Niemann Pick Disease Type C Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

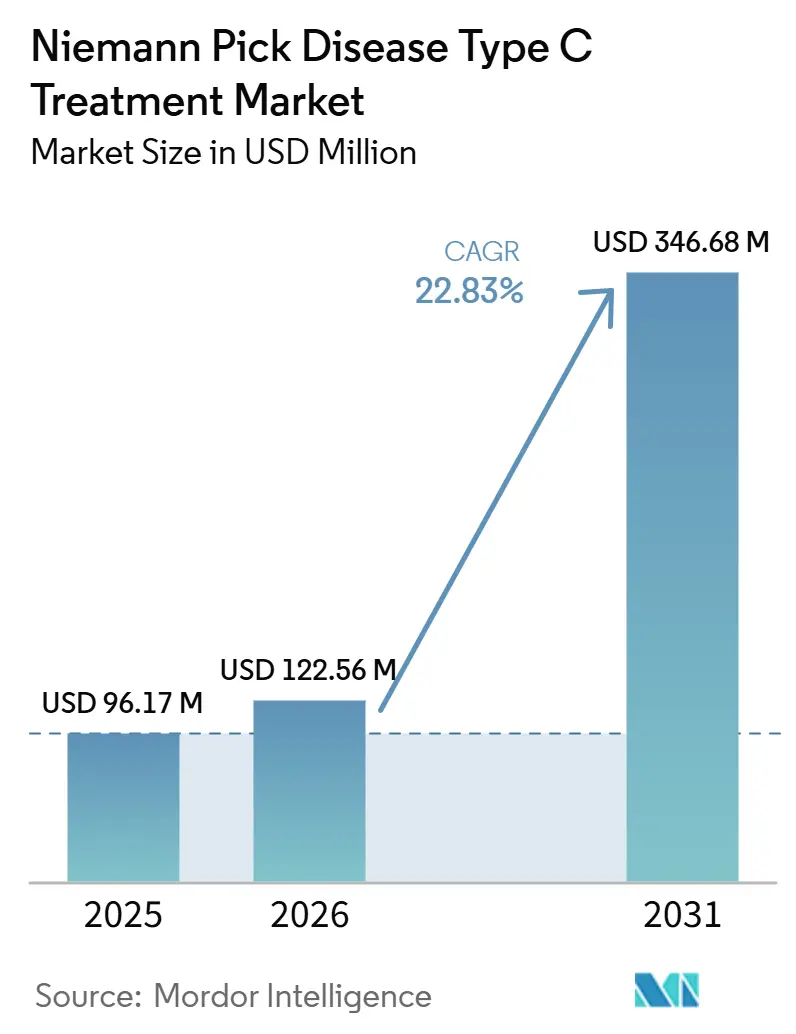

| Market Size (2026) | USD 122.56 Million |

| Market Size (2031) | USD 346.68 Million |

| Growth Rate (2026 - 2031) | 22.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Niemann Pick Disease Type C Treatment Market Analysis by Mordor Intelligence

The Niemann Pick Disease Type C Treatment Market size is projected to be USD 96.17 million in 2025, USD 122.56 million in 2026, and reach USD 346.68 million by 2031, growing at a CAGR of 22.83% from 2026 to 2031.

The market is being driven by recent regulatory approvals of disease-specific therapies, improved genetic diagnosis, increasing awareness of rare lysosomal storage disorders, and a growing pipeline of disease-modifying treatments. Expanding newborn screening initiatives, stronger patient advocacy, and increasing investments in orphan drug development are accelerating treatment adoption. In addition, advancements in gene therapy, substrate reduction therapy, and neuroprotective approaches are expected to broaden future therapeutic options and support sustained market growth.

Key Report Takeaways

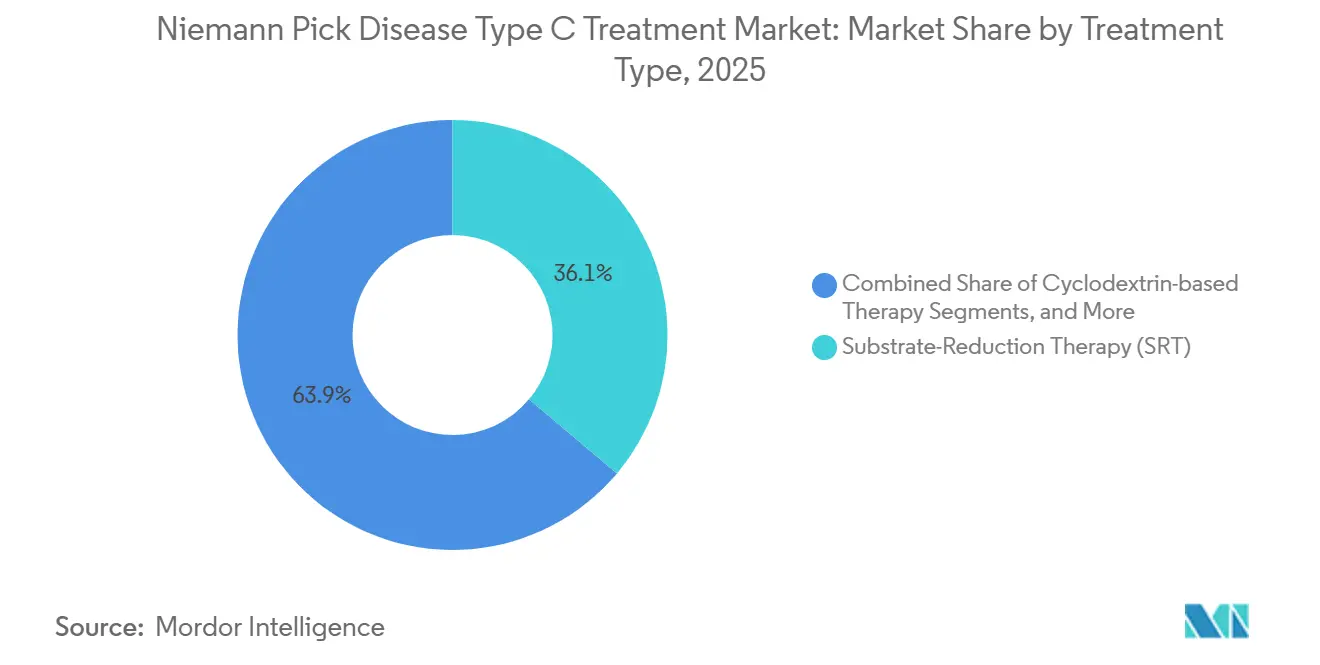

- By treatment type, substrate-reduction therapy (SRT) led the Niemann-Pick Disease Type C treatment market with a 36.13% market share in 2025. In contrast, gene therapy is projected to register the fastest CAGR of 26.25% during 2026–2031.

- By molecule type, small molecules accounted for 56.14% of the Niemann-Pick Disease Type C treatment market in 2025, while gene vectors are expected to witness the highest CAGR of 25.52% through 2031.

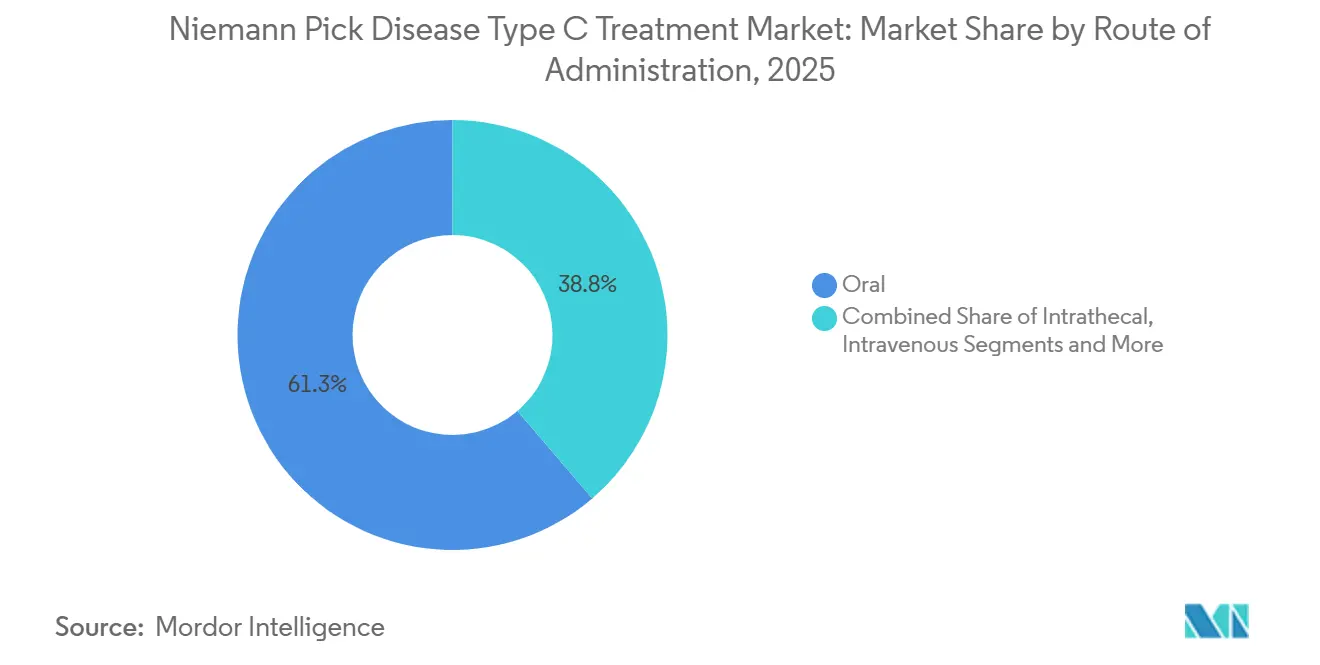

- By route of administration, oral therapies commanded 61.25% of the Niemann-Pick Disease Type C treatment market in 2025. In contrast, intravenous therapies are forecast to expand at the fastest CAGR of 24.73% over the forecast period.

- By patient age group, the pediatric (2–11 years) segment captured 53.63% of the Niemann-Pick Disease Type C treatment market in 2025, while the neonatal (<1 month) segment is anticipated to grow at the highest CAGR of 24.86% through 2031.

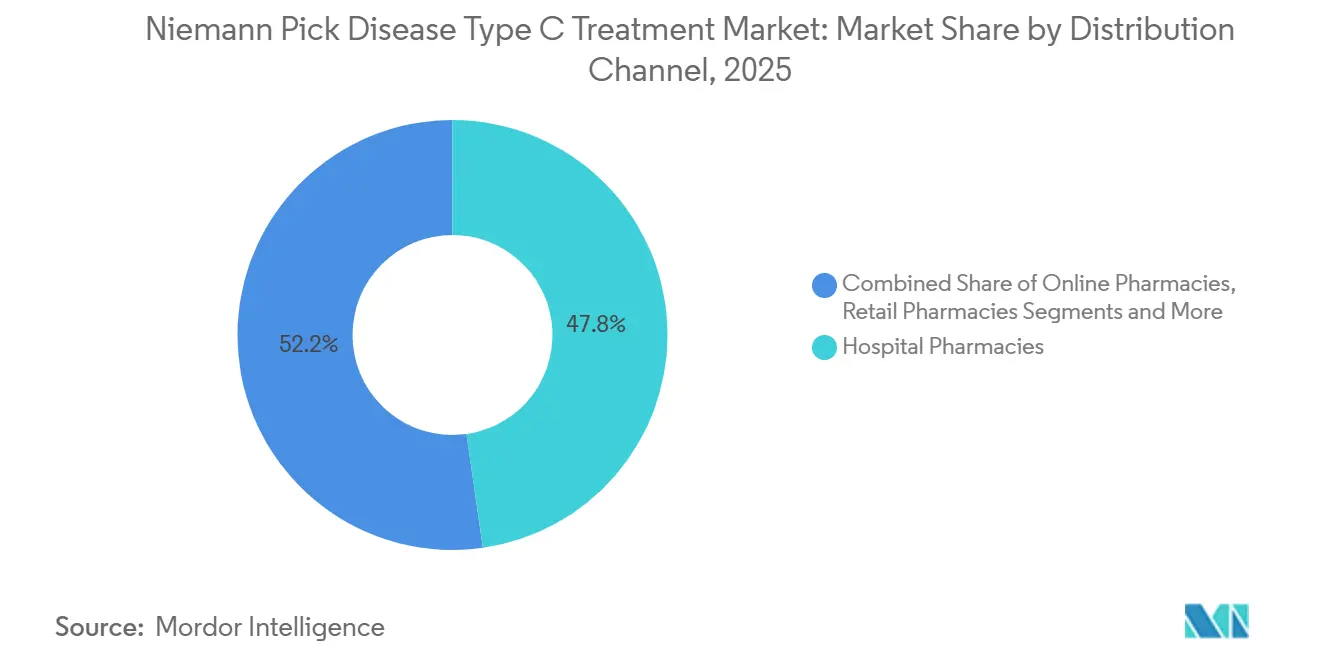

- By distribution channel, hospital pharmacies held a 47.76% share of the Niemann-Pick Disease Type C treatment market in 2025. In contrast, specialty pharmacies are projected to record the fastest CAGR of 26.16% during the forecast period.

- By geography, North America held 41.33% of the Niemann-Pick Disease Type C treatment market share in 2025, while Asia-Pacific is expected to be the fastest-growing regional market with a CAGR of 24.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Niemann Pick Disease Type C Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA Priority Review Vouchers for Ultra-Rare Diseases | +4.2% | North America, spillover to EU | Short term (≤ 2 years) |

| Venture Philanthropy-Backed Biotech Funding Surge | +3.8% | Global, U.S. East Coast hubs | Medium term (2-4 years) |

| Platform Gene-Therapy Technologies Maturing | +3.5% | North America and EU, early adoption in Japan | Long term (≥ 4 years) |

| Orphan-Drug Exclusivity Extensions in APAC | +2.9% | Japan, South Korea, China, Southeast Asia | Medium term (2-4 years) |

| Companion Digital Biomarkers Accelerating Trials | +2.4% | Global, led by U.S. FDA and EMA pilots | Medium term (2-4 years) |

| Industry-Academia Natural History Consortia | +2.1% | Global, anchored by NIH and EU Reference Networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDA Priority Review Vouchers for Ultra-Rare Diseases

The Rare Pediatric Disease Priority Review Voucher program developed into a pivotal subsidy when vouchers changed hands for USD 95 million to USD 110 million in 2024–2025.[1]Food and Drug Administration, “Rare Pediatric Disease Priority Review Voucher Program,” U.S. Food and Drug Administration, fda.gov Zevra Therapeutics and IntraBio recovered roughly half of Phase 3 spending upon voucher sale, reshaping net-present-value calculations that once discouraged investment in populations below 4,000 U.S. patients. Congress extended voucher eligibility through 2026, preserving momentum and encouraging sponsors to target pediatric subgroups first to secure designation. The resulting influx of Investigational New Drug filings is expected to sustain double-digit pipeline growth.

Venture Philanthropy-Backed Biotech Funding Surge

Patient foundations now invest as equity holders, recycling returns into subsequent programs. The Ara Parseghian Fund and similar groups co-financed IntraBio and Regenxbio, shaving a year off typical Series A timelines and supplying vital registries, which otherwise cost USD 5 million to build. Impact-investor families, exemplified by the Gilbert Family Foundation’s USD 125 million neurofibromatosis commitment, view ultra-rare programs as high-upswing social ventures.

Platform Gene-Therapy Technologies Maturing

AAV9 vectors have posted 60-70% NPC1 transgene expression in Purkinje cells and hepatocytes in large-animal models, doubling median survival in knockout mice.[2]Nicholas Druce, “Systemic AAV9-Mediated Gene Therapy for Niemann-Pick Disease Type C,” bioRxiv, biorxiv.org Next-generation capsids such as AAV-PHP.B cross the blood-brain barrier far more efficiently, making single-dose intravenous delivery viable for infants. CDMOs like Catalent and Lonza are tripling AAV output by 2027, which will relieve current dose-supply strain and enable multi-regional launches.

Orphan-Drug Exclusivity Extensions in APAC

Japan stretched exclusivity to 12 years, South Korea to 15 years, and China slashed review times by half for drugs already U.S.- or EU-approved. These incentives matter because pan-Asian prevalence is twice that of Europe yet historically under-diagnosed. Manufacturers can now recoup investment sooner, and tiered pricing in China encourages higher treated-patient volume in exchange for lower per-patient revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Intrathecal Delivery Complication Rates | −2.3% | Global, acute in pediatric cohorts | Short term (≤ 2 years) |

| CMC Scale-Up Hurdles for Cyclodextrin | −1.9% | North America and EU manufacturing hubs | Medium term (2-4 years) |

| Bankruptcy Risks Among Single-Asset Start-Ups | −1.6% | Global, notably venture-backed U.S. and EU firms | Short term (≤ 2 years) |

| Limited Payer Real-World Evidence Datasets | −1.4% | Europe and U.S. HTA jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Intrathecal Delivery Complication Rates

Chemical meningitis and catheter infections occur in 8-12% of intrathecally dosed patients, triggering extra neuro-imaging and payer scrutiny.[3]Stephanie White, “Intrathecal Cyclodextrin Therapy Complications in Niemann-Pick Disease,” Journal of Inherited Metabolic Disease, jimd.net The U.K. National Institute for Health and Care Excellence withheld recommendation for intrathecal miglustat in 2025, citing risk-benefit uncertainty. Gene therapy’s intravenous route aims to sidestep these safety liabilities, though immune-response management remains essential.

CMC Scale-Up Hurdles for Cyclodextrin Formulations

Hydroxypropyl-beta-cyclodextrin batches exceeding 100 kilograms must meet tight impurity thresholds, and failed lots cost up to USD 1 million each. Cyclo Therapeutics postponed its Biologics License Application from Q4 2024 to Q2 2025, stressing limited process robustness at commercial scale. Regulators demand three consecutive compliant runs, a requirement that forces smaller sponsors into CDMO partnerships, inflating cost-of-goods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Gene Therapy Gains Ground

Substrate-Reduction Therapy retained 36.13% Niemann Pick Disease Type C Treatment market share in 2025, largely due to miglustat’s entrenched off-label status. Gene Therapy is projected to compound at 26.25% annually, underpinned by AAV9 candidates such as RGX-NPC1 and PBGM01 entering multicenter trials. The Niemann Pick Disease Type C Treatment market for Gene Therapy is supported by single-dose durability claims and regulatory acceptance of external natural-history controls. Cyclodextrin-based Therapy has adverse event rates and manufacturing hurdles may cap growth. Molecular-chaperone Therapy, led by arimoclomol, benefits from first-mover advantage yet faces skepticism after narrowly missing its primary endpoint.

In clinical models, AAV9 vectors restore 65-70% NPC1 expression and extend survival by half relative to untreated controls. The FDA’s 2024 guidance allows single-arm designs, trimming trial costs by 30%. Cyclodextrins’ ototoxicity signals and logistic burden, including weekly lumbar punctures, challenge physician adoption. Consequently, combination regimens pairing substrate reduction with gene therapy are being explored to offset each modality’s shortcomings.

By Molecule Type: Vectors Surge Despite Small-Molecule Dominance

Small Molecules comprised 56.14% of 2025 revenue, but their dominance will erode as vectors expand at 25.52% CAGR. The Niemann Pick Disease Type C Treatment market share for Gene Vectors is forecast to rise to 34% by 2031, reflecting increasing patient preference for single-dose interventions. Complex Carbohydrates retain a 20% slice yet face CMC barriers. Biologic enzymes remain exploratory due to blood-brain barrier limits.

Preclinical data show AAV9 durability beyond 18 months in non-human primates. Small molecules, though scalable and orally convenient, primarily slow rather than halt neurodegeneration. Complex carbohydrates could lose relevance if gene therapy proves curative and safer intravenous formulations fail to match intrathecal efficacy. Enzyme-replacement strategies may resurface once receptor-mediated transcytosis platforms mature.

By Route of Administration: Oral Leads, Intravenous Accelerates

Oral therapies held 61.25% share in 2025, a testament to patient preference and ease of distribution. Intravenous modalities will grow at a 24.73% CAGR, buoyed by both cyclodextrin infusions and systemic AAV gene therapy. Intrathecal procedures grow more modestly due to complication rates and infrastructure needs.

Intravenous gene therapy broadens eligibility to neonates who cannot undergo lumbar punctures, cutting per-patient procedural costs by up to USD 50,000. Oral agents will continue as maintenance therapy post-gene-transfer. Intrathecal cyclodextrin shows cerebrospinal fluid cholesterol reductions of 30-40% but faces logistical obstacles. Intracerebroventricular reservoirs remain restricted to tertiary centers with neurosurgical capacity.

By Patient Age Group: Neonatal Screening Transforms Demand

Pediatric patients accounted for 53.63% share in 2025, yet neonatal diagnoses will climb rapidly thanks to expanded newborn panels in U.S. states and select EU nations. The Niemann Pick Disease Type C Treatment market share for neonates is growing at 24.86% CAGR. Infant and pediatric cohorts will still dominate absolute volumes, while adolescent and adult groups remain under-diagnosed due to psychiatric-first presentations.

Newborn screening enables presymptomatic intervention, delaying neurological onset by up to 18 months when treatment begins in the first weeks of life. Gene therapy’s one-time dosing fits neonatal care pathways, whereas chronic oral regimens face adherence issues. Diagnostic delays in adolescents compress therapeutic windows, but advocacy campaigns and expanded genetic testing could shorten latency.

By Distribution Channel: Specialty Pharmacies Rise

Hospital pharmacies accounted for 47.76% of revenue in 2025, yet specialty pharmacies will post a 26.16% CAGR, capitalizing on home-based dispensing and outcomes tracking. Retail outlets contribute marginally, and online channels remain nascent due to tight regulation.

Specialty providers manage value-based contracts, supporting adherence and data collection that payers increasingly require. Hospital pharmacies will continue leading for gene therapy infusions and intrathecal dosing. Retail pharmacies might gain only if once-daily oral agents emerge, while online pharmacies face scrutiny under remote-dispensing rules.

Geography Analysis

North America held 41.33% Niemann Pick Disease Type C Treatment market share in 2025. FDA approvals of Miplyffa and Aqneursa, alongside NIH-funded natural-history networks, reduced trial costs and accelerated uptake. Canada’s 2024 ultra-rare disease framework co-funds provincial coverage, improving access, whereas Mexico remains under-penetrated but is building centers of excellence in private hospitals. The region’s reimbursement environment supports list prices above USD 300,000 annually.

In Europe, Germany, France, and the U.K. benefit from long-standing lysosomal storage disease registries, but fragmented health-technology assessment processes delay market entry by over a year after EMA approval. Cross-border European Reference Networks are harmonizing diagnostics and reducing per-patient enrollment costs; however, payer negotiations hinge on long-term efficacy evidence.

Asia-Pacific is projected to grow at 24.02% CAGR through 2031. Japan’s exclusivity extension to 12 years and fast-track reviews shorten commercialization timelines. China’s Priority Review pathway halves median approval time, though reimbursement varies starkly between tier-1 and tier-3 cities. South Korea and Australia have launched government-backed rare-disease registries, attracting global sponsors. India remains nascent because out-of-pocket costs deter uptake.

Rest of World, includes Latin America, the Middle East, and Africa. Brazil’s judicial route occasionally secures orphan-drug coverage, while Gulf countries are investing in genomic medicine as part of national visions. Diagnostic capacity and reimbursement frameworks will remain limiting factors until late in the forecast period.

Competitive Landscape

The Niemann Pick Disease Type C Treatment market is highly fragmented. Tier-one firms (Johnson & Johnson’s Actelion, Sanofi) coexist with venture-backed specialists (IntraBio, Regenxbio, Passage Bio, Cyclo Therapeutics). Actelion’s legacy registries position it for potential acquisitions of late-stage gene-therapy candidates. Smaller firms leverage patient-advocacy partnerships to shorten enrollment cycles; IntraBio completed pivotal trials in 18 months, half the ultra-rare average.

White-space opportunities include combination regimens and next-gen AAV capsids with superior blood-brain barrier penetration. Patent filings for AAV-PHP.B and AAV-PHP.eB reveal a hedging strategy against first-generation obsolescence. CDMOs with lysosomal storage disease suites, notably Catalent and Lonza, gain negotiating power as manufacturing gatekeepers. Regulatory strategy also differentiates contenders: securing a Rare Pediatric Disease Voucher delivers USD 100 million of non-dilutive capital, funding pipeline expansion and reinforcing competitive advantage.

Niemann Pick Disease Type C Treatment Industry Leaders

Johnson & Johnson

IntraBio Ltd.

Rafael Holdings

Mandos LLC

Orphazyme A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Data from Cyclo Therapeutics’ Phase 3 TransportNPC open-label sub-study of Trappsol Cyclo were presented at the 15th ICIEM, highlighting intravenous dosing at 2,000 mg/kg

- September 2024: The FDA cleared Zevra Therapeutics’ Miplyffa for NPC, granting the company a Priority Review Voucher valued near USD 100 million

- September 2024: IntraBio received FDA approval for Aqneursa, securing a Priority Review Voucher and initiating a 5-year, 200-patient registry

Global Niemann Pick Disease Type C Treatment Market Report Scope

Niemann-Pick Disease Type C (NPC) treatment is a multidisciplinary approach aimed at slowing the progression of this rare neurodegenerative disorder by managing symptoms and reducing lipid accumulation in the brain and tissues.

The Niemann-Pick Disease Type C Treatment Market Report is segmented by Treatment Type, Molecule Type, Route of Administration, Patient Age Group, Distribution Channel, and Geography. By Treatment Type, the market is segmented into Substrate-Reduction Therapy, Cyclodextrin-based Therapy, Molecular-Chaperone Therapy, Gene Therapy, and Symptomatic/Adjunctive Therapy. By Molecule Type, the market is segmented into Small Molecule, Complex Carbohydrate, Gene Vector, Biologic Enzyme, and Combination/Other. By Route of Administration, the market is segmented into Oral, Intrathecal, Intravenous, Intracerebroventricular, and Subcutaneous. By Patient Age Group, the market is segmented into Neonate, Infant, Pediatric, Adolescent, Adult, and Geriatric. By Distribution Channel, the market is segmented into Hospital Pharmacies, Specialty Pharmacies, Retail Pharmacies, and Online Pharmacies. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of World. Market Forecasts are Provided in Terms of Value (USD).

| Substrate-Reduction Therapy (SRT) |

| Cyclodextrin-based Therapy |

| Molecular-Chaperone Therapy |

| Gene Therapy |

| Symptomatic / Adjunctive Therapy |

| Small Molecule |

| Complex Carbohydrate |

| Gene Vector |

| Biologic Enzyme |

| Combination / Other |

| Oral |

| Intrathecal |

| Intravenous |

| Intracerebroventricular (ICV) |

| Subcutaneous (supportive) |

| Neonate (< 1 month) |

| Infant (1–24 months) |

| Pediatric (2–11 years) |

| Adolescent (12–17 years) |

| Adult (18–64 years) |

| Geriatric (≥ 65 years) |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Treatment Type | Substrate-Reduction Therapy (SRT) | |

| Cyclodextrin-based Therapy | ||

| Molecular-Chaperone Therapy | ||

| Gene Therapy | ||

| Symptomatic / Adjunctive Therapy | ||

| By Molecule Type | Small Molecule | |

| Complex Carbohydrate | ||

| Gene Vector | ||

| Biologic Enzyme | ||

| Combination / Other | ||

| By Route of Administration | Oral | |

| Intrathecal | ||

| Intravenous | ||

| Intracerebroventricular (ICV) | ||

| Subcutaneous (supportive) | ||

| By Patient Age Group | Neonate (< 1 month) | |

| Infant (1–24 months) | ||

| Pediatric (2–11 years) | ||

| Adolescent (12–17 years) | ||

| Adult (18–64 years) | ||

| Geriatric (≥ 65 years) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the projected value of the Niemann Pick Disease Type C Treatment market in 2031?

The market is forecast to reach USD 346.68 million by 2031 at a 22.83% CAGR.

Which treatment modality is expected to grow the fastest through 2031?

Gene Therapy is poised to expand at a 26.25% CAGR, buoyed by AAV9-based candidates entering mid-stage trials.

How significant are specialty pharmacies in future distribution?

Specialty pharmacies are forecast to grow at 26.16% CAGR and surpass USD 140 million in channel revenue by 2031.

Why is the Asia-Pacific region attractive for sponsors?

APAC growth at 24.02% CAGR stems from Japan’s longer exclusivity windows and China’s expedited review pathways.

What are the main safety concerns limiting intrathecal therapies?

Chemical meningitis and catheter infections occur in up to 12% of cases, prompting payer caution and regulatory monitoring.

How do Priority Review Vouchers impact developer economics?

Vouchers worth roughly USD 100 million can offset nearly half of late-stage trial costs, encouraging investment in ultra-rare indications.

Page last updated on: