Cricket Apparel And Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

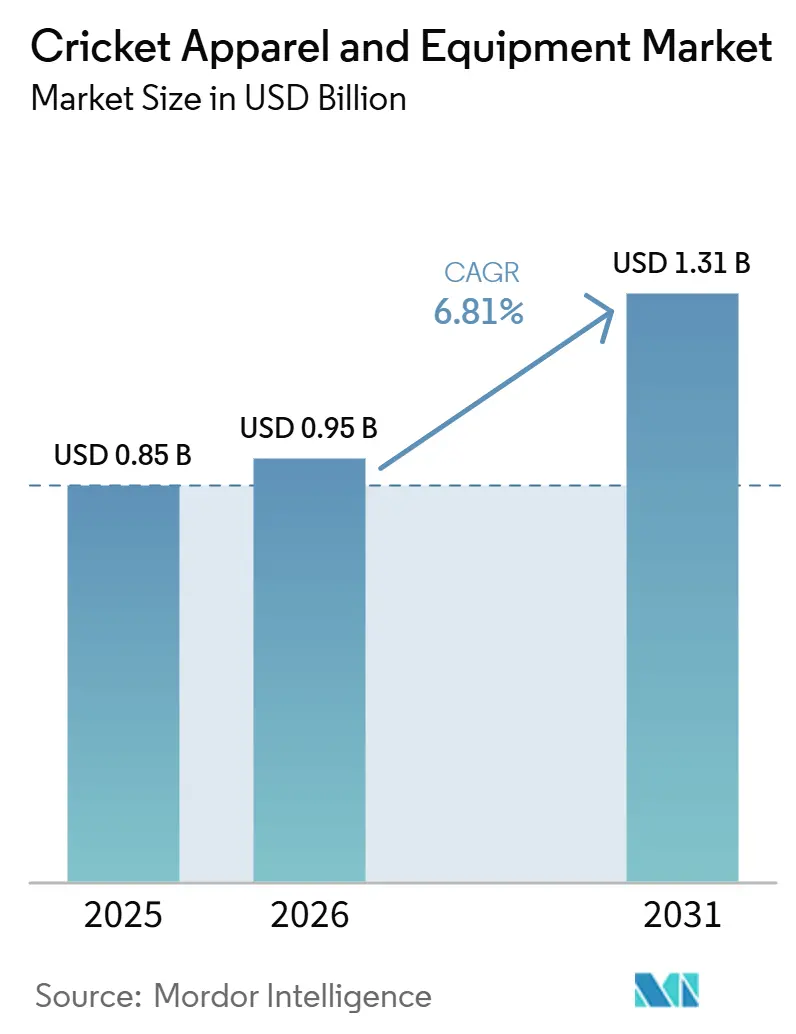

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

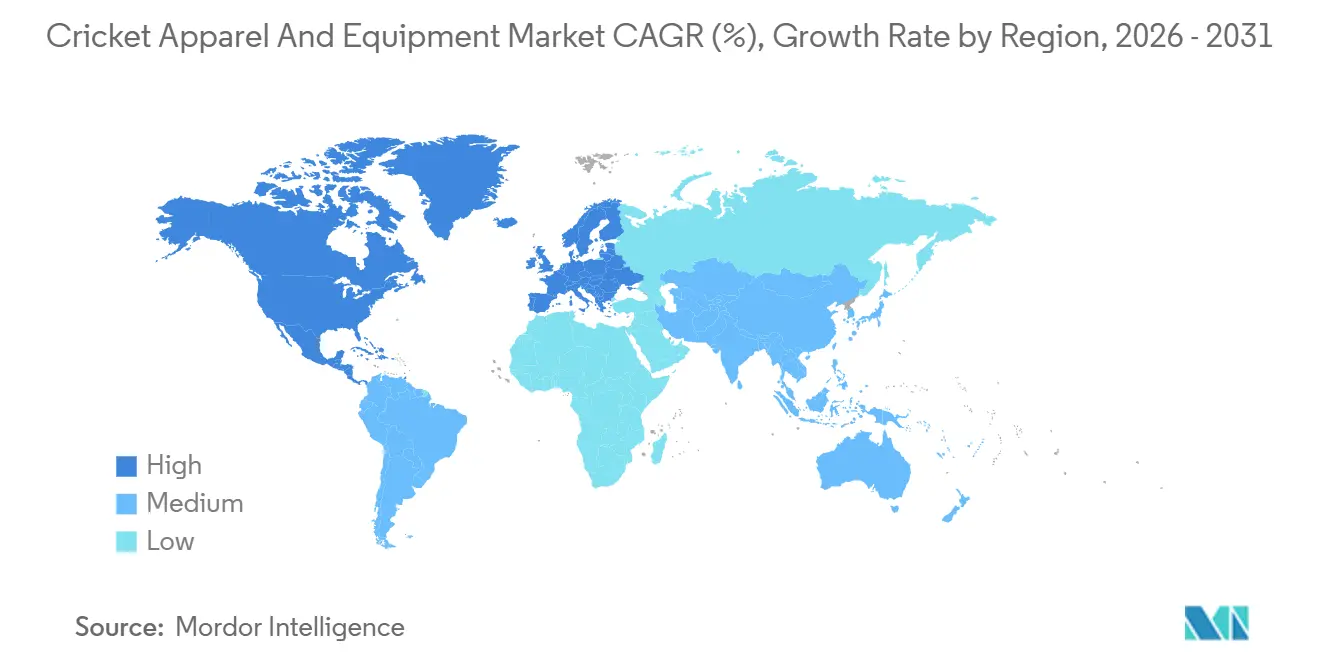

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cricket Apparel And Equipment Market Analysis by Mordor Intelligence

The global cricket apparel and equipment market size is expected to grow from USD 0.85 billion in 2025 to USD 0.95 billion in 2026 and is forecast to reach USD 1.31 billion by 2031 at a 6.81% CAGR over 2026-2031. The global cricket apparel and equipment market is driven by the growing popularity of cricket in both traditional regions and emerging markets. This growth is supported by the rise of franchise-based T20 leagues, such as the Indian Premier League and Big Bash League, which have significantly increased fan engagement and participation. The increasing involvement of youth, women, and amateur players, along with the integration of cricket into school and grassroots programs, is further boosting demand for apparel and equipment. Technological advancements in product design, including lightweight bats, high-performance fabrics, and improved protective gear, are prompting players to upgrade their equipment more frequently. Moreover, rising investments in sports infrastructure, enhanced visibility through media broadcasting and digital platforms, and the influence of professional player endorsements are shaping consumer preferences and driving market growth. The expansion of e-commerce and organized sports retail channels has improved global product accessibility, while growing awareness of safety standards is encouraging the adoption of high-quality protective gear, collectively supporting sustained market growth.

Key Report Takeaways

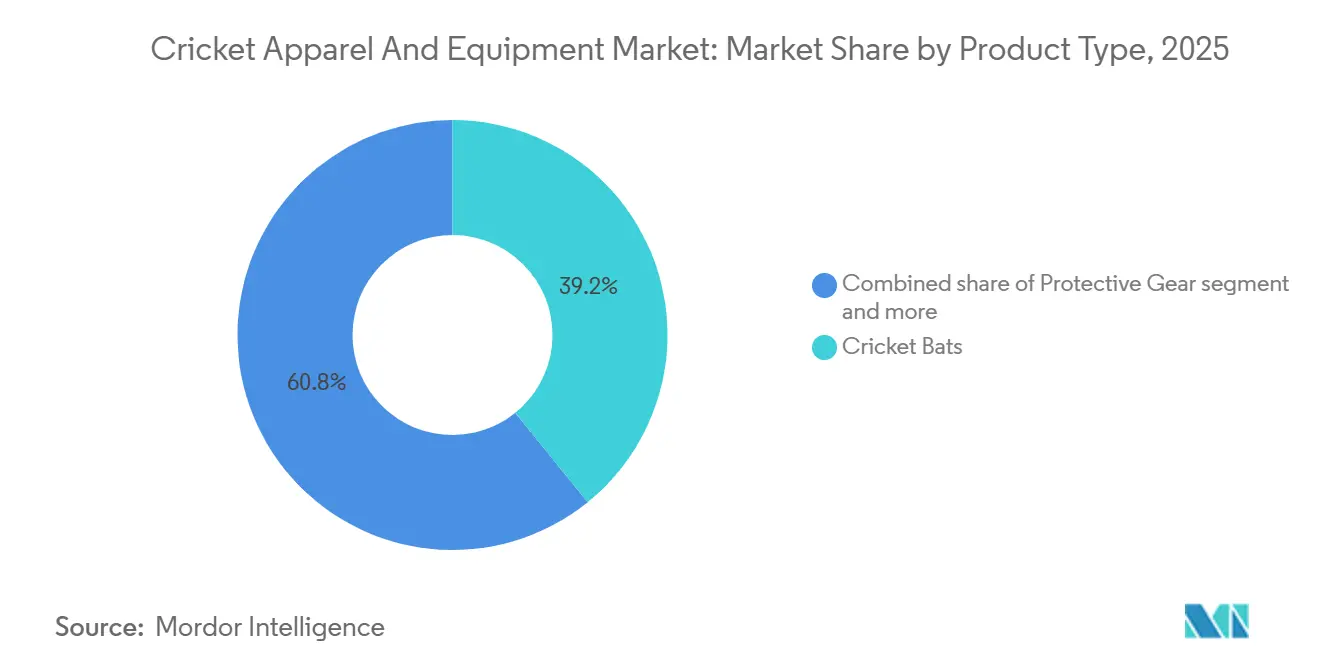

- By product type, cricket bats held 39.18% of the cricket apparel and equipment market share in 2025, while protective gear is projected to expand at a 7.32% CAGR through 2031.

- By end user, adults contributed 79.17% of demand in 2025; the kids segment is set to rise at a 7.47% CAGR during 2026-2031.

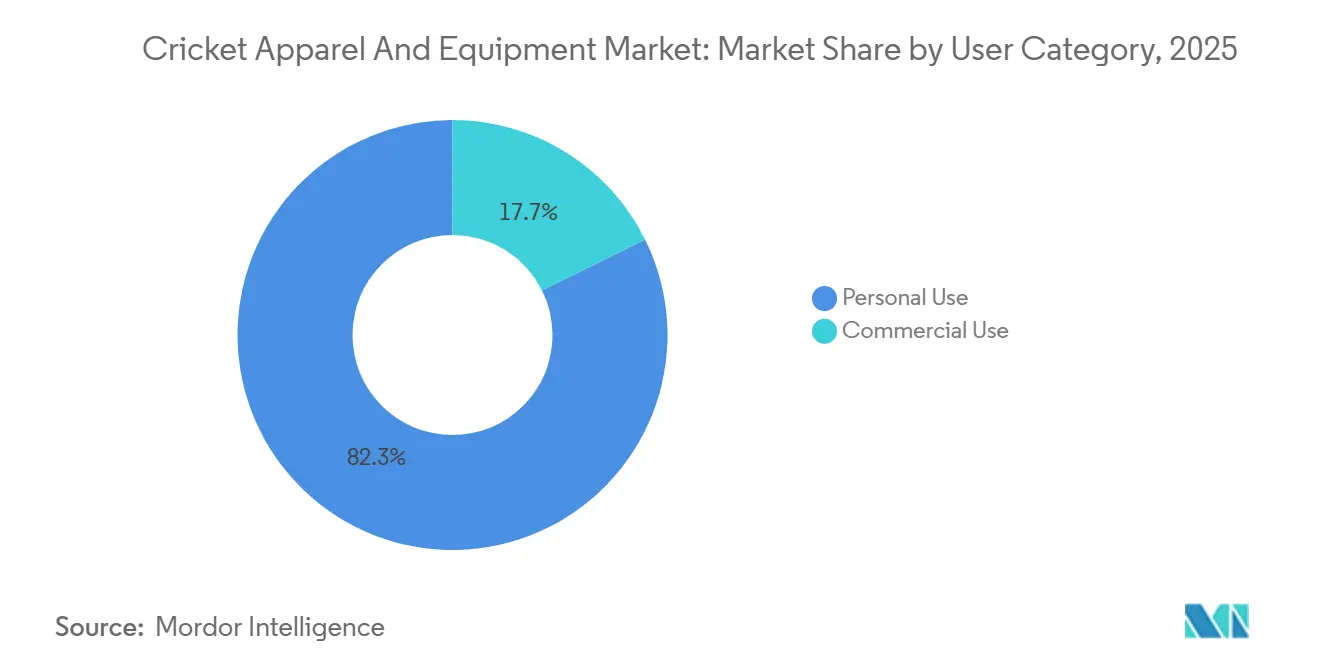

- By user category, personal use accounted for 82.33% of the cricket apparel and equipment market size in 2025, whereas commercial use is advancing at a 7.68% CAGR through 2031.

- By distribution channel, offline retail commanded 79.67% revenue in 2025, yet online retail is forecast to grow at 8.05% CAGR to 2031.

- By geography, Asia-Pacific generated 65.56% revenue in 2025, while North America leads growth with an 7.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cricket Apparel And Equipment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of professional cricket leagues | +1.8% | Global, with concentration in India, Australia, United Kingdom, United Arab Emirates | Medium term (2-4 years) |

| Growth of women's cricket | +1.2% | Global, led by India, Australia, England, New Zealand | Long term (≥ 4 years) |

| Technological advancements in equipment design | +1.0% | Global, early adoption in Australia, India, United Kingdom | Medium term (2-4 years) |

| Increasing grassroots and academy-level participation | +0.9% | Asia-Pacific core, spill-over to North America and Middle East and Africa | Long term (≥ 4 years) |

| Increasing influence of professional players and endorsements | +0.7% | Global, strongest in India and Australia | Short term (≤ 2 years) |

| Rising demand for customized and personalized gear | +0.6% | North America, Europe, urban India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of professional cricket leagues

The growing popularity of professional cricket leagues is a significant driver of the global cricket apparel and equipment market. These leagues enhance the sport's visibility, increase fan engagement, and elevate its aspirational appeal. High-profile tournaments, such as franchise-based T20 leagues, attract large global audiences through broadcast and digital platforms. This exposure encourages greater participation at amateur and semi-professional levels, driving demand for branded apparel, bats, protective gear, and accessories. The sport's strong digital presence further supports this trend. The International Cricket Council (ICC) has surpassed 10 billion video views across social media platforms and is projected to exceed 16 billion views in 2024, underscoring cricket's expanding global reach[1]Source: International Cricket Council, "ICC MEN’S T20 WORLD CUP 2026 DELIVERING UNPRECEDENTED GLOBAL DIGITAL GROWTH AND ACCESS," icc-cricket.com. This increase in online engagement not only strengthens fan loyalty but also boosts merchandise sales, as viewers aspire to emulate professional players. Furthermore, the commercialization driven by leagues, including team sponsorships, player endorsements, and licensed merchandise, is fostering product innovation and intensifying brand competition. These factors collectively contribute to the sustained growth of cricket-related apparel and equipment worldwide.

Growth of women’s cricket

The growth of women’s cricket is becoming a significant driver of the global cricket apparel and equipment market. Increased investment, greater visibility, and institutional support are boosting female participation at both professional and grassroots levels. A key example of this trend is the rise in financial support, with the International Cricket Council increasing the prize pool for the Women’s Cricket World Cup from USD 3.5 million in 2022 to USD 13.88 million in 2025. This amount surpasses the USD 10 million awarded to the 2023 Men’s World Cup champions, highlighting efforts to achieve parity in the sport[2]Source: International Cricket Council, "ICC Women’s Cricket World Cup 2025," icc-cricket.com. This development is encouraging more women and girls to participate in cricket, driving demand for specialized apparel, footwear, and equipment designed for female athletes. Furthermore, increased media coverage, sponsorship agreements, and the creation of women-focused leagues are enhancing the sport’s commercial appeal. This has prompted brands to expand product offerings and invest in gender-specific innovations. Consequently, the growing ecosystem of women’s cricket is not only transforming participation trends but also contributing significantly to the global demand for cricket apparel and equipment.

Increasing grassroots and academy-level participation

Increasing participation at the grassroots and academy levels is a key driver of the global cricket apparel and equipment market. Structured training programs, school initiatives, and community-based cricket development efforts are steadily expanding the player base. Cricket boards, foundations, and private academies are investing in early-stage talent development, generating consistent demand for entry-level and intermediate gear, including bats, pads, gloves, and training apparel. For example, the Lancashire Cricket Foundation reported 121,503 participants across schools, clubs, and community programs in its 2024 Impact Report, highlighting the growing reach of organized cricket at the grassroots level[3]Source: Lancashire Cricket, "Grassroots cricket participation grows to record levels across Lancashire in 2024," cricket.lancashirecricket.co.uk. These initiatives not only build long-term interest in the sport but also encourage regular equipment upgrades as players advance through skill levels. Furthermore, the increasing professionalization of coaching infrastructure and the focus on performance training are driving demand for high-quality and specialized products, supporting sustained growth in the global cricket apparel and equipment market.

Increasing influence of professional players and endorsements

The growing influence of professional players and endorsements is a significant driver of the global cricket apparel and equipment market. Consumers increasingly associate product quality and performance with the credibility of elite athletes. Endorsements by prominent cricketers not only shape brand perception but also create aspirational value, encouraging fans and amateur players to purchase gear similar to that used by their favorite players. For instance, Sanspareils Greenlands offers player-endorsed product lines such as the Hardik Pandya HP series, KL Rahul KL series, Rishabh Pant RP series, and the Smriti Mandhana collection. These products are often promoted with targeted discounts of approximately 10% to enhance accessibility. Such collaborations combine professional-grade performance features with celebrity appeal, fostering greater consumer engagement and brand loyalty. Additionally, the increasing visibility of players on digital platforms and in global leagues amplifies their influence, driving frequent product upgrades and premium purchases. This trend is contributing to the accelerated demand growth across cricket apparel and equipment categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of counterfeit and low-quality products | -0.8% | India, Pakistan, Bangladesh, emerging markets | Short term (≤ 2 years) |

| Limited global reach of cricket as a sport | -0.6% | Global, most acute outside Commonwealth nations | Long term (≥ 4 years) |

| Supply chain dependence on specific raw materials | -0.5% | Global, acute in India, United Kingdom, Australia | Medium term (2-4 years) |

| Seasonal and format-dependent demand fluctuations | -0.4% | Global, varies by domestic cricket calendar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Risk of counterfeit and low-quality products

The prevalence of counterfeit and low-quality products poses a significant challenge to the global cricket apparel and equipment market. The availability of imitation goods undermines brand credibility and erodes consumer trust. Unregulated local manufacturers and unauthorized sellers often produce substandard bats, protective gear, and apparel that do not meet safety or performance standards, increasing the risk of player injuries and diminishing the overall user experience. These lower-cost alternatives, available in both offline and online marketplaces, create price-based competition, discouraging consumers from purchasing genuine, high-quality products from established brands such as Kookaburra Sport and Gray-Nicolls. Furthermore, counterfeit products dilute brand value and reduce revenue for legitimate manufacturers, restricting their capacity to invest in innovation and product development. This issue is particularly acute in price-sensitive markets, where affordability often takes precedence over authenticity, thereby limiting the growth potential of the organized cricket apparel and equipment industry.

Limited global reach of cricket as a sport

The limited global appeal of cricket significantly restrains the growth of the global cricket apparel and equipment market. The sport's popularity is predominantly concentrated in regions such as South Asia, the United Kingdom, and Australia, while engagement remains relatively low in major markets across North America, Europe, and parts of East Asia. Unlike widely popular sports such as football or basketball, cricket faces challenges such as insufficient infrastructure, limited media presence, and a lack of grassroots development in many high-potential countries. Although the International Cricket Council continues efforts to promote cricket in non-traditional regions, progress has been slow and inconsistent due to cultural preferences and restricted access to facilities. This geographic concentration of interest limits global demand for cricket-specific apparel and equipment, thereby constraining market growth and reducing incentives for brands to invest in untapped regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protective Gear Outpaces Traditional Bat Demand

The cricket bat segment continues to dominate the cricket apparel and equipment market, holding a 39.18% share in 2025. This demand is driven by the growing participation of players across professional, amateur, and grassroots levels, coupled with ongoing advancements in bat design and performance features. Players increasingly seek bats that provide enhanced power, balance, and stroke precision, prompting manufacturers to develop advanced willow grades, optimized blade profiles, and lightweight constructions. The preferences of professional cricketers significantly influence consumer choices, as many players aim to replicate the equipment used by elite athletes, thereby boosting sales of premium bats. Additionally, the rising popularity of shorter formats like T20 cricket has heightened the focus on aggressive batting styles, further increasing the demand for high-performance bats designed for power-hitting. Frequent bat replacement cycles due to wear and tear, along with the growing availability of specialized sports retail and e-commerce platforms, are also contributing to sustained growth in this segment.

The protective gear segment is projected to grow at a 7.32% compound annual growth rate (CAGR) through 2031, driven by increasing awareness of player safety, stricter regulations, and the rising intensity of the game across formats. As cricket becomes faster and more competitive, players at all levels are prioritizing high-quality protective equipment, including helmets, pads, gloves, and guards, to reduce the risk of injuries. Governing bodies such as the International Cricket Council have reinforced safety standards, particularly regarding helmet usage and impact protection, encouraging the widespread adoption of certified gear. Technological advancements, such as lightweight materials, improved shock absorption, and ergonomic designs, are further enhancing product appeal and comfort, leading to higher replacement rates. Additionally, increasing participation in youth and amateur cricket, where safety concerns are more pronounced among new players and parents, is significantly driving demand for reliable and standardized protective equipment globally.

By End User: Youth Segment Accelerates Amid Academy Proliferation

The adult end-user segment in the cricket apparel and equipment market held a dominant 79.17% market share in 2025, driven by increasing participation in recreational leagues, corporate tournaments, and semi-professional cricket, where individuals actively invest in higher-quality and performance-oriented gear. Adults prioritize durability, brand reputation, and advanced features such as lightweight materials, ergonomic designs, and enhanced protection, resulting in higher spending per capita compared to other segments. The influence of professional cricket leagues and player endorsements further motivates adult consumers to purchase premium and branded products that replicate professional standards. Additionally, rising health awareness and the growing popularity of sports as a fitness activity are encouraging more adults to engage in cricket, thereby boosting consistent demand for apparel, bats, and protective equipment. The expansion of organized retail and e-commerce platforms also facilitates easy access to a wide range of specialized products, supporting sustained growth in this segment.

The kids end-user segment, growing at a compound annual growth rate (CAGR) of 7.47% through 2031, is driven by the increasing focus on early sports engagement, school-level cricket programs, and structured coaching academies that encourage participation from a young age. Parents are investing in cricket equipment and apparel for children to support skill development, physical activity, and potential career pathways in sports. The availability of affordable, size-specific, and beginner-friendly equipment tailored for children is further facilitating adoption, making it easier for young players to access the sport. Additionally, the influence of star cricketers and media exposure inspires children to take up cricket, driving demand for visually appealing and branded products. Safety concerns also play a critical role, as parents prioritize protective gear such as helmets, pads, and gloves, contributing to higher product uptake. Together, these factors are strengthening the demand for cricket apparel and equipment within the kids segment globally.

By User Category: Commercial Segment Driven by Infrastructure Investment

Personal use is accounted for 82.33% of the market share in 2025. This segment in the cricket apparel and equipment market is primarily driven by the increasing participation of individuals in recreational and amateur cricket. Factors such as growing health awareness and the adoption of sports as a lifestyle activity contribute to this trend. Consumers in this category are motivated by fitness goals, social interaction, and skill development, which sustain the demand for bats, apparel, and protective gear for casual play. The rising popularity of local leagues, weekend matches, and informal cricket formats further encourages individuals to invest in personal equipment rather than relying on shared resources. Additionally, exposure to professional cricket through media and digital platforms inspires enthusiasts to purchase branded and performance-oriented products that align with professional standards. The availability of affordable product ranges and the convenience of online retail channels also facilitate access to a wide variety of cricket gear, supporting the growth of the personal use segment.

The commercial use segment is expected to grow at a compound annual growth rate (CAGR) of 7.68% through 2031. This growth is driven by the expansion of organized cricket infrastructure, including academies, schools, clubs, and training centers, which require bulk procurement of apparel and equipment. Institutions prioritize standardized, durable, and high-quality gear to support training programs, tournaments, and regular practice sessions, ensuring consistent demand at scale. The increasing professionalization of coaching and the establishment of cricket academies in both emerging and established markets further strengthen this segment. These organizations regularly upgrade equipment to maintain safety and performance standards. Additionally, corporate leagues, event organizers, and sports facilities contribute to commercial demand by purchasing equipment for team-based activities and rental purposes. Support from governing bodies, such as the International Cricket Council, in promoting structured cricket development also bolsters investments in infrastructure and training ecosystems, driving sustained demand in the commercial use segment.

By Distribution Channel: Digital Channels Disrupt Traditional Retail

Offline channels held a 79.67% market share in 2025. Sales through these channels are driven by consumers' strong preference for physically evaluating products, especially items like bats, gloves, and protective gear that require proper fit, balance, and comfort assessment before purchase. In-store experiences allow customers to test weight distribution, grip, and material quality, which are critical for performance-oriented equipment. Specialty sports stores and authorized dealers enhance the shopping experience by offering expert guidance, customization services, and immediate product availability, thereby boosting buyer confidence and satisfaction. Additionally, offline channels mitigate the risk of counterfeit purchases, which is particularly important in markets prone to fake products. The presence of established retail networks and local sports shops near cricket-playing communities further ensures consistent footfall, solidifying offline channels as a dominant and reliable sales avenue.

Online retail is expected to grow at a CAGR of 8.05% through 2031. This growth is driven by the increasing penetration of e-commerce platforms, the convenience of digital shopping, and the availability of a wide range of products across various price points and brands. Consumers benefit from features such as easy price comparisons, access to customer reviews, and doorstep delivery, which streamline purchasing decisions. The rise of digital marketing, influencer promotions, and player endorsements on social media platforms is also directing traffic to online stores, encouraging impulse purchases and brand exploration. Furthermore, online channels often provide discounts, bundled deals, and exclusive product launches, appealing to price-sensitive buyers. The adoption of direct-to-consumer strategies by brands, coupled with improved logistics and return policies, is further driving online sales, particularly among younger, tech-savvy consumers in the cricket apparel and equipment market.

Geography Analysis

In 2025, Asia-Pacific accounted for 65.56% of the revenue in the cricket apparel and equipment market. This dominance is primarily driven by the deep-rooted popularity of cricket in countries such as India, Australia, Pakistan, and Bangladesh, where the sport serves as both a major recreational activity and a significant commercial industry. High viewership of domestic and international tournaments, combined with strong fan loyalty, continues to drive demand for cricket apparel and equipment. The region benefits from well-established cricket infrastructure, widespread grassroots programs, and increasing participation across various age groups, which support consistent product consumption. Furthermore, endorsements by professional players, franchise leagues, and the adoption of premium products contribute to market growth. The expansion of organized retail and online platforms has also enhanced product availability in urban and semi-urban areas.

North America is projected to achieve a compound annual growth rate (CAGR) of 7.81% from 2026 to 2031. The market's growth in this region is fueled by the increasing popularity of cricket among immigrant populations, particularly those from South Asia and the Caribbean. This has led to the establishment of local leagues, clubs, and community tournaments. The sport's visibility is further enhanced by franchise-based competitions and international events hosted in the region, broadening its appeal beyond traditional audiences. Investments in cricket infrastructure, including stadiums and training facilities, along with the emergence of professional leagues, are encouraging participation at amateur and semi-professional levels. Additionally, the growth of specialty sports retailers and e-commerce platforms is improving product accessibility, while youth engagement programs are gradually building a sustainable consumer base for cricket-related products.

In Europe, South America, and the Middle East and Africa, the cricket apparel and equipment market is driven by a combination of expatriate-driven demand, gradual expansion of the sport, and increasing institutional support. In the United Kingdom, cricket maintains a strong traditional base supported by established club systems. In the Middle East, the sport is gaining traction due to large South Asian populations and the hosting of international tournaments. Emerging interest in parts of Europe and South America is bolstered by development programs and efforts by the International Cricket Council to globalize the sport. Additionally, rising investments in sports infrastructure, growth in school and academy-level participation, and improved access to cricket equipment through retail and digital channels are collectively contributing to market expansion in these regions.

Competitive Landscape

The cricket apparel and equipment market is moderately consolidated, featuring a mix of large global sportswear companies, specialized cricket-focused manufacturers, and emerging direct-to-consumer brands. Competition in the market is influenced by a balance between scale advantages and niche expertise. Established players benefit from extensive distribution networks and strong brand recognition, while specialized manufacturers maintain their position through sport-specific innovations and long-standing institutional relationships. Meanwhile, new entrants are disrupting the market by adopting digital-first strategies, offering customization options, and utilizing agile production models, allowing them to compete effectively without relying on traditional retail channels.

Strategic activities in the market indicate a trend toward consolidation and portfolio diversification. Horizontal integration has become a key strategy for achieving operational efficiencies and expanding product offerings. Mergers and partnerships are increasingly aimed at combining complementary sports categories, optimizing seasonal demand cycles, and enhancing licensing and distribution capabilities. These strategies enable companies to scale manufacturing, improve supply chain efficiency, and enter adjacent product segments while preserving distinct brand identities. Additionally, competitive approaches vary, with some players focusing on high-visibility marketing through sponsorships and endorsements, while others emphasize product differentiation through innovation, performance improvements, and long-term institutional partnerships.

The market offers significant growth opportunities in areas such as smart equipment, sustainable materials, and women-specific product lines, where current offerings are underdeveloped relative to consumer demand. Emerging players are addressing these gaps by introducing sensor-enabled gear, data-driven training solutions, and environmentally sustainable products. They are also leveraging advanced digital tools, such as online customization platforms and authentication technologies, to combat counterfeit products. Furthermore, increasing investment in cricket-related assets, including franchise-based ecosystems, is reshaping the competitive landscape. These investments are creating integrated platforms for merchandising, media monetization, and brand expansion. Additionally, evolving regulatory standards and advancements in material technology are lowering entry barriers, fostering innovation, and intensifying competition across the market.

Cricket Apparel And Equipment Industry Leaders

-

Adidas AG

-

Nike Inc.

-

Gunn & Moore

-

Sanspareils Greenlands Private Limited

-

Kookaburra Sport Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Kane Williamson entered the cricket equipment market with a premium alloy-based groin protection product inspired by a prior injury from a high-speed delivery by Dale Steyn. The product addresses gaps in traditional protective gear with enhanced impact resistance, improving player confidence and safety. Tested across various playing levels, it is positioned as a high-performance alternative, emphasizing innovation-driven product development.

- November 2025: Gray-Nicolls launched its 2026 product range, focusing on portfolio diversification and innovation across bats, protective gear, and apparel. The expanded bat lineup includes models for various playing styles, skill levels, and consumer segments, with specialized designs for women and professional athletes. The initiative emphasized player-focused development by aligning bat specifications with international cricketers' preferences and incorporating features like optimized profiles, lightweight pick-up, and enhanced power. This launch aimed to strengthen brand positioning through innovation, inclusivity, and athlete-driven customization, catering to both elite and grassroots players.

- June 2025: SG Cricket introduced its 2025 professional-grade cricket balls featuring enhanced seam durability and consistent swing performance, crafted with superior leather quality and hand-stitched construction. These balls received positive reviews for their reliability in match conditions.

- May 2025: Tech startup Nebula Cricket released the first smart bat with embedded sensors providing real-time analytics on swing speed, ball impact position, and shot power. The bat syncs with a mobile app delivering data-driven feedback for players and coaches, a significant leap in cricket training technology.

- January 2025: Kookaburra unveiled new helmets, pads, and gloves leveraging carbon fiber and titanium composites for lightweight yet highly impact-resistant protection. Notable innovations include multi-layered energy-absorbing helmet foam and moisture-wicking fabric linings in gloves for better grip and comfort.

- December 2024: Gunn & Moore (GM) introduced three new high-performance cricket bats, the Psyche, Brava, and an updated Range model, featuring advanced willow curing and innovative blade profiles. These bats offer improved balance, increased sweet spot size, and lightweight designs catered to modern stroke play.

Global Cricket Apparel And Equipment Market Report Scope

| Cricket Bats |

| Cricket Balls |

| Protective Gear |

| Cricket Apparel |

| Footwear |

| Accessories and Others |

| Kids |

| Adults |

| Personal Use |

| Commercial Use |

| Offline Channels |

| Online Channels |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | United Kingdom |

| Ireland | |

| Scotland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | India |

| Australia | |

| Pakistan | |

| New Zealand | |

| Bangladesh | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Oman | |

| Zimbabwe | |

| Rest of Middle East and Africa |

| By Product Type | Cricket Bats | |

| Cricket Balls | ||

| Protective Gear | ||

| Cricket Apparel | ||

| Footwear | ||

| Accessories and Others | ||

| By End User | Kids | |

| Adults | ||

| By User Category | Personal Use | |

| Commercial Use | ||

| By Distribution Channel | Offline Channels | |

| Online Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Ireland | ||

| Scotland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| Australia | ||

| Pakistan | ||

| New Zealand | ||

| Bangladesh | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Oman | ||

| Zimbabwe | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will the cricket apparel and equipment market grow through 2031?

It is forecast to expand at a 6.81% CAGR between 2026 and 2031, rising from USD 0.95 billion in 2026 to USD 1.31 billion by 2031.

Which product category is expected to outperform bats over the forecast period?

Protective gear, driven by mandatory helmet-replacement rules, is projected to grow at a 7.32% CAGR, outpacing bat sales.

Why is North America viewed as the fastest-growing region?

Major League and Minor League Cricket have achieved double-digit growth in attendance and viewership, contributing to a regional CAGR of 7.81%.

How are online channels influencing traditional cricket-gear retail?

Online specialists offering customized bats and D2C pricing are forecast to grow at an 8.05% CAGR, eroding offline share and pressuring legacy margins.

Page last updated on: