Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

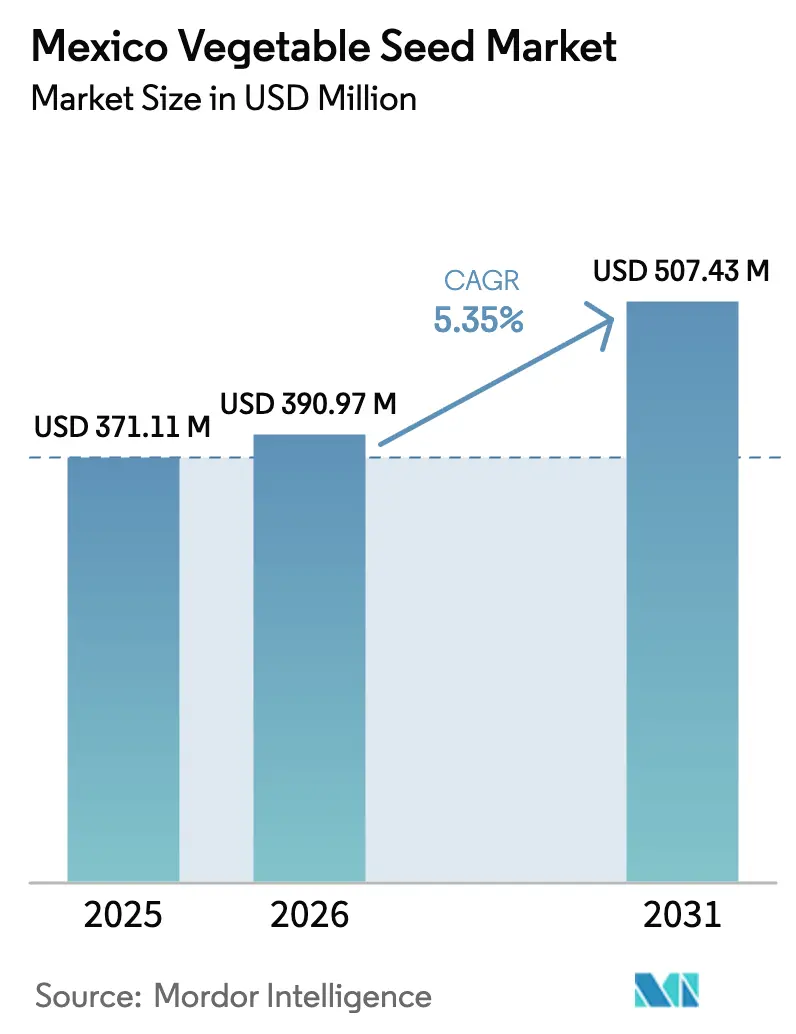

| Base Year Market Size (2025) | USD 371.11 Million |

| Market Size (2026) | USD 390.97 Million |

| Market Size (2031) | USD 507.43 Million |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Vegetable Seed Market Analysis by Mordor Intelligence

The Mexico vegetable seed market size was valued at USD 371.11 million in 2025 and estimated to grow from USD 390.97 million in 2026 to reach USD 507.43 million by 2031, at a CAGR of 5.35% during the forecast period (2026-2031). Sustained growth stems from Mexico’s role as a year-round supplier to North American retailers, the rapid scale-up of protected cultivation, and public programs that subsidize certified hybrids. Ongoing greenhouse expansion, rising demand for virus-resistant tomatoes and peppers, and widening e-commerce access to quality seed continue to lift volumes despite drought-related acreage cuts in the Northwest. Multinational breeders strengthen their local pipelines through disease-resistance and shelf-life traits tailored to export logistics, while domestic firms leverage southern states’ favorable agro-climates to multiply seed for specialty crops.

Key Report Takeaways

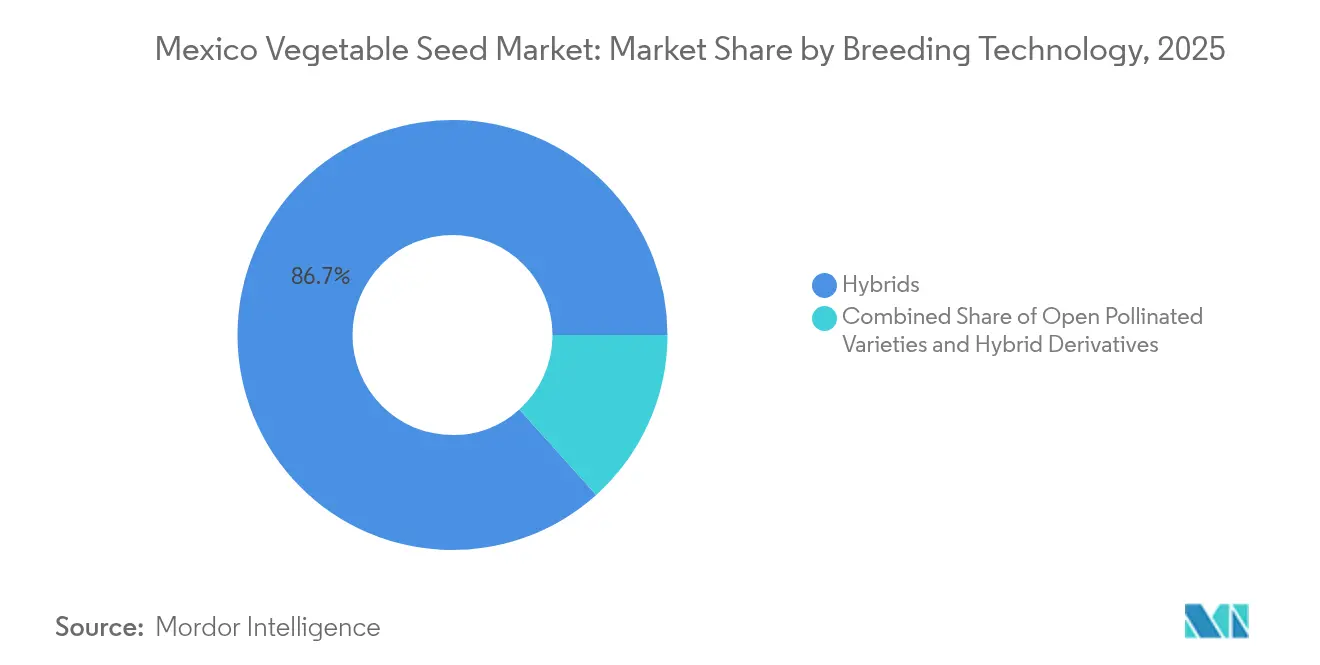

- By breeding technology, hybrids led with 86.65% of the Mexico vegetable seed market share in 2025, and are anticipated to rise at 5.35% CAGR to 2031.

- By cultivation mechanism, the open-field segment held 86.40% revenue in 2025. Protected systems grew at a 6.65% CAGR through 2031.

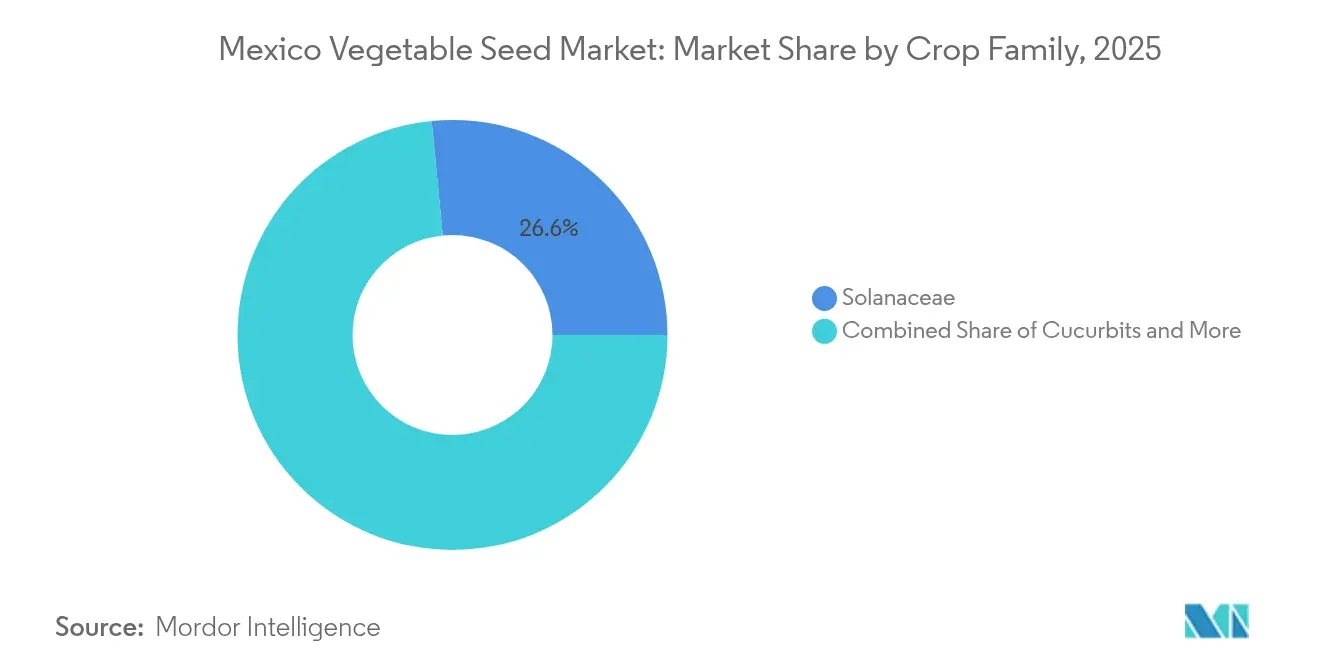

- By crop family, Solanaceae commanded 26.55% of the Mexico vegetable seed market size in 2025, and is anticipated to rise at a 5.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Vegetable Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-oriented greenhouse boom | +1.2% | National, concentrated in Sinaloa, Sonora, and Baja California | Medium term (2-4 years) |

| Government support for certified hybrid adoption | +0.8% | National, prioritizing southern states | Long term (≥ 4 years) |

| Rising demand for virus-resistant tomato and pepper seeds | +0.9% | National, strongest in Chiapas, Sinaloa production zones | Short term (≤ 2 years) |

| E-commerce channels reaching smallholders | +0.4% | National, initial focus Bajío and Occidente regions | Medium term (2-4 years) |

| Domestic seed-import tariffs encourage local multiplication | +0.6% | National, benefiting domestic production centers | Long term (≥ 4 years) |

| (Clustered regularly interspaced short palindromic repeats) CRISPR-enabled drought-tolerant varieties | +0.7% | Northwestern states, expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-Oriented Greenhouse Boom

Mexico's protected cultivation sector has become the cornerstone of vegetable seed demand growth, with greenhouse infrastructure expanding to capture premium export markets. The sector's productivity advantage is measurable, with protected tomato production yielding approximately four times more than open-field cultivation. This enables Mexico to compete directly with established producers such as Florida[1]Source: Zhengfei Guan and Feng Wu, “Government Support in Mexican Agriculture: The Agri-Food Productivity and Competitiveness Program,” University of Florida IFAS, ifas.ufl.edu. This infrastructure investment directly translates to increased demand for specialized hybrid varieties optimized for controlled environments, particularly those offering disease resistance and extended shelf life for export logistics. The sector's export orientation creates a feedback loop where international quality standards drive continuous variety improvement and seed technology adoption.

Government Support for Certified Hybrid Adoption

The Mexican government's systematic support for certified hybrid adoption represents a strategic shift toward agricultural modernization and food sovereignty. The "Cosechando Soberanía" program commits USD 2.7 billion in 2025, escalating to USD 4.2 billion by 2030, targeting 750,000 small and medium-scale producers across 1,184 municipalities [2]Source: Secretaría de Agricultura y Desarrollo Rural, “Presenta Gobierno de México plan para aumentar la soberanía y la autosuficiencia alimentaria,” gob.mx. The legacy MasAgro initiative connected 35 Mexican seed companies to global germplasm pools, laying the groundwork for today’s domestic multiplication clusters. Producers gain predictable pricing via crop insurance and minimum-price schemes that cushion adoption risk.

Rising Demand for Virus-resistant Tomato and Pepper Seed

Disease pressure intensification has elevated virus-resistant varieties to critical importance in Mexico's vegetable production systems. Syngenta's Mexico hot pepper innovation program demonstrates this focus, developing varieties like Mexica, Tlapaneco, Purépecha, Chametla, Silex, and Obsidiana with enhanced bacterial leaf spot resistance and soil wilt tolerance. Climate change amplification of pest and disease pressure, particularly in Northern Mexico, increases the premium value of resistance traits. Export market requirements further drive demand, as international buyers increasingly specify disease-resistant varieties to ensure supply chain reliability and reduce post-harvest losses.

E-commerce Channels Reaching Smallholders

Digital storefronts close the distance between breeders and rural buyers. Bayer’s Nucle.ag platform debuted in 2022 and now spans all major cropping belts, giving farmers transparent price discovery and doorstep delivery. Online bundling of agronomic advice, credit, and crop insurance trims transaction friction and discourages grey-market intermediaries. Early sales data from Bajío and Occidente states show repeat purchase rates exceeding within one year, signaling sticky behavior among resource-limited growers adopting certified seed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-scarcity-driven planting cuts in Northwestern states | -1.1% | Sinaloa, Sonora, and Chihuahua | Short term (≤ 2 years) |

| Concentrated supplier power inflating seed prices | -0.7% | National, acute in remote regions | Medium term (2-4 years) |

| Counterfeit/gray-market seed inflow | -0.5% | National hotspots | Short term (≤ 2 years) |

| GMO-related regulatory uncertainty | -0.4% | National, affecting biotechnology adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water-Scarcity Driven Planting Cuts in Northwestern States

Irrigation reservoirs in Sinaloa average 7.1% and Sonora 12.2% of capacity, slashing vegetable acreage by nearly half in 2025. Farmers pivot to wheat or barley that consume less water, undercutting immediate hybrid demand. Emergency federal relief funds prioritize potable water, leaving growers to self-finance drip upgrades. The downturn temporarily blunts Mexico vegetable seed market momentum yet accelerates interest in drought-immune genetics. This agricultural restructuring creates both immediate demand destruction for traditional vegetable seeds and emerging opportunities for drought-tolerant varieties and water-efficient cultivation systems.

Concentrated Supplier Power Inflating Seed Prices

Market concentration among seed suppliers has intensified pricing pressures, particularly affecting smallholder access to certified varieties. The counterfeit seed market's annual impact, representing approximately 10% of Mexico's total seed market, demonstrates the price sensitivity driving farmers toward unregulated alternatives. E-commerce platforms like Bayer's Nucle.ag, launched in Mexico in 2022 and expanding from Bajío and Occidente states nationwide, represent potential solutions to distribution inefficiencies that contribute to pricing pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid dominance anchored by export yield premiums

Hybrids captured 86.65% market share in 2025 and are projected to maintain the overall market growth rate of 5.35% through 2031, reflecting their established dominance in Mexico's commercial vegetable production. The segment's performance stems from yield advantages and disease resistance traits that justify premium pricing, particularly in export-oriented production systems where consistency and quality standards are paramount. Syngenta's Mexico hot pepper program, producing varieties like Mexica, Tlapaneco, and Purépecha with enhanced bacterial leaf spot resistance, illustrates the specialized breeding focus on local disease pressures and market requirements.

Open Pollinated Varieties and Hybrid Derivatives occupy the remaining market share, serving primarily smallholder and traditional production systems where seed saving practices remain economically viable. The government's constitutional amendment promoting "traditional agricultural practices using native seeds and agroecological methods" may provide policy support for this segment, though commercial impact remains limited given the productivity gap with hybrids.

By Cultivation Mechanism: Protected systems propel value and resilience

Open field cultivation commands 86.40% market share in 2025, reflecting Mexico's traditional agricultural structure and the cost constraints facing smallholder producers. Protected cultivation demonstrates superior growth potential with a 6.65% CAGR through 2031, driven by export market requirements and productivity advantages. Protected tomato production achieves approximately 4 times the yields of open-field systems, enabling Mexican producers to compete effectively against established regions like Florida.

Mexico vegetable seed market size in protected niches is forecast to top by 2031, implying nearly 17.4% of total dollar sales due to premium price points and multicycle plantings. Seed firms co-locate demo houses alongside local agronomists, compressing learning curves and lifting repeat purchase rates above 70% within two seasons. Counter-season global demand remains robust, cushioning revenue when drought curtails open-field plantings.

By Crop Family: Solanaceae scale leads; specialty vegetables accelerate diversification

By crop family, Solanaceae commanded 26.55% of the Mexico vegetable seed market size in 2025, and is anticipated to rise at a 5.95% CAGR to 2031. Disease resistance breakthroughs against ToBRFV and bacterial spot keep replacement cycles short, while consumer appetite for differentiated flavors supports color and capsaicin segment splits. Hybrid jalapeño packages now bundle five-gene pyramids that trim spray counts by 20% per harvest.

Growth momentum shifts toward unclassified vegetables, posting 6.72% CAGR as growers chase niche margins in asparagus, lettuce, and baby leaf mixes for direct-to-retail clamshells. Organic acreage touches nearly 50,000 hectares nationwide, and specialty growers demand untreated or bio-primed seed formats. Brassicas and cucurbits hold a steady share, benefiting from expanded mid-latitude plantings in Guanajuato and Michoacán, where climatic risk is lower than in the parched Northwest. Root crops such as carrots and beets find room in protected tunnels, extending Northern supply windows into December.

Geography Analysis

Northern powerhouse Sinaloa historically underpinned the Mexico vegetable seed market, yet 2025 drought conditions halved regional output and slashed hybrid call-offs. Dam levels at 7.1% forced growers to idle high-water crops and pivot to wheat rotations, triggering an immediate demand gap for tomato and cucumber genetics. Despite the setback, Sinaloa’s proximity to United States ports of entry keeps it indispensable for rapid truck delivery that matches tight supermarket shelf-life windows. Seed suppliers embed drought-tolerance screening plots to secure comeback potential once water allocations stabilize.

Central states Guanajuato, Jalisco, and Querétaro emerge as the new growth belt for the Mexico vegetable seed market. Bayer’s MXN 63 million (USD 3.15 million) 2025 line expansion in Guanajuato anchors a rising input hub that serves contiguous greenhouse corridors. The area benefits from high-elevation microclimates that slash pest pressure by up to 30%, allowing more economical residue-free programs sought by United States and Canadian buyers. Municipal incentives cover up to 50% of greenhouse steel frame costs, spurring mid-sized operators to upscale.

Southern Mexico demonstrates the fastest percentage gains as the Cosechando Soberanía program channels into credit, irrigation modules, and extension staff. Chiapas doubles as a hybrid seed-production enclave, exporting habanero and cucumber seed under eight-year phytosanitary contracts. Lower land values and abundant rainfall attract firms to establish isolation fields for parent lines, safe from cross-pollination. E-logistics through revamped rail links to Veracruz port widens access to European clients, further embedding the south in the export value chain and bolstering overall Mexico vegetable seed market resilience.

Competitive Landscape

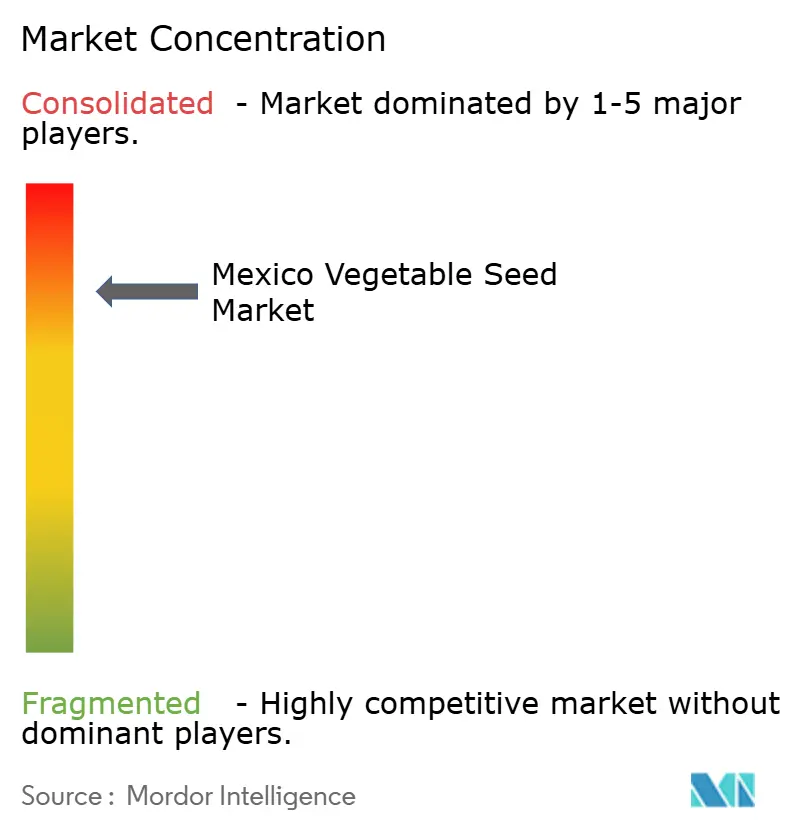

The Mexico vegetable seed market exhibits high concentration, with established multinational players maintaining dominant positions through technological innovation and distribution network advantages. Market leadership remains fragmented across crop categories, with companies like Syngenta Group, Bayer AG, Groupe Limagrain, and Rijk Zwaan Zaadteelt en Zaadhandel BV leveraging specialized breeding programs and local production capabilities to capture share. Bayer maintains a comprehensive presence in Mexico.

Syngenta leverages a pepper-focused breeding base in Los Mochis, escalating jalapeño and serrano lines that target ToBRFV. The firm’s February 2025 onion licensing pact with Emerald Seed introduces broader germplasm diversity to local partners, signaling deeper vertical integration. East-West Seed maintains outreach through demo clusters in the southern highlands, championing high-germ small-pack hybrids for resource-poor farmers and eroding counterfeit appeal.

Counterfeit crackdowns create opportunities for legitimate suppliers. These suppliers collaborate with federal customs to implement QR trackers on every 5-kg can. Additionally, water scarcity is influencing strategies, with breeders raising drought-scoring thresholds during multi-environment trials, aiming for long-term benefits as climatic volatility stabilizes. In this evolving landscape, the Mexico vegetable seed market favors companies that combine trait innovation, risk-sharing financial models, and omnichannel distribution strategies.

Mexico Vegetable Seed Industry Leaders

BASF SE

Bayer AG

Groupe Limagrain

Rijk Zwaan Zaadteelt en Zaadhandel BV

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bayer invested MXN 63 million (USD 3.15 million) in Guanajuato plant expansion, enhancing production capabilities for the Mexican market. This investment reflects continued confidence in Mexico's agricultural growth potential despite regional challenges.

- April 2025: PROSEBIEN established a government seed production facility in Calera, Zacatecas, focusing on bean and rice seed production as part of Mexico's food sovereignty initiative.

Mexico Vegetable Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field, Protected Cultivation are covered as segments by Cultivation Mechanism. Brassicas, Cucurbits, Roots & Bulbs, Solanaceae, Unclassified Vegetables are covered as segments by Crop Family.Breeding Technology

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Crop Family

| Brassicas | Cabbage |

| Cauliflower and Broccoli | |

| Other Brassicas | |

| Cucurbits | Cucumber and Gherkin |

| Pumpkin and Squash | |

| Other Cucurbits | |

| Roots and Bulbs | Garlic |

| Onion | |

| Potato | |

| Other Roots and Bulbs | |

| Solanaceae | Chilli |

| Eggplant | |

| Tomato | |

| Other Solanaceae | |

| Unclassified Vegetables | Asparagus |

| Lettuce | |

| Okra | |

| Peas | |

| Spinach | |

| Other Unclassified Vegetables |

| Breeding Technology | Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives | ||

| Cultivation Mechanism | Open Field | |

| Protected Cultivation | ||

| Crop Family | Brassicas | Cabbage |

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Roots and Bulbs | Garlic | |

| Onion | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Solanaceae | Chilli | |

| Eggplant | ||

| Tomato | ||

| Other Solanaceae | ||

| Unclassified Vegetables | Asparagus | |

| Lettuce | ||

| Okra | ||

| Peas | ||

| Spinach | ||

| Other Unclassified Vegetables | ||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms