Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

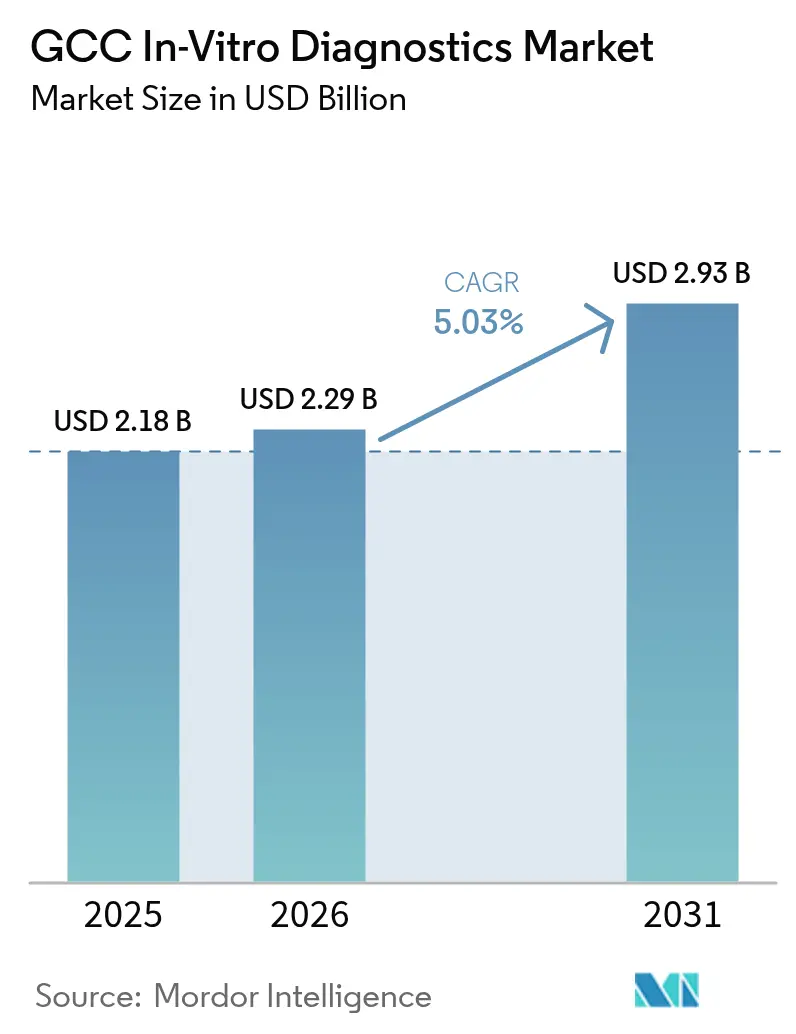

| Base Year Market Size (2025) | USD 2.18 Billion |

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 2.93 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The GCC in-vitro diagnostics market size is expected to grow from USD 2.18 billion in 2025 to USD 2.29 billion in 2026 and is forecast to reach USD 2.93 billion by 2031 at 5.03% CAGR over 2026-2031. The expansion is being propelled by Vision 2030 reforms in Saudi Arabia, parallel modernization programs in the UAE and Qatar, and a deliberate shift from treatment-centric care models to prevention-oriented systems where laboratory evidence guides early clinical decisions. The GCC in-vitro diagnostics market is responding to post-pandemic vigilance, rapidly rising diabetes prevalence, and sustained government spending that favors advanced testing infrastructure. Large reference laboratories are investing in high-throughput immunochemistry and molecular platforms, while hospitals are upgrading bedside testing to improve turnaround times. The GCC in-vitro diagnostics market also benefits from a swelling health-insured expatriate base, streamlined CPT-based reimbursement, and growing importer–manufacturer partnerships that localize reagent filling and software support. Competitive intensity is sharpening as regional chains integrate artificial intelligence into workflows and multinationals hedge against supply risk by co-developing local manufacturing.

Key Report Takeaways

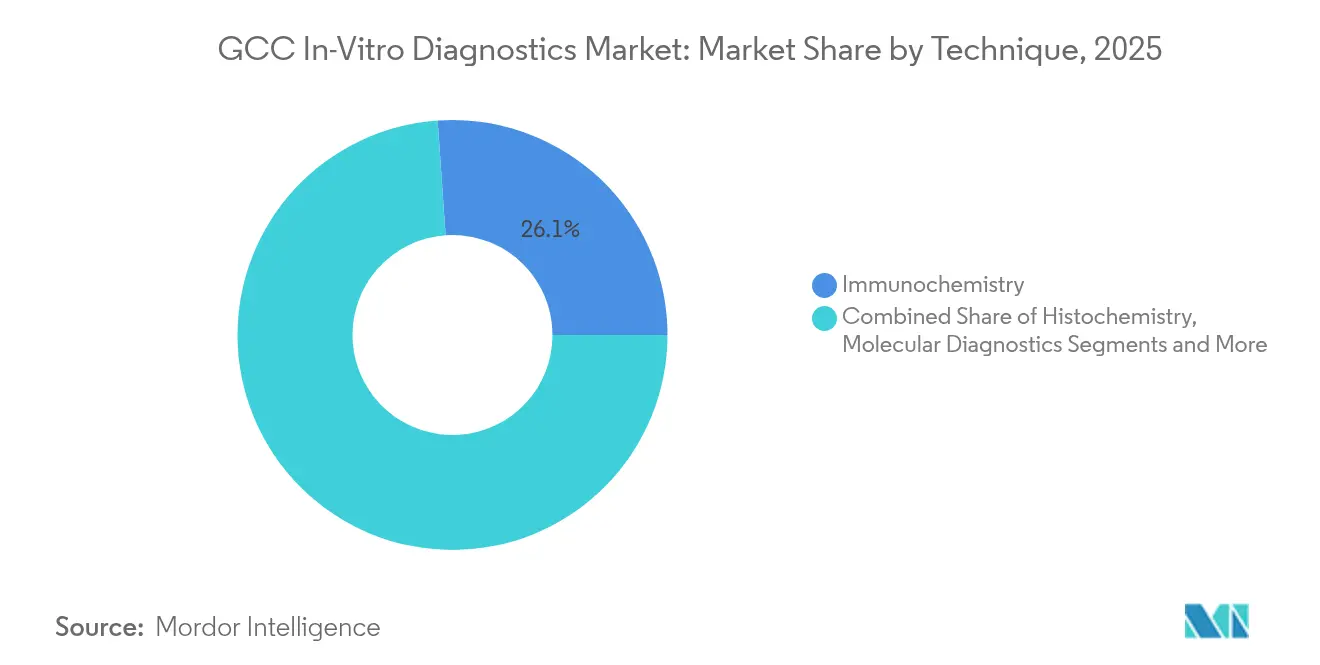

- By technique, immunochemistry led with a 26.10% revenue share of the GCC in-vitro diagnostics market in 2025 while molecular diagnostics is projected to expand at an 11.26% CAGR through 2031.

- By product category, reagents and consumables captured 60.45% of the GCC in-vitro diagnostics market share in 2025; software and services show the fastest outlook at a 13.55% CAGR to 2031.

- By usability, disposable IVD devices retained 88.10% share in 2025; home-use disposable devices are expanding at a 11.38% CAGR to 2031.

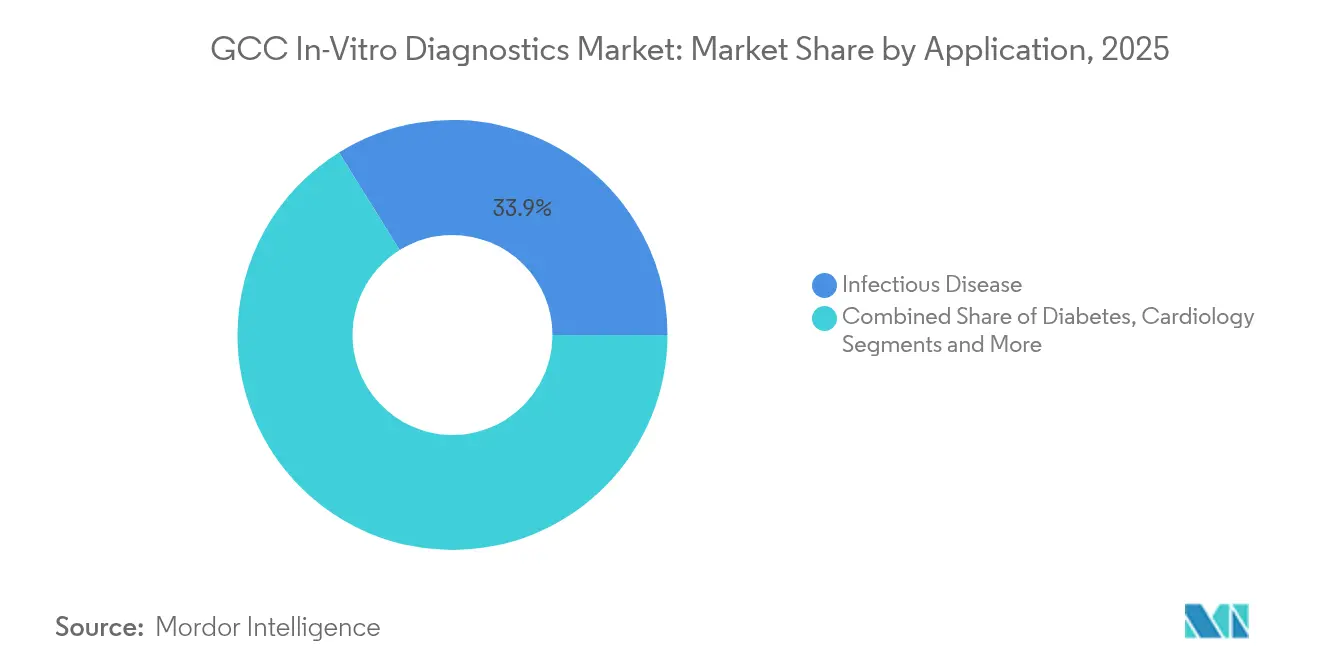

- By application, infectious disease testing commanded 33.85% of the GCC in-vitro diagnostics market size in 2025 and oncology diagnostics is advancing at a 11.95% CAGR over 2026-2031.

- By end user, diagnostic laboratories held 55.20% of the GCC in-vitro diagnostics market in 2025 while the home-care and self-testing setting posts the highest forecast CAGR at 12.12%.

- By diagnostic approach, centralized laboratory testing retained 68.35% of the GCC in-vitro diagnostics market in 2025; point-of-care platforms are expected to grow 12.72% per year up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Chronic & Infectious Diseases Across GCC | +1.1% | All GCC countries, with highest impact in Saudi Arabia and UAE | Long term (≥ 4 years) |

| Government-Led Healthcare Capacity Expansion & Modernization | +1.4% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Rising Adoption of Advanced Diagnostic Technologies (Molecular, Digital, AI) | +0.9% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Favorable National Screening & Preventive Health Programs | +0.6% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Expanding Health-Insurance Coverage Including Mandatory Expat Benefits | +0.4% | UAE, Saudi Arabia, Oman | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic & Infectious Diseases Across GCC

Diabetes affects between 8% and 22% of GCC citizens, creating an economic drain estimated at USD 50 billion in care costs and lost productivity. A 2024 study reported 152,854 deaths and 3 million potential life-years lost to nine non-communicable diseases, translating into USD 23.9 billion in losses. This burden stimulates continuous glucose monitoring demand and keeps infectious disease surveillance budgets intact because expatriate mobility and religious tourism sustain cross-border pathogen risks. Saudi Arabia increased its public health outlay in response, and PCR networks built for COVID-19 testing are now redeployed for tuberculosis and respiratory virus panels. The GCC in-vitro diagnostics market therefore gains steady volume from both chronic disease follow-up and outbreak preparedness.

Government-Led Healthcare Capacity Expansion & Modernization

Saudi Arabia targets a jump in private hospital capacity from 23% to 68% under Vision 2030, while the UAE positions specialized oncology and transplant centers to attract medical tourists. Qatar allocates capital to digital hospital ecosystems that embed laboratory automation. The construction wave demands integrated laboratory networks that run 24/7 with minimal error, benefiting vendors who can supply middleware, track-and-trace logistics, and workforce training. These investments reshape procurement criteria: authorities look beyond device cost toward uptime, reagent security, and data interoperability, factors that redefine supplier rankings within the GCC in-vitro diagnostics market.

Rising Adoption of Advanced Diagnostic Technologies

AI platforms now assist pathologists in slide screening and automate molecular assay interpretation. Saudi Arabia’s National Platform for Healthcare Information Exchange creates a standardized data backbone that connects laboratory results with primary-care portals[1]Riyadh Valley Company, “MedTech Report,” rvc.com.sa. PCR instruments purchased in 2021 are repurposed for oncology and pharmacogenomics, while next-generation sequencing supports national genome projects in Qatar. Vendors differentiate through cloud analytics and real-time quality control dashboards, which improve throughput and reduce error rates. As a result, the GCC in-vitro diagnostics market experiences revenue migration from hardware replacement cycles toward subscription-based analytics modules.

Favorable National Screening & Preventive Health Programs

Vision 2030 mandates periodic diabetes, cardiovascular, and cancer checks for insured Saudis, and the UAE is adding vitamin D and colonoscopy reimbursement triggers. Structured screening produces predictable specimen volumes that let laboratories plan reagent inventory and depreciation schedules with greater accuracy. Preventive focus broadens panels beyond infection markers to include genetic risk profiles and metabolic biomarkers, stimulating demand for multiplex assays. These nationwide programs therefore convert episodic demand into annuity-style revenue, strengthening the growth profile of the GCC in-vitro diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Reliance on Imports and Resultant Cost Pressures | -1.0% | All GCC countries | Medium term (2-4 years) |

| Complex & Heterogeneous Regulatory Approval Processes | -0.6% | All GCC countries, with highest impact in Saudi Arabia | Medium term (2-4 years) |

| Workforce Constraints in Specialized Laboratory Skills | -0.4% | All GCC countries, with highest impact in smaller markets (Oman, Bahrain) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heavy Reliance on Imports and Resultant Cost Pressures

More than 80% of reagents, plastics, and capital equipment are sourced offshore, exposing laboratories to freight bottlenecks and currency swings. While the UAE and Saudi Arabia announce biotech parks and reagent fill-finish plants, commercial output will take time to reach scale. Interim countermeasures include framework contracts that hedge exchange risk and consignment stock warehousing. Smaller providers in Oman and Bahrain struggle to secure volume discounts, which may limit decentralized testing penetration and slow overall uptake in the GCC in-vitro diagnostics market.

Complex & Heterogeneous Regulatory Approval Processes

The SFDA’s in-house IVD guidance and its new AI device dossier rules require granular performance data and local representative responsibilities[2]Gulf Central Committee for Drug Registration, “Guidance on the Development of IVDs for In-House Use,” gccbdi.org. Parallel submissions to Dubai or Doha regulators add cost and delay. Harmonization talks progress, yet device makers still tailor labeling, vigilance reporting, and language requirements for each jurisdiction. This fragmentation raises the barrier to entry for niche assay developers and can postpone the launch of breakthrough technologies, tempering growth momentum within the GCC in-vitro diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Molecular Diagnostics Reshaping Testing Paradigms

Immunochemistry commanded 26.10% of the GCC in-vitro diagnostics market in 2025, fueled by high-volume HbA1c, thyroid, and cardiac marker panels. Molecular assays accounted for a smaller share but register the fastest 11.26% CAGR because PCR capacity built during the pandemic now tackles oncology biomarkers and pharmacogenomic profiling. The GCC in-vitro diagnostics market size for molecular assays is projected to expand as next-generation sequencing instruments enter reference laboratories. Hematology and microbiology remain clinical staples, whereas histochemistry grows alongside expanding cancer programs. The region’s diabetes epidemic sustains self-blood glucose testing, and coagulation analyzers find steady demand from cardiovascular disease management. Continued AI integration in result interpretation keeps immunochemistry competitive, yet the molecular upgrade cycle drives incremental reagent revenue for suppliers.

Digitalization shapes future workflows. Saudi and Emirati labs integrate middleware that auto-verifies immunoassay runs, while cloud-based databases archive molecular raw data for secondary analysis. Vendors able to deliver both assay kits and analytics secure multi-year managed service contracts. This convergence of wet chemistry and informatics underpins future differentiation in the GCC in-vitro diagnostics market.

By Product: Software Integration Driving Value Creation

Reagents and consumables generated 60.45% of GCC in-vitro diagnostics market revenue in 2025, reflecting repeat-purchase dependency. Capital equipment sales benefit from periodic automation upgrades, yet software and services, now a single-digit share, will post a 13.55% CAGR to 2031. AI modules that flag result anomalies, auto-triage critical values, and streamline quality control transform laboratories into data hubs. The GCC in-vitro diagnostics market share for software climbs as providers shift from one-time analyzer sales to recurring license models. Regional partnerships, such as Roche Diagnostics and Burjeel Holdings, illustrate the pivot toward digital diagnostics.

Instrument suppliers bundle reagent leases with uptime guarantees while co-hosting dashboards in sovereign clouds to meet data-residency laws. Local value-added distributors hire bioinformaticians, turning service revenue into a strategic lever. This blended portfolio of chemistry, equipment, and code redefines competitive positioning in the GCC in-vitro diagnostics market.

By Usability: Disposables Dominate While Home Testing Accelerates

Disposable devices held 88.10% market share in 2025 because single-use formats match infection-control norms and insurer payment codes. Reusable cartridges cater to specialized coagulation and some point-of-care chemistry analyzers but remain niche. Within disposables, home-use kits for glucose, cholesterol, and pregnancy display 11.38% CAGR, reflecting rising chronic disease self-management. Wi-Fi or Bluetooth-enabled meters transmit readings to care portals, fitting GCC telehealth policies that aim to shift 50% of routine care to virtual channels by 2028. The GCC in-vitro diagnostics market integrates wearable sensors and smartphone apps that gamify adherence, expanding manufacturer revenue beyond strip sales toward subscription analytics.

By Application: Cancer Diagnostics Gaining Momentum

Infectious diseases retained 33.85% of GCC in-vitro diagnostics market revenue in 2025, buttressed by mandatory screening for inbound pilgrims and expatriates. Diabetes testing remains sizable due to prevalence but oncology assays exhibit a 11.95% CAGR outlook. Governments add breast, colon, and bladder cancer panels to coverage lists; Guardant Health’s liquid biopsy adoption in Abu Dhabi and Wellesta’s VECanDx test introduction illustrate the trend. Cardiology panels hold steady importance, and autoimmune diagnostics benefit from improved awareness. Emerging genetic wellness screens enter employer health programs, expanding the breadth of the GCC in-vitro diagnostics market.

By End User: Self-Testing Environments Expanding Rapidly

Diagnostic laboratories captured 55.20% of spending in 2025 through consolidated reference operations. Hospitals rely on these labs for high-complexity tests but keep STAT analyzers for emergencies. Home-care and self-testing sites show 12.12% CAGR as insurers reimburse connected glucometers and coagulation self-tests. SGS training on the EU IVDR transition, promoted in the region, accelerates manufacturer readiness for direct-to-consumer kits. Retail clinics inside malls and workplaces join the “other” category, widening specimen access points within the GCC in-vitro diagnostics market.

By Diagnostic Approach: Point-of-Care Gaining Strategic Importance

Central laboratories contributed 68.35% of revenue in 2025; however, point-of-care solutions add 12.72% annual growth as clinicians demand immediate actionable results. Rapid antigen respiratory panels, sexually transmitted infection tests, and bedside troponin kits shorten emergency department cycles. Vendors such as Fapon showcase one-stop platforms using CLIA, LFA, and FIA technologies, coupled with local manufacturing commitments that dovetail with import-substitution policies. This decentralized testing momentum reshapes procurement criteria and rewards suppliers who integrate connectivity, quality controls, and flexible cartridge menus.

Geography Analysis

Saudi Arabia represents the largest contributor to GCC in-vitro diagnostics market revenue, buoyed by a high population base and the Kingdom’s aggressive health-capital expenditure. The market benefits from Vision 2030’s pledge to triple private sector involvement, which funnels investment into molecular laboratories and AI-enabled quality programs. Saudi providers negotiate reagent-rental contracts that stabilize cash flows and rely on domestic biomanufacturing plans to hedge import costs. The GCC in-vitro diagnostics market size for Saudi Arabia is set to widen as oncology and genetics programs mature.

The UAE leads on per-capita spending and technology adoption. Large hospital groups integrate robotics in sample handling and treat diagnostics as a tourism magnet, drawing international patients seeking rapid precision reports. Mandatory insurance for expatriates expands test volume, and Dubai Science Park’s reagent fill-finish projects begin to localize supply. These dynamics keep the GCC in-vitro diagnostics market vibrant in the Emirates.

Qatar, Kuwait, Oman, and Bahrain collectively add incremental growth through specialty centers and national screening drives. Qatar’s genome initiative accelerates sequencing demand, while Kuwait’s preventive health programs stimulate immunoassay volumes. Smaller markets focus on decentralizing services to reach remote areas, turning to cloud-linked point-of-care devices. Import dependence remains a shared vulnerability, yet harmonized procurement among these states improves negotiating leverage, reinforcing a unified GCC in-vitro diagnostics market direction.

Regulatory Landscape

In Saudi Arabia, in-vitro diagnostics are regulated as medical devices by the Saudi Food and Drug Authority (SFDA) under the Medical Devices and Supplies Law (Royal Decree No. M/54, 6/7/1442 AH). An SFDA Medical Device Marketing Authorization (MDMA) is required to place an IVD on the market, and IVDs follow a risk-based classification approach in SFDA requirements and classification guidance. This drives the depth of technical documentation and performance evidence expected for approval.

Market access also depends on establishment licensing and quality-system readiness. SFDA licensing applies to manufacturers, importers, distributors, and authorized representatives, with QMS expectations aligned to ISO 13485 (or equivalent) through an SFDA-recognized body. The framework also covers specific guidance for in-house IVD development and companion diagnostics (CDx), which adds documentation, validation, and post-market performance monitoring obligations. For specialized assays, these requirements can lengthen timelines for new entrants while raising the compliance bar.

Competitive Landscape

The GCC in-vitro diagnostics market exhibits moderate concentration. Multinationals such as Roche, Abbott, Siemens Healthineers, and Beckman Coulter dominate high-throughput analyzers and reagent leases. Regional groups like Al-Borg Diagnostics and PureHealth strengthen scale through chain acquisitions and strategic digital upgrades. Partnerships that merge hardware with analytics differentiate market leaders: Roche aligns with Burjeel to embed middleware dashboards; Fapon signs a memorandum with Dubai Chambers to accelerate local manufacturing.

White-space growth lies in localized reagents and assays designed for GCC genomic traits. Disruptive entrants leverage next-generation sequencing and AI-augmented digital pathology to carve niches. Investors, including Quadria’s USD 1 billion fund, assign 25% to GCC diagnostics, signaling capital depth for innovators[3]AGBI, “Quadria commits 25% from USD 1 bn healthcare fund to GCC,” agbi.com. Success factors now extend beyond sensitivity ratings to include supply resilience, data integration, and regulatory fluency, shaping future share allocation within the GCC in-vitro diagnostics market.

GCC In-Vitro Diagnostics Industry Leaders

Abbott Laboratories.

Danaher Corporation

F. Hoffmann-La Roche AG

Becton, Dickinson and Company

Sysmex Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity lies in localization of molecular diagnostics and reagent supply chains, aimed at easing the region's heavy import dependence (more than 80% for reagents, plastics, and capital equipment in the current market context). Co-Diagnostics provides a visible signal of progress through its Saudi joint venture CoMira, including April 2026 approval for a planned manufacturing facility in Sudair Industrial City and a June 2026 technology-transfer step tied to an automated PCR test-kit manufacturing line. Together, these actions create room for suppliers that can support local assay production, validation, and the ongoing quality and post-market performance processes under SFDA requirements.

Another opportunity is the shift from standalone analyzers toward integrated software, connectivity, and managed services as health systems expand and screening programs scale. Vision 2030 and related modernization efforts continue to favor scaled laboratory networks, and partnerships such as Roche Diagnostics Middle East aligning with AlFarabi Medical Labs and Aster DM Healthcare in Riyadh (April 2026) point to demand for workflow upgrades alongside platforms. Vendors that can align SFDA authorization, establishment licensing, and data interoperability requirements, while serving both centralized procurement channels (such as NUPCO) and large private hospital groups, are positioned to capture recurring revenue from middleware, analytics, and service contracts in addition to consumables.

Recent Industry Developments

- June 2026: Co-Diagnostics hosted its Saudi joint venture CoMira Diagnostics delegation at its Salt Lake City headquarters and unveiled plans for a future automated PCR test kit manufacturing line as part of a technology-transfer program. The initiative supports building local manufacturing capability for molecular diagnostics in Saudi Arabia, which aligns with localization priorities and can improve supply resilience for high-throughput testing menus.

- May 2025: Roche Diagnostics intensified engagement in Saudi Arabia to support preventive, personalized, data-driven healthcare aligned with Vision 2030. The push reinforces the shift in customer demand toward integrated diagnostics offerings that combine instruments, assays, and digital workflow capabilities in large health systems.

- April 2024: Becton Dickinson (BD) launched the BD Training Center at its regional headquarters in Riyadh to provide professional development for healthcare providers, including areas linked to sepsis and antimicrobial resistance. The investment strengthens local capability building around laboratory and clinical workflows, supporting adoption and sustained utilization of advanced diagnostic platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers in vitro diagnostic products and testing solutions used on patient samples in GCC healthcare settings to detect, monitor, or screen diseases. We count the value of commonly used IVD instruments, reagents, and related items sold across GCC countries.

Scope exclusions: We exclude in vivo imaging diagnostics, therapeutic drugs, and purely research-use-only consumables that are not intended for clinical diagnosis.

Segmentation Overview

- By Technique

- Histochemistry

- Molecular Diagnostics

- Hematology

- Self-Blood Glucose Testing

- Immunochemistry

- Microbiology

- Coagulation

- Other Techniques

- By Product

- Instruments

- Reagents & Consumables

- Software & Services

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Application

- Infectious Disease

- Diabetes

- Cancer / Oncology

- Cardiology

- Autoimmune Disease

- Other Applications

- By End User

- Diagnostic Laboratories

- Hospitals & Clinics

- Home-Care & Self-Testing Settings

- Other End Users

- By Diagnostic Approach

- Point-of-Care Diagnostics

- Centralised Laboratory-based Diagnostics

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with publicly available health and trade signals that explain where testing demand is coming from and how procurement is structured in the GCC. We mainly refer to sources such as WHO and World Bank health indicators, ministries of health and national statistics portals, and GCC customs and import-export reporting where available.

To ground the model assumptions, we also review peer-reviewed clinical and lab-medicine journals for testing trends, regulator and standards body updates (for example, device registration and quality requirements), and hospital and laboratory network announcements in reputed press. Company annual reports, investor presentations, and product brochures are used to understand product mix shifts and pricing direction. We also use paid subscriptions for company financials and news to confirm timelines and expansion activity. The source list mentioned here is illustrative, and many other public references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the demand story across Saudi Arabia, the UAE, and the smaller GCC markets, since procurement cycles and test mix can vary by setting. We spoke with labs, hospitals and clinics, distributors, and industry specialists to confirm utilization patterns, reagent pull-through assumptions, and the split between centralized laboratory testing and point-of-care use.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | |

| Mid tier: 60% | Functional/Unit leaders: 33% | |

| Smaller Players: 14% | Managers: 54% |

Market-Sizing & Forecasting

Sizing is built from a top-down demand pool assessment, where GCC testing volumes and care delivery patterns are reconstructed using disease burden and screening intensity signals, then translated into spend through price and mix logic. We corroborate totals with selective bottom-up approximations using sampled reagent consumption per test, instrument placements in larger labs, and channel feedback from annual purchasing to adjust obvious gaps.

Key inputs tracked in the model include the split of testing done in hospitals versus independent diagnostic laboratories, the pace of expansion in centralized reference labs, point-of-care penetration in clinics, and mix shifts across clinical chemistry, immunochemistry, hematology, microbiology, and molecular diagnostics. For the value build, average selling price movement is treated separately for reagents and instruments because reagent pull-through and tendering cycles tend to behave differently across GCC countries.

For forecasting, we use scenario analysis supported by simple regression checks on drivers such as population growth, diabetes prevalence, infectious disease testing intensity, and planned capacity additions in lab networks. Where country-level data is incomplete, we use proportional allocation based on healthcare spend and service capacity, and we validate the splits again during expert follow-ups.

Data Validation & Update Cycle

Validation is done through stepwise checks that compare model outputs against independent signals, then analyst review before sign-off. We look for unusual jumps in country totals, unrealistic reagent to instrument ratios, and inconsistencies between point-of-care shares and known site-of-care adoption, and these are investigated and corrected.

If a variance cannot be explained using desk sources, we re-contact respondents to confirm what changed, which is common around tender resets, major lab expansion announcements, or policy updates. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Vitro Diagnostics Gulf Cooperation Council Gcc Market Size Versus Other Published Estimates

Published GCC IVD market values can look quite different because each study chooses its own year, scope, and pricing logic, and those choices quickly change the final number. Differences also show up when one estimate relies more on shipment proxies, while another relies more on lab utilization or healthcare spending.

The largest gaps usually come from what gets counted as IVD value and how price is treated across instruments and reagents, especially in tender-driven markets. Some sources also roll software and services more broadly into IVD, or they use aggressive growth assumptions for molecular testing without validating how fast installed capacity is being utilized across GCC countries.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.18 B (2025) | |

| Global Consultancy A | USD 2.68 B (2024) | Uses an earlier base year and appears to apply faster growth expectations for advanced testing, which can lift totals if utilization and tender pricing are not normalized country by country. |

| Regional Consultancy B | USD 1.70 B (2025) | Tends to size from a narrower spend pool that can undercount parts of the market when reagent pull-through linked to instrument placements and broader test menu coverage are not fully captured. |

The table shows that year selection, what is included in IVD, and how reagent and instrument pricing is refreshed are the practical reasons for the spread. When reagent pull-through and the split between centralized labs and point-of-care testing are explicitly modeled and rechecked with GCC stakeholders, the value lands closer to a transparent demand-led number, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the GCC in-vitro diagnostics market?

The market stands at USD 2.29 billion in 2026 and is projected to rise to USD 2.93 billion by 2031.

Which technique leads GCC diagnostic spending?

Immunochemistry holds 26.10% of 2025 revenue, driven by routine chronic disease panels.

How fast is molecular diagnostics growing in the GCC?

Molecular assays are forecast to advance at an 11.26% CAGR through 2031 as PCR and sequencing move beyond infectious diseases.

Why are reagents and consumables so dominant?

Imported reagents generate recurring sales and captured 60.45% of 2025 market revenue because most testing volume depends on disposable cartridges and kits.

What role does point-of-care testing play in GCC healthcare?

Point-of-care platforms are expanding 12.72% per year, empowering clinicians with rapid results and supporting national goals for decentralized and preventive care.

Page last updated on: