Market Overview

| Study Period | 2021 - 2031 |

|---|---|

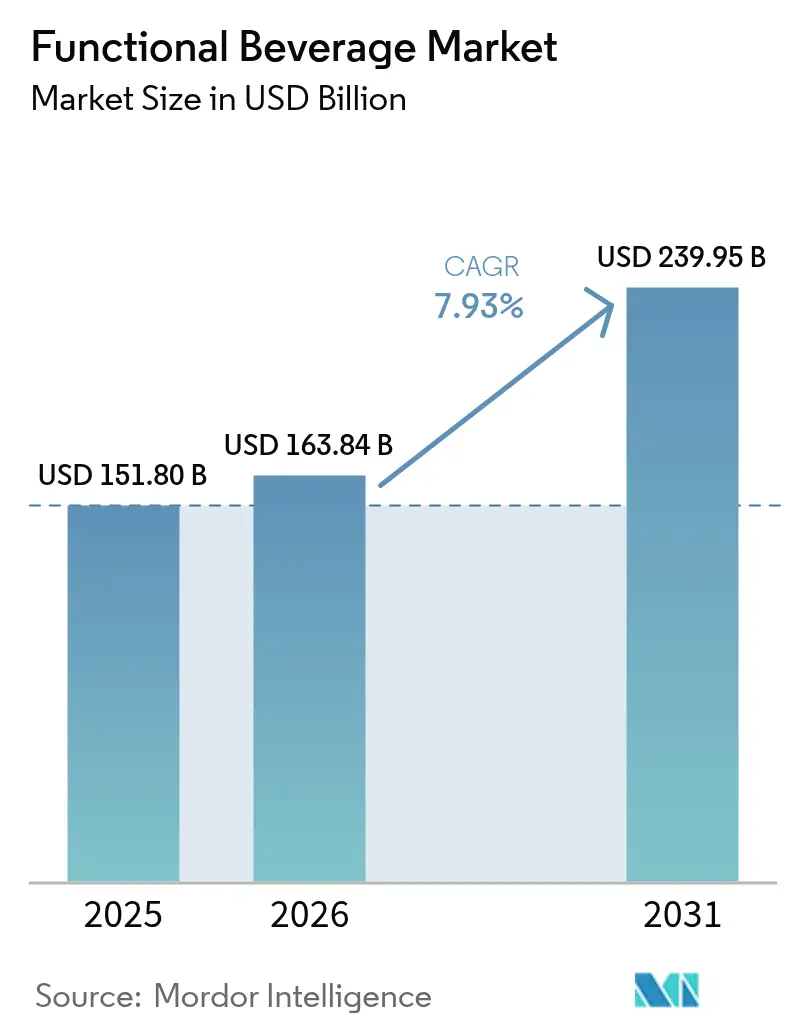

| Market Size (2026) | USD 163.84 Billion |

| Market Size (2031) | USD 239.95 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

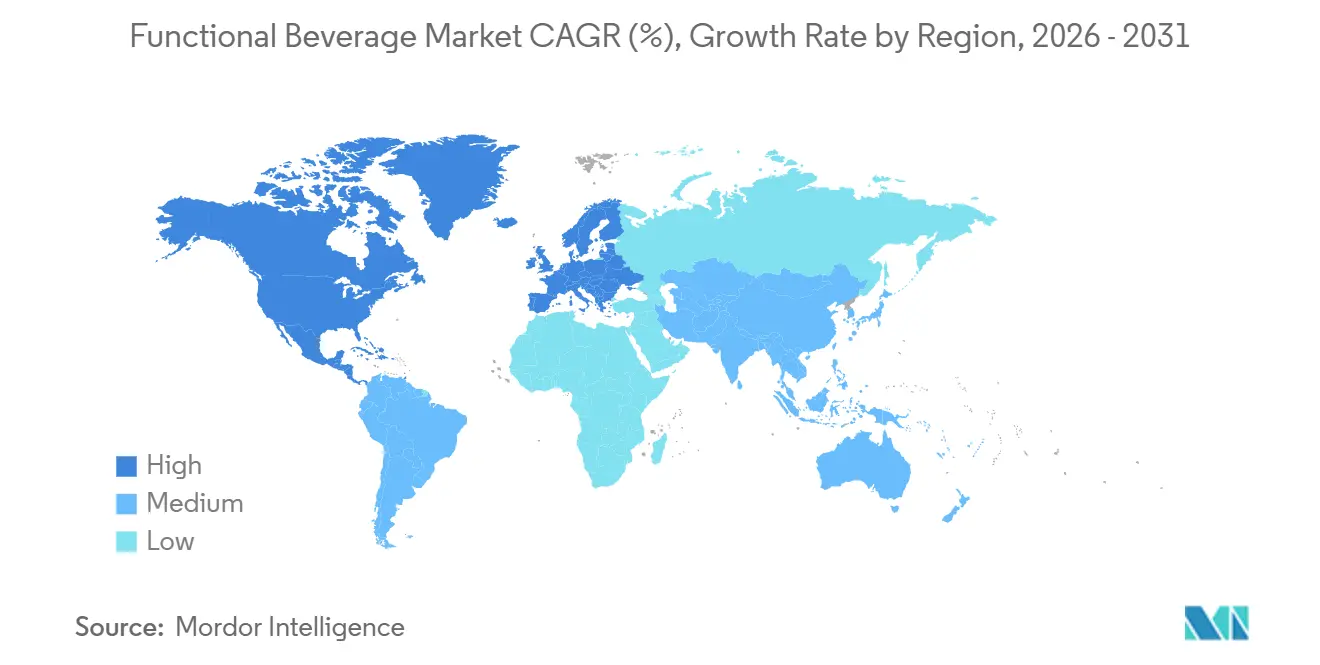

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and North Africa |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Functional Beverage Market Analysis by Mordor Intelligence

The functional beverage market size is expected to grow from USD 151.80 billion in 2025 to USD 163.84 billion in 2026 and is forecast to reach USD 239.95 billion by 2031 at a 7.93% CAGR over 2026-2031. This growth is driven by increasing consumer preference for beverages that not only hydrate but also offer specific wellness benefits. While energy drinks continue to dominate in volume, there's a noticeable shift towards hydration for sports performance, support for gut microbiomes, and solutions for stress relief. Data from the British Soft Drinks Association highlights that in 2024, the UK saw a consumption of 1.2 billion liters of sports and energy drinks, up from 1.1 billion liters in 2023[1]Source: British Soft Drinks Association, "BSDA Annual Report 2024 UK Soft Drinks Report", britishsoftdrinks.com. Global brands are rapidly introducing products enriched with probiotics, adaptogens, and vitamin-mineral combinations. Enhanced packaging now prioritizes ingredient protection and user convenience. Furthermore, as supply chains become more efficient and retail moves further into the digital realm, manufacturers are responding to stricter regulatory definitions of "healthy" by opting for cleaner labels across the functional beverage industry and ensuring their claims are backed by evidence in the functional beverage market.

Key Report Takeaways

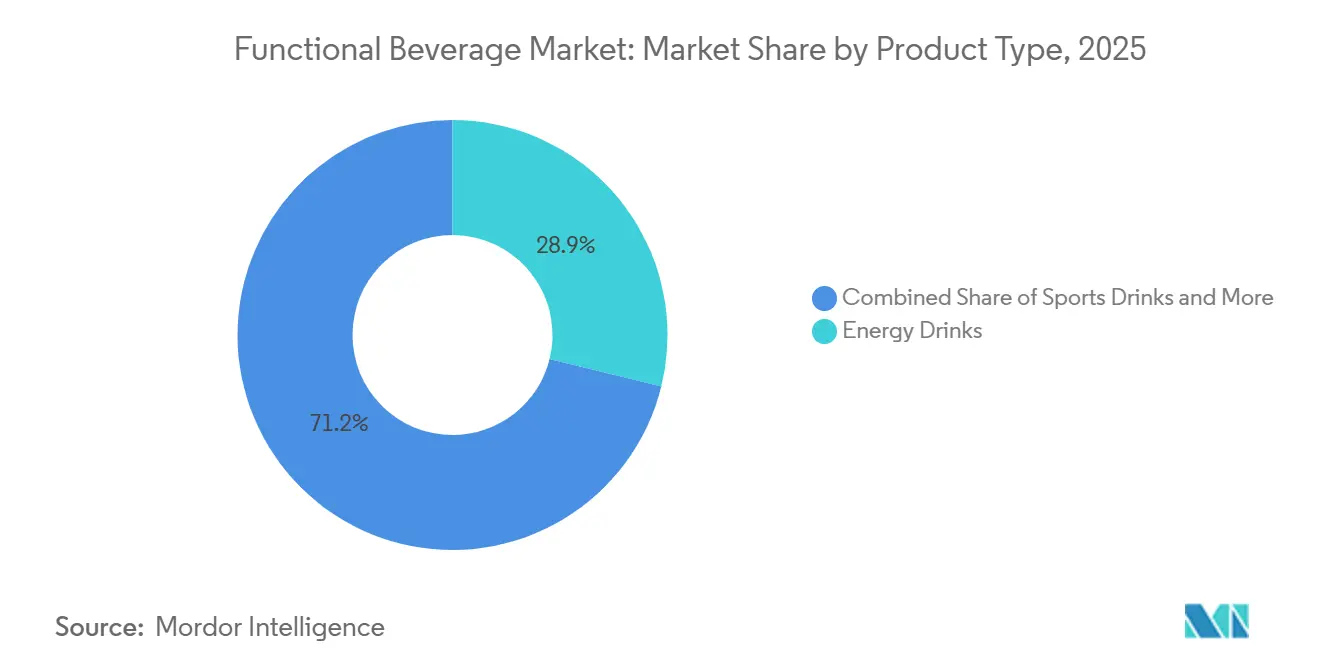

- By product category, energy drinks led with a 28.85% functional beverage market share in 2025, whereas sports drinks are projected to post the fastest 8.42% CAGR through 2031 in the functional beverage market.

- By packaging, PET/glass bottles captured 36.55% of the functional beverage market size in 2025; cans are advancing at a 8.85% CAGR to 2031 in the functional beverage market.

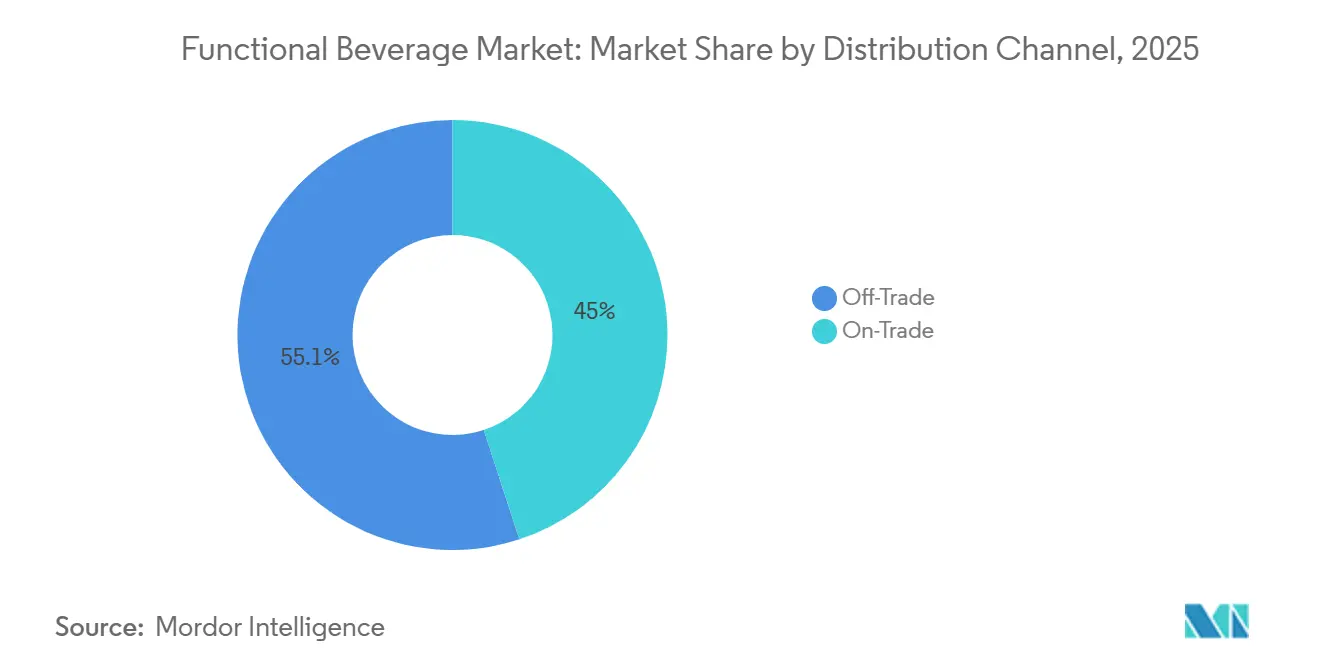

- By distribution, off-trade channels accounted for 55.05% of 2025 revenues, while on-trade outlets are on course for a 8.88% CAGR to 2031 in the functional beverage market.

- By region, North America dominated with a 39.05% revenue share in 2025, but Asia Pacific is poised for an 8.29% CAGR through 2031 in the functional beverage market.

- PepsiCo, Coca-Cola, and Celsius collectively held an estimated 27.65% share of the 2025 functional beverage market size, reflecting ongoing consolidation in the functional beverage market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Functional Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Consumer Focus on Health and Wellness | +2.1% | Global, with the strongest impact in North America and Europe | Long term (≥ 4 years) |

| Demand for Clean Label and Natural Ingredients | +1.8% | Global, particularly strong in developed markets | Medium term (2-4 years) |

| Growing Awareness of Gut Health and Microbiome | +1.4% | North America and Europe leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Innovation in Ingredients and Formulations | +1.2% | Global, with research and development centers in North America and Europe | Long term (≥ 4 years) |

| Sustainability and Ethical Sourcing Focus | +0.9% | Europe is leading, spreading globally | Long term (≥ 4 years) |

| Personalization and Targeted Functional Benefits | +0.7% | North America and select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Focus on Health and Wellness

As consumers become more health-conscious, their focus has shifted from basic nutrition to specific wellness outcomes. This evolution underscores a growing belief among many that food and beverages can serve medicinal purposes. Today, gut health takes precedence for most, closely followed by an emphasis on mental well-being. This trend, which gained momentum in the wake of the pandemic, sees consumers gravitating towards products that bolster immune function, manage stress, and enhance cognitive performance. Highlighting this shift, Kirin Holdings noted a 40% surge in sales of its LC-Plasma product series from January to June 2024. Notably, their immune care beverages alone saw a staggering 183% year-on-year growth, underscoring the market's appetite for health-centric offerings. This burgeoning demand is birthing new market categories. For instance, while probiotics have long been a staple, postbiotic beverages are now emerging as the next big thing in the functional beverage market. A testament to this trend is Asahi Beverages America's recent launch of 'Refrezz', a beverage specifically targeting sleep and relaxation.

Demand for Clean Label and Natural Ingredients

As consumers increasingly demand transparency and recognizable ingredients in functional beverages, clean label requirements are reshaping formulation strategies. This trend not only focuses on ingredient lists but also delves into sourcing practices, processing methods, and packaging sustainability. Such demands pose intricate challenges for manufacturers navigating their supply chains. Reinforcing this trend, the FDA's updated definition of "Healthy," set to take effect in February 2025, introduces stricter criteria for health claims. These criteria mandate that products adhere to specific nutrient profiles, with limitations on added sugars, saturated fats, and sodium. In response, manufacturers are not only reformulating existing products but also crafting new ones to meet clean label standards. However, this alignment often comes at the cost of increased production expenses and heightened complexity in the functional beverage industry. The challenge amplifies with the inclusion of functional ingredients like adaptogens and nootropics. While consumers gravitate towards these natural alternatives over synthetic compounds, they grapple with taste and stability hurdles. Addressing these challenges necessitates advanced masking and preservation technologies. Furthermore, health-conscious consumption patterns have catalyzed unprecedented innovation in clean-label formulations, with consumers globally actively limiting sugar intake and seeking transparency in ingredient sourcing in the functional beverage market. According to the International Food Information Council, in 2023, approximately 29% of respondents in the United States mentioned that they buy food and beverages on a regular basis because they are labeled as "clean ingredients[2]Source: International Food Information Council, "Food & Health Survey 2023", ific.org.

Growing Awareness of Gut Health and Microbiome

Microbiome science has transformed gut health from a niche concern into a mainstream wellness priority, spurring innovations in probiotic, prebiotic, and postbiotic beverage formulations. Over the past decade, the US digestive health market has nearly tripled, with consumers increasingly recognizing the link between good digestive health and overall well-being. This heightened awareness has fueled product innovations, evident in major brands like Coca-Cola and PepsiCo launching prebiotic sodas, such as Simply Pop and Prebiotic Cola, each boasting 3-6 grams of prebiotic fiber per serving. As research deepens into the gut-brain axis, market opportunities are expanding from just digestive health to encompass mental wellness and cognitive function. Yet, challenges remain: ensuring probiotic viability during processing and shelf life, while also crafting taste profiles that resonate with consumers in the functional beverage market. This is especially true for non-dairy alternatives, where traditional fermentation flavors might be unfamiliar to the broader market in the functional beverage industry.

Innovation in Ingredients and Formulations

Ingredient innovation is shifting from traditional vitamins and minerals to advanced bioactive compounds, including adaptogens, nootropics, and specialized proteins, all aimed at achieving specific physiological outcomes. Today's consumers are gravitating towards beverages that simultaneously offer a range of benefits: energy boosts, digestive health, immunity support, mental clarity, and stress relief. This evolving demand has prompted manufacturers to delve into and adopt novel, bioactive, plant-based ingredients. These include turmeric, maca, lion’s mane mushroom, adaptogens like ashwagandha, CBD, various botanicals, and alternative proteins such as hemp and pea. When these ingredients are artfully blended, they not only ensure efficacy but also deliver a palatable taste, a key factor for consumer approval and repeat purchases in the functional beverage market. Furthermore, the rise of sugar alternatives that provide sweetness without the extra calories has paved the way for healthier product innovations. However, as manufacturers strive to meld multiple functional ingredients, they face challenges in preserving taste, stability, and bioavailability. This often necessitates the use of proprietary delivery systems and masking technologies. On the technological front, PepsiCo's recent patent filing highlights the industry's direction: beverage cans equipped with ingredient chambers for the separate storage and controlled release of sensitive compounds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Labeling Requirements | -1.3% | Global, with varying intensity by region | Medium term (2-4 years) |

| Packaging and Sustainability Challenges | -0.8% | Europe leading, expanding globally | Long term (≥ 4 years) |

| Taste and Consumer Palatability Challenges | -0.6% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| High Production and Ingredient Costs | -1.1% | Global, with acute impact in cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Labeling Requirements

As health authorities worldwide tighten their grip on functional beverage claims and ingredient safety, the complexity of regulations is escalating. Starting February 2028, the FDA's revamped definition of "Healthy" mandates manufacturers to keep meticulous compliance records and adhere to specific nutrient benchmarks, pressuring them to reformulate significantly. In Europe, regulations are tightening too. In August 2024, the EU denied health claims for isomaltulose, pointing to a lack of scientific backing and the risk of confusing consumers. Meanwhile, Korea's "Food with Functional Claims" system blurs the lines for consumers, distinguishing between health foods that undergo rigorous testing and those with loosely regulated claims. Such regional regulatory disparities not only inflate compliance costs but also erect barriers to market entry. This is especially challenging for smaller manufacturers who often lack the expertise and resources to adeptly navigate the maze of global regulations in the functional beverage market.

High Production and Ingredient Costs

Manufacturers grapple with rising expenses for specialized functional ingredients, advanced processing equipment, and compliance infrastructure, leading to constrained market growth. Pricing pressures in maltodextrin markets are set to persist through 2024, driven by climate-related disruptions to corn and wheat yields. These disruptions impact a key ingredient in numerous functional beverage formulations. For example, the US Department of Agriculture reported that in 2024, the price per ton of sweet corn for the processing market in the United States was USD 102[3]Source: US Department of Agriculture, "Vegetables summary 2024", nass.usda.gov. While companies in the functional beverage industry like PepsiCo are honing in on productivity improvements, Coca-Cola is contending with rising agricultural costs, highlighting a disparity in input cost normalization across ingredient categories and exerting margin pressures industry-wide. The cost challenges aren't limited to raw materials. Specialized processing demands, essential for maintaining ingredient stability and bioactivity, often necessitate costly equipment and rigorous quality control systems. Despite projected revenue growth in functional beverages, manufacturers are navigating formulation hurdles such as ingredient solubility, texture optimization, and shelf-life extension in the functional beverage market that amplify production complexity and costs in the functional beverage industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sports Drinks Accelerate Beyond Energy Dominance

In 2025, energy drinks command a 28.85% market share, but sports drinks are surging ahead with the fastest growth rate, boasting an 8.42% CAGR projected through 2031. This trend underscores a shift in consumer preferences, leaning towards hydration and recovery solutions that emphasize performance. While energy categories hint at market maturation, sports nutrition is broadening its appeal, reaching out to mainstream wellness enthusiasts, not just traditional athletes. Innovations in electrolyte formulations, natural caffeine sources, and recovery-centric ingredients, such as branched-chain amino acids and adaptogens are propelling the popularity of sports drinks. These advancements cater to fitness aficionados who prioritize functional hydration, as highlighted by the International Food Information Council.

As consumers gravitate towards familiar formats infused with functional benefits, fortified juices and dairy alternatives witness steady growth. Meanwhile, functional water emerges as a category, championed by its convenience and clean-label appeal. The "Others" segment, which includes kombucha, kefir, and other specialty functional beverages, is on a rapid ascent. This surge is fueled by manufacturers' willingness to experiment with unique ingredients and innovative delivery methods. The FDA's revamped "Healthy" definition is making waves in product formulations. It's particularly influencing energy drinks laden with sugars, simultaneously paving the way for naturally sweetened substitutes. The competitive arena is heating up, underscored by significant moves like Celsius's USD 1.8 billion acquisition of Alani Nutrition in April 2025, a deal that's reshaping the functional beverage market landscape and bolstering the share of health-centric energy alternatives.

By Packaging Type: Cans Gain Momentum Through Sustainability

In 2025, PET and glass bottles capture a 36.55% share of the market, underscoring consumer preferences for transparency and perceived quality. Meanwhile, cans are on an upswing, boasting a 8.85% CAGR growth rate projected through 2031, fueled by sustainability drives and the allure of convenience. This shift in packaging underscores a broader change in consumer values, emphasizing environmental responsibility and a penchant for on-the-go consumption. Japan's draft standards for PET bottles, which mandate 15% recycled content and set recyclability benchmarks, highlight the regulatory push steering packaging innovations. Echoing this sentiment, the EU's Packaging and Packaging Waste Regulation sets ambitious targets: 10% reusable packaging by 2030 and a leap to 40% by 2040, imposing hefty compliance challenges for beverage producers.

Alternative packaging formats, like Tetra Pak, are carving a niche, especially in the realm of plant-based and organic functional beverages, where eco-friendly packaging resonates with brand ethos. The beverage carton industry, buoyed by EU packaging mandates, is gearing up with a hefty investment of EUR 200 million in recycling capabilities, with an eye on an extra EUR 100 million by 2027, as reported by the Food and Beverage Carton Alliance. Packaging innovation isn't just about materials; it's also about design. A case in point is PepsiCo's groundbreaking patent for beverage cans featuring ingredient chambers, designed for the optimal delivery of sensitive compounds. As the packaging domain evolves, manufacturers find themselves navigating a maze of sustainability mandates, shifting consumer tastes, budgetary constraints, and the imperative to safeguard functional ingredients in the functional beverage market.

By Distribution Channel: On-Trade Acceleration Signals Premiumization

In 2025, off-trade channels, including supermarkets, convenience stores, and e-commerce platforms, dominate the market with a 55.05% share, serving as the primary venues for discovering and purchasing functional beverages. Meanwhile, on-trade channels are witnessing a robust growth rate of 8.88% CAGR through 2031, underscoring trends of premiumization and a shift towards experiential consumption. Consumers are increasingly willing to pay a premium for curated experiences with functional beverages. This shift in channel dynamics highlights a broader change in consumer behavior, with functional beverages evolving from mere utilitarian purchases to integral components of lifestyle and social occasions in the functional beverage market.

Within the off-trade landscape, e-commerce is surging, prompting beverage companies to bolster their digital capabilities and direct-to-consumer strategies. This move is in response to evolving shopping habits. Subscription models and personalized nutrition platforms are emerging as pivotal distribution avenues, especially for specialized functional beverages aimed at specific health outcomes. Convenience stores are carving out a significant role in functional beverage sales, acting as impulse purchase hubs for energy and sports drinks, while also expanding their refrigerated sections for premium options. Pharmacies and health stores are increasingly aligning functional beverages with supplements and wellness products, targeting health-conscious consumers in search of therapeutic benefits. This distribution evolution is bolstered by advancements in cold chain logistics and technology, ensuring product freshness and an expanded geographic reach across various retail formats.

Geography Analysis

In 2025, North America accounted for 39.05% of sales, driven by high disposable incomes, a sophisticated retail infrastructure, and an early embrace of wellness concepts. New product introductions keep shelves dynamic, while the 2025 FDA's "Healthy" rule brings clarity, fostering a science-driven competitive landscape. Major players are intensifying consolidation, acquiring digital-native startups to tap into emerging growth areas. Despite high category penetration, the regional functional beverage market enjoys mid-single-digit growth rates, buoyed by premiumization and functional layering in the functional beverage market.

Asia Pacific is set to lead with an impressive 8.29% CAGR through 2031, driven by urbanization, a burgeoning affluent middle class, and a blend of traditional herbal remedies with contemporary ready-to-drink formats. In China, Japan, and South Korea, the market for protein drinks and microbiome-focused tonics is thriving, spurred by the rise of fitness apps and the influence of youth culture. The use of locally sourced ingredients like red ginseng, pandan, and chrysanthemum not only enhances product localization but also boosts price competitiveness in the functional beverage market.

Europe grapples with strong demand while navigating stringent environmental and health-claim regulations. Brands that align with the EU’s packaging reuse mandates and can substantiate their nutritional claims gain a competitive edge on the shelves. While South America and the Middle East and Africa lag in overall spending, there's a noticeable uptick in interest for energy and immunity-boosting drinks, thanks to rising disposable incomes and enhanced retail cool-chain networks. To capitalize on these trends, multinationals are increasingly rolling out pilot lines in these regions, eyeing first-mover advantages.

Competitive Landscape

The global functional beverages market is characterized by intense competition between established multinational beverage giants and agile, niche wellness brands, with major players relying on acquisitions, product innovation, and expanded distribution to grow market share in 2024 and 2025. Large-scale corporations like PepsiCo and Coca-Cola are actively acquiring and investing in smaller, disruptive brands to quickly access new consumer trends, demonstrating a strategy of consolidation to capture market growth. In a significant move, PepsiCo acquired the prebiotic soda brand Poppi in March 2025 for USD 1.95 billion, leveraging its distribution power to scale a product that bridges the gap between traditional soda and health-conscious alternatives. Similarly, Coca-Cola entered the prebiotic soda category in February 2025 with the launch of Simply Pop under its Simply brand, aiming to meet evolving consumer needs for functional benefits like gut health in the functional beverage market.

In the energy drink sector, Keurig Dr Pepper made a strategic investment in October 2024 by acquiring a 60% stake in the fast-growing Ghost Energy brand for USD 990 million, strengthening its portfolio in the highly competitive energy drink market. Meanwhile, niche brands like Celsius and Alani Nutrition are rapidly expanding by focusing on zero-sugar energy drinks and leveraging influencer marketing to build strong consumer communities, with Celsius acquiring Alani Nutrition for USD 1.65 billion in February 2025 to create a more dominant platform. Other agile players like Poppi and Bloom Nutrition have thrived by using direct-to-consumer (DTC) channels and targeted digital marketing to disrupt categories and establish authentic connections with younger demographics, with Bloom securing significant funding in 2024 and 2025 to fuel its growth.

Beyond acquisitions, product innovation is a key battleground, with companies focusing on clean-label ingredients, specific health benefits, and sustainability. For instance, Danone, a major player in dairy and water, focuses on expanding its portfolio with functional dairy, water, and plant-based alternatives, emphasizing sustainability with efforts like using 100% rPET bottles for its Evian brand. This highly competitive landscape underscores that success hinges on a combination of strategic acquisitions, continuous product innovation, and effective distribution strategies tailored to evolving consumer demands for health and wellness in the functional beverage industry.

Functional Beverage Industry Leaders

-

PepsiCo, Inc.

-

Monster Beverage Corporation

-

Red Bull GmbH

-

Danone SA

-

The Coca-Cola Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pressed Juicery introduced Blue Pineapple and Cherry Limeade Energy Tonics, zero-sugar beverages with electrolytes, B vitamins, and minerals designed to support energy, mental clarity, hydration, and reduce oxidative stress.

- July 2025: O’Neill Vintners & Distillers entered the functional beverage market with the launch of Catalyst, an energy drink designed for health-conscious consumers. Catalyst featured 120mg of plant-based caffeine, 10 calories, zero sugar, no artificial sweeteners, and was asserted to be fortified with vitamins B12 and B6. It emphasized sustained mental clarity and metabolism support without sugar crashes and was made available in six flavors.

- July 2025: Virtue, known for clean energy drinks, expanded into hydration with Virtue Electrolytes Hydration sachets, which featured zero sugar, 2,540mg of essential electrolytes, and added immunity support. The product targeted daily hydration, recovery, and performance, and is sold online and in major United Kingdom grocery retailers.

- July 2024: Bloom Nutrition launched Bloom Pop, a fizzy, flavor-packed soda with 3-4g sugar, 20 calories, and clinically-backed prebiotics for gut health benefits. Made with a patented prebiotic (PreticX XOS), it was asserted to support digestion without common side effects.

Global Functional Beverage Market Report Scope

A functional beverage is a non-alcoholic drink containing minerals, vitamins, amino acids, dietary fibers (DFs), probiotics, and raw fruits, which provide essential nutritional value and various health benefits.

The global functional beverage market is segmented by type, distribution channel, and geography. The market is segmented based on type into energy drinks, fortified juice, sports drinks, dairy and dairy alternative drinks, and functional/fortified water. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, drug stores and pharmacies, convenience stores, online retail stores, and other distribution channels. The market is segmented based on geography into North America, Europe, Asia-Pacific, South America, the Middle East and Africa. The report offers the market size in value terms in USD for all the abovementioned segments.

By Product Type

| Energy Drinks |

| Sports Drinks |

| Fortified Juice |

| Dairy and Dairy Alternative Beverages |

| Functional/Fortified Water |

| Others |

By Packaging Type

| PET/Glass Bottles |

| Cans |

| Tetra Pak |

| Other Types |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Pharmacies and Health Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Energy Drinks | |

| Sports Drinks | ||

| Fortified Juice | ||

| Dairy and Dairy Alternative Beverages | ||

| Functional/Fortified Water | ||

| Others | ||

| By Packaging Type | PET/Glass Bottles | |

| Cans | ||

| Tetra Pak | ||

| Other Types | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Pharmacies and Health Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the functional beverage market in 2026?

The functional beverage market size reached USD 163.84 billion in 2026.

What CAGR is projected for functional beverages through 2031?

The market is forecast to expand at an 7.93% CAGR from 2026 to 2031.

Which product segment is expected to grow the quickest?

Sports drinks are on track for an 8.42% CAGR, the fastest among product types.

Which region will add the most incremental demand?

Asia Pacific leads growth with an 8.29% CAGR through 2031.

Why are aluminum cans gaining favor in functional drinks?

Cans deliver high recyclability, lightweight logistics, and superior light protection, driving a 8.85% CAGR in can-packaged volumes.

How are regulations influencing product reformulation?

The FDA’s 2025 “Healthy” definition restricts added sugars and sodium, pushing brands toward cleaner labels and natural sweeteners.

Page last updated on: