Knee Cartilage Repair Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Knee Cartilage Repair Market Analysis by Mordor Intelligence

The knee cartilage repair market size is expected to grow from USD 1.88 billion in 2025 to USD 1.99 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 5.71% CAGR over 2026-2031. Steady growth rests on the worldwide rise in knee osteoarthritis cases, wider adoption of minimally invasive surgery, and technology that improves scaffold design and cell processing. Strong reimbursement in high-income nations and expanding outpatient care models further widen patient access. At the same time, 3D printing and allogeneic cell platforms shorten lead times, reduce costs, and position suppliers for large-scale production.

Key Report Takeaways

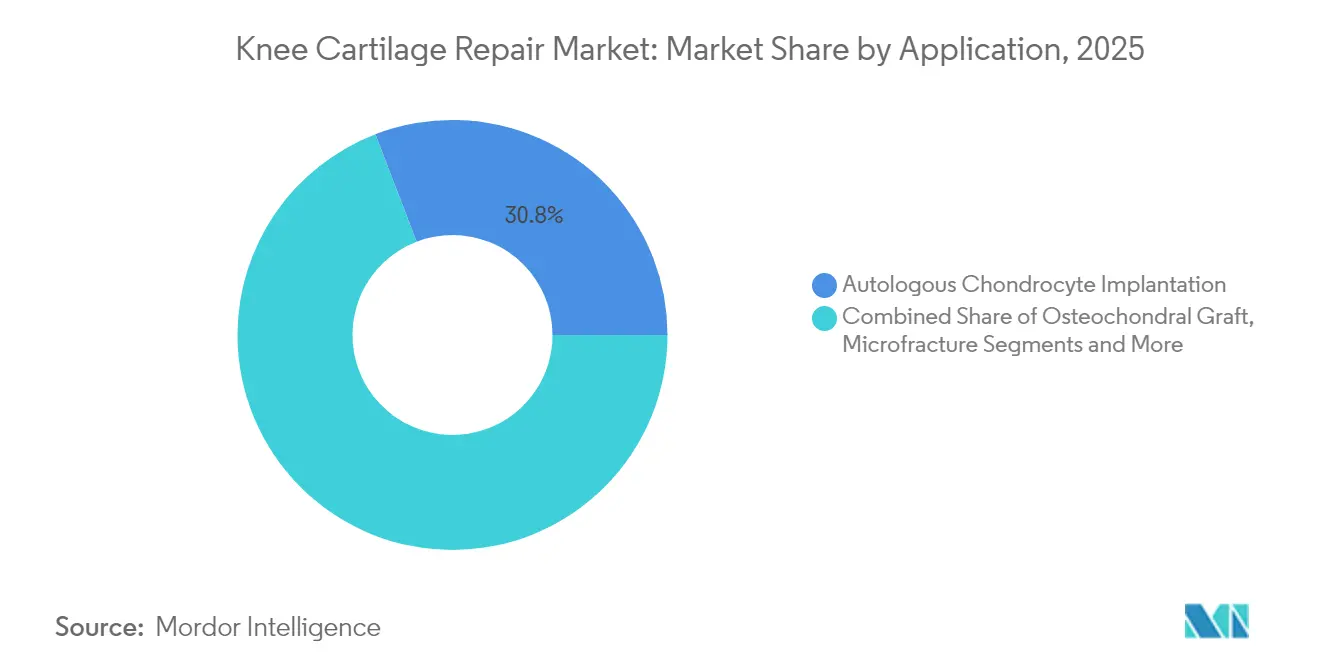

- By application, autologous chondrocyte implantation led with 30.84% knee cartilage repair market share in 2025, while synthetic and 3D printed scaffolds are projected to grow at an 8.56% CAGR to 2031.

- By surgical approach, conventional arthroscopy held 61.92% of the knee cartilage repair market size in 2025; robotic-assisted systems record the fastest CAGR at 8.01% through 2031.

- By biomaterial type, collagen-based scaffolds accounted for 35.78% of the knee cartilage repair market size in 2025; 3D bioprinted osteochondral constructs are set to expand at 9.6% CAGR to 2031.

- By cell source, autologous chondrocytes commanded 39.22% knee cartilage repair market share in 2025, yet allogeneic chondrocytes are on track for a 9.32% CAGR through 2031.

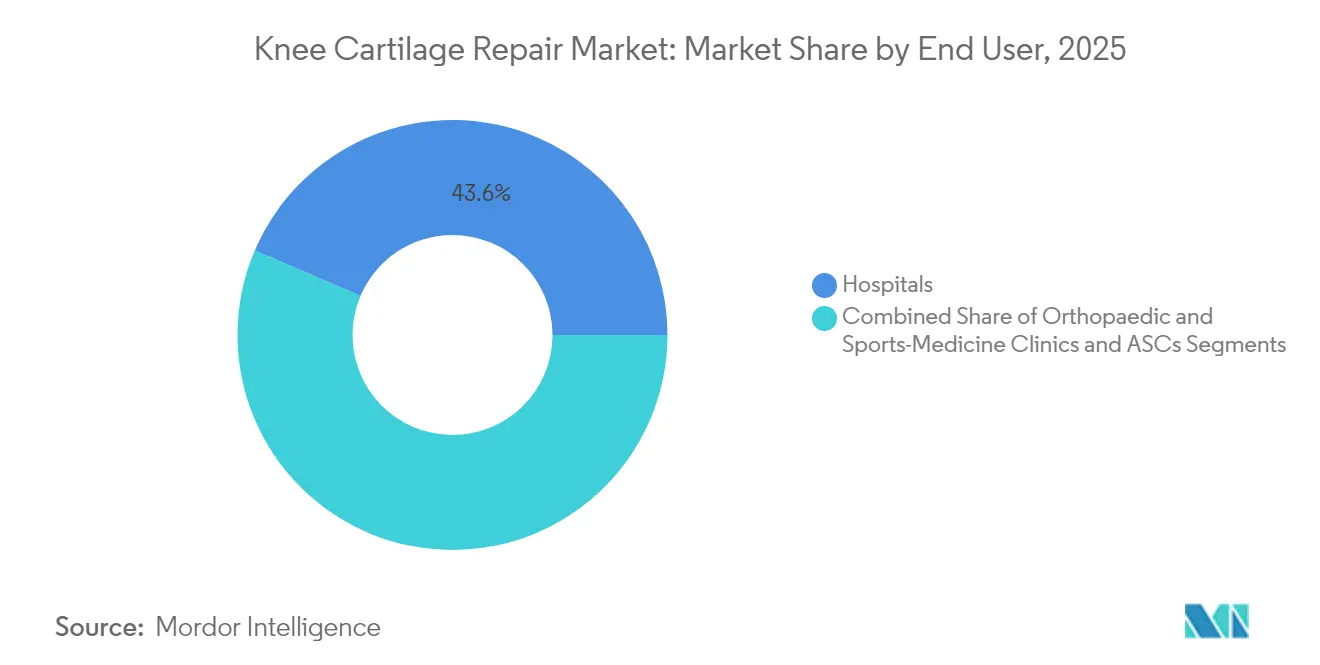

- By end user, hospitals captured 43.58% of the knee cartilage repair market in 2025, whereas ambulatory centers will rise at 7.97% CAGR to 2031.

- By patient age group, individuals aged 45-64 years held 46.03% knee cartilage repair market share in 2025; the 25-44-year cohort is the fastest growing at 7.33% CAGR to 2031.

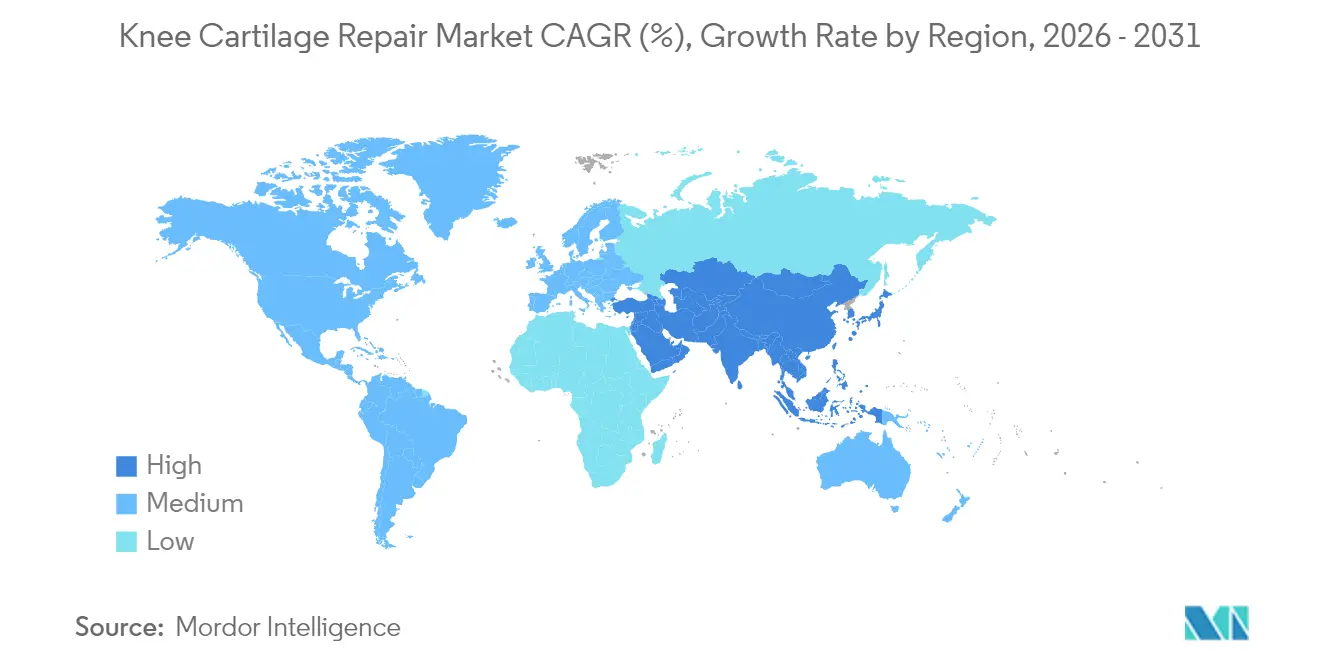

- By geography, North America led with 35.05% knee cartilage repair market share in 2025, while Asia-Pacific is forecast to climb at 8.35% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Knee Cartilage Repair Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly-Ageing Population & Knee-OA Prevalence | 1.8% | Global, with concentration in Japan, Europe, North America | Long term (≥ 4 years) |

| Rising Sports & Road-Trauma Injuries | 1.2% | North America, Europe, emerging APAC markets | Medium term (2-4 years) |

| Preference For Minimally-Invasive & Outpatient Arthroscopy | 1.0% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Regulatory Green-Lighting Of Allogeneic Chondrocyte Products | 0.9% | North America, EU, with spillover to APAC | Medium term (2-4 years) |

| 3-D Printed Osteochondral Scaffolds Entering Pivotal Trials | 0.7% | North America, select EU markets | Long term (≥ 4 years) |

| Bundled-Payment Shift Accelerating Same-Day Knee Procedures | 0.6% | United States primarily, early adoption in select EU markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapidly ageing population and knee osteoarthritis prevalence

Global osteoarthritis cases exceeded 607 million in 2021, with knee disease making up the largest share. Female patients carry a disproportionate burden and high body mass index multiplies disability risk, driving earlier intervention needs.[1]A. Cui et al., “Global, Regional Prevalence, Incidence and Risk Factors of Knee Osteoarthritis in Population-Based Studies,” EClinicalMedicine, thelancet.com Younger yet heavier cohorts therefore seek durable regenerative solutions rather than short-term palliative care. The resulting demand for scalable therapies stretches across regions and underpins long-term growth for the knee cartilage repair market.

Rising sports and road-trauma injuries

Younger adults account for a sharp rise in acute cartilage lesions. The 25–44-year bracket shows the fastest procedure growth because athletes and accident patients insist on high-function recovery. Engineered nasal-septum cartilage matured for two weeks has outperformed traditional constructs in recent trials, helping players return to impact activities sooner.[2]S. Nakamura et al., “Clinical Outcomes of Bone Marrow Aspirate Concentrate for Knee Osteoarthritis: A Systematic Review,” Medicina, mdpi.com Insurers and employers value the productivity gains, supporting premium pricing within the knee cartilage repair market.

Preference for minimally invasive and outpatient arthroscopy

Arthroscopic techniques move many knee cartilage repairs into ambulatory centers where costs are lower and same-day discharge is standard. Meta-analyses report no safety penalty when compared with inpatient care while emphasizing savings that appeal to payers.[3]Nikhil Ponugoti, “Safety, Efficacy and Cost-Effectiveness of Outpatient versus Inpatient Joint Arthroplasty: A Systematic Review and Meta-Analysis,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com In 2024, the US regulator cleared arthroscopic delivery of MACI, broadening the surgeon pool and accelerating adoption. These advances favor devices purpose-built for small-incision work in the knee cartilage repair market.

Regulatory approval of allogeneic chondrocyte products

The push toward standardized donor cell lines lifts capacity constraints that hinder autologous approaches. In pivotal trials, umbilical cord blood-derived mesenchymal stem cells repaired larger defects more effectively than microfracture nature.com. Regulatory fast-track programs in the United States and Europe shorten review cycles, enabling pharmaceutical-style manufacturing and global distribution that expand the knee cartilage repair market.

Restraints Impact Analysis of Knee Cartilage Repair Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Episode-Of-Care Cost & Reimbursement Uncertainty | -1.4% | Global, with acute impact in price-sensitive markets | Short term (≤ 2 years) |

| Variability In Long-Term Clinical Outcomes | -0.8% | Global, particularly affecting adoption in evidence-based markets | Medium term (2-4 years) |

| Limited GMP Cell-Processing Capacity Causing Therapy Delays | -0.6% | North America, EU, with emerging impact in APAC | Short term (≤ 2 years) |

| Surgeon Learning-Curve For Advanced Biologic Techniques | -0.4% | Global, with regional variations in training infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High episode-of-care cost and reimbursement uncertainty

Robot-assisted total knee surgery carries extra costs of USD 2,400–15,000 per case despite shorter stays and fewer complications. When payers question long-term value, hospitals hesitate to adopt new implants, restraining early volumes in the knee cartilage repair market.

Variability in long-term clinical outcomes

Patient-reported improvements diverge widely across lesion sizes, defect locations, and comorbidity profiles. In some cohorts, microfracture results degrade after two years, whereas cell-based implants sustain benefit. The evidence gap keeps guidelines cautious and slows broad uptake in the knee cartilage repair market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Knee Cartilage Repair Market Segment Analysis

By Application:

Cell-Based Therapies Lead InnovationAutologous chondrocyte implantation captured 30.84% knee cartilage repair market share in 2025 on the back of long-standing clinical data and growing use of MACI patches. Prospective trials showed durable pain relief and structural repair when compared with microfracture at five years. Synthetic and 3D printed scaffolds are expanding at an 8.56% CAGR to 2031 because they eliminate two-stage harvest and culture, improve logistics, and lower overall operating room time.

Microfracture remains common for small defects but faces erosion as larger lesions demand true hyaline repair. Osteochondral autografts and allografts serve focal cavities where immediate structural support is essential. Research teams have also reported “dancing molecule” peptides that trigger rapid chondrogenesis, a discovery that could transform early-stage interventions should human data confirm preclinical findings.

By Surgical Approach:

Robotic Precision Gains MomentumConventional arthroscopy represented 61.92% of the knee cartilage repair market size in 2025 due to its familiarity, short case times, and widespread instrumentation. Robotic systems, however, advance at an 8.01% CAGR through 2031 as hospitals seek reproducible alignment and defect mapping. Clinical audits found the VELYS platform cut 90-day revisit rates to 13.9% against 22.8% for other robots and trimmed total episode costs.

Open surgery still matters for complex reconstructions that surpass the reach of arthroscopic portals, yet volume declines as scopes and robots extend capability. Artificial intelligence overlays and augmented reality displays are already in pilot use, offering step-by-step guidance that shortens the learning curve and raises consistency across the knee cartilage repair market.

By Biomaterial Type:

3D Bioprinting Transforms PossibilitiesCollagen remains the workhorse scaffold, supporting 35.78% of market revenue in 2025 with its proven safety and well-defined regulatory path. Next-generation 3D bioprinted osteochondral constructs climb at 9.6% CAGR because layer-by-layer deposition matches native depth-dependent mechanical properties. Investigators using anisotropic printing have matched compressive moduli seen in healthy femoral condyles.

Hyaluronic acid gels and chitosan sheets serve low-load areas, while polylactic and polycaprolactone polymers deliver strength and controlled resorption. Ceramic additives increase stiffness for high-impact zones. Blending these materials with cell suspensions during printing opens the door to single-procedure cartilage resurfacing within the knee cartilage repair market.

By Cell Source:

Allogeneic Solutions Address ScalabilityAutologous chondrocytes generated 39.22% knee cartilage repair market share in 2025 yet require patient tissue harvest and weeks of culture. Allogeneic chondrocytes escalate at 9.32% CAGR, leveraging donor lots that remove the waiting period. Randomized studies report superior International Knee Documentation Committee scores for umbilical cord-derived mesenchymal cells versus microfracture in moderate lesions.

Adipose-derived stem cells also show rapid pain relief within 3 months post-injection, though stromal vascular fraction therapies need up to 12 months for similar benefit. Acellular matrices laden with growth factors appeal where regulatory or immunologic hurdles limit live-cell imports.

By End User:

Ambulatory Centers Capture GrowthHospitals hold 43.58% of revenue due to intensive care infrastructure and insurance contracts. Ambulatory surgical centers expand at 7.97% CAGR as payers reward lower facility fees and patients prefer next-day mobility. Meta-reviews of more than 260,000 cases reveal equivalent infection and readmission rates between outpatient and inpatient cohorts.

Specialized orthopedic clinics focus on athletes and military personnel who demand accelerated rehab. Integration of imaging, surgery, and physiotherapy under one roof boosts care continuity and revenue capture, a model expected to propagate further within the knee cartilage repair market.

By Patient Age Group:

Middle-Aged Patients Drive VolumeAdults aged 45-64 supply nearly half of total procedures because their cartilage degeneration is symptomatic yet their joint life expectancy favors preservation over replacement. The knee cartilage repair market size for this cohort will keep rising as obesity amplifies lesion incidence. Meanwhile, the 25-44 group grows fastest as sports injuries and active lifestyles converge with willingness to pursue restorative options.

Pediatric demand is nascent yet important. A multicenter US trial evaluates MACI against microfracture in patients 10-17 years old, aiming to secure a label extension that could reduce long-term disability risk.

At the opposite end, patients over 65 often show diminished regenerative capacity, though bone marrow aspirate concentrate has achieved meaningful pain relief in moderate osteoarthritis.

Geography Analysis

North America Knee Cartilage Repair Market

North America accounted for 35.05% knee cartilage repair market share in 2025, supported by robust reimbursement, a large installed base of arthroscopes and robots, and ongoing surgeon training programs. Autologous procedures dominate, yet insurers now authorize donor-cell implants under coverage with evidence pathways, broadening therapeutic choice. CPT and HCPCS code updates in 2025 streamline claims, reducing administrative delays and reinforcing volume growth.

Europe Knee Cartilage Repair Market

Europe remains technologically advanced but cost containment policies moderate high-price implant uptake. EU Medical Devices Regulation mandates stricter post-market vigilance, pushing suppliers to expand clinical follow-up and registry participation. Nations with bundled payment pilots, such as Germany and the Netherlands, prioritize day-surgery conversions that benefit arthroscopic MACI and scaffold implants.

APAC Knee Cartilage Repair Market

Asia-Pacific advances at an 8.35% CAGR through 2031 as China, South Korea, and Australia scale specialty orthopedic centers. Hospital records show escalating knee arthroplasty in younger Chinese patients, a warning sign that early cartilage repair demand will grow rapidly. Japan confronts consumer hesitancy; only 17% of patients have opted for knee surgery in surveys, citing fear and limited awareness. Educational campaigns and minimally invasive options aim to lift uptake, providing upside for the knee cartilage repair market.

Middle East and South America Knee Cartilage Repair Market

Emerging Middle East and South American economies invest in private orthopedic clinics catering to medical tourists. Although procedure counts remain small, improving insurance coverage and surgeon repatriation programs indicate long-term opportunity. Import tariffs and registration lags, however, currently restrict immediate market entry.

Competitive Landscape

The knee cartilage repair market shows moderate fragmentation. Global orthopedic majors pursue bolt-on deals to secure novel biomaterials and cell lines. Smith+Nephew paid USD 180 million for CartiHeal in January 2024 to gain a coral-derived scaffold that cuts the need for early total knee replacement by 87% at four years. Integration leverages the buyer’s distribution scale and surgeon network to accelerate uptake.

Zimmer Biomet posted USD 745.1 million in knee revenues in Q3 2024, up 5.5%, reflecting steady demand for legacy implants and early traction for its mini-incision systems. DePuy Synthes invests heavily in 3D printing to customize osteochondral plugs, while Stryker channels R&D into robot-enabled navigation modules that enhance defect mapping accuracy.

Younger firms focus on platform innovations. CytexOrtho secured USD 18 million in grants to refine polycaprolactone scaffolds that match native cartilage modulus and aim for Class III device clearance. Active Implants continues pivotal trials for a polyurethane meniscus replacement that has FDA breakthrough status. These ventures rely on venture and grant funding to reach regulatory milestones before partnering with larger strategics.

Long-term differentiation stems less from niche mechanical tweaks and more from scalable manufacturing, proven durability, and health-economic evidence. Players able to justify premium list prices with real-world outcome data will consolidate share as payers shift to value-based contracts.

Knee Cartilage Repair Industry Leaders

-

Smith & Nephew

-

Stryker

-

Zimmer Biomet Holdings, Inc.

-

Johnson & Johnson

-

Arthrex Inc

- *Disclaimer: Major Players sorted in no particular order

Knee Cartilage Repair Market Companies Covered in this Report

- Anika Therapeutics

- Arthrex

- B. Braun

- Conmed

- Johnson & Johnson

- Kolon TissueGene

- MEDIPOST

- Smiths Group

- Stryker

- Vericel

- Zimmer Biomet

- Geistlich Pharma

- Orthocell

- BioTissue AG

- CollPlant Biotechnologies

- Tissue Regenix Group

- Hyalex Orthopaedics

- CytexOrtho

Recent Industry Developments in Knee Cartilage Repair Market

- March 2025: University of Basel scientists reported that two-week maturation of nasal-septum cell constructs improved clinical cartilage repair outcomes in a 98-patient study.

- March 2025: Montefiore Orthopedics began implanting the Smith+Nephew AGILI-C device for focal cartilage and bone lesions in eligible US patients.

- November 2024: CytexOrtho received USD 18 million in government grants to progress biocompatible polycaprolactone implants aimed at early-stage osteoarthritis.

- October 2024: Regenity Biosciences obtained US clearance for RejuvaKnee, a collagen meniscal scaffold designed for minimally invasive insertion.

Global Knee Cartilage Repair Market Report Scope

As per the scope of the report, cartilage damage is repaired using arthroscopic surgery, which means minimal impact on healthy parts of the knee, less scarring, and quicker recovery times. The report includes both products and therapies. The cartilage may be removed, trimmed, or smoothed down using special tools. The Knee Cartilage Repair Market is Segmented by Application (Arthroscopic Chondroplasty, Autologous Chondrocyte Implantation, Cell-based Cartilage Resurfacing, Osteochondral Grafts Transplantation, and Others), End User (Hospitals, Ambulatory Surgical Centers, and Orthopedic Clinics), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

Segmentation Overview

| Arthroscopic Chondroplasty |

| Microfracture |

| Osteochondral Graft |

| Autologous Chondrocyte Implantation (ACI & MACI) |

| Cell-based Cartilage Resurfacing (MSC, SVF, iPSC) |

| Synthetic / 3-D Printed Scaffold Implants |

| Open Surgery |

| Conventional Arthroscopy |

| Robotic-Assisted Arthroscopy |

| Collagen-based |

| Hyaluronic-Acid / Chitosan |

| Synthetic Polymer (PGA, PLA, PCL) |

| Ceramic / Composite |

| 3-D Bioprinted Osteochondral Scaffolds |

| Autologous Chondrocytes |

| Allogeneic Chondrocytes |

| Mesenchymal Stem Cells |

| Acellular Biologic Grafts |

| Hospitals |

| Ambulatory Surgical Centers |

| Orthopaedic & Sports-Medicine Clinics |

| < 25 years |

| 25 – 44 years |

| 45 – 64 years |

| ≥ 65 years |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Arthroscopic Chondroplasty | |

| Microfracture | ||

| Osteochondral Graft | ||

| Autologous Chondrocyte Implantation (ACI & MACI) | ||

| Cell-based Cartilage Resurfacing (MSC, SVF, iPSC) | ||

| Synthetic / 3-D Printed Scaffold Implants | ||

| By Surgical Approach | Open Surgery | |

| Conventional Arthroscopy | ||

| Robotic-Assisted Arthroscopy | ||

| By Biomaterial Type | Collagen-based | |

| Hyaluronic-Acid / Chitosan | ||

| Synthetic Polymer (PGA, PLA, PCL) | ||

| Ceramic / Composite | ||

| 3-D Bioprinted Osteochondral Scaffolds | ||

| By Cell Source | Autologous Chondrocytes | |

| Allogeneic Chondrocytes | ||

| Mesenchymal Stem Cells | ||

| Acellular Biologic Grafts | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Orthopaedic & Sports-Medicine Clinics | ||

| By Patient Age Group | < 25 years | |

| 25 – 44 years | ||

| 45 – 64 years | ||

| ≥ 65 years | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the knee cartilage repair market?

The market is valued at USD 1.99 billion in 2026 and is projected to reach USD 2.62 billion by 2031, reflecting a 5.71% CAGR.

Which application segment leads the knee cartilage repair market?

Autologous chondrocyte implantation led with 30.84% revenue share in 2025, supported by strong long-term clinical data.

How fast is the robotic-assisted segment growing?

Robotic platforms are advancing at an 8.01% CAGR through 2031, outpacing conventional arthroscopy.

Why are allogeneic chondrocytes gaining attention?

Allogeneic cell lines remove the patient-specific culture step, enabling faster treatment and economies of scale that support a 9.32% CAGR.

Which region is the fastest-growing market?

Asia-Pacific is forecast to expand at 8.35% CAGR due to aging populations and improving surgical infrastructure.

Page last updated on: