Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

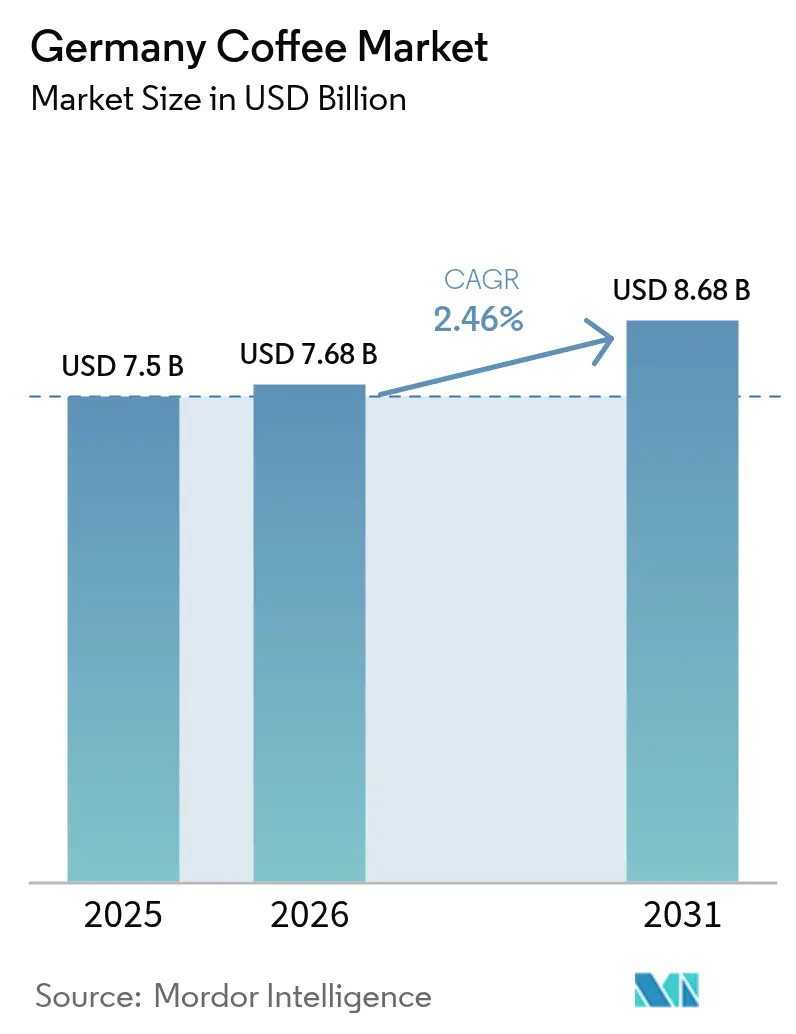

| Base Year Market Size (2025) | USD 7.50 Billion |

| Market Size (2026) | USD 7.68 Billion |

| Market Size (2031) | USD 8.68 Billion |

| Growth Rate (2026 - 2031) | 2.46% CAGR |

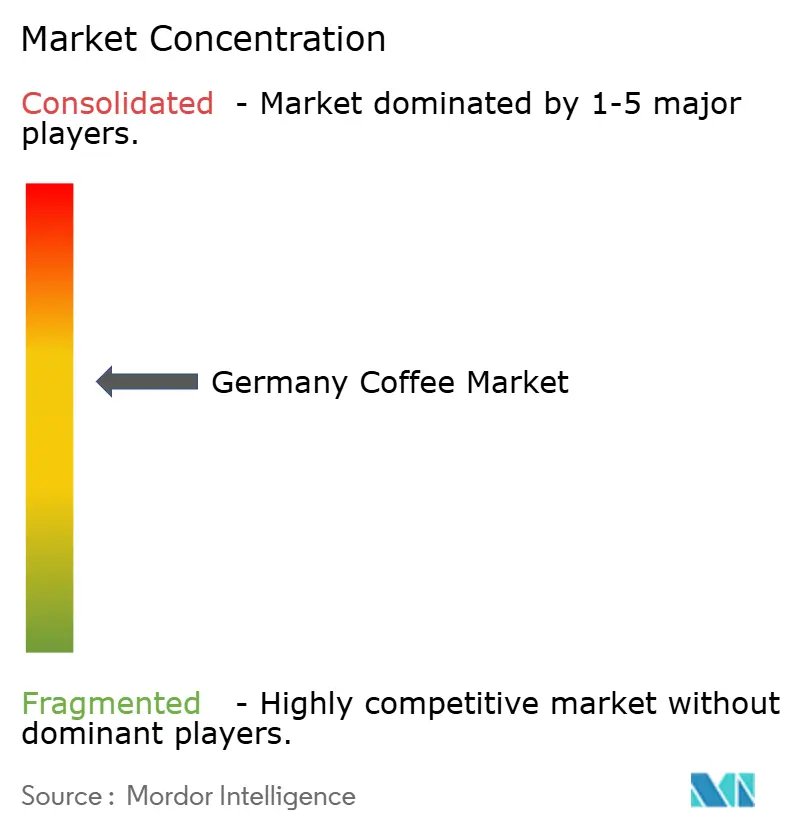

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Coffee Market Analysis by Mordor Intelligence

The German coffee market size was valued at USD 7.50 billion in 2025 and estimated to grow from USD 7.68 billion in 2026 to reach USD 8.68 billion by 2031, at a CAGR of 2.46% during the forecast period (2026-2031). The market is characterized by a strong presence of both domestic and international players, with growth driven by multiple factors, including the rising home-barista trend, specialty coffee shops, and increasing demand for premium coffee varieties. German consumers are increasingly prioritizing quality, origin, and sustainability in their purchasing decisions, leading to higher sales of certified organic and fair-trade coffee products. While traditional coffee remains popular, the market has adapted to include newer brewing methods and formats, particularly coffee pods and capsules. The e-commerce channel has strengthened its position in coffee sales, supported by changing consumer shopping patterns. The out-of-home consumption segment has demonstrated notable recovery in cafes and restaurants across major German cities, complemented by increased investment in coffee roasting facilities and distribution networks. With these diverse market dynamics and evolving consumer preferences, the German coffee market is well-positioned for sustained growth and innovation in the coming years.

Key Report Takeaways

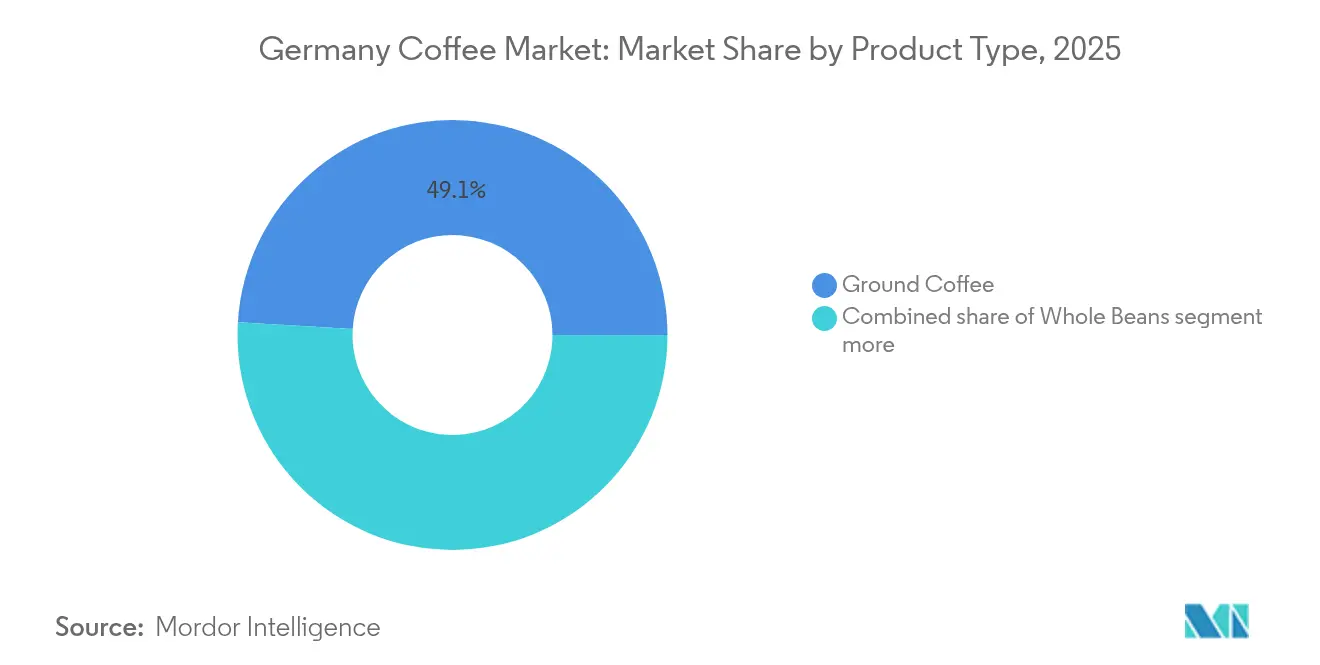

- By product type, ground coffee held the largest 49.05% German Coffee market share in 2025, while whole beans are projected to deliver the fastest 3.55% CAGR nationwide through 2031.

- By type, conventional coffee dominated 84.35% of sales in 2025, yet specialty coffee will post an 8.60% CAGR.

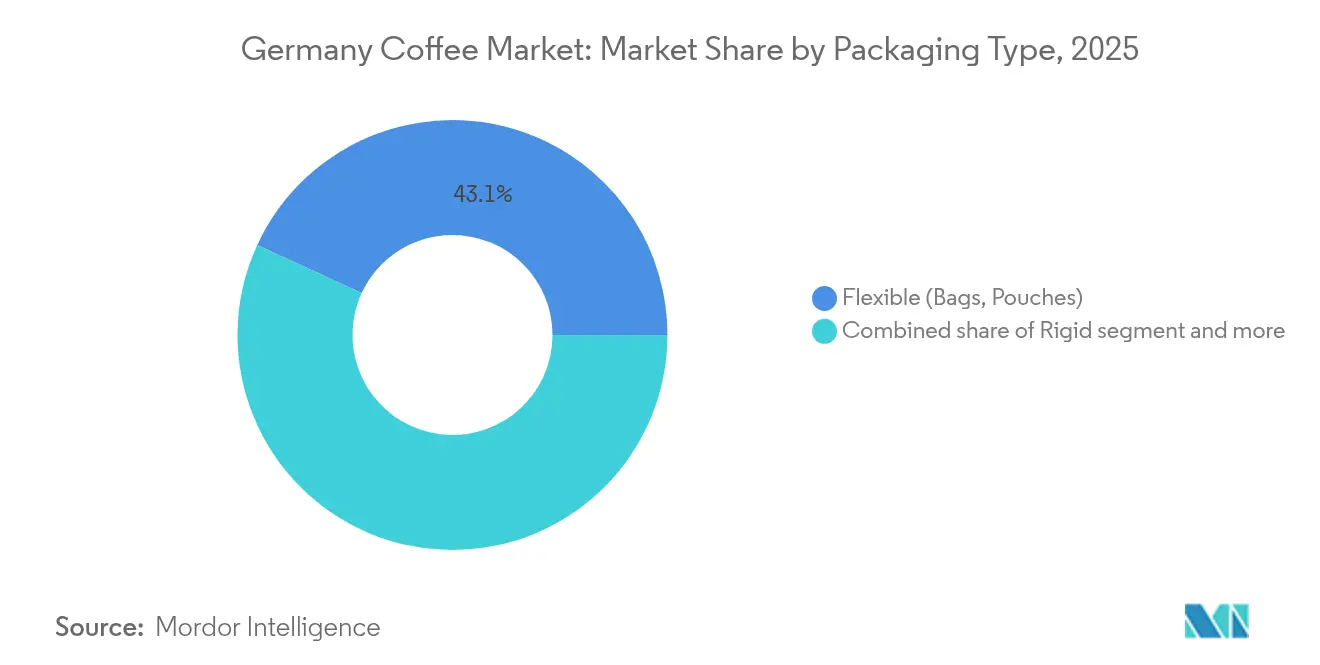

- By packaging, the flexible (bags, pouches) segment captured 43.12% of volume in 2025, but the single-serve segment will lead growth at 3.76% CAGR.

- By distribution channel, off-trade accounted for 73.40% of revenue in 2025; on-trade will expand 2.94% annually, led by urban cafés in Southern Germany.

- By geography, Western Germany retained the top regional position at 29.30% of the German Coffee market size in 2025, while Eastern Germany will grow fastest at 4.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and third-wave coffee boom | +1.2% | Urban clusters in Western and Southern Germany | Medium term (3-4 years) |

| Growth of home-barista equipment boosting whole-bean sales | +0.9% | Nationwide, skewed to affluent households | Medium term (3-4 years) |

| Rising demand for roasted coffee | +0.6% | National, logistics hubs in Hamburg and Bremen | Long term (≥ 5 years) |

| Innovation in coffee brewing methods | +0.5% | Metropolitan centres, spillover to suburbs | Short term (≤ 2 years) |

| Urbanisation and fast-paced lifestyle | +0.4% | All major cities | Long term (≥ 5 years) |

| Growing demand for functional coffee | +0.3% | Early-adopter urban consumers | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and Third-Wave Coffee Boom

The rising trend of premiumization and third-wave coffee culture in Germany, particularly in urban areas, is transforming coffee consumption patterns. German consumers are increasingly seeking high-quality, specialty coffee beans and artisanal brewing methods, moving away from traditional mass-market products. This shift is evident in the proliferation of specialty coffee shops, micro-roasteries, and coffee bars across major cities like Berlin, Hamburg, and Munich. This consumer behavior is supported by rising disposable income and sophisticated taste preferences, with emphasis on coffee origin, sustainable sourcing, and precise brewing methods. The trend is further reinforced by the growing availability of specialty coffee equipment and beans through both physical and online retail channels. Urban consumers demonstrate a strong willingness to pay premium prices for high-quality coffee experiences, with 78% of German coffee drinkers preferring to pay more for organic options, according to the European Ministry of Foreign Affairs[1]Source: European Ministry of Foreign Affairs, "European Market Potential for Speciality Coffee", cbi.eu. In response, major retailers are expanding their specialty offerings, while established companies like Tchibo and Dallmayr are repositioning their premium lines to capture this growing market segment.

Growth of Home-Barista Equipment Boosting Whole-Bean Sales

The increasing popularity of home-brewing equipment, such as espresso machines, grinders, and pour-over devices, has evolved into a sustained trend, with German consumers investing in sophisticated brewing equipment that rivals café quality. This home-barista movement directly drives the growth in whole bean coffee sales as consumers seek fresher, more flavorful brews. Coffee enthusiasts increasingly view brewing as a craft to be mastered rather than a convenience to be outsourced, leading to increased consumer knowledge about coffee brewing techniques and bean quality. The rise in remote work arrangements has further solidified this trend, with consumers prioritizing premium coffee experiences within their homes. Manufacturers are responding with innovations targeting this segment, exemplified by Gruppo Illy's launch of the new X-CAPS capsule system in April 2025. Additionally, the cost savings associated with home brewing compared to daily cafe purchases motivate consumers to invest in quality brewing equipment and whole beans. Coffee enthusiasts also appreciate the flexibility to adjust grind sizes for different brewing methods, contributing to the growing demand for whole bean coffee in the retail segment.

Rising Demand for Roasted Coffee

Consumer preferences for freshly roasted coffee beans have driven significant growth in Germany's roasting industry, leading to the establishment of new facilities and the expansion of existing ones. The country maintains its market dominance through extensive domestic roasting capabilities that enable quick adaptation to these evolving preferences, particularly in specialty and premium coffee segments. Local roasters are experiencing substantial growth by offering customized roasting profiles, artisanal experiences, and craft coffee options. The expansion of coffee shop chains, independent cafes, and direct-to-consumer sales through e-commerce platforms has created a steady demand for roasted coffee beans nationwide. This robust infrastructure enables German roasters to ensure product freshness, maintain quality control, and develop specialized blends for different markets. PROBAT's introduction of the P05 hydrogen roaster demonstrates Germany's technological advancement in the industry, indicating potential growth in coffee bean demand. According to UN Comtrade data, Germany ranks as the second-largest coffee importer globally after the United States, with imports valued at USD 4,121.38 million in 2023[2]Source: UN Comtrade, "Leading Coffee Importing Countries Worldwide in 2023", comtrade.un.org. Germany's combination of large-scale operations and technological innovation enables its roasters to meet the growing consumer demand for fresh, ethically sourced coffee.

Innovation in Coffee Brewing Methods

The coffee brewing methods market in Germany exemplifies the global shift towards diverse and sophisticated preparation techniques, driven by the third-wave coffee culture and increasing consumer interest in artisanal coffee preparation. According to Balance Coffee, German consumers, who drink an average of 3.4 cups per day as of February 2024, have expanded their preferences beyond traditional filter coffee to embrace methods such as cold brew, pour-over, AeroPress, and siphon brewing[3]Source: Balance Coffee, "Coffee Consumption Statistics", balancecoffee.co.uk. This evolution is supported by the growing availability of specialized coffee brewing equipment for home use and the accessibility of brewing knowledge through social media platforms and online tutorials. The market's growth is further characterized by a focus on sustainable brewing methods, including reusable filters and manual brewers, reflecting environmental consciousness among consumers. The integration of coffee into various consumption occasions, including coffee cocktails, has extended its role beyond morning routines, contributing to record per-capita consumption levels in Germany.

Restraints Impact Analysis*

| Restraint | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| German coffee tax and import tariff volatility | –0.8% | Entire market, heavier on low-priced SKUs | Long term (≥ 5 years) |

| Climate-induced supply shocks | –0.7% | Supply chain-wide | Medium term (3-4 years) |

| Environmental and sustainability concerns | –0.3% | Eco-aware urban segments | Medium term (3-4 years) |

| Health-Driven shift to lower-caffeine drinks | –0.2% | Younger demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

German Coffee Tax and Import Tariff Volatility

Germany's unique coffee tax (Kaffeesteuer) creates significant cost pressures in the market, with levies of EUR 2.19/kg on roasted coffee and EUR 4.78/kg on instant coffee, alongside EU import tariffs of 7.5% on roasted coffee[4]Source: EuroTax, "Excise Duties for Coffee in Germany", eurotax.fr. This tax structure, unparalleled in other EU nations, combined with volatile international coffee prices and varying import duties, poses substantial challenges for market participants. Small and medium-sized businesses are particularly affected, as they have limited capacity to absorb cost fluctuations and manage complex tax compliance requirements. These financial pressures often force companies to choose between reducing profit margins or increasing consumer prices, potentially impacting market growth and consumption patterns. While green coffee beans remain exempt from import duties, the overall tax and regulatory framework continues to influence market dynamics and business operations in Germany's coffee industry.

Climate-Induced Supply Shocks

Climate-related challenges significantly impact the German coffee market through disruptions in supply chains and production patterns. Extreme weather events, including droughts, floods, and unseasonable temperatures, affect harvests in key producing nations, particularly Brazil and Vietnam, disrupting growing cycles and reducing crop yields. These disruptions result in crop failures and quality issues, forcing producers to increase prices to offset losses. The combination of supply constraints and growing demand from Asian markets has intensified pricing pressures across the industry. The situation affects bean quality and availability, impacting product innovation in the specialty coffee segment. Furthermore, unpredictable weather patterns make it difficult for farmers to plan cultivation cycles effectively, leading to irregular supply patterns and increased costs for crop insurance and risk management measures. These factors contribute to price volatility in the green bean market, affecting both domestic supply chains and international trade flows, necessitating continued investment in sustainable farming practices and supply chain resilience to maintain market equilibrium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whole Beans Challenge Ground Coffee Dominance

Ground coffee dominates with a 49.05% market share in 2025, driven by convenience and established consumer preferences. Whole bean coffee demonstrates strong growth potential with a projected CAGR of 3.55% during 2026-2031, exceeding the market's overall growth rate of 2.46%. This trend indicates German consumers' increasing preference for quality coffee experiences, supported by investments in home grinding equipment. The growing popularity of specialty coffee shops has influenced consumers to replicate cafe-quality beverages at home, further strengthening ground coffee's market position. Additionally, the availability of diverse flavor profiles and origins in ground coffee formats continues to attract consumers seeking authentic coffee experiences.

While instant coffee maintains its presence among convenience-focused consumers, it faces competition from ready-to-drink formats and single-serve options. The coffee pods and capsules segment remains stable, with developments like Nespresso's introduction of 100% biodegradable capsules highlighting the importance of sustainable solutions. The market continues to evolve as consumers seek products that balance convenience with quality. German retailers have expanded their instant coffee selections to include premium varieties and organic options, addressing changing consumer preferences. The emergence of specialized instant coffee brands targeting younger consumers with innovative flavors and sustainable packaging has also contributed to market dynamics.

By Type: Specialty Coffee Disrupts Conventional Market

The conventional coffee segment dominates the German market with an 84.35% share in 2025, providing consistent quality at accessible price points. However, the specialty coffee segment is experiencing explosive growth at 8.60% CAGR (2026-2031), more than three times the overall market rate. This growth is driven by increasing consumer knowledge about coffee origins, processing methods, and flavor profiles. The specialty segment is characterized by direct trade relationships, transparency in sourcing, and emphasis on unique sensory experiences. Digital marketplaces are enhancing connections between producers and roasters, while e-commerce is facilitating consumer access to specialty offerings.

The specialty coffee boom is reshaping competitive dynamics, with multinational companies acquiring specialty brands to capitalize on this trend. Simultaneously, small independent roasters are gaining market share by emphasizing craftsmanship and sustainability. The specialty segment's influence extends beyond its market share, as its emphasis on quality and ethics increasingly informs conventional coffee positioning. Julius Meinl's introduction of specialty coffees in 2024 from Costa Rica and Burundi exemplifies how established players are expanding their premium offerings to meet evolving consumer preferences. This segment's continued growth suggests a fundamental shift in how German consumers perceive and value coffee, with implications for pricing strategies and product development across the market.

By Packaging Format: Sustainability Drives Innovation

Flexible packaging dominates the German coffee market with a 43.12% share in 2025, primarily due to its cost-effectiveness and relatively low environmental footprint. The packaging landscape continues to evolve with sustainability as a key driver, leading to innovations that balance environmental impact with product freshness preservation. Rigid packaging maintains its position in premium segments where presentation and reusability are valued. Manufacturers are increasingly adopting multi-layer flexible materials that enhance shelf life while reducing material usage and transportation costs. The integration of advanced barrier technologies in flexible packaging materials has enabled manufacturers to extend product shelf life while maintaining flavor integrity.

Single-serve packaging formats, including capsules, pods, and sachets, are experiencing the highest growth rate at 3.76% CAGR (2026-2031), driven by consumer demand for convenience and portion control. This trend aligns with broader industry sustainability initiatives, as demonstrated by Mondi's collaboration with a packaging machine provider in May 2024 to develop paper-based coffee wrappers, reflecting the industry's commitment to environmentally responsible packaging solutions while maintaining product quality. The market has also witnessed increased investment in recyclable and compostable single-serve packaging options, with major brands introducing aluminum-free alternatives to traditional coffee capsules.

By Distribution Channel: On-Trade Growth Challenges Off-Trade Dominance

The off-trade channel commands 73.40% of the German coffee market in 2025, with supermarkets and hypermarkets serving as primary purchase points for home consumption. However, the on-trade channel is growing faster at 2.94% CAGR (2026-2031), reflecting the post-pandemic resurgence of out-of-home consumption and the expansion of specialty coffee shops. This growth is particularly evident in urban areas, where coffee shops function as social spaces and showcases for premium offerings. Traditional retailers are responding to this trend by expanding their premium coffee selections and introducing in-store coffee experiences to maintain their market position.

Within the off-trade segment, online retail is gaining share as consumers seek specialty products not available in conventional retail. Convenience stores are adapting by upgrading their coffee offerings to compete with specialty shops. The distribution landscape is increasingly omnichannel, with brands like Tchibo operating across retail stores, dedicated shops with integrated coffee bars, and e-commerce platforms. This multi-channel approach reflects the complex purchasing patterns of German coffee consumers, who may buy different products through different channels based on occasion and need state. Retailers investing in both physical and digital presence are experiencing higher customer retention rates and increased sales volumes.

Geography Analysis

Western Germany leads the coffee market with a 29.30% share in 2025, benefiting from high population density, strong purchasing power, and established coffee culture in cities like Cologne, Düsseldorf, and Frankfurt. The region's dominance is reinforced by the concentration of major coffee companies and roasters, creating a robust infrastructure for product innovation and distribution. Consumer preferences in Western Germany skew toward specialty and premium offerings, with higher-than-average spending on out-of-home consumption. The region serves as a bellwether for national trends, often being the first to adopt new coffee concepts and brewing methods.

Eastern Germany presents the highest growth potential with a projected 4.34% CAGR from 2026-2031, nearly double the national average. This growth is driven by rising disposable incomes, urbanization in cities like Dresden and Leipzig, and the expansion of specialty coffee culture. The region's lower market saturation compared to Western and Southern Germany creates opportunities for both established players and new entrants. Eastern Germany's coffee consumption patterns are evolving rapidly, with increasing preference for whole beans and specialty offerings, particularly among younger consumers. The region's growth trajectory suggests a convergence with Western German consumption patterns, though price sensitivity remains higher, influencing product positioning and promotional strategies.

Competitive Landscape

The German coffee market exhibits moderate concentration, with established leaders facing increasing competition from specialty players and private labels. Major players include JDE Peet's N.V., JJ Darboven GmbH & Co. KG, Nestle S.A, Alois Dallmayr KG, and Tchibo GmbH. The market dynamics are influenced by changing consumer preferences, with a growing demand for premium and specialty coffee products. German consumers are increasingly prioritizing quality and sustainability in their coffee purchases, driving companies to adapt their product portfolios and sourcing practices.

Companies are increasingly pursuing vertical integration, extending control from sourcing to retail to protect margins and strengthen sustainability credentials. This strategy enables companies to maintain better quality control and respond quickly to market demands. The integration strategy also helps companies build stronger relationships with coffee producers and ensure sustainable supply chain practices.

Growth opportunities exist in functional coffee formulations targeting specific health benefits and premium ready-to-drink products for mobile consumption. Specialty roasters are transforming market dynamics through direct trade relationships with producers and brand positioning based on quality and ethics. The industry is adopting new technologies throughout the value chain, implementing blockchain traceability systems and AI-driven roasting profiles to maintain consistent quality.

Germany Coffee Industry Leaders

-

J J Darboven GmbH & Co. KG

-

Tchibo GmbH

-

Alois Dallmayr KG

-

JDE Peet's N.V.

-

Nestle S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dallmayr expanded its Röstkunst specialty coffee range in Germany with seven new coffee varieties. The new products include four entry-level options - three espresso blends (Velvet Noir, Italian Vibe, Dolce Samba) and one Caffè Crema blend (Golden Silk) - compatible with espresso machines and automatic coffee makers. The company also introduced three "Omni Roast" single-origin coffees (Costa Rica Las Nubes Red Honey, Colombia Villa Flor Pink Bourbon, Ethiopia Finchawa Anaerobic), suitable for both filter and espresso brewing methods.

- March 2025: Melitta introduced compostable coffee balls in partnership with CoffeeB. The German coffee group expanded its product line by incorporating CoffeeB's compostable coffee balls, originally developed by Switzerland's Migros. The new product range includes CoffeeB, Melitta, BellaCrema La Crema, and CoffeeB Melitta Auslese Klassisch.

- July 2023: JDE Peet's introduced recyclable paper-based packaging for its instant coffee brands, including L'OR, Kenco, Jacobs, and Douwe Egberts. The packaging, which was composed of more than 85% paper, enabled the reuse of existing glass and tin containers while reducing carbon emissions. This packaging solution expanded across major markets throughout 2024 and represented the company's lowest carbon footprint packaging option to date.

- April 2023: CoffeeB introduced a capsule-free coffee system in Germany featuring the "Coffee Ball" - a compressed coffee sphere coated with alginate that is fully compostable. The system delivers the convenience and taste quality of capsule coffee without generating plastic.

Germany Coffee Market Report Scope

Coffee represents a significant beverage segment produced through the processing of roasted Coffea plant seeds, known commercially as coffee beans. The product maintains substantial market presence due to its characteristic aroma and caffeine properties, positioning it as a dominant player in the global beverage market.

The market is segmented by product type, type, packaging format, distribution channel, and geography. The report segments the product type into whole bean, ground coffee, instant coffee, and coffee pods and capsules. Based on type, the market is segmented into conventional and specialty coffee. By packaging format, the market is divided into flexible (bags, pouches), rigid (cans, jars), and single-serve (capsules, pods, sachets). Furthermore, by distribution channel, the market has been segmented into off-trade and on-trade. Off-trade is further sub-segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other off-trade channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Whole Bean |

| Ground Coffee |

| Instant Coffee |

| Coffee Pods and Capsules |

By Type

| Conventional Coffee |

| Specialty Coffee |

By Packaging Format

| Flexible (Bags, Pouches) |

| Rigid (Cans, Jars) |

| Single-Serve (Capsules, Pods, Sachets) |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail | |

| Other Off-Trade Channels |

By Region

| Northern Germany |

| Western Germany |

| Central Germany |

| Sothern Germany |

| Eastern Germany |

| By Product Type | Whole Bean | |

| Ground Coffee | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| By Type | Conventional Coffee | |

| Specialty Coffee | ||

| By Packaging Format | Flexible (Bags, Pouches) | |

| Rigid (Cans, Jars) | ||

| Single-Serve (Capsules, Pods, Sachets) | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail | ||

| Other Off-Trade Channels | ||

| By Region | Northern Germany | |

| Western Germany | ||

| Central Germany | ||

| Sothern Germany | ||

| Eastern Germany | ||

Key Questions Answered in the Report

What is the current German Coffee market size?

The German Coffee market size stands at USD 7.68 billion for 2026 and is forecast to reach USD 8.68 billion by 2031.

How fast is the German Coffee industry expected to grow?

Industry revenue is projected to rise at a 2.46% CAGR between 2026 and 2031, with specialty and whole-bean formats growing faster.

Which product type has the highest German Coffee market share?

Ground coffee leads with 49.05% share, although whole-bean sales are accelerating quickest.

Why is specialty coffee gaining momentum in Germany?

Consumers increasingly value transparent sourcing, origin authenticity, and premium flavour, driving specialty coffee’s 8.60% forecast CAGR.

Which German region offers the highest growth potential?

Eastern Germany is forecast to deliver a 4.34% CAGR through 2031 owing to rising incomes and rapid adoption of specialty formats.

Page last updated on: