Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.26 Billion |

| Market Size (2026) | USD 32.16 Billion |

| Market Size (2031) | USD 43.58 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia Pacific Coffee Market Analysis by Mordor Intelligence

The Asia-Pacific coffee market size is expected to grow from USD 30.26 billion in 2025 to USD 32.16 billion in 2026 and is forecast to reach USD 43.58 billion by 2031 at 6.27% CAGR over 2026-2031. Robust expansion reflects a steady shift from traditional tea habits toward coffee as a lifestyle symbol, a change reinforced by rising disposable incomes, rapid urbanization, and digitally driven purchasing habits. Demographic change amplifies momentum; a fast-growing youth cohort actively trades up to premium single-serve formats, while middle-class households support mainstream instant coffee for everyday use. Supply-side recalibration also underpins growth, with frequent climate shocks encouraging origin diversification and direct-trade models that raise transparency and quality consistency. Finally, the region’s flourishing café culture blends social interaction with remote-work convenience, widening usage occasions and encouraging new entrants to experiment with flavors, functional additives, and sustainable packaging solutions.

Key Report Takeaways

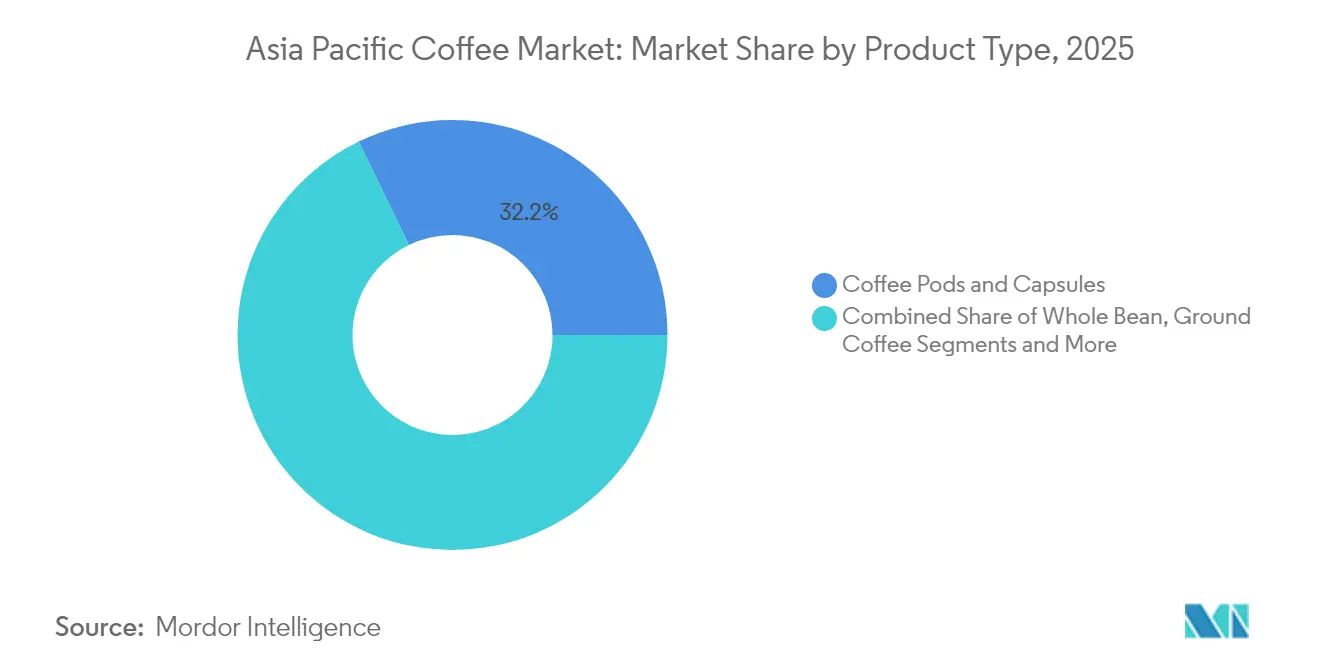

- By product type, Coffee Pods and Capsules held 32.18% of the Asia-Pacific coffee market share in 2025, while Instant Coffee is projected to register the quickest 6.61% CAGR through 2031.

- By flavor, Plain coffee retained 83.12% revenue share in 2025; Flavored variants are anticipated to log a 6.44% CAGR over the same horizon.

- By category, Conventional offerings captured 90.55% share of the Asia-Pacific coffee market size in 2025; Single Origin/Specialty/Organic alternatives are forecast to climb at a 7.45% CAGR to 2031.

- By bean type, Robusta dominated with 53.96% share in 2025, whereas Arabica is poised for a 6.88% CAGR through 2031.

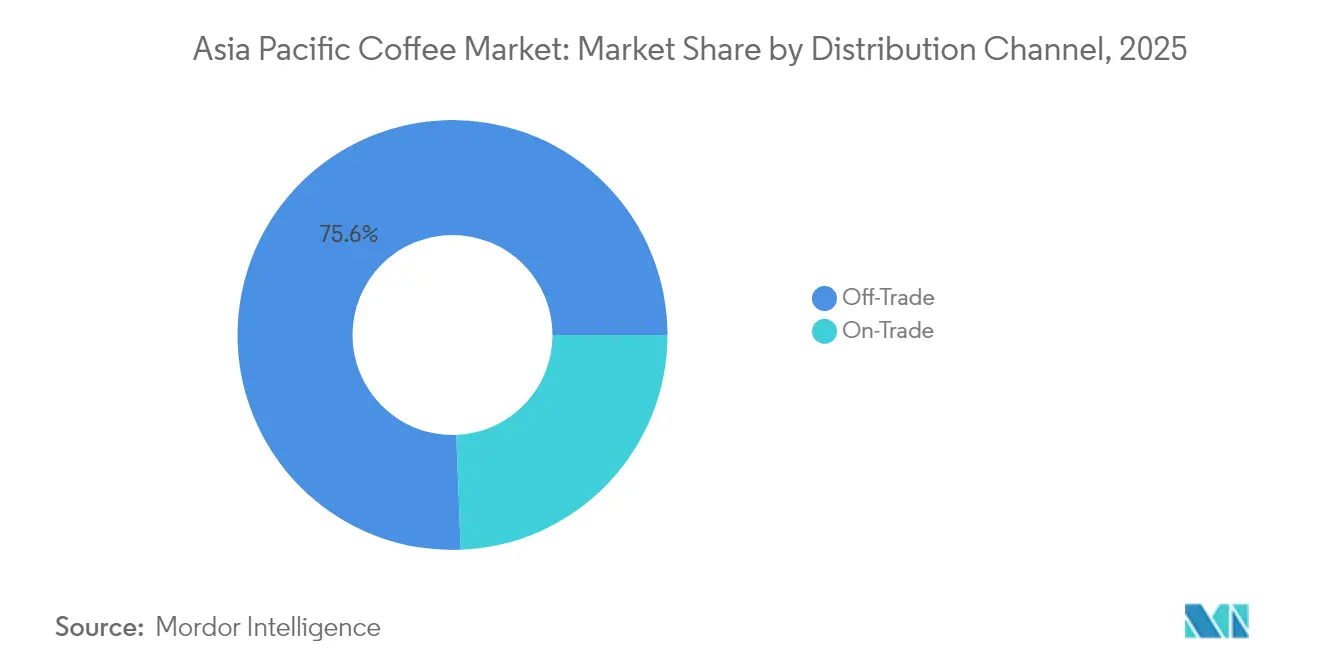

- By distribution channel, Off-Trade accounted for 75.61% of 2025 sales, while the On-Trade segment is slated to expand at a 6.74% CAGR, powered by third-wave café formats.

- By geography, China held 28.74% of Asia-Pacific coffee market share in 2025 while India is projected to grow at a CAGR of 6.94% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for specialty and premium coffee | +1.2% | China, Japan, South Korea, Australia | Medium term (2-4 years) |

| Rising cafe culture and coffee consumption | +1.8% | Asia-Pacific wide, strongest in urban centers | Short term (≤ 2 years) |

| Expanding youth population with evolving preferences | +1.4% | India, Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Innovation in flavors, formats, and packaging | +0.9% | Developed Asia-Pacific markets, spill-over to emerging | Medium term (2-4 years) |

| Health and wellness trends boosting consumption of organic and certified coffee | +0.7% | Australia, Japan, Singapore, urban China | Medium term (2-4 years) |

| Favorable government initiatives promoting coffee production and exports | +0.4% | Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for specialty and premium coffee

The Asia-Pacific coffee market is experiencing significant growth driven by the rising demand for specialty and premium coffee. This surge is largely fueled by a burgeoning middle class with increasing disposable incomes and a growing appreciation for high-quality coffee experiences.The market is significantly influenced by India, where domestic coffee consumption has been steadily rising over recent years. This growing internal demand is supported by increasing consumer awareness and a preference for high-quality coffee products. Concurrently, India has seen a remarkable surge in its coffee exports, which have more than doubled over the past decade, reaching USD 1.8 billion in FY24, according to the Ministry of External Affairs as of June 2025 [1]Source: Ministry of External Affairs, "India’s coffee exports double in a decade, touch USD 1.8 bn in FY24," indbiz.gov.in. The growth in exports underscores India’s strengthening position as a global coffee supplier, particularly in specialty and value-added coffee segments. Major export destinations include key markets in Europe such as Italy, Germany, and Belgium, as well as growing demand from countries in East Asia and the Middle East. Strategic initiatives by the Coffee Board of India, including promotional campaigns and support for sustainable coffee farming, have played a pivotal role in driving this growth and enhancing the country's global presence in the coffee trade.

Rising cafe culture and coffee consumption

The rising café culture and growing coffee consumption are major drivers of the Asia-Pacific coffee market. Urbanization, growing disposable incomes, and changing lifestyles have fueled a surge in coffee demand, especially among younger and affluent consumers in countries such as China, India, Japan, and South Korea. Cafés have evolved into vibrant social hubs where premium coffee experiences and unique beverage innovations are highly valued. Notably, Luckin Coffee operates over 22,000 stores across China as of 2024, utilizing an asset-light franchise model and rapid innovation cycles to consistently introduce new beverages and maintain strong customer engagement [2]Source: Luckin Coffee Inc., "Luckin Coffee Announces Fourth Quarter and Fiscal Year 2024 Financial Results", luckincoffee.com . Its digital-first, cashier-less stores enable convenient mobile ordering and pick-up or delivery, offering competitive prices about 30% lower than Starbucks in the region. This combination of scale, technology, and quick product iteration has helped Luckin solidify its leadership in China while driving broader interest and adoption of café culture throughout Asia-Pacific. The expanding café ecosystem supported by international chains and local specialty shops continues to boost coffee consumption and market growth.

Expanding youth population with evolving preferences

The expanding youth population in the Asia-Pacific region is a significant driver for the coffee market, particularly as South Asia hosts the largest population of young people globally, with 30% of the world's total adolescents—approximately 340 million—residing in this region [3]Source: United Nations Children's Fund, "Youth-led Action in South Asia", www.unicef.org. This vast and growing youth demographic exhibits evolving consumption preferences that strongly influence market trends. Young consumers in South Asia, including countries like India, Pakistan, and Bangladesh, are increasingly embracing coffee culture, driving demand for premium, specialty, and convenient coffee products. Their preference for innovative coffee experiences, convenience, and lifestyle-oriented brands is reshaping coffee consumption patterns across the region. Furthermore, rising urbanization and increasing disposable incomes among these young populations further propel market growth. As a result, companies are focusing marketing, product development, and distribution strategies to cater to the tastes and lifestyle demands of this dynamic and sizeable youth segment, unlocking significant opportunities in the Asia-Pacific coffee market.

Health and wellness trends boosting consumption of organic and certified coffee

Health and wellness trends are significantly boosting the consumption of organic and certified coffee in the Asia-Pacific market. Increasing consumer awareness about the benefits of organic products, including reduced exposure to synthetic chemicals and pesticides, is driving demand for organic coffee, especially in countries like India and China. Young consumers, in particular, are motivated by sustainability, ethical sourcing, and health-conscious choices, preferring coffee that aligns with their values. This has encouraged key market players to expand their portfolios with organic and specialty coffee options, such as Lavazza’s Tierra Bio-Organic and Blue Tokai’s biodegradable specialty capsules. The rise in demand is further supported by shifting eating habits and the desire for higher-quality, natural products, fueling expansion in coffee pods and capsules as well. Additionally, sustainable packaging and clean labeling are becoming crucial factors for brand success in the region, reinforcing the trend toward premium and organic coffee consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and supply chain disruptions | -1.1% | Regional, highest impact on import-dependent markets | Short term (≤ 2 years) |

| Competition from other alternative beverages | -0.8% | Traditional tea markets: China, Japan, India | Medium term (2-4 years) |

| Climate change impact on coffee production | -0.6% | Producer countries: Vietnam, Indonesia, Thailand | Long term (≥ 4 years) |

| High operational and raw material costs | -0.9% | Urban markets with high real estate costs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price volatility and supply chain disruptions

Price volatility and supply chain disruptions pose significant restraints to the Asia-Pacific Coffee Market. The region has experienced notable fluctuations in coffee bean prices, driven by adverse weather conditions in key producing countries like Brazil and Vietnam, which have led to lower yields and tightened supply. For example, Arabica coffee prices surged nearly 30% and Robusta prices soared over 40% in mid-2025, reaching their highest levels in over a decade. Added to this are geopolitical tensions, rising tariffs (such as the 50% tariff imposed by the U.S. on Brazilian coffee imports), and increased logistics and labor costs, all of which contribute to rising operational expenses. Supply chain interruptions due to regulatory changes, tighter export rules, and freight challenges further complicate the market environment. These factors collectively lead to higher wholesale and retail prices, reduce profit margins for roasters and distributors, and create uncer

Competition from other alternative beverages

Competition from alternative beverages poses a significant restraint to the Asia-Pacific Coffee Market. The region’s diverse and rapidly expanding landscape includes strong consumer preference growth for tea, herbal drinks, functional beverages, and ready-to-drink (RTD) products such as flavored waters and energy drinks. Traditional tea consumption remains deeply rooted in many Asia-Pacific countries, and emerging health and wellness trends encourage consumers to explore non-coffee options perceived as lighter or more beneficial for digestion and hydration. Additionally, the rapid proliferation of RTD coffee and non-coffee beverages offers convenient, on-the-go alternatives that attract busy, younger consumers. This competition not only limits market share expansion for traditional coffee products but also forces coffee players to innovate in product offerings and marketing strategies. As a result, the coffee market faces ongoing challenges in retaining and growing consumer loyalty amidst a growing variety of beverage choices vying for consumer attention and expenditure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pods Dominate While Instant Accelerates

Coffee pods and capsules accounted for the largest market share in 2025, standing at 32.18% in the market. This dominance highlights consumers’ strong preference for convenience without compromising on quality or flavor consistency. Pods and capsules offer a premium coffeehouse experience at home or in the workplace, making them particularly attractive in urban and fast-paced lifestyles across the region. The growing penetration of single-serve brewing machines in households and offices further supports this segment’s expansion. Additionally, the availability of a wide variety of flavor options and innovations in sustainable packaging are reinforcing consumer acceptance. International coffee brands and regional players are increasingly focusing on this format, as it provides high margins and strong brand loyalty.

While pods and capsules hold the largest share, instant coffee stands out as the fastest-growing segment in the Asia-Pacific coffee market, with a projected CAGR of 6.61% through 2031. Traditionally seen as an economical and accessible option, instant coffee has been undergoing significant transformation due to advancements in freeze-drying and flavor preservation technologies. These improvements are reducing the quality gap between instant varieties and freshly brewed coffee, making the category more appealing to younger and discerning consumers. Rising demand in emerging economies, combined with on-the-go lifestyles, is amplifying this trend. Moreover, manufacturers are launching premium, specialty, and flavored instant coffee formats to capture evolving consumer palates. The strong push towards convenience, affordability, and evolving perceptions of quality positions instant coffee as a dynamic growth driver in the overall Asia-Pacific coffee market.

By Flavor: Plain Coffee Holds Ground Against Innovation

In 2025, plain coffee variants commanded the majority share of the Asia-Pacific coffee market, securing an impressive 83.12%. This dominance affirms that most consumers across the region continue to value traditional taste profiles over experimental options. Despite significant efforts by brands to introduce flavored varieties, classic coffee retains loyalty due to its authenticity and familiarity. The strength of this segment is further reinforced by its widespread presence across both retail and foodservice channels. Cultural preference for unaltered coffee flavors, particularly in mature markets, has underpinned its sustained leadership. Moreover, the affordability and wide availability of plain coffee in multiple formats make it the go-to choice for price-sensitive as well as habitual consumers. This entrenched preference reflects how tradition continues to outweigh innovation when it comes to mainstream consumption drivers in Asia-Pacific.

In contrast to the dominance of plain coffee, flavored coffee has emerged as the fastest-growing segment, projected to expand at a robust CAGR of 6.44% through 2031. This growth is strongly influenced by younger demographics who show a clear inclination toward variety and novelty in their consumption choices. Seasonal campaigns and limited-edition launches by leading coffee brands are creating excitement and boosting trial among new consumers. Moreover, flavored coffee aligns with lifestyle-driven demand for indulgence and experiential consumption, particularly within urban markets and café culture. The proliferation of ready-to-drink flavored coffee beverages and specialized café menus further enhances accessibility and desirability. As a result, flavored coffee is steadily reshaping the competitive landscape, offering a blend of innovation and personalization that appeals to modern consumers. This momentum positions the segment as a key challenger to traditional preferences over the forecast period.

By Category: Conventional Dominance Faces Specialty Challenge

In 2025, conventional coffee dominated the Asia-Pacific market with a commanding 90.55% share, underscoring its position as the mainstream preference. This overwhelming dominance is largely attributed to price sensitivity across the region, where affordability often outweighs premium considerations. Established supply chain efficiencies, combined with widespread retail penetration, ensure that conventional coffee remains accessible to the largest consumer base. For the majority of households and foodservice operators, consistent quality at an affordable price remains the top priority. The segment also benefits from strong brand familiarity and established consumption habits that have been built over decades. Taken together, these factors highlight why conventional coffee has entrenched itself as the backbone of the regional coffee industry, serving mass market requirements with reliability and scale.

Although conventional coffee dominates by volume, the fastest-growing momentum lies in specialty, organic, and single-origin varieties, which are projected to expand at a CAGR of 7.45% through 2031. This growth reflects a shift toward premiumization, with consumers increasingly valuing transparency, sustainability, and elevated taste experiences. Younger and more affluent demographics are particularly willing to pay higher prices for coffee that emphasizes ethical sourcing and unique flavor profiles. Cafés, boutique roasters, and online specialty platforms are accelerating this trend by educating consumers about origin stories and artisanal processing techniques. Furthermore, the rise of health-conscious and environmentally aware lifestyles provides a strong foundation for the organic and fair-trade certified segments. While the volume contribution of these premium categories is modest, their disproportionate value growth illustrates a clear bifurcation in the market, where niche yet high-margin offerings are reshaping long-term competitiveness.

By Bean Type: Robusta Leads Despite Arabica's Premium Push

In 2025, Robusta beans held the majority share of the Asia-Pacific coffee market, accounting for 53.96%. This dominance is closely tied to the region’s production strengths, as several Asia-Pacific countries are leading global producers of Robusta. Its cost efficiency and higher yield compared to Arabica make it the preferred choice for mass-market coffee products. Price-sensitive consumers and producers alike favor Robusta, as it delivers affordability without completely compromising quality. Additionally, its strong flavor profile makes it suitable for instant coffee and blends, reinforcing its widespread application in both retail and foodservice channels. The stability of supply chains and competitive pricing have enabled Robusta beans to secure long-standing consumer loyalty. Thus, Robusta continues to be the foundation of the regional coffee market, ensuring accessibility and volume leadership.

While Robusta dominates in volume terms, Arabica beans are expected to record the fastest growth, with a projected CAGR of 6.88% through 2031. This trend reflects the rising influence of premiumization, as consumers increasingly differentiate coffee purchases based on quality and origin. Arabica is favored for its smoother, lighter, and more aromatic flavor profile, appealing to quality-conscious and urban demographics. Growing consumer education about coffee varieties and the influence of specialty cafés are accelerating this demand shift. Moreover, Arabica’s association with origin prestige and artisanal craftsmanship resonates strongly with younger and more affluent buyers willing to pay premium prices. The segment is steadily gaining ground despite higher costs, as evolving preferences underline a move toward value-driven consumption over sheer affordability. This dynamic growth positions Arabica as a key driver of premium coffee evolution in Asia-Pacific.

By Distribution Channel: Off-Trade Dominance Meets On-Trade Growth

In 2025, off-trade channels dominated the Asia-Pacific coffee market, commanding a 75.61% share. This preference is strongly rooted in consumer demand for home consumption, which allows for flexibility in preparation and cost savings compared to on-trade alternatives. Retail distribution through supermarkets, hypermarkets, e-commerce platforms, and convenience stores has boosted accessibility and ensured broad product availability. Off-trade channels also enable bulk purchasing, price comparison, and promotional offers, appealing to families and cost-conscious buyers across the region. The segment benefits from established retail infrastructure and the rise of online grocery platforms, which further strengthen its reach. With convenience, affordability, and product variety as its defining attributes, off-trade remains the backbone of volume sales in the Asia-Pacific coffee market. Its entrenched position highlights how consumer priorities still revolve around practicality and cost efficiency for everyday coffee consumption.

In contrast, on-trade channels represent the fastest-growing segment, projected to expand at a CAGR of 6.74% through 2031. This growth is fueled by the rising popularity of café culture and the experiential value associated with coffee prepared by experts. Social interaction, ambiance, and customization options are driving more consumers, particularly younger generations, to cafés, restaurants, and specialty coffee outlets. The premiumization trend also supports on-trade expansion, as consumers increasingly perceive café-prepared beverages as indulgent and high-quality alternatives to at-home brewing. Urbanization, coupled with the growth of international coffeehouse chains and local specialty cafés, further strengthens this channel’s appeal. Although the segment holds a smaller share compared to off-trade, its momentum underscores a behavioral shift where coffee is not only consumed as a beverage but also experienced as part of a lifestyle. This signals a growing balance in consumption patterns between convenience-driven retail and socially engaging on-premise experiences.

Geography Analysis

In 2025, China commands a dominant 28.74% share of the coffee market, a testament to its vast consumer base and swift urbanization, particularly in tier-one and tier-two cities. The market's sophistication is underscored by local brands harnessing mobile payment and delivery platforms to cater to convenience-driven consumers. These platforms not only enhance accessibility but also align with the fast-paced lifestyles of urban dwellers. In contrast, international players focus on premium positioning and enhancing the overall experience by introducing high-quality products and unique store formats. While the government bolsters domestic consumption and streamlines imports, creating a conducive environment for growth, foreign brands must navigate the intricate regulatory landscape.

India is set to outpace its peers, boasting a robust 6.94% CAGR growth rate through 2031. This surge is fueled by a youthful demographic and increasing disposable incomes, paving the way for an expanded lifestyle category. With current penetration rates still low, the market's potential is vast, offering significant opportunities for both new entrants and established players. Cultural shifts see younger generations adopting coffee not just as a beverage but as a social staple and productivity enhancer, with cafes becoming popular hubs for socializing and remote work. While regional tastes lean towards milk-based coffee, there's ample room for innovative formats and local adaptations, such as flavored options and ready-to-drink variants. As tier-two and tier-three cities witness infrastructure growth, the addressable market expands significantly, enabling businesses to tap into previously underserved areas.

In Japan and South Korea, mature markets are witnessing value growth driven by premiumization and innovative experiences, even as volumes plateau. South Korea's adults guzzle an impressive 405 cups of coffee each annually, paving the way for diverse formats and occasion-centric marketing. Meanwhile, Japan's discerning palate, with its emphasis on meticulous sourcing and preparation, opens doors for specialty and artisanal coffee ventures. Both nations are not just markets but also serve as experimental hubs for global brands, fine-tuning their premium strategies for a wider Asia-Pacific outreach. In Southeast Asia, countries like Indonesia, Thailand, Vietnam, and Malaysia, alongside Australia and New Zealand, showcase varied growth trajectories. Here, local production meets rising consumption, presenting a golden opportunity for regional players to weave an integrated value chain.

Competitive Landscape

The competitive landscape of the Asia-Pacific coffee market is characterized by moderate market concentration and a fragmented competitive structure. This fragmentation allows global brands and regional specialists to coexist, fostering opportunities for niche positioning and format innovation. Health-conscious segments and premium categories, where brand differentiation outweighs scale advantages, are particularly ripe for growth. Global players such as Nestlé, Starbucks, and JDE Peet's leverage their extensive portfolios and supply chain efficiencies to maintain a strong foothold. Meanwhile, regional champions like Luckin Coffee, UCC Ueshima, and Tata Consumer Products utilize their deep understanding of local markets and cultural nuances to gain a competitive edge. The interplay between global and regional players creates a dynamic environment that drives innovation and diversification across the market.

Technology adoption has emerged as a critical differentiator in the Asia-Pacific coffee market. Digital-first brands are increasingly utilizing mobile platforms, data analytics, and delivery integration to enhance customer engagement and streamline operations. These technological advancements provide a competitive advantage over traditional retail-focused competitors, enabling brands to cater to evolving consumer preferences more effectively. Additionally, the integration of technology into the value chain supports personalized marketing strategies and enhances supply chain transparency, further strengthening brand loyalty. As consumers in the region increasingly embrace digital solutions, the role of technology in shaping market dynamics continues to grow.

Strategic collaborations are becoming a cornerstone of success in the Asia-Pacific coffee market. Coffee brands are increasingly partnering with technology platforms, retail chains, and foodservice operators to develop integrated ecosystems that offer comprehensive value propositions. These partnerships enable brands to capture a larger share of consumer spending by addressing multiple consumption occasions and preferences. Furthermore, the focus on ecosystem development over standalone product competition reflects a shift in market strategies, emphasizing long-term consumer engagement and loyalty. This trend underscores the importance of adaptability and innovation in navigating the competitive landscape of the Asia-Pacific coffee market.

Asia Pacific Coffee Industry Leaders

-

The Kraft Heinz Company

-

Starbucks Corporation

-

Luigi Lavazza S.p.A.

-

Nestlé S.A.

-

The J.M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CCL Products (India) Ltd., one of India's largest coffee manufacturers, expanded its premium instant coffee brand, Continental Spéciale. The brand introduced four new flavored variants: Mocha, Vanilla, Caramel, and Hazelnut. This marked the first time these flavors were added to the Continental Spéciale portfolio, underscoring the company's strategic push into India's burgeoning flavored coffee market.

- March 2025: Trung Nguyên Legend established a vast 530,000 sq ft factory in Buôn Ma Thuột, Đắk Lắk province, enhancing its capabilities in processing and exporting robusta coffee. Nestled in Vietnam’s main coffee-growing area, this cutting-edge facility marked a substantial investment of VND 2 trillion (USD 78 million). Importantly, the factory was designed to meet Net Zero sustainability standards.

- January 2025: Nestle Japan rolled out Nescafe Gold Blend Caffeine Half, an instant coffee boasting half the caffeine of its standard counterparts. Nescafe Gold Blend Caffeine Half was available in 20-stick packs in select Japanese drugstores and on Amazon in March.

- February 2024: Hindustan Unilever Limited expanded its Bru Gold portfolio by introducing new coffee flavors, including vanilla, caramel, and hazelnut. This initiative aimed to cater to evolving consumer preferences and enhance its product offerings in the premium coffee segment.

Asia Pacific Coffee Market Report Scope

Coffee is the most popular and consumed brewed drink prepared from roasted coffee beans, which are the seeds of a certain Coffea species. Further, the coffee market is segmented by product type, distribution channel, and geography. Based on product type, the coffee market is segmented into whole-bean, ground coffee, instant coffee, and coffee pods and capsules. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into India, China, Japan, Australia, and the Rest of Asia Pacific. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Whole Bean |

| Ground Coffee |

| Instant Coffee |

| Coffee Pods and Capsules |

| Ready-to-Drink (RTD) Coffee |

By Flavor

| Plain |

| Flavored |

By Category

| Conventional |

| Single Origin/Specialty/Organic |

By Bean Type

| Arabica |

| Robusta |

| Others |

By Distribution Channel

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia |

| New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Rest of Asia-Pacific |

| By Product Type | Whole Bean | |

| Ground Coffee | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| Ready-to-Drink (RTD) Coffee | ||

| By Flavor | Plain | |

| Flavored | ||

| By Category | Conventional | |

| Single Origin/Specialty/Organic | ||

| By Bean Type | Arabica | |

| Robusta | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large will consumer spending on coffee in Asia-Pacific be by 2031?

Aggregate expenditure is projected to reach USD 43.58 billion, reflecting the Asia-Pacific coffee market size growth at a 6.27% CAGR over 2026-2031.

Which product type is expanding the quickest across the region?

Instant Coffee is the fastest mover, posting a 6.61% CAGR as improved freeze-drying narrows flavor gaps with freshly brewed beverages.

What share do pods and capsules currently command?

Pods and Capsules accounted for 32.18% of 2025 revenue, topping the product-type rankings in the Asia-Pacific coffee market.

Which distribution channel will add the most incremental value?

On-Trade outlets—cafés, restaurants, and convenience stores with bean-to-cup machines—are forecast to add the most value, expanding at a 6.74% CAGR thanks to experiential demand.

Why is Arabica gaining traction despite higher prices?

Consumers pursuing smoother flavor and origin storytelling are driving Arabica’s 6.88% CAGR, even though Robusta remains the volume leader.

Page last updated on: