Meat Flavors Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.40 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

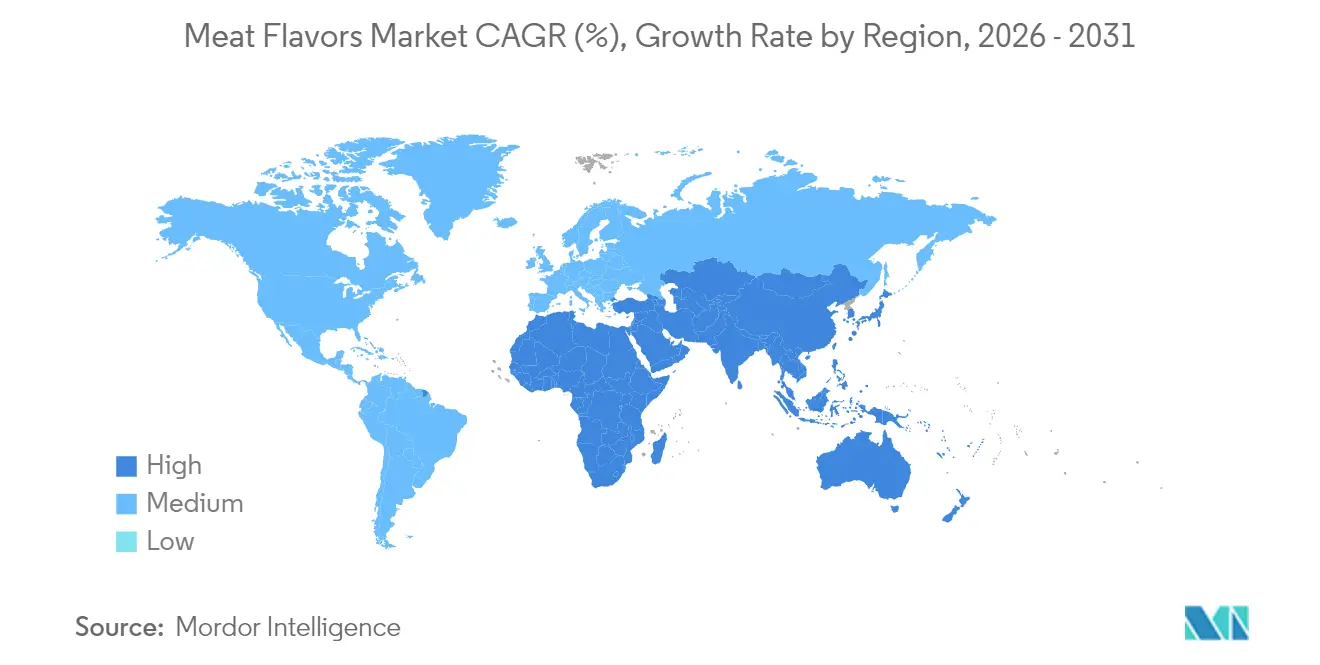

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

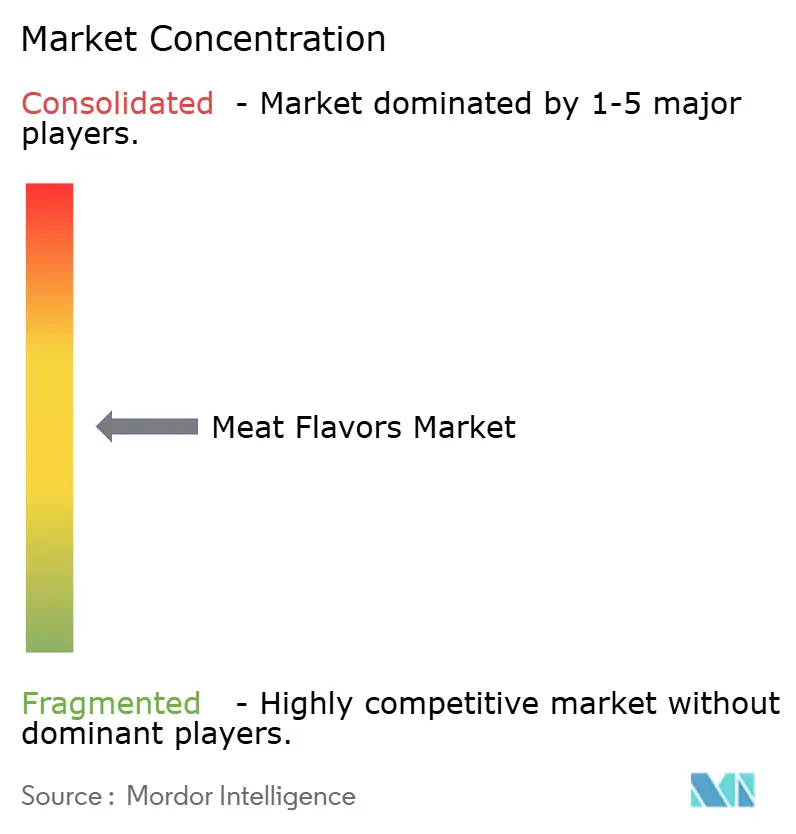

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Meat Flavors Market Analysis by Mordor Intelligence

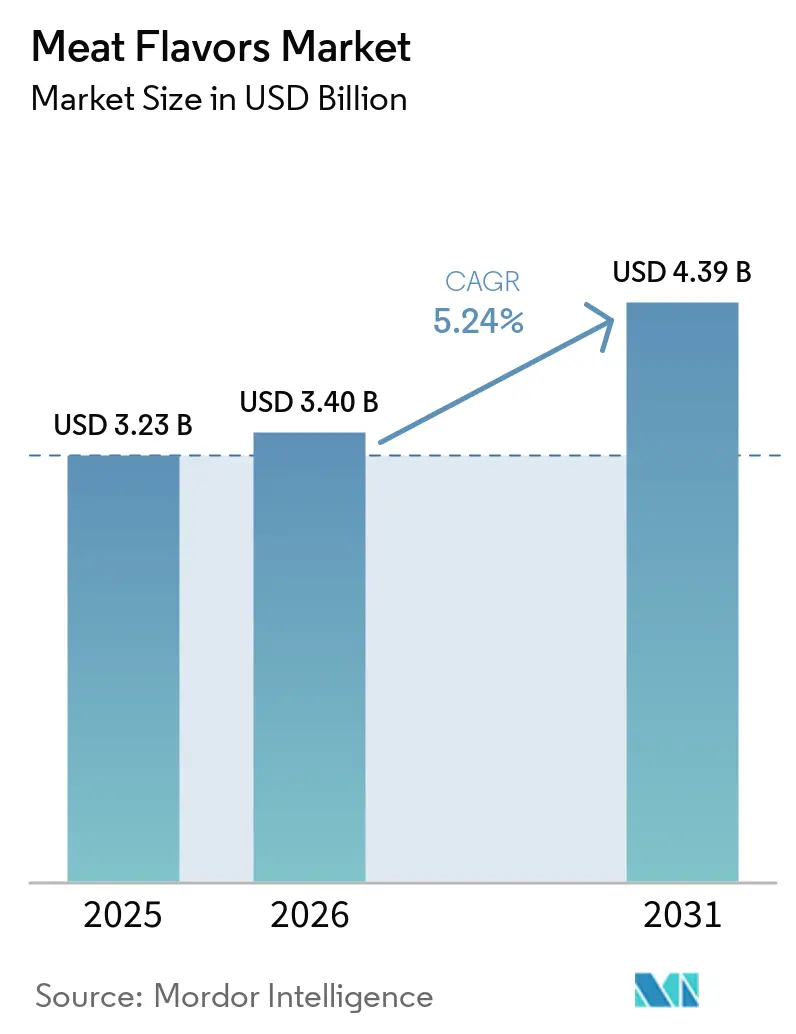

The meat flavors market size was valued at USD 3.23 billion in 2025 and estimated to grow from USD 3.4 billion in 2026 to reach USD 4.39 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). As demand surges for clean-label convenience foods, suppliers are reshaping their economics and product portfolios. This shift is driven by advancements in precision fermentation and a growing regulatory acceptance of nature-identical pathways. In North America and Europe, regulations favor enzymatic and microbial routes, anchoring growth in natural formulations. However, artificial variants still cater to value-tier segments where cost considerations overshadow label scrutiny. Flavor houses are innovating processes to counter raw-material volatility, with a keen eye on geographic expansion in Asia-Pacific. Here, volumes of instant noodles and ready meals far surpass Western benchmarks. While competitive intensity remains moderate, allowing space for regional specialists and biotech newcomers, the market's top five suppliers are ramping up merger and aquisitions activities to secure fermentation assets, as highlighted by Kerry Group.

Key Report Takeaways

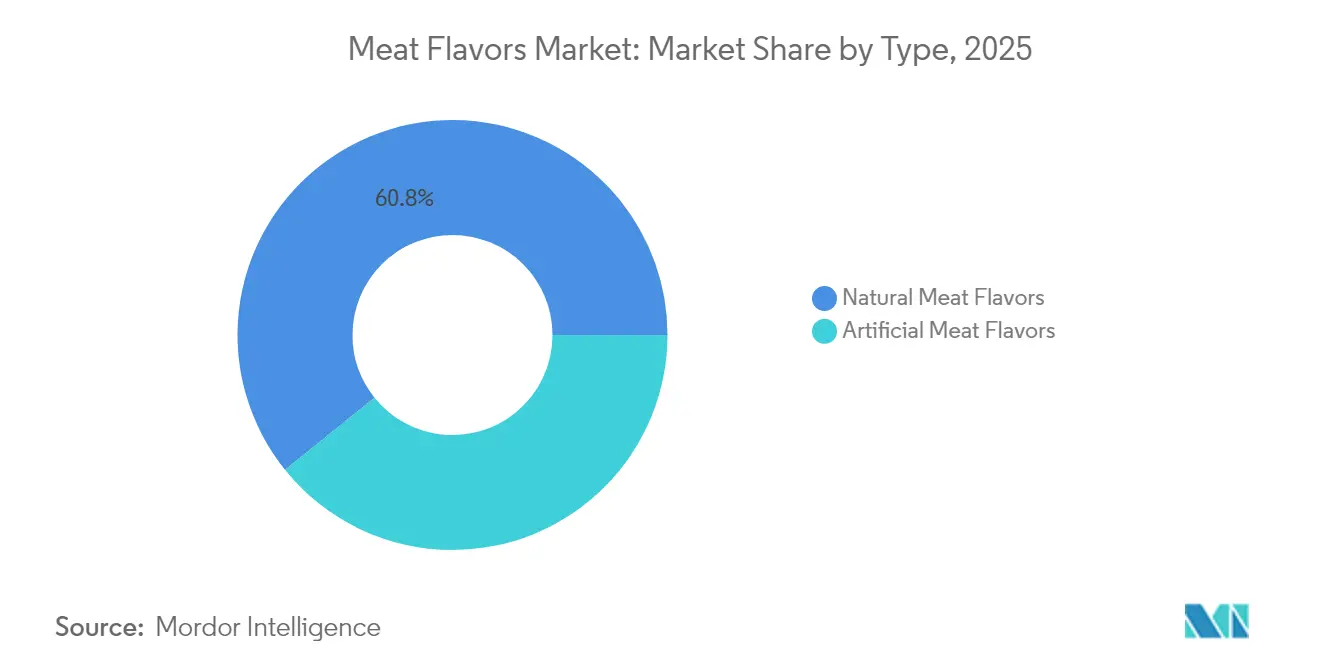

- By type, natural meat flavors held 60.78% of 2025 revenue and are forecast to expand at a 4.95% CAGR through 2031, while artificial variants lag at 4.12% CAGR.

- By flavor, beef led with 27.10% of 2025 sales; chicken is set to post the fastest 5.05% CAGR between 2026 and 2031 on plant-based and halal tailwinds.

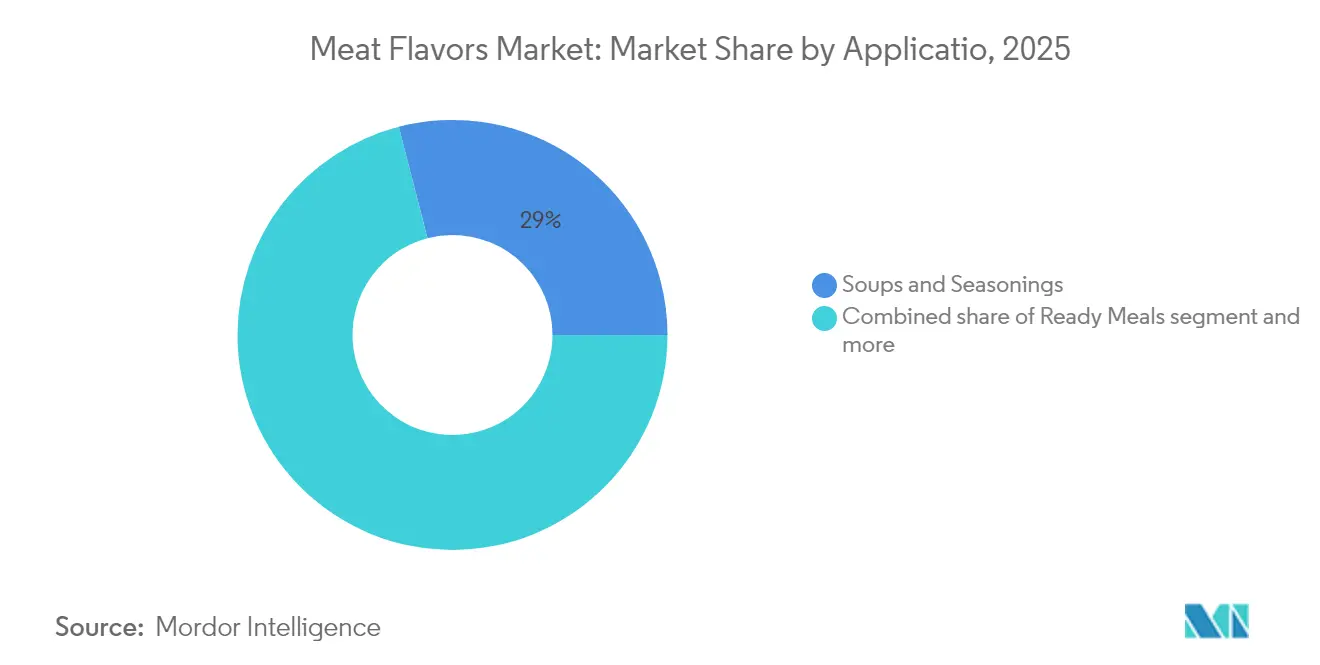

- By application, soups and seasonings commanded 29.02% share in 2025, yet ready meals are projected to grow at a 5.83% CAGR to 2031.

- By geography, North America accounted for 33.78% of 2025 turnover; Asia-Pacific is expected to record the quickest 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meat Flavors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience and ready-to-eat meals | +1.2% | Global, strongest in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Shift toward natural and clean-label ingredients | +1.0% | North America, EU core, premium Asia-Pacific spillover | Long term (≥ 4 years) |

| Expansion of plant-based meat alternatives | +0.8% | North America, Europe, Australia, tier-1 Chinese cities | Medium term (2-4 years) |

| Enzymatic and precision-fermentation breakthroughs | +0.6% | Global, led by United States and Europe research and development hubs | Long term (≥ 4 years) |

| Direct-to-consumer savory snack launches | +0.5% | North America, Europe, emerging Southeast Asia | Short term (≤ 2 years) |

| Regulatory, nutrition, and reformulation pressure | +0.4% | Europe and North America, cascading to Asia exporters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience and ready-to-eat meals

In 2024, households prioritized speed without sacrificing taste complexity, leading frozen and ambient ready meals to capture 38% of the incremental meat flavor volume. The U.S. frozen-entree category saw unit sales grow by 6.2% in 2024, surpassing pre-pandemic baselines. Meanwhile, in India, instant noodles consumption surged to 8.2 billion servings, up from 7.1 billion in 2023, as reported by the World Instant Noodles Association[1]Source: World Instant Noodles Association, " Demand Rankings" , instantnoodles.org. This rising demand is prompting flavor houses to craft heat-stable, microwave-resilient profiles that maintain their integrity during reheating. A testament to this trend is Kerry Group's 2024 introduction of a lipid-encapsulated beef flavor, tailored for 900-watt microwaves, ensuring a consistent Maillard character across diverse power settings. The message is unmistakable: flavor suppliers now need to collaborate closely with packaging engineers to uphold sensory integrity throughout the cold chain and during the final heating process.

Shift toward natural and clean-label ingredients

In 2024, natural meat flavors dominated the market, claiming a 61.27% share. However, the term "natural" is hotly debated worldwide. While the FDA's 21 CFR 101.22 allows for enzymatic hydrolysis and fermentation to be labeled as natural, the EU, under its Regulation 1334/2008, takes a stricter stance, excluding certain microbial strains. This divergence means brands operating on both sides of the Atlantic must create two formulations. As a result of this regulatory split, multinational companies are seeing compliance costs rise by an estimated 12% to 15%. In response, DSM Firmenich streamlined its natural-flavor research and development in 2024, centering it on a single platform that meets EU standards. They opted for a heftier initial investment to sidestep the need for multiple market-specific SKUs. The broader lesson? While clean-label premiums exist, they're not universally applicable. Companies aligning with the strictest standards may find operational ease, but it often comes at the cost of immediate profit margins.

Expansion of plant-based meat alternatives requiring authentic meat flavors

In 2024, global retail sales of plant-based meat analogs hit USD 7.8 billion, with chicken and beef alternatives making up 72% of the volume. However, consumer repeat purchase rates linger below 40%, primarily due to perceived gaps in flavor and texture. In response to this sensory shortfall, alt-protein brands are ramping up flavor intensity by 20% to 30% compared to traditional meat products. This shift has carved out a lucrative niche for suppliers adept at delivering heme-like umami and fat-soluble roasted notes, all without relying on animal inputs. Highlighting this trend, Givaudan forged a partnership in 2024 with a precision-fermentation startup, aiming to craft heme proteins specifically for plant-based burgers. This move signals a blending of flavor and functional ingredients. The overarching takeaway is that suppliers traditionally focused on meat flavors are now positioning themselves as sensory designers within the alt-protein realm, a pivot that allows them to command margins 25% to 35% higher than standard commodity applications.

Enzymatic and precision-fermentation breakthroughs lowering cost of high-fidelity meat notes

In 2024, precision fermentation platforms matched the costs of select volatile compounds with those derived from animals. This milestone was achieved as microbial strain optimization and bioreactor scale-up efforts slashed production costs by 35% to 40% year-over-year. Meanwhile, IFF's innovative enzymatic method, which utilizes lipase catalysis to produce roasted-chicken volatiles, successfully shortened the cycle time from 72 hours to 43 hours. This advancement led to a notable 28% decrease in capital intensity for each kilogram of the finished flavor. Such innovations are broadening access to high-fidelity flavor profiles, once reserved for premium tiers. This shift is narrowing price bands and compelling established players to pivot their competition focus from raw flavor potency to application support. Strategically, this evolution underscores the rising importance of process patents, which are now overshadowing traditional formulation secrecy as the key asset for defense.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global regulations on flavor additives and labeling | -0.7% | EU and North America; cascading to export markets in Asia and South America | Medium term (2-4 years) |

| Volatility of animal-derived raw-material costs and supply | -0.6% | Global, with acute pressure in Asia-Pacific and South America | Short term (≤ 2 years) |

| Consumer sensory-fatigue shift to subtler profiles | -0.4% | North America and Europe premium segments; limited impact in Asia-Pacific | Long term (≥ 4 years) |

| Biotech universal umami boosters reducing need for meat-specific flavors | -0.3% | Global, led by North America and Europe innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent global regulations on flavor additives and labeling

Regulatory differences among FDA's GRAS, EU's Regulation 1334/2008, and JECFA standards are fragmenting global flavor portfolios and driving up compliance costs. The EU's 2024 amendment to Regulation 1334/2008 set stricter limits on certain pyrazines and furans, often associated with roasted-meat flavors[2]Source: European Food Safety Authority, " Safety and efficacy of pyrazine derivatives including saturated ones belonging to chemical group 24 when used as flavourings for all animal species", efsa.onlinelibrary.wiley.com. This change necessitated reformulations for about 18% of the region's marketed SKUs. While FEMA's GRAS status in the U.S. is recognized, it doesn't guarantee approval in the EU. This discrepancy mandates the preparation of separate safety dossiers, delaying market entry by an additional 9 to 12 months. As a result of these regulatory challenges, multinational flavor companies are now adopting the most stringent standards as their global norm, prioritizing operational simplicity over cost efficiency.

Volatility of animal-derived raw-material costs and supply

In 2024, prices for core meat flavor precursors hydrolyzed vegetable protein, yeast extracts, and rendered animal fats swung between 18% and 25%. These fluctuations were driven by drought-induced feed-crop shortages in South America and outbreaks of African swine fever in Southeast Asia. Such volatility has tightened margins for flavor suppliers bound by fixed-price contracts with food manufacturers, particularly impacting profitability in lower-tier applications. Cargill's move in 2024 to establish a USD 120 million fermentation facility in Iowa for yeast-extract production underscores a significant industry trend. This shift towards captive supply chains aims to mitigate input volatility. The overarching message is clear: hedging raw materials and backward integration have transitioned from being mere optimizations to essential competitive strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Formulations Dominate Amid Fermentation Convergence

In 2025, natural meat flavors dominated the market, capturing a 60.78% share. Forecasted to expand at a 4.95% CAGR until 2031, this segment's growth is largely attributed to clean-label mandates in North America and Europe. These mandates favor enzymatic hydrolysis and microbial fermentation methods, steering clear of synthetic precursors. Thanks to strides in precision fermentation and enhanced bioreactor efficiencies, the cost gap between natural and artificial meat flavors shrank to 15% in 2024, down from 28% in 2020. This reduction has muddied the waters between regulatory definitions of "natural" and "nature-identical." Notably, microbial strains engineered for meat volatiles are now challenging traditional interpretations under both FDA and EU guidelines.

While artificial meat flavors are on a slower growth trajectory, they play a pivotal role in price-sensitive markets. These include sectors like institutional foodservice and export-driven instant noodles, where consumer scrutiny is less intense. Despite their tempered expansion, artificial flavors boast benefits such as heat stability and an extended shelf life. These traits are crucial for ambient noodle seasonings, especially in regions like Southeast Asia and Latin America, which grapple with limited cold-chain infrastructure. Yet, a growing global aversion to "artificial" labeling is evident. A 2024 survey highlighted this trend, revealing that 42% of urban Chinese consumers now shun products with artificial flavors, a notable rise from 31% in 2023. This evolving sentiment is prompting multinational brands to pivot, reformulating products with natural substitutes, even at the cost of an 8-12% margin squeeze. As a result, artificial flavors are carving out a niche, primarily utilized where cost or technical requirements take precedence over consumer inclinations.

By Flavor Type: Chicken Surges on Plant-Based and Halal Tailwinds

In 2025, beef flavor dominated the market, seizing 27.10% of the share, thanks to its deep-rooted presence in soups, sauces, and instant noodles. Its rich, familiar taste keeps it at the forefront of retail and foodservice menus, especially in comfort and everyday savory dishes. This stronghold in essential categories ensures a steady, high-volume demand across regions. Additionally, its widespread acceptance across diverse cuisines and its ability to enhance the umami profile of dishes further reinforce its position. Thus, while the meat flavor portfolio diversifies, beef flavor remains its primary anchor, consistently driving demand and maintaining its relevance.

Chicken flavor is rapidly gaining traction, boasting a 5.05% CAGR. Manufacturers are increasingly incorporating it into plant-based meat matrices and products that adhere to global halal standards. Its milder, less polarizing profile permits a more pronounced flavor in alt-protein formats, sidestepping the metallic or livery off-notes that often plague beef alternatives. This adaptability positions chicken flavor as a prime candidate for innovation in both conventional and alternative protein products. Furthermore, its compatibility with a wide range of culinary applications, from soups and broths to snacks and ready-to-eat meals, enhances its appeal. As a result, chicken is solidifying its role as the growth engine in the meat flavors category, particularly for brands catering to health-, ethics-, and religion-focused consumers.

By Application: Ready Meals Outpace Soups as Convenience Preimmunizes

In 2025, soups and seasonings dominated the market, capturing 29.02% of the share. Their prevalent use in instant noodles and bouillon cubes, both in retail and foodservice, underscores their significance. Particularly in the Asia-Pacific region, where instant noodle consumption soars, these ingredients anchor the global demand for meat flavors. While other applications are on the rise, the consistent demand for soups and seasonings not only stabilizes production planning but also optimizes capacity utilization. This solidified stance guarantees their status as the primary revenue source for flavor suppliers throughout the forecast period.

Ready meals are on a rapid ascent, with projections indicating a 5.83% CAGR. This surge is fueled by the post-pandemic appetite for restaurant-style convenience at home, especially through frozen and chilled SKUs. Unlike instant noodles, which see flavor-loading costs at 0.4% to 0.6% of the finished product, ready meals can shoulder higher costs of 0.8% to 1.2%. This flexibility allows manufacturers to opt for premium natural and fermented flavor systems, justifying a 20% to 30% price premium. Their readiness to invest in superior taste profiles not only highlights the value of ready meals but also steers suppliers to focus their innovation efforts in this direction. Thus, while soups and seasonings command the largest volume share, ready meals are carving out a niche as the primary engine of value growth.

Geography Analysis

In 2025, North America accounted for 33.78% of total revenue. However, growth has decelerated to a 4.62% CAGR. This slowdown comes as restaurant traffic sees a rebound, reducing the demand for at-home meal solutions, and household formations reach a plateau, limiting new consumer segments. Regulatory costs pose a challenge, as FDA GRAS petitions and state-level disclosures can extend launch a product's launch timelines by an entire year, increasing time-to-market and associated expenses. In Canada, immigration is driving a surge in demand for soups and noodles, as diverse consumer groups seek convenient meal options. Meanwhile, in Mexico, the snack-seasonings market is witnessing a robust 6.8% CAGR, fueled by brands tailoring their profiles to local tastes and preferences, which resonate strongly with regional consumers.

Asia-Pacific emerges as the region with the fastest growth, boasting a 6.88% CAGR. This expansion is largely driven by China's staggering consumption of 46.2 billion instant noodle servings annually, reflecting the region's strong demand for quick and affordable meal options. Additionally, a growing preference for premium SKUs priced above CNY 5 highlights an increasing willingness among consumers to spend on higher-quality products. In India, the ready-meal segment is on an upswing, advancing at a notable 9.2% CAGR, thanks to the rise of dual-income households in urban areas, which prioritize convenience in their food choices. However, these households still exhibit a preference for lower flavor-loading rates, indicating a demand for milder taste profiles. In Southeast Asia, Halal certification plays a crucial role in shaping consumer preferences, with compliant products enjoying a price premium of 15%–20%, as they cater to the region's significant Muslim population and their dietary requirements.

Europe, contributing 24: 23.74% to the overall revenue, faces constraints, managing only a 4.32% CAGR. This limitation is attributed to stringent labeling regulations, which increase compliance costs and slow product launches, and a noticeable consumer shift towards more subtle flavor profiles, reflecting changing taste preferences. However, Eastern Europe is bucking the trend, outpacing the broader region with a growth rate between 6.5% and 7.0%, largely due to the expansion of organized retail, which improves product accessibility and availability. South America, along with the Middle East and Africa, together account for 17.19% of total sales. Yet, they are experiencing a commendable growth rate of 6.2%–6.8%, driven by urbanization, which increases demand for convenient food options, and a focus on localized savory offerings that align with regional tastes and cultural preferences.

Competitive Landscape

The meat flavors market exhibits moderate concentration. The meat flavors market sees key players like Kerry, DSM Firmenich, IFF, Givaudan, and Symrise in the top tier, though none hold outright dominance. These companies are actively pursuing strategic initiatives to strengthen their market positions. For instance, incumbents are acquiring fermentation assets, highlighted by Kerry’s 2024 purchase of a microbial strain, aiming to bolster natural claims and lessen reliance on animal sources. Such acquisitions enable companies to meet evolving consumer preferences for clean-label and sustainable products. Meanwhile, smaller Asian specialists are capitalizing on underrepresented fish and turkey profiles, filling gaps in the portfolios of larger multinationals and addressing niche demands in regional markets.

In this landscape, technology reigns supreme over sheer capacity. IFF has pioneered a lipase-catalyzed process that slashes production time by 40% while maintaining FEMA GRAS status, underscoring the significance of process patents as protective barriers. This technological advancement not only enhances efficiency but also ensures compliance with regulatory standards. Startups like Motif FoodWorks, rooted in precision fermentation, are forging alliances with major flavor companies, merging biotech intellectual property with sensory expertise to cater to the surging demand for plant-based meats. These partnerships are pivotal in addressing the growing consumer shift toward alternative protein sources.

In the Middle East and Southeast Asia, halal-certified solutions command a 15%–20% price premium, spurring regional collaborations. These certifications are crucial in catering to the dietary requirements of Muslim consumers, creating opportunities for market expansion. Industry leaders are not just offering flavors but are co-developing solutions that harmonize flavor performance with challenges in processing, packaging, and shelf life. This collaborative approach ensures that products meet both consumer expectations and operational constraints. While certifications like ISO 22000 and FSSC 22000 serve as foundational benchmarks, the real value now emerges from application engineering, transcending mere compliance and driving innovation in product development.

Meat Flavors Industry Leaders

-

Kerry Group plc

-

International Flavors & Fragrances Inc.

-

DSM Firmenich

-

Givaudan SA

-

Symrise AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DSM Firmenich unveiled a precision-fermentation facility in Singapore, investing EUR 85 million (USD 92 million). The facility, with an annual capacity of 2,400 metric tons, is set to produce natural meat flavors tailored for instant-noodle and ready-meal producers across the Asia-Pacific. The company is also pursuing halal certification for its offerings.

- November 2024: Kerry Group bolstered its natural-flavor portfolio by acquiring a microbial-strain library from a European biotech, renowned for its expertise in umami-compound biosynthesis. This strategic move not only diversifies Kerry's flavor sources but also diminishes its dependence on animal-derived ingredients. The integration of this library is projected to slash production costs by 18% by 2026

- October 2024: Givaudan forged a partnership with Motif FoodWorks, aiming to co-create heme-protein flavors tailored for plant-based beef and pork substitutes. This collaboration melds Givaudan's sensory prowess with Motif's cutting-edge precision-fermentation platform, promising authentic roasted and grilled flavors in alternative protein products.

- September 2024: IFF introduced a groundbreaking lipase-catalyzed enzymatic method for producing roasted-chicken volatiles. This innovation trims the production cycle from 72 hours to a swift 43 hours. Achieving FEMA GRAS status, the process ensures cost competitiveness with traditional extraction methods, all while upholding the integrity of natural labeling.

Global Meat Flavors Market Report Scope

Meat flavors market broadly includes natural and artificial meat flavor offering flavors such as beef, chicken, pork, turkey, fish & seafood and other types. The products offered are applicable in soups & sauces, instant noodles, ready meals, savories, baked goods and other industries

| Natural Meat Flavor |

| Artificial Meat Flavor |

| Beef |

| Chicken |

| Pork |

| Turkey |

| Fish and Seafood |

| Others |

| Soups and Sauces |

| Instant Noodles |

| Ready Meals |

| Snacks and Seasonings |

| Baked Goods |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Natural Meat Flavor | |

| Artificial Meat Flavor | ||

| By Flavor Type | Beef | |

| Chicken | ||

| Pork | ||

| Turkey | ||

| Fish and Seafood | ||

| Others | ||

| By Application | Soups and Sauces | |

| Instant Noodles | ||

| Ready Meals | ||

| Snacks and Seasonings | ||

| Baked Goods | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the Middle East and Africa chocolate market in 2031?

The market is forecast to reach USD 6.90 billion by 2031 on a 5.82% CAGR.

Which country currently leads regional chocolate revenue?

Saudi Arabia, with 43.12% of 2024 revenue thanks to Ramadan and Eid gifting peaks.

Which chocolate type is expanding fastest in the region?

Dark chocolate is projected to grow at 7.24% CAGR between 2025 and 2030 as health concerns rise.

How quickly is online chocolate retail growing in the region?

Online sales are set to advance at a 7.12% CAGR, fueled by 15-minute quick-commerce delivery.

Page last updated on: