GCC Swollen Knee Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

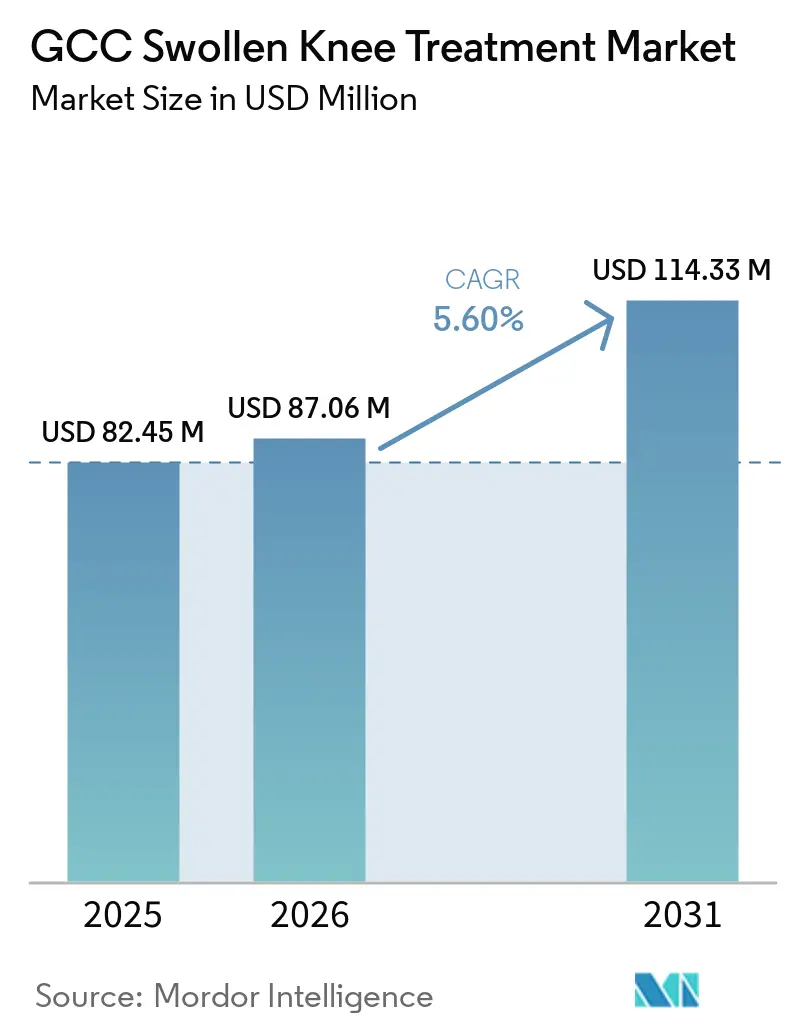

| Base Year Market Size (2025) | USD 82.45 Million |

| Market Size (2026) | USD 87.06 Million |

| Market Size (2031) | USD 114.33 Million |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Swollen Knee Treatment Market Analysis by Mordor Intelligence

The GCC Swollen Knee Treatment Market size is expected to increase from USD 82.45 million in 2025 to USD 87.06 million in 2026 and reach USD 114.33 million by 2031, growing at a CAGR of 5.60% over 2026-2031.

The GCC swollen knee treatment market is driven by persistent health challenges and the expansion of treatment facilities, particularly in orthopedics, rehabilitation, and specialized outpatient care. Rising knee osteoarthritis cases in Bahrain and the UAE highlight a growing disease burden, leading to an increase in diagnosed and treated cases across the region. Elevated obesity and diabetes rates are further expanding the patient pool, as joint swelling is increasingly linked to chronic inflammatory pathways requiring ongoing clinical management. Private orthopedic and sports medicine clinics are increasing access to injections, rehabilitation, and follow-up care, shifting the market away from a hospital-centric model. Additionally, factors such as insurance expansion, digital follow-up tools, reliance on imported products, and inconsistent treatment standards are influencing the pace at which demand converts into paid care episodes in the GCC swollen knee treatment market.

Key Report Takeaways

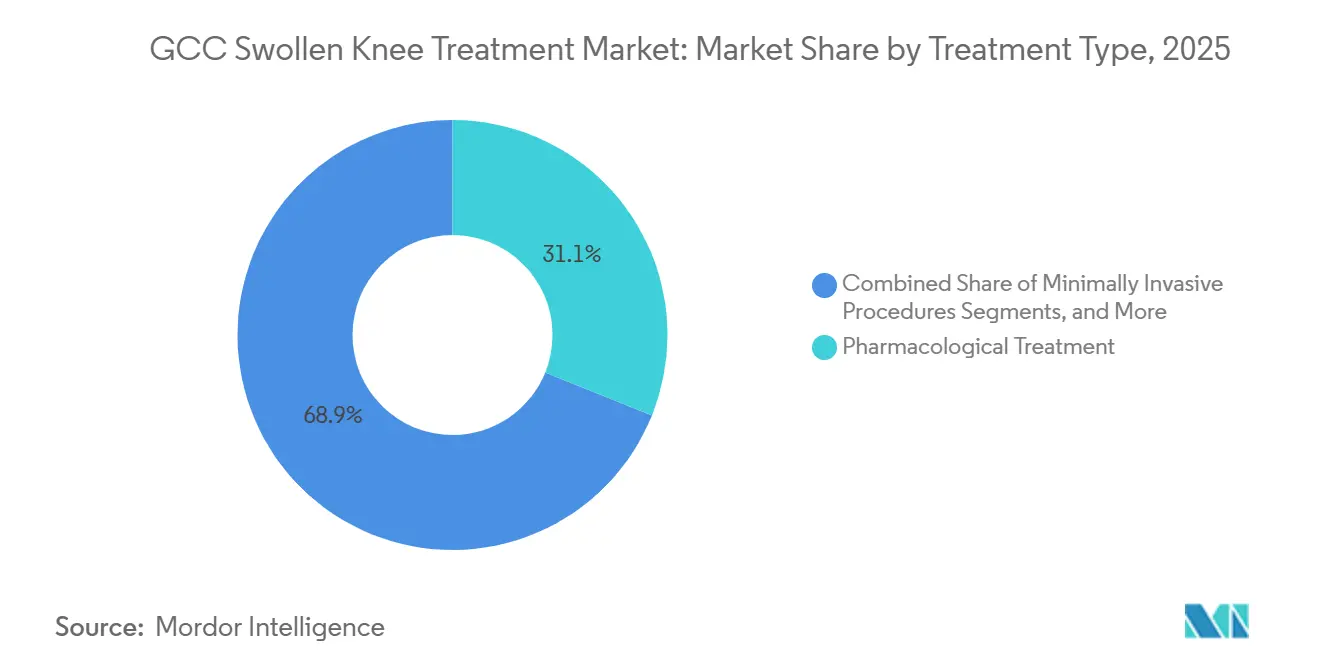

- By treatment type, pharmacological treatment led with 31.1% share in 2025, while minimally invasive procedures are forecasted to grow at a 5.98% CAGR through 2031 in the GCC swollen knee treatment market.

- By cause or clinical indication, osteoarthritis accounted for 32.4% of the GCC swollen knee treatment market size in 2025, while sports injury is projected to expand at a 6.25% CAGR through 2031.

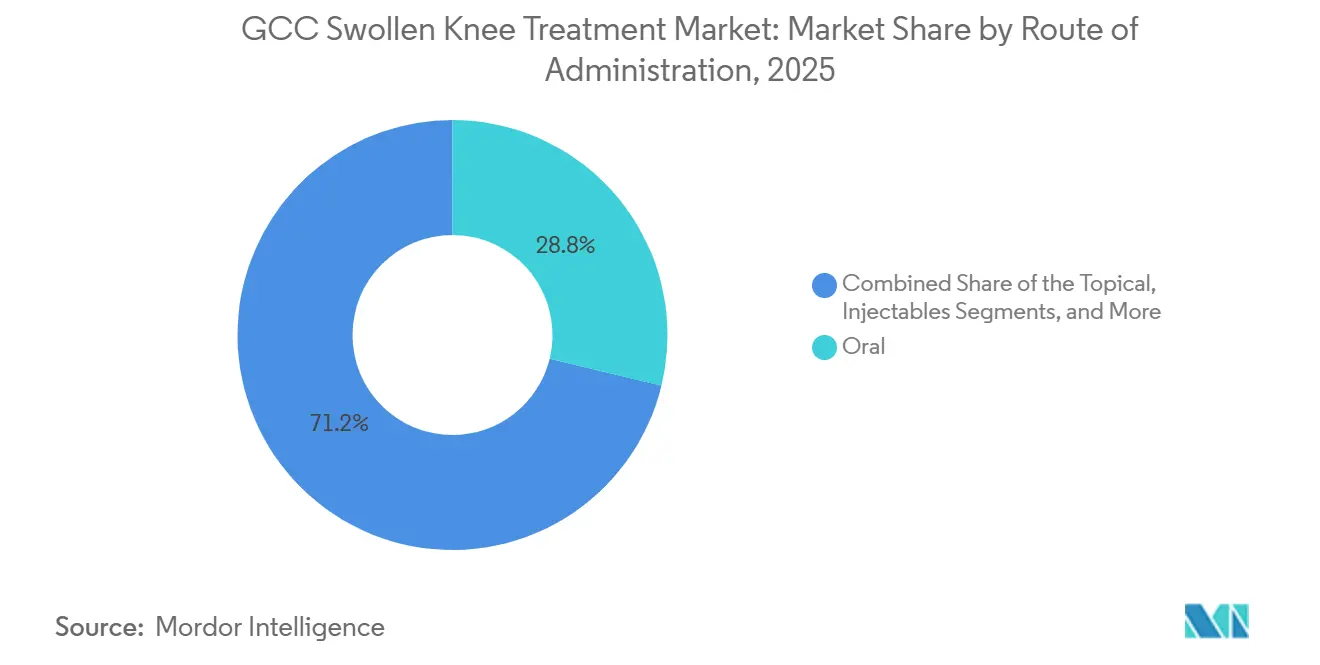

- By route of administration, oral therapies held 28.77% of the GCC swollen knee treatment market size in 2025, while injectable routes are forecasted to rise at a 6.78% CAGR through 2031.

- By end user, hospitals accounted for 35.88% of the GCC swollen knee treatment market share in 2025, while orthopedic and sports medicine clinics are expected to post the highest CAGR of 7.44% through 2031.

- By geography, Saudi Arabia held 26.45% of the GCC swollen knee treatment market share in 2025, while the UAE is projected to record the fastest growth at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Swollen Knee Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising knee osteoarthritis burden across GCC countries | +1.3% | All GCC countries, concentrated in Saudi Arabia, the UAE, and Bahrain | Long term (≥ 4 years) |

| Growth in obesity and diabetes linked to joint inflammation | +1.2% | All GCC countries, with highest impact in Saudi Arabia and Kuwait | Long term (≥ 4 years) |

| Expansion of private orthopedic and sports medicine clinics | +0.9% | UAE and Saudi Arabia primarily, with spillover to Qatar and Kuwait | Medium term (2-4 years) |

| Wider adoption of minimally invasive injection therapies | +0.8% | GCC-wide, with early gains in the UAE and Saudi Arabia | Medium term (2-4 years) |

| Stronger health insurance penetration for specialist care | +0.7% | UAE and Saudi Arabia, expanding into Oman and Bahrain | Short term (≤ 2 years) |

| Digital triage and tele-rehabilitation supporting follow-up care | +0.4% | Saudi Arabia and the UAE first, expanding across the GCC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Knee Osteoarthritis Burden Across GCC Countries

Knee osteoarthritis (OA) in the GCC is no longer confined to the elderly, impacting both national and expatriate populations. Women often face a higher burden, and working-age adults are entering treatment earlier. Between 1990 and 2024, Bahrain and the UAE recorded some of the steepest global increases in knee OA incidence.[1]Emirates Hospitals Group, “PRP Injection Package for Knee, Elbow or Joint in Dubai,” Emirates Hospitals, emirateshospitals.ae This long-term trend is driving repeated demand for analgesics, injections, rehabilitation, and imaging. As orthopedic access improves, the GCC swollen knee treatment market is expected to capture a larger share of untreated cases.

Growth In Obesity And Diabetes Linked To Joint Inflammation

High obesity and diabetes rates in the GCC are expanding the patient base for swollen knee treatments through mechanical stress and inflammation. From 2020 to 2024, over 65% of Saudi adults were classified as overweight or obese. In 2024, the MENA region had 84.7 million adults with diabetes, with a prevalence of 17.6%.[2]Anika Therapeutics, “Anika Therapeutics Touts $3B TAM, Cingal & Hyalofast Growth Plans at Canaccord MSK Conference,” The Lincolnian Online, thelincolnianonline.com These conditions complicate treatment and follow-up care, increasing demand for precise dosing and specialist oversight in the GCC swollen knee treatment market.

Expansion Of Private Orthopedic And Sports Medicine Clinics

Private investments are transforming care delivery in the GCC, expanding access to swollen knee treatments. In 2025, Burjeel Holdings enhanced its Saudi rehabilitation network, while the Emirates Growth Fund acquired a minority stake in Tarmeem Healthcare, which serves over 20,000 patients annually. Ambulatory orthopedic sites are improving efficiency and access to outpatient care, reducing reliance on tertiary hospitals for routine interventions in the GCC swollen knee treatment market.

Wider Adoption Of Minimally Invasive Injection Therapies

Minimally invasive procedures are the fastest-growing segment in the GCC swollen knee treatment market, with a projected CAGR of 5.98% through 2031. Clinicians increasingly prefer viscosupplementation and platelet-rich plasma (PRP) as alternatives to surgery. A 2025 meta-analysis showed leukocyte-poor PRP outperformed hyaluronic acid in knee OA outcomes. Enhanced injection accuracy and follow-up systems are improving adherence to repeat procedures, further driving growth in the GCC market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited local clinical standardization for swollen knee pathways | -0.5% | All GCC countries, with sharper impact in Oman and Bahrain | Short term (≤ 2 years) |

| High out-of-pocket cost for repeated injection-based care | -0.7% | Qatar, Kuwait, Oman, and Bahrain, especially where specialist coverage is thinner | Medium term (2-4 years) |

| Dependence on imported orthopedic and injectable products | -0.4% | All GCC countries | Long term (≥ 4 years) |

| Patient preference for conservative self-medication before specialist care | -0.4% | All GCC countries, strongest among lower-income expatriate groups | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Local Clinical Standardization For Swollen Knee Pathways

Inconsistent clinical standards across the GCC hinder efficient patient treatment. Referral practices vary significantly, leading to different treatment approaches for similar cases. This inconsistency impacts the adoption of premium therapies. Regulatory fragmentation further complicates product approvals and reimbursement processes, creating challenges for suppliers, especially with newer treatments. Without standardization, the GCC swollen knee treatment market will remain below its potential.

High Out-Of-Pocket Cost For Repeated Injection-Based Care

Repeated injection treatments are financially challenging for many patients, particularly where private insurance offers limited coverage. In Riyadh, PRP sessions cost between SAR 700 and SAR 4,000 (USD 186.7 to USD 1,066.7), while Dubai hospitals charge approximately AED 2,200 (USD 599.5). These costs increase with multiple sessions or ongoing therapy. Although coverage is better in the UAE and Saudi Arabia, affordability remains a key barrier, limiting market expansion despite strong clinical interest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Pharmacological Dominance Meets A Procedural Pivot

In 2025, pharmacological treatments accounted for 31.1% of the GCC swollen knee treatment market, highlighting the reliance on drug-based management for early and mid-stage care. Oral NSAIDs, topical diclofenac, and hospital-administered analgesics dominate due to their established use in primary care, emergency settings, and outpatient follow-ups. Corticosteroids remain significant but are used cautiously in diabetic patients due to potential complications in glucose management. Non-pharmacological treatments are gaining traction with expanded rehabilitation networks, while surgical treatments are shifting towards minimally invasive arthroscopy and shorter recovery pathways.

Minimally invasive procedures are projected to grow at a 5.98% CAGR through 2031, driven by physician acceptance of viscosupplementation and PRP, improved imaging-guided delivery, and patient preference for non-surgical options. These procedures align with ambulatory care economics, offering faster delivery and higher per-episode value. Anika Therapeutics reported 16% growth in international osteoarthritis pain management revenue in 2024, supported by geographic expansion into markets like the GCC. This trend is reshaping the treatment mix, moving care towards planned outpatient procedures over repeat symptomatic medication.

By Cause Or Clinical Indication: Osteoarthritis As Anchor, Sports Injury As Growth Engine

Osteoarthritis led the GCC swollen knee treatment market in 2025 with a 32.4% share, driven by obesity trends, an aging population, and improved early diagnosis of degenerative diseases. Obesity-related cytokines like leptin and TNF-α are linked to synovial inflammation, intensifying some cases through metabolic pathways. Rheumatoid arthritis and other inflammatory conditions, though smaller in volume, require complex biologic and specialist care. Secondary cases like bursitis, tendinitis, and post-traumatic swelling remain significant, especially in labor-intensive sectors, ensuring a diverse clinical mix in the market.

Sports injuries are forecasted to grow at a 6.25% CAGR from 2026 to 2031, making them the fastest-growing indication in the GCC swollen knee treatment market. This growth is fueled by investments in youth sports, organized athletic participation, and treatments for ligament injuries and training-related swelling. The UAE data highlights a male-skewed burden of knee osteoarthritis, linked to the active expatriate workforce. The demand is shifting towards active patients seeking structured recovery, reflecting a transformation in care episodes and patient expectations.

By Route Of Administration: Oral Entrenched, Injectable Gaining Institutional Ground

Oral therapies held a 28.77% share in 2025, maintaining their dominance in the GCC swollen knee treatment market. Oral NSAIDs are widely prescribed and distributed, offering convenience in early-stage pain management and conservative care. Topical products are gaining visibility for targeted pain relief, while procedural routes like arthrocentesis and radiofrequency are building credibility in specialist centers. Oral therapies remain entrenched even as the market diversifies its treatment routes.

Injectable routes are projected to grow at a 6.78% CAGR through 2031, supported by evidence for PRP and hyaluronic acid use and their role as bridge therapies between oral treatments and surgery. A 2025 review validated the efficacy of at least two PRP injections for sustained results over 24 weeks. The GCC's 2024 corticosteroid consumption of 3,300 tons, valued at USD 670 million, highlights an established ecosystem for injectable therapies. This infrastructure supports the expansion of knee-specific injectables, transitioning them from niche to standardized care.

By End User: Hospitals Anchor Demand, Specialist Clinics Reset The Growth Equation

Hospitals accounted for 35.88% of the GCC swollen knee treatment market in 2025, reflecting their role in acute care, post-surgical management, and complex knee cases. Tertiary facilities provide deeper formularies, broader device access, and stable staffing for procedures like aspiration and injections. Ambulatory surgical centers are gaining relevance with private participation and faster discharge models, while physiotherapy and rehabilitation centers capture more volume as musculoskeletal recovery becomes structured post-injection or surgery.

Orthopedic and sports medicine clinics are projected to grow at a 7.44% CAGR through 2031, making them the fastest-growing segment in the GCC swollen knee treatment market. Their growth is driven by a shift towards specialized care with faster patient turnover and favorable procedure economics. Burjeel Holdings expanded capacity with the Burjeel Orthopedic Institute in Abu Dhabi in 2025, focusing on surgery, sports medicine, and rehabilitation. Digital monitoring tools are enhancing post-procedure adherence, positioning clinics to manage the full cycle of care and reshaping patient relationship dynamics in the market.

Geography Analysis

In 2025, Saudi Arabia accounted for 26.45% of the GCC swollen knee treatment market, making it the largest national segment. This leadership is driven by its large population, a significant overweight and obese adult demographic, and a well-developed healthcare system supporting both hospital-led and outpatient orthopedic care. The country’s insurance framework enhances specialist access for expatriate workers, crucial for a treatment category requiring repeat consultations. Hikma expanded its injectable pain portfolio in Saudi Arabia in 2024, strengthening local distribution channels aligned with swollen knee management. Saudi Arabia’s combination of patient volume, reimbursement access, and supply chain efficiency solidifies its market dominance.

The UAE is projected to grow at a 7.12% CAGR through 2031, making it the fastest-growing segment in the GCC swollen knee treatment market. Growth is supported by mandatory insurance, high specialist density, and its role as a medical tourism hub for orthopedic and rehabilitation services. Burjeel’s 2025 launch of a dedicated orthopedic institute in Abu Dhabi expanded capacity in surgery, sports medicine, and rehabilitation. Additionally, Abu Dhabi’s 2024 stem cell trial for knee osteoarthritis highlights the UAE’s focus on treatment innovation and clinical advancements, driving its accelerated market growth.

Oman, Bahrain, Kuwait, and other GCC nations represent emerging opportunities in the swollen knee treatment market. Bahrain’s rising knee osteoarthritis incidence indicates latent demand that could grow with improved referral pathways. Kuwait’s high obesity rates create a significant base for pharmacological and injection-based treatments. Oman’s expanding insurance coverage is gradually improving access to specialist care beyond public hospitals. While these markets currently hold a smaller share, they are positioned for growth as orthopedic capacity, private sector involvement, and patient awareness increase.

Competitive Landscape

The GCC market for swollen knee treatment is moderately fragmented, with companies competing across various stages of the care pathway rather than focusing on a single product class. Major pharmaceutical firms like Pfizer and Novartis dominate oral analgesics and anti-inflammatory treatments, while orthobiologic specialists focus on viscosupplementation and PRP-related procedures. Device manufacturers lead in surgical reconstructions, robotic support, and advanced technologies in high-acuity orthopedic settings. This segmentation results in broad competition, with purchasing decisions varying among hospitals, specialty clinics, ambulatory centers, and rehabilitation sites.

In pharmacological care, companies such as Pfizer, Novartis, and Hikma leverage their established prescribing familiarity and hospital access. Hikma expanded its regional presence in 2024 by introducing injectable pain medications in Saudi Arabia, Jordan, and Iraq, strengthening its role in pain-management pathways linked to orthopedic care. In injection-led treatments, firms like Anika Therapeutics, Bioventus, IBSA, and Ferring compete on formulation quality, dosing patterns, and physician confidence. Anika’s international growth in osteoarthritis pain management in 2024 highlights the benefits of overseas expansion. Burjeel’s investment in orthopedic and rehabilitation capacity reflects a trend toward provider-side consolidation, influencing the scaling of products and procedures.

Strategic initiatives in the GCC swollen knee treatment market focus on regional distribution, specialist clinic expansion, and digital or procedural differentiation. Companies combining local channel expertise with clinician training and repeat-care support are better positioned for long-term success. There is also an opportunity for mid-priced injectable offerings targeting under-insured or self-paying patients. Regenerative medicine could disrupt the market if cell-based programs in Abu Dhabi progress from safety trials to commercialization. While hyaluronic acid, corticosteroids, and conventional analgesics dominate the current treatment mix, innovation in regenerative medicine adds a potential growth layer.

GCC Swollen Knee Treatment Industry Leaders

B. Braun SE

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Arthrex, Inc.

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Grand Hyatt in Dubai, UAE, hosted the Dubai Global Knee Innovation Summit from January 22-24, 2026. The summit highlighted advancements in knee arthroplasty, trauma care, and sports medicine, featuring innovations such as robotic-assisted surgical tools and regenerative medicine technologies.

- October 2025: Aster Hospital Mankhool in Dubai launched a Robotic Surgery Centre equipped with the ROSA Robotic Knee System. This is the first facility of its kind within the Aster Hospitals network, enhancing precision total knee arthroplasty capabilities in the UAE.

- June 2025: Johnson & Johnson MedTech introduced the KINCISE 2 Surgical Automated System. This automated power tool is designed for both primary and revision procedures in hip and knee replacements, aiming to improve surgical efficiency and reduce the physical strain on surgeons.

- May 2025: The Emirates Growth Fund announced its first investment, acquiring a strategic minority stake in Tarmeem Healthcare Holding. Based in Abu Dhabi, Tarmeem specializes in orthopedics and spine care, serving over 20,000 patients annually.

GCC Swollen Knee Treatment Market Report Scope

As per the scope of the report, a swollen knee (joint effusion) occurs when excess fluid builds up in or around the joint. Treatment focuses on addressing the underlying cause and managing symptoms using the R.I.C.E. method: rest, Ice, Compression, and elevation, combined with physical therapy, pain relievers, or medical drainage.

The GCC swollen knee treatment market is segmented by treatment type, cause or clinical indication, route of administration, end-user, and geography. By treatment type, the market includes pharmacological treatment, non-pharmacological treatment, minimally invasive procedures, and surgical treatment. By cause or clinical indication, the market is segmented into osteoarthritis, sports injury, rheumatoid arthritis and other inflammatory arthritis, bursitis and tendinitis, post-traumatic swelling, and others. By route of administration, the market is categorized into oral, topical, injectable, procedural, and device-based. By end-user, the market is segmented into hospitals, orthopedic and sports medicine clinics, ambulatory surgical centers, physiotherapy and rehabilitation centers, and home care settings. By country, the market is segmented into Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman, Bahrain, and the rest of GCC. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Pharmacological Treatment |

| Non-Pharmacological Treatment |

| Minimally Invasive Procedures |

| Surgical Treatment |

| Osteoarthritis |

| Sports Injury |

| Rheumatoid Arthritis and Other Inflammatory Arthritis |

| Bursitis and Tendinitis |

| Post-Traumatic Swelling |

| Others |

| Oral |

| Topical |

| Injectable |

| Procedural and Device-Based |

| Hospitals |

| Orthopedic and Sports Medicine Clinics |

| Ambulatory Surgical Centers |

| Physiotherapy and Rehabilitation Centers |

| Home Care Settings |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Rest of GCC |

| By Treatment Type | Pharmacological Treatment |

| Non-Pharmacological Treatment | |

| Minimally Invasive Procedures | |

| Surgical Treatment | |

| By Cause or Clinical Indication | Osteoarthritis |

| Sports Injury | |

| Rheumatoid Arthritis and Other Inflammatory Arthritis | |

| Bursitis and Tendinitis | |

| Post-Traumatic Swelling | |

| Others | |

| By Route of Administration | Oral |

| Topical | |

| Injectable | |

| Procedural and Device-Based | |

| By End User | Hospitals |

| Orthopedic and Sports Medicine Clinics | |

| Ambulatory Surgical Centers | |

| Physiotherapy and Rehabilitation Centers | |

| Home Care Settings | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of GCC |

Key Questions Answered in the Report

What is the current size of the GCC swollen knee treatment market?

The GCC swollen knee treatment market is valued at USD 87.06 million in 2026 and is forecast to reach USD 144.33 million by 2031, growing at a CAGR of 5.60% over the period.

Which treatment segment is growing the fastest in the GCC swollen knee treatment market?

Minimally invasive procedures are the fastest-growing treatment type, with a projected CAGR of 5.98% through 2031, supported by stronger use of viscosupplementation and PRP in specialist settings.

What is driving demand for swollen knee treatment across GCC countries?

The main demand drivers are rising osteoarthritis incidence, very high obesity and diabetes prevalence, broader orthopedic clinic capacity, and stronger use of injection-based treatment in ambulatory care.

Which country leads the GCC swollen knee treatment market?

Saudi Arabia held the largest share at 26.45% in 2025, supported by population scale, wider specialist access, and strong pharmaceutical and injectable supply presence.

Which route of administration is expanding fastest in the region?

Injectable therapies are growing the fastest, with a projected CAGR of 6.78% through 2031, as clinicians use them more often between oral treatment and surgery.

How competitive is the GCC swollen knee treatment market?

The market is moderately fragmented because pharmaceutical firms, orthobiologic suppliers, and device companies compete across different treatment pathways rather than under one highly concentrated structure.

Page last updated on: