United States Garden Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.20 Billion |

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

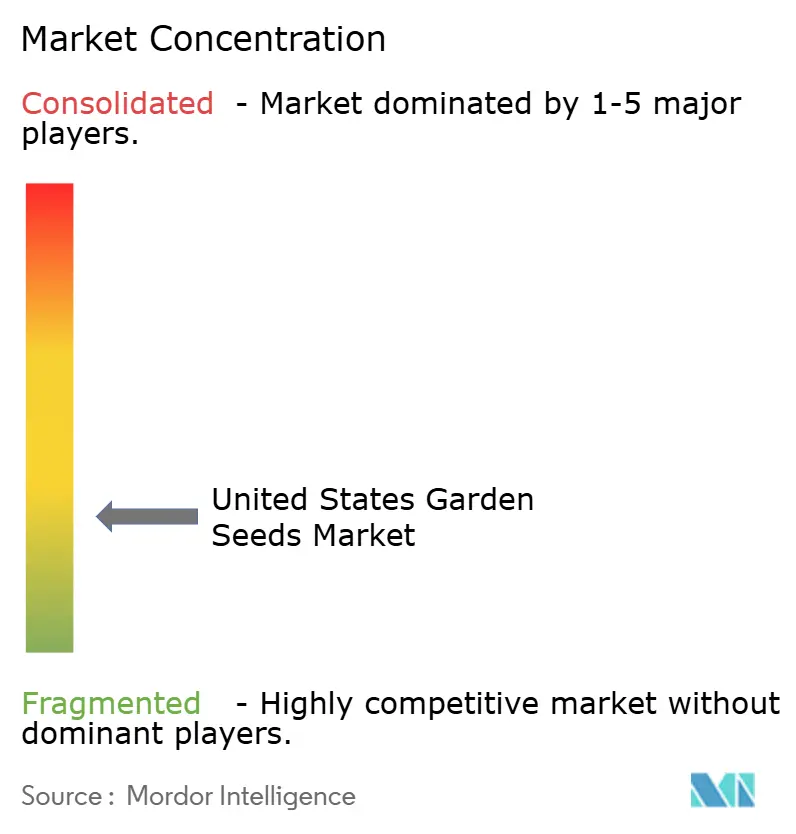

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Garden Seeds Market Analysis by Mordor Intelligence

The United States garden seeds market size was valued at USD 1.20 billion in 2025 and estimated to grow from USD 1.26 billion in 2026 to reach USD 1.59 billion by 2031, at a CAGR of 4.79% during the forecast period (2026-2031). Pandemic-era enthusiasm matured into sustained home-growing habits, while climate awareness and food-price volatility continue to motivate seed purchases. Urban migration fuels demand for compact, container-friendly cultivars, while stricter organic certification standards reinforce the premium segment. Innovation in climate-resilient hybrids, pollinator-friendly varieties, and heirloom collections is gaining traction, particularly among younger and eco-conscious consumers. At the same time, digital disruption through online marketplaces, mobile apps, and subscription services is transforming access, variety, and care guidance, fostering stronger customer engagement. Competitive intensity remains high, as brand loyalty, trust, and educational content increasingly outweigh price competition, creating room for niche breeders and specialty players to thrive alongside established legacy firms.

Key Report Takeaways

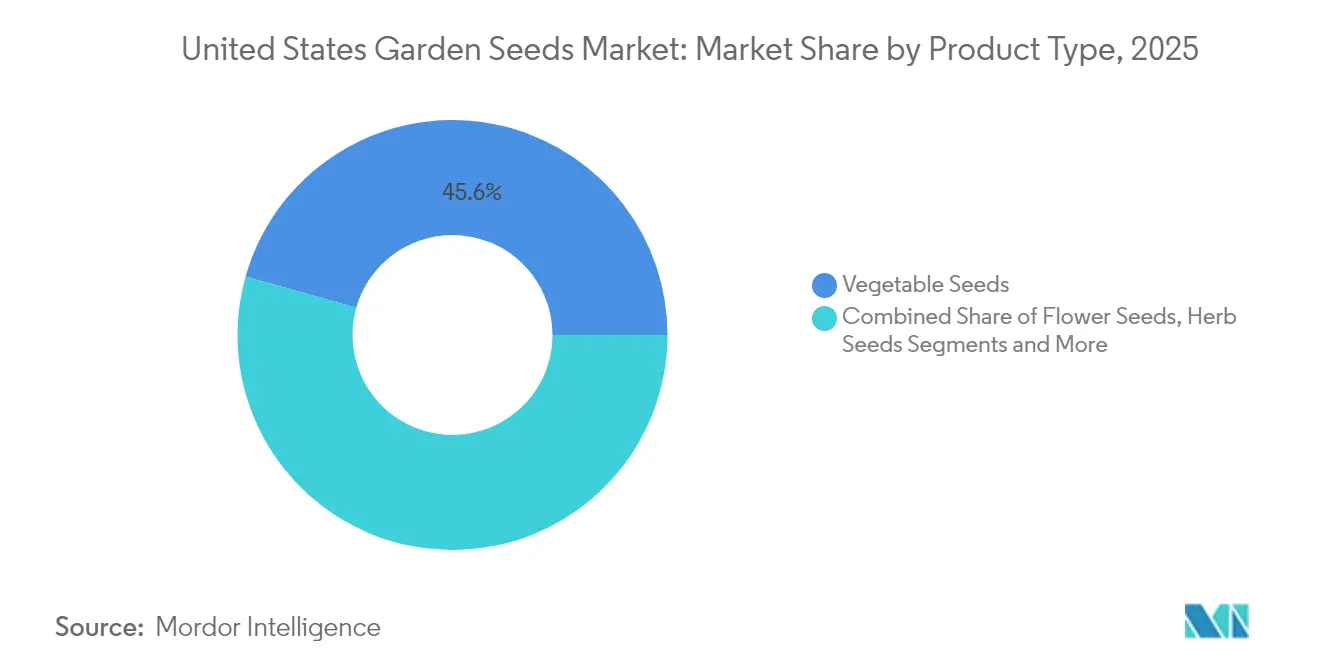

- By product type, vegetable seeds held 45.62% of the United States garden seeds market size in 2025, whereas herb seeds are forecast to grow at a 8.69% CAGR to 2031.

- By distribution channel, garden centers and nurseries led with 33.52% market share in 2025, and online marketplaces and Subscriptions are advancing at a 12.32% CAGR through 2031.

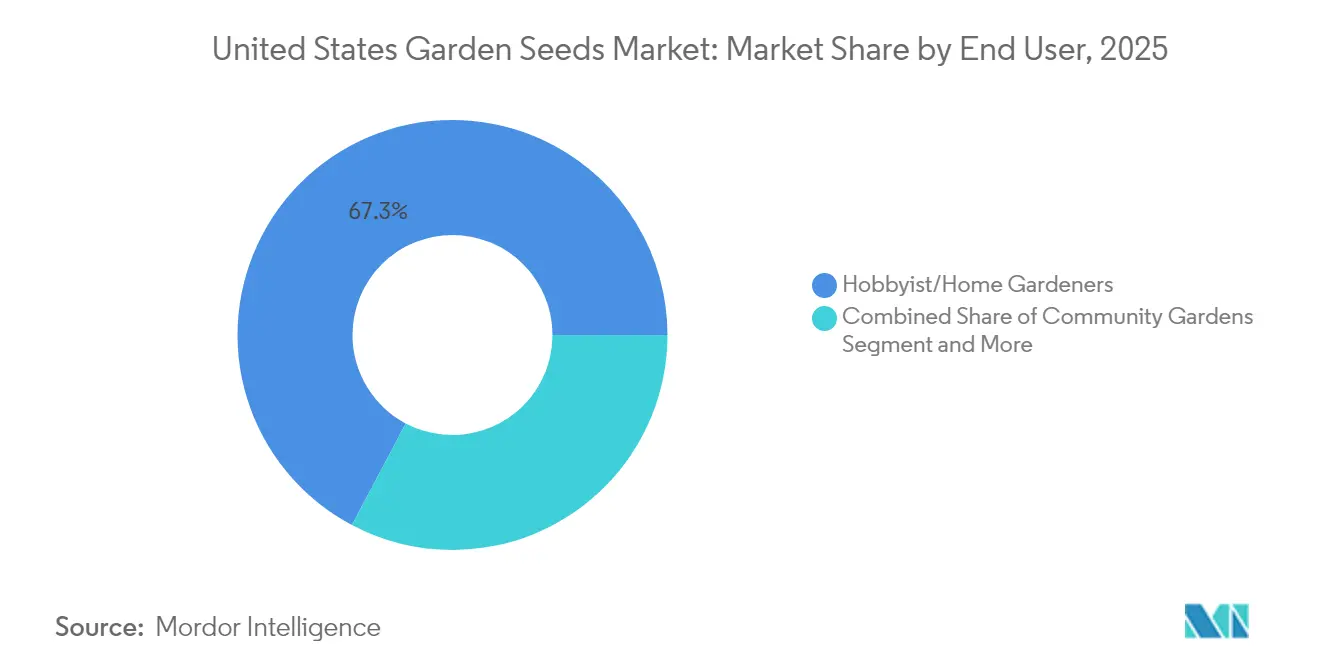

- By end user, hobbyists/home gardeners accounted for 67.25% share of the United States garden seeds market size in 2025, while community gardens are poised to expand at a 9.92% CAGR to 2031.

- By seed form, the open pollinated 39.92% market share in 2025, and the organic seeds are set to post the fastest 11.18% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Garden Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in home gardening post-pandemic | +1.2% | Nationwide, strongest in suburbs | Medium term (2-4 years) |

| Expansion of farm-to-table movement | +0.8% | Urban centers, West, and Northeast | Long term (≥4 years) |

| Growth in organic and non-GMO preferences | +1.0% | Nationwide, premium coastal markets | Long term (≥4 years) |

| Municipal incentives for urban gardens | +0.6% | Metropolitan food deserts | Medium term (2-4 years) |

| Rising adoption of e-commerce seed subscriptions | +0.7% | Nationwide, digital-native consumers | Short term (≤2 years) |

| Climate-resilient seed R&D grants | +0.5% | Drought-prone and farming states | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in Home Gardening Post-Pandemic

In United States households, about 89% engaged in gardening in 2024, spending an average of USD 671 as of 2024 compared to USD 458 in 2020, showing durable demand for starter kits, disease-resistant varieties, and patio-sized cultivars. Younger cohorts cement this trend, with 65.4% of Gen Z reporting additional gardening time in 2024 and nearly 70% planning more in 2025. Remote work flexibility and mental-wellness awareness underpin the persistence of home food production. Product managers respond with easy-grow seed tapes, QR-code tutorials, and grow-light bundles that align with apartment living.

Expansion of Farm-to-Table Movement

Restaurants increasingly stipulate regional sourcing, which encourages smallholders to seek specialty seeds adapted to highly specific microclimates. Urban Community Supported Agriculture (CSA) operators now demand rapid-maturity lettuces, compact tomatoes, and other crops that can reliably fit weekly harvest and box delivery schedules. Cut-flower growers mirror this trend, selecting long-stem, sequential-bloom cultivars that guarantee continuity of supply for local florists. Alongside this, community-based distribution hubs are expanding, connecting breeders, seed savers, and chefs, thereby embedding locality and freshness as a durable competitive moat within the United States garden seeds market.

Municipal Incentives for Urban Gardens

The USDA Urban Agriculture and Innovative Production grants disbursed USD 14.4 million in 2025, helping fund seed purchases for community plots, educational farms, and school garden projects [1]USDA Office of Urban Agriculture and Innovative Production, “Grant Awards FY 2025,” usda.gov. Cities such as Cleveland supplement this momentum, reimbursing up to USD 5,000 per entrepreneur for seed and tool expenses [2]USDA National Institute of Food and Agriculture, “Plant Breeding Grants 2024,” usda.gov. Such programs stimulate steady institutional demand for container-adapted, high-yield seed lines suitable for small spaces. Vendors who bundle bulk seed packs with lesson plans, training modules, and community engagement materials increase their chances of winning public tenders and forging recurring partnerships with municipalities and schools.

Rising Adoption of E-Commerce Seed Subscriptions

Digital-native consumers increasingly favor algorithm-curated seed subscription boxes that arrive seasonally with pre-marked sow-by dates, companion planting tips, and even chatbot coaching for novice growers. These services improve planting success and lower churn rates, with some firms reporting cancellations below 9% because timely deliveries prevent missed sowing windows. To remain competitive, traditional seed companies are pivoting toward digital integration, layering mobile apps and augmented-reality plant-spacing tools into their offerings. This evolution sustains brand relevance and ensures broader appeal in the rapidly digitizing United States garden seeds market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seed supply disruptions from extreme weather | -1.1% | Pacific Northwest and Gulf Coast seed farms | Short term (≤2 years) |

| Tightening state-level GMO regulations | -0.4% | California, Maine, and Vermont | Medium term (2-4 years) |

| Consolidation of commercial seed genetics | -0.6% | Nationwide independent breeders | Long term (≥4 years) |

| Labor shortages affecting small seed farms | -0.5% | Idaho, Oregon, and Michigan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seed Supply Disruptions from Extreme Weather

Intensifying hurricanes, late frosts, and prolonged droughts increasingly shorten pollination windows and complicate the isolation distances needed to maintain seed purity, directly reducing reliable output and elevating wholesale prices [3]USDA Climate Hubs, “Seed Production and Climate Risk,” climatehubs.usda.gov. Larger companies are diversifying growing sites across multiple climate zones, adding greenhouse capacity, and investing in cold-storage buffers to stabilize supply chains. Smaller operators, however, often lack such capital reserves, creating catalog gaps, frustrating loyal customers, and constraining overall market growth in the United States garden seeds sector when seasonal shortages cascade across distribution networks.

Tightening State-Level GMO Regulations

New labeling mandates in California and Northeastern states require clear GMO disclosures, raising compliance costs while elevating consumer scrutiny of seed provenance and traceability. Retailers increasingly demand verified documentation from marketers, which lengthens lead times and slows rapid product launches. For smaller seed firms, fragmented regulations compound testing and certification expenses. Meanwhile, established OEMs leverage compliance infrastructure to reinforce brand credibility, but the cumulative regulatory pressure creates uneven competition and challenges agile innovation, constraining flexibility in the evolving United States garden seeds market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetable Dominance, Herb Upswing

Vegetable Seeds contributed 45.62% to the United States garden seeds market size in 2025, reflecting the practical appeal of kitchen crops for food security and flavor diversity. Heirloom tomatoes, cut-and-come-again lettuces, and disease-resistant beans lead reorder volumes. Herb Seeds register the highest 8.69% CAGR outlook, supported by wellness narratives around basil, cilantro, and medicinal lavender. Flower Seeds maintain a stable share through pollinator-friendly mixes and long-bloom zinnias, while Fruit Seeds struggle due to space and patience requirements.

Seasonal catalogs emphasize open-pollinated lines and seed-saving tips, nurturing community exchanges that reinforce customer loyalty. USDA-funded drought-tolerant peppers and short-season melons expand relevance in warming northern zones. Container-suitable varieties, such as patio eggplants, align with urban balcony gardening and lift premium SKU counts inside the United States garden seeds market.

By Distribution Channel: Specialist Service versus Digital Convenience

Garden Centers and Nurseries led 2025 distribution with 33.52% share, leveraging on-site expertise and plant-health guarantees. Staff recommendations help convert browsers into purchasers of higher-margin specialty packs. Online Marketplaces and Subscriptions, advancing at a 12.32% CAGR, respond to click-to-door expectations and broaden cultivar access beyond regional inventories.

Hybrid retail emerges as stores launch e-commerce platforms with curbside pickup and member-only webinars. Home-Improvement Stores cross-sell seed racks beside soil and raised-bed kits, capturing impulse buyers. Mail-Order Catalogs retain niche appeal among master gardeners seeking exhaustive variety descriptions, sustaining a bibliophile subculture within the United States garden seeds market.

By End User: Hobby Buyers Anchor Demand

Hobbyists/Home Gardeners generated 67.25% of 2025 revenue, spanning novices trialing salad greens to experienced seed savers cultivating rare heirlooms. Post-pandemic mental-health narratives and grocery inflation solidify this cohort. Community Gardens are projected to record a 9.92% CAGR through 2031, catalyzed by civic grants and nonprofit initiatives that finance bulk seed purchases and raised-bed installations.

Small-scale Commercial Growers supply farmers' markets and farm-to-table eateries, demanding reliable germination, uniform maturation, and recognizable flavor profiles. Institutional campuses integrate edible landscapes into wellness programs, selecting low-maintenance perennial herbs and salad mixes that require minimal oversight yet maximize employee engagement.

By Form Seeds: Open-Pollinated Roots, Organic Momentum

Open-pollinated varieties accounted for 39.92% of the United States garden seeds market share in 2025. These seeds allow gardeners to save seeds and adapt plant lines to local conditions, providing long-term cost efficiency. Their contribution to biodiversity conservation and self-sufficiency adds to their appeal among gardeners. Hybrid seeds maintain their market position due to their consistent size, enhanced disease resistance, and higher yields, particularly among hobby gardeners with limited space. Conventional treated seeds continue to serve price-sensitive consumers by offering reliable germination rates.

The organic seeds segment demonstrates the highest growth rate, with an 11.18% CAGR projected through 2031. Enhanced federal regulations have improved certification standards and reduced substandard imports. Despite commanding 20-40% price premiums, organic seeds attract consumers, particularly those who regularly purchase organic produce. The USDA's USD 2.2 million educational funding through the Organic Trade Association supports this growth. While affluent urban consumers drive demand, the market is expanding into suburban and rural areas. Heirloom varieties maintain a specialized market position due to their distinct flavors and historical significance, though their inconsistent shapes and yields limit their broader market adoption.

Geography Analysis

The Midwest’s captured of 28.74% of the United States garden seeds market in 2025 stems from cultural familiarity with seed cultivation, readily available backyard space, and short supply chains that keep packets fresh. Specialty-crop cash receipts exceeding USD 3.8 billion in 2024 signal healthy spillover into consumer seed demand. Extension agents collaborate with local breeders to trial disease-resistant sweet corn and frost-tolerant kale, ensuring regional catalogs stay relevant.

The West’s rapid growth, projected to grow at a CAGR of 8.21% through 2031, aligns with rising population, sustainability priorities, and stringent water regulations that elevate interest in xerophytic and fire-resistant species. California’s organic acreage, the nation’s largest, normalizes premium pricing for certified packets, while rebate programs for lawn-to-garden conversions redirect household spending to seeds and drip-irrigation kits. Tech-savvy residents adopt gardening apps pairing climatic data with sowing alerts, integrating digital habits into traditional horticulture.

The South and Northeast occupy mid-tier growth trajectories, each facing distinctive climatic challenges. Southern heat and humidity accelerate disease pressure, fueling demand for downy-mildew-resistant basil and heat-stable lettuce. Northeastern urbanization restricts space, promoting dwarf tomatoes and vertically growing beans. Cooperative extension webinars and seed libraries encourage participation, broadening the addressable base for the United States garden seeds market.

Competitive Landscape

Competition in the United States garden seeds market remains fragmented, with heritage brands and global breeders competing for market presence. W. Atlee Burpee Company maintains strong consumer loyalty through its 150-year legacy, multi-channel presence, and educational media. Johnny's Selected Seeds establishes its market position through trial-backed cultivars and detailed crop guides that reduce purchasing risks for serious gardeners. Baker Creek Heirloom Seeds attracts heritage enthusiasts through rare varieties and biannual festivals that serve as cultural gatherings and marketing events.

Regional specialists like Territorial Seed Company focus on Pacific Northwest-specific assortments, while major genetics companies, including Ball Horticultural Company, Syngenta Seeds, LLC (Vegetable Seeds US), and Bayer AG, partner with mass-market retailers for broader distribution. Product development advances through technology partnerships, exemplified by Bayer AG's 2025 collaboration with Source.ag to incorporate AI-driven simulations in variety trials. The market evolution continues with subscription-based companies using data analytics to provide customized seasonal seed boxes and complementary soil amendments, targeting younger consumers and generating recurring revenue.

Regulatory requirements create distinct competitive barriers. Companies with established auditing systems benefit from USDA organic enforcement, while postal weight limits for seed packets influence distribution strategies. Major breeders such as Sakata Seed Corporation, Enza Zaden Beheer B.V., Groupe Limagrain, and Rijk Zwaan Zaadteelt en Zaadhandel B.V. consolidate intellectual property rights, prompting independent companies to adopt open-source or public-domain genetics to strengthen community relationships, despite ongoing funding requirements. The market success factors include authenticity, effective customer education, and operational flexibility rather than size alone.

United States Garden Seeds Industry Leaders

Johnny’s Selected Seeds

Baker Creek Heirloom Seeds

Ball Horticultural Company

Territorial Seed Company

W. Atlee Burpee Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Namdhari Seeds acquired 100% of Axia Vegetable Seeds’ open-field portfolio, including the US Agriseeds brand, to expand distribution in North America.

- January 2024: NativeSeed Group acquired Star Seed, Inc. of Kansas, expanding its footprint in the Midwest and deepening access to native and conservation species. While primarily restoration-focused, the deal strengthens the supply of wildflower and cover crop seeds, indirectly supporting United States garden seed demand for pollinator-friendly and climate-resilient varieties.

- February 2023: W. Atlee Burpee Company launched new seed varieties, including Vivacious Hybrid Tomato, Creme Brulee Sunflower, Rise and Shine Squash, Two Tasty Hybrid Tomato, Bliss Tomato Hybrid, and Party Time Cucumber.

United States Garden Seeds Market Report Scope

Garden seeds are packaged seeds directly sold to consumers through various sales channels, including online sales, groceries, and specialized stores. The report provides information on garden seeds and includes community and home gardens while estimating the market numbers.

The United States Garden Seed Market is Segmented by Seed Type (Vegetable Seeds (Tomato, Cucumber, Carrot, Culinary Herbs, and Other Vegetable Seeds), Flowers and Ornamental Seeds, and Fruit Seeds (Berries, Melons, and Other Fruit Seeds)) and Sales Channel (Online Sales, Specialized Stores, and Groceries). The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Vegetable Seeds |

| Flower Seeds |

| Herb Seeds |

| Fruit Seeds |

| Others (e.g., hobby cereals such as groundnut) |

| Garden Centers and Nurseries |

| Home Improvement Stores |

| Grocery and Mass Retail |

| Mail-Order Catalogs |

| Online Marketplaces and Subscriptions |

| Hobbyist/Home Gardeners |

| Community Gardens |

| Commercial Growers (Small-scale) |

| Institutional and Corporate Campuses |

| Open Pollinated |

| Hybrid |

| Organic |

| Others |

| By Product Type | Vegetable Seeds |

| Flower Seeds | |

| Herb Seeds | |

| Fruit Seeds | |

| Others (e.g., hobby cereals such as groundnut) | |

| By Distribution Channel | Garden Centers and Nurseries |

| Home Improvement Stores | |

| Grocery and Mass Retail | |

| Mail-Order Catalogs | |

| Online Marketplaces and Subscriptions | |

| By End User | Hobbyist/Home Gardeners |

| Community Gardens | |

| Commercial Growers (Small-scale) | |

| Institutional and Corporate Campuses | |

| By Seed Form | Open Pollinated |

| Hybrid | |

| Organic | |

| Others |

Key Questions Answered in the Report

How large is the United States garden seeds market in 2026?

The market is valued at USD 1.26 billion in 2026 and is expected to reach USD 1.59 billion by 2031.

What is the projected growth rate for garden seeds through 2031?

A 4.79% CAGR is forecast for 2026-2031, driven by sustained home-gardening and organic trends.

Which product segment leads sales?

Vegetable Seeds dominate with 45.62% share in 2025, meeting demand for home food production.

What role do online channels play?

Online Marketplaces and Subscriptions are growing at 12.32% CAGR, propelled by convenience and curated seasonal boxes.

Page last updated on: