Functional Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.98 Billion |

| Market Size (2031) | USD 8.48 Billion |

| Growth Rate (2026 - 2031) | 11.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

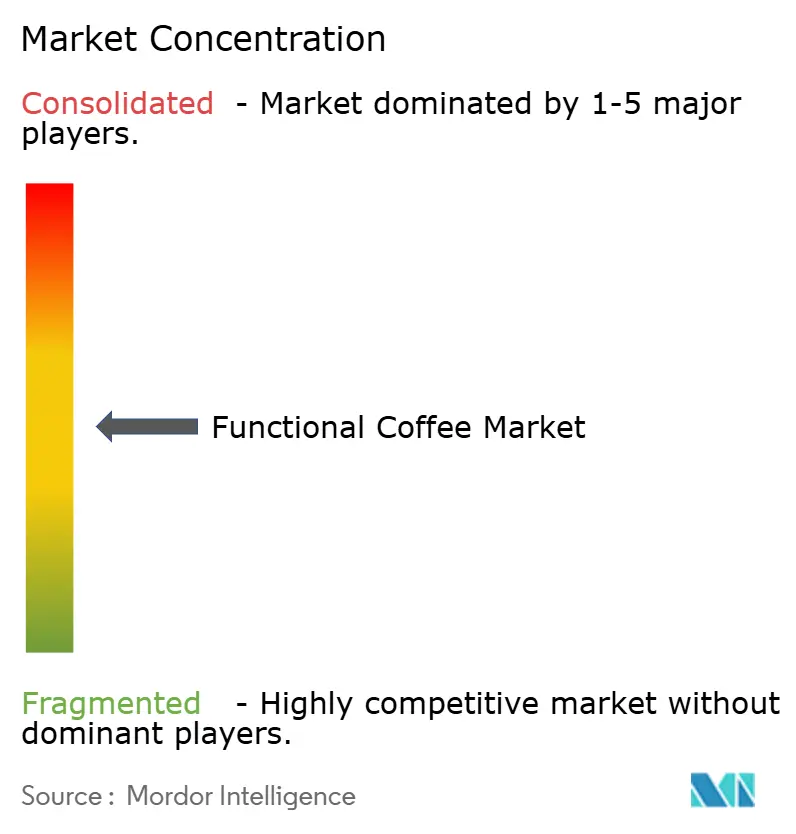

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Functional Coffee Market Analysis by Mordor Intelligence

The global functional coffee market size was valued at USD 4.48 billion in 2025 and estimated to grow from USD 4.98 billion in 2026 to reach USD 8.48 billion by 2031, at a CAGR of 11.23% during the forecast period (2026-2031). The market expansion is driven by increasing consumer preference for beverages that provide health benefits beyond traditional caffeine effects. Ready-to-drink formats dominated with 68.88% market share in 2024 and are projected to maintain the highest growth rate at 12.53% CAGR through 2030. Consumer demand focuses on beverages that combine energy, cognitive support, immunity benefits, and clean-label ingredients in a single product. Manufacturers are incorporating adaptogens, nootropics, and probiotics alongside caffeine to create distinctive products. Ready-to-drink (RTD) products remain significant due to their precise dosing, portability, and extended shelf life, while single-serve pods gain momentum in the home segment as sustainable designs transition from development to commercial production.

Key Report Takeaways

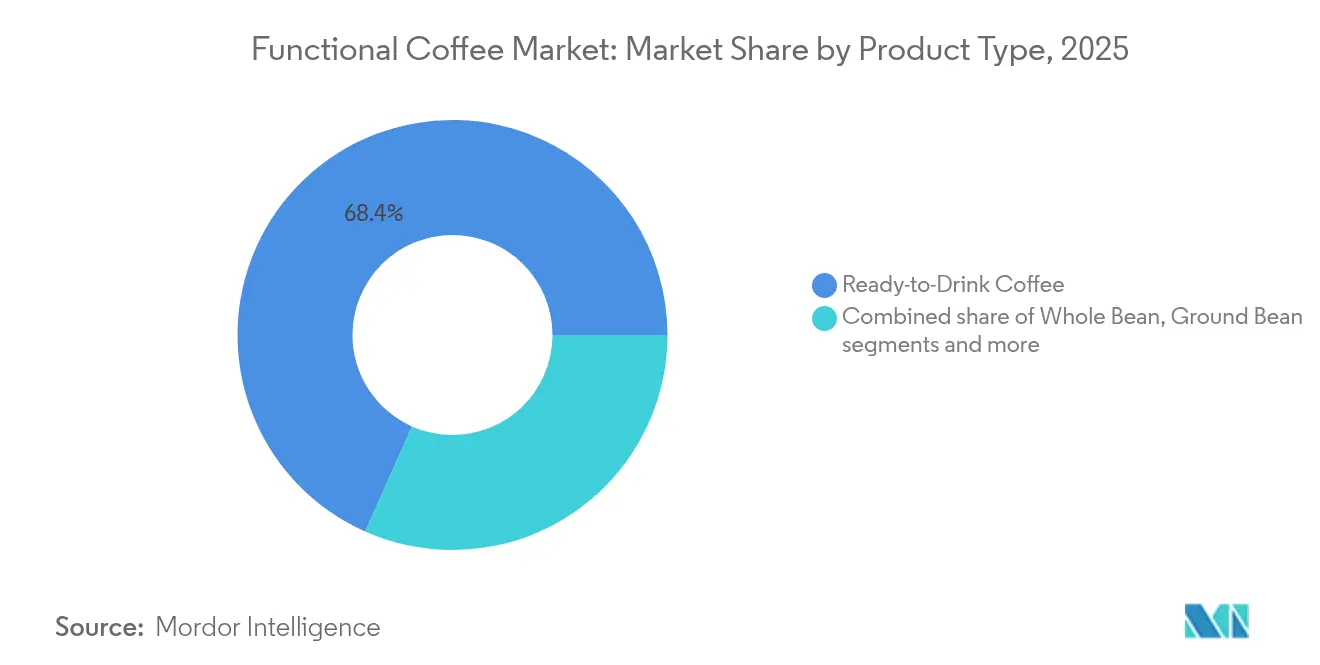

- By product type, RTD coffee held 68.35% of functional coffee market share in 2025 and is projected to post a 12.18% CAGR through 2031.

- By functional claim, energy-focused formulations commanded 33.25% revenue share in 2025, while nootropic/mental-focus beverages are set to expand at a 12.05% CAGR between 2026-2031.

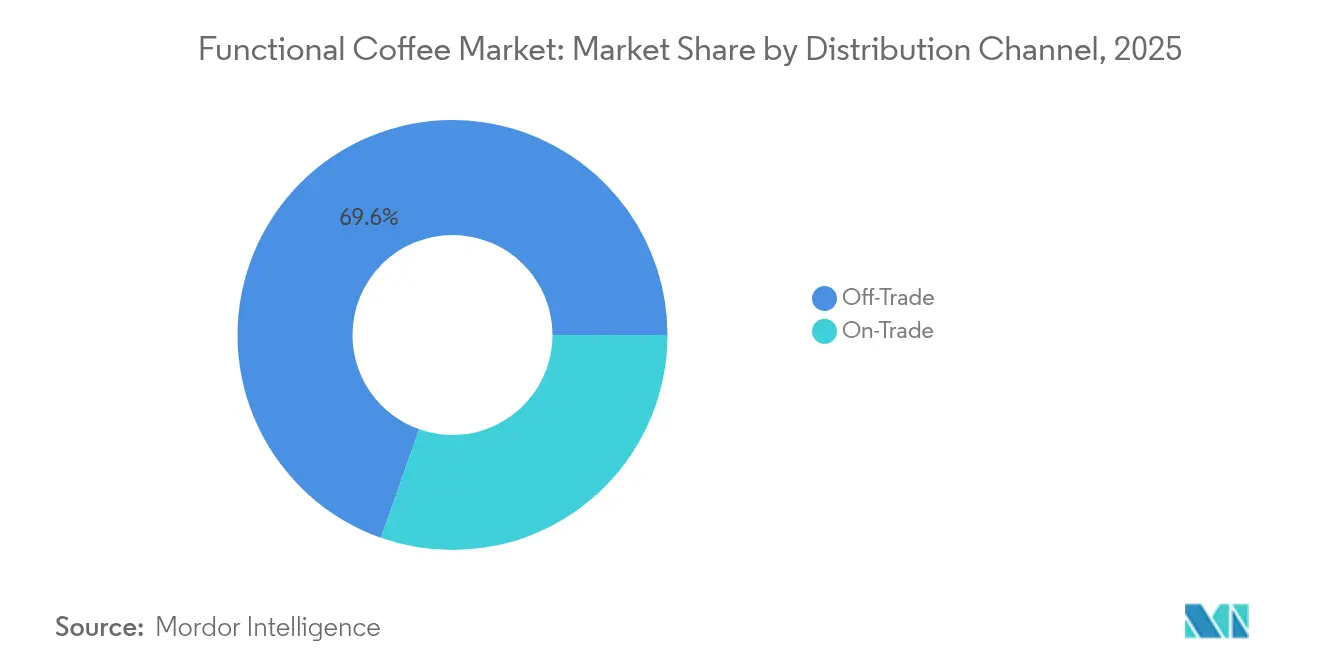

- By distribution channel, off-trade platforms accounted for 69.60% sales in 2025; on-trade venues are forecast to climb at a 12.20% CAGR to 2031 as coffee shops widen functional menus.

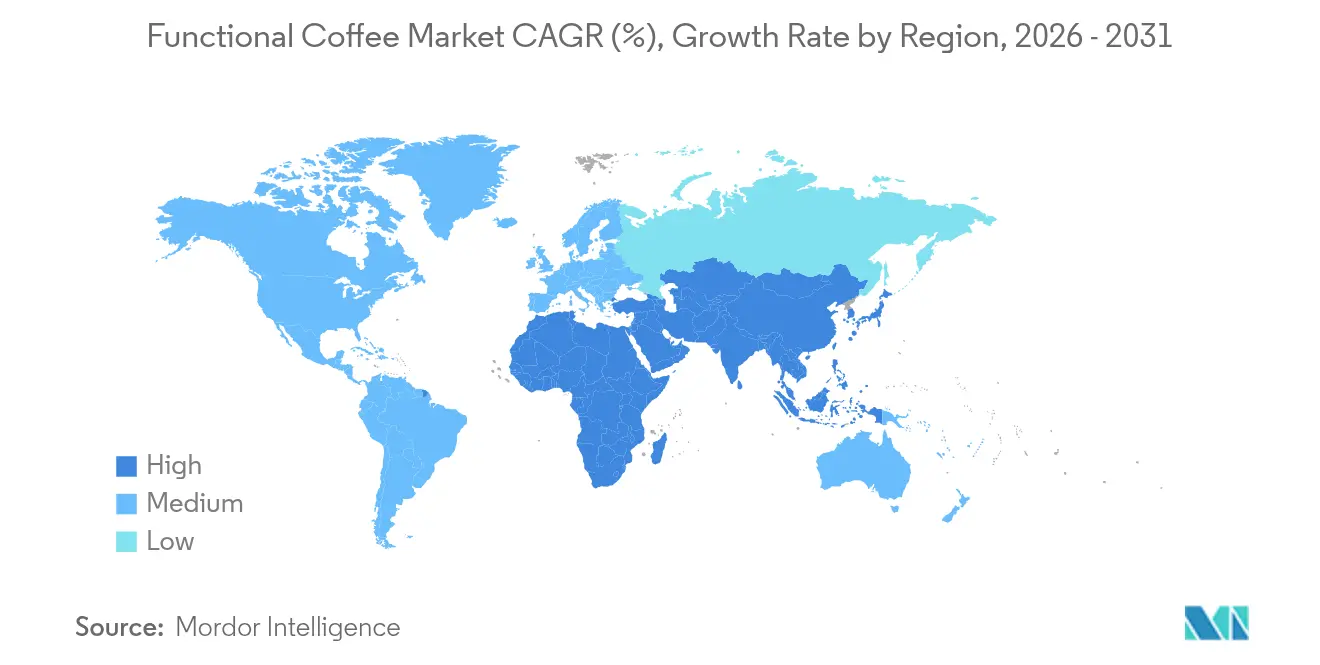

- By geography, North America captured 68.60% share of functional coffee market size in 2025, whereas Asia-Pacific is advancing at a 13.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Functional Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of adaptogens and nootropics in coffee formulations | +2.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of product innovation incorporating botanicals, probiotics, and superfoods | +2.1% | North America core, expanding to Asia-Pacific markets | Long term (≥ 4 years) |

| Rising penetration of ready-to-drink (RTD) functional coffee products | +3.2% | Global, particularly strong in Asia-Pacific | Short term (≤ 2 years) |

| Consumer preference for clean-label and natural ingredient products | +1.9% | North America and Europe primary, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Advancements in extraction and infusion technologies for precise formulation | +1.4% | Global, with technology hubs in North America and Europe | Long term (≥ 4 years) |

| Growing awareness of benefits of antioxidants and anti-inflammatory ingredients | +1.7% | Global, with educational campaigns in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Popularity of Adaptogens and Nootropics in Coffee Formulations

Adaptogenic ingredients such as ashwagandha, reishi mushrooms, and lion's mane are increasingly being incorporated into coffee formulations, driven by growing consumer interest in health and wellness. These ingredients are known for their potential to reduce stress, improve focus, and enhance overall cognitive function, making them appealing additions to functional beverages. The partnership between RYZE Superfoods and Calm highlights this trend, emphasizing products designed to provide cognitive benefits and sustained energy. This collaboration underscores the industry's growing focus on functional beverages that align with consumer wellness preferences, as more consumers seek products that support mental clarity and balanced energy levels. Similarly, Clevr's functional coffee brand has expanded its retail distribution to Target stores, featuring Fair Trade coffee blends infused with reishi and ashwagandha. This move reflects the broader acceptance of adaptogenic ingredients in mainstream markets, as consumers increasingly prioritize functional benefits in their daily routines. The nootropic beverage market is witnessing significant growth, driven by demand from gaming communities and professionals seeking cognitive enhancement through coffee-based products. These beverages cater to a growing demographic looking for convenient and effective ways to boost mental performance and productivity.

Expansion of Product Innovation Incorporating Botanicals, Probiotics, and Superfoods

Coffee product innovation reflects key advancements driven by changing consumer preferences and industry requirements. The integration of probiotics has introduced functional beverages that cater to the increasing focus on digestive health and overall wellness. These beverages not only provide the benefits of coffee but also support gut health, making them a dual-purpose option for consumers. Additionally, the market has expanded to include protein-enriched coffee formulations and mushroom coffee varieties, designed to appeal to health-conscious consumers seeking added nutritional benefits beyond traditional coffee. Protein-enriched coffee offers an energy boost combined with muscle recovery benefits, while mushroom coffee is gaining popularity for its potential adaptogenic properties and immune support. In terms of cultivation, the use of botanical pesticides enhances soil fertility while maintaining crop quality, promoting sustainable farming practices. These practices not only ensure long-term agricultural productivity but also align with the increasing consumer demand for environmentally friendly products. The functional beverages market is experiencing strong growth, highlighting substantial potential for health-focused coffee products that align with current wellness trends and consumer priorities.

Rising Penetration of Ready-to-Drink (RTD) Functional Coffee Products

Ready-to-drink (RTD) functional coffee products are experiencing significant market growth across Asia-Pacific regions, where urban consumers value products that complement their fast-paced lifestyles through convenience and portability. The younger consumer demographic is actively transitioning from traditional carbonated beverages to functional coffee options, with latte variants demonstrating strong market preference due to their enhanced functional properties. In response to this market demand, BKON has introduced its innovative Coldstretto® technology, incorporating Reverse Atmospheric Infusion (RAIN) methodology. This advancement produces shelf-stable cold espresso while reducing preparation time by more than 500%. As a result, food service establishments can now efficiently deliver premium functional coffee offerings to their customers without investing extensive resources in employee training programs [1]Source: Speciality Coffee Association, “Transforming Cold Espresso Creation for Foodservice and Consumers,” new.sca.coffee.

Consumer Preference for Clean-Label and Natural Ingredient Products

Consumers are increasingly seeking functional coffee products labeled as "no artificial ingredients" and "no preservatives." This shift in preferences has prompted manufacturers to reformulate their products using natural sweeteners such as allulose and stevia while preserving the desired taste. Taste remains the primary factor influencing the selection of healthy beverages, as consumers prioritize flavor alongside health benefits. To address this, manufacturers are adopting advanced flavor masking techniques to ensure that functional ingredients do not compromise the taste profile of their products. Additionally, consumers are placing greater emphasis on the overall health benefits, sustainability, and nutritional value of the products they consume. This growing awareness is further driving the demand for clean-label options, as consumers seek products that align with their health-conscious and environmentally responsible lifestyles. To build trust and remain competitive, companies are focusing on clean-label positioning and transparent communication regarding ingredient sourcing, nutritional benefits, and processing methods. By clearly articulating these aspects, brands can meet consumer expectations while also differentiating themselves in a crowded market. Highlighting their commitment to quality, transparency, and sustainability allows companies to establish a stronger connection with their target audience and reinforce their market presence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory frameworks on health claims and functional ingredients | -1.8% | Global, particularly restrictive in Europe and North America | Long term (≥ 4 years) |

| Complex supply chains and challenges sourcing specialty ingredients | -2.3% | Global, acute in regions dependent on imports | Short term (≤ 2 years) |

| High production costs associated with functional ingredient integration | -1.6% | Global, more pronounced in price-sensitive emerging markets | Medium term (2-4 years) |

| Limited consumer awareness in emerging markets about functional coffee benefits | -1.1% | Asia-Pacific emerging markets, Latin America, Middle East and Afica | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Frameworks on Health Claims and Functional Ingredients

The U.S. Food and Drug Administration (FDA) maintains strict oversight of caffeine through the Federal Food, Drug, and Cosmetic Act, designating it as a food additive with Generally Recognized as Safe (GRAS) status. For adults, the FDA has established a daily consumption limit of approximately 400 mg [2]Source: U.S. Food & Drug Administration, “Spilling the Beans: How Much Caffeine is Too Much?,” fda.gov. The regulatory body implements heightened monitoring and mandatory adverse event reporting protocols for energy-based products to ensure consumer safety. Companies developing functional coffee products must navigate a complex landscape of regulatory requirements, particularly regarding structure/function claims. These claims require robust scientific substantiation and must be carefully worded to avoid any implications of disease treatment, which would trigger more stringent drug regulations. The implementation of new caffeine limits in 2025 across the United States and European Union markets will necessitate significant adjustments to product formulations and increase compliance-related expenses for manufacturers. The European Food Safety Authority (EFSA) offers more flexibility in permissible health claims compared to the FDA's conservative approach to disease risk reduction claims, creating strategic opportunities for companies operating in multiple markets. For botanical ingredients, manufacturers must complete comprehensive safety evaluations and adhere to established food additive regulatory frameworks. The classification distinction between liquid dietary supplements and conventional beverages significantly impacts how companies approach their product labeling and develop their marketing strategies.

High Production Costs Associated with Functional Ingredient Integration

The integration of functional ingredients substantially increases production costs through specialized extraction methods, quality control processes, and premium raw material sourcing, which directly influences retail pricing strategies. While supercritical CO2 extraction equipment demands significant initial capital investment, it delivers long-term cost advantages through improved operational efficiency and elimination of solvents for high-value compounds. Keurig Dr Pepper experienced a decline in U.S. Coffee segment net sales during the first quarter, primarily due to volume and mix reductions resulting from pricing adjustments in response to elevated green coffee costs. The incorporation of probiotic strains necessitates specific handling and storage conditions, which adds to manufacturing complexity and operational expenses. Market research demonstrates that a majority of functional product consumers express willingness to pay premium prices for health benefits, though price sensitivity fluctuates considerably across geographical regions and demographic segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RTD Coffee Dominates Through Convenience Innovation

The ready-to-drink coffee segment demonstrates market dominance, capturing 68.35% of the market share in 2025. This segment is experiencing robust growth momentum, with projections indicating a CAGR of 12.18% through 2031. The expansion is primarily attributed to rapid urbanization patterns and evolving consumer preferences for beverages that offer both portability and functional benefits. RTD coffee products excel in delivering precise measurements of functional ingredients through advanced shelf-stable systems, effectively preserving bioactive compounds while eliminating the need for consumer expertise in preparation.

In the broader coffee market landscape, instant coffee maintains its significant position through efficient manufacturing processes and extended product longevity, particularly resonating in markets where price sensitivity influences purchasing decisions more than premium positioning. The ground and whole bean segments continue to attract dedicated coffee enthusiasts seeking personalized functional experiences. These segments have evolved as specialty roasters incorporate innovative elements, such as adaptogenic blends and superfood infusions, into conventional brewing methodologies, meeting the growing consumer demand for customizable coffee experiences.

By Functional Claims: Energy Focus Leads While Cognitive Enhancement Accelerates

The functional beverage market reflects a strong consumer preference for energy-focused formulations, which hold a significant 33.25% market share in 2025. These beverages combine traditional caffeine benefits with B-vitamins and natural stimulants, utilizing advanced sustained-release mechanisms to help consumers avoid energy crashes. The mental focus and cognitive enhancement segment is experiencing notable growth, with a 12.05% CAGR, driven by increasing consumer interest, as 66% of global consumers actively seek cognitive health products. This trend aligns with the broader nootropic market, which is expanding at a robust 17.5% CAGR.

The market is diversifying with specialized formulations catering to various consumer needs. Weight management products include scientifically-supported ingredients designed to boost metabolism and control appetite, while gut health beverages incorporate probiotics and prebiotic fibers to promote digestive wellness. The immunity segment has seen significant growth post-pandemic, with 44% of functional beverage consumers prioritizing immune support benefits. This has increased demand for products enriched with vitamin C, zinc, and botanical extracts.

By Distribution Channel: Off-Trade Dominance Challenged by On-Trade Innovation

Off-trade channels dominate with a 69.60% market share in 2025, driven by distribution through supermarkets, convenience stores, and online retail platforms. These channels provide consumers with easy access and competitive prices. Online retail shows significant growth in functional coffee sales through direct-to-consumer relationships, subscription models, and educational content that guides premium product purchases. Convenience stores benefit from impulse purchases and on-the-go consumption, while supermarkets and hypermarkets offer extensive shelf space for brand visibility and promotions.

On-trade venues are growing at a 12.20% CAGR as coffee shops incorporate functional beverages into their premium menus, creating experiential consumption opportunities at higher price points. The East Asian branded coffee shop market experienced significant expansion in outlet numbers during the past year, reaching a substantial number of stores. China represents a considerable portion of these outlets. The market continues to evolve with changing consumer preferences toward convenience, as a majority of consumers regularly utilize coffee shop delivery services. This behavioral shift presents opportunities for businesses to incorporate functional coffee products into their existing delivery infrastructure.

Geography Analysis

The North American market holds a commanding position with a 68.60% market share in 2025, establishing itself as the industry leader. This dominance is built on strong consumer trust in functional ingredients and a well-developed premium coffee culture. In the United States, specialty coffee has become a significant part of retail consumption. According to the National Coffee Association of the USA, 46% of American adults consumed specialty coffee in 2024 . Companies in the region benefit from supportive regulations that enable health claim validations, as seen in the United States, where Bulletproof successfully expanded from niche biohacker communities to mainstream consumers. The market's strength is further reinforced by the seamless business operations between Canada, the United States, and Mexico, supported by efficient supply chains and aligned consumer health preferences.

The Asia-Pacific market is experiencing remarkable growth at 13.08% CAGR, making it the fastest-growing region. Business opportunities are expanding rapidly in markets like India and Vietnam, where increasing consumer purchasing power directly correlates with higher coffee consumption. The market has shown particular adaptability in China, where traditional tea culture has influenced innovative coffee products. Indonesia's business landscape has evolved significantly, with coffee establishments becoming essential commercial and social centers. While companies face varying regulatory requirements across countries, these differences create opportunities for market-specific product innovations.

The European market continues to perform steadily, supported by well-structured functional food regulations and health-conscious consumers. Business potential remains largely untapped in South America and Middle East and Africa, where increasing urbanization and rising consumer income levels are creating new market opportunities. These regions demonstrate promising business prospects as consumer awareness grows alongside improving economic conditions.

Competitive Landscape

The functional coffee market landscape presents a balanced competitive environment where both established industry players and innovative newcomers find opportunities to build their presence. Through thoughtfully crafted functional formulations and strategic market positioning, companies continue to carve out their market segments. Industry leaders such as Nestlé, JDE Peet's, and Keurig Dr Pepper have built their success on well-established distribution channels and strong consumer trust. While these companies have successfully incorporated functional ingredients into their existing product lines, some face operational challenges. For instance, Keurig reported a 3.7% decrease in net sales during Q1 2025 in its U.S. Coffee segment, primarily due to increased green coffee costs.

In their pursuit of market growth, companies have embraced various technological solutions to enhance their competitive edge. The implementation of supercritical CO2 extraction enables precise recovery of bioactive compounds, while BKON's RAIN technology has transformed cold brew production methods. The industry has also witnessed innovations in fermentation techniques, enabling the production of beanless coffee alternatives. Companies have strengthened their market presence by developing direct relationships with consumers through subscription models and implementing educational marketing strategies that highlight their products' functional benefits to health-conscious customers. The market continues to offer growth potential in areas such as beauty and skin health formulations, personalized nutrition solutions, and expansion into emerging markets where consumer awareness remains developing. A notable example of industry innovation comes from Atomo Coffee, which secured USD 7.8 million in Series B funding to develop sustainable coffee alternatives that reduce carbon emissions by 83% while maintaining traditional coffee characteristics.

The industry operates within a complex regulatory framework overseen by the FDA and EFSA. These regulatory requirements create distinct business environments across different regions, with European manufacturers operating under more flexible health claim regulations compared to their U.S. counterparts, who face more stringent structure/function requirements. These regulatory differences continue to influence how companies develop products and position themselves across various geographical markets.

Functional Coffee Industry Leaders

Nestlé S.A.

Dutch Bros Inc.

Bulletproof 360 Inc.

Laird Superfood Inc.

Super Coffee

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: London Nootropics, known for its adaptogenic coffee blends, strategically allied with Hifas Da Terra to infuse their mushroom extracts into its offerings. This partnership melds functional wellness components, allowing consumers to seamlessly integrate the potential benefits of Hifas Da Terra's medicinal mushrooms into their everyday lives.

- October 2024: Laird Superfood partnered with Smirk’s Ltd, a prominent supplier of organic and natural ingredients, to co-create innovative, premium products tailored for health-conscious consumers. This collaboration underscores the commitment of both Laird Superfood and Smirk’s Ltd to their shared vision of offering nutritious and sustainably sourced ingredients.

- September 2024: Nespresso collaborated with HIVED to elevate its customer delivery experience. With this partnership, Nespresso assures its clientele of real-time order tracking, regular live updates, and the ability to chat directly with HIVED's customer service. Additionally, Nespresso highlights that all deliveries by HIVED are fully electric, including the crucial middle mile from the distribution center to the depot.

Global Functional Coffee Market Report Scope

Coffee, a popular brewed beverage, is derived from roasted coffee beans, which are the seeds of specific coffee species' berries. Functional coffee goes a step further, blending traditional coffee with additional ingredients like botanicals and proteins, offering consumers benefits beyond just caffeine.

The global functional coffee market is categorized by product type, distribution channel, and geography. Product types include whole bean, ground coffee, ready-to-drink (RTD) coffee, and other variations. Distribution channels are divided into on-trade and off-trade segments. The off-trade segment encompasses supermarkets/hypermarkets, convenience stores, online stores, and other channels. The report also provides a geographical analysis of the market, focusing on both developed and emerging regions, namely North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

Market sizing is presented in USD value terms for all segments mentioned above.

| Whole Bean |

| Ground Bean |

| Instant Coffee |

| Ready-to-Drink Coffee |

| Coffee Pods and Capsules |

| Energy Focus |

| Weight Management |

| Mental Focus/Cognitive |

| Gut Health |

| Immunity Boost |

| Beauty and Skin Health |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Whole Bean | |

| Ground Bean | ||

| Instant Coffee | ||

| Ready-to-Drink Coffee | ||

| Coffee Pods and Capsules | ||

| By Functional Claims | Energy Focus | |

| Weight Management | ||

| Mental Focus/Cognitive | ||

| Gut Health | ||

| Immunity Boost | ||

| Beauty and Skin Health | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will functional coffee sales be by 2031?

Global revenue is projected to climb to USD 8.48 billion by 2031, up from USD 4.98 billion in 2026.

Which product format is currently leading consumer purchases?

Ready-to-drink functional coffees hold 68.35% of 2025 sales thanks to portability and precise nutrient dosing.

What health benefits do nootropic coffee blends promise?

They typically combine caffeine with L-theanine, lion’s mane, or ginkgo to support sustained focus, memory, and reduced jitters.

Where is demand expanding fastest?

Asia-Pacific leads growth, advancing at a 13.08% CAGR to 2031 as coffee culture spreads beyond urban elites.

How are brands addressing sustainability concerns?

Initiatives include plastic-free pods, upcycling coffee-cherry by-products, and investing in green extraction methods that minimize solvent use.

Page last updated on: