Matcha Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

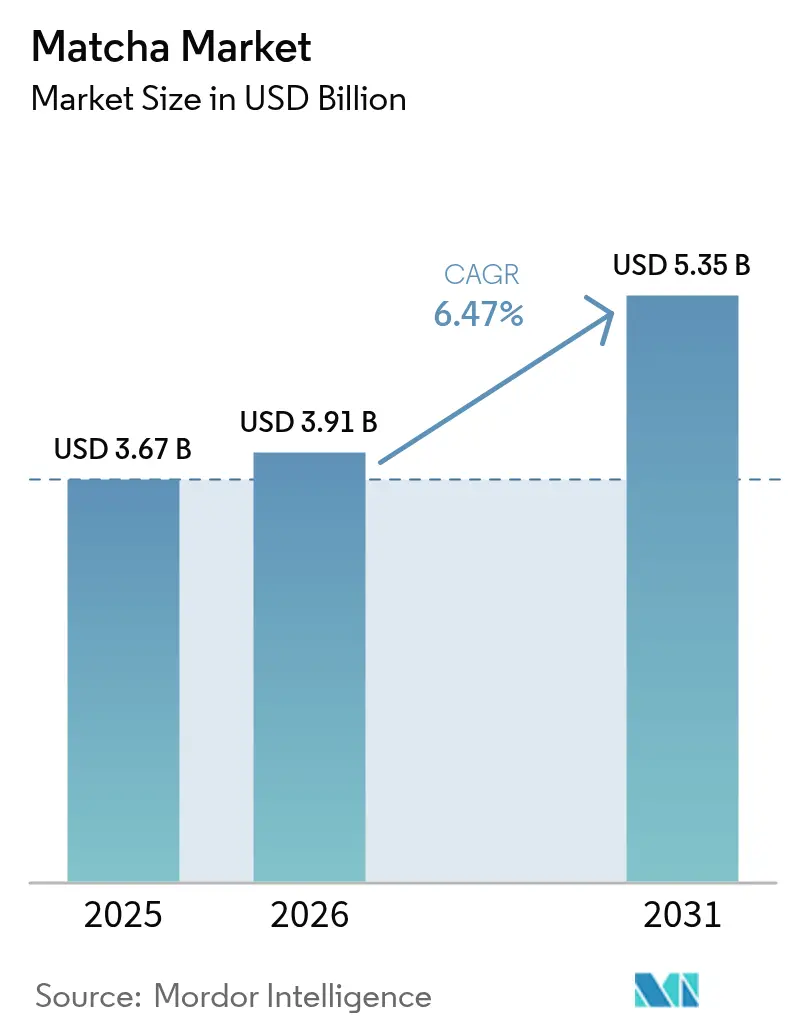

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 5.35 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

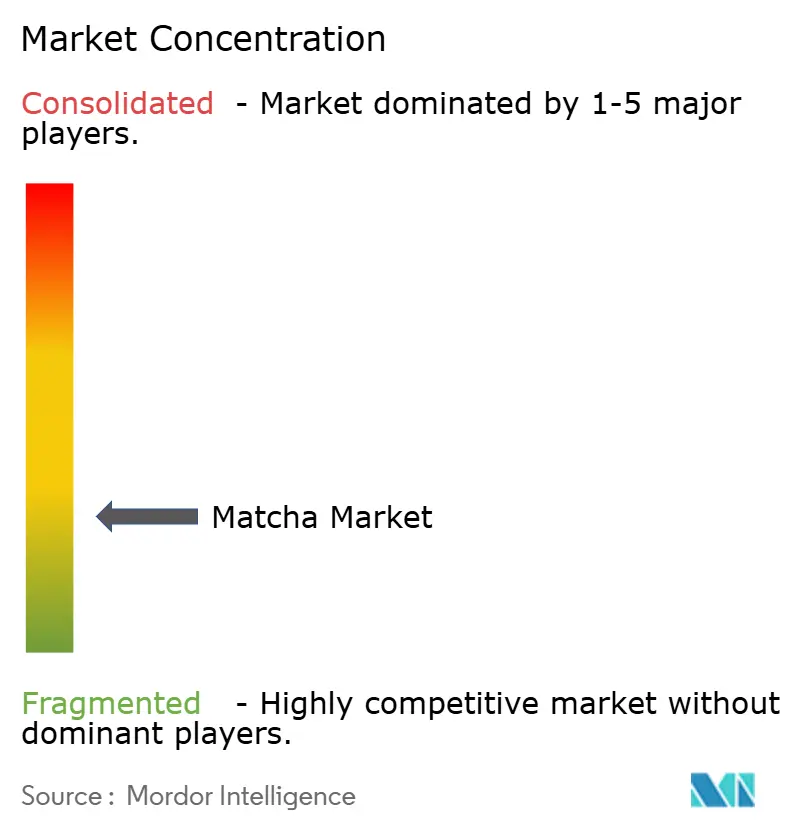

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Matcha Market Analysis by Mordor Intelligence

The matcha market size was valued at USD 3.67 billion in 2025 and estimated to grow from USD 3.91 billion in 2026 to reach USD 5.35 billion by 2031, at a CAGR of 6.47% during the forecast period (2026-2031). This expansion reflects sustained health-centric consumption, social-media visibility that normalizes ceremonial tea traditions, and premium pricing made possible by tight raw material supplies. Robust demand converges with functional food trends, with brands highlighting high L-theanine and antioxidant content to differentiate from conventional caffeinated drinks. The rising adoption of plant-based diets in North America and Europe gives matcha a competitive edge as a dairy-free energy alternative, while rapid e-commerce penetration strengthens direct-to-consumer models that ensure origin authenticity and reinforce premium positioning. Supply diversification initiatives in China and subsidies for Japanese tencha growers aim to mitigate shortages, yet continuing climate and labor constraints keep inventories tight, sustaining higher price realizations.

Key Report Takeaways

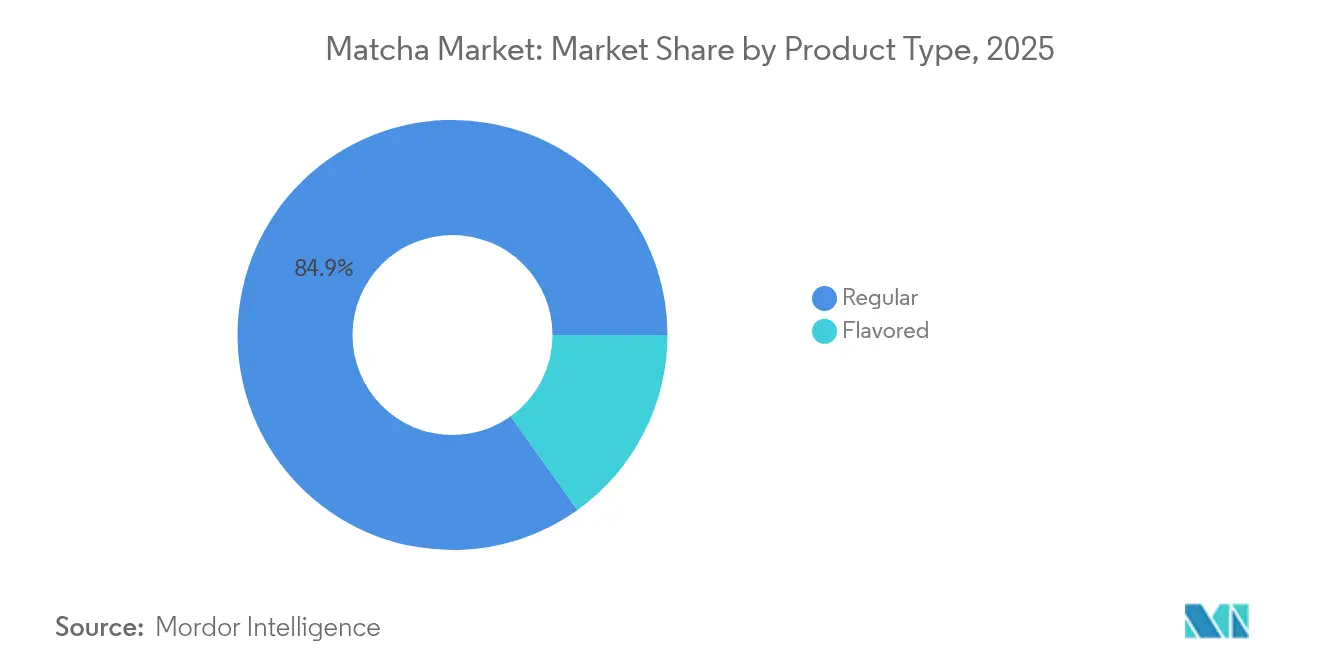

- By product type, regular powder commanded 84.88% of the matcha market share in 2025, while flavored variants are projected to grow at a 7.26% CAGR from 2026-2031.

- By grade, classic led with 53.70% market share in 2025; ceremonial grade is forecast to expand at an 7.98% CAGR through 2031.

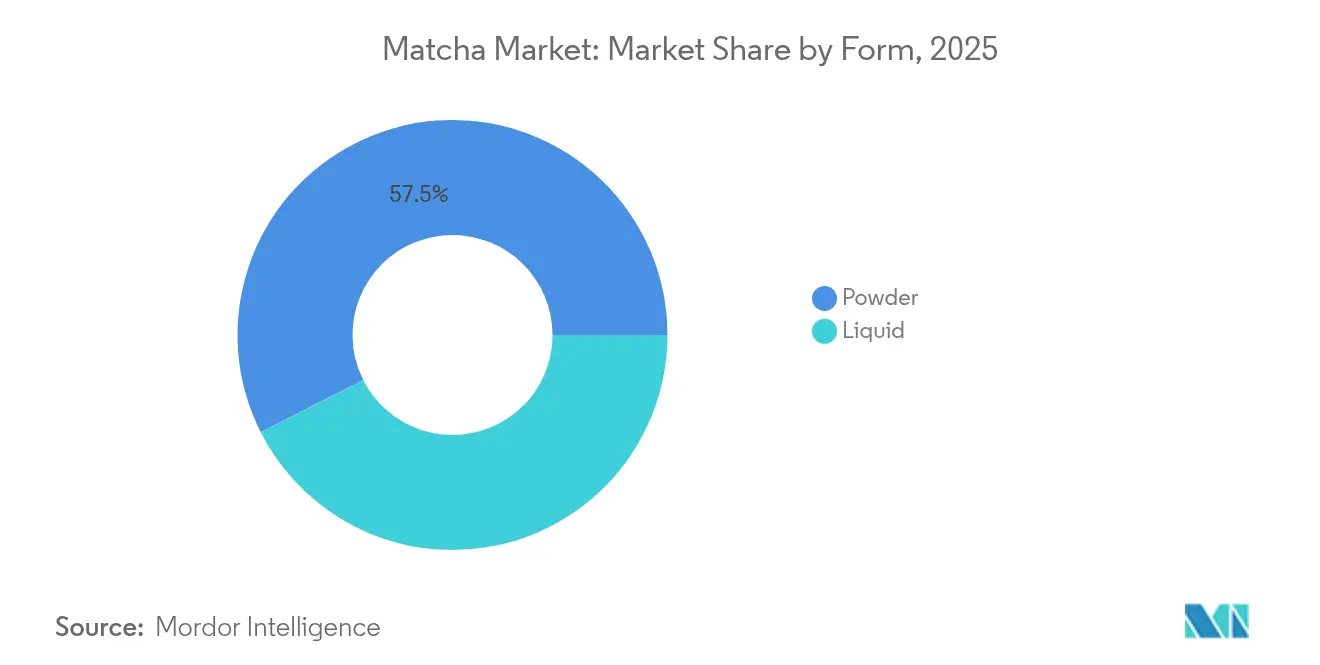

- By Form, the Powder segment led with 57.45% of the market share, while the liquid is expected to grow at a CAGR of 8.41%

- By distribution channel, online retail captured 41.10% share of the matcha market size in 2025, whereas foodservice is advancing at a 7.42% CAGR to 2031.

- By geography, the Asia Pacific held 44.60% of the 2025 value, while North America records the highest regional CAGR at 7.59% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Matcha Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Popularity of functional foods and beverages | +1.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Expansion of plant-based and vegan diets | +1.2% | North America and EU core, spill-over to APAC urban centers | Long term (≥ 4 years) |

| Growth in e-commerce and online retail | +1.0% | Global, particularly strong in emerging markets | Short term (≤ 2 years) |

| Increasing Product Innovation | +0.9% | North America and APAC, with selective EU adoption | Medium term (2-4 years) |

| Increasing Demand for Premium Beverages | +0.7% | Global urban centers, concentrated in high-income demographics | Long term (≥ 4 years) |

| Geographic expansion beyond Asia | +0.6% | North America, Europe, Middle East and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Popularity of Functional Foods and Beverages

Matcha, a key player in the functional foods revolution, offers brands a chance to stand out by backing their claims of health benefits with science. Each serving of matcha packs 2,213 µg/g of caffeine and 20mg of L-theanine, ensuring a steady energy boost without the post-coffee slump. This distinct amino acid blend allows brands to appeal to urban consumers, especially those stressed and seeking cognitive boosts, in a market where mental wellness is highly valued. In Saudi Arabia, research highlights a strong belief in matcha's benefits for heart health and diabetes management. Yet, the sporadic consumption hints at a need for more education rather than a lack of interest. With regulatory bodies, like the FDA, backing functional food claims, brands have a golden opportunity to carve a niche by emphasizing scientifically-validated health benefits over generic wellness claims.

Expansion of Plant-Based and Vegan Diets

As consumers increasingly turn to plant-based diets, the demand for matcha is surging, especially as it offers a protein-rich alternative to traditional dairy beverages. With 17.3g of protein per 100g serving, matcha stands out as a rich source of complete plant protein. According to The Good Food Institute, dollar sales of plant-based proteins in U.S. foodservice channels have grown by 8%, largely driven by younger consumers who align closely with matcha's primary demographic. According to the United States Department of Agriculture data from 2023, 1.58 million people in Germany have a plant-based diet[1]Source: United States Department of Agriculture, " Plant-Based Consumption in Germany", fas.usda.gov. Oatside's recent introduction of a matcha oat latte, boasting 3,750mg of authentic matcha in every 250ml, underscores the trend. This innovation not only highlights matcha's functional advantages but also navigates the taste adaptation hurdles prevalent in Asian markets. Such developments present matcha brands with a golden opportunity: to stake a claim in the burgeoning plant-based market and set premium prices, all while emphasizing health benefits. This trend is especially advantageous for powdered matcha products, which blend effortlessly into plant-based recipes, maintaining both flavor and nutritional integrity.

Growth in E-commerce and Online Retail

As e-commerce expands, it empowers direct-to-consumer models to sidestep traditional retail markups. This shift is pivotal for premium matcha brands, especially amid rising quality concerns over cheaper alternatives. In 2024, online retail channels command a 41.67% market share, underscoring consumer demand for in-depth product details, origin verification, and subscription models that guarantee supply consistency during shortages. This channel proves especially advantageous in emerging markets, where limited traditional retail access to premium Japanese matcha allows brands to engage price-sensitive consumers through direct imports. Furthermore, digital platforms play a crucial role in educating consumers about matcha preparation methods and grade distinctions, effectively dismantling adoption barriers in regions less familiar with the culture.

Increasing Product Innovation

Market expansion is fueled by product innovation, which adapts tastes to uphold matcha's functional benefits. This approach not only navigates cultural acceptance hurdles in non-Asian markets but also fortifies first-mover brands with sustainable competitive advantages. ITO EN's debut of the Matcha Banana Latte and Matcha Cacao Latte in ready-to-drink formats underscores a successful flavor innovation. These offerings cater to convenience-driven consumers, all the while upholding authentic Japanese sourcing credentials. Aiya's launch of a sugar-free sweetened matcha, eyeing the USD 65.31 billion sugar-free beverage market by 2029, showcases how innovation can simultaneously capture market share across diverse health-conscious demographics. Liquid-form products, especially ready-to-drink variants, are witnessing a surge due to their ability to simplify preparation complexities. These formats not only command higher margins than their powdered counterparts but also broaden the market's reach. This trend predominantly favors established players with robust research and development capabilities, posing significant entry challenges for smaller producers who lack formulation expertise.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative superfoods | -0.8% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Price sensitivity in emerging markets | -0.6% | APAC emerging markets, Latin America, MEA | Short term (≤ 2 years) |

| Flavor and cultural acceptance barriers | -0.5% | Non-Asian markets, particularly rural demographics | Long term (≥ 4 years) |

| Adulteration and quality inconsistency | -0.4% | Global, with highest impact in price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Superfoods

As turmeric lattes, spirulina smoothies, and moringa-based drinks vie for the attention of health-conscious consumers, the competition among alternative superfoods heats up. These contenders not only share a similar functional appeal but often come at more accessible price points and boast a deeper cultural resonance. Take the superfood latte arena: matcha finds itself in a tussle with golden milk and other wellness staples. These rivals tout similar antioxidant benefits but sidestep the need for consumers to grasp nuances like preparation methods or quality grades. This rivalry hits hardest in the flavored matcha segment, where taste adjustments blur matcha's distinct profile, aligning it more closely with other functional ingredients. The stakes rise in emerging markets, where local favorites like turmeric, with its akin health benefits, lure price-sensitive consumers due to its significantly lower import costs. To carve out a niche, brands must spotlight matcha's unique bioactive traits, especially its L-theanine content, and educate consumers on its distinct cognitive advantages.

Price Sensitivity in Emerging Markets

In emerging markets, price sensitivity poses adoption challenges. Premium Japanese matcha, priced 3-5 times higher than local tea alternatives, struggles to penetrate the market, even as urban consumers grow more health-conscious. In India, while matcha cafes expand and cultural acceptance rises, higher price points limit accessibility to affluent demographics. This challenge is exacerbated by supply shortages, pushing prices even higher. Major producers, like ITO EN, have implemented 100% price hikes, hitting hardest in price-sensitive markets where purchasing power is limited. In Guizhou Province, China's matcha production is set to expand to a capacity of 5,000 tons by 2025. This move aims to address price sensitivity by introducing lower-cost alternatives, yet concerns over quality hinder entry into the premium market. To navigate these challenges, brands should consider tiered pricing strategies and forge local sourcing partnerships, ensuring they uphold quality standards that validate their premium positioning in more developed markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Regular Dominates Despite Flavored Innovation

In 2025, regular matcha dominates the market with an 84.88% share, underscoring consumer preference for its authentic taste and versatility in culinary and beverage applications. Meanwhile, flavored matcha variants are on track to grow at a 7.26% CAGR from 2026 to 2031, thanks to adept taste adaptation strategies aimed at markets less familiar with matcha. The stronghold of regular matcha in the market suggests that, even with ongoing innovations, core consumers remain steadfast in their appreciation for authenticity and traditional preparation methods that highlight matcha's unique umami flavor. The surge in flavored matcha is predominantly seen in North America and Europe, regions where traditional matcha faces taste adoption challenges. Products like matcha vanilla and matcha chocolate have successfully navigated these palatability hurdles, offering familiar flavors while retaining matcha's functional benefits.

Flavored matcha innovations are leaning towards premium positioning, steering clear of a mere volume chase. Brands such as Aiya are rolling out sugar-free variants, catering to health-conscious consumers who prioritize convenience without sidelining their dietary needs. This segment's allure spans multiple categories, allowing matcha brands to siphon market share from the flavored coffee and tea domains. This cross-category appeal not only familiarizes consumers with matcha but also sets the stage for potential future adoption of regular matcha. However, flavored products face heightened scrutiny in terms of regulatory compliance. The FDA's stringent labeling mandates for added ingredients and allergen disclosures introduce complexities absent in the straightforward labeling of single-ingredient regular matcha.

By Grade: Classic Leads While Ceremonial Commands Premium

In 2025, classic grade matcha commands a dominant 53.70% share of the market, primarily fueling culinary applications and commercial beverage preparations. Meanwhile, ceremonial grade matcha, despite its smaller footprint, is on an impressive trajectory, boasting an 7.98% CAGR from 2026 to 2031. This growth is largely attributed to supply constraints, allowing for premium positioning strategies that resonate with consumers' desire for authenticity. The segmentation by grade underscores their unique applications: classic grade caters to food service and retail, prioritizing cost efficiency, while ceremonial grade's ascent is bolstered by cultural appreciation and social media, transforming matcha consumption into an experiential journey rather than a mere functional one.

While culinary-grade matcha occupies the value segment, predominantly finding its way into food manufacturing and budget-friendly beverages, specific market share figures remain closely guarded secrets among leading producers. Supply chain intricacies play a pivotal role in ceremonial grade's availability. Traditional Japanese producers, valuing their long-standing ceremonial clientele, often sidestep commercial expansion. This selective focus cultivates a scarcity premium, bolstering profit margins. Across all grades, ensuring quality authentication is paramount. Fluorescence spectroscopy and machine learning-based origin identification have demonstrated about 93% accuracy in distinguishing genuine Japanese matcha from matcha of other origins.

By Form: Powder Maintains Versatility Advantage

In 2025, powder matcha commands a dominant 57.45% share of the market. Meanwhile, liquid matcha, despite its smaller footprint, is expected to reach an 8.41% CAGR from 2026 to 2031. Powdered matcha, with its versatility, dominates the market, seamlessly transitioning from traditional ceremonies to diverse applications in food and beverage manufacturing. Meanwhile, liquid, ready-to-drink formats cater to urban consumers, driving growth through a focus on convenience and on-the-go consumption. Powder's market leadership is bolstered by its longer shelf life, reduced transportation costs, and its ability to serve both ceremonial and culinary purposes without being confined to a specific format. E-commerce has further amplified the powder's advantage, allowing for efficient shipping and quality maintenance, unlike its liquid counterpart, which demands meticulous cold chain management.

Liquid matcha products cater to convenience-driven consumers, addressing scenarios where the traditional powder's preparation complexity poses challenges. ITO EN's innovations in portable, ready-to-drink matcha packaging highlight the liquid format's prowess, successfully drawing market share from coffee and energy drinks, all while upholding authentic Japanese sourcing. Liquid format innovations emphasize functional enhancements, exemplified by Oatside's matcha oat latte boasting 3,750mg of real matcha per 250ml, a significant leap from standard market offerings. This segment enjoys premium pricing, as liquid products not only command higher per-serving prices but also simplify the preparation process, overcoming barriers that often hinder powder adoption.

By Distribution Channels: Online Retail Leads Digital Transformation

Online retail achieves 41.10% market share in 2025, reflecting consumer preferences for authenticity verification, detailed product information, and direct-to-consumer relationships that bypass traditional retail markups, while foodservice channels achieve 7.42% CAGR (2026-2031) through menu integration at coffee shops and restaurants targeting experience-focused consumption. The online dominance enables brands to control quality narratives and educate consumers about grade differences, preparation methods, and origin authentication that traditional retail environments cannot effectively communicate. Digital channels particularly benefit premium positioning strategies, as detailed product descriptions and customer reviews support higher price points compared to shelf-based retail competition.

Foodservice growth reflects matcha's transition from specialty ingredient to mainstream menu option, with major chains like Starbucks integrating matcha beverages that introduce new consumers to the category while building familiarity for future retail purchases. Owing to the rising expansion of foodservice channels like coffee shops, restaurants, and others, the demand for matcha products is also growing. According to the Starbucks data from 2024, the company has 10,158 stores in the United States. Specialty stores maintain relevance through curated selection and expert guidance, particularly for ceremonial-grade products requiring preparation knowledge that online channels cannot fully replicate. Supermarket and hypermarket channels face challenges from supply constraints and quality concerns, as mass retail price pressures conflict with premium positioning requirements necessary for authentic Japanese matcha. The distribution landscape increasingly favors channels that can support premium pricing and quality authentication, creating structural advantages for direct-to-consumer and specialty retail models over traditional mass market approaches.

Geography Analysis

In 2025, the Asia Pacific region commands a 44.60% market share, buoyed by Japan's traditional consumption and a surge in adoption in China, India, and Southeast Asia. However, Japan grapples with supply constraints, as its domestic production struggles to satisfy both regional demand and export needs. The region's market dominance is rooted in cultural familiarity and well-established supply chains. Yet, growth rates trail behind those of emerging markets, a reflection of the market's maturity in key consumption areas. Japan, as the primary producer, enjoys certain advantages but also faces vulnerabilities. According to Japan's Ministry of Agriculture, the country's shipments of matcha and other green tea increased by 4% year-on-year to USD 7.47 million in January-May 2023. Meanwhile, in a bid to counteract supply shortages, China's Guizhou Province is ramping up matcha production, eyeing a target of 5,000 tons of capacity by 2025. However, positioning this output in terms of quality remains a hurdle when juxtaposed with traditional Japanese sources, as noted by Our China Story. In India, the burgeoning matcha cafe culture signals regional growth potential, yet price sensitivity curtails widespread market penetration, confining it largely to affluent urban demographics.

North America is set to witness the fastest regional growth, boasting a 7.59% CAGR from 2026 to 2031. This surge is fueled by a rising health consciousness, the pervasive influence of social media, and adept strategies that have successfully navigated cultural unfamiliarity. Innovations in flavored and ready-to-drink matcha have played a pivotal role in this adaptation. The region's robust e-commerce infrastructure bolsters direct-to-consumer models. This dynamic allows premium Japanese producers not only to uphold quality control and assert pricing power but also to educate consumers on authenticity and preparation methods. While Canada and Mexico emerge as promising markets, development is predominantly centered in major urban hubs, where health-conscious consumers resonate with matcha's premium allure. Furthermore, the region's growth is bolstered by regulatory frameworks endorsing functional food claims. This support empowers brands to distinguish themselves through scientifically-validated health benefits, moving beyond generic wellness narratives.

Europe, South America, and the Middle East and Africa present burgeoning growth prospects, each with unique regional traits. These nuances necessitate bespoke market entry strategies that cater to local taste inclinations, price sensitivities, and cultural acceptance hurdles. South America, still in its infancy regarding matcha consumption, offers a canvas for brands. By forging local partnerships to address price concerns while upholding quality, brands can carve a niche in this underdeveloped market. However, entering these emerging regions isn't without challenges. Brands must invest heavily in consumer education and cultural adaptation. Yet, the rewards are significant: first-mover advantages await those who adeptly navigate entry barriers and establish genuine positioning before the market reaches saturation.

Competitive Landscape

The matcha market, rated at a moderate concentration, presents a dual opportunity: established players can fortify their positions, while emerging brands can carve out their niche. These newcomers are leveraging differentiated strategies that prioritize quality, authenticity, and cultural adaptation. Traditional Japanese producers, including ITO EN, Marukyu Koyamaen, and Aiya, boast competitive edges rooted in authentic origins and long-standing supply relationships. However, these advantages come with a caveat: capacity constraints that hinder expansion. This limitation paves the way for alternative sourcing strategies. A notable trend is the push towards vertical integration.

Leading players are forging direct farming ties and enhancing processing capabilities. This not only ensures stringent quality control but also mitigates supply chain risks, which have been exacerbated by climate challenges and surges in tourism-driven demand. Emerging markets present a unique challenge: cultural unfamiliarity. This creates hurdles for traditional players, but also opens doors for innovative brands. By adapting tastes, offering convenient formats, and employing educational marketing, these brands are successfully building category awareness and capturing market share. In this landscape, technology adoption stands out as a pivotal differentiator. Tools like fluorescence spectroscopy and AI-driven quality assessments are not just tech novelties; they're essential for verifying authenticity. This is especially crucial given rising consumer concerns over adulteration and origin fraud.

Disruptors such as Isshiki Matcha are making waves by harnessing digital strategies and community engagement, establishing brand recognition without the need for traditional retail investments. In contrast, industry giants like Starbucks and PepsiCo wield distribution scale advantages, positioning them for rapid market expansion once they achieve consumer acceptance. Navigating the competitive dynamics further complicates the landscape, especially with FDA compliance. Regulatory mandates on import safety and labeling precision tend to favor established players, who often have robust quality management systems, over smaller producers that may lack such compliance infrastructure.

Matcha Industry Leaders

-

AOI Tea

-

AIYA America Inc

-

Pique

-

ITO EN Ltd.

-

Midori Spring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Actress Sanya Malhotra launched a new matcha brand, Bree Matcha in partnership with Essanza Nutrition. The brand offers ceremonial matcha, regular matcha, and a matcha kit.

- June 2025: Miko launched a range of premium matcha powder. Miko's genuine Matcha Japanese green tea, boasting an earthy and bittersweet flavor, is packed with antioxidants and nutrients, making it a versatile choice for both hot and cold beverages.

- June 2025: Starbucks Japan launched a new limited-edition matcha drink at selected stores. The products include matcha green tea, matcha pistachio mousse latte, and many others. The drinks have smooth texture and unique taste.

- February 2024: Aiya Matcha acquired a majority stake in OMGTea to bring matcha to the masses. This collaboration aimed to expand and build a more extensive presence in the United Kingdom.

Global Matcha Market Report Scope

Matcha is a unique, powerful form of green tea grown in the shadow for three to four weeks before harvest. The global matcha market is segmented by product, form, distribution channel, and geography. By product, the market is segmented into regular tea and flavored tea. By state, the market is segmented into powder and liquid forms. By distribution channel, the market is segmented into hypermarkets/supermarkets, specialty stores, online retail stores, and others. By geography, this report includes an analysis of regions like North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). For each segment, the market sizing and forecasts have been done based on value (in USD).

| Regular |

| Flavored |

| Ceremonial |

| Classic |

| Culinary |

| Powder |

| Liquid |

| Foodservice | |

| Retail | Supermarket/Hypermarkets |

| Specialty Stores | |

| Online Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Regular | |

| Flavored | ||

| By Grade | Ceremonial | |

| Classic | ||

| Culinary | ||

| By Form | Powder | |

| Liquid | ||

| By Distriution Channels | Foodservice | |

| Retail | Supermarket/Hypermarkets | |

| Specialty Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for matcha be in 2031?

Forecasts indicate the matcha market will reach USD 5.35 billion by 2031, up from USD 3.91 billion in 2026.

Which region is expanding fastest for matcha products?

North America posts the quickest growth with a 7.59% CAGR between 2026 and 2031, supported by plant-based diet trends and strong café culture.

Which sales channel dominates matcha distribution?

Online retail commands 41.10% of 2025 revenue, reflecting consumer trust in direct-to-consumer authenticity assurances.

What are the main challenges for new matcha entrants?

Key barriers include high raw material costs, authentication requirements to combat adulteration, and consumer education on preparation techniques.

Page last updated on: