Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

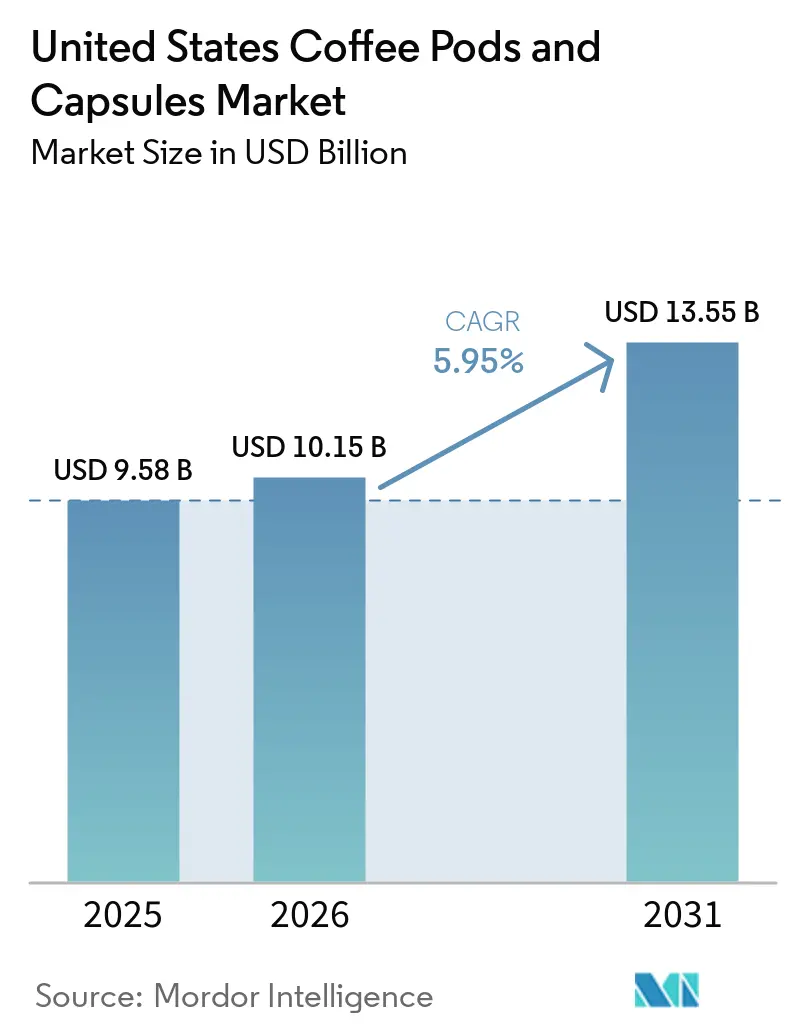

| Base Year Market Size (2025) | USD 9.58 Billion |

| Market Size (2026) | USD 10.15 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

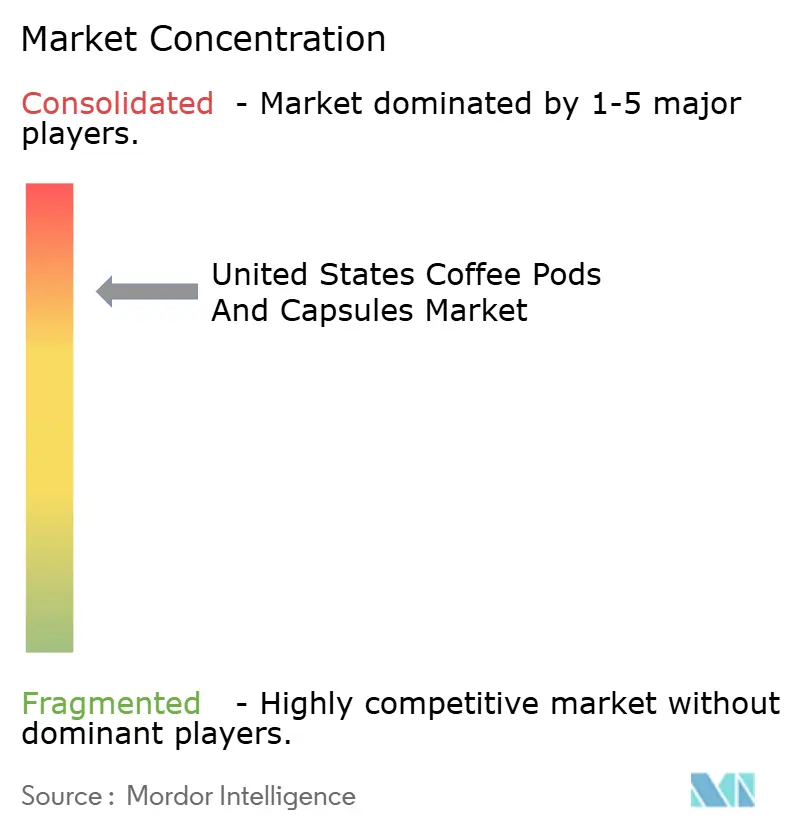

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Coffee Pods and Capsules Market Analysis by Mordor Intelligence

The United States coffee pods and capsules market size was valued at USD 9.58 billion in 2025 and estimated to grow from USD 10.15 billion in 2026 to reach USD 13.55 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031). Convenience remains the primary purchase driver, yet regulatory scrutiny and consumer concern over single-use waste are pushing material innovation and product redesign. Leading brands have begun repositioning portfolios around compostable formats, premium single-origin SKUs, and connected brewing systems that automate replenishment. Moreover, premiumization is widening the average selling price gap as households trade up for specialty flavors, organic certification, and IoT-enabled brewers that simplify ordering. Competitive intensity is also rising as sustainability-focused entrants target niches underserved by the incumbents, while large retailers tighten shelf-space allocations in favor of demonstrably circular solutions.

Key Report Takeaways

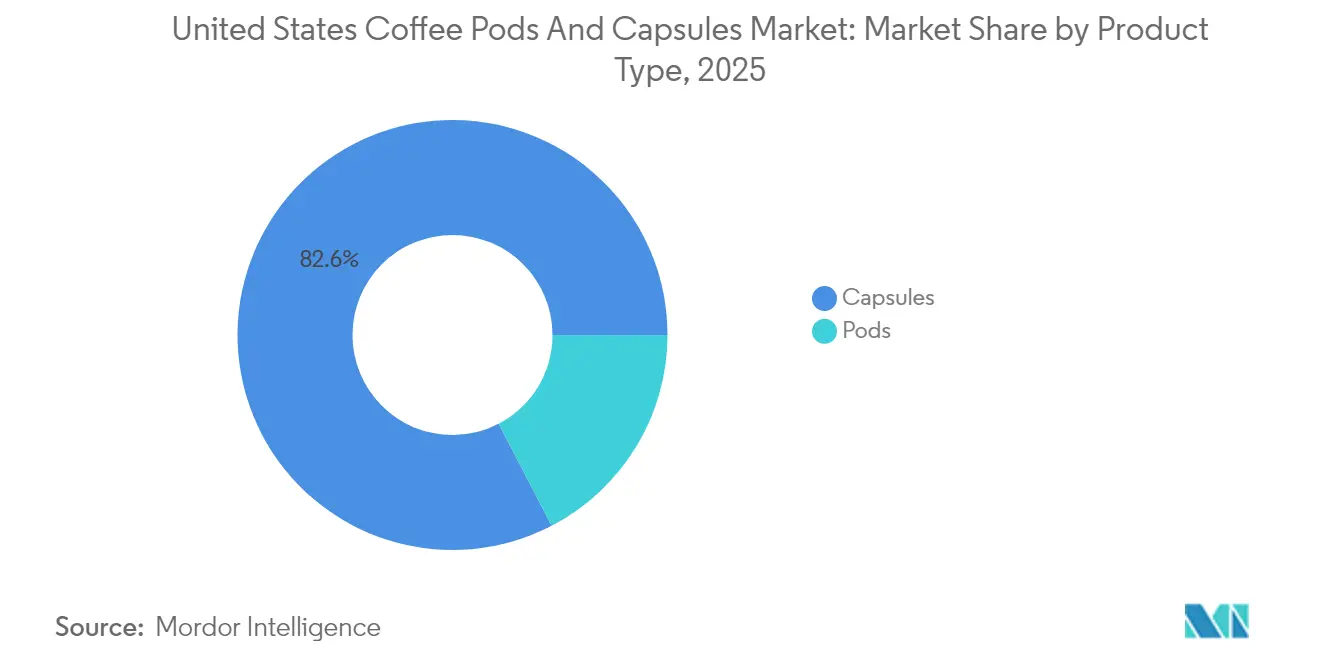

- By product type, capsules led with an 82.63% revenue share in 2025, whereas pods are projected to expand at a 7.85% CAGR through 2031.

- By flavor, plain coffee commanded 72.05% in 2025; flavored variants are set to increase at a 7.43% CAGR.

- By packaging material, plastic retained a 45.88% share in 2025; compostable/biodegradable formats are advancing at a 6.95% CAGR.

- By coffee roast, medium roast accounted for 50.74% of the coffee pods and capsules market size in 2025; light roast is expected to rise at a 7.08% CAGR.

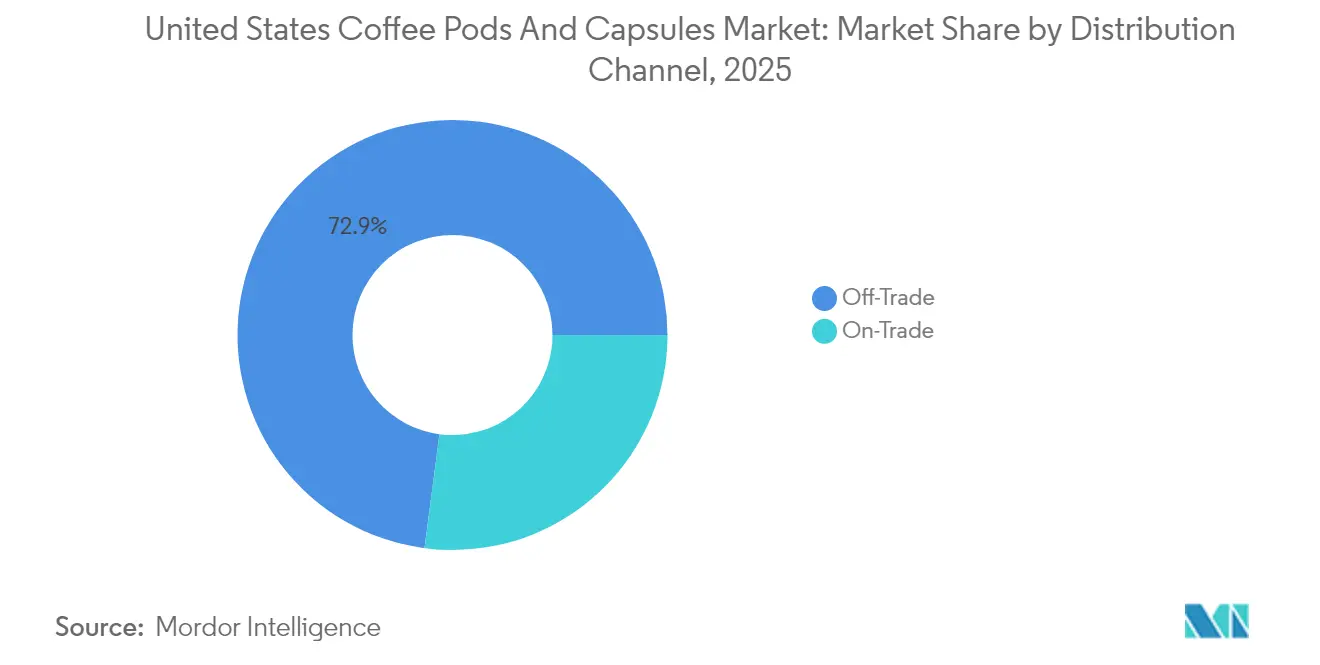

- By distribution channel, off-trade captured 72.92% of the coffee pods and capsules market share in 2025, while on-trade is forecast to grow at a 7.56% CAGR through 2031.

- By source, conventional beans maintained a 75.83% share in 2025; single-origin and organic specialty coffee is projected to climb at a 7.7% CAGR.

- By geography, the South region held a 36.14% share in 2025; the West region is poised for the fastest growth at 6.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Coffee Pods and Capsules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for convenient single-serve coffee in households | +1.2% | National, with strongest adoption in Northeast and West regions | Medium term (2-4 years) |

| Expanding availability of specialty and premium pods/capsules | +1.0% | National, with early gains in West and Northeast markets | Medium term (2-4 years) |

| Introduction of new flavors, fortified options, and enhanced functionalities | +0.8% | National, with flavor innovation concentrated in South and Midwest | Short term (≤ 2 years) |

| Advancements in eco-friendly product solutions | +1.1% | National, driven by regulatory pressure in West and Northeast | Long term (≥ 4 years) |

| Marketing strategies and promotional efforts for coffee pods and capsules | +0.6% | National, with celebrity partnerships driving youth engagement | Short term (≤ 2 years) |

| Emergence of IoT-connected brewers enabling data-driven replenishment | +0.4% | West and Northeast regions, expanding to urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for convenient single-serve coffee in households

The coffee market shows a significant shift toward single-serve options, with 66% of Americans consuming coffee daily and single-cup brewing systems representing 42% of brewing preferences, according to the Spring 2025 National Coffee Data Trends report [1]Source: National Coffee Association (NCA), "More Americans drink coffee each day than any other beverage, bottled water back in second place", ncausa.org. The convenience of single-serve pods has effectively bridged the gap between home brewing and coffee shop quality, as evidenced by consistent weekly out-of-home coffee purchases among consumers. Besides, Americans consume 516 million cups of coffee daily, with pod-based systems steadily replacing traditional drip brewing methods. Also, the FDA's recent classification permitting coffee with less than 5 calories to be labeled as "healthy" is expected to increase demand for low-calorie coffee pod varieties. Major companies, including Keurig Dr Pepper, Nestlé's Nespresso, and Starbucks, have responded to this trend by developing pods that offer diverse flavors and sustainable options. The expanded availability of coffee pods through online and retail channels has improved consumer access to various options for quality home brewing. This accessibility, combined with consumer preferences for health-conscious and sustainable products, continues to drive the growth of the coffee pods and capsules market.

Expanding availability of specialty and premium pods/capsules

Premium and specialty coffee pods and capsules have become essential offerings in the market, evolving beyond niche segments. The Specialty Coffee Association's 2024 National Coffee Data Trends report indicates that 45% of Americans consumed specialty coffee in the past week, demonstrating substantial market demand [2]Source: Specialty Coffee Association, "2024 National Coffee Data Trends Specialty Coffee Breakout Report Now Available", sca.coffee. Premium offerings now encompass single-origin certifications, organic compliance, and functional ingredients, enabling higher profit margins. The implementation of the USDA's Strengthening Organic Enforcement Rule in March 2024 has enhanced premium coffee positioning through improved organic certification guidelines and supply chain verification. Millennials significantly influence this market transformation, with more than two-thirds of consumers aged 18-34 preferring single-serve ready-to-drink coffee and demonstrating willingness to pay more for sustainable options. Market innovation is evident in strategic partnerships, such as Nespresso's collaboration with Oatly to produce Barista Edition coffee pods in 2025. Companies like Illy, Lavazza, and Peet's Coffee have expanded their specialty capsule offerings to meet consumer demand for ethically sourced, distinctive coffees in convenient formats. Hence, the U.S. specialty coffee market continues to grow, prompting retailers and producers to increase their premium pods and capsules offerings. This focus on quality and sustainability drives market expansion and product innovation in the coffee pod segment.

Introduction of new flavors, fortified options, and enhanced functionalities

Brands in the United States coffee pods and capsules market are driving innovation through the introduction of new flavors, fortified options, and enhanced functionalities. Moving beyond traditional seasonal flavors, companies are focusing on functional offerings that align with evolving consumer health and taste preferences. A prime example is Eggo Coffee's launch in August 2024, in collaboration with Two Rivers Coffee Company. These pods feature five waffle-inspired flavors: Blueberry, Chocolate Chip, Cinnamon Toast, Maple Syrup, and Vanilla. By combining nostalgic waffle tastes with premium coffee, these profiles aim to expand coffee's appeal, particularly during breakfast. Similarly, OGI Coffee's Kona Cherry Blend, infused with chaga mushrooms, highlights the growing demand for functional coffee, catering to consumers seeking cognitive and health benefits. The FDA's GRAS Notice No. 868 authorizes the use of up to 300mg of coffee fruit extract per serving, enabling the development of antioxidant-rich formulations and reinforcing the industry's focus on health-centric beverages. Additionally, innovations like Xpod's reusable coffee pods, which allow the use of any coffee beans, merge customization with environmental sustainability. These advancements are broadening the flavor and functional spectrum of coffee pods, attracting a more health-conscious and environmentally aware consumer base while enhancing the appeal of single-serve coffee in the United States.

Advancements in eco-friendly product solutions

Environmental sustainability has become a core operational requirement in coffee pods and capsules manufacturing, driving significant advancements in eco-friendly product development. Recent material science developments have enabled the production of viable compostable pods, including NatureWorks and IMA's KEYGEA pods manufactured from Ingeo™ PLA biopolymer for industrial composting while maintaining brewing standards. Nespresso demonstrated this progress by introducing home-compostable capsules composed of 82% paper pulp with a biodegradable polymer lining at Milan Design Week 2024. These capsules maintain coffee quality and aroma preservation while meeting both home and industrial composting certifications through specialized manufacturing processes. This development aligns with increasing regulations, such as the EU's Packaging and Packaging Waste Regulation, requiring compostability within 24 months, and the ISO 59010:2024 framework promoting circular business models. In the United States, Extended Producer Responsibility legislation requires manufacturers to financially account for packaging disposal, driving sustainable product development. Thus, premium coffee brands are incorporating environmental considerations into their product development while maintaining quality standards, reflecting market requirements for both sustainability and performance in the coffee pods and capsules market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns over single-use waste | -0.9% | National, with strongest regulatory pressure in West and Northeast | Medium term (2-4 years) |

| Compatibility issues impacting consumer choice | -0.6% | National, with proprietary systems limiting switching | Long term (≥ 4 years) |

| Volatility with raw material sourcing or distribution | -0.7% | National, with supply chain concentration in Brazil and Vietnam | Short term (≤ 2 years) |

| High cost compared to bulk/brewed options | -0.5% | National, with price sensitivity highest in Midwest and South | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental concerns over single-use waste

Environmental concerns regarding single-use coffee pod waste have transformed into regulatory and corporate accountability challenges in the coffee pods and capsules market. In 2024, the U.S. Securities and Exchange Commission (SEC) imposed a USD 1.5 million fine on Keurig Dr Pepper for misleading statements about K-Cup pod recyclability. The SEC determined that Keurig's annual reports for fiscal years 2019 and 2020 claimed effective pod recyclability while omitting that major recycling companies had questioned the feasibility of curbside recycling for these pods and would not accept them. Moreover, Extended Producer Responsibility (EPR) laws in Oregon, Colorado, California, Minnesota, and Maine now require manufacturers to fund packaging disposal, affecting the economic model of single-use pods. These regulations create compliance costs that impact smaller manufacturers and require industry-wide investment in sustainable alternatives, despite their higher production costs. The combination of strict regulations and increased environmental awareness compels coffee pod manufacturers to develop sustainable solutions that remain commercially viable. This shift highlights the importance of accurate environmental reporting and the need to improve packaging design and disposal methods to reduce the environmental impact of single-use coffee systems.

Compatibility issues impacting consumer choice

Proprietary brewing systems create artificial barriers in the coffee pods and capsules market, limiting consumer choice while ensuring recurring revenue for manufacturers. Keurig's 2.0 system demonstrates this through its pod recognition technology, which displays "Oops!" messages when detecting non-Keurig pods, preventing the use of third-party products. This approach restricts consumers to Keurig-branded pods and limits market opportunities for other manufacturers. The lack of standardization among major platforms, including Keurig, Nespresso, and other systems, requires consumers to commit to specific device-pod combinations. This limitation reduces market flexibility and creates entry barriers for companies with new product offerings. The current market structure impedes price competition and innovation by constraining consumers within closed ecosystems rather than allowing selection based on quality or preference. The growing consumer demand for flexible brewing options has created tension between manufacturers' proprietary systems and users' expectations for compatibility. This market dynamic challenges the industry to balance manufacturer control with consumer choice to ensure continued market development in the coffee pods and capsules segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Capsules Dominate Despite Pod Innovation

Capsules hold 82.63% market share in 2025, as consumers value their consistent brewing performance and flavor preservation capabilities through sealed aluminum and plastic designs. Pods are growing at an 7.85% CAGR through 2031, driven by developments like Keurig's K-Round compostable pods and reusable pod systems that combine environmental responsibility with convenience. This growth pattern indicates environmental concerns' influence on product development, with capsule manufacturers focusing on compostable materials and pod makers advancing material science solutions. Recent innovations like Nespresso's paper pulp capsules and FLO Group's KEYGEA compostable pods show both segments moving toward sustainable options.

Competition between capsules and pods now focuses on brewing system compatibility and environmental performance rather than convenience alone. Capsules maintain advantages through established distribution networks and consumer familiarity. Pods offer market entry opportunities for third-party manufacturers without requiring proprietary system development. Products like Xpod, which allow users to create reusable pods with any coffee beans, indicate pods may gain market share through customization options that capsule systems cannot match. ISO 18606:2013 organic recycling standards influence material selection in both segments, creating regulatory alignment that may reduce capsules' traditional technical advantages.

By Flavor: Plain Coffee Maintains Dominance Amid Flavor Innovation

In 2025, plain coffee holds a dominant 72.05% market share, reflecting a strong consumer preference for traditional coffee values that emphasize bean quality and expert roasting over artificial flavors. Meanwhile, flavored coffees are on a growth trajectory, expanding at a 7.43% CAGR through 2031. This growth is driven by brand collaborations and the integration of functional ingredients, creating differentiated offerings that go beyond conventional coffee profiles. Notable innovations, such as Eggo Coffee's five waffle-inspired flavors and Nespresso's partnership with Oatly Barista, demonstrate how manufacturers are leveraging familiar taste profiles to extend coffee consumption occasions beyond traditional moments.

Flavor innovations are increasingly combining taste with functional benefits. For example, OGI Coffee's chaga mushroom-infused Kona Cherry Blend targets health-conscious consumers by offering cognitive enhancement alongside traditional caffeine benefits. The FDA's GRAS approval for coffee fruit extract (up to 300mg per serving) enables manufacturers to introduce antioxidant-rich formulations that align with wellness trends and command premium pricing. Besides, seasonal offerings, such as Dunkin's limited-edition S'mores, create urgency and collectibility, driving repeat purchases while allowing manufacturers to test market acceptance for potential permanent flavors. Data from the National Coffee Association identifies vanilla and mocha as the most popular flavored options, providing manufacturers with insights to balance innovation with proven consumer preferences.

By Packaging Material: Sustainability Drives Material Innovation

In 2025, plastic remains a dominant force in the packaging material landscape, capturing a 45.88% market share. However, compostable and biodegradable alternatives are gaining traction, with a projected CAGR of 6.95% through 2031. This growth underscores the increasing importance of sustainable materials as regulatory pressures and evolving consumer preferences challenge manufacturers reliant on conventional packaging. The EU's Packaging and Packaging Waste Regulation, which enforces compostability within 24 months, has driven significant investments in material science across the industry. Aluminum packaging continues to hold a premium position due to its superior barrier properties and robust recycling infrastructure, while advancements such as NatureWorks' Ingeo™ PLA biopolymer technology are enabling compostable alternatives to achieve comparable performance.

Extended Producer Responsibility laws in states like Oregon, Colorado, California, Minnesota, and Maine are transforming packaging economics by requiring manufacturers to assume financial responsibility for disposal costs. These regulations create direct economic incentives for sustainable design. ISO 59020:2024 provides a standardized framework for assessing circularity performance in packaging, while ISO 59010:2024 offers guidance for transitioning to circular business models. Collaborative efforts are also facilitating this shift. For example, NatureWorks and IMA's compostable pod system demonstrates how supply chain partnerships enable smaller manufacturers to adopt sustainable packaging solutions without significant capital investments. Additionally, W&H Group's recyclable coffee stand-up pouch, featuring only 2% EVOH content while exceeding recycling standards, exemplifies how innovation is driving sustainability without compromising barrier performance.

By Coffee Roast: Medium Roast Leadership Faces Light Roast Growth

Medium roast coffee holds a leading 50.74% market share in 2025, reflecting consumer preferences for balanced flavor profiles that optimize acidity and body while avoiding the bitterness associated with darker roasts. Light roast coffee is experiencing the fastest growth, with a 7.08% CAGR projected through 2031. This growth is driven by specialty coffee trends emphasizing origin characteristics and the increasing sophistication of consumer palates seeking nuanced flavor experiences. This pattern aligns with the broader premiumization trend, where consumers are willing to pay premium prices for products offering distinctive sensory experiences and artisanal appeal.

The shift toward lighter roasts is closely tied to the expansion of single-origin and organic specialty coffee, which represents the fastest-growing source category with a 7.7% CAGR. Dark roast coffee maintains a stable but declining share as consumer preferences shift from traditional diner-style coffee to more complex flavor profiles that highlight terroir and processing methods. Research from the Specialty Coffee Association in 2024 indicates that 45% of Americans consumed specialty coffee in the past week, demonstrating that roast preferences are increasingly shaped by education and exposure to high-quality coffee experiences. While regulatory compliance factors have minimal impact on roast segmentation, USDA organic certification requirements influence sourcing decisions, indirectly affecting roast profile optimization for certified products.

By Distribution Channel: Off-Trade Dominance Amid On-Trade Recovery

Off-trade channels dominate with a 72.92% market share in 2025, underscoring the convenience of single-serve systems that let consumers enjoy coffeehouse experiences at home or in the office. Meanwhile, on-trade channels are witnessing a robust expansion, growing at a 7.56% CAGR through 2031. This growth is fueled by foodservice operators who are not only seeking premium pricing through differentiated offerings but are also looking to cut down on labor costs typically associated with traditional espresso preparation. The surge in on-trade channels is a testament to the post-pandemic rebound in foodservice consumption. Moreover, sectors like hospitality, healthcare, and corporate environments are increasingly adopting single-serve systems, prioritizing consistency and speed over artisanal preparation methods.

Partnerships between manufacturers and foodservice distributors play a pivotal role in this on-trade expansion. These collaborations offer turnkey solutions, encompassing equipment, supplies, and maintenance services. A case in point is Keurig Dr Pepper's broadened alliance with Lavazza, highlighting how manufacturers are tapping into established foodservice networks to make inroads into commercial markets. Specialty on-trade applications are on the rise, with hotels and healthcare facilities turning to single-serve systems for both guest and patient services. This shift not only enhances service quality but also opens up revenue streams that are more lucrative than those from traditional retail channels. While off-trade channels continue to thrive, buoyed by the convenience of e-commerce and subscription-based models, they grapple with margin pressures stemming from retail consolidation, especially in conventional grocery outlets.

By Source: Conventional Coffee Leads While Specialty Gains Momentum

In 2025, conventional coffee commands a dominant 75.83% market share. This dominance underscores the cost-sensitive dynamics of single-serve systems, where the dual pressures of packaging and processing costs push for tighter raw material optimization. Meanwhile, the segment encompassing single-origin, organic, and specialty coffee is on a robust growth trajectory, boasting a 7.7% CAGR projected through 2031. This surge is largely fueled by consumers' readiness to pay a premium for products that not only promise traceability and sustainability but also deliver unique flavor experiences. Such trends suggest a market bifurcation: on one side, value-driven conventional products; on the other, premium specialty offerings that leverage their distinctiveness for higher margins.

March 2024 marks the rollout of the USDA's Strengthening Organic Enforcement Rule. This initiative streamlines certification processes, empowering manufacturers to command premium prices for organic goods, all while upholding supply chain integrity . Meanwhile, the National Organic Program's 2025 review has granted a fresh lease on life to 47 substances on the National List, ensuring regulatory clarity for organic coffee processing up to 2030. Specialty coffee is evolving, with an increasing emphasis on functional benefits. For instance, coffee fruit extract formulations, now FDA GRAS Notice No. 868 approved, can tout antioxidant claims, bolstering their premium pricing justification. Partnerships like Planet2050 and the Coffee Impact Collective's insetting program highlight a pivotal shift: sustainability efforts are crafting novel value propositions for specialty coffee, transcending the boundaries of conventional organic certification.

Geography Analysis

The South region holds a dominant 36.14% share of the coffee pods and capsules market in 2025, driven by its large population base and established coffee consumption habits favoring convenience-oriented products. This leadership is further supported by the region's extensive retail infrastructure and distribution networks, enabling efficient product placement across diverse demographic segments. The South's preference for flavored coffee options, particularly vanilla and mocha, aligns with the broader market trend toward flavor innovation, which drives premium pricing and brand differentiation. In contrast, the West region is experiencing the fastest growth, with a 6.65% CAGR through 2031, fueled by higher disposable incomes, environmental consciousness, and early adoption of premium coffee products that command higher margins.

The Northeast region leads in coffee consumption intensity, with 67% of residents consuming coffee daily, according to National Coffee Association data. However, it represents a smaller share of the pods and capsules market due to a stronger preference for traditional brewing methods and artisanal coffee experiences. This region's sophisticated coffee culture creates opportunities for premium single-serve products emphasizing origin characteristics and sustainable sourcing, though price sensitivity remains a barrier to broader market penetration. The Midwest region demonstrates steady demand patterns with moderate growth expectations, reflecting the region's pragmatic approach to coffee consumption, where convenience and value proposition drive purchasing decisions more than premium positioning or environmental considerations.

Regional regulatory dynamics are increasingly shaping market development. Extended Producer Responsibility laws in California, Oregon, and other Western states are introducing compliance costs that manufacturers must incorporate into pricing strategies. The West region's leadership in environmental regulations is driving innovation in sustainable packaging solutions, which may eventually become industry standards as other regions adopt similar frameworks. Demographic trends indicate that millennials in urban centers across all regions are willing to pay premiums for sustainably sourced coffee, with over two-thirds consuming single-serve ready-to-drink options that balance convenience and quality. The emergence of regional partnerships, such as Select Milk Producers' collaboration with Westrock Coffee to build processing facilities in Texas, highlights how geographic proximity to raw materials and processing capabilities influences market development strategies.

Competitive Landscape

Major players, including Keurig Dr Pepper, Nestlé S.A., Kraft Heinz Company, Luigi Lavazza, and JAB Holding Company, dominate the highly consolidated coffee pods and capsules market in the United States. These companies utilize proprietary brewing systems, exclusive retail partnerships, and significant marketing investments to establish high entry barriers and sustain premium pricing by locking consumers into their ecosystems. As environmental regulations become stricter and consumer preferences shift, the competitive focus is moving from convenience to sustainability and premiumization. This trend is driving manufacturers to adopt compostable pods and circular economy models.

Leading companies, such as Keurig Dr Pepper, are shifting from defensive strategies to aggressive innovation. They are introducing next-generation brewing systems and eco-friendly compostable pods to address environmental concerns while maintaining their proprietary advantages. Meanwhile, emerging players like OGI Coffee are identifying white-space opportunities by launching concentrated coffee formats that minimize packaging waste and incorporate health-focused ingredients like chaga mushrooms. These innovations align with the growing consumer demand for sustainable and functionally enhanced products.

Technology adoption is accelerating within the market. IoT-connected brewers enable data-driven replenishment and predictive ordering, providing competitive advantages through deeper consumer behavior insights and recurring revenue streams. Regulatory developments are also shaping the competitive landscape. For instance, in 2024, the SEC imposed a USD 1.5 million fine on Keurig Dr Pepper for misleading recyclability claims. This incident underscores the increasing importance of transparency and compliance as critical competitive differentiators in the market.

United States Coffee Pods and Capsules Industry Leaders

-

Keurig Dr Pepper Inc.

-

Nestlé S.A.

-

JAB Holding Company

-

Luigi Lavazza S.p.A.

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Oatly, the Swedish oat milk company, collaborated with Nespresso, the Nestlé-owned coffee giant, to introduce a limited-edition line of oat milk coffee capsules on a global scale. Nespresso's "Oatly Barista Edition" coffee was launched in over 15 countries, including the UK, the US, China, and Australia. This exclusive blend was made available through Nespresso's official online platforms and boutiques worldwide for a limited period.

- November 2024: Trilliant Food & Nutrition, a prominent vertically integrated coffee manufacturer based in the U.S., announced the launch of its latest product: Victor Allen's High Quality, Premium Coffee Pods. These coffee pods were offered in a 60-count variety pack, designed to be compatible with single-serve pod coffee makers. The pack included 15 pods of each flavorful roast, featuring the Colombia Coffee Blend, Espresso Roast, Mexico Coffee Blend, and Brazil Coffee Blend.

- September 2024: New England Coffee Company, a renowned coffee roaster with over a century of expertise, announced the launch of its BPI-certified, commercially compostable single-serve pods made with plant-based mesh. All single-serve flavors, including popular blends such as Breakfast Blend, Blueberry Cobbler, Carmel Macchiato, Hazelnut Crème, and more, were introduced in the new pod format.

United States Coffee Pods and Capsules Market Report Scope

Pods and capsules are single-portion dosages of coffee. A coffee pod or pad is a pre-packaged dose of ground coffee in a paper filter like a round teabag. Coffee capsules are the same concept as pods in that they are pre-packaged, measured doses of coffee. They are contained within a 'capsule' that, once used, must be disposed of.

The United States coffee pods and capsules market is segmented by type and distribution channel. By type, the market is bifurcated into pods and capsules. Based on distribution channels, the market is segmented into off-trade and on-trade. The off-trade distribution channel is further segmented into supermarkets/hypermarkets, specialty stores, convenience/grocery stores, and online retail stores.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Pods |

| Capsules |

By Flavor

| Plain |

| Flavored |

By Packaging Material

| Aluminum |

| Plastic |

| Compostable/Biodegradable |

By Coffee Roast

| Light Roast |

| Medium Roast |

| Dark Roast |

By Distribution Channel

| Off-Trade | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

By Source

| Conventional |

| Single Origin/Organic/Speciality Coffee |

By Region

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Pods | |

| Capsules | ||

| By Flavor | Plain | |

| Flavored | ||

| By Packaging Material | Aluminum | |

| Plastic | ||

| Compostable/Biodegradable | ||

| By Coffee Roast | Light Roast | |

| Medium Roast | ||

| Dark Roast | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Source | Conventional | |

| Single Origin/Organic/Speciality Coffee | ||

| By Region | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the current value of the U.S. coffee pods and capsules market?

The market is valued at USD 10.15 billion in 2026 and is projected to reach USD 13.55 billion by 2031.

Which product format is growing fastest?

Pod formats are expanding at an 7.85% CAGR thanks to compostable materials and reusable designs.

Which U.S. region is projected to grow the fastest?

The West region is forecast to post a 6.65% CAGR because of higher incomes and strong eco-consciousness.

How significant is sustainability in purchasing decisions?

New regulations and consumer demand are pushing compostable and recyclable packaging, prompting rapid innovation across the supply chain.

Page last updated on: