Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

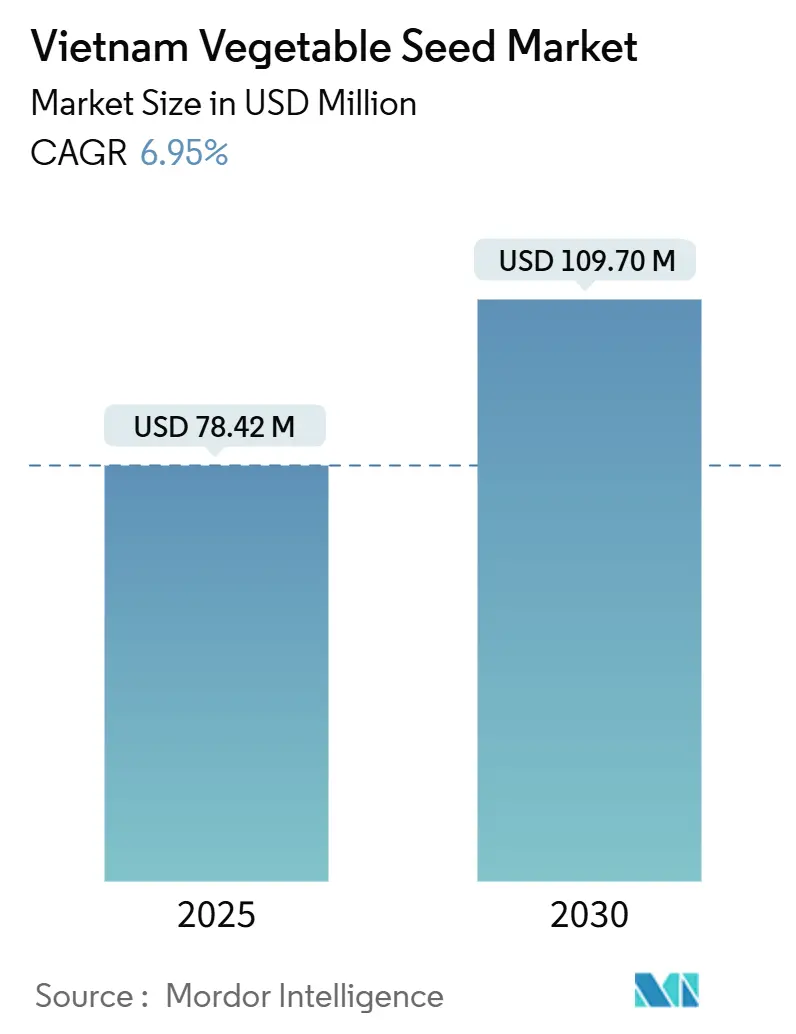

| Market Size (2025) | USD 78.42 Million |

| Market Size (2030) | USD 109.70 Million |

| Growth Rate (2025 - 2030) | 6.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Vegetable Seed Market Analysis by Mordor Intelligence

The Vietnam vegetable seed market size reached USD 78.42 million in 2025 and is forecast to climb to USD 109.70 million by 2030, reflecting a 6.95% CAGR over the period. Growth stems from rising hybrid‐seed penetration, protected cultivation investments, and government programs that channel funding toward domestic breeding and digital traceability[1]Source: Báo Chính Phủ, “Chuẩn hóa thủ tục trong trồng trọt và bảo vệ thực vật,” baochinhphu.vn. Seed companies scale marker-assisted selection to shorten development cycles, while exporters demand varieties with documented phytosanitary compliance for premium overseas channels. Counterfeit seed crackdowns, led by Ministry of Industry and Trade enforcement campaigns, further steer farmers toward certified suppliers [2]Source: Thư Viện Pháp Luật, “Quyết định 1398/QĐ-BCT năm 2025 về Kế hoạch cao điểm…,” thuvienphapluat.vn. Multinationals and Vietnam National Seed Group (VINASEED) leverage these trends to expand product portfolios, yet fragmented smallholder demand and climate volatility temper near-term gains. Overall, the Vietnam vegetable seed market continues to reward firms that pair genetics innovation with data-rich advisory services.

Key Report Takeaways

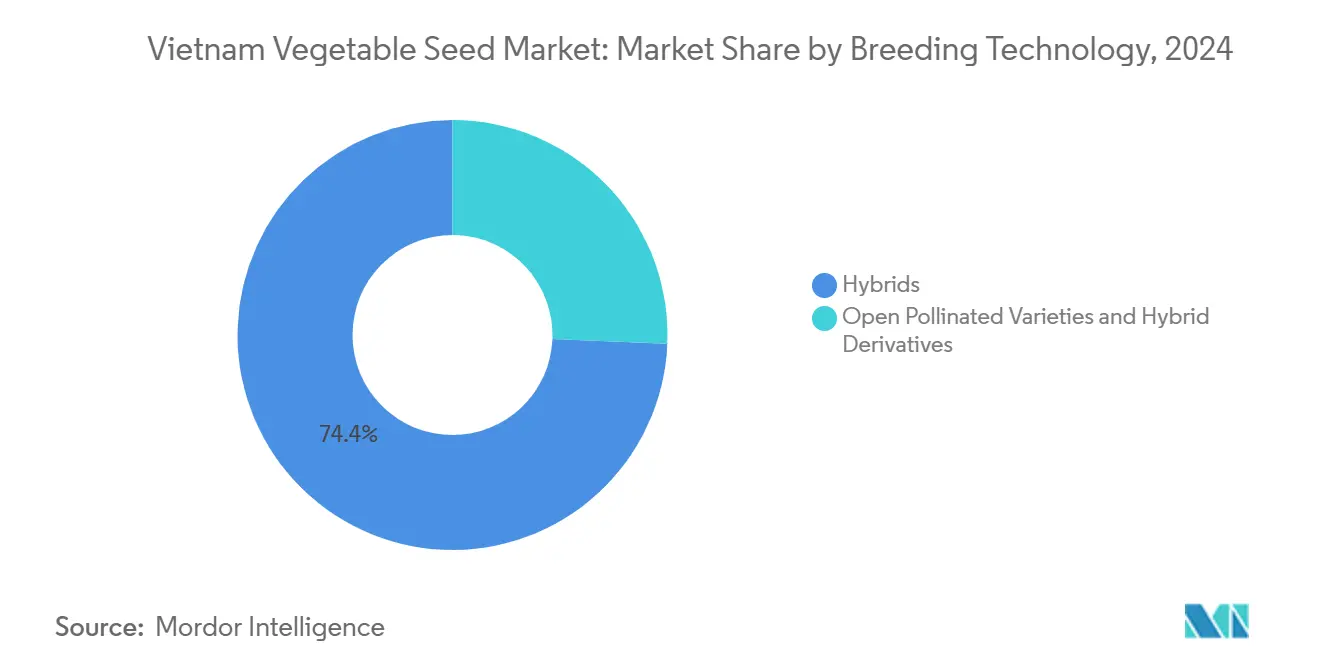

- By breeding technology, hybrids captured 74.4% of the Vietnam vegetable seed market share in 2024, while the same segment also logged the fastest 7.31% CAGR projected through 2030.

- By cultivation mechanism, open-field systems accounted for 99.98% of the Vietnam vegetable seed market size in 2024; protected cultivation is forecast to advance at a 12.72% CAGR to 2030.

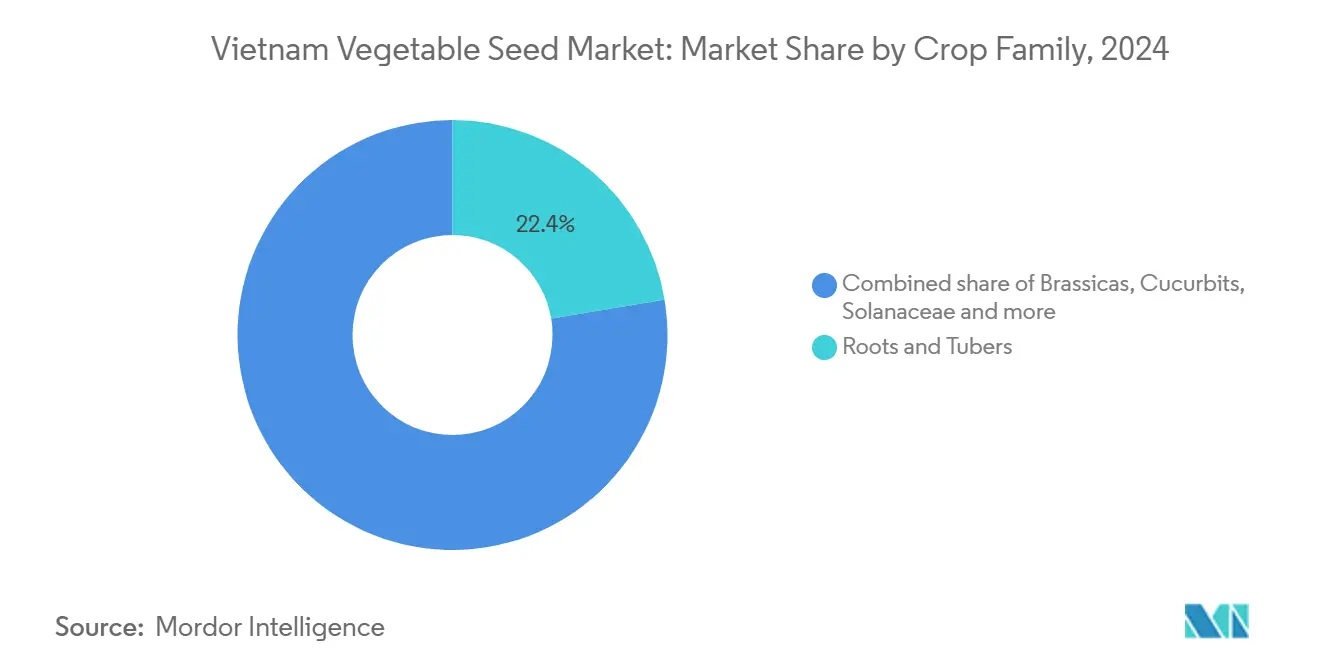

- By crop family, roots and tubers led with 22.4% revenue share in 2024, whereas Solanaceae is set to expand at a 5.07% CAGR through 2030.

Vietnam Vegetable Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-adoption push to raise yields | +1.8% | National, with highest impact in Northern and Southern Vietnam | Medium term (2-4 years) |

| Export-oriented quality compliance | +1.5% | National, concentrated in major export provinces | Short term (≤ 2 years) |

| Rising protected-cultivation acreage | +1.2% | Southern Vietnam leading, expanding to Central regions | Long term (≥ 4 years) |

| Government seed-sector modernization plan | +1.0% | National implementation with regional variations | Medium term (2-4 years) |

| Rapid purity-testing and marker-assisted breeding adoption | +0.8% | Concentrated in major seed production centers | Long term (≥ 4 years) |

| E-commerce channels for seed distribution | +0.7% | Urban and peri-urban areas, expanding to rural regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hybrid-adoption push to raise yields

Farmers adopt hybrids to offset shrinking arable land and lift yields by 20-30% compared with open-pollinated lines. Vietnam National Seed Group (VINASEED) aims to boost hybrid seeds from 34% to 37% of gross profit with climate-adaptive releases suited for the He Thu season. Regional gaps persist; several northern provinces approach 90% hybrid usage, whereas parts of the south favor traditional varieties due to cost. Seed firms, therefore, invest in parent-line farms and engage farmers through field days, promoting hybrids as reliable income stabilizers. As productivity gains translate into higher export quality, hybrids become a strategic lever within the Vietnamese vegetable seed market.

Export-oriented quality compliance

Vietnam's vegetable export goals have driven strict quality compliance requirements, affecting seed selection and cultivation. The Ministry of Agriculture and Rural Development's amended Law on Crop Production requires packing-facility and growing-area codes to meet export standards for the European Union, Japan, and the United States markets. These regulations provide advantages to seed companies offering varieties with documented traceability and phytosanitary compliance, specifically for Tomato Brown Rugose Fruit Virus (ToBRFV) regulations in tomato and pepper imports. Export-focused producers seek seed varieties with consistent quality, extended shelf life, and resistance to deterioration during transport. The Ministry of Industry and Trade's eCoSys platform requires Certificate of Origin documentation within three working days, benefiting seed suppliers with digital infrastructure and compliance systems.[3]Source: Evrim Ağacı, “Vietnam Strengthens Measures Against Trade Fraud,” evrimagaci.org

Government Seed-Sector Modernization Plan

Vietnam's seed sector modernization program, established through Decision 1748, provides funding for domestic breeding programs and tax incentives for private sector research investments. The policy focuses on developing climate-resilient seed varieties and sustainable cultivation methods to support the Mekong Delta's "1 million hectare quality rice" initiative, which also benefits vegetable seed development. The regulatory framework standardizes a variety of naming conventions and trial registration requirements across regions to prevent confusion from multiple designations of the same varieties. The government's digital transformation initiative implements online systems for seed registration, quality inspection, and administrative processes, reducing delays in variety approvals. These changes benefit companies with strong research capabilities and digital systems, but may create challenges for smaller firms that lack the resources to meet new regulatory and documentation requirements.

Rapid purity-testing and marker-assisted breeding adoption

Advanced breeding technologies in Vietnam have reduced seed development timelines from 36 months to 12 months through DNA-based purity testing and marker-assisted selection. Syngenta collaborates with Vietnamese research institutions to implement gene editing and marker-assisted selection for developing locally-adapted varieties. The National Institute of Agricultural Planning and Projection works with Chinese institutions through PAN Group to implement genomic selection and tissue culture propagation. While Vietnamese seed companies invest in laboratory infrastructure and technical expertise, adoption remains limited to larger companies with adequate capital and capabilities, creating a competitive divide between established companies and smaller regional seed producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit/low-quality seeds in informal trade | -1.20% | National, concentrated in remote rural areas | Short term (≤ 2 years) |

| Climate-induced pest pressure variability | -0.90% | National, with highest impact in Central Vietnam | Medium term (2-4 years) |

| Tight phytosanitary rules (ToBRFV listing) | -0.70% | National, affecting import-dependent regions | Short term (≤ 2 years) |

| Fragmented smallholder demand and price sensitivity | -0.60% | Rural areas with traditional farming systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit/Low-Quality Seeds in Informal Trade

The proliferation of counterfeit and substandard seeds through informal trade channels undermines farmer confidence by bypassing quality control mechanisms and regulatory oversight. The Ministry of Industry and Trade implemented Decision 1398/QĐ-BCT, initiating an enforcement campaign from May to June 2025 to combat smuggling, commercial fraud, and counterfeit goods, focusing on agricultural inputs and e-commerce platforms. Under Decree 98/2020/NĐ-CP, violations involving plant varieties face doubled fines, with enforcement agencies authorized to impose penalties on organizations trading counterfeit seeds. Rural areas with limited regulatory oversight remain susceptible to counterfeit seed distribution, especially during peak planting seasons when demand surpasses authorized dealer capacity. The circulation of low-quality seeds negatively impacts legitimate seed companies' reputation and reduces farmers' willingness to invest in premium varieties, limiting market growth and technology adoption.

Climate-Induced Pest Pressure Variability

Climate change creates unpredictable challenges in pest and disease management, complicating seed variety selection and risk management for farmers. Weather variability affects pest lifecycles and geographic distributions, reducing the effectiveness of existing resistance traits and necessitating ongoing variety development. The Ministry of Science and Technology's Circular 01/2024/TT-BKHCN implements new market inspection procedures for seed quality testing, adding compliance requirements during periods when farmers require reliable seed performance. In Central Vietnam, typhoons and flooding significantly impact seed production schedules, leading to supply shortages during key planting periods. Seed companies invest more in developing climate-resilient varieties, while farmers become hesitant to adopt new varieties without proven performance in variable weather conditions, which slows market growth and innovation adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Drive Premium Market Expansion

Hybrids hold 74.4% market share in 2024 and are growing at 7.31% CAGR through 2030. This dominance stems from farmers' recognition of their superior yield performance and quality consistency, supporting premium pricing. Vietnam National Seed Group (VINASEED) plans to increase hybrid seed contribution to gross margin from 34% to 37% by 2025, with emphasis on climate-adaptive varieties for the He Thu season, when environmental conditions are most challenging. Open Pollinated Varieties and Hybrid Derivatives remain important for price-sensitive smallholder farmers and traditional crop segments where hybrid benefits are less significant, though their market share decreases as hybrid production costs fall and performance differences increase.

Marker-assisted breeding and genomic selection reduce hybrid development time from 36 months to 12 months. This acceleration allows seed companies to address emerging pest pressures and climate challenges more efficiently while reducing per-variety development costs. Syngenta's partnerships with Vietnamese research institutions showcase gene editing applications in developing locally-adapted hybrids with improved disease resistance. The amended Biodiversity Law provides clear GMO definitions and establishes frameworks for gene-edited varieties, potentially expanding opportunities for biotechnology-enhanced seeds in the medium term.

By Cultivation Mechanism: Protected Systems Transform Production Economics

Open field cultivation holds 99.98% of the market share in 2024, reflecting Vietnam's traditional agricultural practices and the economic limitations of smallholder farmers who constitute most vegetable producers. Protected cultivation is growing at 12.72% CAGR, driven by investments in greenhouse and net-house facilities that enable continuous production throughout the year and allow farmers to position high-value crops for premium markets. The transformation is most prominent in southern provinces, where private and public investments in climate-controlled facilities are supported by the CROPS4DELTA project's demonstrations of salt-tolerant crop production in controlled environments.

Protected cultivation systems require specific seed varieties adapted for controlled environments, artificial lighting, and intensive production schedules, enabling 3-4 crop cycles annually compared to 2 cycles in open fields. Seed companies are developing specialized varieties for protected cultivation that feature shorter maturation periods, enhanced disease resistance in high humidity conditions, and optimized performance under LED lighting systems. While this technological shift creates opportunities for premium pricing and expanded technical services beyond traditional seed supply, adoption remains limited to larger commercial producers who have the necessary capital and technical expertise for system implementation.

By Crop Family: Solanaceae Innovation Drives Growth Momentum

Roots and Tubers hold the largest market share at 22.4% in 2024, supported by Vietnam's established cultivation practices and strong domestic consumption of potatoes, onions, and garlic for both fresh markets and processing. The Solanaceae family exhibits the highest growth rate at 5.07% CAGR through 2030, attributed to increased production of tomatoes, chilies, and eggplants that meet domestic and export market requirements for quality and shelf life.

Brassica vegetables maintain consistent demand through cabbage, cauliflower, and broccoli varieties that align with traditional Vietnamese cuisine while meeting modern retail requirements. Cucurbit production, including cucumbers and pumpkins, shows growth in urban and export markets despite limitations from seasonal production cycles and post-harvest handling issues. Unclassified vegetables, such as asparagus and spinach, present growth potential due to increasing health-conscious consumption and international cuisine influences. The implementation of variety naming standards and self-declaration requirements creates product differentiation opportunities for established seed companies while presenting challenges for smaller market participants with limited registration and marketing resources.

Geography Analysis

Northern provinces exhibit the nation’s highest hybrid penetration, touching 90% in peri-urban belts where growers supply Hanoi’s supermarkets. Reliable cold-chain links and technical outreach accelerate new-variety turnover. Central Vietnam grapples with typhoons, flooding, and salinity intrusion that raise seed failure risk, so farmers lean on climate-resilient lines and are early adopters of greenhouse tunnels that shelter high-value leaf crops. The region’s export orientation drives demand for varieties matching European Union residue and traceability standards.

Southern Vietnam anchors protected cultivation expansion. Mekong Delta growers leverage CROPS4DELTA findings to plant salt-tolerant cucumbers and tomatoes year-round, commanding price premiums during northern off-season gaps. Proximity to Ho Chi Minh City concentrates input distributors and finance providers, allowing rapid scaling of electric-cooling irrigation pumps. Despite these advantages, smallholder fragmentation persists: plot consolidation lags, and informal seed saving depresses hybrid uptake.

Across all regions, the Vietnam vegetable seed market coalesces around integrated support models that bundle genetics, advisory, and digital traceability. Provincial departments promote QR-based labeling that lets consumers scan farm origin, nudging retailers to favor certified seed adopters. Geographic differentiation, therefore, shapes targeted product pipelines and marketing spend, sharpening competitive positioning nationwide.

Competitive Landscape

The Vietnam vegetable seed market shows moderate concentration, with the top five companies holding a significant market share. This market structure creates a competitive environment that combines the technical expertise of multinational companies with the local market knowledge and distribution networks of domestic firms. The balanced market dynamics enable both international and local players to leverage their respective strengths, fostering innovation and market development while ensuring efficient seed distribution across Vietnam's agricultural regions.

Bayer AG leads the market through comprehensive product portfolios and technical support services, followed by Syngenta AG and Groupe Limagrain, which leverage global breeding programs and local adaptation capabilities to serve diverse crop segments and regional preferences. This concentration enables sustained research and development investments while maintaining competitive pressure that drives innovation and market expansion.

Strategic patterns emphasize hybrid development, digital distribution, and technical service integration as companies seek to differentiate beyond traditional seed supply relationships. Vietnam National Seed Group (VINASEED) demonstrates domestic player strategies through targeted investments in climate-adaptive varieties and margin enhancement initiatives that increase hybrid seed contribution from 34% to 37% of gross profits Vietnam National Seed Group. White-space opportunities emerge in protected cultivation seed varieties, e-commerce distribution platforms, and smallholder financing solutions that address market fragmentation challenges.

Vietnam Vegetable Seed Industry Leaders

Bayer AG

Groupe Limagrain

Vietnam National Seed Group (VINASEED)

Enza Zaden B.V.

Syngenta AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vietnam National Seed Group (VINASEED) and the World Vegetable Center (WorldVeg) collaborated to develop new pumpkin hybrid varieties in Laos. The partnership demonstrates international cooperation in creating resilient crops. The new varieties, developed through joint trials in Vietnam and Laos, exhibit high yields, elevated beta-carotene content, and enhanced virus resistance.

- June 2025: Vietnam National Seed Group (VINASEED) announced its plans to transform its Research Center into a Research Institute, focusing on international collaboration in seed development and agricultural technologies while prioritizing research and development personnel training.

Vietnam Vegetable Seed Market Report Scope

The Vietnam Vegetable Seed Market Report is Segmented by Breeding Technology (Hybrids, Open Pollinated Varieties, and Hybrid Derivatives), Cultivation Mechanism (Open Field, Protected Cultivation), Crop Family (Brassicas, Cucurbits, Roots and Bulbs, Solanaceae, Unclassified Vegetables), and Geography (Vietnam). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Breeding Technology

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Crop Family

| Brassicas | Cabbage |

| Cauliflower and Broccoli | |

| Other Brassicas | |

| Cucurbits | Cucumber and Gherkin |

| Pumpkin and Squash | |

| Other Cucurbits | |

| Roots and Bulbs | Garlic |

| Onion | |

| Potato | |

| Other Roots and Bulbs | |

| Solanaceae | Chilli |

| Eggplant | |

| Tomato | |

| Other Solanaceae | |

| Unclassified Vegetables | Asparagus |

| Spinach | |

| Other Unclassified Vegetables |

| Breeding Technology | Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives | ||

| Cultivation Mechanism | Open Field | |

| Protected Cultivation | ||

| Crop Family | Brassicas | Cabbage |

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Roots and Bulbs | Garlic | |

| Onion | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Solanaceae | Chilli | |

| Eggplant | ||

| Tomato | ||

| Other Solanaceae | ||

| Unclassified Vegetables | Asparagus | |

| Spinach | ||

| Other Unclassified Vegetables | ||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms