Cruciate Ligament Repair Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.44 Billion |

| Market Size (2031) | USD 26.12 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

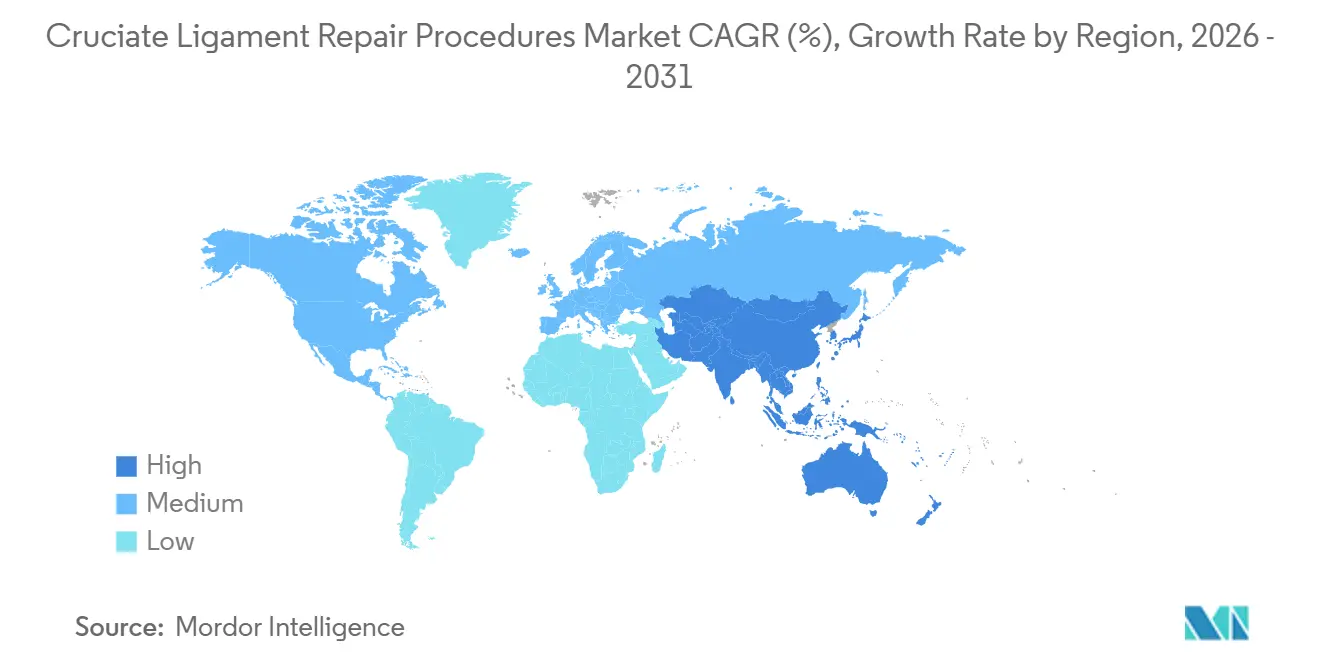

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

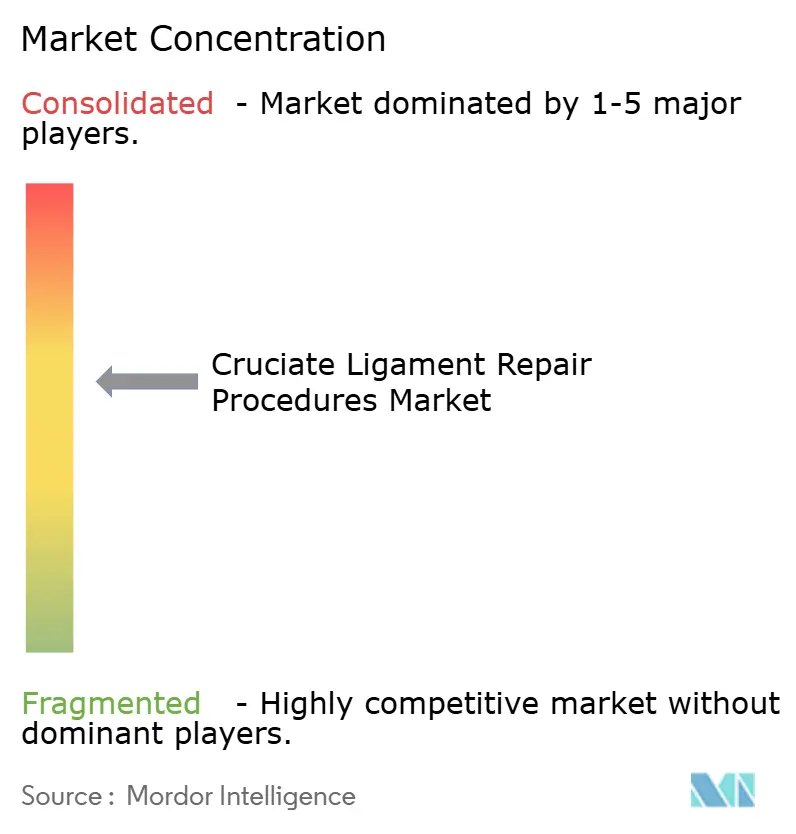

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cruciate Ligament Repair Procedures Market Analysis by Mordor Intelligence

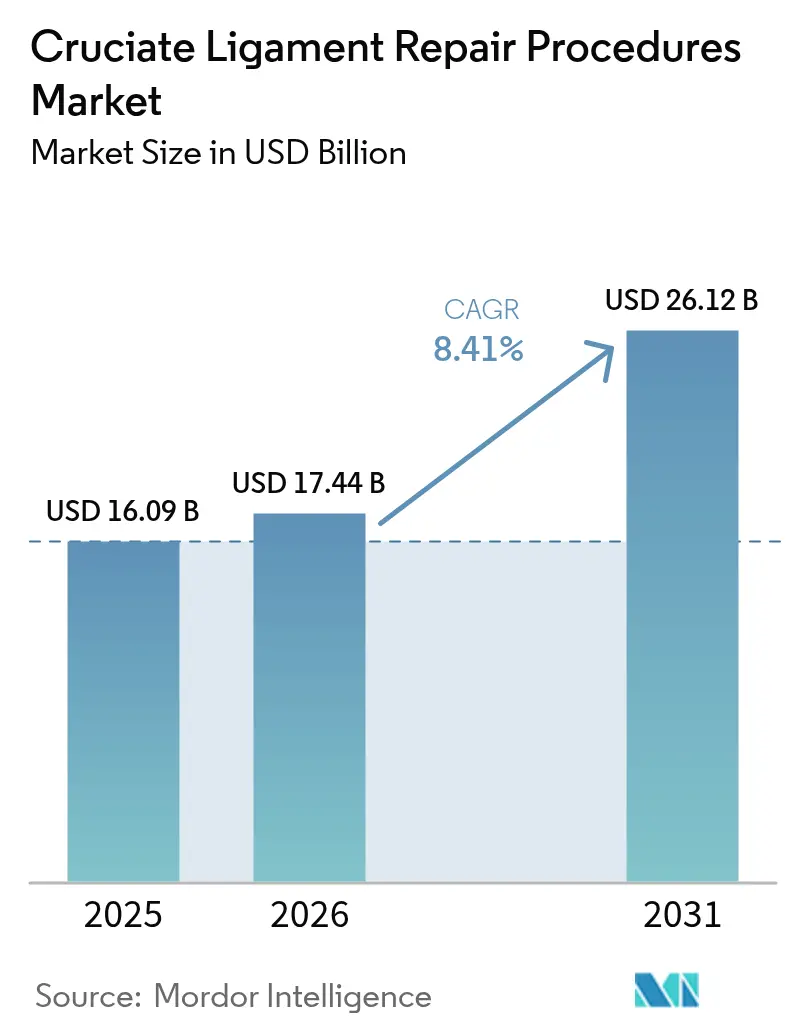

The Cruciate Ligament Repair Procedures Market size is projected to expand from USD 16.09 billion in 2025 and USD 17.44 billion in 2026 to USD 26.12 billion by 2031, registering a CAGR of 8.41% between 2026 to 2031.

The preference for surgical interventions over conservative care continues to grow, despite epidemiologic studies reporting a 3.43% decline in annual anterior cruciate ligament (ACL) tear incidents between 2010 and 2020. The U.S. Food and Drug Administration’s (FDA) January 2026 label update for the BEAR implant, which confirmed a reduced risk of post-traumatic osteoarthritis, has strengthened market confidence in biologic scaffolds. Expanding outpatient capacity, demonstrated by the removal of 275 orthopedic procedures from the Medicare inpatient-only list in 2024, is driving a shift toward cost-efficient ambulatory surgery centers. In China, volume-based procurement reforms have reduced knee-implant prices by 82%, improving accessibility but exerting pressure on multinational profit margins. To address these challenges, leading vendors are leveraging differentiated biologics, artificial intelligence (AI) planning, and robotic assistance to minimize technical failures, which remain the primary cause of 60%–70% of graft ruptures.

Key Report Takeaways

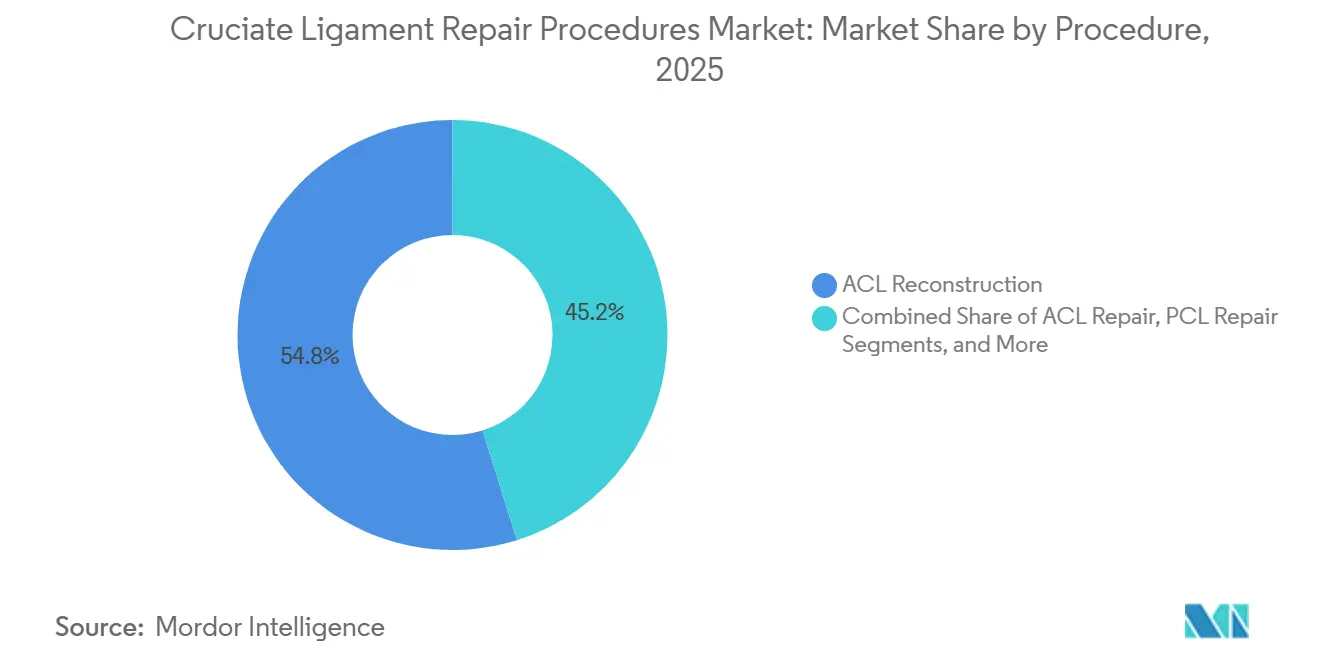

- By procedure, ACL reconstruction held 54.84% of the cruciate ligament repair procedures market share in 2025, while ACL repair is projected to expand at a 10.53% CAGR through 2031.

- By graft type, autograft tissue accounted for 46.76% share of the cruciate ligament repair procedures market size in 2025 and biologic scaffolds are advancing at a 10.87% CAGR to 2031.

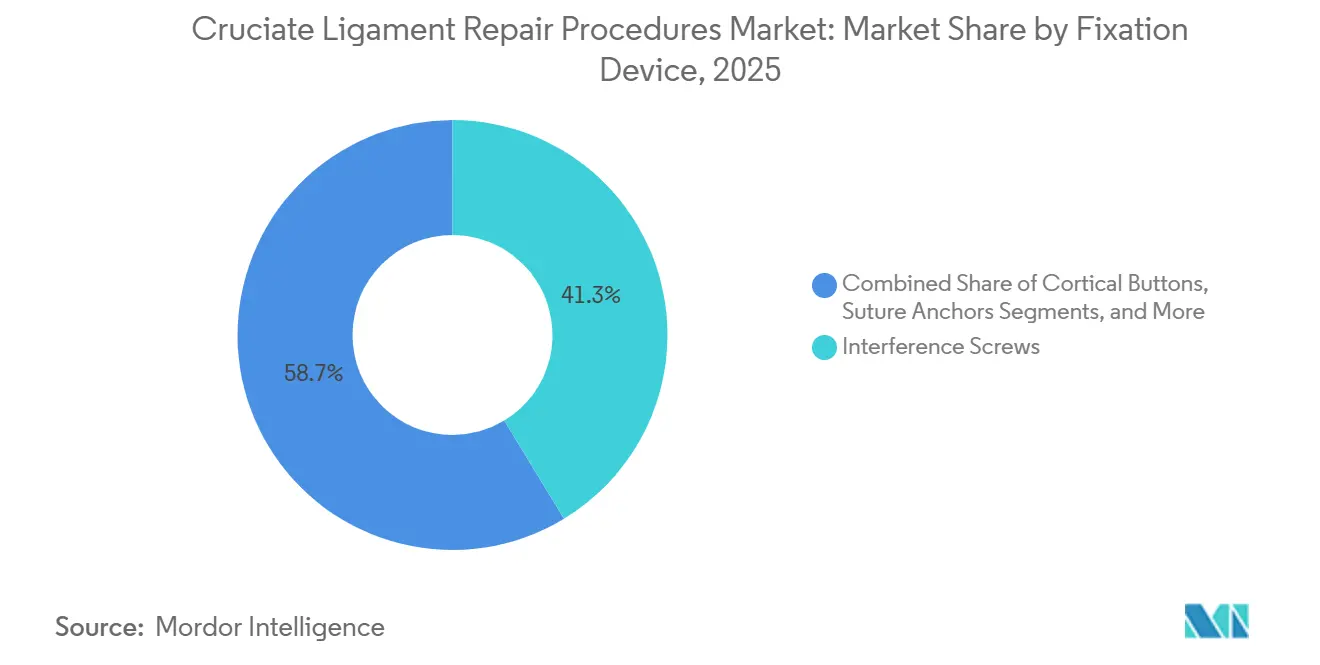

- By fixation device, interference screws retained 41.32% of segment revenue in 2025, whereas cortical buttons are forecast to grow at an 11.21% CAGR between 2026 and 2031.

- By end user, hospitals captured 60.32% of revenue in 2025; ambulatory surgery centers are moving ahead at an 11.45% CAGR through 2031.

- By geography, North America led with 42.65% revenue share in 2025, and Asia-Pacific is expected to record the fastest 9.54% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cruciate Ligament Repair Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Incidence Of Knee Ligament Injuries | +1.8% | Global, peak in North America & Europe | Medium term (2–4 years) |

| Rising Preference For Minimally Invasive Orthopedic Procedures | +2.1% | North America & EU, early APAC uptake | Short term (≤2 years) |

| Growing Availability Of Outpatient Ambulatory Surgery Centers | +1.9% | North America core, Western Europe spill-over | Medium term (2–4 years) |

| Advancements In Biologic And Synthetic Graft Technologies | +2.3% | Global, regulatory lead in North America & EU | Long term (≥4 years) |

| Expanding Sports Medicine Physician Workforce In Emerging Markets | +1.2% | APAC core, Latin America & MEA | Long term (≥4 years) |

| Integration Of Artificial Intelligence Into Surgical Planning & Navigation | +1.5% | North America & EU early adopters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Knee Ligament Injuries

ACL tears occur at a rate of 75.19 per 100,000 person-years in the United States, resulting in 100,000–200,000 new cases annually[1]European Sports Medicine Society, “Arthroscopic Technique Survey 2023,” ncbi.nlm.nih.gov. Female athletes experience rupture rates two- to eight-fold higher than males because of anatomic and hormonal factors, while the 16-to-39-year bracket sees the most trauma. Although annual injury counts eased after 2010, surgical reconstruction volumes continued to climb by 2.15% per year as payers expanded reimbursement and patients demanded quicker return-to-sport timelines. The shift is most visible in North America and Western Europe, where third-party coverage for arthroscopy encourages early surgical decision-making.

Rising Preference for Minimally Invasive Orthopedic Procedures

All-inside arthroscopic techniques now dominate because they avoid tibial tunnel exit points and reduce postoperative pain. European surveys show transtibial drilling fell from 14.3% to 3.6% of high-volume surgeons between 2016 and 2023, while anteromedial and all-inside portals increased. Quadriceps-tendon harvests, which spare the patellar tendon, further improve donor-site morbidity. Arthrex extended its TightRope adjustable-loop button to pediatric ACL reconstruction in 2023, allowing all-epiphyseal fixation that protects the growth plate.

Advancements In Biologic and Synthetic Graft Technologies

The January 2026 BEAR implant label update exhibited lower osteoarthritis progression at two-year follow-up compared with autograft reconstruction. More than 5,000 patients have received the scaffold since FDA expanded indications in March 2025 to children and partial tears[2]FDA, “Expanded Indications for BEAR,” fda.gov. Two-year data report a 15% re-tear rate, paralleling autograft outcomes, and show earlier hamstring-strength recovery. Synthetic polymers are also resurging: Stryker bought Artelon in June 2024 to access bioabsorbable fibers with tensile strengths exceeding 2,000 N.

Integration of Artificial Intelligence into Surgical Planning & Navigation

Machine-learning algorithms achieve up to 98% accuracy for ACL tear diagnosis on magnetic resonance imaging, reducing the need for diagnostic arthroscopy. Planning platforms now suggest tunnel placement and graft diameter tailored to patient anatomy, directly mitigating the technical errors that cause most graft failures. Zimmer Biomet’s OrthoGrid integration and THINK Surgical alliance embed computer-vision guidance into ligament workflows. Smith & Nephew partnered with HOPCo to feed AI analytics into ambulatory centers’ scheduling software.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Total Procedure Cost And Limited Payer Coverage | -1.4% | North America & EU, acute in U.S. private insurance | Short term (≤2 years) |

| Risk Of Surgical Failure And Need For Revision Procedures | -1.1% | Global, highest in young athletes | Medium term (2–4 years) |

| Stringent Regulatory Pathways For Novel Biologic Implants | -0.7% | North America & EU | Long term (≥4 years) |

| Skill Gap Among Surgeons In Emerging Economies | -0.5% | APAC, Latin America & MEA | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Elevated Total Procedure Cost and Limited Payer Coverage

Uninsured U.S. patients face bills of USD 20,000-50,000, while insured patients often pay USD 2,000–6,000 out of pocket. Adolescent charges climbed 70% between 2010 and 2022, prompting stricter prior-authorization guidelines. Medicare’s allowable for CPT 27429 is USD 1,172, which many ambulatory centers consider below cost. Cigna’s August 2024 policy still classifies primary ACL repair as investigational, curbing reimbursement for the BEAR scaffold[3]Cigna, “Medical Necessity for ACL Repair,” cigna.com.

Risk of Surgical Failure and Need for Revision Procedures

Primary reconstruction fails in 3.2%–11.1% of cases, rising to 34.2% among young athletes who return to sport inside nine months. Allograft failure rates reach 25% in patients under 25, compared with 9.6% for autograft. Revision success averages 70%–75%, and two-stage revisions add USD 10,000–15,000 in costs. Only half of all reconstructed patients resume competitive sport, tempering expectations and fueling litigation when outcomes fall short.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure: Repair Gains Traction Amid Biologic Innovation

ACL reconstruction maintained a 54.84% share of the cruciate ligament repair procedures market in 2025. However, ACL repair is forecast to grow at a 10.53% CAGR through 2031 as the BEAR scaffold expands indications. More than 5,000 BEAR procedures have been performed since March 2025, with early data showing a 15% two-year re-tear rate comparable to that of autograft. As a result, repair could capture 15%–20% of primary cases by 2031, especially in younger cohorts that value hamstring preservation and faster rehabilitation. Posterior cruciate ligament (PCL) work accounts for less than 10% of volume because PCL injuries represent only 3%–5% of knee trauma. Revision reconstruction is a stable but growing niche, driven by aging grafts and repeat injuries.

By Graft Type: Autograft Dominance Challenged By Biologic Scaffolds

Autograft tissue generated 46.76% revenue in 2025, supported by bone-patellar tendon-bone and hamstring grafts, which show a 9.6% failure rate under 25 years. Quadriceps-tendon options, commercialized with Smith & Nephew’s QUADTRAC guide, deliver the lowest 2.4% one-year reoperation rate. Allografts remain preferred for older or revision cases despite their 25% failure in young athletes, partly because they shave 15–20 minutes off operating time. Biologic scaffolds, the fastest-growing segment at 10.87% CAGR, are riding the BEAR implant’s expanded clearances and Stryker’s synthetic integrations. Next-generation synthetic grafts may reach a 5%–8% share by 2031 if their durability matches that of autografts.

By Fixation Device: Cortical Buttons Ascend on Adjustability

Interference screws still accounted for 41.32% of revenue in 2025, thanks to lower unit costs, but cortical buttons are projected to grow 11.21% annually as surgeons favor adjustable-loop tensioning. European usage jumped from 52.9% to 69.3% between 2016 and 2023. Buttons reduce tunnel widening and simplify pediatric all-epiphyseal fixation, which received FDA clearance in 2023. Bioabsorbable screws now account for 62.7% of tibial fixation, yet continue to raise concerns about a foreign-body response, sustaining interest in titanium options. Suture anchors and hybrid devices are used in niche applications, such as salvage revisions.

By End User: Ambulatory Surgery Centers Capture Share

Hospitals accounted for 60.32% of end-user revenue in 2025, reflecting their dominance in complex revisions, pediatric cases, and multi-ligament injuries. Still, ambulatory surgery centers are expanding at an 11.45% CAGR because Medicare’s 2024 outpatient rule shifted uncomplicated ACL cases to same-day discharge. ASC facility charges are 20%–30% lower than those of hospital outpatient departments, and surgeon equity incentives attract talent amid a looming orthopedic workforce shortfall. Orthopedic clinics, though vital for referrals and rehab, contribute less than one-fifth of surgical revenue because few possess accredited operating theaters.

Geography Analysis

North America retained 42.65% of global revenue in 2025, performing 100,000–200,000 ACL procedures annually, but growth is moderating as incidence declines while intervention rates plateau. Europe held roughly one-quarter of revenue, transitioning to anatomic tunnel placement and lateral extra-articular augmentation. Asia-Pacific is set to grow 9.54% through 2031, lifted by China’s 82% price cuts that widened rural access even as they pressured supplier margins. Japan and South Korea leverage high bed density to maintain leading procedure rates, whereas India’s fragmented coverage restrains uptake. The Middle East & Africa and South America share about 12%–15% of revenue; investment in Gulf sports medicine and Brazil’s faster device approvals support incremental gains.

Competitive Landscape

The top five vendors—Arthrex, Stryker, Smith & Nephew, Zimmer Biomet, and DePuy Synthes—held 55%–60% of 2025 revenue, pointing to moderate concentration. Stryker’s June 2024 Artelon deal adds synthetic soft-tissue scaffolds, while Smith & Nephew’s USD 330 million CartiHeal acquisition extends its cartilage solutions. Zimmer Biomet’s 2023 purchase of Embody supplied collagen-based implants and helped its sports medicine line grow 13.1% in 2024. Miach Orthopaedics is disrupting with the BEAR scaffold, having treated 5,000+ patients since 2025. Every leader is converging on biologics, robotics, and AI navigation to differentiate from commodity screws and sutures. China’s volume-based procurement is forcing tiered product portfolios and local manufacturing to defend share against MicroPort and Meril.

Cruciate Ligament Repair Procedures Industry Leaders

Zimmer Biomet

Smith & Nephew

Johnson & Johnson Services, Inc. (DePuy Synthes)

CONMED Corporation

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FDA updated the BEAR implant label to include data showing lower post-traumatic osteoarthritis versus autograft ACL reconstruction.

- September 2025: ValleyOrtho introduced a groundbreaking new procedure for ACL repair, promising faster recovery and better outcomes. This innovative technique is poised to revolutionize the treatment of knee injuries.

- June 2024: Stryker acquired Artelon to gain next-generation bioabsorbable synthetic graft technology.

Global Cruciate Ligament Repair Procedures Market Report Scope

As per the scope, cruciate ligaments, also known as cruciform ligaments, are pairs of ligaments that intersect each other like the letter X, and they usually occur in the knee joint and the atlantoaxial joint.

The Cruciate Ligament Repair Procedures Market is Segmented by Procedure (ACL Repair, ACL Reconstruction, PCL Repair, PCL Reconstruction, and Revision Procedures), Graft Type (Autograft, Allograft, Synthetic Graft, nd Biologic Scaffolds), Fixation Device (Interference Screws, Cortical Buttons, Suture Anchors, and Other Fixation Devices), End User (Hospitals, Ambulatory Surgical Centers, and Orthopedic & Sports Medicine Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| ACL Repair |

| ACL Reconstruction |

| PCL Repair |

| PCL Reconstruction |

| Revision Procedures |

| Autograft |

| Allograft |

| Synthetic Graft |

| Biologic Scaffolds |

| Interference Screws |

| Cortical Buttons |

| Suture Anchors |

| Other Fixation Devices |

| Hospitals |

| Ambulatory Surgical Centers |

| Orthopedic & Sports Medicine Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure | ACL Repair | |

| ACL Reconstruction | ||

| PCL Repair | ||

| PCL Reconstruction | ||

| Revision Procedures | ||

| By Graft Type | Autograft | |

| Allograft | ||

| Synthetic Graft | ||

| Biologic Scaffolds | ||

| By Fixation Device | Interference Screws | |

| Cortical Buttons | ||

| Suture Anchors | ||

| Other Fixation Devices | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Orthopedic & Sports Medicine Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the cruciate ligament repair procedures market?

The market is estimated at USD 17.44 billion in 2026.

How fast will the market grow through 2031?

Revenue is expected to rise at an 8.41% CAGR between 2026 and 2031.

Which procedure segment is expanding the quickest?

ACL repair is forecast to grow 10.53% annually as biologic scaffolds gain adoption.

Why are ambulatory surgery centers gaining share?

Medicare's 2024 rule shift and 20%Ð30% lower facility fees are steering uncomplicated ACL cases to same-day centers.

What region shows the fastest future growth?

Asia-Pacific is projected to post a 9.54% CAGR because of wider access and regulatory acceleration.

Which fixation device type is most rapidly adopted?

Cortical buttons lead growth with an 11.21% CAGR due to adjustable tensioning and reduced tunnel widening.

Page last updated on: