Unicompartmental Knee Prosthesis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

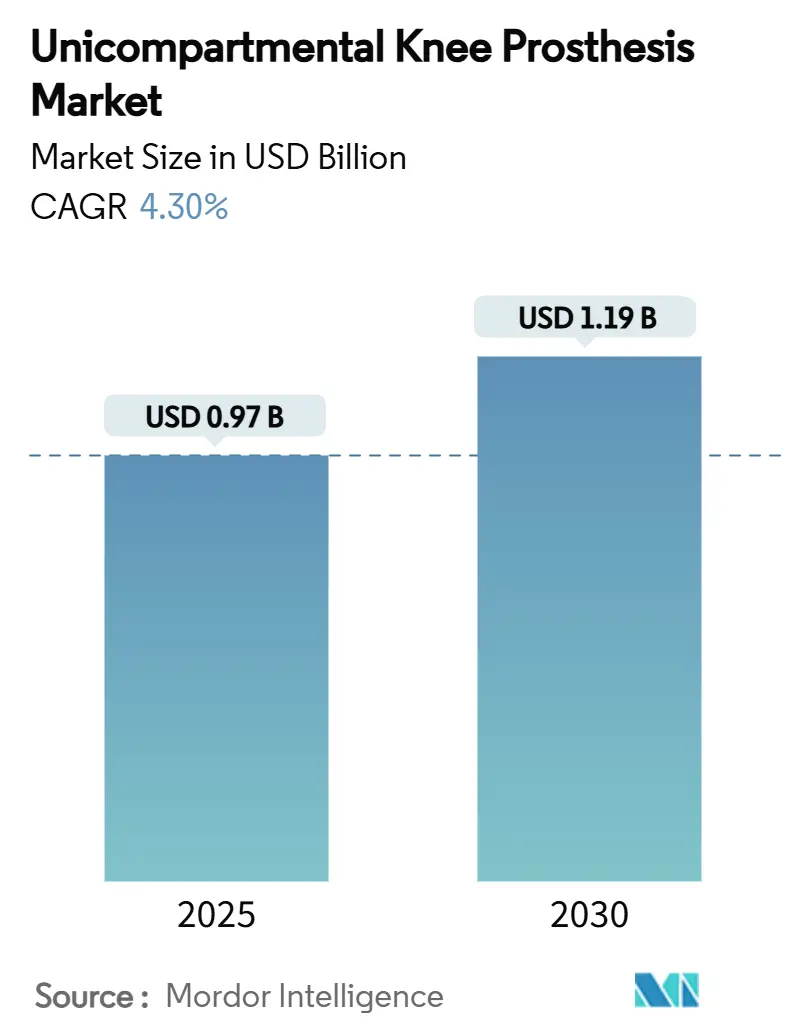

| Market Size (2025) | USD 0.97 Billion |

| Market Size (2030) | USD 1.19 Billion |

| Growth Rate (2025 - 2030) | 4.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unicompartmental Knee Prosthesis Market Analysis by Mordor Intelligence

The unicompartmental knee prosthesis market size touched USD 0.97 billion in 2025 and is forecast to expand at a 4.3% CAGR to USD 1.19 billion by 2030, underscoring the steady but decisive shift toward focused joint-preserving surgery. Technology that blends cementless fixation, mobile-bearing kinematics, and robotic precision is broadening surgeon confidence while appealing to younger, more active patients who value shorter stays and higher functional scores. Demand also benefits from ambulatory surgical center (ASC) reimbursement reforms that reward outpatient partial-knee episodes and from accelerated device approvals that shorten innovation cycles. Meanwhile, specialized suppliers use patient-specific guides and high-porosity titanium coatings to match the longevity expectations of a cohort whose average age at surgery keeps falling. Competitive positioning now revolves around comprehensive platforms that wrap implants, navigation software, and analytics into a single procedural workflow.

Key Report Takeaways

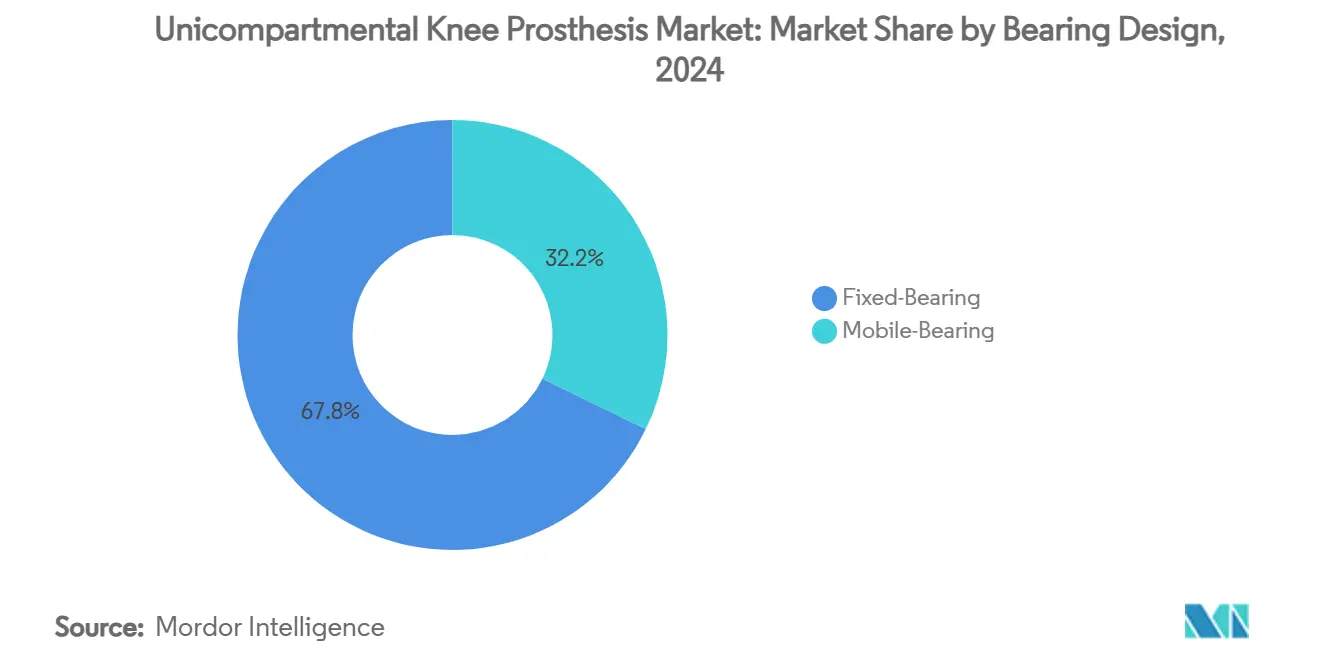

- By bearing design, fixed systems accounted for 67.8% of 2024 revenue, whereas mobile systems are projected to post the fastest 4.9% CAGR through 2030.

- By fixation method, cemented solutions held 72.6% of 2024 volume; cementless variants are advancing at a 4.7% CAGR on ten-year survivorship gains.

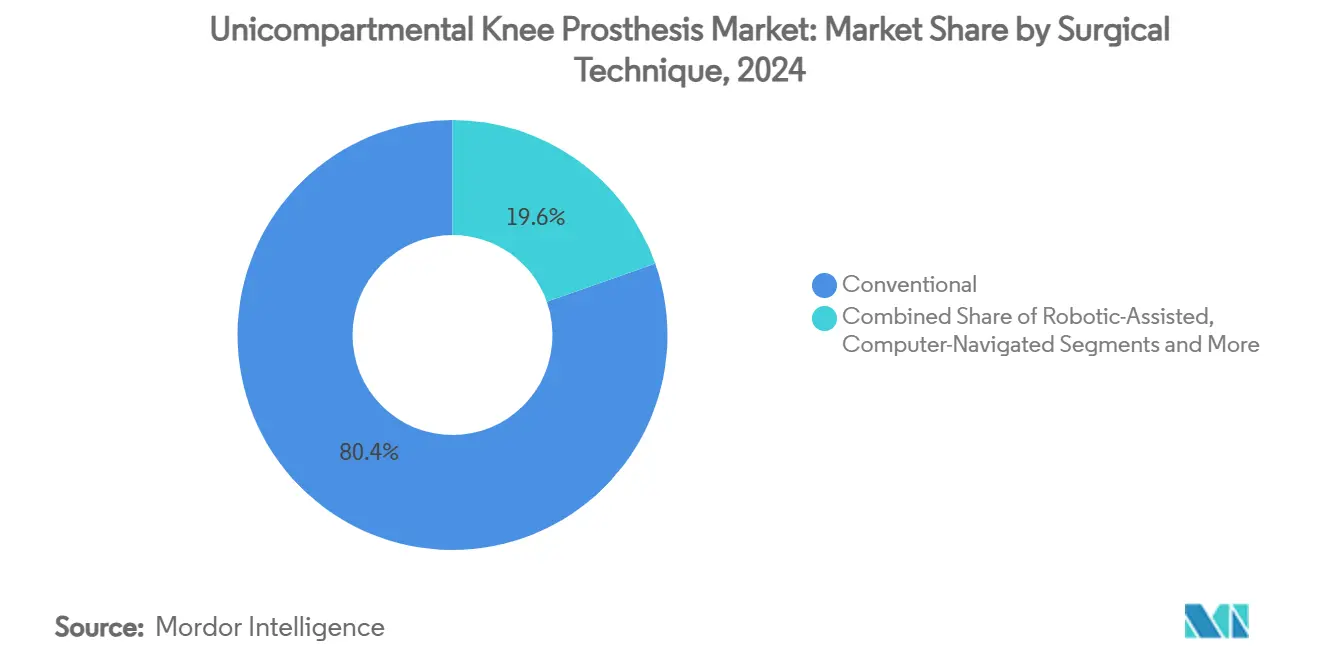

- By surgical technique, robotic-assisted surgery represented the quickest-expanding technique, growing at 5.7% CAGR versus manual approaches that still controlled 80.4% of 2024 procedures.

- The end-user mix is tilting toward ASCs, whose 5.5% CAGR outpaces hospital growth and reflects reimbursement adjustments favouring outpatient partial knee work.

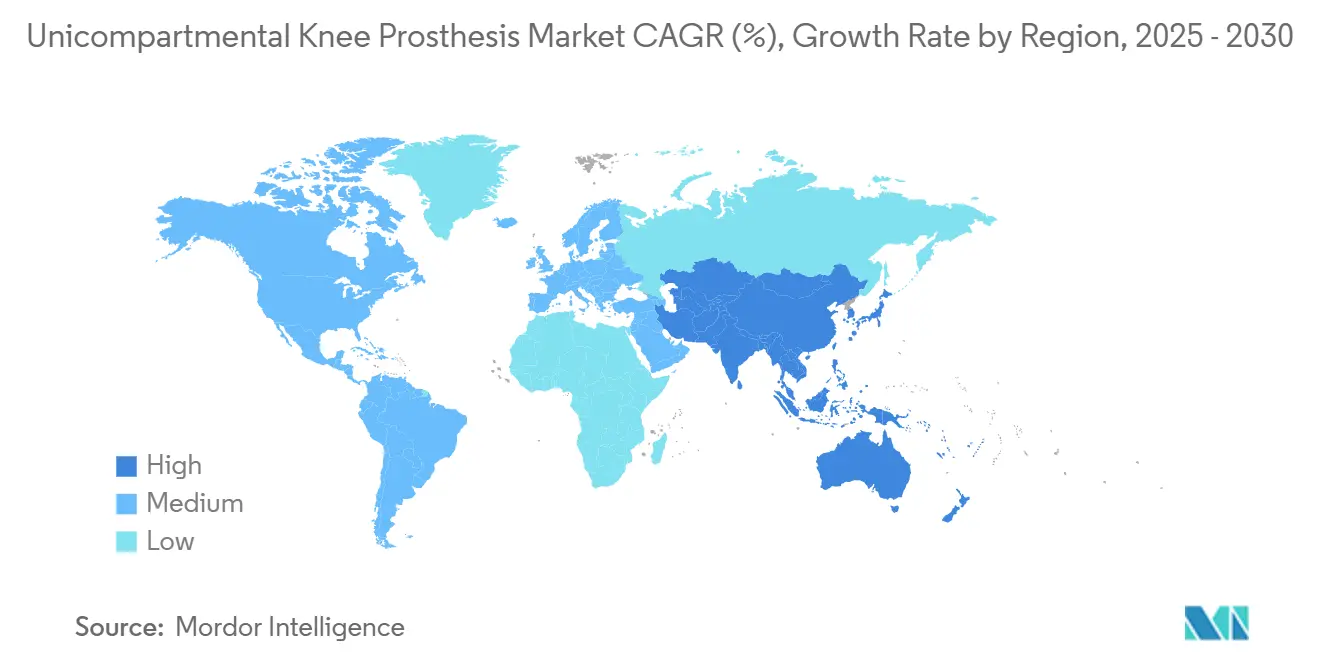

- Geographically, North America captured 40.3% of 2024 sales, while Asia-Pacific leads growth at 5.2% CAGR, mirroring infrastructure upgrades and ageing demographics.

Global Unicompartmental Knee Prosthesis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Unicompartmental Osteoarthritis In Aging & Obese Populations | +1.20% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Faster Rehabilitation & Superior Kinematics Versus Total Knee Arthroplasty (TKA) | +0.80% | Global, particularly APAC emerging markets | Medium term (2-4 years) |

| Improvements In Implant Design (Mobile-Bearing, Cementless, High-Porosity Ti) Raise Survivorship | +0.70% | North America & Europe leading, APAC following | Medium term (2-4 years) |

| Expansion Of Access & Reimbursement For Partial-Knee Procedures In Emerging Markets | +0.60% | APAC core, spill-over to Latin America | Long term (≥ 4 years) |

| ASC-Friendly Reimbursement Policies Accelerating Outpatient Partial-Knee Volume | +0.50% | North America leading, Europe following | Short term (≤ 2 years) |

| Patient-Specific 3-D Printed Cutting Guides Lowering Surgeon Learning Curve | +0.40% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Unicompartmental Osteoarthritis in Aging & Obese Populations

Global incidence of isolated medial compartment disease is accelerating alongside gains in life expectancy and obesity. The fast-growing cohort of patients under 65 seeks cartilage-sparing options rather than early total joint replacement, a reality reflected in six-month Hospital for Special Surgery scores of 92.21 for UKA versus 83.22 for TKA.[1]Xiangtao Zhang, “Clinical Efficacy of Unicompartmental Knee Arthroplasty,” biomedcentral.com Health systems that reward patient-reported outcomes translate these functional advantages into tangible funding priorities, driving volume even in cost-conscious settings. Device makers respond with wear-resistant bearings and porous titanium coatings aimed at multi-decade durability. Orthopedic societies now frame UKA as a standard rather than a niche solution for appropriately selected active adults.

Faster Rehabilitation & Superior Kinematics Versus Total Knee Arthroplasty

Finite-element modelling shows UKA imposes only 4-7% strain shielding compared with 30% for TKA, preserving tibial bone stock and native ligament tension.[2]Jennifer Stoddart, “Load Transfer in Bone After Arthroplasty,” frontiersin.org This mechanical fidelity underpins return-to-sport rates of up to 100% within six months, including participation in high-impact pursuits formerly advised against after knee replacement. Shorter recovery dovetails with bundled-payment models seeking to compress post-operative care windows. Mobilization-with-movement protocols further amplify early functional wins, a finding corroborated by randomized trials demonstrating superior scores as early as two weeks post-op. Collectively, these data accelerate surgeon acceptance and payer endorsement of procedure migration to outpatient sites.

Improvements in Implant Design Raise Survivorship

Additive manufacturing now produces high-porosity Ti6Al4V surfaces that foster rapid osseointegration and remove cement-related failure modes. Ten-year Oxford cementless wear rates of 0.06 mm per year match cemented counterparts while eliminating third-body debris associated with polymethyl-methacrylate. Mobile bearings dissipate contact stresses and mimic natural roll-glide, although recent registry reviews still attribute a 1.2-point survivorship edge to fixed constructs at five years.[3]Kevin Fricka, “Outcomes of Fixed vs. Mobile UKA,” bjj.boneandjoint.org.uk Industry increasingly bundles patient-specific guides with such implants, a pairing that standardizes tibial slope and femoral rotation, thereby narrowing outcome variability between low- and high-volume surgeons.

ASC-Friendly Reimbursement Policies Accelerating Outpatient Volume

Medicare’s removal of knee arthroplasty from the Inpatient-Only list, followed by Diagnostic-Related Group updates that favor partial knees, allows ASCs to retain a higher share of the global payment for UKA compared with TKA. Facility fees aligned with shorter stays and fewer comorbidities amplify the economic appeal of ASCs to both providers and payers. Robotic solutions requiring no pre-op CT further lower capital and workflow barriers, permitting rapid integration into smaller centers. Facility migration is already visible in payment data trends, where ASC professional revenues for knee procedures are outpacing hospital outpatient department growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Historical Revision & Failure Rates Relative To TKA | -0.90% | Global, particularly impacting surgeon adoption | Medium term (2-4 years) |

| Strict Patient-Selection Criteria Limit Eligible Cohort Size | -0.50% | Global, with variations in clinical practice patterns | Long term (≥ 4 years) |

| Payer Reluctance / Variable DRG Coding Outside U.S. Slows Adoption | -0.30% | Europe & APAC, limited impact in North America | Medium term (2-4 years) |

| Additive-Manufacturing Titanium Powder Supply Constraints For Cementless UKA | -0.20% | Global, affecting premium segment adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Historical Revision & Failure Rates Relative to TKA

Long-running Scandinavian registries still show 15-year UKA survivorship trailing TKA by nearly 20 percentage points, a legacy statistic that shapes surgeon caution despite new-generation implants. Occasional-use orthopedists drive much of the excess failure curve, while high-volume specialists achieve outcomes approaching total knee benchmarks. Recent conversion studies suggest that when revision is necessary, using the same platform simplifies instrumentation and limits bone loss, mitigating some historical downside. Nevertheless, medico-legal risk and reputation considerations continue to dampen procedure adoption outside centers of excellence.

Strict Patient-Selection Criteria Limit Eligible Cohort Size

Classical indications—isolated compartment disease, intact ACL, and limited deformity—historically excluded up to 85% of osteoarthritic knees. Although new data validate acceptable results in certain ACL-deficient or lateral compartment scenarios, survey work shows that 81% of experienced surgeons still cap annual UKA volumes at fewer than 50 cases, adhering to conservative thresholds. Training curricula and robotic alignment tools aim to widen usage, yet genuine anatomical constraints ensure that market volume will never fully mirror total knee incidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bearing Design: Mobile Systems Challenge Fixed Dominance

Fixed-bearing platforms commanded 67.8% revenue in 2024, yet their share is expected to soften as mobile options log a 4.9% CAGR through 2030, the most rapid pace within the unicompartmental knee prosthesis market. Fixed constructs deliver 97.2% five-year survivorship—1.2 points higher than mobile—but accept a narrower flexion envelope once post-operative fibrosis develops. Mobile bearings counter with improved kinematics that translate into higher patient-reported satisfaction scores and wider cultural acceptance of activities such as kneeling, which is critical in APAC markets. Recent design tweaks, including anteromedial cage containment, have reduced historical dislocation risks and repositioned the Oxford mobile platform at the frontier of cementless innovation.

Clinic adoption reflects generational training patterns: surgeons entering practice within the last decade are more likely to alternate between mobile and fixed constructs based on individualized gait analysis rather than default to a single philosophy. That flexibility aligns with payers pushing for value-based purchasing, where outcomes rather than implant cost alone drive reimbursement. Long-term, integration of sensor-laden polyethylene inserts capable of transmitting real-time load data may grant mobile systems an additional differentiation point, potentially accelerating their penetration in the unicompartmental knee prosthesis market.

By Fixation Type: Cementless Revolution Gains Momentum

Cemented implants held 72.6% of 2024 volume, yet cementless designs are set to expand at 4.7% CAGR, reflecting growing confidence in porous titanium ingrowth and a generational tilt toward bone-preserving techniques. A decade-long randomized trial shows equal wear between cemented and cementless bearings, highlighting that surgical discipline, not fixation choice, dictates long-term polyethylene integrity. Meanwhile, advanced atomization processes have eased earlier bottlenecks in Ti6Al4V powder supply, trimming production costs and improving sustainability metrics.

Cementless uptake is particularly vigorous in health systems emphasizing outpatient workflows because the absence of cement shortens operative time and lowers tourniquet duration, both predictors of early discharge. Hybrid approaches—cemented tibia with cementless femur—remain a niche bridging strategy but lack the straightforward surgical algorithm hospitals crave to maintain throughput. Over the forecast horizon, incremental gains in trabecular-mimicking lattice design are expected to anchor cementless units as the premium tier of the unicompartmental knee prosthesis market.

By Surgical Technique: Robotics Accelerate Precision Medicine

Manual instruments still facilitated 80.4% of 2024 procedures, yet robotic assistance is logging 5.7% CAGR as evidence mounts that mechanical axis, tibial slope, and joint-line restoration variance fall by half under imageless guidance. DePuy Synthes secured 510(k) clearance for its VELYS solution in 2024, enabling both medial and lateral UKA without radiation-intensive CT scans. Economic modelling suggests capital payback in five to seven years for high-volume centers because revision avoidance offsets purchase and maintenance costs.

Surgeons transitioning from manual to robot-enabled workflows cite reduced learning curve stress, with novice UKA operators achieving gap balance parity with experts after 20 robotic cases versus 75 manual. Over time, the technology’s granular data collection may feed predictive analytics that flag over-correction risks before bone resection occurs. This value proposition positions robotics as a cornerstone capability for institutions competing in a patient-choice environment increasingly sensitive to digitally quantified outcomes.

By End User: ASCs Reshape Service Delivery

Hospitals retained a 60.4% share in 2024, but the fastest 5.5% CAGR comes from ASCs, which exploit bundled-payment incentives and minimal overnight-stay rules to become default venues for healthy UKA candidates. Outpatient settings report infection rates up to 50% lower than inpatient wards, an outcome that dovetails with payer quality metrics. High-volume ASC chains are negotiating direct-to-employer contracts that price UKA at a discount to TKA yet deliver equal or better satisfaction scores, expanding addressable lives for the unicompartmental knee prosthesis market.

Orthopedic specialty clinics sit between the two extremes, functioning as referral hubs for complex revisions while channeling straightforward partial knees to partner ASCs. Regional disparities remain significant: the United States leads ASC penetration; Western Europe is cautiously catching up; emerging APAC markets still rely on hospitals due to regulatory inertia and capital constraints. Vendors that bundle implants with ASC-tailored service packages—navigation software, sterilization support, and throughput analytics—stand to cement long-term supplier agreements.

Geography Analysis

North America’s 40.3% 2024 revenue share is anchored by robust registry oversight, aggressive ASC migration, and early adoption of robotic platforms, reinforcing the region’s status as an innovation testbed for the unicompartmental knee prosthesis market. Medicare policy shifts permitting outpatient knees and refined DRG codes that advantage partial procedures augment commercial momentum. Canada’s single-payer structure deploys UKA mainly to relieve TKA waiting lists, while Mexico’s private sector drives premium device uptake in metropolitan hubs.

Europe follows as the second-largest terrain, its joint registries building a formidable evidence vault that guides reimbursement committees toward well-documented systems. Established manufacturing clusters in Switzerland, Germany, and the United Kingdom facilitate iterative design cycles, ensuring European surgeons gain early access to porous coatings and innovative instrumentation. Stiffer procurement protocols, however, slow cementless rollouts in specific public hospital networks, privileging proven cemented workhorses.

Asia-Pacific clocks the fastest 5.2% CAGR, reflecting demographic ageing, rising obesity, and hospital modernisation efforts that shorten average knee-replacement stays from 15 to 5 days in China alone. Japan and South Korea pioneer robot-enabled UK, a country backed by universal coverage systems willing to bankroll capital expenditures. China’s populous tier-2 cities invest in arthroplasty centres as provincial authorities chase healthcare quality parity with coastal provinces. India illustrates the cautionary tale of under-regulated device markets; gaps exposed by past hip implant crises are nudging policymakers toward stricter post-market surveillance, a prerequisite for cementless and robotic technologies to scale.

Competitive Landscape

The unicompartmental knee prosthesis market features a moderately concentrated field where top-tier multinationals coexist with agile specialists. Zimmer Biomet’s Oxford franchise underscores how a first-to-market cementless partial knee, coupled with a vast evidence pool, can create a temporary moat. Stryker counters with the next-generation Mako 4 platform that crosses total and partial procedures, aiming to lock institutions into a single robotic ecosystem. DePuy Synthes bets on VELYS’ imageless workflow to entice cost-conscious centers wary of pre-op CT outlays.

Specialists such as Medacta and ConforMIS carve niches via kinematic alignment and patient-specific 3-D printed guides, respectively, extracting value from surgeon cohorts that prioritize individualized restoration. Their leaner structures allow faster iteration but expose them to supply-chain and regulatory shocks that larger peers can absorb. Collaborations between component makers and analytics start-ups are emerging; embedded sensors that collect real-time load data may become table stakes for future tenders.

Across all tiers, portfolio completeness—encompassing implants, disposables, navigation, data, and after-sales service—now eclipses unit price as the primary tender criterion. Firms with global distribution, manufacturing redundancy, and regulatory fluency retain an edge, yet disruptive entrants with differentiated ease-of-use propositions can still win share in focused geographies or clinical segments, sustaining a dynamic strategic landscape within theunicompartmental knee prosthesis market.

Unicompartmental Knee Prosthesis Industry Leaders

Zimmer Biomet

Johnson & Johnson

Stryker

Smith + Nephew

Medacta

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson & Johnson MedTech showcased its VELYS robotic solution for medial and lateral partial knees at AAOS 2025, emphasizing imageless navigation integration with ATTUNE and SIGMA HP implants.

- March 2025: Stryker unveiled the Mako 4 SmartRobotics system, citing 1.5 million cumulative robotic knee procedures as proof of clinical traction.

- November 2024: Zimmer Biomet secured FDA approval for the Oxford Cementless Partial Knee, the first and only cementless partial implant cleared in the United States.

- June 2024: DePuy Synthes gained 510(k) clearance for VELYS in unicompartmental applications, extending its robotic scope beyond total knees.

Global Unicompartmental Knee Prosthesis Market Report Scope

| Fixed-Bearing |

| Mobile-Bearing |

| Cemented |

| Cementless |

| Hybrid |

| Conventional (Manual) |

| Robotic-Assisted |

| Computer-Navigated (Non-robotic) |

| Hospitals |

| Orthopedic Specialty Clinics |

| Ambulatory Surgical Centers (ASCs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Bearing Design | Fixed-Bearing | |

| Mobile-Bearing | ||

| By Fixation Type | Cemented | |

| Cementless | ||

| Hybrid | ||

| By Surgical Technique | Conventional (Manual) | |

| Robotic-Assisted | ||

| Computer-Navigated (Non-robotic) | ||

| By End User | Hospitals | |

| Orthopedic Specialty Clinics | ||

| Ambulatory Surgical Centers (ASCs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the unicompartmental knee prosthesis market in 2025?

The unicompartmental knee prosthesis market size reached USD 0.97 billion in 2025 and is forecast to climb to USD 1.19 billion by 2030.

What is the expected growth rate for unicompartmental partial knees to 2030?

The market’s compound annual growth rate is projected at 4.3% through the end of the decade, driven by cementless fixation and robotic workflows.

Which region is expanding fastest for partial knee procedures?

Asia-Pacific leads with a 5.2% CAGR as ageing demographics, shorter hospital stays and infrastructure upgrades accelerate adoption.

Why are ambulatory surgical centers important to UKA growth?

Favorable reimbursement and quicker discharge protocols give ASCs a 5.5% CAGR, making them the fastest-growing end-user segment.

How do cementless implants compare to cemented options over 10 years?

Randomized data show identical polyethylene wear of 0.06 mm per year, while avoiding cement-related complications and shortening operative time.

Are robotic systems cost-effective for partial knees?

Ten-year analyses indicate that lower revision rates offset upfront capital outlays, rendering robotics economically favorable in high-volume centers.

Page last updated on: