Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

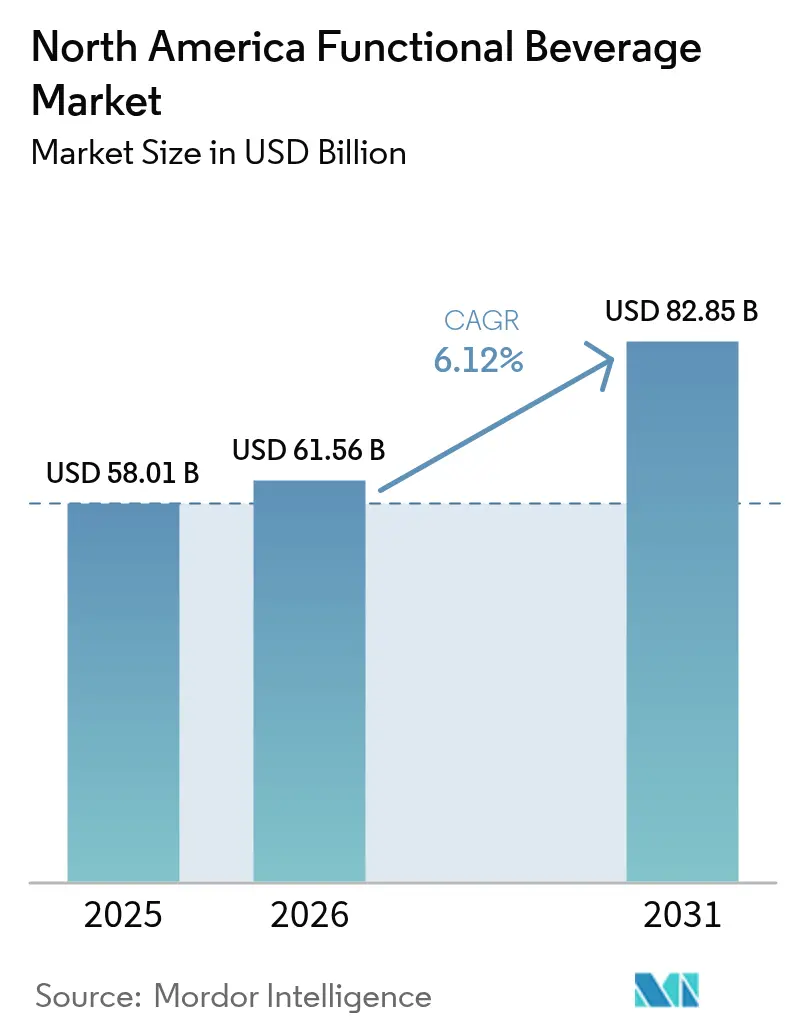

| Base Year Market Size (2025) | USD 58.01 Billion |

| Market Size (2026) | USD 61.56 Billion |

| Market Size (2031) | USD 82.85 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

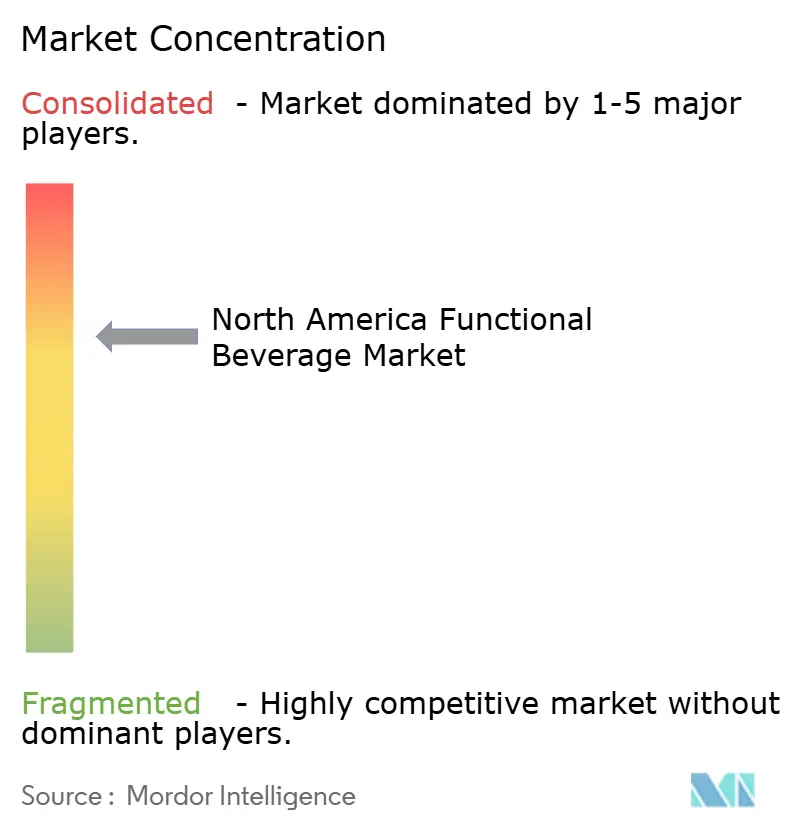

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Functional Beverage Market Analysis by Mordor Intelligence

The North American functional beverages market size was valued at USD 58.01 billion in 2025 and estimated to grow from USD 61.56 billion in 2026 to reach USD 82.85 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). The market expansion is attributed to heightened consumer health consciousness, increased demand for immunity-enhancing ingredients, and the proliferation of sports and fitness activities that necessitate hydration and energy-supplementing beverages. Market development is facilitated by innovations in beverage formulations, the introduction of reduced and zero-sugar variants, and the increasing adoption of plant-based alternatives. The robust sports and fitness industry in North America continues to generate substantial demand for sports beverages, protein-enriched drinks, and enhanced water products. The expansion of e-commerce platforms has enhanced consumer accessibility to functional beverages, incorporating subscription-based purchasing options.

Key Report Takeaways

- By Product Type – Energy drinks led with 33.22% revenue share in 2025, while fermented drinks are projected to post the fastest 8.24% CAGR through 2031.

- By Packaging Type – PET and glass bottles captured 47.85% share in 2025; cans are growing the quickest at 6.98% CAGR to 2031.

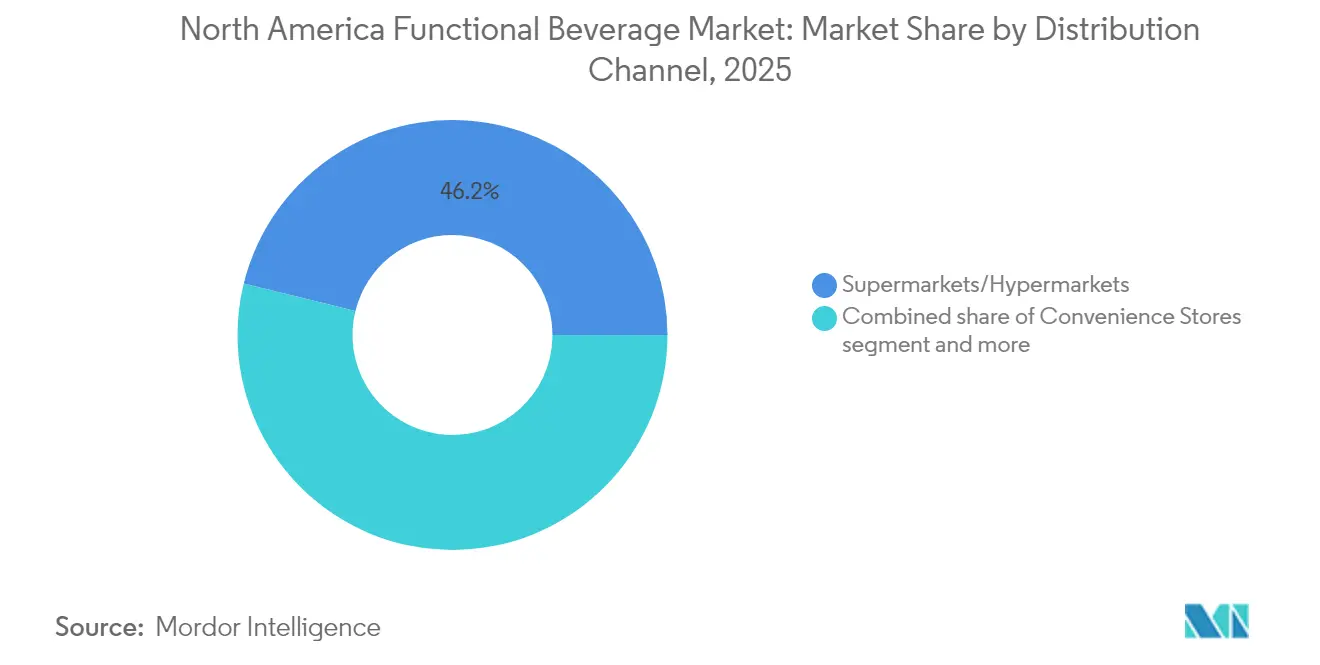

- By Distribution Channel – Supermarkets and hypermarkets held 46.15% share in 2025, whereas online retailers are advancing at a 8.93% CAGR through 2031.

- By Geography – The United States commanded 73.65% of the 2025 value; Mexico is forecast to record a 5.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Functional Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-conscious consumer base and immunity focus | +1.2% | North America, Strongest in the States urban markets | Medium term (2-4 years) |

| Sports and fitness culture expansion | +0.8% | North America, concentrated in United States and Canada | Long term (≥ 4 years) |

| Product reformulation toward low/no-sugar variants | +0.9% | United States and Canada, emerging in Mexico | Short term (≤ 2 years) |

| Rising popularity of plant-based beverages | +0.7% | United States and Canada, with limited Mexico penetration | Long term (≥ 4 years) |

| Convenience and On-the-Go lifestyles | +1.1% | North America, urban centers across region | Medium term (2-4 years) |

| Premiumization and lifestyle positioning | +0.6% | United States premium markets, expanding to Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health-conscious consumer base and immunity focus

The North American functional beverages market demonstrates significant expansion, primarily attributed to the increasing prevalence of health-conscious consumers and heightened emphasis on immunological well-being. Contemporary consumers exhibit enhanced knowledge regarding health maintenance and actively pursue products that deliver supplementary nutritional advantages beyond fundamental hydration requirements. The amplified focus on immune system enhancement, particularly in response to recent global health developments, has generated substantial demand for functional beverages incorporating essential vitamins, minerals, antioxidants, and probiotic components. This transformation in consumer preferences has necessitated manufacturers to develop products that align with the requirements of wellness-oriented consumers seeking efficient health solutions. The market has additionally witnessed strategic involvement from prominent personalities, exemplified by Lionel Messi's introduction of Más+ by Messi, a specialized hydration beverage for the Canadian market, in July 2024.

Sports and Fitness Culture Expansion

The North American functional beverages market is experiencing significant growth driven by the expanding sports and fitness culture. As health and wellness awareness increases, more consumers participate in physical activities and fitness programs, creating higher demand for beverages that support hydration, energy, muscle recovery, and performance enhancement. Sports drinks and performance nutrition beverages have become essential for athletes, fitness enthusiasts, and active lifestyle consumers. The growth in fitness infrastructure further strengthens this trend. According to Canada Statistics, the number of fitness and recreational sports centers in Canada increased from 9,290 in December 2022 to 9,493 in June 2023 [1]Source: Statistics Canada, "Working out the numbers for your gym resolution", www.statcan.gc.ca. This expansion in fitness facilities creates a larger base of active consumers who incorporate functional beverages into their health and exercise routines. The increasing number of fitness centers provides functional beverage companies with opportunities to reach and expand their consumer base, contributing to overall market growth.

Product reformulation toward low/no-sugar variants

The North America functional beverages market demonstrates substantial growth propelled by systematic product reformulation toward low- and no-sugar variants. Consumer awareness regarding the adverse health implications of excessive sugar consumption, specifically obesity, diabetes, and metabolic disorders, has generated increased demand for nutritionally optimized beverage alternatives. Beverage manufacturers have implemented strategic formulation changes, incorporating low-calorie sweeteners and natural alternatives, including stevia and monk fruit, to maintain organoleptic properties while reducing sugar content. The introduction of GURU Organic Energy Corp's Zero Sugar line in the United States in September 2024 exemplifies this market transformation. Additionally, according to the International Food Information Council (IFIC) survey in 2024, 37% of United States respondents consider low in sugar a primary indicator of healthy food choices [2]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey", https://ific.org. This consumer preference has prompted manufacturers to develop reformulation strategies aligned with these evolving health requirements.

Rising popularity of plant-based beverages

TThe North America functional beverages market is experiencing growth driven by increasing consumer preference for plant-based beverages. This trend stems from heightened health awareness, increased recognition of lactose intolerance, adoption of vegan and flexitarian diets, and growing environmental consciousness. Consumers seek products with specific nutritional advantages, including reduced cholesterol, lower caloric content, and added plant proteins. Food and beverage companies are responding through substantial investments in product development, nutrient fortification, and flavor enhancement. For instance, in May 2024, Lactalis entered the Canadian market with a new plant-based beverage line offering eight grams of pea protein per 250 ml serving. This product launch demonstrates the industry's response to consumer demand for nutritious, sustainable, and protein-rich plant-based beverages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory compliance | -0.8% | United States and Canada, emerging Mexico requirements | Short term (≤ 2 years) |

| Intense market competition | -1.1% | North America, particularly concentrated in the United States | Medium term (2-4 years) |

| Supply chain and ingredient sourcing challenges | -0.9% | North America, acute in specialty ingredients | Long term (≥ 4 years) |

| Shelf life and stability issues | -0.6% | North America, critical for natural formulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance

Regulatory compliance requirements significantly constrain the North American functional beverages market. The complex regulatory environment governing ingredient safety, labeling, health claims, and manufacturing processes creates substantial challenges for beverage manufacturers. For instance, in 2024, the United States Food and Drug Administration (FDA) revised the definition and labeling guidelines for the term healthy, affecting how functional beverage companies communicate their nutritional benefits. Meeting these regulations requires extensive documentation, testing, and formula modifications, which increases production costs and extends product launch timelines. The regulatory burden particularly affects smaller and emerging brands, which must allocate significant resources to meet compliance standards. These requirements limit market innovation and product diversity while strengthening the position of established companies with existing regulatory expertise and established supply chains.

Intense Market Competition

The North American functional beverages market faces constraints due to market saturation in core energy drink segments, leading to heightened competition. Established brands defend their market positions through aggressive pricing and promotional activities, resulting in reduced profit margins across the category. The increasing number of functional beverage brands has created intense competition for retail shelf space, benefiting companies with robust distribution networks and substantial marketing resources. This market environment presents challenges for new brands attempting to secure retail presence, despite offering innovative products. The competitive intensity is reflected in the 2024 volume performance of category leaders, with Monster reporting a 1.9% decline and Red Bull experiencing a 3.8% decrease. These results indicate that established market leaders face pressure from emerging competitors such as Celsius and wellness-focused brands, which attract consumers through distinct offerings centered on health benefits, natural ingredients, and specialized functionalities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Energy Drinks Lead Despite Fermented Growth Surge

Energy drinks held a market share of 33.22% in 2025, driven by consumer demand for products that enhance physical and mental performance. The growth stems from busy lifestyles, increasing fitness awareness, and the widespread need for convenient energy sources during work and exercise routines. According to Glanbia Nutritionals, in 2024, 7% of United States functional beverage consumers started using energy drinks, while 26% of existing users increased their consumption frequency. These patterns demonstrate heightened consumer acceptance of energy drinks as reliable sources for sustained energy boosts, mental focus enhancement, and improved athletic performance, reinforcing their strong market dominance.

Fermented drinks are projected to grow at a CAGR of 8.24% through 2031, driven by increased consumer awareness of probiotic benefits for gut health. These beverages are gaining significant popularity for their immune system support, enhanced nutrient absorption, and comprehensive health benefits. The growing demand for fermented drinks like kombucha, kefir, and probiotic-rich beverages stems from consumers seeking functional beverages that support microbiome balance, reduce inflammation, and improve digestive health. The segment's growth is further strengthened by consumer preference for natural, clean-label products, increased focus on preventive health through functional nutrition, and the rising adoption of traditional fermentation practices in modern wellness routines.

By Packaging Type: Sustainability Drives Can Innovation

PET and glass bottles maintained a 47.85% market share in 2025, driving significant growth in the functional beverages market through their distinct material properties and consumer preferences. Glass packaging demonstrates substantial market presence among health-conscious consumers due to its superior preservation capabilities for functional ingredients, which accelerates premium segment expansion in the functional beverages sector. PET bottles drive operational efficiency in functional beverage distribution through substantial cost advantages and enhanced logistics performance due to their reduced weight characteristics. Both packaging materials drive market competitiveness in the functional beverages industry by facilitating optimal product visibility and enabling manufacturers to establish distinct market positioning in retail environments.

The cans segment is projected to achieve a CAGR of 6.98% through 2031. The segment's growth is primarily attributed to the inherent advantages of cans, including their portability, storage efficiency, and resealable characteristics, which align with modern consumption patterns. The recyclability and reduced environmental footprint of aluminum cans, in comparison to plastic packaging alternatives, have garnered significant attention from environmentally conscious consumers. Manufacturing advancements in the can industry, specifically in lightweighting technology and digital printing capabilities, have enhanced both the aesthetic value and production efficiency, thereby increasing their utilization among functional beverage manufacturers.

By Distribution Channel: Digital Commerce Reshapes Retail Landscape

Supermarkets and hypermarkets held a commanding 46.15% share of the North America functional beverages market in 2025, making them the largest distribution channel in the region. This dominance stems from their broad reach and convenience, as consumers prefer one-stop shopping with diverse functional beverage options available under one roof. These retail formats utilize their extensive shelf space to showcase multiple brands across various categories, including energy drinks, sports drinks, and fortified waters. Supermarkets and hypermarkets also drive sales through marketing campaigns, price promotions, and loyalty programs that encourage repeat purchases and brand exploration.

Online retail channels in the North American functional beverages market are expected to grow at a CAGR of 8.93% through 2031. This growth stems from consumers' increasing preference for convenience, wider smartphone and internet adoption, and greater acceptance of e-commerce for regular shopping. Online platforms provide easy product browsing, personalized recommendations, subscription options, and home delivery services, catering to health-conscious consumers with busy schedules. The United States Census Bureau reported that retail e-commerce sales in the second quarter of 2025 reached USD 304.2 billion, an increase of 1.4% from the first quarter of 2025, indicating a continued shift toward online purchasing .

Geography Analysis

The United States maintains a dominant position with 73.65% market share in the North American functional beverages market as of 2025. Metropolitan centers, including New York, Los Angeles, and Chicago, function as primary testing locations for innovative functional beverage formulations and marketing initiatives before national distribution. These urban markets present optimal conditions through their concentration of health-conscious consumers and sophisticated distribution infrastructure, enabling efficient product commercialization.

The Canadian market operates under Health Canada's comprehensive regulatory framework for supplemented foods, which governs product formulation and marketing parameters. The province of Quebec demonstrates distinctive consumer preferences that influence beverage product development and market positioning, whereas western provinces exhibit increased receptivity to premium-priced functional beverages corresponding to wellness-oriented lifestyle preferences. These regional market variations necessitate specifically tailored strategic approaches that address local consumer behavior patterns and regulatory requirements.

Mexico demonstrates superior market growth in the North American functional beverages segment, achieving a compound annual growth rate of 5.21% through 2031. This market expansion is attributed to increasing middle-class purchasing capacity, accelerated urbanization, and regulatory modifications that facilitate market entry for international beverage manufacturers. Additional North American territories, while representing smaller individual markets, contribute to aggregate regional growth through established cross-border trade mechanisms and tourism-driven consumption patterns.

Competitive Landscape

The North American functional beverages market shows moderate consolidation, with major beverage companies acquiring wellness brands to target health-conscious consumer segments. Companies like PepsiCo Inc., The Coca-Cola Company, Monster Beverage Corporation, Danone S.A., and Nestlé S.A. expand their portfolios through acquisitions and product development to maintain market positions.

Companies differentiate themselves through continuous product innovation and new flavor launches to address changing consumer preferences. Red Bull's March 2025 launch of its first United States Spring Edition energy drink with Grapefruit & Blossom flavor demonstrates how brands use seasonal offerings to generate consumer interest and drive sales.

The market offers expansion opportunities in personalized nutrition, sustainable packaging, and demographic-specific products targeting seniors, athletes, and health-conscious consumers. However, strict regulatory requirements for health claims and ingredient standards create significant barriers. Distribution access remains challenging for new entrants, giving established companies with existing infrastructure and retail networks a competitive advantage.

North America Functional Beverage Industry Leaders

-

PepsiCo Inc.

-

The Coca-Cola Company

-

Monster Beverage Corporation

-

Danone S.A.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: O'Neill Vintners & Distillers has launched its energy drinks brand in the United States. The product contains 120mg of caffeine and zero sugar per 35.5cl can. The range includes six flavors: Citrus Spark, Fruit Fusion, Grapefruit Frost, Orange Dream, PomPower, and SuperBerry.

- May 2025: Danone expanded its Oikos brand beyond dairy products with the introduction of Oikos Protein Shakes, a ready-to-drink, shelf-stable beverage line containing 30g of protein per bottle.

- October 2024: STōK Cold Brew Coffee introduced STōK Cold Brew Energy, which combines cold brew coffee with caffeine, B-vitamins, ginseng, and guarana to enhance focus and energy.

- July 2024: Tim Hortons launched energy drinks in Canada under the brand name Infusr. The beverages are available in two flavors: Blackberry Yuzu and Mango Starfruit. Each can contains 80 mg of caffeine.

North America Functional Beverage Market Report Scope

A functional beverage is classified as a conventional liquid food marketed to convey product ingredients or supposed health benefits.

The North American functional beverage market is segmented by type, distribution channel, and geography. Based on type, the market is segmented into energy drinks, sports drinks, fortified juice, dairy and dairy alternative beverage, and other types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, drug stores and pharmacies, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into the United States, Canada, Mexico, and the Rest of North America.

For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Energy Drinks |

| Sports Drinks |

| Fortified Juices |

| Electrolyte Drinks |

| Fermented Drinks |

| Protein-Based Drinks |

| Others |

By Packaging Type

| PET/Glass Bottles |

| Cans |

| Tetra Packs |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retailers |

| Other Distribution Channel |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Energy Drinks |

| Sports Drinks | |

| Fortified Juices | |

| Electrolyte Drinks | |

| Fermented Drinks | |

| Protein-Based Drinks | |

| Others | |

| By Packaging Type | PET/Glass Bottles |

| Cans | |

| Tetra Packs | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retailers | |

| Other Distribution Channel | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the projected value of the North America functional beverages market by 2031?

The market is forecast to reach USD 82.85 billion by 2031.

Which product category currently holds the largest share?

Energy drinks lead with 33.22% share of 2025 revenue.

Which segment is growing the fastest through 2031?

Fermented drinks are set to register the quickest 8.24% CAGR through 2031.

How quickly is the online channel expanding?

Online retailers are advancing at a 8.93% CAGR between 2026 and 2031.

Page last updated on: