Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 52.99 Billion |

| Market Size (2026) | USD 55.98 Billion |

| Market Size (2031) | USD 73.67 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Coffee Market Analysis by Mordor Intelligence

The European coffee market size is expected to grow from USD 52.99 billion in 2025 to USD 55.98 billion in 2026 and is forecast to reach USD 73.67 billion by 2031 at 5.65% CAGR over 2026-2031. Europe remains one of the world's largest coffee-consuming regions, supported by established cultural practices and a strong café culture across many countries. While traditional coffee products maintain market dominance through widespread availability and an established consumer base, the market is experiencing increased demand for specialty, organic, and sustainably sourced varieties. Product format innovations are expanding consumer options and attracting younger consumers. The market growth is further supported by premium coffee experiences in both retail and foodservice segments. Market development is also influenced by digital transformation, environmental consciousness, and increased investments from major coffee chains. The European coffee market continues to evolve as consumers demand higher quality, ethical sourcing, and customized coffee options, creating a competitive and diverse market environment.

Key Report Takeaways

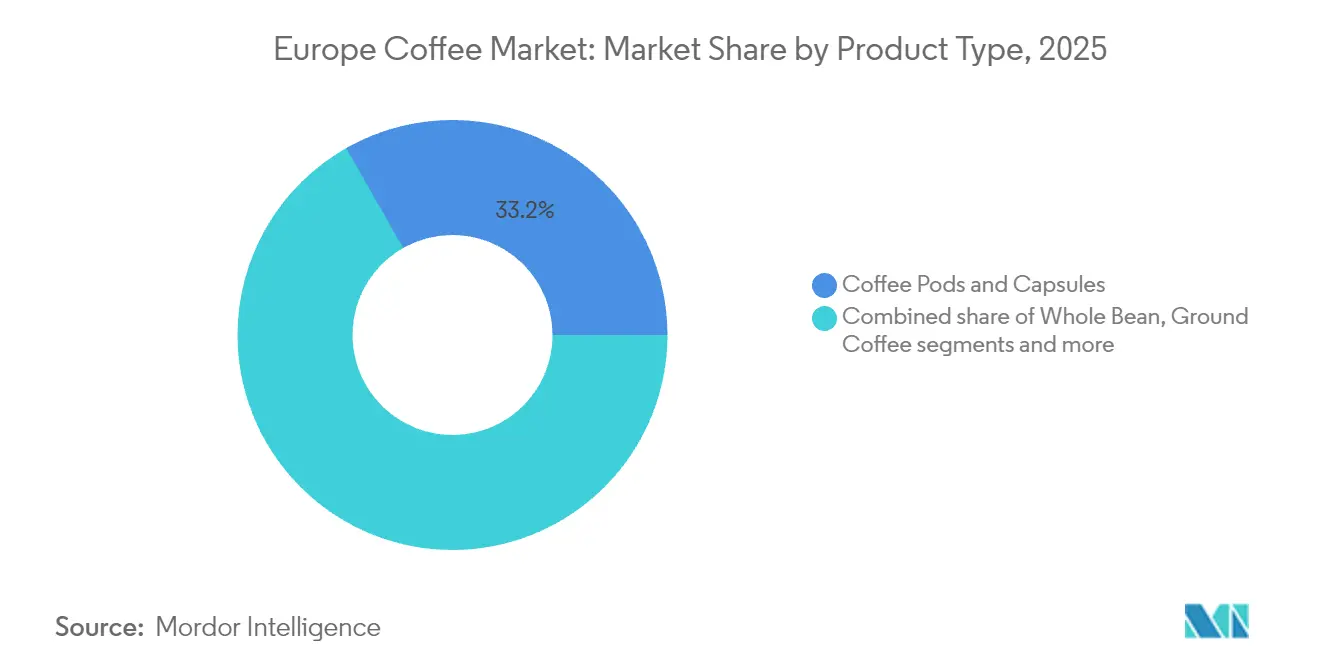

- By product type, pods and capsules captured 33.22% revenue share in 2025; whole-bean coffee is projected to advance at a 7.28% CAGR to 2031.

- By flavor, plain coffee commanded 81.72% of 2025 sales, whereas flavored variants are forecast to grow at a 7.64% CAGR through 2031.

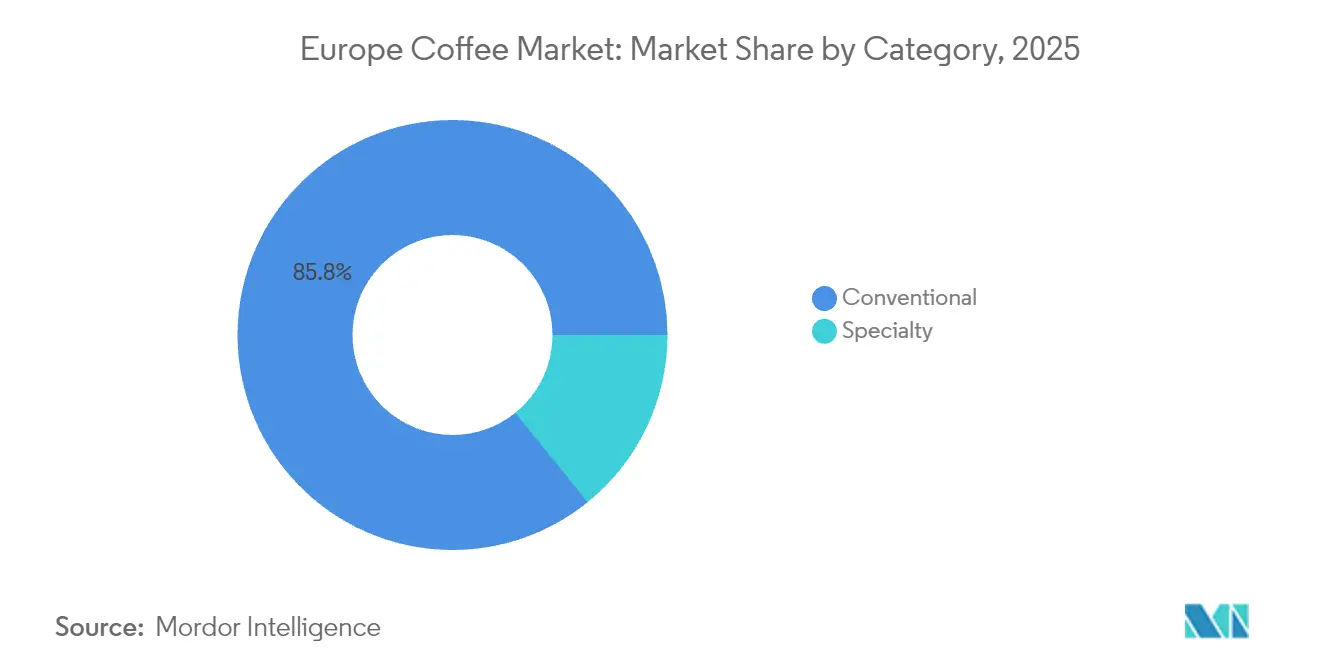

- By category type, conventional coffee accounted for 85.82% of the Europe coffee market size in 2025, whereas specialty coffee is rising at an 8.74% CAGR over the same horizon.

- By bean type, Arabica maintained 70.54% share of the Europe coffee market size in 2025; Robusta is expected to grow at a 5.98% CAGR between 2026 and 2031.

- By distribution channel, off-trade outlets controlled 80.34% of Europe coffee market share in 2025, while on-trade sales are set to accelerate at a 5.69% CAGR through 2031.

- By geography, Germany held 15.96% of Europe coffee market share in 2025 while expanding at a 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for specialty and premium coffee | +1.8% | Germany, United Kingdom, Scandinavia, Netherlands | Medium term (2-4 years) |

| Rising cafe culture and social coffee consumption | +1.2% | Urban centers across Western Europe | Short term (≤ 2 years) |

| Sustainability emerges as a key market driver | +1.0% | European Union-wide, strongest in Germany and the Netherlands | Long term (≥ 4 years) |

| Product innovation fuel market development | +0.9% | Technology hubs in Germany, the United Kingdom, and Italy | Medium term (2-4 years) |

| Health consciousness and awareness of coffee benefits | +0.7% | Northern Europe, urban demographics | Medium term (2-4 years) |

| Premiumization of whole bean and fresh coffee | +0.6% | Western Europe, affluent segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Specialty and Premium Coffee

The growing demand for specialty and premium coffee in Europe is driven by a sophisticated consumer base that increasingly prioritizes quality, unique flavor profiles, and ethical sourcing over mass-produced coffee products. European coffee drinkers demonstrate increased awareness of coffee origins, processing methods, and brewing techniques, which has enhanced the market for artisanal, single-origin, organic, and sustainable coffee varieties. The third-wave coffee movement, emphasizing craftsmanship, traceability, and product origin stories, reinforces this premium market segment. Consumers demonstrate a readiness to pay higher prices for coffee that delivers specific taste experiences while adhering to environmental and fair trade standards. In August 2024, John Farrer & Co of Kendal expanded its signature specialty coffee collection with three new products, focusing on small-batch, seasonal single-origin coffees from global sources. This product launch illustrates how established coffee roasters are adapting their offerings to address consumer preferences for distinctive, high-quality coffee products that highlight origin, seasonality, and production expertise.

Rising Cafe Culture and Social Coffee Consumption

The growing café culture and social coffee consumption in Europe are transforming the coffee market by focusing on experiences beyond the beverage. European consumers view coffee shops as social spaces for connecting, working, relaxing, and enjoying quality coffee. This shift is driven by demand for specialty coffees in appealing environments, often complemented by food options, events, and spaces suitable for socializing or remote work. The café experience represents lifestyle, community, and personal expression, drawing consumers seeking authentic experiences that combine traditional and modern elements. The expansion of independent cafés alongside established chains demonstrates consumer preference for distinctive, local coffee experiences. The Department for Environment, Food & Rural Affairs of the United Kingdom reported average out-of-home coffee consumption of 40 mL per person per week in 2023, highlighting the significance of social coffee drinking. This data indicates the recovery of on-trade coffee consumption as cafés strengthen their position as community spaces in modern consumer lifestyles.

Sustainability Emerges as Key Market Driver

The European coffee market is experiencing a fundamental transformation driven by sustainability imperatives, as both consumers and industry stakeholders prioritize environmental conservation, ethical sourcing protocols, and social responsibility measures. European coffee consumers demonstrate an increasing preference for products bearing certifications that validate sustainable agricultural practices, equitable labor conditions, and environmental preservation standards. Consumer purchasing patterns indicate a strong correlation with sustainability metrics, favoring organizations that demonstrate measurable commitments to biodiversity conservation, carbon footprint reduction, and agricultural community welfare. For instance, Tchibo's strategic initiative to implement 100% responsible coffee sourcing by 2027 illustrates the integration of sustainability frameworks into corporate strategies among European coffee enterprises to maintain market relevance and consumer loyalty.

Product Innovation Fuel Market Development

Product innovation drives the development of the European coffee market by enhancing consumer experiences and expanding product offerings. European consumers seek quality, unique flavor profiles, and technological advancements that improve brewing convenience, customization, and sustainability. The innovation encompasses new brewing equipment, novel coffee blends, functional coffee beverages, and environmentally friendly packaging. These developments address the needs of sophisticated consumers who value both traditional and modern coffee experiences. Companies maintain competitiveness through research and development, responding to health and lifestyle trends while delivering personalized coffee experiences for different customer segments. For instance, in June 2024, Costa Coffee demonstrated this commitment by opening an Innovation and Development Centre in Loudwater, United Kingdom. This facility enables their Innovation and Research and Development teams to test and develop advanced equipment, supporting Costa Coffee Professional's strategy to expand its coffee solutions portfolio and align with future consumer needs and industry developments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and supply chain disruptions | -1.5% | European Union-wide, particularly import-dependent markets | Short term (≤ 2 years) |

| Competition from alternative beverages | -0.8% | Northern Europe, health-conscious demographics | Medium term (2-4 years) |

| Climate change impact on coffee production | -0.6% | Global supply chains affecting European Union imports | Long term (≥ 4 years) |

| High operational and raw material costs | -0.4% | European Union-wide, particularly affecting small operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Volatility and Supply Chain Disruptions

The European coffee market faces significant constraints due to price volatility and supply chain disruptions, which create uncertainty throughout the value chain. Multiple factors influence coffee prices, including climate variability, extreme weather events, geopolitical tensions, and labor shortages in major producing countries. These challenges reduce crop yields and quality while constricting supply volumes and increasing production and logistics costs. The resulting price inflation directly affects retail coffee prices in Europe, impacting consumer purchasing behavior and consumption patterns. The highly globalized coffee supply chain remains susceptible to transportation delays, increasing freight costs, and regulatory changes, which add further cost pressures and complicate market operations. In Germany, one of Europe's largest coffee-consuming countries, the Federal Statistical Office reported a 12.2% year-over-year increase in consumer prices for ground coffee in April 2025 [1]Source: Federal Statistical Office, "Bean coffee in April 2025 12.2% more expensive than a year earlier", destatis.de. This price surge demonstrates how inflationary pressures can influence consumer behavior, potentially driving shifts toward more affordable alternatives such as instant coffee or blends with higher robusta content.

Competition from Alternative Beverages

The European coffee market experiences significant competitive pressure from the proliferation of alternative beverages, which redirect consumer expenditure from conventional coffee products. European consumers, particularly within younger demographic segments, demonstrate increasing preferences for diverse beverage categories, including traditional tea, energy-based beverages, functional and botanical formulations, plant-derived lattes, and non-caffeinated wellness-oriented options such as matcha, kombucha, and herbal preparations. These alternative beverages attract health-conscious consumers through their distinct flavor profiles, reduced caffeine content, and nutritional advantages, including antioxidant properties, vitamin content, and probiotic benefits. The diversification of beverage options necessitates coffee manufacturers to implement strategic innovations across product development, marketing initiatives, and consumer engagement protocols to maintain consumer retention and expand market presence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pods Drive Convenience Revolution

Coffee pods and capsules constituted 33.22% of the market share in 2025, demonstrating European consumers' pronounced strategic orientation toward systematized home brewing methodologies. The segment's substantial market presence is fundamentally attributed to its operational sophistication, standardized preparation protocols, and quantifiable beverage quality parameters. The systematic implementation of single-serve coffee machines, in conjunction with technological advancements in capsule manufacturing specifications and comprehensive flavor taxonomies, continues to facilitate this segment's methodical market progression.

The whole bean coffee segment is projected to grow at a CAGR of 7.28% through 2031, driven by consumers who prioritize freshness, quality, and customized brewing options. This growth reflects an increasing preference for premium coffee experiences, with consumers seeking authentic flavors and aromas that whole beans preserve better than pre-ground alternatives. Supporting this trend, the United States Department of Agriculture (USDA) reports that the European Union dominated domestic consumption of green coffee beans in the 2024/2025 marketing year, utilizing over 42.0 million 60-kilogram bags. This high consumption level indicates a growing preference among European consumers for freshly roasted coffee and home roasting, which enables greater control over their coffee preparation.

By Flavor: Plain Dominates Despite Flavored Growth

Plain coffee maintains a commanding market position with an 81.72% share in 2025, demonstrating the predominant preference among European consumers for traditional coffee consumption. Market analysis indicates a significant consumer orientation toward authentic characteristics derived from coffee origin, bean varieties, and precise roasting profiles rather than flavored alternatives. This substantial market concentration in plain coffee consumption illustrates the European market's refined appreciation for premium quality and distinctive taste characteristics inherent in regional coffee varieties and specialized roasting methodologies, aligning with the continent's established coffee heritage.

The flavored coffee is growing at a CAGR of 7.64%, driven by younger consumers seeking diverse and seasonal varieties beyond traditional coffee options. This market segment attracts consumers looking for enhanced taste experiences and customized selections that align with modern lifestyle preferences. Product innovations featuring natural flavorings without added sugar address health-conscious consumer demands while meeting the need for premium offerings. For instance, in 2024, Nestlé S.A. expanded its Nescafé Classic range in Central and Eastern Europe by introducing caramel and hazelnut flavors, both containing natural flavorings without added sugar.

By Category Type: Specialty Gains Despite Conventional Dominance

In 2025, conventional coffee constituted 85.82% of the European market share, establishing its predominant position among consumers. This market dominance is attributed to the region's deep-rooted cultural affinity for traditional coffee varieties, as consumers prioritize established flavor profiles and product consistency. The comprehensive distribution network of conventional coffee through on-trade and off-trade channels ensures sustained market penetration. The strategic combination of competitive price points and established brand recognition maintains conventional coffee's status as the primary choice for daily consumption.

The specialty coffee segment in Europe is experiencing significant growth, with a CAGR of 8.74%, exceeding the overall market growth rate by nearly twofold. European consumers are increasingly prioritizing premium quality, sustainability, and ethical sourcing in their coffee choices. The appeal of specialty coffees stems from their distinct flavor profiles, artisanal production methods, and transparent supply chains. Certifications such as Fairtrade, Organic, and Rainforest Alliance have evolved from market differentiators to essential requirements. The European Union's position as a major organic product importer is evidenced by its 2.7 million metric tonnes of organic imports in 2023, as reported by the Centre for the Promotion of Imports (CBI) . This import volume demonstrates the strong consumer preference for products that support sustainable agriculture and ethical sourcing practices.

By Bean Type: Arabica Dominates While Robusta Gains

Arabica beans constitute 70.54% of the market share in 2025, demonstrating comprehensive empirical validation of European consumers' established predilection for their multifaceted organoleptic profiles and distinguished aromatic characteristics. The quantifiable superior acidity parameters and refined gustatory attributes of Arabica coffee demonstrate precise statistical correlation with Europe's sophisticated coffee consumption methodologies. The region's institutionalized adherence to standardized quality parameters and origin-specific characteristics establishes Arabica as the preeminent selection for specialized coffee production and premium blend formulation protocols.

Robusta beans demonstrate a growth trajectory at a CAGR of 5.98%, attributed to implemented climate adaptation protocols and enhanced flavor optimization methodologies. Despite historical market limitations in Europe due to its pronounced taste profile and elevated caffeine concentration, Robusta has experienced significant advancement through refined processing protocols and systematic blending procedures that optimize its flavor characteristics. The variety's inherent resistance to agricultural pests and environmental adaptability positions it as a strategic component in maintaining supply chain continuity amid climate-related challenges.

By Distribution Channel: Off-Trade Leads While On-Trade Recovers

Off-trade channels held a market share of 80.34% in 2025, demonstrating European consumers' preference for consuming coffee at home. This dominance stems from the convenience offered through retail outlets such as supermarkets, hypermarkets, and online platforms. The off-trade segment's strength reflects consumer trends toward home consumption, with individuals seeking to create café-quality experiences domestically. These channels provide consumers access to a wide range of coffee products across different brands, formats, and price points. The growth of e-commerce and online grocery shopping has further strengthened the off-trade segment by simplifying the coffee purchasing process for consumers.

The European on-trade coffee market demonstrates a compound annual growth rate (CAGR) of 5.69%, primarily attributed to the region's well-established café culture, wherein coffee consumption functions as both a utilitarian and social activity. Market expansion is facilitated by ongoing urbanization and heightened consumer demand for premium coffee experiences, encompassing superior beverage quality and refined café environments. The European Labour Authority reports that the hospitality sector, inclusive of coffee establishments, constituted 4.7% of total employment in 2023 . This statistical evidence substantiates the market's substantial economic impact and its fundamental role in facilitating community engagement throughout Europe.

Geography Analysis

Germany holds Europe's largest coffee market share at 15.96% in 2025 and demonstrates the region's highest growth rate at 6.61% CAGR through 2031. The market combines established consumption patterns with increasing demand for specialty and sustainable products, creating diverse opportunities across segments. Germany's dual position as the largest importer and fastest-growing market highlights its effective market development approach that integrates traditional preferences with modern trends.

Italy maintains its position as Europe's second-largest coffee market, supported by its established espresso culture and extensive domestic roasting industry. While the specialty coffee segment remains limited, it shows growth potential, particularly among younger consumers seeking alternatives to traditional espresso, presenting opportunities for innovative products that align with Italian coffee traditions.

France demonstrates significant market potential, with green coffee imports reaching 226 thousand tonnes in 2023. The United Kingdom shows notable market evolution, while Spain's market concentrates on commercial coffee with expanding specialty segments. The Netherlands functions as a key trading center with substantial re-export operations that impact European market flows. Belgium's strategic position as a major importer and re-exporter benefits companies seeking European market entry. Poland and Sweden present growth opportunities driven by evolving consumer preferences and economic growth.

Competitive Landscape

The European coffee market maintains moderate concentration, with multinational companies competing alongside specialty roasters and direct-trade specialists. Market leaders such as Nestlé SA, Luigi Lavazza SpA, Starbucks Corporation, and Strauss Group utilize extensive distribution networks and established brand recognition. These companies face increasing competition from sustainability-focused businesses that prioritize traceability and ethical sourcing.

Industry consolidation continues through strategic acquisitions, as demonstrated by Lofbergs' acquisition of Danish roaster Peter Larsen Kaffe in February 2025. Companies are investing in technology as a competitive advantage, implementing blockchain traceability systems, sustainable packaging solutions, and digital customer engagement platforms to meet regulatory requirements and strengthen market positions.

Market opportunities remain in sustainable single-serve products, direct-trade platforms, and regional specialty coffee segments, where consumers demonstrate willingness to pay premium prices. New market entrants, particularly technology companies developing compostable pods and digital platforms connecting consumers directly with coffee farmers, are challenging traditional European coffee market distribution models.

Europe Coffee Industry Leaders

-

Nestlé SA

-

Luigi Lavazza SpA

-

Starbucks Corporation

-

Strauss Group

-

Melitta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JDE Peet's launched two new sachet products under its Kenco brand, targeting younger coffee consumers. The product line includes Whipped Americano Frappe and Creamy Latte flavors, which can be served hot or iced.

- April 2025: Nestlé introduced the Nescafé Espresso Concentrated product line in Europe. The range offers three flavors - vanilla, caramel, and classic, with each bottle providing 16 servings.

- April 2025: Lavazza launched Tabli, a 100% coffee capsule system that eliminates traditional capsule packaging, providing a waste-free coffee solution.

- May 2024: Fresh Black established a distribution hub in Poland to facilitate shipping across European markets. The company launched a European Union website featuring its 200g packaged specialty coffee products, whole bean blends, and drip coffee bags.

Europe Coffee Market Report Scope

Coffee is a brewed drink prepared from roasted coffee beans, the seeds of berries from certain coffee species.

The European coffee market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into whole bean, ground coffee, instant coffee, and coffee pods and capsules. By distribution channel, the market is segmented into on-trade and off-trade distribution channels. The off-trade channel is further segmented into convenience stores, specialist retailers, supermarkets/hypermarkets, and other distribution channels. By geography, the market studied is segmented into France, Germany, the United Kingdom, Spain, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

By Product Type

| Whole Bean |

| Ground Coffee |

| Instant Coffee |

| Coffee Pods and Capsules |

| Ready-to-Drink (RTD) Coffee |

By Flavor

| Plain |

| Flavored |

By Category

| Conventional |

| Speciality (Organic/Single-Origin) |

By Bean Type

| Arabica |

| Robusta |

| Others |

By Distribution Channel

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Whole Bean | |

| Ground Coffee | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| Ready-to-Drink (RTD) Coffee | ||

| By Flavor | Plain | |

| Flavored | ||

| By Category | Conventional | |

| Speciality (Organic/Single-Origin) | ||

| By Bean Type | Arabica | |

| Robusta | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe coffee market?

The Europe coffee market is worth USD 55.98 billion in 2026.

How fast will the market expand over the next five years?

Forecasts show a 5.65% CAGR, lifting revenue to USD 73.67 billion by 2031.

Which product segment leads regional sales?

Pods and capsules hold 33.22% of revenue and continue to benefit from convenience demand.

Why is Germany pivotal for suppliers?

Germany combines 15.96% market share with the region’s fastest 6.61% CAGR, making it both the largest and quickest-growing national market.

Page last updated on: