Natural Food Flavors Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.81 Billion |

| Market Size (2031) | USD 9.53 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

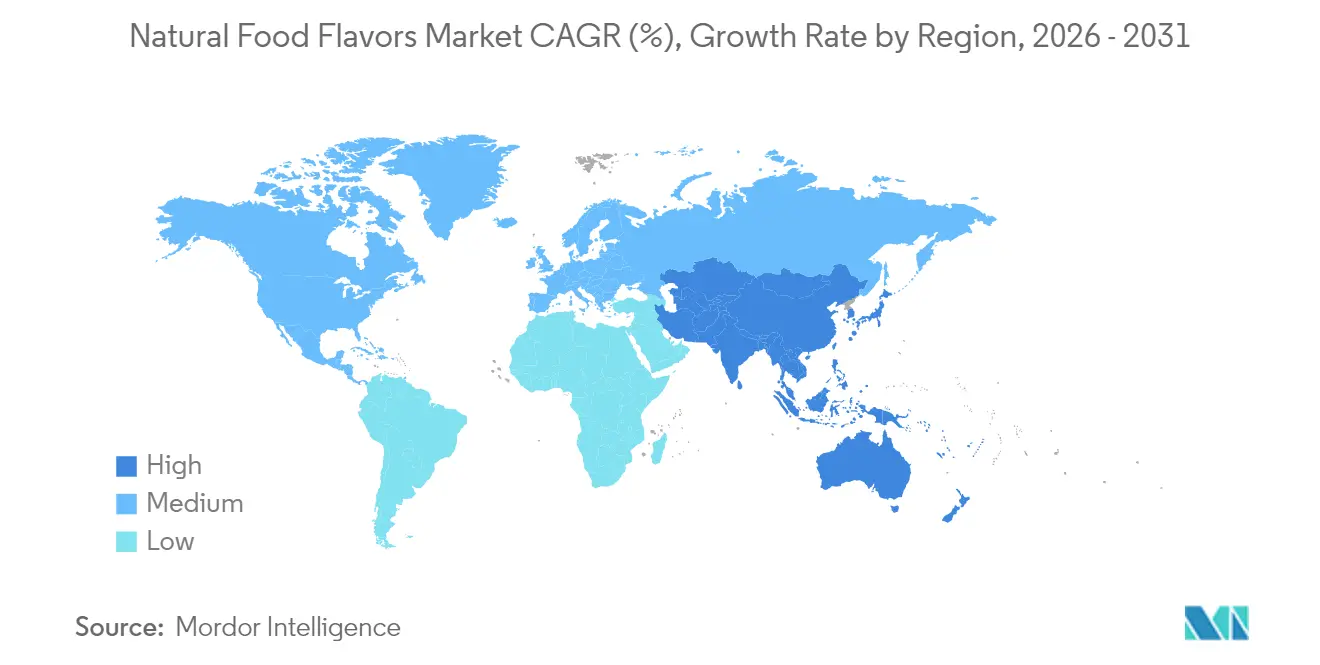

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Natural Food Flavors Market Analysis by Mordor Intelligence

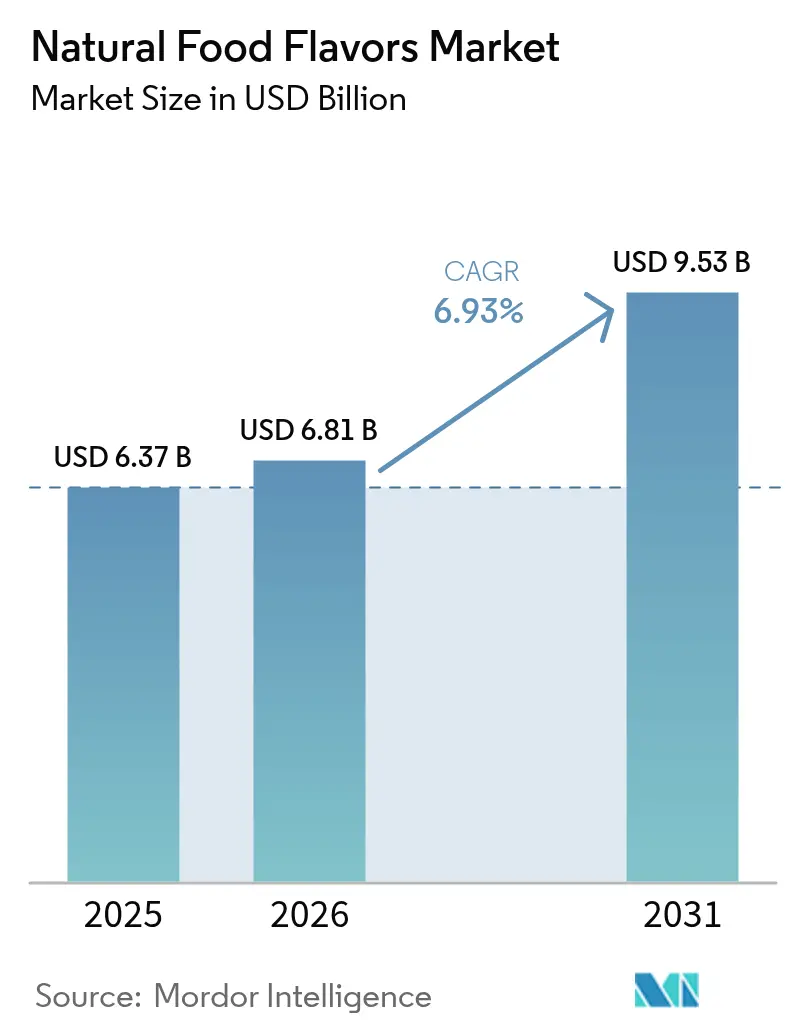

The natural food flavors market size is expected to grow from USD 6.37 billion in 2025 to USD 6.81 billion in 2026 and is forecast to reach USD 9.53 billion by 2031 at 6.93% CAGR over 2026-2031. This growth is driven by increasing consumer preference for clean-label products and the food industry's transition from synthetic alternatives due to stricter global regulations. The market expansion is further supported by consumer demand for natural ingredients, regulatory requirements, and supply chain considerations. Companies are adopting fermentation, bioconversion, and advanced extraction technologies to maintain product quality, minimize agricultural risks, and ensure compliance with natural ingredient regulations across regions. The combination of health-conscious consumers, regulatory requirements, and supply chain considerations has made technological advancement a key factor in market competition. To meet natural classification standards while reducing agricultural dependency, companies are investing in fermentation-based production and bioconversion processes across various regulatory environments.

Key Report Takeaways

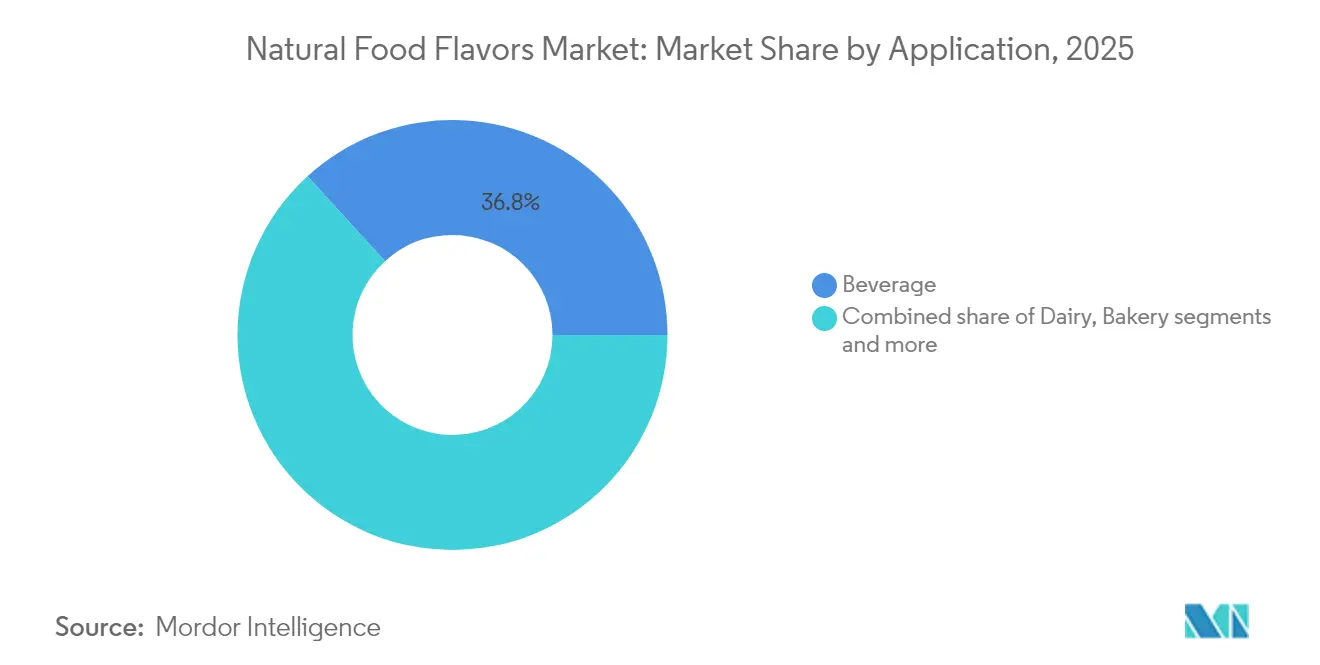

- By application, beverages led with a 36.78% market share of natural food flavors in 2025 and are projected to grow at a 7.31% CAGR through 2031.

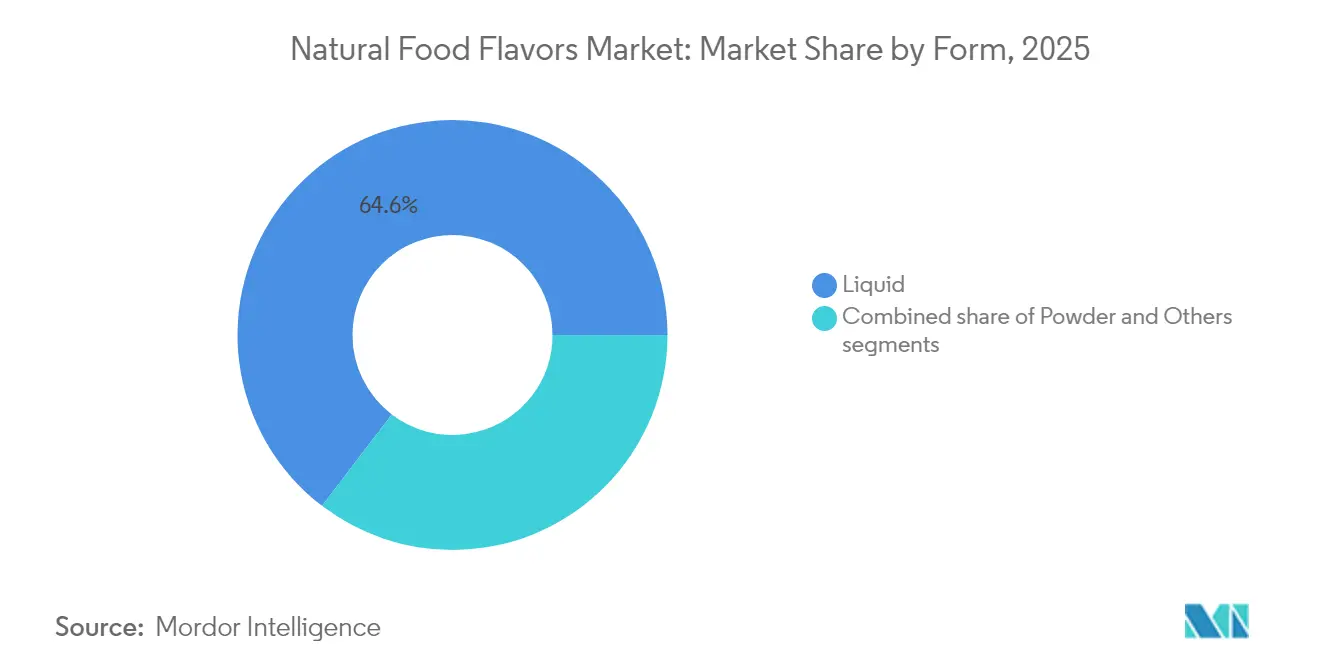

- By form, liquids captured 64.62% of the natural food flavors market size in 2025, while powders are projected to grow at the fastest rate, with a 7.44% CAGR during 2026-2031.

- By geography, Asia-Pacific accounted for 32.11% of the natural food flavors market share in 2025 and is forecast to expand at a 7.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Natural Food Flavors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancement in stabilization techniques enhancing shelf life of natural flavors | +1.2% | Global, with early adoption in North America and European Union | Medium term (2-4 years) |

| Increasing availability of diverse natural sources through global sourcing and cultivation | +0.8% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Consumer inclination towards clean label products to boost the market | +1.5% | Global, strongest in North America and European Union | Short term (≤ 2 years) |

| Rising demand for plant-based flavor to boost the market growth | +1.1% | Global, with premium growth in Asia-Pacific | Medium term (2-4 years) |

| Innovation in flavor extraction technologies | +0.9% | Global, concentrated in research and development hubs | Long term (≥ 4 years) |

| Increasing demand from the beverage and bakery industries | +1.3% | Global, accelerated in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer inclination towards clean label products to boost the market

Clean label regulations are reshaping product formulations across food categories, as manufacturers focus on ingredient transparency and natural components. The European Union's amendments to flavor regulations have removed synthetic smoke flavoring options, requiring companies to use natural alternatives that cost 3-5 times more than synthetic versions [1]Source: European Commission, “Flavoring Regulation Updates,” food.ec.europa.eu. This regulatory change creates a mandatory compliance requirement, making the transition to natural flavors essential in European markets. The impact extends beyond Europe, as global brands align their formulations to avoid operating separate production systems and maintain consistency across regions. Consumer acceptance of premium pricing for natural products has evolved significantly, making clean label compliance a fundamental requirement for market entry rather than a competitive advantage. This shift has prompted manufacturers to invest heavily in research and development to identify cost-effective natural alternatives while maintaining product quality and taste profiles.

Rising demand for plant-based flavor to boost the market growth

Plant-based flavor development has achieved technological advancements that overcome previous performance constraints and expand applications across food and beverage categories. Fermentation processes using Bacillus subtilis produce natural fruit flavors with increased antioxidant properties, enabling manufacturers to create more authentic taste profiles. This biotechnology method reduces supply chain risks associated with agricultural sourcing while maintaining natural classification under regulations, ensuring consistent flavor production throughout the year. The growth of plant-based foods and flavor innovation has created markets where conventional flavor profiles are redeveloped through botanical extraction methods, offering improved stability and enhanced sensory characteristics. Companies are investing in advanced extraction methods and biotechnology platforms to achieve authentic taste profiles while maintaining natural ingredient declarations. The market has split between mass-market plant-based products and premium botanical extracts, with premium extracts commanding higher prices despite limited supply. This price differentiation reflects both the sophisticated processing technologies required and the growing consumer preference for natural, sustainably sourced ingredients.

Innovation in flavor extraction technologies

Biotechnological extraction methods improve natural flavor production by providing consistent quality profiles and reducing dependency on agricultural sources. These methods address natural flavor standardization challenges through controlled production environments that minimize seasonal variations and quality inconsistencies. Advanced fermentation techniques and precision enzyme applications enable manufacturers to maintain uniform flavor profiles throughout the year. The patent landscape shows increased investment in enzyme-based conversion systems and fermentation optimization, indicating a shift toward biotechnology-driven production. Research and development efforts focus on enhancing extraction efficiency and developing novel bioconversion pathways. Companies using these technologies benefit from enhanced supply chain stability and production scalability independent of agricultural limitations. The implementation of biotechnology-based methods also supports sustainable practices by optimizing resource utilization and reducing waste generation in flavor production processes.

Increasing demand from beverage and bakery industries

Beverage manufacturers are driving natural flavor adoption through reformulation initiatives aimed at reducing synthetic ingredient dependencies while maintaining sensory appeal. The industry's focus on functional beverages and health-conscious positioning creates demand for natural flavors that complement nutritional claims without compromising taste profiles. According to the Australian Bureau of Statistics data from 2024, per capita consumption of soft drinks in Australia was 164.8 milliliters [2]Source: Australian Bureau of Statistics, "Per Capita Consumption of Soft Drinks in Australia", abs.gov.au. Moreover, bakery applications present unique technical challenges where natural flavors must withstand high-temperature processing while delivering consistent sensory experiences across batch production. The convergence of clean label requirements and functional food trends is expanding the addressable market for natural flavors beyond traditional applications into nutraceutical and dietary supplement categories. Regional preferences for specific flavor profiles are creating opportunities for localized natural flavor development, particularly in Asia-Pacific markets where traditional botanical ingredients align with consumer expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Changing regulatory landscape | -0.7% | Global, with varying regional interpretations | Short term (≤ 2 years) |

| Inconsistent flavor performance impacts the market growth | -0.5% | Global, acute in temperature-sensitive applications | Medium term (2-4 years) |

| Higher cost associated with natural food flavor | -1.1% | Global, most pronounced in price-sensitive segments | Short term (≤ 2 years) |

| Challenges in standardizing taste and aroma profile | -0.6% | Global, critical in industrial food production | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher cost associated with natural food flavor

Natural flavors command price premiums of 3-7 times compared to their synthetic counterparts, creating significant margin pressure across food categories. This cost differential particularly affects price-sensitive market segments, where consumers have limited willingness to pay higher prices. Food manufacturers face the challenge of balancing product quality with cost considerations, especially in categories like beverages, snacks, and dairy products. In response, manufacturers either optimize their formulations through ingredient substitution and process improvements or accept lower margins to maintain market share. Companies are pursuing vertical integration strategies, such as acquiring natural ingredient suppliers and developing in-house production capabilities. Additionally, they are investing in biotechnology-based production methods, including fermentation and enzyme technologies, to reduce costs while maintaining the natural classification of their flavors. These initiatives aim to achieve cost parity with synthetic alternatives without compromising the clean label appeal that consumers demand.

Challenges in standardizing taste and aroma profile

Natural flavor standardization faces significant challenges due to inherent variations in botanical sources, which directly impact quality control processes in industrial food production. Agricultural factors such as soil composition, nutrient availability, seasonal climate patterns, and precise harvest timing create notable inconsistencies between production batches, which synthetic production methods avoid through tightly controlled chemical processes. Natural flavors must maintain consistent stability across diverse food matrices and various processing conditions while delivering uniform sensory profiles to meet consumer expectations. Modern extraction and purification technologies, including advanced chromatography and molecular distillation techniques, help achieve better standardization in natural flavor production. However, these sophisticated technological solutions substantially increase production costs and operational complexity compared to synthetic alternatives, presenting manufacturers with important cost-benefit considerations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Beverage Segment Leads Clean Label Transformation

The beverage application commanded 36.78% market share in 2025, with the segment projected to maintain its leadership position through 7.31% CAGR growth during 2026-2031. Major beverage manufacturers are reformulating products to eliminate synthetic flavoring agents, driven by consumer health consciousness and regulatory pressures across key markets. Dairy applications represent the second-largest segment, benefiting from the clean label trend in yogurt, milk-based beverages, and cheese products, where natural flavors enhance sensory appeal without compromising nutritional positioning.

Bakery applications are experiencing robust growth as manufacturers seek natural alternatives that withstand high-temperature processing while delivering consistent flavor profiles across batch production. Confectionery segments face unique challenges where natural flavors must provide intense sensory experiences traditionally achieved through synthetic compounds, driving innovation in concentration techniques and flavor delivery systems. Savory snack applications are emerging as a high-growth opportunity where natural flavors align with premium positioning and health-conscious consumer preferences. Meat applications, while smaller in volume, represent a specialized segment where natural flavors enhance processed meat products and plant-based alternatives, with Beyond Meat's patent portfolio demonstrating the technical complexity of achieving meat-like sensory profiles through natural ingredients.

By Form: Liquid Dominance Faces Powder Innovation Challenge

Liquid formulations maintained 64.62% market share in 2025, reflecting their versatility across beverage applications and ease of integration in industrial food production processes. However, powder formulations are experiencing accelerated growth at 7.44% CAGR through 2031, driven by advantages in storage stability, shipping efficiency, and application flexibility in dry food products. The shift toward powder formulations reflects technological advances in spray-drying and encapsulation technologies that preserve flavor integrity while extending shelf life and reducing transportation costs.

Encapsulation innovations are enabling powder formulations to compete with liquid alternatives in previously challenging applications, with Givaudan's expansion of encapsulation capacity in Mexico doubling its global production capabilities to meet growing demand. Other form categories, including paste and emulsion formulations, serve specialized applications where specific texture and release characteristics are required. The form selection increasingly depends on end-application requirements, with liquid formulations preferred for beverages and powder forms gaining traction in bakery, confectionery, and processed food applications where moisture control and extended shelf life are critical factors.

Geography Analysis

Asia-Pacific holds 32.11% market share in 2025 and is expected to grow at 7.62% CAGR through 2031, functioning as both a primary consumer and supplier of natural flavors. China's implementation of GB 2760-2024 Standard has improved the regulatory environment, providing clearer guidelines for product approval and market access. The growth is further supported by India's expanding food processing industry and Japan's premium consumer market, with both countries aligning their regulations with international natural ingredient standards. While the region's botanical diversity provides sourcing advantages, companies must manage complex supply chains across multiple jurisdictions. Givaudan's USD 37.5 million investment in an Indonesian facility in October 2024 highlights the importance of regional manufacturing presence to meet local demand.

North America and Europe maintain steady market growth through established regulatory frameworks and high consumer acceptance. The US FDA's natural flavor definition under 21 CFR 101.22 provides a stable foundation for industry investment, while European markets operate under stricter requirements that benefit companies with sophisticated extraction methods. IFF's 30,000 square foot Citrus Innovation Center in Florida, opening in April 2025, demonstrates the industry's commitment to botanical research and sustainable production. Moreover, the International Food Information Council's 2024 survey indicated that 11% of United States respondents adhere to clean-label eating practices . This consumer segment drives market demand for ingredient transparency and simplicity, contributing to increased sales of natural food flavors manufactured from botanical extracts and essential oils rather than synthetic ingredients.

South America, and Middle East and Africa show increasing market potential driven by economic growth and urbanization. These regions currently face challenges, including limited extraction infrastructure, dependence on flavor imports, and price sensitivity affecting premium product adoption. As consumer preferences shift toward natural ingredients and regulatory frameworks evolve, these markets offer significant growth opportunities. Market participants must develop cost-effective solutions while establishing local supply chain networks to meet growing demand efficiently.

Competitive Landscape

The natural food flavors market exhibits moderate fragmentation, indicating significant competitive intensity among established players while creating opportunities for specialized technology providers and regional suppliers. Market leaders, including Givaudan, DSM-Firmenich, and IFF, are pursuing differentiated strategies that combine scale advantages with technological innovation. The competitive landscape is characterized by vertical integration initiatives, biotechnological production investments, and strategic acquisitions that consolidate extraction capabilities and expand geographic reach.

Additionally, companies are investing in research and development to produce natural flavors that match the performance of artificial additives while complying with clean-label and sustainability standards. The production methods incorporate extraction techniques, enzymatic processes, and fermentation-based systems that maintain flavor quality and minimize environmental impact. Companies implementing regulatory compliance measures and supply chain traceability increase consumer confidence and competitive advantage. This strategy allows them to address the increasing demand for organic snacks, natural beverages, and healthier packaged foods.

Technology adoption is becoming the primary competitive differentiator as companies invest in fermentation-based production methods, advanced extraction techniques, and analytical verification systems to achieve consistent quality while reducing agricultural dependencies. Patent portfolios in vanillin biosynthesis, enzyme-based conversion systems, and encapsulation technologies create competitive moats that enable premium pricing and market share protection. White-space opportunities exist in biotechnological production methods, specialized application development, and regional market penetration, where local botanical knowledge and supply chain relationships provide competitive advantages over global players.

Natural Food Flavors Industry Leaders

-

Givaudan SA

-

Symrise AG

-

DSM-Firmenich

-

Takasago International Corp.

-

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: T. Hasegawa USA implemented an expansion of its flavor development capabilities in California. The upgraded facility incorporated dedicated laboratories for sweet and savory flavor compounding, as well as a specialized area for beverage flavor development.

- October 2024: Synergy Flavors introduced a new line of 'heat and fire' flavors in response to increased consumer demand for intense flavors. The product range comprised natural flavors and pastes that food manufacturers could utilize to enhance their products. These flavors were compatible with various food items, including ready meals, plant-based meats, and baked goods. The range enabled manufacturers to customize heat levels and flavor profiles according to consumer preferences.

- June 2024: Tate & Lyle announced its decision to acquire CP Kelco for USD 1.8 billion to establish a comprehensive specialty food and beverage solutions business. The acquisition was designed to expand the company's capabilities in sweetening, mouthfeel, and fortification solutions.

- March 2024: BASF Aroma Ingredients' brand Isobionics introduced a new natural flavor product, Isobionics Natural beta-Caryophyllene 80. This addition to the Isobionics portfolio demonstrated the company's focus on developing natural flavors based on customer requirements.

Global Natural Food Flavors Market Report Scope

Food flavors and enhancers improve food taste and aroma completely and increase its attractiveness and palatability.

The global food flavors and fragrances market is segmented by product type, type, application, form, and geography. By product type, the market is segmented into food flavors and food enhancers. By type, the market is segmented into natural, synthetic, and nature-identical. By application, the market is segmented into dairy, bakery, confectionery, savory snacks, meat, beverages, and other applications. the market is segmented by form into powder, liquid, and others. By geography, the market is segmented into North America, Europe, South America, Asia-Pacific, and Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

| Powder |

| Liquid |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Poland | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Turkey | |

| Morocco | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Application | Dairy | |

| Bakery | ||

| Confectionery | ||

| Savory Snack | ||

| Meat | ||

| Beverage | ||

| Other Applications | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Poland | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Turkey | ||

| Morocco | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the natural food flavors market?

The natural food flavors market size reached USD 6.81 billion in 2026 and is projected to hit USD 9.53 billion by 2031 at a 6.93% CAGR.

Which application holds the largest share of natural food flavors?

Beverages led with 36.78% of 2025 revenue and are on track for a 7.31% CAGR during 2026-2031.

Which region is growing fastest for natural food flavors?

Asia-Pacific commands the highest share at 32.11% and is also the fastest-growing region, forecast at 7.62% CAGR to 2031.

How are companies mitigating supply volatility in natural flavors?

Leading firms invest in fermentation-based production, vertical integration of key crops, and encapsulation technologies that stabilize supply and reduce dependency on seasonal harvests.

Page last updated on: