Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 23.76 Billion |

| Market Size (2026) | USD 24.98 Billion |

| Market Size (2031) | USD 31.05 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Coffee Market Analysis by Mordor Intelligence

The US coffee market size is expected to grow from USD 23.76 billion in 2025 to USD 24.98 billion in 2026 and reach USD 31.05 billion by 2031, growing at a 4.45% CAGR. This growth is anchored in premiumization, third-wave adoption, and resilient household demand even as arabica prices spike because of climate-related supply shocks in Brazil and Vietnam. Brands that communicate origin, processing method, and sustainability credentials continue to trade consumers up from commodity drip to margin-rich specialty offerings, protecting profits while raw-bean costs surge. Competitive dynamics remain moderately consolidated, yet direct-to-consumer (DTC) startups fragment the specialty tier, forcing incumbents to innovate in formats, flavors, and packaging to defend shelf space. Retail e-commerce subscriptions are normalizing post-pandemic but still outpace physical-store growth, while on-trade venues such as coffee houses and quick-service restaurants are recovering traffic as hybrid work settles into a steady rhythm.

Key Report Takeaways

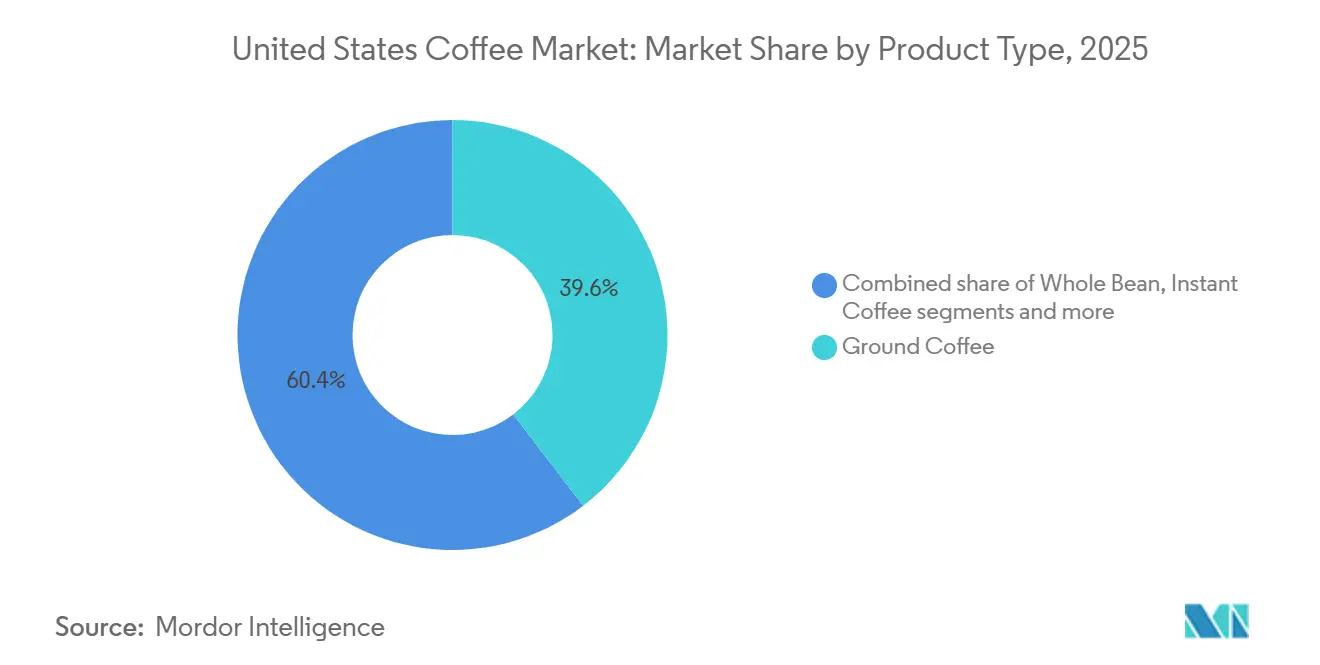

- By product type, ground coffee led with 39.60% of the US coffee market share in 2025, while pods and capsules are forecast to expand at a 5.93% CAGR from 2026 to 2031.

- By type, conventional coffee held a 53.95% share of the US coffee market size in 2025; specialty coffee is advancing at a 7.03% CAGR through 2031.

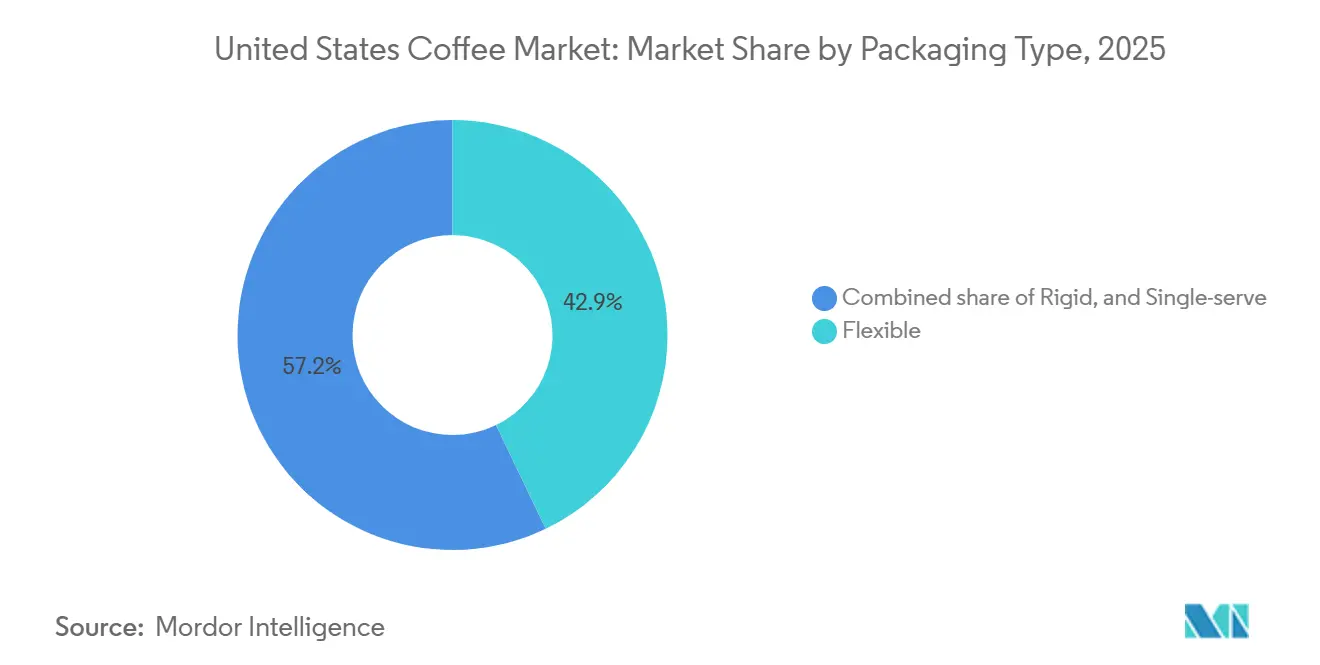

- By packaging, flexible formats captured a 42.85% share in 2025; single-serve packaging is projected to grow fastest at a 6.36% CAGR to 2031.

- By distribution channel, off-trade accounted for 87.25% of sales in 2025 and should rise at a 5.22% CAGR, while on-trade venues regain share as urban footfall rebounds.

- By geography, California contributed 24.17% of 2025 revenue, but Florida is poised for the quickest lift with a 6.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Coffee Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and third-wave adoption | +0.8% | National; highest in West Coast and Northeast metros | Medium term (2–4 years) |

| Growing demand for functional blends | +0.6% | California, Texas, Florida; strongest among Gen Z and millennials | Long term (≥ 4 years) |

| Urbanization reviving on-trade traffic | +0.4% | Metropolitan Statistical Areas > 1 million; Sun Belt cores such as Phoenix and Austin | Short term (≤ 2 years) |

| State compostable-packaging mandates | +0.3% | California, New York, Washington, Oregon | Medium term (2–4 years) |

| Home-barista equipment uptake | +0.5% | Households earning > USD 75,000; concentrated in West and Northeast | Medium term (2–4 years) |

| Expansion of coffee-house footprints | +0.4% | Highest density in California, Texas, New York; rising in second-tier cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization and third-wave adoption among consumers

Third-wave coffee has transitioned from niche to mainstream, with 45% of Americans consuming specialty coffee on any given day in 2024, up from 25% a decade earlier, according to the National Coffee Association (NCA)[1]Source: National Coffee Association, "National Coffee Data Trends: Specialty Coffee Breakout Report 2024", ncausa.org. This shift is most pronounced among 25-to-39-year-olds, 64% of whom drank specialty coffee in the past week in 2025, a cohort that values transparency around origin, processing method, and roaster relationships with farmers. The willingness to pay extra for a single-origin pour-over or a nitro cold brew creates a margin buffer that insulates roasters from commodity-price volatility, specialty brands absorbed the increase without losing customers because the value proposition rests on craft and story rather than price per ounce. West Coast markets lead adoption, with 58% of consumers in the region purchasing specialty coffee, but the trend is diffusing eastward as independent roasters open tasting rooms and subscription services deliver freshly roasted beans direct to doorsteps. This premiumization dynamic explains why the specialty segment will grow annually through 2031.

Growing demand for functional and specialty coffee range

In 2024, searches for mushroom coffee on Ocado's platform skyrocketed, reflecting a surge of interest in the United States for blends that merge caffeine with adaptogens. This trend highlights a growing consumer shift toward functional beverages that cater to both wellness and lifestyle needs. Brands like MUD/WTR are blending cacao, lion's mane, and chaga, aligning with Gen Z's wellness aspirations for focused energy without the jitters. These products appeal to health-conscious consumers seeking alternatives to traditional high-caffeine beverages. While the Food and Drug Administration (FDA) guidelines set a daily caffeine cap of 400 mg for adults, this opens avenues for lower-caffeine products that emphasize nootropic and anti-inflammatory advantages, offering a balance between functionality and safety. This evolution compels conventional roasters to delve deeper into ingredient science and navigate regulatory validations to remain competitive. The convergence of coffee and wellness trends is driving innovation, pushing brands to adapt and meet the growing demand for functional, health-oriented beverages.

Urbanization and a fast-paced lifestyle drive demand in on-trade distribution

On-trade channels such as coffee houses, quick-service restaurants, and workplace cafeterias are reclaiming share after pandemic-era declines as hybrid work stabilizes and urbanization accelerates in Sun Belt metros. Starbucks plans to reach 55,000 stores globally by 2030, up from 40,576 currently, with a stated goal to double its United States footprint from approximately 17,000 locations. The National Coffee Association found that drip coffee makers remain the most popular brewing method, yet single-cup machines have surged over five years, reflecting a preference for convenience and portion control that on-trade venues replicate with mobile ordering and loyalty apps. Urbanization also concentrates demand in walkable neighborhoods where coffee houses serve as third spaces for remote workers and social gatherings, a dynamic that explains why metropolitan statistical areas with populations exceeding 1 million account for a disproportionate share of on-trade growth. The challenge for chains is maintaining traffic when comparable-store sales decline by differentiating through exclusive blends, seasonal offerings, and experiential retail that justifies premium pricing.

Growth in the coffee house stores fueling market demand

As coffee chains proliferate across the United States, they're not just boosting consumption but also familiarizing a broader audience with specialty coffee. Starbucks, for instance, upped its United States company-owned store count from 8,941 in 2020 to 10,158 in 2024[2]Source: Starbucks, "Starbucks Corporation Annual Report 2024", starbucks.com. This expansion has not only widened the geographic reach of specialty coffee but also introduced it to diverse consumer segments, enhancing both accessibility and awareness. The allure of the market remains strong, with Luckin Coffee eyeing a 2025 debut in the United States starting in New York City. Known for its app-centric ordering and competitive pricing, Luckin's arrival is poised to intensify competition and spur tech-driven service innovations. In urban settings, coffee isn't just a beverage; it's woven into the fabric of daily life. Coffee shops, now staples of urban neighborhoods, draw significant foot traffic and enjoy robust financial health, thanks to loyal patrons and a varied drink menu. This vibrant scene has fueled steady growth in cafe and bar sales, underscoring the strong demand for coffee-centric experiences.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-induced yield volatility | -0.6% | Brazil, Vietnam, Colombia supply 57% of United States imports | Long term (≥ 4 years) |

| Environmental burden of single-serve pods | -0.3% | Regulatory pressure strongest in California, New York, Washington, Oregon | Medium term (2–4 years) |

| Rising awareness of caffeine health effects | -0.3% | Gen Z and wellness-focused millennials nationwide | Medium term (2–4 years) |

| Competition from alternative beverages | -0.3% | Urban cores with high social-media influence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-induced yield volatility raising costs

Severe weather events in key coffee-growing regions have disrupted production, leading to fluctuations in United States market prices. According to Food and Agriculture Organization (FAO) data, these weather-related supply disruptions were responsible for 40% of price hikes in 2024. In Vietnam, coffee production plummeted by 20% in 2023/24 due to extended dry spells, resulting in a 10% drop in exports for the second consecutive year. Indonesia witnessed a 16.5% year-on-year decline in production, as rains in April-May 2023 damaged coffee cherries, leading to a 23% cut in exports. Brazil's production forecast for 2023/24 was revised from an anticipated 5.5% increase to a 1.6% decline, primarily due to drought conditions in pivotal states like Minas Gerais and São Paulo[3]Source: Food and Agriculture Organization, "Adverse ClimatiC conditions Drive Coffee Prices to Highest Level In Years", fao.org. These supply challenges have driven up retail coffee prices. Furthermore, climate models indicate a shrinking suitable land for coffee cultivation, perpetuating price pressures and constraining growth in markets sensitive to price changes.

Detrimental impact of coffee pods and capsules on the environment

Single-serve pods generate billions of units of landfill waste annually in the United States, a figure that has drawn regulatory scrutiny and consumer backlash despite the format's convenience and portion control. The United States Securities and Exchange Commission fined Keurig USD 1.5 million in September 2024 for misleading recyclability claims, a precedent that signals regulators will enforce truth-in-advertising standards for environmental assertions (SEC). California's AB 1201 requires that compostable products achieve a 75% collection-and-acceptance rate by January 2026, a threshold that most bioplastic pods fail because municipal systems lack the industrial composting capacity to process them at scale (CalRecycle). The restraint manifests as brand risk: consumers who prioritize sustainability may switch to whole-bean or ground formats, and as compliance cost, since redesigning pods with compostable materials and building reverse-logistics networks requires capital that smaller roasters cannot afford.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Household Penetration Keeps Ground Coffee on Top

In 2025, the US coffee market saw ground coffee commanding a 39.60% share. While price-sensitive households continue to buy bulk canisters, maintaining a steady volume, premium niches are also flourishing due to increasing consumer interest in high-quality and specialty coffee products. Yet, the ascent of single-cup machines and the burgeoning home-barista trend are nibbling away at this share, as consumers seek convenience and the ability to replicate café-style beverages at home.

The pods and capsules will see a 5.93% CAGR growth through 2031, driven by convenience seekers poised to switch formats once compostable solutions achieve scale. Whole-bean coffee benefits from a craft preparation image and a fresher aroma, while instant coffee's growth is fueled by premium sticks marketed for travel and outdoor enthusiasts. To counter direct-to-consumer (DTC) roasters, mass-market incumbents are integrating subscription models with loyalty apps. Their value proposition now combines freshness guarantees, carbon-neutral shipping, and storytelling about coffee origins, bridging the experiential divide with boutique brands.

By Type: Specialty Outpaces Conventional

In 2025, conventional coffee commanded a dominant 53.95% share of the US coffee market, bolstered by extensive grocery distribution and strategic price promotions. During the commodity price spikes of 2024-25, some consumers opted for conventional coffee, underscoring its resilience amid inflationary pressures.

Meanwhile, the specialty coffee segment is set to grow at a robust 7.03% rate through 2031, outpacing the broader US coffee market. This growth is driven by younger consumers who increasingly view coffee as an artisanal experience rather than just a caffeine fix, valuing unique flavors, premium quality, and ethical sourcing. Specialty coffee's footprint is expanding beyond major cities, with secondary metros embracing micro-roasters and barista training labs. These developments are fostering a culture of coffee craftsmanship and education in previously untapped regions. In response, corporate giants are unveiling reserve collections to capitalize on this trend.

By Packaging Type: Flexible Formats Dominate While Single-Serve Accelerates

In 2025, flexible pouches accounted for 42.85% of sales, striking a balance between freshness, shelf efficiency, and reduced material weight. These pouches are increasingly favored for their lightweight nature, which reduces transportation costs and environmental impact. Stand-up bags equipped with one-way valves cater to users who prefer multi-week stock without the risk of staling, ensuring product quality over extended periods.

As compostable innovations align with state mandates, the US coffee market for single-serve packaging is projected to grow at a 6.36% CAGR through 2031, driven by increasing consumer demand for sustainable and convenient solutions. While rigid metal and glass canisters remain popular in the instant and gift segments, they grapple with elevated freight emissions and energy-intensive recycling processes, which pose challenges in meeting sustainability goals. Although Nespresso touts a 35% recycling capture for its aluminum capsules, the limited acceptance at the municipal level curtails its overall impact, highlighting the need for broader recycling infrastructure.

By Distribution Channel: Off-trade Dominance Reflects Shifting Consumption Patterns

In 2025, off-trade distribution claimed 87.25% of the US coffee market, led by supermarkets, hypermarkets, convenience stores, and online retailers. These channels leverage a wide selection and promotional pricing to boost sales volume. The dominance of off-trade channels stems from structural advantages: grocery shopping is a weekly ritual, and coffee is a pantry essential. Consumers are increasingly turning to online platforms for subscription convenience and curated product discovery.

Off-trade distribution is projected to grow at an annual rate of 5.22% through 2031. This growth rate indicates saturation in established grocery channels and a pivot towards e-commerce. Conversely, on-trade venues, including coffee houses and quick-service restaurants, are regaining market share. This resurgence is attributed to the normalization of hybrid work and urbanization, which concentrates demand in walkable neighborhoods. As private-label brands enhance their quality and sustainability credentials, national roasters are compelled to invest in brand storytelling, limited-edition releases, and direct-to-consumer channels.

Geography Analysis

In 2025, California accounted for 24.17% of the US coffee market's revenue. This dominance is attributed to the state's 39 million residents, affluent demographics, and a plethora of third-wave roasters, especially in urban hubs like San Francisco and Los Angeles. Moreover, California's legislative moves on compostable packaging frequently set national benchmarks, nudging suppliers to realign their product offerings. The state's focus on sustainability and innovation in packaging has also encouraged the adoption of environmentally friendly practices across the supply chain. Yet, challenges loom: the state's steep operating costs and a trend of net outmigration could hinder sustained volume growth. Businesses operating in California must navigate these hurdles while leveraging the state's strong consumer base and trendsetting influence.

Florida is emerging as a coffee market hotspot, boasting a projected CAGR of 6.19% through 2031. This surge is spurred by a 2024 influx of 350,000 net domestic migrants and a climate that amplifies the demand for cold brews. Young professionals migrating from the Northeast and Midwest, with their penchant for specialty coffee, are driving up per-capita spending. The state's growing population and diverse cultural influences are fostering innovation in coffee offerings, with drive-through coffee chains and canned coffee enjoying consistent demand. Miami's café scene, in particular, is seamlessly blending Latin flavors like café con leche and cortadito into its mainstream offerings, reflecting the region's rich cultural heritage. Florida's coffee market is also benefiting from increased investments in retail infrastructure and marketing campaigns targeting younger demographics.

Texas, home to 30 million residents, stands third in coffee market value, with Dallas, Houston, and Austin leading the charge. Here, tech hiring and suburban expansion fuel a growing appetite for grab-and-go coffee. Dutch Bros' foray into secondary cities like Lubbock and Waco highlights the untapped potential in less saturated areas. The state's robust economic growth and diverse population create opportunities for both premium and value-oriented coffee brands. While New York remains a top-three revenue contender, its growth is plateauing, hampered by market saturation and a dip in Manhattan's foot traffic due to remote work trends. However, the state's established coffee culture and high per-capita spending continue to make it a critical market. States like Pennsylvania, Illinois, and others across theUnited States are riding a stable wave, buoyed by rising incomes in the Mountain West and Southeast regions, which are now warming up to premium coffee. These regions, previously under-indexed in the premium segment, are witnessing increased consumer interest, driven by urbanization and changing lifestyle preferences.

Competitive Landscape

The US coffee market is moderately concentrated. While giants like Starbucks, Keurig Dr Pepper, and Nestlé dominate both retail and on-trade sectors, a multitude of regional roasters carve out the specialty niche. Keurig Dr Pepper's USD 18 billion acquisition of JDE Peet’s, announced in August 2025, is set to forge a dedicated coffee powerhouse, poised to negotiate bean contracts on a grand scale and invest heavily in sustainable packaging. This acquisition is expected to reshape the competitive landscape by enabling economies of scale and fostering innovation in product offerings. Despite operating 16,466 stores across the United States, Starbucks reported a 6% dip in same-store sales for Q4 FY 2024, underscoring the traffic challenges even industry leaders face. This decline highlights the growing need for established players to adapt to shifting consumer preferences and intensifying competition.

Technology is reshaping competitive advantages. Blockchain initiatives trace coffee beans from their origin to the cup, enhancing transparency and trust in the supply chain; AI systems offer tailored roast suggestions, improving customer engagement and satisfaction; and drone data enhances agricultural inputs, optimizing yields and reducing waste. Nespresso’s aluminum capsule recycling initiative showcases the potential of reverse logistics as a brand differentiator, though gaps in municipal participation hinder widespread recovery. This highlights the importance of collaboration between private companies and public systems to achieve sustainability goals. Emerging brands like MUD/WTR and RISE Brewing are rebranding coffee as a wellness choice, appealing to younger demographics and encroaching on the energy drink market. These brands emphasize functional benefits, such as improved focus and reduced caffeine jitters, to differentiate themselves. However, they face challenges in scaling up: costs for green-bean procurement, freight, and compliance surge significantly beyond micro-roasting volumes, creating barriers to broader market penetration.

As conglomerates chase margin-boosting niches, continued merger and acquisition activity looms on the horizon, underscoring the industry's push for diversification and fortified market positions. Larger players are expected to target specialty brands and innovative startups to expand their portfolios and capture emerging trends. Concurrently, specialty roasters are likely to merge, leveraging shared roasting facilities and unified e-commerce platforms to enhance procurement efficiency and cut operational expenses. This consolidation could enable smaller players to compete more effectively with larger corporations. The competitive spotlight will shine on sustainable packaging and product enhancements, driven by heightened consumer awareness and evolving regulatory scrutiny, fueling both innovation and compliance in the market. Companies that successfully align with these trends are likely to gain a competitive edge, as sustainability and functionality become key differentiators in the evolving global coffee market.

US Coffee Industry Leaders

-

Starbucks Corporation

-

The J.M. Smucker Company

-

Nestlé SA

-

Keurig Dr Pepper Inc.

-

Luigi Lavazza S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Starbucks, through its joint venture with PepsiCo under the North American Coffee Partnership (NACP), introduced Starbucks Coffee & Protein, a new ready-to-drink (RTD) beverage line. The coffee is available in classic caffè and caffè mocha flavors, aimed at health-conscious, active consumers seeking functional nutrition as part of their morning routines.

- August 2025: Keurig Dr Pepper announced a significant USD 18 billion acquisition of JDE Peet’s, accompanied by plans to separate into two independent entities: one dedicated to refreshment beverages and the other focused on becoming a global coffee leader. The initiative is described as transformative, altering the competitive dynamics in both the beverage and coffee markets while positioning each entity for sustained growth.

- April 2025: Dutch Bros teamed up with Trilliant Food & Nutrition, LLC. Under this licensing agreement, Dutch Bros is debuting its inaugural line of branded ground coffees and K-Cup packages. This partnership enables Dutch Bros to bring its products to United States retail shelves for the first time, expanding its presence beyond its traditional service locations.

US Coffee Market Report Scope

Coffee is a brewed beverage made from roasted coffee beans, which are the seeds of berries from plants belonging to the Coffea genus. The US coffee market is categorized by product type, type, packaging format, distribution channel, and geography. By product type, the market is segmented by whole bean, ground coffee, instant coffee, and coffee pods and capsules. By type, the market is segmented by conventional and specialty coffee. By packaging format, the market is segmented by flexible, rigid, and single-serve. By distribution channel, the market is segmented by on-trade and off-trade, including supermarkets/hypermarkets, convenience/grocery stores, online retail, and other off-trade channels. By Geography, the market is studied across California, Texas, Florida, New York, Pennsylvania, Illinois, and the rest of the United States. Market sizing is presented in both value terms (USD) and volume (tons) across all the above segments.

By Product Type

| Whole Bean |

| Ground Coffee |

| Instant Coffee |

| Coffee Pods and Capsules |

By Type

| Conventional Coffee |

| Specialty Coffee |

By Packaging Type

| Flexible |

| Rigid |

| Single-Serve |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other off-trade Channels |

By Geography

| California |

| Texas |

| Florida |

| New York |

| Pennsylvania |

| Illinois |

| Rest of the United States |

| By Product Type | Whole Bean | |

| Ground Coffee | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| By Type | Conventional Coffee | |

| Specialty Coffee | ||

| By Packaging Type | Flexible | |

| Rigid | ||

| Single-Serve | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other off-trade Channels | ||

| By Geography | California | |

| Texas | ||

| Florida | ||

| New York | ||

| Pennsylvania | ||

| Illinois | ||

| Rest of the United States | ||

Key Questions Answered in the Report

What is the current size of the United States coffee market?

The market is valued at USD 24.98 billion in 2026 and is projected to climb to USD 31.05 billion by 2031.

Which product segment is expanding fastest?

Coffee pods and capsules lead growth with a projected 5.93% CAGR through 2031.

What regions show the strongest growth prospects?

Florida leads with a 6.19% projected CAGR to 2031, driven by tourism, a growing Hispanic population, and year-round demand for iced formats.

Which competitive strategies are shaping the market?

Scale partnerships, functional ingredient innovation, compostable packaging, and direct-to-consumer subscriptions are key levers for growth and differentiation.

Page last updated on: