Freeze-Dried Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

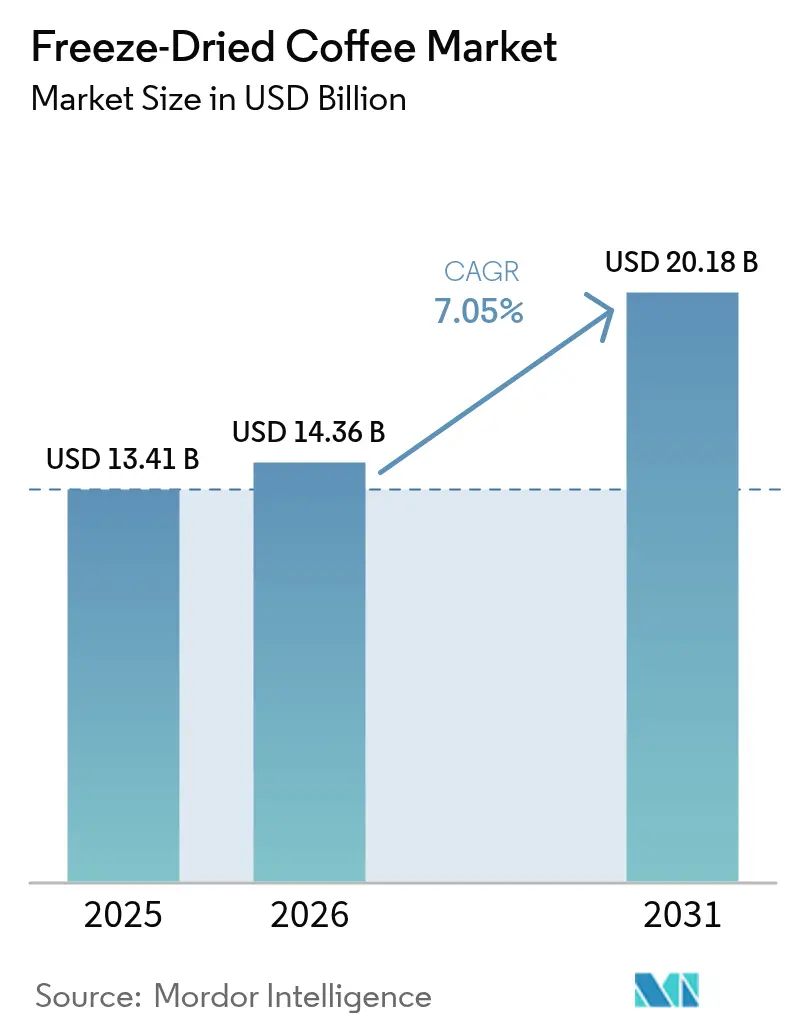

| Market Size (2026) | USD 14.36 Billion |

| Market Size (2031) | USD 20.18 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

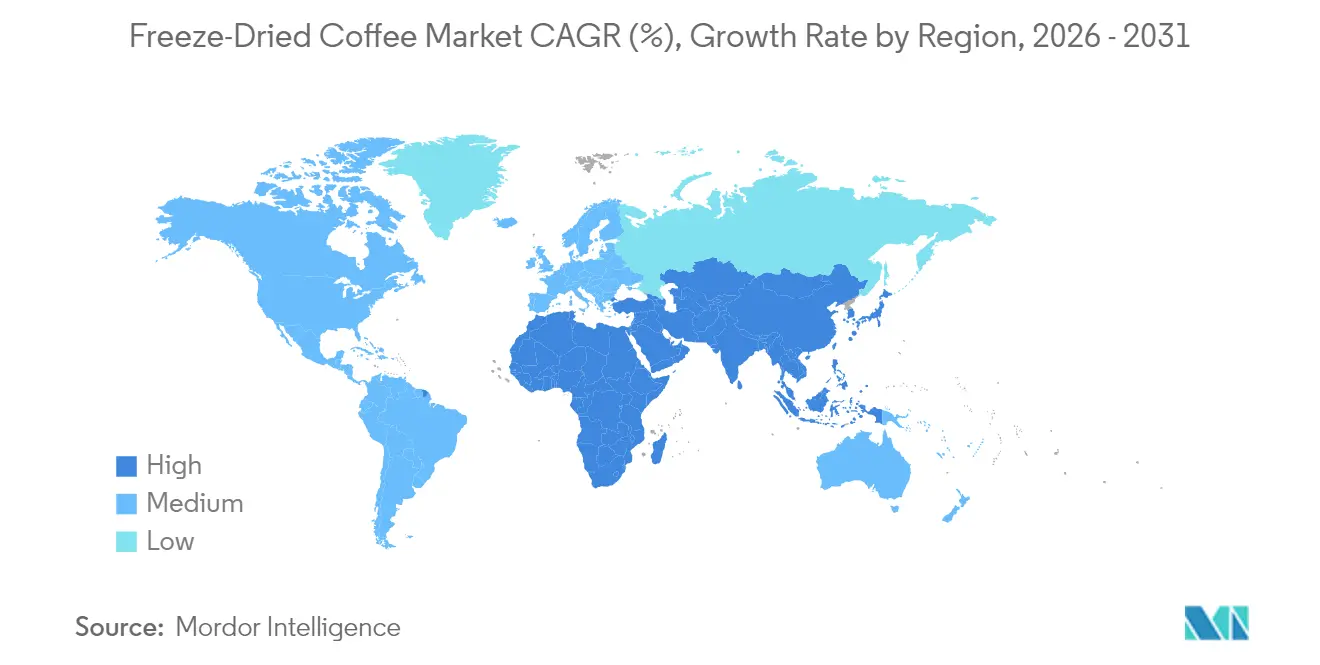

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

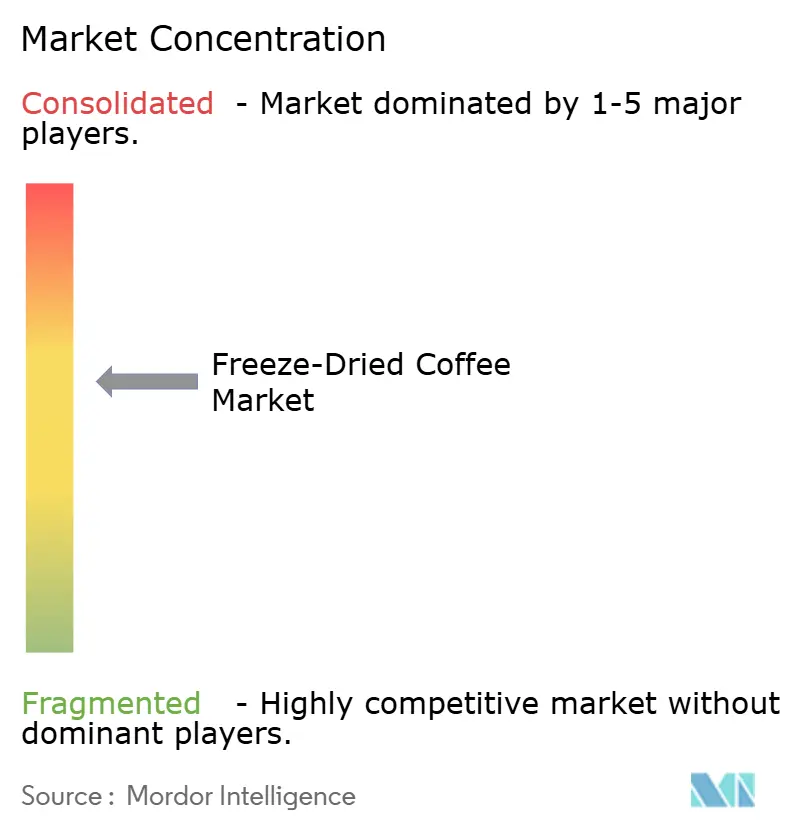

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Freeze-Dried Coffee Market Analysis by Mordor Intelligence

The freeze-dried coffee market size is expected to grow from USD 13.41 billion in 2025 to USD 14.36 billion in 2026 and is forecast to reach USD 20.18 billion by 2031 at 7.05% CAGR over 2026-2031. This growth trajectory is driven by several factors, including advancements in sublimation technology, which enhance the quality and efficiency of freeze-drying processes, and broader access to premium coffee beans, catering to evolving consumer preferences. Additionally, the rising trend of at-home coffee consumption, fueled by convenience and affordability, significantly contributes to market expansion. The Asia-Pacific region's robust acceptance of coffee, coupled with the growing coffee culture in the Middle East and Africa, continues to drive volume growth. At the same time, trends such as premiumization, which focuses on offering high-quality and exclusive products, and sustainability initiatives, which align with environmentally conscious consumer demands, bolster the market's value. Multinational roasters, adept at integrating sourcing, processing, and distribution, maintain pricing power and agility in innovation, enabling them to adapt to market dynamics effectively. However, rising energy costs pose challenges by tempering profit margins. Looking ahead, the freeze-dried coffee market is poised to capitalize on emerging opportunities in digital commerce, functional formulations that cater to health-conscious consumers, and eco-friendly packaging solutions that address sustainability concerns.

Key Report Takeaways

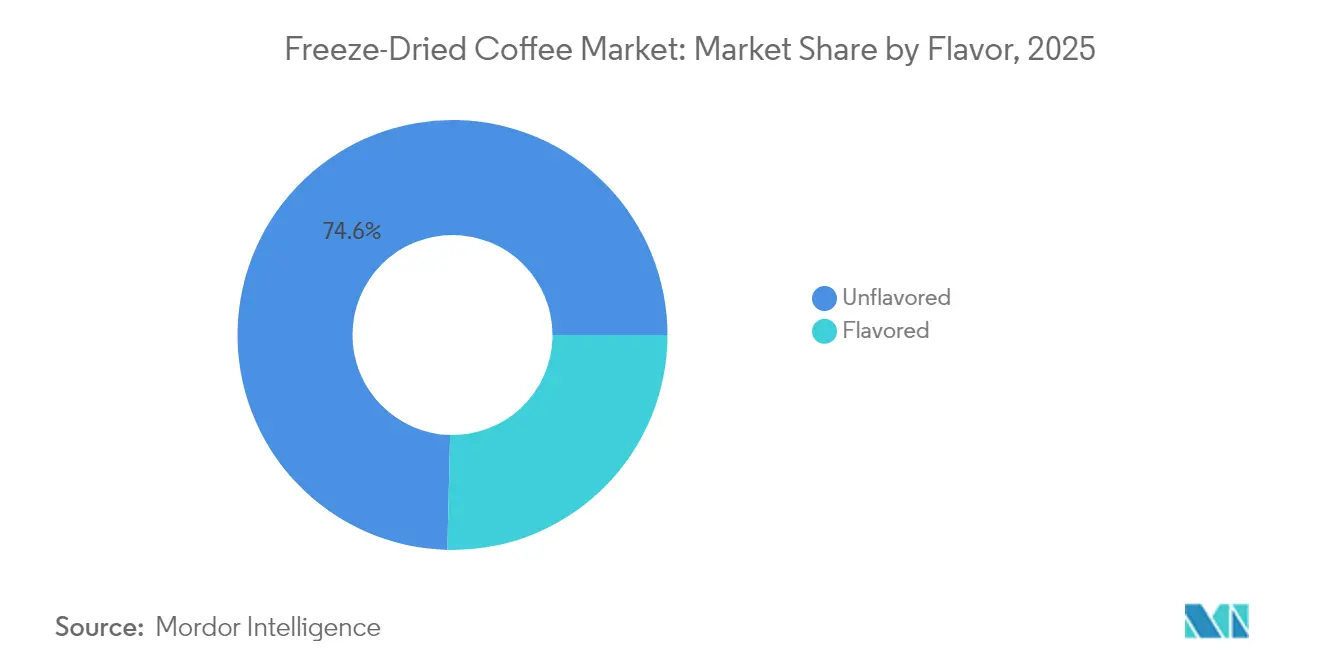

- By flavor, unflavored variants held 74.62% of the freeze-dried coffee market size in 2025, while flavored coffee is expanding at a 7.12% CAGR to 2031.

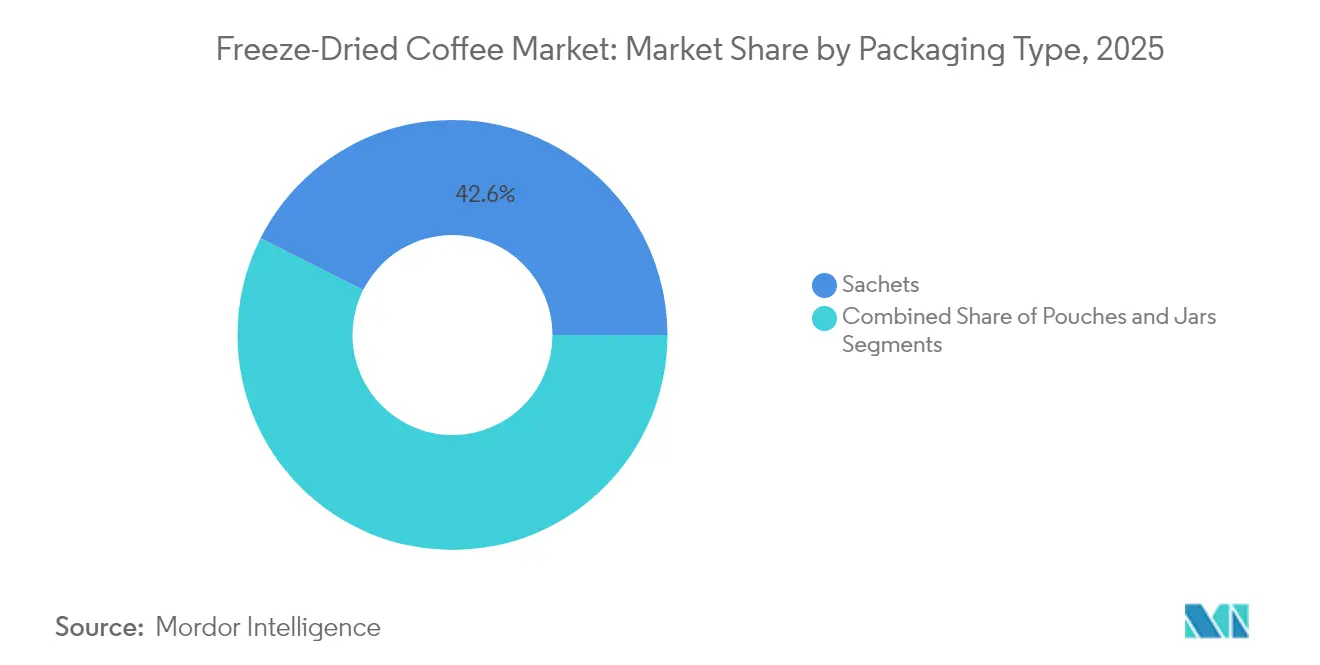

- By packaging, sachets led with 42.58% of freeze-dried coffee market share in 2025; pouches record the highest projected CAGR at 7.47% over the forecast window.

- By bean type, arabica accounted for 58.02% of the freeze-dried coffee market size in 2025 and robusta is growing at a 7.46% CAGR through 2031.

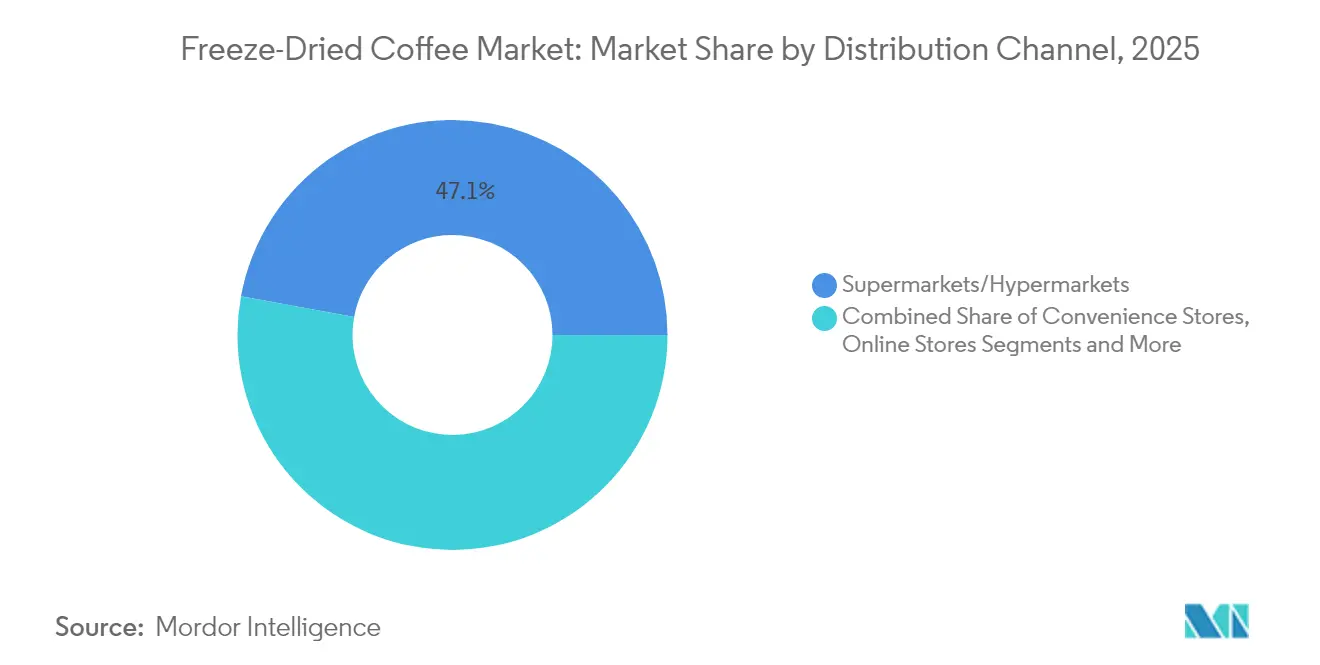

- By distribution channel, supermarkets and hypermarkets represented 47.12% of the freeze-dried coffee market size in 2025, whereas online retail is rising at an 7.76% CAGR to 2031.

- By geography, Asia-Pacific commanded 35.94% of freeze-dried coffee market share in 2025; the Middle East and Africa is advancing at an 7.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Freeze-Dried Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for instant coffee products | +1.8% | Global, with Asia-Pacific core and Middle East and Africa acceleration | Medium term (2-4 years) |

| Technological advancements in freeze-drying processes | +1.2% | North America and Europe innovation centers, global deployment | Long term (≥ 4 years) |

| Increasing demand for premium and specialty coffee options | +1.5% | North America, Europe, urban Asia-Pacific markets | Medium term (2-4 years) |

| Growing coffee consumption in emerging markets | +2.1% | Asia-Pacific core, Middle East and Africa, South America | Long term (≥ 4 years) |

| Superior flavor and aroma retention over other instant coffee methods | +0.9% | Global premium segments | Short term (≤ 2 years) |

| Product innovation and diversification (flavored, organic, etc.) | +1.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for instant coffee products

Instant coffee consumption in emerging economies is accelerating, driven by urbanization and evolving lifestyle preferences that emphasize convenience and quick preparation. In China, coffee consumption reached approximately 7.2 cups per person annually in 2024, signaling substantial growth potential compared to developed markets where averages are significantly higher[1]Source: World Coffee Portal, "JDE Peet’s raises full-year outlook following strong six-month trading", worldcoffeeportal.com. The shift toward at-home coffee consumption has been further reinforced by remote work trends, propelling demand for freeze-dried instant formats that offer café-quality taste without the complexity of brewing. Premium instant coffee segments have demonstrated resilience amid economic uncertainties, as consumers trade down from costly café visits while sustaining high-quality expectations. Southeast Asian markets, particularly Malaysia and Thailand, have shown especially strong adoption rates with double-digit growth in packaged coffee consumption, indicating broader regional momentum. This sustained demand fosters volume growth opportunities for freeze-dried coffee manufacturers, who can capitalize on consumer preferences for convenience combined with uncompromised taste quality, thereby strengthening their market positioning.

Technological advancements in freeze-drying processes

Technological advancements in freeze-drying processes are a key driver for the freeze-dried coffee market, significantly improving product quality and manufacturing efficiency. Innovations such as optimized freeze-drying cycles, precise control of temperature and vacuum pressure, and AI-based quality control systems enable better preservation of coffee’s aroma, flavor, and nutritional content. For example, Nestlé has developed new freeze-drying technology that enhances solubility in cold liquids and eliminates clumping, marking a major breakthrough in cold coffee products. These advancements not only improve the consumer experience but also expand application possibilities across different coffee formats. Moreover, government and industry bodies recognize the importance of such technological innovation, with agencies like the U.S. Department of Energy highlighting efforts to improve energy efficiency in freeze-drying operations. The Specialty Coffee Association and other trade organizations support Research and Development initiatives that promote sustainable and scalable freeze-drying methods, promoting broader adoption and market growth.

Increasing demand for premium and specialty coffee options

The growing demand for premium and specialty coffee options is significantly driving the freeze-dried coffee market. Consumers today are more conscious about the quality, origin, and ethical sourcing of their coffee, seeking products that offer distinctive flavor profiles and authenticity. This shift is fueled by an expanding coffee culture that values artisanal craftsmanship and sustainable practices. Such consumers often desire convenience but are unwilling to compromise on quality, making freeze-dried specialty coffee an attractive choice. Additionally, evolving lifestyles and the rise of third-wave coffee culture have cultivated sophisticated palates that appreciate nuanced flavors found in premium coffee. The National Coffee Association of the USA reports that 46% of American adults consumed specialty coffee in 2024 [2]Source: National Coffee Association of USA, "NCDT Specialty Coffee Report," ncausa.org, highlighting the broad appeal and mainstream adoption of this market segment. As a result, freeze-dried coffee manufacturers are increasingly focusing on premium blends and ethical sourcing to meet heightened consumer expectations and stimulate market growth.

Growing coffee consumption in emerging markets

Growing coffee consumption in emerging markets of the Middle East and Africa is a key driver of the freeze-dried coffee market. In Africa, coffee consumption accounted for 12.5 million 60-kg bags in 2023, up from 12.2 million bags in 2022 [3]Source: International Coffee Organization, "Coffee Report and Outlook December 2023", icocoffee.org, reflecting a steady increase driven by rising urban populations, expanding middle classes, and growing café culture. Key African coffee-consuming countries like Ethiopia, Kenya, and Uganda are seeing rising interest in specialty and premium coffee, shifting consumption away from instant blends to more authentic flavors. Meanwhile, the Middle East market is witnessing rapid growth fueled by strong young consumer demographics, increasing disposable incomes, and evolving coffee cultures in countries such as Saudi Arabia, the UAE, and Qatar. Expansion of branded coffee outlets, surge in café culture, and growing at-home consumption supported by innovative products and digital retail penetration further escalate demand. Together, these regional growth dynamics create robust opportunities for freeze-dried coffee manufacturers to capture market share by delivering convenient, quality-centric coffee formats aligned with evolving consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and operational costs due to energy-intensive freeze-drying | -1.4% | Global manufacturing centers | Short term (≤ 2 years) |

| Price sensitivity among consumers | -0.8% | Emerging markets, price-conscious segments | Medium term (2-4 years) |

| Strong competition from freshly ground, pod, and RTD coffee alternatives | -1.1% | Developed markets with diverse coffee options | Medium term (2-4 years) |

| Quality perception issues versus freshly brewed coffee | -0.6% | Premium coffee segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High production and operational costs due to energy-intensive freeze-drying

High production and operational costs due to the energy-intensive freeze-drying process represent a significant restraint for the freeze-dried coffee market. Freeze-drying preserves flavor and aroma by sublimating water under vacuum conditions at low temperatures, which is a highly complex and resource-intensive technique. This process requires substantial energy consumption, especially for maintaining low temperatures and operating vacuum systems, contributing to elevated electricity and operational expenses. These high costs can impact the overall profitability of manufacturers, as well as the retail pricing of freeze-dried coffee products, making them less accessible for price-sensitive consumers. Despite innovations such as advanced cooling technologies and efforts to improve energy efficiency, the inherent energy demands of freeze-drying remain a challenge. Consequently, companies must balance product quality with cost management, pushing ongoing research into sustainable and cost-effective production methods to maintain competitiveness while addressing environmental and economic concerns.

Price sensitivity among consumers

Price sensitivity among consumers is a significant market restraint for the freeze-dried coffee market, particularly in developing and price-conscious regions. Despite the superior flavor retention and premium quality offered by freeze-dried coffee, its higher production costs result in a retail price that is considerably above regular instant coffee and ground coffee options. Many consumers in emerging markets prioritize affordability, which limits the wider adoption of freeze-dried coffee products in these areas. Research indicates that price is the key factor influencing consumer preference and purchasing decisions for instant coffee, often outweighing perceived quality differences. This sensitivity compels manufacturers to focus on cost efficiencies and competitive pricing strategies to expand market penetration. Consequently, while freeze-dried coffee appeals to discerning consumers seeking a premium experience, price constraints restrict its mainstream growth, especially in price-competitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Unflavored Dominance Drives Volume Scale

Unflavored freeze-dried coffee held a dominant market share of 74.62% in 2025, reflecting strong consumer preference for authentic coffee taste profiles. This segment's popularity stems from its ability to deliver a consistent and pure coffee flavor while allowing consumers to customize their drinks with additives as desired. Unflavored variants benefit from cost advantages in production, which contribute to their affordability and wide acceptance across a broad range of taste preferences. The segment’s extensive consumer base spans different demographics and geographic areas, further supporting its market leadership. Additionally, the manufacturing processes are well-established, leading to efficiencies that help maintain competitive pricing. These factors combined ensure that unflavored freeze-dried coffee remains the foundational choice for consumers seeking traditional flavor with convenience.

Flavored freeze-dried coffee, while occupying a smaller share, is the fastest-growing segment in this market, with a robust CAGR of 7.12% projected through 2031. This growth is primarily driven by the innovation of sophisticated flavor combinations aimed at attracting younger and more experimental consumers. Manufacturers are increasingly investing in flavor development, targeting evolving consumer palates that seek variety and novel experiences. Marketing efforts often focus on lifestyle and indulgence themes, resonating well with urban and millennial demographics. Furthermore, flavored variants tap into the increasing demand for ready-to-drink and on-the-go coffee solutions. The segment’s accelerated expansion highlights its potential to gradually capture a larger share as consumer preferences diversify beyond traditional coffee tastes.

By Packaging Type: Sachets Lead While Pouches Accelerate

Sachets maintained a leading market share of 42.58% in 2025, benefiting from features such as precise portion control, extended shelf life, and convenience in distribution across diverse retail channels. This packaging format is especially well-suited for emerging markets, where single-serve purchasing patterns match income constraints and consumer habits. The easy-to-use and portable nature of sachets appeals to busy consumers who prioritize quick and hygienic coffee preparation. Retailers also favor sachets because they optimize shelf space and facilitate competitive pricing strategies. Furthermore, sachets cater to on-the-go consumption, which is gaining popularity among younger demographics and urban dwellers. Overall, sachets have established themselves as a practical and preferred packaging option across many regions, driven by accessibility and consumer convenience.

Pouches are emerging as the fastest-growing packaging format, with a projected CAGR of 7.47%, driven largely by sustainability concerns and consumer preference for bulk purchasing. They appeal to environmentally conscious buyers due to their reduced packaging waste compared to traditional rigid containers. Additionally, pouches offer flexibility in size options, from single-serve to larger family packs, aligning with varied consumption needs. The resealable features of pouches help maintain coffee freshness after opening, elevating their utility for home use. Retailers are also adopting pouches as a lightweight and cost-efficient alternative that lowers transportation and storage expenses. As consumer demand shifts towards eco-friendly and practical packaging, pouches are poised to capture an increasing share of the freeze-dried coffee market globally.

By Bean Type: Arabica Premium Positioning Versus Robusta Value Growth

Arabica varieties held the largest share of 58.02% in the freeze-dried coffee market in 2025, leveraging their superior flavor profiles and strong consumer perceptions of quality. This segment benefits from well-established supply chains and advanced processing expertise that help preserve Arabica’s delicate flavor compounds during the freeze-drying process. The premium positioning of Arabica coffee appeals to consumers who prioritize taste and origin characteristics, reinforcing its leadership. Its nuanced acidity and aromatic qualities set it apart in the premium instant coffee sector, attracting discerning coffee drinkers. Robust cultivation and sourcing partnerships further support consistent supply and product innovation. Overall, Arabica’s dominance reflects both consumer preference for quality and the industry’s capability to deliver premium freeze-dried coffee products.

Robusta varieties are the fastest-growing segment within the freeze-dried coffee market, projected to expand at a CAGR of 7.46% through 2031. This growth is driven by Robusta’s cost advantages and its resilience to climate variability, which contribute to more stable supply chains. Although Robusta generally has a stronger, more bitter taste profile, its higher caffeine content and affordability appeal to price-sensitive consumers and large-scale manufacturers. Additionally, Robusta plays a critical role in blended instant coffee products, widening its usage and market penetration. The segment’s robust growth signals increasing demand in emerging markets and among consumers seeking cost-effective coffee solutions. The contrasting growth patterns between Arabica and Robusta highlight a market bifurcation balancing premium quality with accessibility.

By Distribution Channel: Traditional Retail Dominance Challenged by Digital Growth

In 2025, supermarkets and hypermarkets led the freeze-dried coffee market with a 47.12% share, supported by well-established consumer shopping habits and extensive product placement opportunities. These channels offer high visibility and convenience, enabling consumers to compare brands, flavors, and prices under one roof. The wide geographic reach and regular foot traffic in these outlets further boost sales volume and brand recognition. Promotional campaigns and strategic shelf positioning contribute to impulse buying behavior, enhancing overall market performance. Moreover, supermarkets and hypermarkets provide reliable supply chains that ensure steady product availability, which is crucial for daily coffee consumption. The dominance of these traditional retail formats underscores their importance in shaping consumer purchasing decisions.

Online retail channels are the fastest-growing segment in the freeze-dried coffee market, projected to expand at a strong CAGR of 7.76% through 2031. This growth is driven by the increasing adoption of e-commerce platforms and direct-to-consumer sales strategies that bypass traditional retail margins. Online shopping offers consumers convenience, wider product selection, and access to detailed product information and customer reviews. Subscription services for regular coffee deliveries are also gaining popularity, promoting customer loyalty and repeat purchases. Additionally, the shift toward digital shopping was accelerated by the pandemic, further establishing e-commerce as a preferred purchasing channel. As consumers increasingly seek contactless and home delivery options, online retail is poised to capture a growing share of the freeze-dried coffee market globally.

Geography Analysis

In 2025, the Asia-Pacific region commands a dominant 35.94% market share, buoyed by entrenched instant coffee consumption habits and demographic advantages in pivotal markets like China, Japan, and Southeast Asia. Local production and a close-knit supply chain bolster the region's cost-competitive stance, enabling manufacturers to cater to both domestic and international demand efficiently. China's burgeoning coffee culture among its youth, driven by increasing disposable incomes and exposure to global coffee trends, propels its growth. Meanwhile, Japan's discerning taste in instant coffee, characterized by a preference for high-quality and innovative products, fuels the premium segment's rise. In Southeast Asia, markets such as Malaysia, Thailand, and Vietnam leverage their strong local production capabilities and cultural affinity for instant coffee to exhibit robust growth. Additionally, the region's proximity to major coffee-producing nations like Indonesia and Vietnam further amplifies its cost advantages, solidifying its competitive edge on the global stage.

Europe, a seasoned player in the coffee market, is witnessing a shift towards premiumization and sustainability. These trends are reshaping packaging innovations and sourcing practices, as consumers increasingly demand environmentally friendly and ethically sourced products. However, the continent grapples with the EU Deforestation Regulation (EUDR), mandating traceability and deforestation-free sourcing in supply chains, a move that reshapes cost dynamics and supplier ties. Germany, France, and the UK lead in consumption, driven by their established coffee-drinking cultures and preference for premium offerings. Meanwhile, Eastern Europe's emerging markets, such as Poland and Hungary, hint at untapped growth potential due to rising disposable incomes and evolving consumer preferences. To align with both regulatory mandates and consumer demands, European manufacturers are channeling significant investments into sustainable packaging and responsible sourcing initiatives, ensuring compliance while maintaining consumer trust.

In North America, a steady demand uptick is evident, fueled by a penchant for convenience and a tilt towards premium products. This trend resonates with value-driven consumers opting for quality over café prices, as they seek affordable yet high-quality alternatives for at-home consumption. The U.S. stands as the regional consumption titan, supported by a well-established coffee culture and a growing preference for instant coffee among busy professionals. Meanwhile, the Middle East and Africa are on a rapid ascent, boasting an 7.90% CAGR. Urbanization in the UAE, Saudi Arabia, and South Africa is catalyzing a swift embrace of coffee culture, with a marked preference for the convenience of instant coffee. These markets are also witnessing increased investments in retail and distribution networks, further supporting growth. In South America, Brazil and Argentina are striking a balance, nurturing domestic consumption while bolstering export capabilities. Brazil, as one of the largest coffee producers globally, plays a pivotal role in supporting global supply chains, while Argentina's growing coffee culture contributes to regional demand expansion.

Regulatory Landscape

Freeze-dried coffee regulatory compliance generally follows broader packaged-food requirements for hygiene, labeling, and import controls, with added scrutiny on ingredient and processing declarations and origin documentation. In the European Union, operators typically align food safety systems with General Food Law (Regulation (EC) No 178/2002) and label finished products under the Food Information to Consumers framework (Regulation (EU) No 1169/2011), while multinational brands also benchmark to Codex Alimentarius hygiene guidance for dehydrated products to support market access.

Cross-border trade requirements remain a key cost and documentation driver. In the United States, import handling depends on correct tariff classification (commonly under HTS heading 2101 for coffee extracts/essences/concentrates), plus FDA food import requirements such as prior notice processes for packaged foods entering the market. A recent example of regulatory volatility affecting landed costs occurred in February 2026 when US Customs and Border Protection (CBP) communicated a 10% ad valorem surcharge under Section 122 of the Trade Act of 1974, followed by a June 2026 US Court of International Trade decision (Slip Op. 26-53) that invalidated the measure and ended collection, underscoring the need for scenario planning in sourcing and pricing for internationally traded instant coffee products.

Value Chain Analysis

The freeze-dried coffee value chain starts with green-bean sourcing and procurement (arabica and robusta), followed by roasting and extraction to produce coffee liquor, then concentration, freezing, and sublimation-based drying in vacuum chambers. Typical manufacturing sequences include extraction and concentration (often around 25-35% total dissolved solids using vacuum or freeze concentration), rapid freezing at around -40 C or lower, and vacuum freeze-drying cycles that can run roughly 18-36 hours, followed by agglomeration/granulation, quality testing, and packaging into jars, sachets, or pouches for retail and foodservice. Quality and compliance checkpoints commonly cover food safety plans (HACCP-based controls), contaminant or processing indicators referenced by buyers (for example, acrylamide-related specifications), and customer or channel requirements such as BRC Global Standard for Food Safety certification for suppliers serving premium brands and export-heavy programs.

Downstream, distribution runs through supermarket/hypermarket networks, wholesalers, and fast-growing online retail and direct-to-consumer models, with brand owners using pack formats such as sachets for affordability and pouches for resealability and logistics efficiency. The chain is sensitive to energy pricing at the processing stage and to ocean freight disruptions at the logistics stage, where Red Sea rerouting has added reported per-container costs and longer lead times that increase working capital needs and inventory buffers. These pressures tend to favor larger, vertically integrated roasters and soluble coffee specialists that can balance procurement, manufacturing throughput, packaging procurement, and multi-region distribution while maintaining consistent aroma and solubility performance demanded by premium instant coffee segments.

Competitive Landscape

The freeze-dried coffee market exhibits a moderately concentrated competitive landscape dominated by several key global players alongside numerous regional and emerging brands. Major corporations such as Nestlé SA, Starbucks, JAB Holding Company, The J.M. Smucker Company, and Unilever hold significant market shares, leveraging their extensive distribution networks, strong brand equity, and continuous innovation efforts. These companies invest heavily in technological advancements in freeze-drying processes, product diversification, and premiumization to meet evolving consumer preferences. Their global reach and established supply chains enable wide market penetration, particularly across key regions like North America, Europe, and Asia-Pacific.

Meanwhile, mid-sized and niche players focus on specialty coffee and organic products to carve out market segments, increasing overall competitiveness. The dynamic rivalry fosters continuous product quality improvements and broader portfolio expansions, benefiting consumers through variety and innovation. Technological advancements play a pivotal role in shaping competition within the freeze-dried coffee segment. Enhanced freeze-drying techniques allow manufacturers to better preserve aroma, flavor, and solubility, narrowing the gap between instant and freshly brewed coffee.

This drives differentiation among players who compete on product quality and specialty offerings. At the same time, sustainability initiatives are becoming a critical component of competitive strategy, with companies adopting eco-friendly packaging solutions and ethically sourced beans. The rise of e-commerce and direct-to-consumer sales channels has further intensified competition by expanding access and enabling smaller brands to challenge incumbents through targeted marketing and consumer engagement. As consumers increasingly seek premium and convenient coffee options, competition is expected to remain robust, with innovation as a key catalyst for growth and differentiation.

Freeze-Dried Coffee Industry Leaders

-

Nestlé S.A.

-

The J.M. Smucker Company

-

Luigi Lavazza S.p.A.

-

JAB Holding Company

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and process differentiation is creating space in cold-soluble and premium instant applications, where freeze-dried formats compete with RTD and pod-based alternatives on convenience while still positioning for higher cup quality. Nestle has showcased freeze-drying innovation for cold consumption through the launch of Nescafe Iced Blend in Japan (introduced alongside a novel freeze-drying method to improve cold solubility and reduce clumping), and Buencafe has highlighted demand-side pull in iced use cases, reporting 35% year-over-year volume growth in iced coffee servings in the first half of 2025 versus 2024. These signals support further portfolio development in flavored and functional variants, with technology-led solubility and aroma retention functioning as a premiumization lever.

Opportunity areas are also being shaped by manufacturing footprint expansion and certification-led access to customers. Capacity additions and modernization projects, such as Vintage Coffee and Beverages commissioning a 4,500 MTPA brownfield expansion at its Telangana facility (taking total soluble coffee capacity to 11,000 MTPA) and Nestle announcing a new coffee plant investment in Thailand, point to continued geographic rebalancing toward Asia for scale, supply security, and proximity to high-growth consumption markets. Supplier-side competitiveness is increasingly tied to food-safety and retailer certifications (for example, BRC certification cited by export-oriented freeze-dried producers) and to energy-efficient extraction and drying roadmaps, including industry and academic work on eco-efficient extraction methods aimed at reducing the energy intensity of soluble coffee production while protecting flavor and aroma compounds.

Recent Industry Developments

- July 2026: Nestle S.A. announced plans to build a USD 690 million coffee production plant in Thailand to support Nescafe operations and distribution across Southeast Asia. The investment expands regional manufacturing capacity and strengthens supply responsiveness for soluble coffee formats, including premium and cold-consumption innovations that use freeze-drying capabilities.

- September 2025: Nestle S.A. announced a BRL 1 billion investment to modernize and expand its Araras, Brazil instant coffee factory, including a stated plan to lift production capacity by 10% by 2028. The upgrade targets higher efficiency and supports broader soluble coffee output, helping global brands manage cost and quality consistency amid volatile green coffee and energy inputs.

- November 2024: Tata Coffee approved an INR 450 crore capacity expansion in Vietnam, including construction of a new 5,500-tonne freeze-dried coffee facility. The project strengthens supply from a major robusta-linked origin and adds export-oriented freeze-dried capacity that can serve both retail and ingredient buyers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the freeze-dried coffee market covers coffee processed through freeze drying and sold as instant granules or powder through retail and out of home channels across major geographies, measured in value terms.

Scope exclusions: We exclude non-freeze-dried formats such as spray-dried instant coffee and ready-to-drink coffee beverages.

Segmentation Overview

-

By Flavor

- Flavored

- Unflavored

-

By Packaging Type

- Jars

- Sachets

- Pouches

-

By Bean Type

- Arabica

- Robusta

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the freeze-dried coffee chain from green coffee inputs to soluble processing and then to packaged retail and foodservice demand. We rely on public references such as International Coffee Organization indicators, USDA coffee outlook and trade notes, FAOSTAT coffee production series, and UN Comtrade trade tables that cover coffee extracts and concentrates.

To make the inputs practical, we also reviewed national customs and statistics portals where available for import and export context, along with company filings, investor presentations, and trade association websites to understand pricing actions, capacity moves, and channel shifts. Peer-reviewed food science and coffee chemistry journals were scanned to understand process trends that can affect yields and product quality, and patent databases were checked to spot technology direction (for example, aroma retention and agglomeration). For additional context on market structure and financial signals, we used a paid subscription covering company financials and another paid subscription covering news and financials. These desk research sources are illustrative only, and many other public references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what desk signals could not fully explain, especially pack price movement by packaging type, channel margins, and how freeze-dried coffee is positioned versus other instant forms. We spoke with respondents across soluble coffee manufacturing, ingredient supply, distribution, and retail and foodservice buying roles, and the coverage spanned the main consumption regions so regional demand patterns were not overgeneralized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 40% |

| Mid tier: 54% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 18% | Managers: 60% | Americas: 24% |

Market-Sizing & Forecasting

The market is first built using top-down logic where coffee production and trade series, followed by soluble conversion assumptions, are used to reconstruct a realistic demand pool for freeze-dried formats by region. That structure is then translated into value using observed price bands and pack mix patterns across jars, sachets, and pouches, with channel splits applied for supermarkets, convenience, online, and other routes.

After the first build, results are corroborated with selective bottom-up approximations so totals stay grounded, such as sampled shelf prices multiplied by estimated volumes, plus supplier-side checks on freeze-dried capacity utilization and export intensity where signals are available. Inputs used as model drivers include green coffee price direction, coffee extract trade flows, retail price per 100g progression, premiumization share within instant coffee, online channel growth rates, and region-level at-home consumption trends. For forecasting, scenario analysis was used and then narrowed through consensus from primary interviews, because pricing, coffee input costs, and consumer trade-down cycles can shift near-term outcomes more than a single trend line would show. Where bottom-up visibility is thin in smaller markets, the gaps are handled through proxy ratios taken from comparable consumption and trade profiles, which are then rechecked with regional experts.

Data Validation & Update Cycle

Validation is done through several checks so the numbers do not depend on one data stream. We compare model outputs against independent signals like coffee extract trade direction, retail price movement, and reported capacity additions, and then anomalies are flagged for rework.

Before sign-off, the work goes through multi-step analyst review where assumptions are rechecked and calculations are replicated to prevent simple errors. If a large variance shows up by region or channel, experts are re-contacted to confirm whether it is a real shift or a modeling miss. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp coffee price swings, major capacity changes, or meaningful channel disruptions. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Freeze Dried Coffee Market Size Compared Against Other Published Estimates

Published market values for freeze-dried coffee can look far apart because the scope and price math are not aligned across studies. The biggest differences usually come from what is counted as freeze-dried versus broader instant coffee, which channels are included, and how pack prices are converted into one annual value.

Some sources combine freeze-dried with wider instant coffee definitions or use blended pricing that does not fully reflect packaging mix by region. For Mordor Intelligence, only freeze-dried coffee is counted and the value build uses jar, sachet, and pouch mix with region-level price bands that are then checked against coffee extract trade direction and interview feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.36 B (2026) | |

| Global Consultancy A | USD 4.52 B (2025) | Applies a narrower interpreted definition that appears closer to selected freeze-dried lines, which can miss parts of mainstream retail and foodservice demand counted in the channel-based model. |

| Industry Publisher B | USD 15.86 B (2024) | Uses a broader freeze-dried instant coffee framing and an earlier base year, which can pull in adjacent instant formats and amplify value when inflation and currency timing are not aligned to the same year. |

The spread across the table mainly comes from category definition and how value is built from prices and mix. By keeping the inputs tied to packaging mix, channel presence, and observable trade and pricing signals, the final market value stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the global value of the freeze-dried coffee market in 2026?

The market is valued at USD 14.36 billion in 2026.

How fast is the freeze-dried coffee market expected to grow?

It is projected to advance at a 7.05% CAGR between 2026 and 2031.

Which region currently leads sales of freeze-dried coffee?

Asia-Pacific holds the largest share at 35.94% in 2025.

What packaging format is growing quickest?

Pouches are forecast to post a 7.47% CAGR through 2031.

Which bean type is expanding faster, arabica or robusta?

Robusta is growing more quickly at a 7.46% CAGR, driven by its lower price point.

Page last updated on: