Instant Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

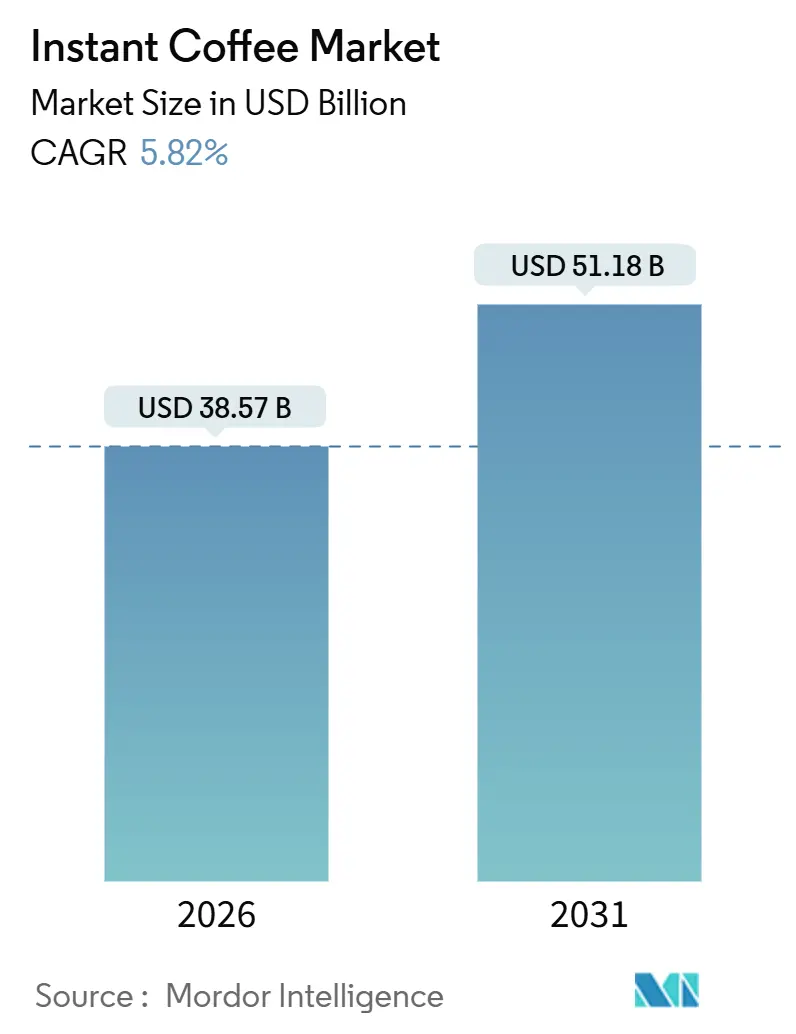

| Market Size (2026) | USD 38.57 Billion |

| Market Size (2031) | USD 51.18 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

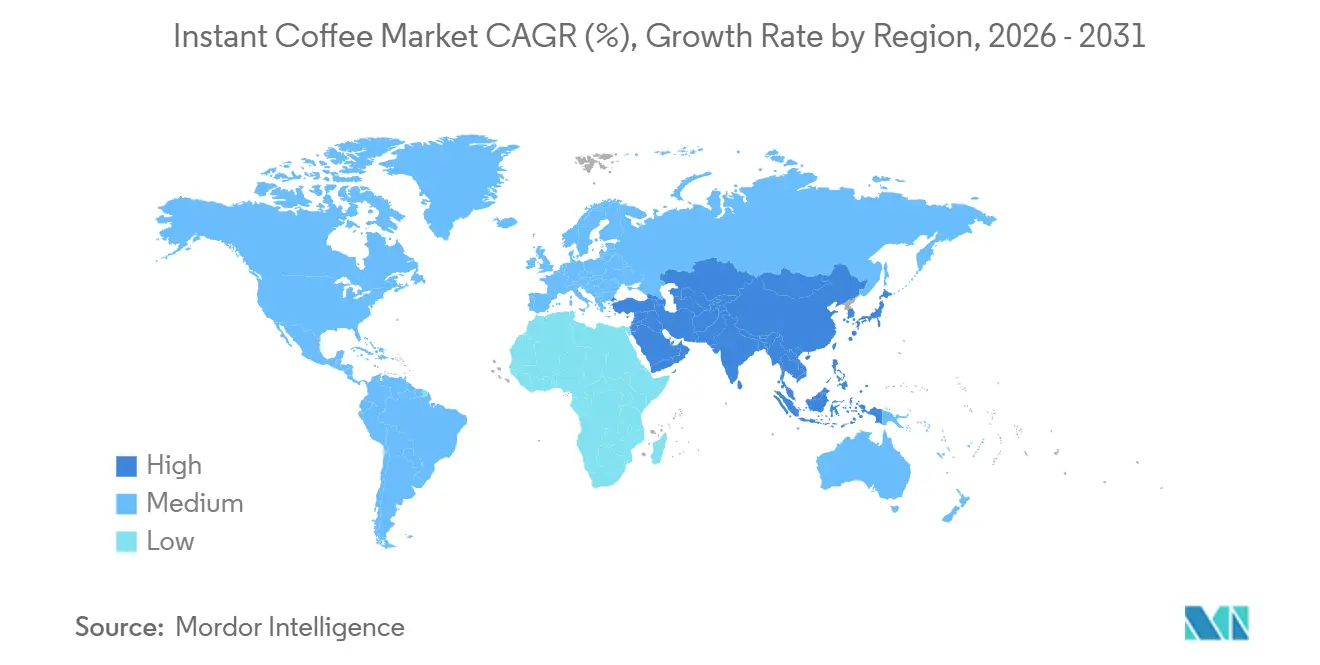

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Instant Coffee Market Analysis by Mordor Intelligence

The instant coffee market size is estimated at USD 38.57 billion in 2026, and is expected to reach USD 51.18 billion by 2031, at a CAGR of 5.82% during the forecast period (2026-2031). This trajectory reflects a sector navigating simultaneous supply-chain stress and demand premiumization, as climate-induced yield volatility in Brazil and Vietnam collides with consumer appetite for single-origin freeze-dried formats. The International Coffee Organization reported that soluble coffee exports fell 28.2% year-over-year in December 2024 to 0.94 million bags, while the composite indicator price surged 75.8% to 310.12 US cents per pound by January 2025, signalling tightening green-coffee availability that compresses instant-coffee margins.

Key Report Takeaways

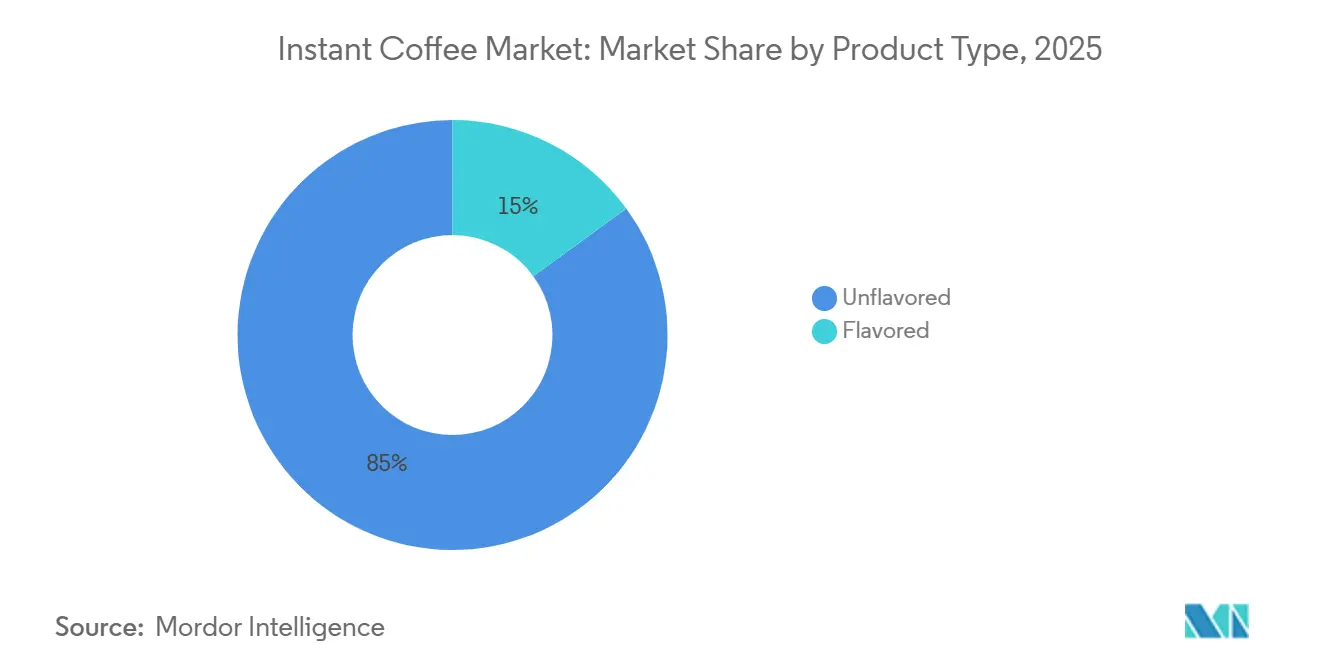

- By product type, unflavored instant coffee led with an 85.01% revenue share in 2025, whereas flavored variants are forecast to advance at a 7.62% CAGR to 2031.

- By production technology, spray-dried formats held a 63.52% share of the instant coffee market size in 2025, while freeze-dried solutions are set to grow at a 6.33% CAGR through 2031.

- By price, mass-priced offerings accounted for 82.77% of the instant coffee market share in 2025; premium lines are poised to accelerate at 7.28% CAGR to 2031.

- By packaging format, jars dominated with a 58.45% share in 2025, yet sachets are projected to expand at a 6.04% CAGR during 2026-2031.

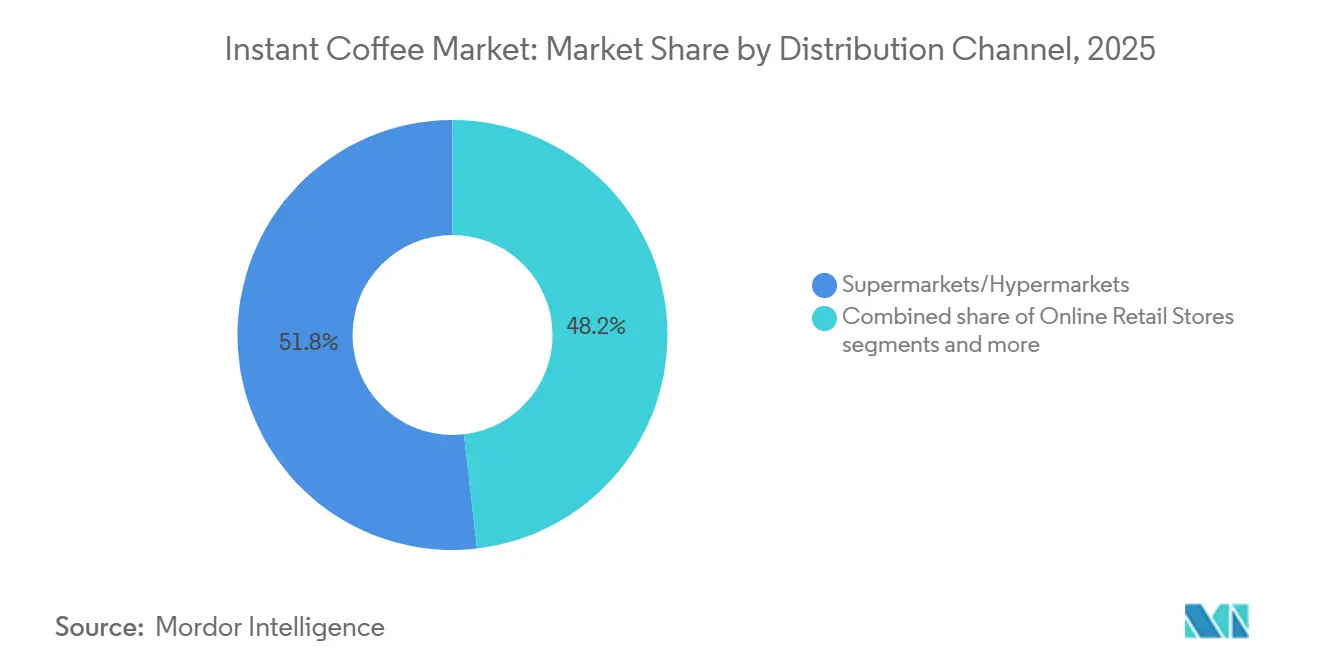

- By distribution channel, supermarkets and hypermarkets captured 51.82% revenue in 2025, whereas online retail is on track for a 6.78% CAGR to 2031.

- By geography, Asia-Pacific commanded 38.36% of 2025 sales, while South America will post the highest 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Instant Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium single-origin instant coffee | +1.8% | North America, Europe, Urban Asia-Pacific | Medium term (2-4 years) |

| Technological advances in freeze-drying | +1.5% | Global, with concentration in Japan, Europe, North America | Medium term (2-4 years) |

| Increasing penetration of ready-to-mix coffee for on-the-go consumption | +1.2% | Global, with emphasis on urban centers across all regions | Short term (≤ 2 years) |

| Strategic capacity expansion by soluble coffee exporters | +0.9% | South America, Southeast Asia, with global market impact | Long term (≥ 4 years) |

| Expansion of retail channels and e-commerce platforms improves product accessibility | +0.7% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Growing café culture influences at-home coffee consumption habits | +0.6% | Urban centers globally, particularly Asia-Pacific and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium Single-Origin Instant Coffee

The premium single-origin segment is fundamentally restructuring the global instant coffee market through substantial shifts in consumer preferences and market dynamics. Market analysis demonstrates a pronounced transition toward traceable, high-quality products with distinctive flavor characteristics, indicating a significant evolution in instant coffee purchasing behavior. This transformation is particularly evident among younger demographic segments, with the National Coffee Association reporting an increase in specialty coffee consumption since 2020, reaching 46% of American adults by January 2025[1]Source: National Coffee Association, "National Coffee Data Trends", ncausa.org. Consumer willingness to pay premiums for traceable, single-origin instant coffee is redefining value propositions across the category. Craft instant-coffee brands such as Swift Cup Coffee partner with approximately 150 specialty roasters to produce small-batch powders sourced from Colombia, Papua New Guinea, and Ethiopia, retailing at six-packs above USD 15 and per-cup prices exceeding USD 2.50, a multiple of 3 to 4 times conventional instant formats.

Technological Advances in Freeze-Drying

Technological advancements are driving the global instant coffee market's growth, especially as consumers increasingly favor convenience and café-style experiences at home. A prime example is Nestlé’s June 2025 launch of freeze-dried, cold-soluble coffee products, including Nescafé Ice Roast and Nescafé Espresso Concentrate. These products cater to the rising demand for cold coffee formats among Gen Z and millennial consumers. Nestlé, utilizing patented freeze-drying and nitrogen-infusion technology, ensures flavor integrity and solubility in cold liquids, an innovation that addresses a major limitation of traditional instant coffee. Supporting this trend, data from the United States Department of Agriculture indicates that in 2024/25, premium green coffee constituted over 60% of China’s coffee imports, surpassing traditional soluble coffee consumption[2]Source: United States Department of Agriculture, "China’s Expanding Coffee Consumption", usda.gov . This shift highlights a global coffee culture transformation, with consumers, particularly in emerging markets, leaning towards higher-quality, origin-specific, and freshly brewed experiences. GEA Group introduced enzymatic-hydrolysis extraction, achieving 65 to 80% yield from green beans, paired with aroma-recovery loops that capture and reintroduce volatile esters post-drying. Purdue University researchers patented gas-hydrate foaming techniques that nucleate ice crystals uniformly, minimizing cell-wall rupture and improving reconstitution speed. These innovations lower the capital-intensity gap between spray-drying and freeze-drying, enabling mid-tier brands to offer freeze-dried formats without prohibitive upfront investment.

Increasing Penetration of Ready-to-Mix Coffee for On-the-Go Consumption

Urbanization and compressed morning routines are driving sachet and stick-pack adoption, particularly in Asia-Pacific markets where 3-in-1 instant-coffee mixes combine coffee, creamer, and sugar in single-serve formats. Video-commerce platforms in Southeast Asia identified 3-in-1 coffee as a hero product, with gross merchandise value multiplying 2.5 times since 2023, as influencers demonstrate preparation in 15-second clips. China's app-driven coffee ordering surged by more than 4 million bags annually, with 80% of orders placed via mobile applications that integrate instant-coffee subscriptions and loyalty rewards. India's instant-coffee consumption rose to 91,000 metric tonnes in 2023, propelled by office-vending machines and railway-station kiosks stocking single-serve sachets. The US Food and Drug Administration's caffeine regulations under 21 CFR 182.1180 and food-additive standards in Parts 170, 172, and 173 ensure that ready-to-mix formats meet safety thresholds, facilitating cross-border trade.

Strategic Capacity Expansion by Soluble Coffee Exporters

Brazil's position as the largest soluble-coffee exporter, shipping 420,000 bags in December 2024 and 977,605 bags from January to March 2025, with spray-dried formats comprising 71.5% and freeze-dried 23%, anchors global supply chains, according to the International Coffee Organization and the Brazilian Coffee Industry Association. ofi's May 2025 inauguration of a dual-line soluble facility in Linhares, employing 300 staff and powered by 100% renewable electricity, strengthens its top-3 independent-producer ranking and secures Rainforest Alliance certification. Nestlé's USD 89 million incremental investment in Brazil's instant-coffee operations in May 2025 underscores a bet on long-term arabica recovery and conilon-robusta substitution. These expansions occur as the European Union Deforestation Regulation compels exporters to document zero-deforestation sourcing, raising compliance costs but differentiating certified volumes in premium channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-induced yield volatility raising costs | -1.2% | Global, with severe impact in Brazil, Vietnam, Colombia | Medium term (2-4 years) |

| Presence of substitutes hampering market growth | -0.8% | North America, Europe, Urban Asia-Pacific | Long term (≥ 4 years) |

| Competition from specialty coffee shops | -0.6% | Urban centers globally, particularly developed markets | Medium term (2-4 years) |

| Supply chain disruptions | -0.5% | Global, with higher impact on import-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-Induced Yield Volatility Raising Costs

Climate change disruptions in coffee production economics pose significant operational challenges for the instant coffee market. Extreme weather events have led to notable price volatility across the value chain, influencing both production costs and market balance. The Food and Agriculture Organization reported that adverse weather in key producing nations led to a 38.8% spike in coffee prices in 2024[3]Source: Food and Agriculture Organization, "Adverse climatic conditions drive coffee prices to highest level in years", fao.org. This surge was particularly pronounced in Arabica prices, which jumped by 58%. Meanwhile, Robusta prices, crucial for instant coffee production, saw an even steeper rise of 70%. These price increases have a cascading effect on the entire value chain, from raw material procurement to final product pricing, making it difficult for manufacturers to absorb costs without impacting profitability. Additionally, supply chain uncertainties, such as delays in transportation, disruptions in sourcing raw materials, and logistical inefficiencies, further exacerbate the challenges. Production capacity limitations, driven by both resource constraints and increased operational costs, add another layer of complexity. Furthermore, manufacturers face difficulties in forecasting demand accurately due to fluctuating prices and inconsistent supply, which can lead to overproduction or underproduction. Together, these factors create considerable hurdles for instant coffee producers striving to maintain consistent output, ensure product availability, and sustain competitive market positioning in the instant coffee market.

Health Concerns Over Added Sugar and Additives

Instant-coffee formulations, especially 3-in-1 mixes, typically contain 8 to 12 grams of sugar per sachet, contributing 32 to 48 kilocalories and raising glycemic-index concerns among diabetic and pre-diabetic populations. The European Food Safety Authority's calls for data on gluconate additives and the European Union's acrylamide benchmark of 850 micrograms per kilogram for soluble coffee reflect regulatory pressure to minimize process contaminants. Median acrylamide levels in instant coffee measured 589 micrograms per kilogram, below the benchmark, yet hydroxymethylfurfural concentrations reached 2,890 milligrams per kilogram, prompting reformulation efforts to reduce Maillard-reaction byproducts. Clean-label trends are driving launches of organic, decaffeinated, and additive-free instant powders; brands such as TrueStart and Nescafé introduced decaf instant lines in 2024, while functional blends incorporating adaptogens, collagen, and nootropics target wellness-oriented consumers. The Belgian Superior Health Council's advisory limiting caffeine intake to 2.5 milligrams per kilogram per day for children and 5.7 milligrams per kilogram per day for adults constrains marketing to younger demographics, narrowing the addressable base for high-caffeine instant formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavored Variants Narrow the Gap

Unflavored instant coffee commands 85.01% of the market share in 2025, establishing itself as the foundation of the instant coffee industry through its versatility and broad consumer acceptance. The segment's dominance is reflected in traditional coffee markets like Brazil, where the United States Department of Agriculture (USDA) forecasts total coffee production for marketing year 2025/26 (July-June) at 65 million bags (60 kilograms per bag) green bean equivalent, representing a 0.5% increase from the 2024/2025. The flavored instant coffee segment is expected to grow at a CAGR of 7.62% from 2026 to 2031, as manufacturers respond to evolving consumer preferences, particularly among younger demographics seeking diverse taste experiences.

The growth in flavored instant coffee reflects changing consumer tastes. Products including vanilla, caramel, hazelnut, mocha, and seasonal variants provide alternatives to conventional coffee offerings. These options particularly resonate with younger consumers who demonstrate increased interest in experimenting with flavor combinations. The range of choices enables instant coffee to reach consumers beyond traditional coffee drinkers. Manufacturers are creating new flavor profiles that blend traditional coffee characteristics with flavored beverages to increase market penetration in the instant coffee market. The segment's growth is supported by advances in flavor encapsulation technologies that better preserve aromas during the drying process, resulting in more authentic flavors that rival fresh-brewed coffee.

By Production Technology: Freeze-Dried Quality Challenges Spray-Dried Dominance

Spray-dried instant coffee held a 63.52% share in 2025, reflecting entrenched capital bases and operational familiarity among large-scale producers. Freeze-dried formats grow at 6.33% CAGR through 2031, driven by patents that reduce cycle times and energy consumption while preserving volatile aromatics. Nestlé's rapid freeze-drying patents halve processing duration, and GEA's enzymatic-hydrolysis extraction achieves 65 to 80% yield from green beans, paired with aroma-recovery systems that reintroduce volatile esters post-drying. Purdue University's gas-hydrate foaming technique nucleates ice crystals uniformly, minimizing cell-wall rupture and improving reconstitution speed, lowering the quality gap between freeze-dried and spray-dried outputs.

Brazil's soluble-coffee exports from January to March 2025 comprised 71.5% spray-dried and 23% freeze-dried formats, illustrating spray-drying's cost advantage in high-volume channels. However, freeze-dried instant commands 30 to 50% price premiums in retail, justifying the higher capital and energy outlays for brands targeting premium tiers. Food Empire Holdings' USD 80 million freeze-dried plant in Vietnam, scheduled for early-2028 completion, will serve Asian markets where freeze-dried instant penetration remains low, presenting a whitespace opportunity. The International Organization for Standardization's quality benchmarks, extraction yield between 18 and 22%, chlorogenic-acid retention, and acrylamide below 850 micrograms per kilogram, are increasingly met by freeze-dried processes, supporting regulatory compliance.

By Price: Premium Tier Expands Despite Inflation

Mass-priced instant coffee accounted for 82.77% of 2025 sales, anchored by supermarket private labels and legacy brands offering 100-gram jars below USD 5. Premium instant coffee grows at a 7.28% CAGR through 2031, fueled by single-origin sourcing, freeze-dried processing, and sustainable-packaging narratives. Swift Cup Coffee's six-packs retail above USD 15, targeting consumers who view instant coffee as a travel or office convenience rather than a daily staple.

Mainstream players are launching premium sub-brands to capture this segment: Starbucks markets 100%-arabica instant sachets featuring Pike Place, Veranda Blend, and Caffè Verona roasts, while Illy offers a 100%-arabica instant powder blending 9 single-origin qualities. The European Union Deforestation Regulation, threatening USD 2.4 billion in Brazilian coffee exports, compels premium brands to document farm-level traceability, inadvertently elevating the narrative appeal and justifying price premiums.

By Distribution Channel: E-commerce Disrupts Traditional Retail Dominance

Supermarkets and hypermarkets accounted for 51.82% of 2025 sales, leveraging shelf visibility, promotional end-caps, and private-label competition to anchor instant-coffee distribution. Online retail grows at a 6.78% CAGR through 2031, propelled by subscription models, direct-to-consumer brands, and marketplace partnerships. The US Census Bureau recorded continued growth in e-commerce sales in the third quarter of 2025. China's app-driven coffee ordering surged by more than 4 million bags annually, with 80% of orders placed via mobile applications integrating instant-coffee subscriptions and loyalty rewards.

Convenience and grocery stores, specialty stores, and other channels collectively serve niche and impulse-purchase occasions. Specialty stores curate craft instant brands such as Swift Cup Coffee and Cometeer, offering tasting notes and brewing guidance that supermarkets cannot replicate. Convenience stores in Colombia and Peru, including OXXO, Exito Express, and TAMBO, expanded footprints in 2024 and 2025, stocking single-serve sachets for commuters and students. Online retail's growth compels incumbents to optimize logistics for smaller, frequent shipments and to invest in augmented-reality packaging that educates consumers on brewing techniques and origin stories, differentiating digital shelf presence from brick-and-mortar commodity displays.

By Packaging Format: Convenience Drives Sachet Growth Despite Jar Dominance

Jars held a 58.45% share in 2025, preferred by multi-person households and institutional buyers seeking bulk convenience and lower per-gram costs. Sachets grow at 6.04% CAGR through 2031, driven by single-person households, on-the-go consumption, and portion control. India's instant-coffee consumption rose from 84,000 metric tonnes in 2012 to 91,000 metric tonnes in 2023, with office-vending machines and railway-station kiosks stocking single-serve sachets, according to the USDA Foreign Agricultural Service. Pouches and other formats occupy the middle ground, offering resealable functionality and premium aesthetics.

Sustainability pressures are reshaping packaging strategies. JDE Peet's rolled out home-recyclable paper refill packs containing more than 85% fiber for Kenco, Douwe Egberts, and L'OR in January 2024, achieving a 97% packaging-weight reduction versus 200-gram glass jars and a 15-month shelf life. Amcor's AmFiber Performance Paper pouch, certified kerbside recyclable by Cepi and Aticelca, delivers a 73% carbon-footprint reduction versus polyethylene-aluminum-polyethylene laminates and potential extended-producer-responsibility fee reductions of 70 to 90%. Nestlé's June 2025 packaging rules mandate mono-polyethylene or mono-polypropylene for flexible formats, stickpacks, sachets, doypacks, eliminating polyvinyl chloride, polyvinylidene chloride, polystyrene, and expanded polystyrene to maximize recycled content.

Geography Analysis

Asia-Pacific holds a 38.36% share of the instant coffee market in 2025, driven by rapid urbanization, rising disposable incomes, and evolving coffee cultures. According to the United States Department of Agriculture (USDA), Chinese consumers used approximately 5.8 million 60-kilogram bags of coffee between 2023 and 2024. The Chinese market has shifted toward higher-quality green coffee, which now represents over 60% of imports. In India, coffee consumption exceeded one million 60-kilogram bags between 2023 and 2024, as reported by the United States Department of Agriculture (USDA).

South America is experiencing the fastest regional growth at 7.22% CAGR (2026-2031), with Brazil transitioning from a traditional producer to a major consumer market. According to Brazil's National Supply Company, coffee production reached 58.81 million 60-kilogram bags in 2024, increasing from 55.07 million bags in 2023. The region's expansion stems from rising domestic consumption, capacity expansions, and increased focus on value-added processing.

North America and Europe maintain stable market positions with established coffee cultures. The National Coffee Association indicates that 66% of American adults consume coffee daily, averaging 3 cups per person. Household instant coffee ownership increased from 27% in 2020 to 35% in 2025. The Middle East and Africa, while holding a smaller market share, demonstrate growth potential through developing coffee cultures and increasing urbanization in the instant coffee industry.

Mordor Intelligence provides coverage of the instant coffee market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The instant-coffee sector exhibits moderate fragmentation, as regional specialists and craft entrants challenge multinational portfolios. Keurig Dr Pepper's USD 18 billion acquisition of JDE Peet's, announced in August 2025 and slated for separation by the end of 2026, will create a Global Coffee Company with USD 15.9 billion in last-twelve-months net sales, approximately USD 400 million in cost synergies over 3 years, and a USD 4 billion pod-manufacturing joint venture with Apollo and KKR providing USD 7 billion in financing. This consolidation reshapes procurement leverage, innovation pipelines, and geographic footprints, yet leaves room for nimble players exploiting premiumization and sustainability niches.

Patent activity underscores technology as a competitive wedge: Nestlé's rapid freeze-drying and membrane-filtration patents, GEA's enzymatic-hydrolysis extraction achieving 65 to 80% yield, and Purdue University's gas-hydrate foaming technique collectively reduce cycle times, energy consumption, and quality gaps between spray-dried and freeze-dried outputs. Opportunities cluster around craft instant coffee, functional blends, and sustainable packaging. Brands such as Swift Cup Coffee, partnering with approximately 150 specialty roasters, and Cometeer, employing liquid-nitrogen flash-freezing for frozen pucks priced between USD 2 and USD 4 per serving, demonstrate that premiumization can coexist with instant formats when provenance, processing transparency, and sensory quality align.

Functional instant-coffee blends incorporating adaptogens, collagen, and nootropics target wellness-oriented consumers, while decaffeinated instant lines from TrueStart and Nescafé address caffeine-sensitive demographics. Packaging innovation - including JDE Peet's home-recyclable paper refill packs, Nestlé's mono-polyethylene sachets, and Amcor's AmFiber Performance Paper pouch - differentiates brands in sustainability-conscious markets and reduces extended-producer-responsibility fees by 70 to 90%. Emerging disruptors such as Sleepy Owl Coffee in India and Blueberry Agro leverage direct-to-consumer channels and regional sourcing to undercut multinational pricing while emphasizing traceability narratives that resonate with millennial and Generation Z cohorts.

Instant Coffee Industry Leaders

-

Nestle S.A.

-

J.M. Smucker Company

-

Kraft Heinz Company

-

Luigi Lavazza S.p.A.

-

JDE Peet's N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and new hubs are expanding the addressable supply base for both spray-dried and freeze-dried instant coffee, and they are also shifting manufacturing closer to robusta-growing origins and fast-growing consumption markets. In Asia, Nestle announced a CHF 563 million investment in July 2026 to build an AI-enabled Nescafe manufacturing and distribution hub in Samut Prakan, Thailand, for soluble coffee and coffee mixes. This facility is positioned to add a large regional platform for scale, speed-to-market, and SKU complexity.

Vietnam is also seeing deeper origin-side value-add. Trung Nguyen Legend announced an USD 83.6 million instant-coffee manufacturing complex expansion in Dak Lak in June 2026, while Vintage Coffee and Beverages increased capacity by 4,500 MTPA in March 2026 at its Telangana facility, indicating ongoing investment in contract manufacturing and private-label capable output. Opportunities are clustering around compliance-driven quality improvements and cost-out initiatives as green-coffee price volatility and safety benchmarks tighten. EFSA issued a positive scientific opinion in January 2026 for Kerry Group's Acrylerase enzyme for reducing acrylamide in coffee extracts, which gives manufacturers a clearer route to reduce process contaminants while maintaining flavor, particularly for premium and export-oriented instant formats. At the plant level, Nestle reported a EUR 900,000 energy-optimization project at its Girona, Spain coffee plant in March 2026, including heat recovery, highlighting how efficiency upgrades can help protect margins when input costs rise and support sustainability-led procurement requirements across key retail and institutional channels.

Recent Industry Developments

- July 2026: Nestle announced a CHF 563 million investment to build an AI-enabled Nescafe manufacturing and distribution hub in Samut Prakan, Thailand, for soluble coffee and coffee mixes. The project adds a large-scale Southeast Asia production base built around automation and data-driven operations. It strengthens supply resilience and supports faster innovation cycles for regional instant and mix portfolios.

- April 2026: Keurig Dr Pepper finalized the acquisition of 96.22% of JDE Peet's N.V. shares and advanced plans for a future independent Global Coffee Co. The move consolidates major coffee brand portfolios and procurement scale under a new corporate structure. It raises the competitive bar for instant coffee innovation and route-to-market coordination across regions.

- May 2024: Nestle disclosed plans to invest USD 196 million in Brazil by 2026 to expand Nescafe capacity and related capabilities. The investment links instant coffee growth to origin-country processing and strengthens access to robusta-heavy supply for soluble formats. It also supports export competitiveness from Brazil amid tighter global green-coffee availability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers packaged instant coffee sold for quick preparation, where soluble coffee is made to dissolve in hot or cold water or milk and is purchased for home, office, and food-service use. Values are tracked at the manufacturer selling price level across major global regions.

Scope exclusions: ready-to-drink coffee, coffee concentrates, and single-serve pod systems are excluded from this sizing.

Segmentation Overview

-

Product Type

- Flavored

- Unflavored

-

Production Technology

- Spray-Dried Instant Coffee

- Freeze-Dried Instant Coffee

-

Price

- Mass

- Premium

-

Packaging Format

- Sachets

- Pouches

- Jars

-

Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail

- Other Distribution Channels

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear demand and supply map for instant coffee, and then aligning it with what is measurable in public data. We refer to official and non-paywalled sources such as UN Comtrade trade statistics, FAOSTAT agriculture data, USDA coffee outlooks, International Coffee Organization publications, and national customs and statistical agencies where coffee extracts and preparations are reported.

These references are paired with company filings, annual reports, investor presentations, and trusted press coverage to understand capacity moves, pricing direction, and distribution shifts. In a few cases, we also use paid database subscriptions for company financials and intelligence, news and financials, and shipment-level import and export checks to validate trade flows and normalize unusual spikes. The examples listed above are illustrative, and they are not exhaustive because other public sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk sources cannot fully explain, especially around channel mix, price realization, and how spray-dried and freeze-dried products are positioned in different countries. We spoke with a mix of manufacturers, ingredient suppliers, packaging participants, distributors, and retail and food-service linked stakeholders across APAC, EMEA, and the Americas. Respondent input was then used to confirm assumptions and close gaps before finalizing estimates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 21% | APAC: 49% |

| Mid tier: 50% | Functional/Unit leaders: 27% | EMEA: 29% |

| Smaller Players: 22% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where production, trade, and consumption indicators are reconstructed into an addressable value pool for instant coffee, and then split across regions and channels based on validated shares. Where the data trail becomes thin, the model is checked with selective bottom-up approximations such as sampled price points by pack type, pack size mapping, and volume-to-value conversions using practical average selling price ranges.

Key inputs used in the model include green coffee availability and price direction, trade flows for coffee extracts and preparations, penetration of instant coffee in at-home versus out-of-home consumption, pack format shifts (sachets versus jars and pouches), premiumization signals reflected in freeze-dried demand, and currency movements in large importing countries. Forecasts are formed using scenario analysis, where demand drivers and price trends are varied within realistic ranges, then aligned to what interviewees expect in their markets. When bottom-up checks suggest missing coverage in smaller channels, the gap is handled through calibrated uplift factors that stay consistent with trade and consumption signals.

Data Validation & Update Cycle

Outputs are validated through stepwise checks, starting with internal consistency across regions, then comparing implied per capita consumption and trade intensity against independent public indicators. We review outliers like sudden jumps in value that are not supported by pricing, volume, or policy signals, and then re-check assumptions with follow-up outreach when variances remain unclear.

Before sign-off, the full model and key assumptions are reviewed by another analyst to reduce avoidable errors. The same definitions are applied across regions to keep the basis consistent. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major price shocks, trade disruptions, or notable capacity expansions. Right before delivery, the latest data is re-scanned so clients receive the most current view available at that time.

Mordor Intelligence's Instant Coffee Market Size Compared With Other Published Estimates

Published market sizes for instant coffee can look far apart even when they use the same label, because included products, price layers, and timing assumptions are not always consistent. Differences also come from whether values are captured at manufacturer selling price or closer to retail, and how exchange rates and inflation are applied across regions.

Ready-to-drink coffee sits outside Mordor Intelligence's scope, and that exclusion can create a wide gap versus figures that mix instant coffee with bottled and canned coffee beverages. Some published estimates also appear to use retail value with higher channel markups, or they apply a faster price progression without checking it against observable trade values for coffee extracts and preparations. Another driver is refresh cadence, where older base years get carried forward even after commodity and packaging cost changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.57 B (2026) | |

| Global Consultancy A | USD 84.61 B (2025) | This figure appears closer to a retail-value view and can also reflect broader coffee beverage inclusion, which increases totals through channel markups and adjacent category overlap. |

| Industry Publisher B | USD 37.90 B (2025) | The base year and horizon differ, and the long-range build suggests a trend-led extrapolation that can under-use trade-based cross-checks when splitting by region and channel. |

The table suggests that product scope and the pricing layer used are the largest reasons numbers move apart, and base-year timing then adds a second level of spread. By anchoring assumptions to public trade signals and consumption checks, we keep the steps repeatable and the totals explainable when updates are made.

Key Questions Answered in the Report

How large will global demand for soluble coffee become by 2031?

The instant coffee market size is forecast to reach USD 51.18 billion by 2031 at a 5.82% CAGR.

Which production technology is growing fastest?

Freeze-dried instant coffee is projected to expand at 6.33% CAGR through 2031, outpacing spray-dried formats thanks to patent-enabled quality and energy gains.

What drives premiumization in soluble coffee?

Single-origin sourcing, freeze-dry processing, and traceability regulations such as the EU Deforestation Regulation have lifted consumer willingness to pay 30%-50% price premiums.

Which region will post the highest growth rate?

South America is set to record the fastest 7.22% CAGR between 2026 and 2031 amid retail modernization and capacity expansion in Brazil and its neighbors.

Page last updated on: