Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

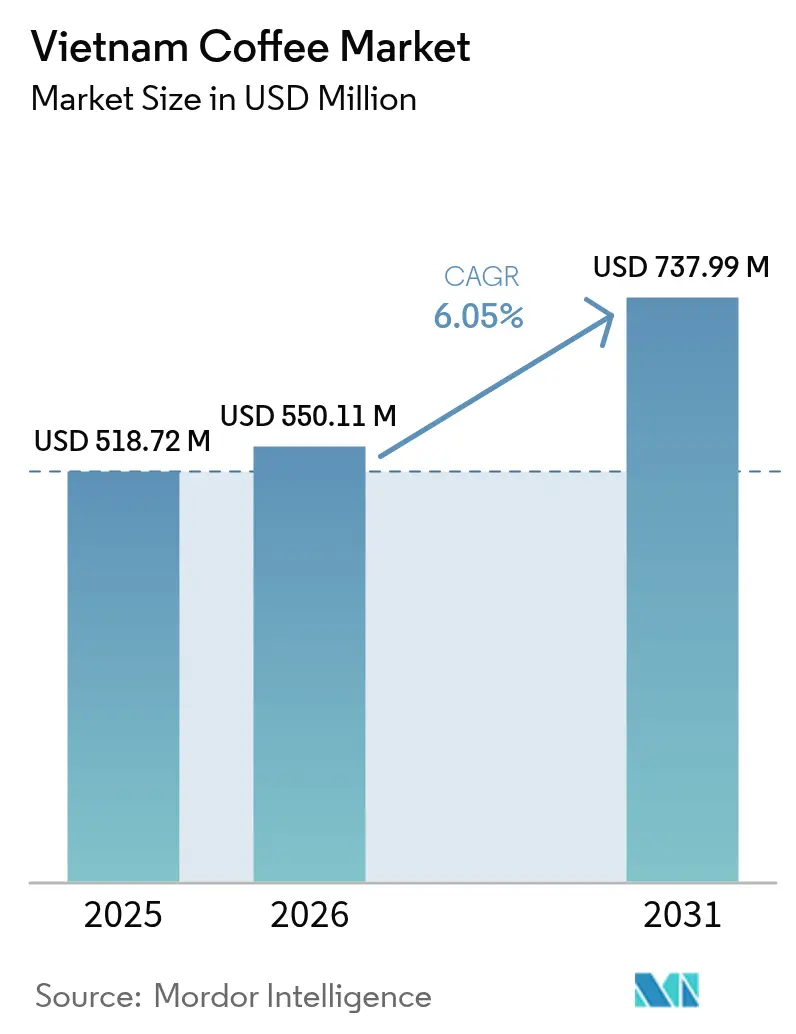

| Base Year Market Size (2025) | USD 518.72 Million |

| Market Size (2026) | USD 550.11 Million |

| Market Size (2031) | USD 737.99 Million |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Coffee Market Analysis by Mordor Intelligence

Vietnam coffee market size in 2026 is estimated at USD 550.11 million, growing from 2025 value of USD 518.72 million with 2031 projections showing USD 737.99 million, growing at 6.05% CAGR over 2026-2031. In the first half of the Financial Year 2024/25, the average export price surged to USD 5,630 per ton, a 143% leap from the previous fiscal year, according to the U.S. Department of Agriculture[1]Source: U.S. Department of Agriculture, "Coffee Annual", apps.fas.usda.gov . The Ministry of Agriculture and Rural Development (Vietnam) highlighted that Vietnam's coffee export revenue in 2024 hit around USD 5.5 billion, a notable rise from USD 4.1 billion the prior year[2]Source: Ministry of Agriculture and Rural Development (Vietnam), "Export revenue of coffee in Vietnam", www.mard.gov.vn. While the total planted area is being adjusted to 610,000-640,000 hectares for a focus on higher-grade output, there's a robust investment push in roasting, soluble, and ready-to-drink capacities. This, coupled with a burgeoning café scene, keeps the momentum alive. Global roasters' demand for Robusta, a domestic tilt towards premium beverages, and the European Union's stringent traceability mandates are collectively elevating quality and fostering vertical integration in Vietnam's coffee landscape. Furthermore, companies embracing sustainability and premiumization not only gain enhanced market access and pricing power but also enjoy fatter margins, bolstering the Vietnam coffee market's long-term competitiveness.

Key Report Takeaways

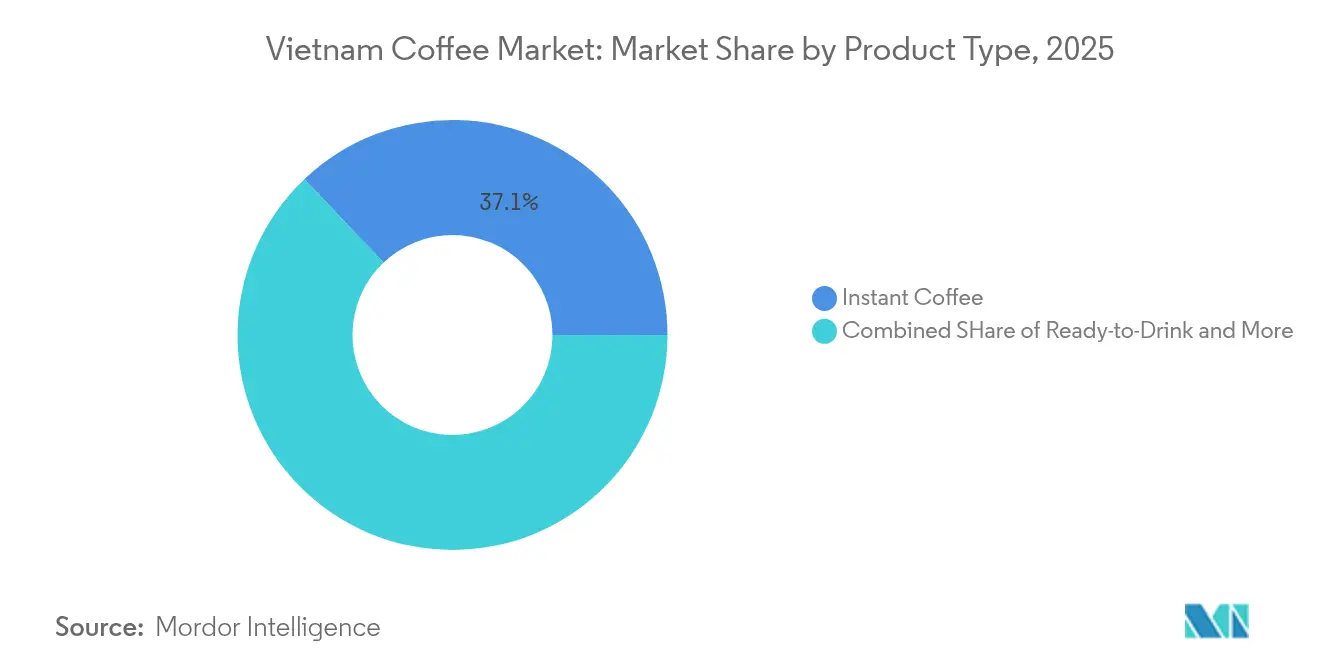

- By product type, Instant Coffee led with 37.10% revenue share in 2025, while Ready-to-Drink beverages are forecast to advance at a 7.55% CAGR through 2031.

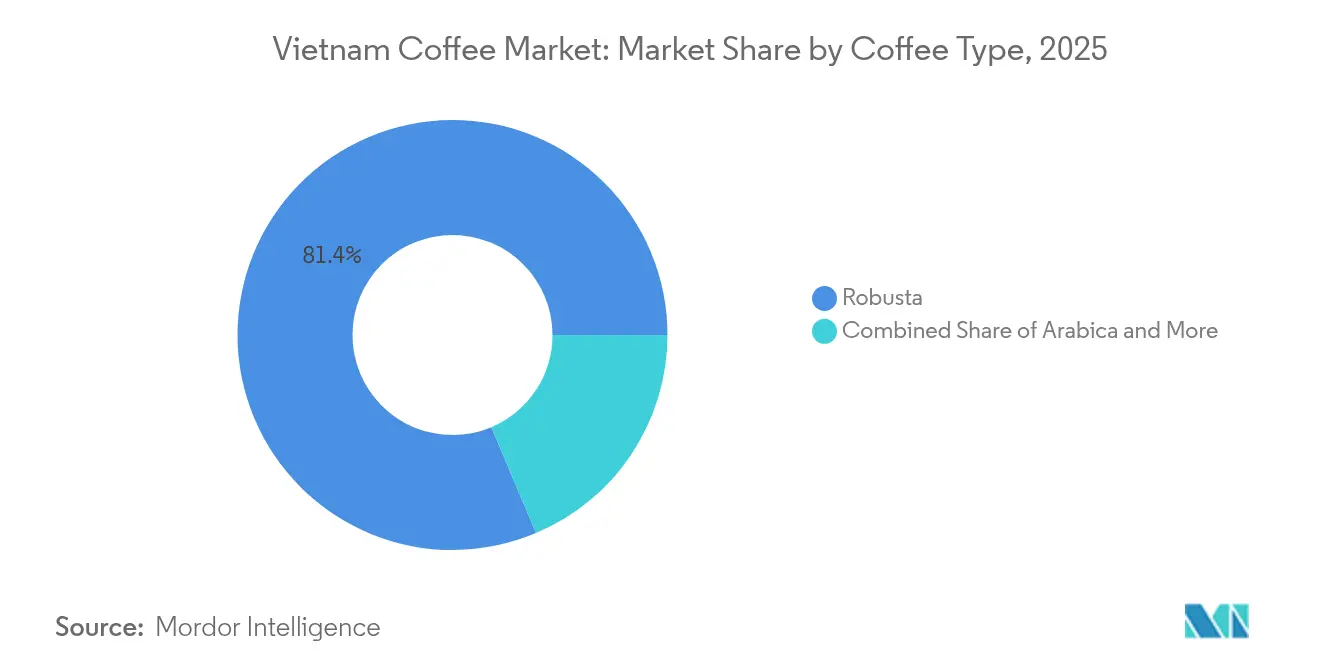

- By coffee type, Robusta captured an 81.35% share of the Vietnam coffee market size in 2025 and continues to outpace other varieties with a 6.55% CAGR to 2031.

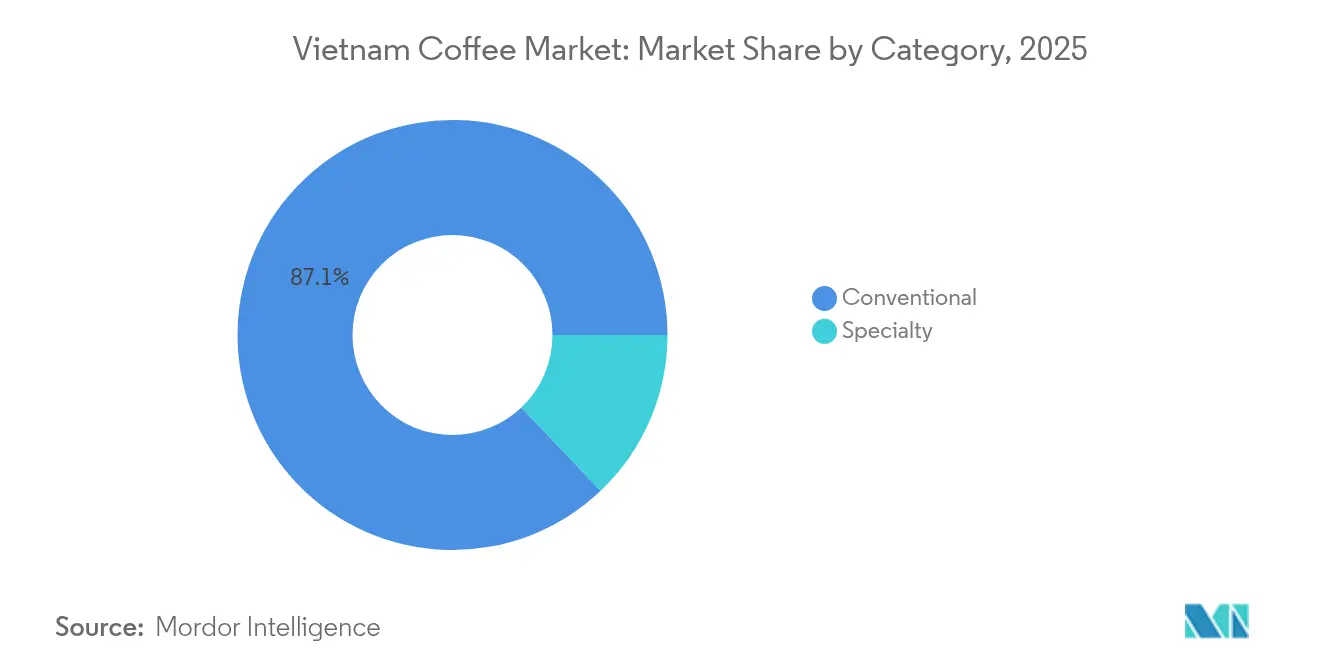

- By category, conventional beans held 87.10% of 2025 sales; the specialty segment is projected to expand at a 6.95% CAGR to 2031.

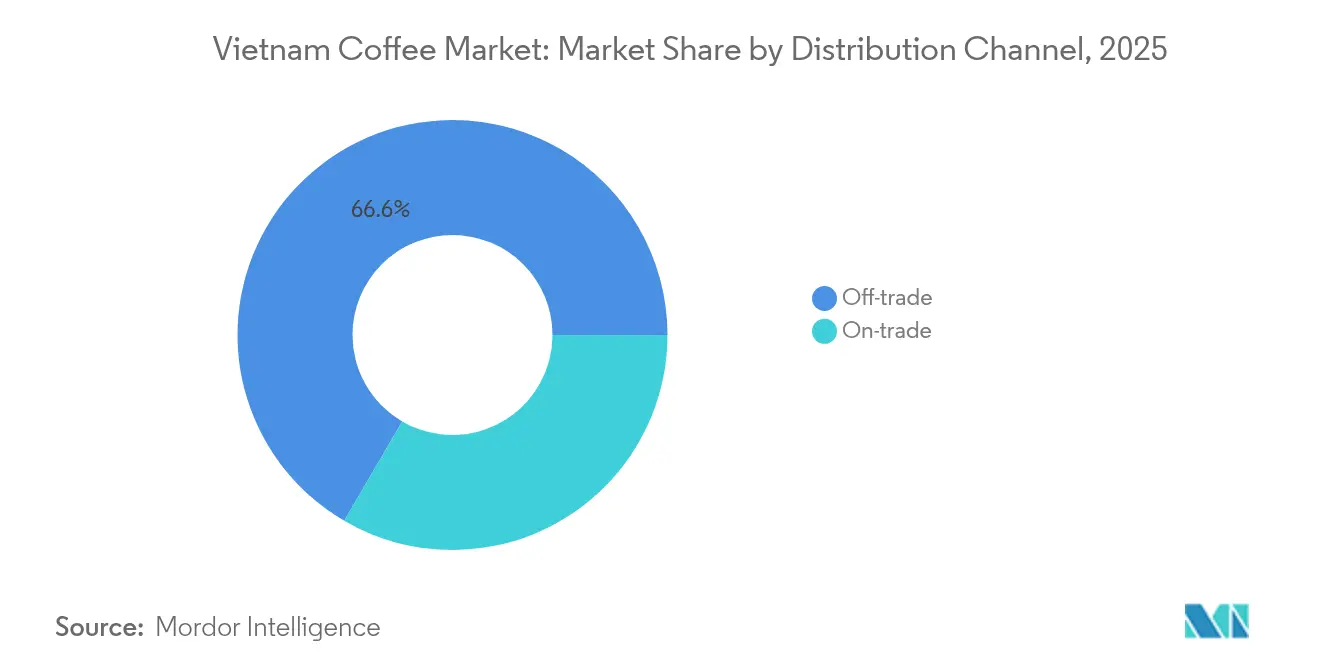

- By distribution channel, off-trade accounted for a 66.60% share in 2025, whereas on-trade venues are growing fastest at a 6.75% CAGR through 2031.

- Nestlé, Trung Nguyên, and Highlands Coffee together controlled more than 50% of branded processing capacity in 2024, anchoring the top tier of the Vietnam coffee market share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Café Chains and Franchise Models | +1.2% | National, with concentration in Ho Chi Minh City, Hanoi | Medium term (2-4 years) |

| Product Innovation with Functional Blends | +0.8% | Global export markets, domestic urban centers | Long term (≥ 4 years) |

| Sustainability and Traceability | +0.9% | Europe markets and North American premium segments | Long term (≥ 4 years) |

| Growth of Specialty and Premium Coffee Culture | +1.1% | Urban Vietnam, international export markets | Medium term (2-4 years) |

| Rise of Home Brewing and Convenience Formats | +0.7% | National, with urban bias | Short term (≤ 2 years) |

| Tech-Enabled Customer Experience | +0.5% | Major cities, e-commerce platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Café Chains and Franchise Models

Vietnam's café chains are shifting their focus from mere coffee sales to creating immersive retail experiences. Highlands Coffee, with 855 stores, boasted a 13% revenue growth in 2024. Meanwhile, Phúc Long made headlines by adding 79 new locations, bringing its total to 237 in 2024. Trung Nguyên Legend is making waves internationally, eyeing 1,000 global stores, with 130 set for China by 2024, showcasing the power of the franchise model. Vietnamese brands are not just stopping at home; they're making strategic moves into billion-dollar markets like the UAE, India, and Qatar. This is in line with the global franchising industry's bullish growth projections. Such strategies not only anchor Vietnamese coffee culture in upscale international arenas but also bolster brand recognition, aiding export endeavors. The triumph of local chains over global giants is evident. Starbucks, with its 127 outlets, pales in comparison to Highlands' 855, underscoring the edge of cultural resonance and strategic pricing.

Product Innovation with Functional Blends

Vietnamese coffee companies are innovating by turning traditional waste into premium exports, marking a shift from mere commodity production. Việt Thảo Nhiên has made waves by exporting coffee husk tea to Japan, a move that underscores the potential of the circular economy. By repurposing discarded Arabica coffee husks, they've crafted a health-benefiting beverage. With a decade of research backing their patented extraction technology, the company eyes expansions into South Korea and Europe. Nestlé's NESCAFÉ Plan, on the other hand, has empowered over 21,000 farmers with high-yield coffee varieties and digital tools, boosting incomes by 30-150% and championing regenerative practices. Meanwhile, Sucafina Instant forecasts a 59% rise in per capita spending on instant coffee by 2029, thanks to its rich flavors and health-focused offerings appealing to both busy professionals and traditionalists. Such strides elevate Vietnamese coffee from basic exports to sought-after, premium products on the global stage.

Sustainability and Traceability

Vietnam's coffee sector grapples with a shifting regulatory landscape, emphasizing the need for robust traceability systems. This shift presents both hurdles in compliance and avenues for competitive edge. Starting December 2024, the EU Deforestation Regulation mandates that Vietnamese exporters demonstrate their coffee is sourced from non-deforested regions. This regulation holds significant weight, given that the EU market constitutes 41% of Vietnam's coffee exports. In response, Vietnam's Ministry of Agriculture is crafting national mapping systems to aid in compliance. The regulation's 12-month extension offers businesses a crucial window for adaptation. Currently, only 25-30% of Vietnamese coffee aligns with sustainability benchmarks. However, certified farms are reaping the benefits, showcasing enhanced yields and income. Leading the charge in sustainability is Lâm Đồng province, boasting over 86,000 hectares either organically certified or meeting export criteria. Cooperatives, such as Bechamp Đắk Nông, are securing organic certifications tailored for global markets, with a notable focus on South Korea. This push towards sustainability is carving a divide in the market: compliant producers are tapping into premium markets, while their non-compliant counterparts face export hurdles. This dynamic could pave the way for a more consolidated industry, favoring larger, tech-savvy operations.

Growth of Specialty and Premium Coffee Culture

Vietnam's coffee culture is evolving, with consumers increasingly gravitating towards specialty products and premium experiences. This shift is reshaping both consumption habits and market dynamics. Per capita coffee consumption is on the rise. In 2024, the specialty coffee segment, holding a 12.3% market share, is the fastest-growing, expanding at a 7.32% CAGR. This growth is largely fueled by urban consumers prioritizing traceability and environmental responsibility. Vietnamese coffee chains are carving out a niche, competing effectively against global brands. By offering culturally resonant experiences at reasonable prices, Highlands Coffee boasts sales exceeding VND 3.5 billion in 2024, while The Coffee House is on a rapid trajectory, expanding to over 100 outlets. Digital sales are making waves, with online transactions accounting for 35% of Phúc Long's revenue. This trend underscores the digital engagement of Gen Z and Millennials, pivotal in propelling the food and beverage sector's growth. The premiumization trend isn't confined to domestic shores. In a notable 2024 milestone, Vietnamese Robusta prices eclipsed those of Arabica in export markets. This shift not only underscores enhancements in quality but also signals a growing market acknowledgment, bolstering strategies aimed at higher-value positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smallholder Fragmentation | -1.8% | Central Highlands, rural production areas | Long term (≥ 4 years) |

| Supply Chain Disruptions | -1.1% | Global export routes, domestic logistics | Short term (≤ 2 years) |

| Price Volatility and Market Uncertainty | -0.9% | Global commodity markets, farmer decision-making | Medium term (2-4 years) |

| Regulatory Uncertainty and Trade Barriers | -0.7% | European markets, the United States trade relations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smallholder Fragmentation

In Vietnam's coffee sector, smallholder fragmentation poses significant challenges. A staggering 91% of farmers cultivate plots smaller than 2 hectares, leading to inefficiencies that hinder scalability and compliance. Data from Vietnam's General Statistics Office reveals a rise in operational farms, from 24.08 thousand in 2022 to approximately 24.94 thousand in 2023. This fragmentation issue is magnified by the EU's Deforestation Regulation. Individual farmers find it challenging to gather essential traceability data and shoulder compliance costs, a burden more easily managed by larger operations. Furthermore, many farmers depend on middlemen for inputs and financing, which complicates the supply chain and diminishes their market access and price negotiation power. While Vietnam boasted a coffee cultivation area of 720,000 hectares in 2023, projections indicate a reduction to 650,000 hectares by 2030. This shift, driven by government initiatives, aims to concentrate production on higher-standard varieties. The U.S. Department of Agriculture reports targets of 80-90% of newly cultivated areas adopting premium cultivars. Given these challenges, there's a pressing need for cooperative models and technology platforms to unify smallholder production and ensure traceability. However, the uptake of such solutions varies across Vietnam's diverse coffee-growing regions.

Supply Chain Disruptions

Vietnam's coffee supply chain faces ongoing disruptions, causing fluctuations in export performance and domestic market stability, hindering growth. Geopolitical tensions and container shortages have disrupted export logistics, reducing export volume from October 2024 to January 2025, despite higher export values driven by price premiums. According to the USDA Foreign Agricultural Service, Vietnam's 2023/24 coffee exports totaled 25 million 60-kilogram bags, down from 28.04 million bags the previous year. Climate-related issues, including earlier dry seasons and low reservoir levels, reduced the 2023-2024 crop to a four-year low. Labor shortages and rising fertilizer and labor costs further strain smallholder farmers, pushing some to switch to more profitable crops like durian, reducing coffee output and creating supply uncertainties for domestic processors and exports. Post-harvest inefficiencies, such as inadequate infrastructure and limited advanced drying and storage facilities, lead to quality variations, restricting access to premium markets. These disruptions perpetuate supply uncertainty and price volatility, complicating long-term planning for producers and buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instant Coffee Dominance Faces RTD Challenge

In 2025, Instant Coffee commands a dominant 37.10% market share, underscoring Vietnam's prowess in catering to convenience-driven consumers and its robust export reach, spanning over 100 countries, with notable brands like G7 and Trung Nguyên. The segment enjoys the advantage of well-established distribution networks and a strong consumer base, especially in rural areas, where adoption stands at 62%, slightly trailing the 72% in urban locales. Meanwhile, the Ready-to-Drink segment is poised as the market's growth engine, boasting a 7.55% CAGR through 2031, fueled by urbanization and shifting preferences among the youth. Ground Coffee and Whole Bean cater to niche markets prioritizing quality and brewing rituals, whereas Coffee Pods and Capsules face challenges in Vietnam, hindered by limited equipment adoption and price sensitivity.

In 2023, Vietnam's instant coffee production hit 171,400 metric tons, as reported by the General Statistics Office of Vietnam, with forecasts suggesting a rise in per capita spending. The segment's shift towards functional blends and health-centric formulations caters to a spectrum of consumers: from busy professionals valuing convenience to traditionalists who savor robust flavors. Westrock Coffee's foray into Ready-to-Drink facilities, highlighted by a new plant in Conway, Arkansas, underscores the global acknowledgment of RTD's growth trajectory and Vietnam's pivotal position in worldwide supply chains. Moreover, the competitive landscape increasingly favors firms with cohesive supply chains and a knack for innovation. As product differentiation gains prominence in the mature instant coffee arena, the RTD sector emphasizes the need for advanced cold-chain logistics and innovative packaging solutions.

By Coffee Type: Robusta Supremacy Reinforces Vietnam's Global Position

In 2025, Robusta coffee holds 81.35% of the market, and Arabica is set to grow at a 6.55% CAGR through 2031, highlighting Vietnam's global coffee dominance. As the top Robusta producer, Vietnam supplies 40% of the global market, supported by favorable Central Highlands conditions, per the World Trade Organization. Improved Robusta quality has driven price premiums, with domestic prices surpassing Arabica for the first time in 2024, reaching VND 131,000 per kilogram. The smaller Arabica segment targets premium export markets and specialty niches like organic and single-origin coffee. Other coffee varieties remain negligible, reflecting Vietnam's focus on Robusta.

Vietnam cultivates Robusta across 716,600 to 730,000 hectares, mainly in Đắk Lắk, Lâm Đồng, Đắk Nông, Gia Lai, and Kon Tum. The Ministry of Agriculture's replanting program (2021-2025) aims to replant 107,000 hectares, increase productivity to 3.5 tons per hectare, and boost incomes by 1.5-2 times. Global dynamics favor Vietnamese Robusta, as Brazil's reduced production and climate issues create supply gaps. This supports Robusta's growth and positions Vietnam's export revenue to exceed USD 7.5 billion by 2025.

By Category: Conventional Dominance Yields to Specialty Growth

In 2025, the Conventional coffee category holds an 87.10% market share, driven by established farming practices and competitive pricing in domestic and export markets. The Specialty segment, including organic and single-origin varieties, is growing at a 6.95% CAGR through 2031, fueled by premium demand and regulatory compliance. This growth highlights a shift where quality-focused producers benefit from sustainability certifications and traceability. Conventional producers face challenges from the EU's Deforestation Regulation and rising demand for eco-friendly products, creating a divide between compliant and non-compliant producers.

Specialty coffee adoption varies across Vietnam, with Lâm Đồng province leading with over 86,000 hectares meeting sustainability standards. Currently, 25-30% of Vietnamese coffee meets these benchmarks, with certified farms achieving higher yields and incomes. The National Agricultural Extension Center promotes sustainable practices through training, while cooperatives like Bechamp Đắk Nông secure organic certifications for export markets such as South Korea. This transition reflects Vietnam's strategy to move from commodity production to value-added exports, as specialty coffee commands premium prices globally.

By Distribution Channel: Off-trade Leadership Meets On-trade Dynamism

In 2025, off-trade channels, including supermarkets, hypermarkets, convenience stores, specialty stores, and online platforms, dominate with a 66.60% market share in Vietnam. This reflects a strong retail infrastructure and consumer preference for home-consumed packaged coffee. On-trade channels, however, show a 6.75% CAGR through 2031, driven by café culture, urbanization, and younger demographics' experiential consumption preferences. While traditional retail leads in volume, foodservice channels capture growth and premium positioning opportunities.

Online retail drives off-trade growth, contributing 35% of Phúc Long's revenue and highlighting digital adoption among Gen Z and Millennials. E-commerce fosters direct-to-consumer ties and premium visibility, while supermarkets and hypermarkets cater to the mass market with instant coffee and packaged goods. Specialty stores target niche markets with quality and brewing equipment, and convenience stores capture impulse buys and ready-to-drink items. On-trade benefits from café chain expansion: Highlands Coffee operates 855 stores, Phúc Long 237 outlets, and Starbucks 127 locations. Distribution channel evolution reflects consumer shifts toward premium experiences, offering opportunities for integrated retail and foodservice players.

Geography Analysis

Vietnam's coffee market showcases distinct regional patterns that enhance production efficiency and shape market dynamics across its varied coffee-growing areas. The Central Highlands dominates with approximately 716,600 to 730,000 hectares of cultivated land, led by Đắk Lắk and Lâm Đồng provinces, especially after recent administrative changes. Price fluctuations across regions highlight quality disparities and market accessibility, with Dak Lak securing premium prices in February 2025. This geographic clustering has fostered robust processing infrastructures, attracting significant investments. Notable facilities include Nestlé's Trị An in Đồng Nai, Trung Nguyên's plant in Buôn Ma Thuột, and Highlands Coffee's roasting hub in Bà Rịa-Vũng Tàu.

Northern regions, while producing smaller coffee volumes, play a crucial role in catering to domestic markets, particularly in urban centers like Hanoi. The growing café culture in these areas drives on-trade channel growth. Meanwhile, the Mekong Delta, though producing less coffee than the Central Highlands, benefits from a well-established agricultural infrastructure that efficiently channels coffee distribution to Ho Chi Minh City and southern markets.

Sustainability practices vary widely across regions. Lâm Đồng aligns with export standards, while Gia Lai faces challenges due to nomadic farming practices that hinder compliance with the EU Deforestation Regulation, despite coffee exports being a significant revenue source for the province. Highlighting Lâm Đồng's strategic importance in Vietnam's coffee evolution, the government has allocated 36,000 of the 107,000 hectares slated for replanting by 2025, aiming to enhance quality across all regions.

Regulatory Landscape

Vietnam's coffee supply chain is increasingly shaped by export-market compliance and domestic food-safety controls. A key external requirement is the EU Deforestation Regulation (EUDR), which requires due diligence and proof that coffee is not sourced from land deforested or degraded after December 31, 2020. The EU accounts for about 41% of Vietnam's coffee exports, which makes compliance material for exporters and processors serving Europe.

On the domestic side, Vietnam applies national technical regulations and standards for green coffee and processing hygiene, including QCVN 01-26:2010/BNNPTNT (food safety and hygiene limits for green coffee) and QCVN 01-06:2009/BNNPTNT (food-safety conditions for green coffee processing facilities), alongside practice standards such as TCVN 12460:2018 (hygiene practice in coffee processing) and TCVN 6602:2013 (guidance for storage and transport). To operationalize EUDR traceability, the Ministry of Agriculture and Rural Development (MARD) piloted a national database for forest and coffee-growing areas in December 2024, supporting farm-level mapping and documentation for access to regulated import markets. While coffee exports are generally not subject to export tax (commonly cited at 0%), exporters still need shipment documentation such as phytosanitary certification for certain destinations.

Value Chain Analysis

Vietnam's coffee value chain starts with a production base dominated by smallholders, with around 640,000 households contributing the bulk of national output, alongside cooperatives and larger estates in the Central Highlands. Input and upstream support include seedling and agronomy programs such as those linked to the Western Highland Agriculture and Forest Science Institute (WASI), which produces about 4 to 5 million seedlings annually, plus supplier networks for fertilizer, irrigation equipment, and post-harvest equipment (including mechanical dryers). Fragmented farm structures and variable farm records keep aggregation and compliance costly, especially for exporters that need plot-level traceability for regulated markets.

Midstream actors include collectors, traders, and more than 100 private exporters, along with processors moving beyond green beans into roasting, soluble, and other deep-processing formats. Processing and export flows depend on both direct sourcing (from farms/cooperatives) and indirect channels (via intermediaries), while some processors also use imports from origins such as Indonesia, Brazil, and India to stabilize supply during off-seasons (commonly March to September). Key bottlenecks include climate volatility in the Central Highlands that disrupts harvesting and drying, increasing humidity-related quality risks and reliance on mechanical drying, as well as logistics and compliance friction tied to land-title gaps and legacy deforestation footprints that complicate EUDR-ready documentation. Coordination and advocacy are supported by bodies such as the Vietnam Coffee-Cocoa Association (VICOFA) working with MARD, while trade frameworks such as the EU-Vietnam Free Trade Agreement (EVFTA) reinforce the importance of maintaining export-grade quality, documentation, and consistent shipment performance into Europe.

Competitive Landscape

Vietnam's coffee market is moderatly consolidated, dynamic, and competitive, dominated by local giants, multinational players, a booming cafe culture, and a government push for value-added exports. Growth strategies focus on retail expansion, digital integration, premium products, and sustainability. Key developments include investments in advanced processing, new product launches, and compliance with international regulations like the EU Deforestation Regulation (EUDR). For instance, Nestlé reaffirmed its commitment to Vietnam in May 2025 with an additional USD 75 million investment in its Tri An plant, bringing total spending for 2024–2025 to USD 175 million. This investment enhances production capabilities to meet growing domestic and export demand for premium products like Nescafé and Starbucks at Home. The company also leverages its sustainable sourcing NESCAFÉ Plan, recognized by Vietnam's Ministry of Agriculture and Rural Development for its positive impact on farmers.

Players are expanding their store presence to boost market penetration. Vietnam's largest cafe chain, Highlands, aimed to surpass 830 stores by the end of 2024 through urban retail saturation. In 2024, Highlands invested 500 billion VND (approx. USD 21 million) in a new roasting plant and launched an expanded "Coconut Series" in February 2025 to cater to health-conscious consumers. Similarly, Trung Nguyên Legend pursued premiumization and expansion. In March 2025, it launched Legend Gold Freeze-Dried Coffee and announced a new factory in Buon Ma Thuot to enhance value-added processing. The brand expanded its cafe network in the US and China while targeting 3,000 stores globally by 2025 through its E-Coffee model. It also reinforced its G7 instant coffee lineup with new mixes in February 2025.

Government actions and international partnerships are reshaping the industry with a focus on sustainability. In December 2024, Vietnam's Ministry of Agriculture and Rural Development (MARD), supported by IDH and JDE Peet's, launched a database system to track forest and coffee-growing areas. This initiative ensures compliance with the EU's Deforestation Regulation, effective January 2026, providing Vietnamese producers with a competitive edge.

Vietnam Coffee Industry Leaders

-

Trung Nguyên

-

Nestlé S.A.

-

Jollibee Foods Corporation

-

Me Trang Coffee

-

Masan Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment and capability upgrades in deep processing create a clearer whitespace beyond green-bean exports, especially for instant and spray-dried products that can better capture value during periods of raw material price volatility. In June 2026, Trung Nguyên Legend began construction of a new factory system in the Tan An industrial cluster in Dak Lak designed to Net Zero standards, including an initial 1,000 kg/hour spray-drying line, alongside an expansion of an existing plant. The project points to active capacity build-out for value-added coffee and tighter sustainability requirements. Separate industry investment signals for additional freeze-drying and spray-drying capacity also support a broader shift toward branded and processed formats for both domestic retail and export channels.

Compliance-driven digitization is another near-term opportunity area, because EUDR implementation in 2026 increases demand for farm-level traceability, mapping, and data services across fragmented production zones. MARD's traceability work (including regional monitoring and reported data collection over large coffee areas) and public-private initiatives provide platforms for exporters and processors to onboard smallholders into compliant supply chains. Programs such as Binh Dien Fertilizer Joint Stock Company's Smart Coffee Farming expansion for the 2025-2026 crop year and Bayer Vietnam's June 2026 Centre of Excellence for coffee farming in the Central Highlands support technology transfer in irrigation, microclimate forecasting, and integrated plant health. Together, these initiatives support higher-grade, documented coffee suited for specialty and regulated markets, while reinforcing domestic premiumization through more consistent quality that helps processors and cafe chains differentiate offerings across instant, RTD, and specialty products.

Recent Industry Developments

- June 2026: Trung Nguyên Legend commenced construction of a new coffee factory system and expanded an existing plant at the Tan An industrial cluster in Dak Lak, targeting deeper processing capacity such as spray-dried products. The move strengthens domestic value-added capability for Robusta and supports tighter sustainability and product-specification requirements from export buyers.

- May 2025: Nestle Vietnam announced an additional USD 75 million investment to expand its Tri An coffee factory in Dong Nai, lifting its total 2024-2025 commitment to USD 175 million. The expansion underpins higher-volume and higher-quality output for branded and premium lines, and it further consolidates scale advantages in processing and sourcing programs.

- December 2024: Vietnam's Ministry of Agriculture and Rural Development (MARD), supported by IDH and JDE Peet's, launched a database system to track forest and coffee-growing areas to support EUDR traceability. This digital infrastructure initiative raises the bar for documentation across the supply chain and helps compliant exporters protect access to the EU market, which represents a large share of Vietnam's coffee exports.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Vietnam coffee market is defined as the value generated from coffee products sold for consumption within Vietnam through retail and foodservice channels, counted in current USD.

Scope exclusions: We do not count raw green coffee traded for export as a finished consumer market sale, and we also exclude farm-level cultivation costs that do not convert into coffee product sales.

Segmentation Overview

-

By Product Type

- Whole Bean

- Ground Coffee

- Instant Coffee

- Coffee Pods and Capsules

- Ready-to-Drink

-

By Coffee Type

- Arabica

- Robusta

- Others

-

By Category

- Conventional

- Speciality (Organic/Single-Origin)

-

By Distribution Channel

- On-trade

-

Off-trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Other Off-trade channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on Vietnam coffee supply, trade, and domestic demand signals, then mapping those signals to how coffee products are sold and priced across retail and foodservice. Public sources such as Vietnam General Statistics Office releases, Vietnam Customs trade statistics, the International Coffee Organization datasets, and USDA commodity notes help set guardrails on volumes, prices, and seasonality patterns that are harder to infer from company news.

We then cross-check category behavior using sources such as central bank or ministry macro indicators, trade association updates (for example, Vietnam Coffee and Cocoa Association publications), and peer-reviewed articles on consumption shifts and product formats. Company annual reports, investor decks, and credible press coverage help validate channel mix and pricing moves, and we also use selective paid databases for company financials plus shipment-level trade checks to confirm directions where public data was thin. These desk research sources are illustrative only, and many other public documents were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary discussions were used to pressure-test the desk assumptions on coffee product mix, the channel split between on-trade and off-trade, and the observed pace of price pass-through from green coffee to packaged coffee and beverages. We spoke with a mix of roasters, distributors, retailers, foodservice operators, and industry experts so that gaps in public data could be filled with practical inputs reflecting how the market is actually sold and consumed in Vietnam.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | |

| Mid tier: 52% | Functional/Unit leaders: 40% | |

| Smaller Players: 19% | Managers: 43% |

Market-Sizing & Forecasting

The market is modeled using a top-down approach where Vietnam consumption channels are sized first, then reconciled to category-level supply and pricing signals that indicate what can realistically be sold in-country. To keep totals grounded, we run selective bottom-up checks using sampled price points across common formats, channel markups, and volume proxies from trade and production indicators, then adjust totals when the two views disagree.

Key inputs used in the model include export and import price trends (to understand cost pressure and timing), the domestic channel mix between on-trade and off-trade, shifts across coffee formats such as instant versus ground, observed retail price bands and promotion intensity, and reported production and stock movements that indicate supply tightness. When a data point is not available at a fine level, the gap is handled through conservative proxy logic, such as using nearby format shares, channel share interviews, and a time-lagged price pass-through assumption.

For forecasting, we mainly apply scenario analysis because coffee is strongly affected by crop cycles and price shocks, which can make straight-line projections misleading. The scenarios are built around expected consumption growth, format premiumization, and price outlook, and then aligned to what industry respondents consider realistic for the next few years.

Data Validation & Update Cycle

Outputs are validated through multiple checks so that any single source does not over-influence the final number. We compare results against independent signals such as trade values, production movements, and reasonable price ranges by channel, then investigate variances that look out of line before sign-off.

The work is reviewed in more than one step, and re-contact is triggered when a key assumption changes, such as a sharp shift in export prices, taxes, or channel pricing behavior. Reports are refreshed annually, with interim updates when major market events materially change the outlook. Before delivery, an analyst performs a fresh pass on the key inputs so clients receive the latest updated view.

Mordor Intelligence's Vietnam Coffee Market Estimate Compared With Other Published Estimates

Market values for Vietnam coffee can look far apart across publications, even when the same country name is used, because the boundary of what counts as the market is not always the same. Differences also come from how firms treat trade value versus consumer sales value, and how quickly price moves are updated into the model.

By tracking channel-level selling prices and consumption-linked volumes, Mordor Intelligence keeps export revenue and raw green coffee trade from being mixed into the domestic coffee products total, which is a common reason the published numbers spread wide.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 518.72 M (2025) | |

| Global Consultancy A | USD 4.05 B (2024) | This estimate appears to align closer to export-linked revenue and broader coffee value-chain activity, so it can overstate the domestic consumer market when trade values are treated as market sales. |

| Industry Publisher B | USD 5.99 B (2024) | The scope likely bundles retail, foodservice, and a wider set of coffee-related revenues, and the price base may be updated differently, which can inflate totals during high green coffee price periods. |

The table shows that the biggest driver is scope, where export and value-chain measures can be mistaken for in-country consumption value. When the market is tied back to product formats and channels sold inside Vietnam, the steps are easier to repeat and the assumptions are easier to check.

Key Questions Answered in the Report

How large is the Vietnam coffee market in 2026?

The Vietnam coffee market size is USD 550.11 million in 2026 and is projected to reach USD 737.99 million by 2031.

What is the dominant coffee variety grown in Vietnam?

Robusta accounts for 81.35% of 2025 volume and continues to expand at a 6.55% CAGR as quality enhancements unlock price premiums.

Which product type is growing fastest through 2031?

Ready-to-Drink beverages lead with a 7.55% CAGR, reflecting urban demand for convenience and lifestyle beverages.

How will EU deforestation rules affect Vietnamese exports?

Exporters serving the 41% of shipments that go to Europe must adopt farm-level geotraceability or risk losing access, which accelerates industry consolidation around compliant processors.

What share of sales moves through cafés and foodservice venues?

On-trade channels currently represent 33.40% of value but are expanding fastest at 6.75% CAGR due to rapid café chain rollout.

Which companies hold the biggest processing capacity?

Nestlé, Trung Nguyên, and Highlands Coffee collectively exceeded 50% of branded processing volume in 2024, giving them scale advantages in sourcing and compliance.

Page last updated on: