in Central and Southern Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Lumber & Input Costs

Around 30%-70% of Mexican timber may be illegally sourced, subjecting legitimate manufacturers to unpredictable raw-material swings that squeeze margins[3]Source: Kerstin Canby, “Illegality in Mexico’s Timber Supply,” Forest Trends, forest-trends.org. Community forestry enterprises control 80% of domestic forests but face cumbersome regulations, limiting their ability to scale output efficiently. Most sawnwood is therefore imported, exposing producers to global price gyrations and currency volatility. Rising polyurethane demand from automotive and construction further competes for foam inputs essential to upholstered furniture manufacturing. Without vertical integration or certified-wood sourcing partnerships, factories risk profit erosion and delivery delays.

Influx of Low-Cost Asian Imports

Dedicated China-to-Mexico shipping lanes reduce transit times and freight rates, enabling overseas suppliers to undercut local prices. Although temporary tariffs of up to 50% aim to counteract dumping, uncertainty over long-term protection complicates investment planning. Online marketplaces such as Shein face scrutiny for tax avoidance, yet their presence proves that Mexican consumers will buy foreign furniture if price and convenience align. Domestic clusters in Chihuahua and Jalisco struggle with outdated machinery and fragmented supply chains, limiting their ability to achieve cost parity. If productivity gaps persist, local players could cede share in economy and mid-range segments despite tariff shields.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Living Room Dominance Drives Market

Living Room & Dining Furniture generated 28.12% of Mexico home furniture market share in 2025, reflecting cultural norms that place family gathering spaces at the heart of household budgets. Bedroom Furniture, while smaller in 2025, is forecast to advance at a 6.85% CAGR, outpacing all other categories as new-build homes and wellness trends emphasize quality sleep environments. Kitchen and bathroom pieces benefit from renovation activity tied to 30% property-price appreciation in Mexico City, spurring upgrades that improve resale values. Home-office furniture, once niche, now commands recurring demand from hybrid workers and near-shored expatriates who will not compromise on ergonomics. Outdoor and specialty items, including children’s and accessibility furniture, round out portfolios and enable retailers to capture incremental add-on sales.

The Mexico home furniture market size for Living Room & Dining items is set to grow steadily given larger ticket values and repeat purchase cycles tied to style obsolescence. Bedroom sets gain momentum from zero-interest mortgage recipients who furnish multiple rooms at once, raising average order values. Growth in the Mexico home furniture market also stems from developers pre-installing fitted kitchens, which sparks after-market demand for complementary tables, stools, and storage. Premium suppliers leverage VR visualization tools so customers can preview entire room packages, shorten sales cycles and raising conversion rates. Overall, product-level dynamics illustrate how functional requirements and lifestyle aspirations dovetail to sustain multi-segment expansion.

By Material: Wood Heritage Meets Polymer Innovation

Wood retained 57.10% market share in 2025, underscoring Mexico’s legacy craftsmanship and consumer affinity for warm aesthetics that suit colonial and contemporary interiors alike. Yet plastic and polymer furniture is projected to log an 7.75% CAGR, reflecting urban buyers’ needs for lightweight, stackable, and moisture-resistant solutions that fit compact apartments. Metal pieces address both industrial and minimalist décor preferences, with rising adoption in loft-style conversions in Guadalajara and Monterrey. Composite and experimental materials, from recycled PET to mushroom-based leather, are moving from prototype to pilot scale as ESG regulations loom. FSC-certified wood now commands price premiums, signaling that legality verification can differentiate brands among environmentally conscientious shoppers.

The Mexico home furniture market size for plastic and polymer goods should accelerate as polyurethane output rises 7% annually, boosting local availability of high-density foams and molded shells. Producers hedge timber volatility by migrating entry-level lines to engineered substrates, insulating margin against raw-wood price shocks. Simultaneously, the Mexico home furniture market shows that wood still reigns in premium tiers where tactile richness justifies higher spend, especially when provenance is traceable. Hybrid constructions-wood frames with polymer components-offer compelling durability-cost ratios, keeping both material groups relevant. Expect innovation clusters near petrochemical hubs in Veracruz to spearhead next-generation polymers for furniture applications.

By Price Range: Mid-Range Stability Anchors Premium Growth

Mid-range SKUs dominated with 52.95% revenue share in 2025, aligning with average disposable income levels and retailer credit programs that extend purchase power over 12-24 months. Premium categories, however, are on a 6.15% CAGR trajectory through 2031 as property gentrification and expatriate influx raise design expectations in zones like Polanco, Roma, and Santa Fe. Economy lines remain essential for low-income households and social housing beneficiaries, yet inflationary pressures could squeeze already thin margins unless producers adopt lean manufacturing techniques. Retail analytics show consumers increasingly treat furnishings as lifestyle statements, not mere necessities, driving upsell opportunities into premium finishes and smart-home integrations. Loyalty programs at Liverpool and Coppel further encourage trade-up behavior by awarding points redeemable for higher-ticket furniture.

Mexico home furniture market share shifts toward premium will also benefit from BNPL (buy-now-pay-later) fintech options that bypass traditional credit checks. Meanwhile, developers of build-to-rent portfolios prefer durable, mid-range fixtures that minimize replacement costs across multiple turnovers. On the supply side, vertical brands like IKEA blur traditional price tiers by offering premium-looking designs at accessible price points, forcing domestic peers to differentiate on service and customization. Data-driven inventory planning reduces markdown risk, vital in a market where promotional calendars can erode perceived value. The Mexico home furniture industry therefore balances price segmentation fluidly, with middle-class expansion underpinning volume and premiumization driving profit.

By Distribution Channel: Specialty Stores Navigate Digital Disruption

Specialty furniture stores continued to hold 43.85% of 2025 revenue by curating showrooms where tactile inspection and design advice boost conversion rates. Yet online platforms will post the fastest 8.35% CAGR because they eliminate geographic constraints and showcase extended assortments impossible to stock in physical outlets. Home centers such as Home Depot capture renovation-linked purchases, bundling tools, lumber, and ready-to-assemble cabinets in one stop. Direct-to-consumer startups exploit social-media storytelling and doorstep delivery to gain share among digital-native shoppers. Legacy chains are therefore racing to adopt click-and-collect, AR visualization, and same-day shipping to stay relevant.

The Mexico home furniture market size attributed to e-commerce could double before 2031 if internet penetration sustains its current 4% annual growth. IKEA’s single DC model illustrates economies of scale, while Liverpool’s 80% digital-sales peak demonstrates demand elasticity once friction is removed. For specialty outlets, experiential retail-coffee bars, interior-design workshops, VR booths-adds value that pure players cannot replicate. Payment innovation such as digital wallets accepted at Oxxo or cash-to-code systems widens the funnel for unbanked customers. Ultimately, winning retailers will merge data from both channels to personalize offers and optimize inventory turns.

Geography Analysis

Central Mexico generated 39.10% of 2025 sales, leveraging Mexico City’s density, purchasing power, and multimodal connectivity that speed inbound materials and outbound deliveries. The region enjoys the nation’s most diversified customer base, allowing retailers to balance premium showrooms in affluent districts with value-oriented formats in surrounding suburbs. Government-backed housing and zero-interest mortgages concentrate heavily here, reinforcing a reliable demand floor for volume-driven categories. E-commerce benefits from fulfillment hubs clustered around Mexico City’s ring roads, cutting last-mile costs and enabling 24-hour delivery promises. Taken together, Central Mexico forms the strategic anchor of the Mexico home furniture market.

The Mexico City Metro area itself is projected to grow at a 6.55% CAGR to 2031, fueled by apartment densification and a 30% five-year spike in property prices that incentivizes interior upgrades. Developers integrate coworking lounges and rooftop gardens, prompting demand for modular, multi-functional pieces that shift between leisure and work. Expatriate arrivals tied to near-shoring further boost furnished-rental demand and raise quality expectations. Digital natives here embrace virtual showrooms, letting overseas buyers furnish investment condos sight unseen. Therefore, the Mexico home furniture market size in the capital is poised for outsized gains relative to national averages.

Northern Mexico rides the near-shoring wave, capturing industrial FDI that could surpass USD 60 billion by 2027 and create thousands of white-collar jobs. Border-adjacent cities like Tijuana and Monterrey require office and residential furnishings for relocated corporate staff, pushing demand for ergonomic seating and turnkey packages. Logistics corridors into the United States also enable exporters to ship finished furniture northbound under USMCA rules, supporting factory utilization rates. Retail footprints expand in tandem, with Home Depot plotting 165 total Mexican stores to serve both contractors and households. Consequently, Northern Mexico emerges as the secondary growth pole within the Mexico home furniture market.

Competitive Landscape

Competition is fragmented yet intensifying as global and domestic heavyweights deploy capital to seize first-mover advantages in omnichannel retail. IKEA’s USD 600 million program placed Mexico’s largest store in Guadalajara and established statewide e-commerce coverage, demonstrating that scale and supply-chain mastery can overcome legacy brand recognition. Home Depot’s USD 1.3 billion pledge aims for 100% local sourcing by 2028, strengthening backward linkages and boosting the Mexico home furniture market’s manufacturing base. Coppel leverages an 88% credit-sales model to court underserved consumers, investing MXN 14.2 billion to open 100 new stores and upgrade digital infrastructure in 2025. Liverpool, which saw online revenue jump fivefold during the pandemic, now operates unified inventory pools, enabling ship-from-store within two hours in major metros[4]Source: Corporate Release, “Liverpool Reports Digital Revenue Surge,” El Puerto de Liverpool, elpuertoliverpool.mx. .

Strategic differentiation increasingly revolves around speed, service, and sustainability rather than sheer assortment breadth. White-glove delivery and assembly services serve as key loyalty drivers for premium buyers unwilling to handle flat-pack logistics. Brands tout FSC certification and recycled-material content to appeal to eco-conscious millennials, with early adopters commanding price premiums up to 15%. B2B channels gain relevance as corporate clients furnish distributed workforces, creating volume contracts for desks, task chairs, and storage. Manufacturers streamline footprints—La-Z-Boy consolidated North American recliner production into its Nuevo León facility—to cut overhead and meet rapid-ship commitments.

Digital capabilities separate leaders from laggards: AI-driven recommendation engines lift average order values, while AR tools reduce return rates by letting shoppers visualize scale and style in real spaces. Partnerships with fintechs allow split-payment options that expand basket sizes without raising default risk. Market entrants focusing on niche propositions—such as modular pet-friendly sofas or space-saving bunk systems—gain traction through social commerce channels. Retailers that fail to modernize run the risk of margin erosion as price transparency widens and import competition persists. Overall, the Mexico home furniture market trends toward gradual consolidation, rewarding firms that pair operational excellence with customer-centric innovation.

Mexico Home Furniture Industry Leaders

IKEA México

El Puerto de Liverpool

Coppel

Walmart de México y Centroamérica

Muebles Dico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mabe allocated USD 668 million to expand appliance manufacturing capacity, indirectly boosting fitted-kitchen and utility-furniture demand.

- March 2025: Walmart de México y Centroamérica announced MXN 125 billion (USD 6 billion) in 2025 capex for new store formats and supply-chain upgrades that will add 5,500 jobs and enhance home-goods offerings.

- January 2025: Home Depot confirmed a USD 1.3 billion investment plan covering 2025-2030, targeting 165 total Mexican stores and 100% domestic sourcing by 2028, with 20,000 jobs to be created.

- January 2025: Coppel approved MXN 14.2 billion (USD 690 million) for 100 additional stores and e-commerce enhancements aimed at credit-dependent households.

Mexico Home Furniture Market Report Scope

Household furniture encompasses all movable items used to furnish a home, including chairs, tables, sofas, and mattresses. This report highlights key international players in the Mexican home furniture market. While a few dominant players hold significant market shares, mid-sized and smaller companies are expanding their presence. These companies are securing new contracts and exploring untapped markets owing to technological advancements and product innovations.

The Mexican home furniture market is segmented by material into wood, metal, plastic, and other materials; type into kitchen furniture, living-room and dining-room furniture, bedroom furniture, and other furniture; and distribution channel into supermarkets and hypermarkets, specialty stores, online stores, and other distribution channels. The report offers market sizes and forecasts for the Mexican home furniture market in value (USD) for all the above segments.

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home-Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Channels |

By Geography

| Northern Mexico |

| Central Mexico (incl. Mexico City) |

| Southern Mexico |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home-Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Channels | |

| By Geography | Northern Mexico |

| Central Mexico (incl. Mexico City) | |

| Southern Mexico |

Key Questions Answered in the Report

How large is the Mexico home furniture market in 2026?

The market is valued at USD 9.25 billion in 2026 and is projected to reach USD 11.41 billion by 2031.

What is the expected growth rate for Mexican home furniture sales?

Revenue is forecast to rise at a 4.29% CAGR between 2026 and 2031, underpinned by housing construction and e-commerce expansion.

Which product segment is growing fastest?

Bedroom furniture leads with a 6.85% CAGR because new home deliveries and sleep-wellness trends spur higher-value purchases.

Why are online channels gaining share in Mexican furniture retail?

E-commerce already equals 23% of total retail sales thanks to nationwide delivery networks, cash payment options, and omnichannel innovations.

Page last updated on: