Australia Vanilla Flavor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

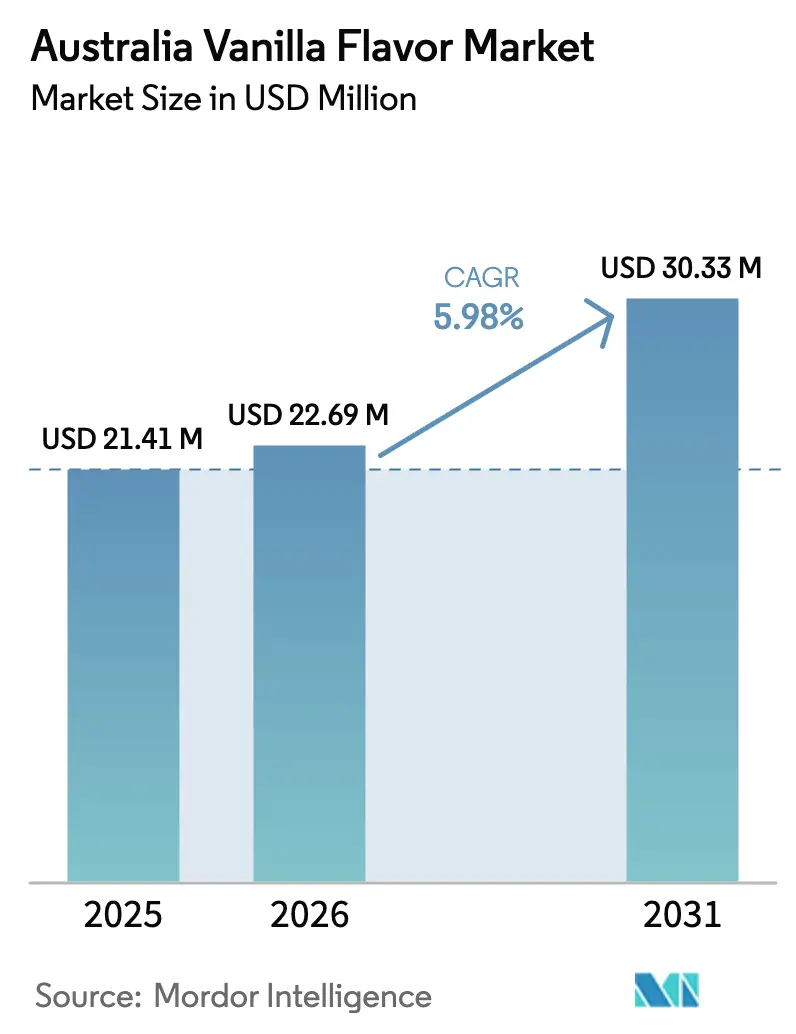

| Base Year Market Size (2025) | USD 21.41 Million |

| Market Size (2026) | USD 22.69 Million |

| Market Size (2031) | USD 30.33 Million |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Vanilla Flavor Market Analysis by Mordor Intelligence

The Australia vanilla flavor market size was valued at USD 21.41 million in 2025, reached USD 22.69 million in 2026, and is projected to grow to USD 30.33 million by 2031, registering a CAGR of 5.98% during the forecast period of 2026–2031. The market is witnessing steady growth, driven by trends in premiumization and clean-label reformulation. Vanilla remains a key flavor in sweet applications due to its ability to enhance sweetness perception, improve aroma complexity, and provide a familiar yet indulgent sensory experience. As manufacturers emphasize product differentiation and the use of high-quality ingredients, the demand for natural and premium vanilla formats continues to rise. Additionally, growth is supported by the increasing adoption of plant-based and dairy-free innovations, where vanilla plays a vital role in masking off-notes and improving taste balance.

Key Report Takeaways

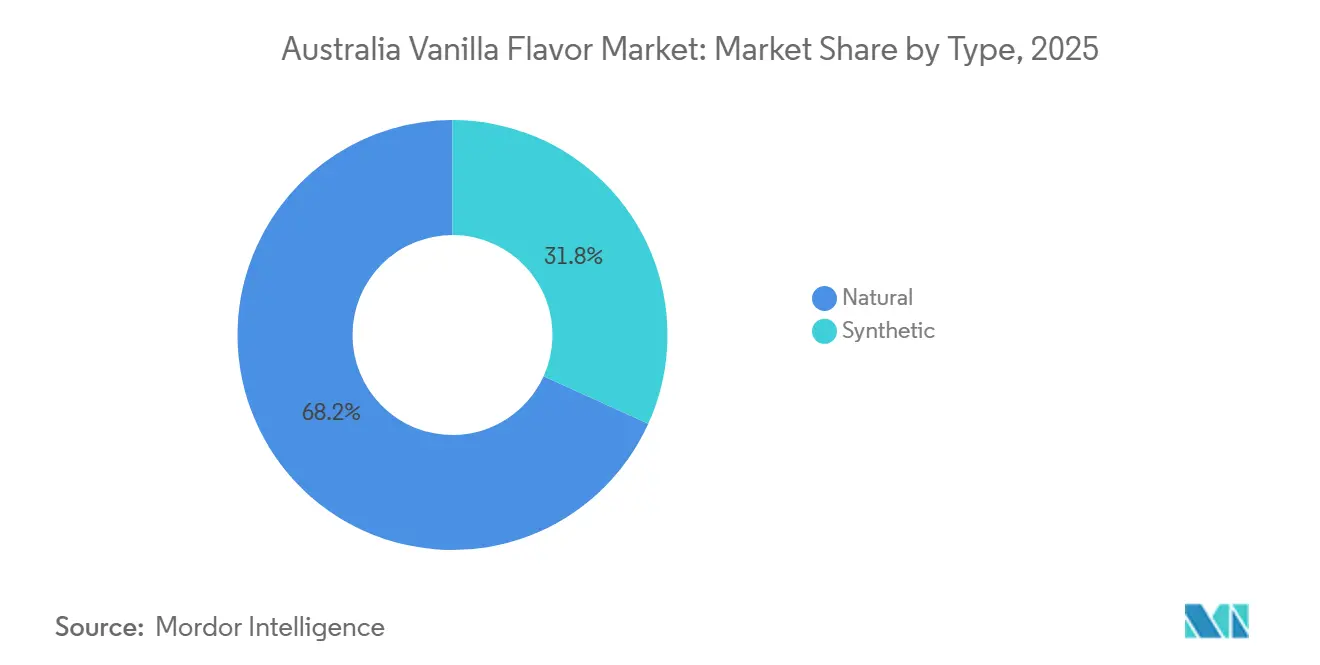

- By type, natural vanilla led with 68.22% of the Australia vanilla flavor market share in 2025; it is expected to advance at a 7.11% CAGR through 2031.

- By form, liquid held 55.62% share in 2025, while paste is projected to expand at a 6.84% CAGR between 2026 and 2031.

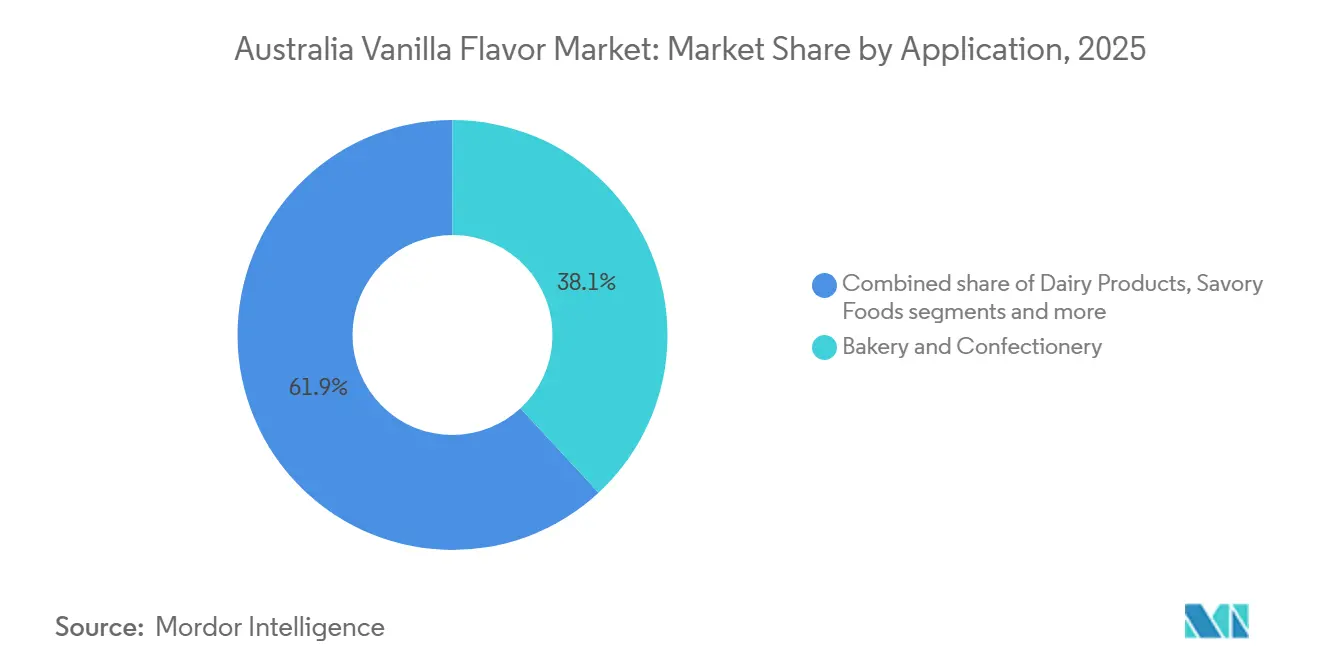

- By application, bakery and confectionery accounted for 38.11% of demand in 2025; dairy products are forecast to record a 7.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Vanilla Flavor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in premium and artisanal bakery and confectionery applications | +1.8% | National, concentrated in Sydney, Melbourne metro areas | Medium term (2-4 years) |

| Clean-label and natural ingredient preference | +1.5% | National, strongest in urban centers and online channels | Short term (≤ 2 years) |

| Foodservice and café culture expansion | +1.2% | National, with early gains in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Expansion of plant-based and dairy-free products | +1.0% | National, driven by metro cafés and supermarket dairy-alternative aisles | Short term (≤ 2 years) |

| Advancements in vanilla farming methods | +0.6% | Global supply impact, indirect benefit to Australian importers | Long term (≥ 4 years) |

| Shift toward gourmet and high-end food products | +0.9% | National, strongest in premium retail and export-oriented segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in premium and artisanal bakery and confectionery applications

The growth of the premium and artisanal bakery and confectionery segments is a key driver for the Australia Vanilla Flavor Market. Vanilla is a fundamental flavor in high-end cakes, pastries, macarons, biscuits, chocolates, and cream-based fillings, where the quality of ingredients significantly impacts sensory appeal and brand perception. With consumers increasingly favoring handcrafted, small-batch, and gourmet products, manufacturers are focusing on high-quality natural pastes, and whole beans to enhance flavor authenticity and depth. The visible presence of vanilla bean specks in frostings, custards, and ice creams further supports premium positioning and justifies higher price points. Artisanal bakeries and specialty dessert brands are prioritizing clean-label ingredients and authentic sourcing, driving a shift from synthetic vanillin to natural vanilla formats. Furthermore, celebration-driven consumption, including customized cakes, festive desserts, and indulgent confectionery, continues to boost demand for rich and well-rounded vanilla flavor profiles.

Clean-label and natural ingredient preference

The increasing consumer preference for clean-label and natural ingredients is driving market growth. Consumers are paying closer attention to ingredient lists, favoring recognizable and minimally processed components. According to the Puratos Group, 68% of consumers consider "naturalness" a key aspect of clean-label foods, highlighting the strong demand for authentic ingredient sourcing [1]Source: Puratos Group, "What Drives Consumers to Clean-Label Foods", puratos.com.a. This trend benefits natural vanilla, as it aligns with transparency, simplicity, and premium product positioning in bakery, dairy, and beverage applications. Food manufacturers are responding by reformulating products to eliminate artificial flavor declarations and replace them with natural vanilla labeling, thereby enhancing brand credibility and consumer trust. Natural vanilla not only supports clean-label claims but also offers superior sensory qualities, complementing premium and functional food innovations.

Foodservice and café culture expansion

The growth of Australia’s foodservice and café sector significantly drives the Vanilla Flavor Market. According to the Australian Bureau of Statistics, annual revenue from cafés, restaurants, and takeaway food services reached AUD 65.5 billion in 2024, underscoring the economic importance of this channel. Vanilla is a key ingredient across café menus and dessert offerings, commonly used in flavored lattes, milkshakes, smoothies, pastries, cakes, custards, and premium desserts. Its versatility and widespread consumer appeal make it one of the most frequently utilized flavoring ingredients in both beverage and dessert applications within foodservice settings. The robust performance of cafés and restaurant chains directly boosts Business-to-Business (B2B) demand for vanilla flavors, syrups, and pastes, as operators prioritize consistent, high-quality flavor profiles across their locations. Furthermore, the growing trend of premium beverage customization, such as vanilla-infused coffees and specialty drinks, has increased the per-outlet usage of vanilla ingredients.

Expansion of plant-based and dairy-free products

The rapid growth of plant-based and dairy-free product categories is a significant driver for the Australian vanilla flavor market. As manufacturers introduce non-dairy alternatives such as almond, oat, soy, and coconut, vanilla has become a widely used flavoring agent in these formulations. Its primary functional role includes masking off-notes commonly associated with plant proteins and legume-based ingredients, while also enhancing sweetness perception and improving overall mouthfeel. This functionality makes vanilla crucial for ensuring consumer acceptance and encouraging repeat purchases of plant-based products. Additionally, vanilla aligns with clean-label positioning, which is particularly important in the plant-based segment, where consumers prioritize natural and recognizable ingredients. Premium plant-based ice creams and fortified dairy alternatives often utilize natural vanilla paste to replicate the creamy and indulgent sensory experience traditionally associated with dairy products. Consequently, the continued expansion of plant-based and dairy-free categories is driving increased demand for both natural and specialty vanilla formats in Australia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global vanilla bean supply | -1.2% | Global, with direct impact on Australian import costs and availability | Short term (≤ 2 years) |

| High cost of natural vanilla flavor | -0.9% | National, affecting price-sensitive mass-market segments and private-label positioning | Medium term (2-4 years) |

| Competition from alternative natural flavors | -0.5% | National, concentrated in mass-market bakery and confectionery segments | Medium term (2-4 years) |

| Strict quality control and regulatory requirements | -0.4% | National, with spillover effects on export-oriented manufacturers targeting EU and U.S. markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in global vanilla bean supply

Volatility in the global vanilla bean supply poses a significant challenge for the Australia Vanilla Flavor Market. The country's heavy reliance on imported vanilla beans makes the domestic market highly susceptible to global production fluctuations. Vanilla cultivation is concentrated in a few tropical regions, where crops are at risk from cyclones, droughts, plant diseases, and political instability. Disruptions in these producing regions can lead to sharp supply reductions, causing sudden price increases and procurement challenges for Australian manufacturers. Additionally, vanilla is a labor-intensive crop that requires hand pollination and an extended curing process, limiting the ability to quickly expand supply during shortages. These structural constraints often result in pronounced price volatility, impacting cost planning and margin stability for food and beverage producers.

High cost of natural vanilla flavor

The high cost of natural vanilla flavor serves as a significant restraint, particularly for mass-market food manufacturers operating in price-sensitive categories. The pricing of natural vanilla is largely determined by global bean supply conditions. Premium varieties, such as Grade A Madagascar Bourbon beans, were traded at approximately USD 200–450 per pound in 2026, creating substantial cost pressures across the value chain. These elevated raw material prices directly increase production costs for manufacturers and producers relying on natural vanilla for clean-label positioning. This price volatility restricts the wider adoption of natural vanilla in entry-level and private-label products, where cost competitiveness is essential. To address margin constraints, many manufacturers may partially replace natural vanilla with synthetic vanillin or blended flavor systems to stabilize costs while maintaining acceptable flavor profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Vanilla Captures Premium Positioning

Natural vanilla is projected to hold a 68.22% market share in 2025 and is expected to grow at a CAGR of 7.11% through 2031, underscoring its dominance in the Australia Vanilla Flavor Market. This growth is primarily driven by structural shifts toward premiumization and clean-label consumption. The increasing demand for authentic ingredients in bakery, confectionery, dairy, and beverage applications, where flavor depth and aroma complexity are key differentiators, fuels the strong performance of natural vanilla. Food manufacturers are reformulating products to replace synthetic vanillin with natural flavors to align with transparent labeling practices and address growing consumer scrutiny of ingredient lists. Natural vanilla is widely regarded as superior in taste quality, offering a richer and more rounded flavor profile that enhances premium cakes, biscuits, ice creams, yogurts, and ready-to-drink beverages.

Synthetic vanilla continues to play a strategically important role in the Australia Vanilla Flavor Market due to its cost efficiency, consistency, and formulation stability. It remains widely used in large-scale industrial applications, particularly in mass-market bakery, confectionery, flavored milk, instant desserts, and packaged snacks, where price competitiveness and margin optimization are critical. Its standardized flavor profile ensures uniform taste across batches, making it highly suitable for high-volume food production. Additionally, synthetic vanilla offers a stable supply chain, mitigating risks associated with global crop volatility and price fluctuations. Its predictable pricing and availability enable manufacturers to maintain production continuity without procurement challenges.

By Form: Paste Gains Ground in Artisan Bakery

Liquid vanilla flavor is projected to command a 55.62% market share in 2025, solidifying its position as the dominant format in the Australia Vanilla Flavor Market. This leadership is attributed to its versatility, ease of use, and broad applicability across various food and beverage categories. Liquid vanilla integrates seamlessly into batters, dairy bases, beverages, and confectionery fillings, making it the preferred choice for bakery manufacturers, ice cream producers, flavored milk processors, and café beverage formulators. The format ensures uniform dispersion, providing consistent flavor distribution and aroma release, which is essential for maintaining product standardization in both artisanal and industrial production settings. Additionally, liquid vanilla offers flexible dosage control, allowing manufacturers and home bakers to precisely adjust intensity based on formulation needs.

Vanilla paste is emerging as the fastest-growing format, with a projected CAGR of 6.84% through 2031, reflecting the market's shift toward premiumization and visual authenticity. Unlike liquid vanilla, vanilla paste combines concentrated with finely ground vanilla bean specks, delivering both intense flavor and visible texture. Manufacturers and foodservice operators increasingly favor vanilla paste for high-end applications due to its stronger flavor impact with lower usage volume, while maintaining a clean-label positioning. Furthermore, vanilla paste offers enhanced convenience compared to whole vanilla beans, eliminating the need for splitting and scraping pods while still providing a natural, premium profile.

By Application: Dairy Products Accelerate on Plant-Based Wave

Bakery and confectionery are projected to account for 38.11% of the market share in 2025, solidifying their position as the leading application segment in the Australia Vanilla Flavor Market. This dominance is attributed to vanilla's essential role as a key flavor in products such as cakes, biscuits, pastries, muffins, chocolates, fillings, and cream-based confectionery. In industrial production, vanilla ensures consistent aroma and taste across large-scale batches, making it vital for standardized formulations. Furthermore, the rising demand for indulgent treats, celebration cakes, and premium dessert offerings continues to drive vanilla consumption in this segment. Reformulation trends favoring clean-label and natural ingredients have further bolstered vanilla's application, as manufacturers increasingly replace synthetic flavorings with natural flavors to enhance product appeal.

Dairy products are expected to grow at a CAGR of 7.03% through 2031, making them the fastest-growing application segment in the Australia Vanilla Flavor Market. This growth is supported by the country's high dairy consumption levels and ongoing product innovation within milk-based categories. According to the Australian Bureau of Statistics (ABS), milk product consumption reached 269.6 grams per capita per day in 2023–24, demonstrating a stable consumption base that underpins demand for flavor ingredients [2]Source: Australian Bureau of Statistics (ABS), "Apparent Consumption of Selected Foodstuffs, Australia", abs.gov.au. Vanilla plays a crucial functional and sensory role in dairy applications, enhancing sweetness perception, improving aroma, and balancing the natural taste of milk fats and proteins. These attributes make vanilla one of the most widely used flavors in the dairy segment.

Geography Analysis

Australia’s vanilla flavor market exhibits a strong geographic concentration in its most urbanized and foodservice-driven states, particularly New South Wales and Victoria. These regions account for the majority of national demand, with metropolitan foodservice networks, including cafés, patisseries, dessert boutiques, and chained restaurant groups, serving as primary consumption hubs. The high density of specialty bakeries, premium ice cream producers, and beverage chains in these states significantly drives ingredient procurement volumes. Additionally, large-scale food manufacturers and contract producers are concentrated in these regions, strengthening localized supply chains and accelerating vanilla usage across bakery, dairy, and beverage applications.

Import dependence plays a critical role in shaping Australia’s regional market dynamics. The country sources the majority of its vanilla beans from international suppliers, making port cities and major logistics hubs strategically important for efficient distribution. According to the Observatory of Economic Complexity (OEC), in 2024, Australia imported USD 4.49 million worth of vanilla, ranking as the 22nd largest importer globally [3]Source: Observatory of Economic Complexity (OEC), "Vanilla in Australia", oec.world. This reliance on imports ties domestic pricing and availability directly to global supply conditions, particularly harvest cycles and export volumes from key producing nations. Consequently, states with stronger import infrastructure and established ingredient distribution networks experience smoother supply flows and faster product turnaround for manufacturers.

While New South Wales and Victoria dominate consumption, other regions such as Queensland and Western Australia contribute steadily to market growth through the expansion of bakery chains, dairy processing units, and retail penetration. However, these markets remain comparatively smaller and more reliant on distribution from eastern import centers. Regional growth is further supported by increasing premium dessert consumption and the expansion of supermarket private-label flavored dairy and bakery products. Overall, Australia’s vanilla flavor market is characterized by an eastern-state concentration, import-driven supply chains, and strong alignment between metropolitan foodservice ecosystems and ingredient demand.

Competitive Landscape

The Australian vanilla flavor market is moderately fragmented, featuring a mix of leading global flavor houses, regional ingredient suppliers, and niche premium brands. Prominent multinational companies such as Solvay SA, Givaudan S.A., Symrise AG, International Flavors & Fragrances Inc., and Kerry Group plc hold strong competitive positions. These firms leverage extensive flavor portfolios, robust Research and Development (R&D) capabilities, and established B2B relationships with large-scale food and beverage manufacturers. Competition among these players is driven by formulation expertise, supply reliability, sustainability initiatives, and customized flavor solutions for applications in bakery, dairy, beverages, and nutraceuticals. Their global sourcing networks enable them to manage raw material volatility effectively while offering both natural and synthetic vanilla variants to cater to different pricing segments.

Competition in the market is increasingly influenced by advancements in sourcing and sustainability strategies. Greenhouse-cultivated Australian vanilla is gaining traction due to its alignment with the country’s clean-and-green image, providing traceability and reducing supply chain risks compared to imported vanilla beans. Additionally, bio-based vanillin derived from renewable feedstocks is emerging as a cost-efficient alternative that meets natural labeling requirements. This segment is particularly appealing to export-oriented manufacturers seeking stable pricing and compliance with international clean-label standards. Companies are also differentiating themselves through organic certifications, ethical sourcing programs, and advanced technologies aimed at enhancing flavor intensity and stability.

Emerging disruptors, particularly precision-fermentation startups, are intensifying competition in the market. These companies produce vanillin using engineered yeast and microalgae platforms, positioning their products as sustainable, scalable, and less susceptible to agricultural volatility. While still in the early stages of commercialization, these biotechnology-driven innovations present alternative production pathways that could challenge traditional and synthesis methods. As sustainability, traceability, and premiumization continue to influence purchasing decisions, the competitive landscape is shifting from price-driven competition to technology-driven differentiation and value-added ingredient solutions.

Australia Vanilla Flavor Industry Leaders

-

Solvay SA

-

Givaudan S.A.

-

Symrise AG

-

International Flavors & Fragrances Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Flavorchem, a global supplier of flavors and ingredients, launched "The Art of Vanilla," a collection that combines premium quality with versatility. This collection highlights the breadth of their premium vanilla portfolio, featuring a carefully curated range of products derived from one of nature's most cherished beans.

- January 2024: Givaudan introduced Scentaurus Vanilla, a new precursor activated by oxygen. This product offers a fresh sensation along with a long-lasting powdery and creamy vanilla effect.

Australia Vanilla Flavor Market Report Scope

Vanilla flavors are produced either through chemical processes or from vanilla seed pods. The predominant vanilla flavor, vanillin, is extracted from diverse sources, including wood, petrochemical products, and vanilla beans. The Australian vanilla flavor market is segmented by type into natural and synthetic. By form, the market is divided into liquid, powder, and paste. Furthermore, its applications include bakery and confectionery, dairy products, savory foods, soups, pastas, noodles, beverages, and other applications. The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Tons).

| Synthetic |

| Natural |

| Liquid |

| Powder |

| Paste |

| Bakery and Confectionery |

| Dairy Products |

| Savory Foods |

| Soups, Pastas, and Noodles |

| Beverages |

| Other Applications |

| By Type | Synthetic |

| Natural | |

| By Form | Liquid |

| Powder | |

| Paste | |

| By Application | Bakery and Confectionery |

| Dairy Products | |

| Savory Foods | |

| Soups, Pastas, and Noodles | |

| Beverages | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the Australia vanilla flavor market?

The Australia vanilla flavor market size stands at USD 22.69 million in 2026 and is projected to reach USD 30.33 million by 2031.

Which segment is expanding fastest within vanilla flavor applications?

Dairy and plant-based dairy products are forecast to grow at a 7.03% CAGR through 2031 on the back of high-protein yogurt and alt-milk reformulation.

Why are paste formats gaining popularity among Australian bakers?

Paste carries visible vanilla seeds that convey authenticity, and its 6.84% CAGR growth reflects its appeal to artisan bakeries and premium dessert makers.

How are supply risks from Madagascar being managed?

Leading suppliers such as Symrise and Givaudan have integrated farmer partnerships and blockchain tracing to stabilize quality and delivery timelines.

Page last updated on: