Garden Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.94 Billion |

| Market Size (2031) | USD 10.55 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

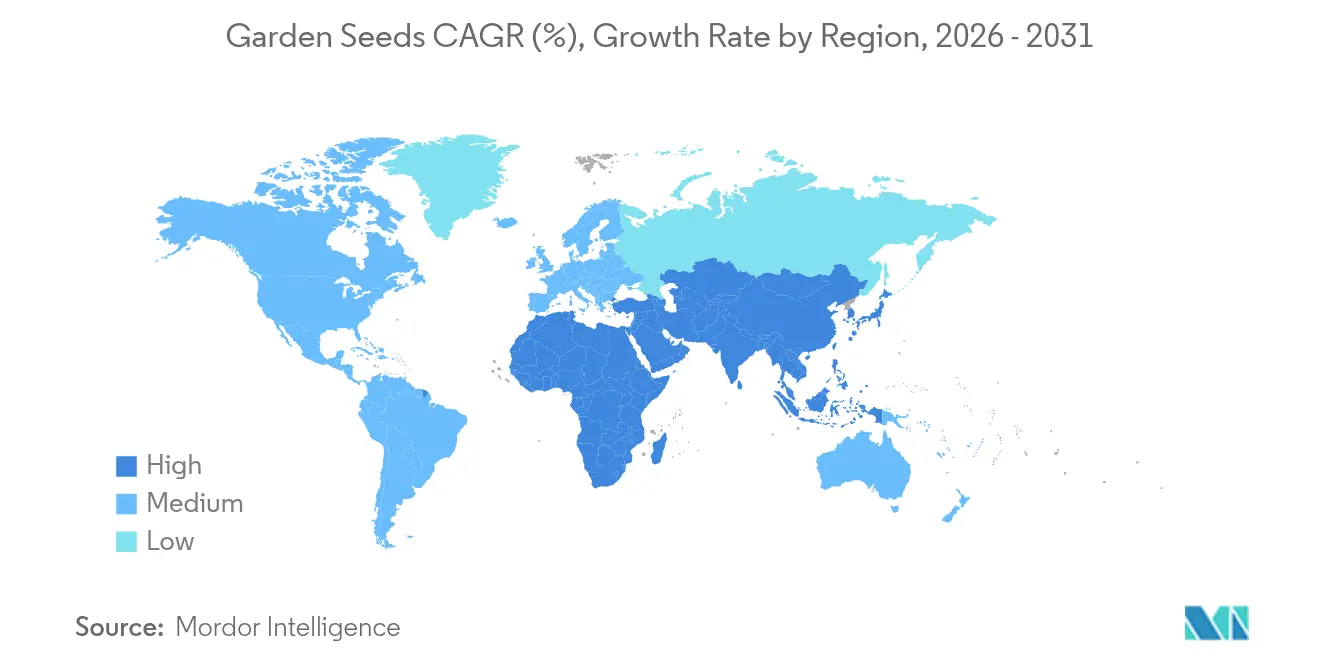

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

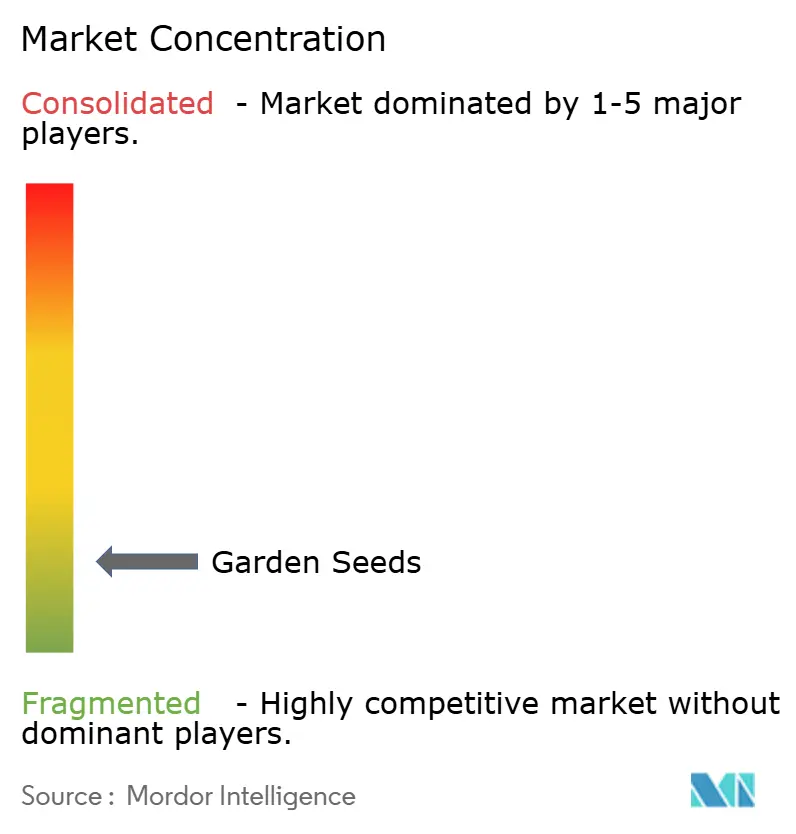

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Garden Seeds Market Analysis by Mordor Intelligence

The garden seeds market size was valued at USD 7.5 billion in 2025 and estimated to grow from USD 7.94 billion in 2026 to reach USD 10.55 billion by 2031, at a CAGR of 5.86% during the forecast period (2026-2031). Sustained momentum comes from the convergence of urban agriculture, e-commerce adoption, and supportive policy frameworks that push consumers toward self-reliance and climate-smart cultivation practices. Vegetable seed dominance persists because food security remains the primary motivation for home growers, while the fruit seed segment captures growth through consumer experimentation with exotic varieties. Online marketplaces record double-digit annual gains as brands invest in direct-to-consumer logistics and data-driven merchandising. Regionally, North America retains leadership due to an entrenched hobby-gardening culture and mature retail networks, but Asia-Pacific delivers the strongest incremental revenue as governments incentivize domestic seed production and smallholder yield improvements. Competitive intensity stays high, yet market fragmentation offers acquisition openings for larger breeders seeking scale efficiencies and broader genetic libraries.

Key Report Takeaways

- By seed type, vegetable seeds held 58.02% of the garden seeds market share in 2025, while fruit seeds are forecast to expand at an 7.72% CAGR to 2031.

- By sales channel, traditional garden centers retained 39.92% of the garden seeds market size in 2025, whereas online marketplaces are growing at 11.02% CAGR through 2031.

- By geography, North America led with a 32.21% revenue share in 2025, Asia-Pacific is advancing at a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Garden Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising interest in home gardening and urban farming | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Expanding e-commerce and online seed subscriptions | +1.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Government incentives for domestic seed multiplication | +1.2% | Asia-Pacific core, spill-over to South America | Long term (≥ 4 years) |

| Boom in micro-greens and edible ornamentals trend | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-powered seed-choice platforms boosting sales conversion | +0.6% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Demand for climate-resilient heirloom cultivars | +0.7% | Global, priority in drought-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Interest in Home Gardening and Urban Farming

Consumer preference for fresh, hyper-local produce intertwines with sustainability goals, leading municipalities to relax zoning rules for rooftop farms and community plots. Vertical farming kits designed for balconies broaden participation beyond suburban settings, while commercial kitchens integrate on-site greens to lower procurement costs and food miles. Millennials and Gen Z value transparency in food supply, spurring seed demand for pesticide-free, Non-GMO cultivars. Retailers respond with starter bundles that combine seed, substrate, and digital coaching apps. The segment’s medium-term influence is reinforced by inflationary pressure on fresh produce, encouraging households to offset grocery bills through home harvests.

Expanding E-commerce and Online Seed Subscriptions

Seed brands leverage live chat agronomy support, augmented-reality garden planners, and AI recommendation engines to lift conversion rates. An omnichannel model that offers curbside pickup for bulky soil accessories while shipping small-packet seeds improves last-mile economics. Subscription boxes deliver season-appropriate assortments, fostering repeat purchases and predictable revenue. Data captured from order frequency and varietal preferences informs breeders’ Research and Development pipelines, shortening the feedback loop between trial introduction and commercial launch. Salesforce reported a 16% merchandise value jump after deploying tailored content journeys for a leading the United States seed vendor.

Government Incentives for Domestic Seed Multiplication

India’s Prime Minister’s Dhan-Dhaanya Krishi Yojana channels agronomic extension services and mini-kit distribution to 100 low-productivity districts, elevating certified-seed adoption among smallholders.[1]National Food Security Mission, “Seed Minikit Programme,” nfsm.gov.in China’s 2025 revision of Plant Variety Rights law tightens IP enforcement while earmarking grants for indigenous breeding programs. Such initiatives pull private investment into local seed production clusters, enhance quality assurance infrastructure, and reduce reliance on imported germplasm. Long-term gains manifest through yield stability and export competitiveness.

Boom in Micro-greens and Edible Ornamentals Trend

Micro-greens command premium shelf prices due to nutrient profiles that outstrip mature vegetables by multiples, encouraging growers to adopt LED-lit racks in spare rooms and shipping containers. Controlled environment agriculture shortens growth cycles to 7-14 days, enabling rapid inventory turns. Restaurants integrate living trays into front-of-house displays, merging décor with functionality. The profit-per-square-foot advantage attracts venture funding into turnkey farm franchises, propelling seed demand for fast-germinating brassica cultivars and vividly pigmented nasturtiums. Scientific studies confirm micro-green antioxidant density, bolstering health claims and consumer willingness to pay.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Major pest and disease outbreaks in seed crops | -1.1% | Global, acute in major production regions | Short term (≤ 2 years) |

| High Research and Development cost for premium, disease-free seed lines | -0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Escalating genetic-patent litigation risks | -0.5% | North America and European Union primarily | Long term (≥ 4 years) |

| Declining pollinator populations hurting open-pollinated seed set | -0.7% | Global, severe in agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Major Pest and Disease Outbreaks in Seed Crops

Fusarium graminearum alone inflicts USD 1 billion in annual crop losses, forcing producers to discard infected seed lots and tighten phytosanitary inspection regimes. Climate-driven shifts in humidity expand the pathogen’s geographic reach, elevating fungicide usage and testing costs that ultimately flow into retail seed pricing. Biosecurity agencies intensify border checks, elongating lead times for international seed shipments and prompting growers to favor locally multiplied stock where possible.

High Research and Development Cost for Premium, Disease-Free Seed Lines

Advanced molecular breeding and gene-editing protocols shorten development cycles but require sizable capital outlays for lab automation and multi-location trials. The Breakthrough Institute notes that genetically modified seed introductions can absorb 700% more investment than their conventional counterparts. Smaller firms struggle with regulatory dossiers that span a decade, accelerating consolidation as cash-rich multinationals acquire promising pipelines. Corteva’s USD 25 million stake in Pairwise illustrates external innovation sourcing to mitigate internal cost burdens.[2]Corteva Agriscience, “Corteva and Pairwise Expand Gene-Editing Collaboration,” corteva.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seed Type: Vegetable Dominance Drives Market Growth

Vegetable seeds captured 58.02% of the garden seeds market in 2025 as households prioritized pantry staples that assure daily meal coverage. Tomato varieties alone are projected to touch USD 1.95 billion by 2031 at a 4.55% CAGR, driven by dual use in fresh salads and sauce processing. Herbs and leafy greens profit from micro-green applications that enable countertop production in high-density urban apartments. The garden seeds market size for vegetable cultivars is forecast to widen in tandem with recipe-sharing social platforms that spur varietal experimentation. Fruit seeds, though smaller in absolute terms, register the fastest 7.72% CAGR. Tropical berries and melons attract hobbyists seeking novel flavors, while dragon fruit and passion fruit seeds sell at premium packet prices due to limited domestic supply chains. This segment diversifies revenue and buffers seasonal swings inherent to annual vegetable cycles.

The demand shift introduces breeding imperatives for compact, container-friendly phenotypes that suit balconies and indoor grow lights. Heirloom strains regain popularity among eco-conscious consumers seeking biodiversity conservation. Concurrently, the garden seeds market share held by open-pollinated lines shrinks modestly as hybrid vigor appeals to yield-oriented gardeners.

By Sales Channel: Digital Transformation Accelerates Market Access

Traditional garden centers retained 39.92% of the garden seeds market size in 2025, benefiting from tactile product assessment and in-store coaching. Online marketplaces are scaling at 11.02% CAGR through 2031, propelled by enhanced user interfaces, how-to video integration, and same-day metro delivery options. The garden seeds market has embraced omnichannel strategies where click-and-collect merges digital convenience with physical immediacy.

Subscription-based seed kits maintain engagement across seasons, reducing customer acquisition costs. Expert Assessments and unboxing content on social media strengthen brand credibility, especially for rare heirloom suppliers. Meanwhile, big-box retail remains relevant for entry-level gardeners who bundle seeds with tools and potting mix during home-improvement trips.

Geography Analysis

North America held 32.21% revenue leadership in 2025 on the back of hobby-gardening traditions, robust logistics, and favorable intellectual property enforcement. Diverse microclimates foster regional testing programs that accelerate new-variety acceptance among both professionals and hobbyists. State universities partner with seed companies to publish extension bulletins, reinforcing evidence-based cultivar selection.

Asia-Pacific, posting a 6.88% CAGR, emerges as the primary growth engine. China’s renewed subsidy framework for local seed enterprises reduces import dependence and boosts research into heat-tolerant horticultural crops. India channels public funds into breeder seed multiplication and village-level distribution networks, elevating certified seed penetration among smallholders. The garden seeds market size in the region scales further as urban rooftop farms proliferate and consumers shift toward antioxidant-rich fruits in response to lifestyle disease prevalence.

Europe records steady mid-single-digit growth anchored in sustainability mandates and organic certification uptake. The Netherlands, Spain, and Italy supply a substantial portion of global vegetable seed exports, leveraging technologically advanced greenhouse seed production hubs. Regulatory uncertainty around gene-edited crops prompts breeders to invest in conventional marker-assisted selection techniques. Eastern European markets provide expansion headroom as rising disposable incomes stimulate DIY gardening spending. Multilateral development banks finance seed laboratory upgrades and farmer demonstration plots, laying the groundwork for demand expansion once macroeconomic volatility eases.

Competitive Landscape

The competitive landscape remains fragmented, with W. Atlee Burpee Company holding the largest market share, followed by Johnny’s Selected Seeds, Sakata Seed Corporation, Takii & Co., Ltd., and Groupe Limagrain (Vilmorin Jardin). Most players maintain proprietary breeding programs, yet no single firm dominates the market, preserving buyer choice and price competition. Mergers and acquisitions are gaining momentum as mid-tier breeders aim for geographic diversification. CANTERRA SEEDS’ acquisition of Alliance Seed expanded its presence in Western Canada.

Technology partnerships characterize innovation strategy. Bayer AG and Source.ag apply machine-learning models to greenhouse trial data, cutting cycle times for disease-resistant tomato lines. AI-centric platforms also refine demand forecasting, minimizing excess inventory and obsolescence risk. Direct-to-consumer portals give legacy brands richer customer insights, informing targeted promotions and cross-selling of soil amendments and biological inoculants.

Vertical integration trends manifest in seed-to-plate brand narratives, where firms bundle seeds with recipe content, fertilizer sachets, and QR-coded cultivation tutorials. Climate-resilient portfolio development remains a strategic imperative as heat, drought, and salinity stress intensify. Intellectual property vigilance grows amid tightening legislation on gene-edited traits, prompting companies to strengthen legal teams and defensive patent filings.

Garden Seeds Industry Leaders

Johnny's Selected Seeds

Sakata Seeds Corporation

Takii & Co., Ltd.

W. Atlee Burpee Company

Groupe Limagrain (Vilmorin Jardin)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sakata Seed Corporation inaugurated a new 2.5-hectare Research and Development station in Antalya, Turkey, to boost cucumber, tomato, and pepper breeding for regional markets. The facility combines traditional and high-tech approaches to develop resilient, high-quality vegetable varieties for Europe, the Middle East, and Central Asia.

- December 2024: Bene Seeds Inc. and Johnny’s Selected Seeds have launched two new cherry tomato varieties - Queen Bee and Honey Bee - developed through a multi-year breeding collaboration. These premium tomatoes combine heirloom flavor with hybrid durability and are sold exclusively through Johnny’s Selected Seeds.

- January 2024: Seed Savers Exchange introduced 18 new seed varieties. These new offerings provide gardeners with a wider range of options for their planting needs.

- February 2023: W. Atlee Burpee and Co. launched new seed varieties for the 2023 season. The products included Vivacious Hybrid Tomato, Creme Brulee Sunflower, Rise and Shine Squash, Two Tasty Hybrid Tomato, Bliss Tomato Hybrid, Party Time Cucumber, and more.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the garden seeds market as retail-packed vegetable, flower, herb, and fruit seeds that home gardeners and community plots sow in containers, yards, or compact beds for personal consumption or ornamental value. The unit of analysis is a seed packet or small bulk bag typically sold through garden centers, hardware chains, supermarkets, and dedicated e-commerce sites.

Scope Exclusions: Seeds destined for large-scale row crops, genetically modified commodity seed, and grow-kit bundles that include soil or nutrients fall outside this study.

Segmentation Overview

- By Seed Type

- Vegetable Seeds

- Tomato

- Cucumber

- Carrot

- Pepper and Chili

- Leafy Greens

- Culinary Herbs

- Other Vegetable Seeds (Eggplant, Squash, etc.)

- Flower and Ornamental Seeds

- Annuals

- Perennials

- Bulbous Flower Seeds

- Fruit Seeds

- Berries

- Melons

- Tropical and Exotic Fruits

- Vegetable Seeds

- By Sales Channel

- Online Marketplaces

- Brand-Owned Webshops

- Garden Centers and Nurseries

- Specialty Seed Stores

- DIY/Home-Improvement Chains

- Grocery and Mass Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with plant breeders, independent garden-center buyers, large online seed retailers, and urban-farm coordinators across North America, Europe, and Asia-Pacific. These conversations verified price elasticity, packet size norms, and the rising preference for certified organic and heirloom cultivars, filling gaps that desk sources could not bridge.

Desk Research

We reviewed statistical series from USDA-NASS, Eurostat crop production files, FAOSTAT trade tables, and the International Seed Federation dashboard to size regional seed flows and average packet weights. Household expenditure surveys in the United States, Germany, Japan, and Brazil, along with Royal Horticultural Society trend notes, grounded demand by age group and dwelling type. Annual reports, online catalog price lists, and seed patents accessed via Questel clarified average selling prices, organic mark-ups, and varietal turnover. We extracted private-company indicators from D&B Hoovers, scanned Dow Jones Factiva for seasonal shortage news, and used Volza shipment logs to validate import blends. The sources named illustrate, rather than exhaust, the wider set employed for data collection and cross-checks.

Market-Sizing & Forecasting

We initiated a top-down reconstruction of household spending on gardening supplies, applied seed-specific penetration rates from consumer surveys, and reconciled results with retail shipment tonnage. Select bottom-up roll-ups of key supplier revenues and sampled average price-times-volume checks adjusted totals where discrepancies arose. Core variables, new gardener adoption, packets per gardener, organic price premium, e-commerce share, and climate-linked growing days feed a multivariate regression that projects values through 2029. Scenario analysis gauges drought or regulatory shocks before finalizing outlooks.

Data Validation & Update Cycle

Outputs undergo variance tests against import-export data and disclosed revenues, followed by multi-level analyst review and senior sign-off. We refresh the model each year, issuing interim updates when droughts, disease outbreaks, or major M&A materially alter supply conditions.

Why Mordor's Garden Seeds Baseline Earns Confidence

Published estimates often diverge because each provider defines 'garden seeds' differently and varies currency, inflation, and refresh cadences. We anchor our numbers to clearly traceable retail packets and update them on a fixed annual timetable.

Key gap drivers include the inclusion of commercial farm seed under some scopes, omission of herb and fruit lines under others, one-time extrapolations from narrow store audits, and lengthy update cycles. Mordor Intelligence employs a stricter consumer focus, dual-path validation, and yearly data refresh to deliver a balanced view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.15 B (2024) | Mordor Intelligence | NA |

| USD 3.73 B (2024) | Global Consultancy A | Counts bulk agricultural seed and garden-kit accessories |

| USD 1.20 B (2025) | Trade Journal B | Excludes herb and fruit seeds; five-region coverage only |

| USD 23.04 B (2024) | Industry Analysis C | Aggregates wider seed categories, undisclosed currency factors |

The comparison shows that disciplined scope setting, annual field checks, and transparent variable selection allow Mordor Intelligence to deliver a dependable baseline that decision-makers can replicate with confidence.

Key Questions Answered in the Report

What is the current value of the garden seeds market and forecasted market size?

The garden seeds market is valued at USD 7.94 billion in 2026 and is set to grow to USD 10.55 billion by 2031.

Which seed type holds the largest share of the garden seeds market?

Vegetable seeds lead with 58.02% share in 2025, reflecting strong consumer focus on food security.

How fast is the online sales channel growing?

Online marketplaces for seeds are expanding at an 11.02% CAGR through 2031, outpacing all other channels.

Which region is projected to see the fastest growth?

Asia-Pacific is projected to register a 6.88% CAGR, buoyed by policy support and urban agriculture expansion.

Who are the leading companies in the garden seeds market?

The competitive landscape remains fragmented, with W. Atlee Burpee Company leading, followed by Johnny’s Selected Seeds, Sakata Seed Corporation, Takii & Co., Ltd., and Groupe Limagrain (Vilmorin Jardin).

What major trend is reshaping product development?

Gene-edited, climate-resilient varieties are gaining traction as firms invest in AI-driven breeding alliances to address heat and drought stress.

Page last updated on: