Photography Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

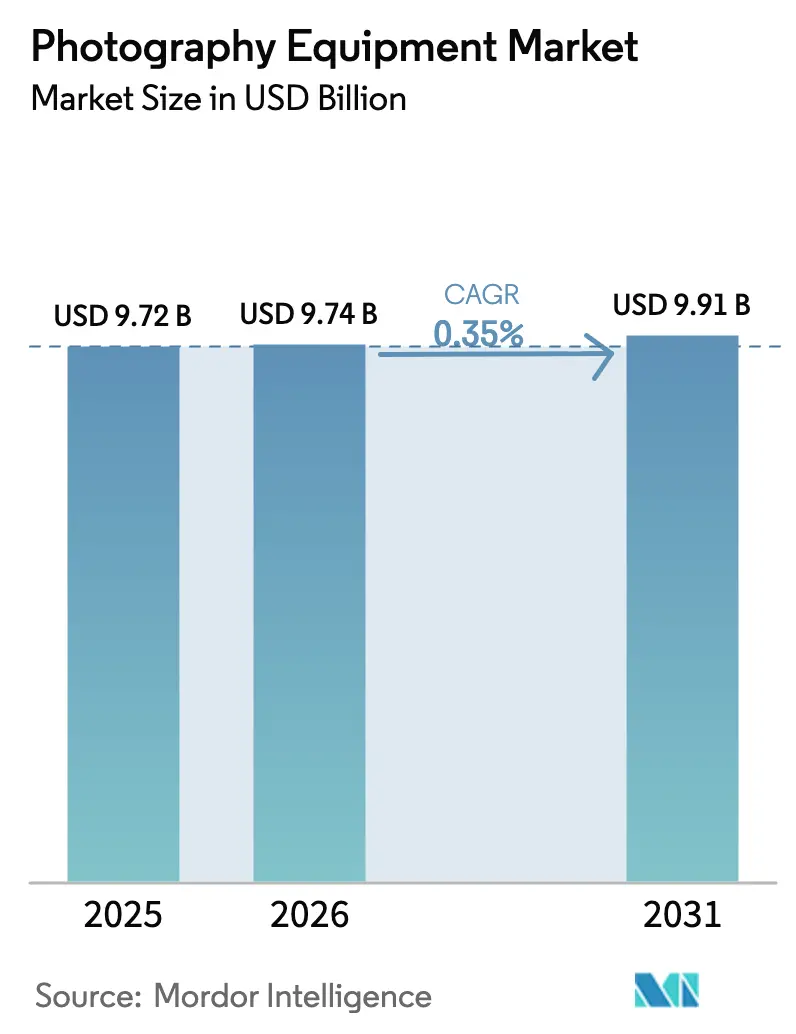

| Market Size (2026) | USD 9.74 Billion |

| Market Size (2031) | USD 9.91 Billion |

| Growth Rate (2026 - 2031) | 0.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

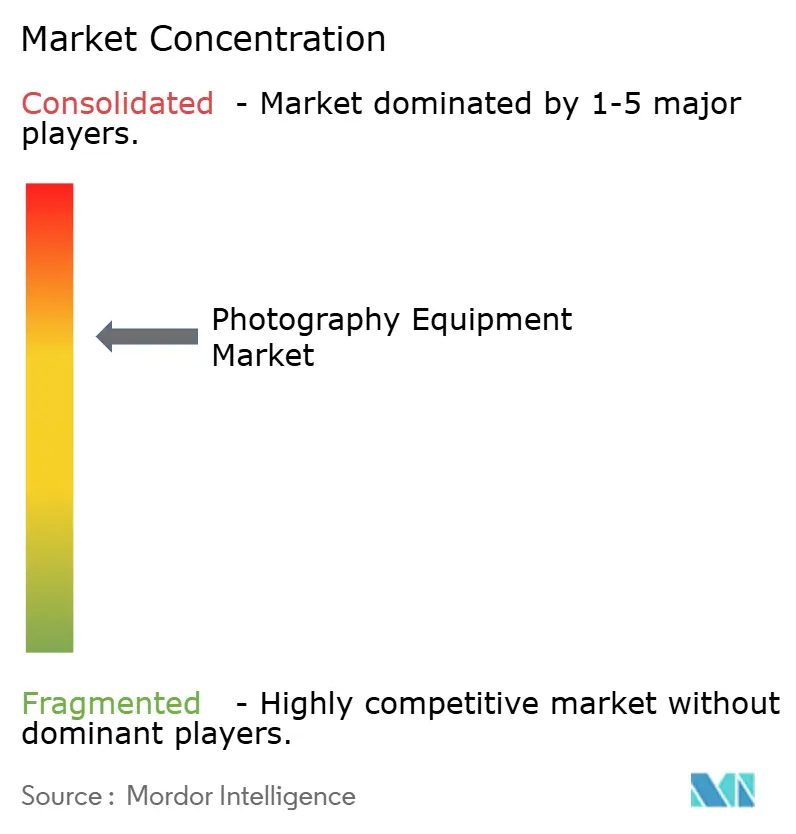

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photography Equipment Market Analysis by Mordor Intelligence

The photography equipment market size is expected to grow from USD 9.72 billion in 2025 to USD 9.74 billion in 2026 and is forecast to reach USD 9.91 billion by 2031 at a 0.35% CAGR over 2026-2031. While the overall growth appears tepid, there's a noticeable shift in the vendor landscape. Demand for entry-level equipment is increasingly gravitating towards smartphones. At the same time, there's a notable uptick in demand for mirrorless cameras, especially those tailored for vlogging and advanced 8K workflows, helping to maintain robust average selling prices. Today's competitive edge hinges on features like AI-driven autofocus, in-body stabilization, and integrated computational workflows that significantly reduce post-production time. However, the supply chain faces challenges, with Sony commanding a dominant 53% share of the global Complementary Metal-Oxide-Semiconductor (CMOS) output, even as Chinese competitors steadily close the gap. In the United States (U.S.) and Europe, tariff pressures are tightening margins, particularly at the lower end of the market. Yet, manufacturers and specialty retailers are finding new avenues for revenue through rental and subscription models, alongside direct-to-creator e-commerce channels.

Key Report Takeaways

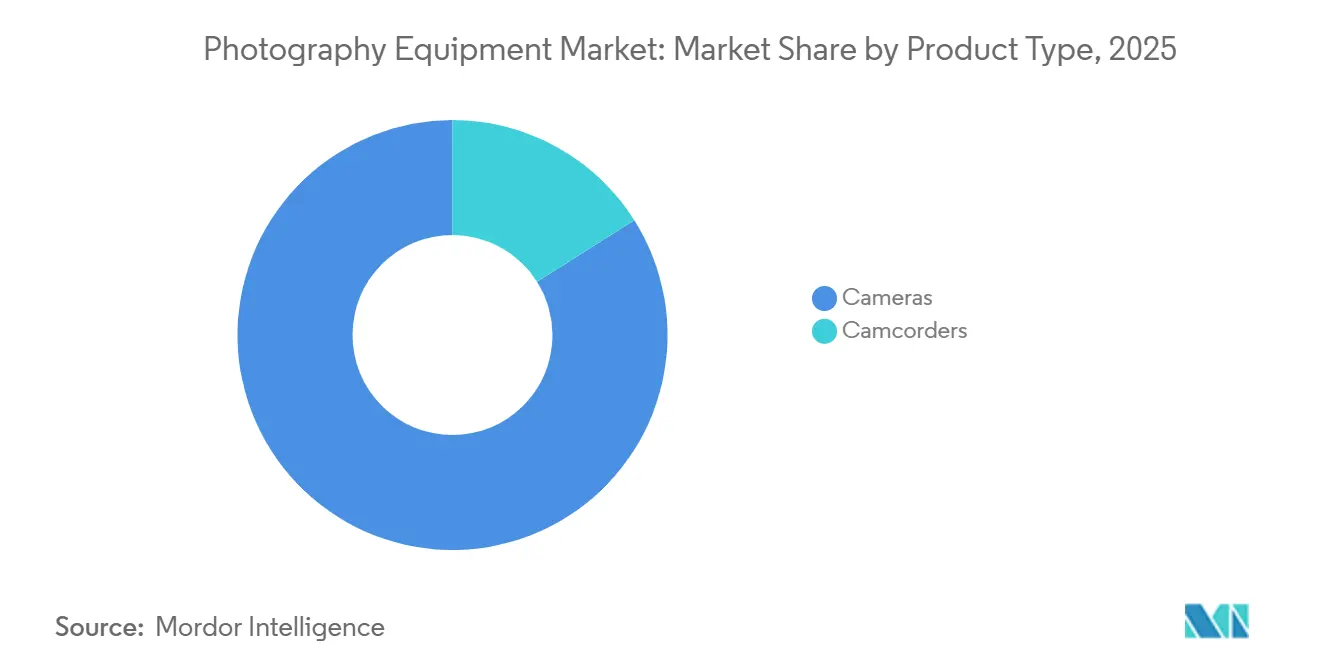

- By product type, cameras led with 83.96% revenue share in 2025; camcorders are projected to expand at a 0.80% CAGR to 2031.

- By category, the premium tier captured 42.82% of the 2025 photography equipment market share, while mass-market models are tracking a 0.93% CAGR through 2031.

- By end user, professional workflows held 59.74% of 2025 revenue; the personal segment is advancing at a 0.93% CAGR on the back of vlogging adoption.

- By distribution channel, online channels accounted for 55.82% of the 2025 turnover, and offline channels are set to grow at a 1.10% CAGR to 2031.

- By geography, North America dominated with 38.43% of 2025 sales; Asia-Pacific is the fastest-growing region at a 1.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Photography Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mirrorless camera adoption and technological advances | +0.8% | Global, with the strongest uptake in North America, Europe, and Asia-Pacific (Japan, China, South Korea) | Medium term (2-4 years) |

| Social-media driven content-creation boom | +0.6% | Global, with early gains in North America, Europe, and Asia-Pacific (India, Southeast Asia) | Short term (≤ 2 years) |

| High-resolution and video-centric sensor demand | +0.5% | Global, with professional segment concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of e-commerce retail channels | +0.3% | Global, led by North America and the Asia-Pacific | Short term (≤ 2 years) |

| Rental and subscription models for premium gear | +0.2% | North America and Europe, emerging in the Asia-Pacific urban centers | Long term (≥ 4 years) |

| AI-powered in-camera computational workflows | +0.4% | Global, with early adoption in North America, Europe, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mirrorless camera adoption and technological advances

As the camera industry pivots from DSLRs to mirrorless systems, revenue dynamics are shifting. Data from CIPA reveals that from January to October 2024, mirrorless camera shipments surged by 14.5%, while DSLR shipments plummeted by 19.8%[1]Source: Camera & Imaging Products Association, “Shipments by Product Type January-October 2024,” cipa.jp. Canon's EOS R5 Mark II, unveiled in July 2024, boasts a 45-megapixel full-frame sensor, 8.5-stop in-body stabilization, and 8K 60p video recording, catering to hybrid shooters who crave both high-quality stills and cinematic footage. Sony's Alpha 7R V, launched in late 2024, is equipped with a specialized AI processing unit that recognizes humans, animals, birds, insects, and vehicles in real-time, leading to an estimated 30% decrease in missed focus during fast-action shots. Nikon's Z8, a compact version of the Z9 and priced USD 1,000 less, made professional-grade autofocus and 8K video accessible to enthusiasts, playing a pivotal role in Nikon's 10.2% uptick in imaging revenue for FY2024. Fujifilm's X-S20, tailored for vloggers with its flip-out screen and enhanced battery life, resonated with YouTube creators who prioritize compactness without compromising on image quality. Beyond just autofocus speed, the mirrorless edge is evident: electronic viewfinders now sport 9.44-million-dot OLED panels with 240 Hz refresh rates, erasing the lag that once held back sports photographers. This advancement has empowered manufacturers to craft lighter, weather-sealed bodies, drawing interest from the travel and adventure markets.

Social-media driven content-creation boom

With TikTok boasting 1.5 billion monthly active users and YouTube reaching 2.7 billion, a vibrant creator economy has emerged, linking gear quality directly to monetization potential. B&H Photo Video highlighted that in Q4 2024, the Sony ZV-E10 II, a vlogging-centric APS-C mirrorless camera featuring a directional microphone and product-showcase mode, surged into its top-five best-sellers, as creators transitioned from smartphone gimbals. Canon's EOS R50, retailing at USD 679 for the body alone, delivers 4K 30p video and boasts a vari-angle touchscreen. This positions it as an ideal entry point for Instagram Reels and TikTok creators seeking the shallow depth-of-field aesthetics that phone cameras can't provide. Nikon's Z30, part of a "Vlogger Kit" priced at USD 1,099 and bundled with the Nikkor Z DX 16-50mm f/3.5-6.3 VR lens, comes with a stereo microphone and features vertical-video recording, catering to the 9:16 aspect ratio that's a favorite on short-form platforms. Launched in late 2024, Fujifilm's X-M5 incorporates film-simulation modes like Velvia, Provia, and Acros, mimicking analog color science. This allows creators to achieve unique in-camera looks, minimizing the need for extensive post-production. While photography equipment imports saw a 22% year-on-year rise in 2024, underscoring the content-creation boom, China's Douyin (the domestic counterpart of TikTok) boasts a staggering 750 million daily active users. Many of these users are turning to mirrorless cameras, seeking enhanced production value, as reported by the Camera and Imaging Products Association.

High-resolution and video-centric sensor demand

As the industry shifts to a hybrid model blending stills and video, sensor designers are prioritizing readout speed and heat management. In FY2024, Sony's Imaging and Sensing Solutions segment reported JPY 1,602.7 billion in revenue, a 14% increase, and JPY 193.5 billion in operating income, driven by demand for stacked CMOS sensors enabling 8K 60p recording without overheating. Canon's dual-gain-output sensor architecture, introduced in the EOS R3 and refined in the R5 Mark II, offers 13 stops of dynamic range at ISO 3200, allowing wedding and event photographers to handle mixed lighting without exposure bracketing. Nikon's April 2024 acquisition of RED Digital Cinema, with undisclosed financial details, highlights its aim to integrate REDCODE RAW compression and color science into future Z-series models, further blurring lines between cinema cameras and premium mirrorless systems. Blackmagic Design's Pocket Cinema Camera 6K Pro, priced at USD 2,495, delivers 13 stops of dynamic range and integrates seamlessly with DaVinci Resolve, making it a favorite among independent filmmakers who previously rented RED or ARRI systems at USD 500-1,000 daily. The professional video sector's demand for higher resolutions is driving sensor pixel counts. For example, Phase One's IQ4 150MP medium-format back, a staple in commercial photography, produces 900-megapixel raw files requiring CFexpress Type B cards and 64 GB of RAM, boosting demand for storage and computing accessories.

AI-powered in-camera computational workflows

Canon's Deep Learning AF, introduced in the EOS R3 and R6 Mark III, uses a neural network trained on 1 million images to distinguish human subjects from background distractions, reducing false-positive focus locks by 40% in crowded events. Sony's AI-driven Real-time Recognition AF, featured in the Alpha 7R V and ZV-E10 II, tracks insects and small birds with 60 AF calculations per second, enabling macro and wildlife photography that previously required manual focus. Nikon's Z8 and Z9 use a 3D-tracking algorithm with data from 493 phase-detect points to predict motion trajectories, maintaining focus on erratic subjects like soccer players or birds in flight. Fujifilm's X-Processor 5, powering the X-H2S and X-T5, includes a subject-detection algorithm optimized for automotive and aviation photography, prioritizing the cockpit or driver's helmet over the vehicle body. Computational photography advancements extend to post-capture processing; AI tools like Adobe Lightroom's AI Denoise and Topaz Photo AI's subject-selection are now integrated into camera firmware, allowing in-camera noise reduction and sharpening, cutting post-production time by 30-50%. DJI's Osmo Action 5 Pro, launched in September 2024, features a variable-aperture sensor (f/2.8-f/4.0) and AI-driven horizon leveling, highlighting the expansion of computational imaging beyond interchangeable-lens systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone substitution effect | -1.2% | Global, with the strongest impact in the entry-level and compact camera segments | Short term (≤ 2 years) |

| High upfront cost of professional equipment | -0.5% | Global, with pronounced effects in emerging markets (India, Southeast Asia, Latin America) | Medium term (2-4 years) |

| Tariff-induced price inflation in key markets | -0.4% | North America, Europe, with spillover to the Asia-Pacific | Short term (≤ 2 years) |

| Supply-chain vulnerabilities in image sensors | -0.3% | Global, with concentration risk in Japan (Sony) and South Korea (Samsung) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smartphone substitution effect

Apple's iPhone 16 Pro and Samsung's Galaxy S25 Ultra have used computational photography to close the image-quality gap with entry-level mirrorless cameras by stacking multiple exposures in real time. CNET's comparison showed the iPhone 16 Pro's night-mode astrophotography matched the noise performance of a USD 1,200 mirrorless camera with a USD 400 lens at ISO 6400, reducing its appeal for casual users. TechRadar noted the Galaxy S25 Ultra's 200-megapixel sensor and AI-driven subject isolation produced sharper portraits than a USD 800 APS-C mirrorless body with a kit lens, particularly in mixed lighting. CIPA data underscores the trend: compact camera shipments dropped 8.2% from January to October 2024, even as the overall camera market grew, as smartphones replaced point-and-shoot models. This effect is most evident in the sub-USD 500 segment, where smartphones offer superior convenience (always-on connectivity, instant sharing, computational HDR) without the complexity of interchangeable lenses. Canon and Nikon have largely exited the compact segment; neither launched a new point-and-shoot in 2024-2025, focusing instead on full-frame mirrorless bodies priced above USD 1,500, where sensor size and lens options remain key advantages. The risk is that smartphone computational photography may soon replicate the shallow depth-of-field and low-light performance of APS-C sensors, shrinking the market to professionals and enthusiasts investing in full-frame or medium-format systems.

High upfront cost of professional equipment

Professional mirrorless kits, often exceeding USD 3,000 for the body, two lenses, memory cards, and accessories, pose a significant hurdle for creators and hobbyists in emerging markets. Lensrentals, a U.S.-based rental service boasting an estimated annual revenue between USD 25-100 million, highlighted in Q4 2024 that Canon's EOS R5 Mark II and Sony's Alpha 7R V topped its rental charts. This trend underscores a growing preference for rentals over ownership, allowing users to better manage their capital outlay. In 2024, Adorama's rental arm, ARC, expanded its inventory by 15%, introducing Nikon Z8 and Fujifilm GFX100S II bodies. This move caters to wedding photographers and commercial studios, who, while needing high-end gear for specific projects, find it hard to justify full purchase prices. While the rental model thrives in the U.S. and Europe, it's still nascent in the Asia-Pacific region. In India, despite a rapidly growing content-creator economy, the absence of robust rental infrastructure forces creators to either invest in entry-level gear or resort to smartphone cameras. Subscription services like Canon's "RF Lens Subscription" (a pilot in Japan) and Sony's "Alpha Gear Subscription" (in Europe) provide monthly access to premium lenses for USD 50-150. However, concerns over equipment condition and peak season availability have limited their adoption. Additionally, tariff-induced price hikes further exacerbate the cost barrier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cameras Anchor Revenue Despite Camcorder Resurgence

In 2025, cameras accounted for 83.96% of the market revenue. However, camcorders are projected to grow at a 0.80% CAGR through 2031, outperforming the market's overall muted growth. This resurgence in camcorders, once deemed obsolete, is driven by rising demand for live-streaming and hybrid events. Canon launched its XA75 and XA70 professional camcorders in Q2 2024, featuring 4K 60p recording and dual SD card slots. These target houses of worship, corporate events, and educational institutions emphasize long-form recording and built-in ND filters over the modular flexibility of mirrorless cameras. Sony's FX6 and FX9, part of its Cinema Line, saw strong FY2024 sales, driven by adoption from Netflix and Amazon Studios for documentary and reality-TV productions. Their appeal is enhanced by Sony's E-mount lens ecosystem and native S-Log3 color profiles. Panasonic's AG-CX350, priced at USD 3,495, offers a 20x optical zoom and dual-codec recording (H.264 and H.265), making it a reliable choice for broadcast journalists and event videographers. The camera segment's dominance is sustained by mirrorless innovation. Canon's EOS R1, unveiled in July 2024 as the flagship successor to the 1D X Mark III DSLR, introduces a global shutter sensor that eliminates rolling-shutter distortion, benefiting sports and wildlife photographers. Nikon's Z9, launched in late 2021, remains a top seller in 2024-2025 with 8K 60p video and 120 fps burst shooting, making it a hybrid tool for photojournalists covering events like the Olympics and World Cup. Fujifilm's GFX100S II, priced at USD 4,999, appeals to commercial and fashion photographers with its 102-megapixel resolution for large-format prints and extensive cropping latitude.

Action cameras and 360-degree cameras are niche but fast-growing segments. DJI's Osmo Action 5 Pro, with a 1/1.3-inch sensor and 13.5 stops of dynamic range, competes with GoPro's HERO12 Black, which faced overheating issues in 8K mode. GoPro's Q3 2024 revenue of USD 255.6 million, down 19% year-on-year, reflects market-share losses to DJI. DJI's Osmo Pocket 3 gimbal camera, priced at USD 519, is praised for superior stabilization and low-light performance. Outdoor and adventure publications consistently rank DJI's Action 5 Pro ahead of GoPro's HERO12 for underwater videography, citing better color accuracy below 10 meters and longer battery life. Insta360's X4 360-degree camera, launched in March 2024, features 8K 30fps recording and AI-powered horizon leveling, opening new use cases for real-estate tours and immersive travel vlogs, capturing share from traditional action cameras.

By Category: Premium Segment Outpaces Mass Market

In 2025, the premium category, accounting for 42.82% of sales, and the mass segment are both growing at a 0.93% CAGR. This growth is driven by prosumer and professional buyers investing in features like advanced autofocus, in-body stabilization, and weather sealing. Canon Marketing Japan's FY2024 results showed a decline in digital interchangeable-lens camera unit sales but an increase in average selling prices due to a shift from entry-level DSLRs to higher-margin mirrorless models priced above USD 2,000. For example, Sony's Alpha 7R V, priced at USD 3,899 body-only, and Nikon's Z8, at USD 3,999, highlight the premium tier's value with 60-megapixel sensors, 8K video, and AI-driven autofocus, justifying their price difference over USD 1,500 mid-tier models. Fujifilm's X100VI, a premium compact priced at USD 1,599, sold out globally within weeks of its February 2024 launch, driven by its retro design and film-simulation modes appealing to street photographers and Instagram influencers. Leica's Q3, priced at USD 5,995, offers a 60-megapixel full-frame sensor and Summilux 28mm f/1.7 lens in a compact body, targeting affluent enthusiasts who prioritize build quality and brand heritage.

The mass segment, including entry-level mirrorless and DSLR bodies priced under USD 1,000, faces challenges from smartphone competition and tariff-induced price hikes. Canon's EOS R50 and Nikon's Z30, both priced around USD 679 body-only, aim to transition smartphone users to interchangeable-lens systems. However, their growth is constrained by the iPhone 16 Pro's computational photography, which mimics professional effects without the complexities of manual settings. Sony's ZV-E10 II, priced at USD 999, bridges the Mass and Premium categories with features like 4K 60p video and a product-showcase mode, appealing to YouTube creators seeking professional-grade features without flagship pricing. For the Mass segment to remain viable, manufacturers must integrate AI-driven features, such as automatic subject tracking and in-camera noise reduction, to differentiate entry-level cameras from smartphones while keeping prices below USD 800 to attract hobbyists and students.

By End User: Professional Demand Anchors Growth

In 2025, professional end-users accounted for 59.74% of the revenue, driven by wedding, event, and commercial photographers seeking features like dual-card slots, weather sealing, and high-speed burst shooting. Nikon's Z8, priced USD 1,000 less than the flagship Z9, gained traction among wedding photographers who previously rented the Z9 for USD 300-500 per weekend. Canon's EOS R5 Mark II, with 8.5-stop in-body stabilization and 8K 60p video, became the preferred choice for hybrid shooters covering corporate events and real-estate tours. Sony's Alpha 1, priced at USD 6,499, remained the top pick for sports and wildlife photographers, offering 30 fps burst shooting and 50-megapixel resolution for cropping without quality loss. Fujifilm's GFX100S II, at USD 4,999, serves commercial and fashion photographers requiring 102-megapixel resolution for large-format advertising prints.

The Personal segment is projected to grow at a 0.93% CAGR as content creators and hobbyists upgrade from smartphones. Canon's EOS R50, Nikon's Z30, and Sony's ZV-E10 II target this segment with vlogging features like flip-out screens, directional microphones, and vertical-video recording. Fujifilm's X-M5, launched in late 2024, includes film-simulation modes replicating analog color science, enabling Instagram and TikTok creators to achieve unique in-camera looks. Growth in this segment varies geographically; India's content-creator economy, expected to reach 100 million producers by 2027, drives demand for entry-level mirrorless cameras, while China's Douyin platform (TikTok's domestic counterpart) has 750 million daily active users, many investing in cameras for higher production value. Long-term growth depends on manufacturers simplifying user interfaces and integrating AI-powered features to ease the learning curve for first-time interchangeable-lens camera buyers.

By Distribution Channel: Online Gains Share

In 2025, online channels accounted for 55.82% of total sales. While offline channels are expected to grow at a modest 1.10% CAGR through 2031, e-commerce platforms are outpacing them. These platforms entice consumers with competitive pricing, customer reviews, and next-day delivery, advantages that brick-and-mortar stores find hard to replicate. In Q4 2024, Amazon reported net product sales of USD 82.2 billion. Of this, online stores contributed USD 75.6 billion, marking a 7% year-on-year increase, fueled by an 11% rise in global paid units. A pricing study by Profitero highlighted that Amazon's electronics, including cameras and lenses, were 14% cheaper than those at other major U.S. retailers. This pricing edge has drawn many price-sensitive consumers to Amazon's online platform. Furthermore, Amazon Prime ramped up its same-day and overnight delivery services by 65% in 2024 compared to 2023, effectively narrowing the delivery speed gap that previously benefited local camera shops. Adorama, a specialty retailer based in New York with revenues estimated between USD 500 million and USD 1.0 billion, boosted its e-commerce platform and rental subsidiary, ARC, by 15% in 2024. They introduced the Nikon Z8 and Fujifilm GFX100S II, catering to the rising demand from wedding photographers and commercial studios. B&H Photo Video, another prominent U.S. specialty retailer, noted that the Sony ZV-E10 II and Canon EOS R50 were among its top-five best-sellers in Q4 2024, largely due to vloggers and content creators upgrading from smartphones.

Despite the growth of offline retail, projected at a 1.10% CAGR through 2031, it continues to excel in high-touch segments. Here, customers prioritize hands-on product evaluations and expert guidance. Major brands like Canon, Nikon, and Sony have established flagship stores in cities like Tokyo, New York, and London. These stores not only sell products but also host workshops, offer lens rentals, and run trade-in programs, all of which bolster brand loyalty among professional photographers. Specialty retailers, including Adorama and

Geography Analysis

In 2025, North America commanded a significant 38.43% share of the revenue, bolstered by its well-established professional ecosystems and a robust rental infrastructure. Data from CIPA highlighted a 21.3% uptick in shipments in February 2025, occurring just before the implementation of tariffs[2]Source: Camera & Imaging Products Association, “Shipments by Product Type January-October 2024,” cipa.jp. However, as manufacturers hiked list prices by up to 12%, the growth momentum waned later in the year. With Canada and Mexico enjoying more lenient import duties, they are emerging as alternative import sources for U.S. buyers, complicating channel management. Looking ahead, the proliferation of subscription models, which ease upfront cost barriers, is expected to drive long-term growth, especially for mid-tier creators.

Asia-Pacific is set to outpace other regions, boasting a projected CAGR of 1.12% through 2031. In February 2025, China witnessed a staggering 78.8% surge in mirrorless shipments, a boost largely credited to Douyin’s monetization strategies that favor high-quality content. With a forecasted creator economy of 100 million by 2027, India is positioning itself as a pivotal growth hub, especially for vlogging kits priced under USD 800. Meanwhile, tariff reductions under the Regional Comprehensive Economic Partnership (RCEP), combined with domestic manufacturing in Japan and Thailand, empower vendors to offer competitive pricing[3]Source: Regional Comprehensive Economic Partnership Secretariat, “RCEP Economic Impact Report 2025,” asean.org. Australia and New Zealand are not just markets but strategic launch pads, facilitating English-language marketing campaigns and beta firmware testing, thus speeding up global release feedback loops.

Europe, South America, and the Middle East-Africa collectively contributed to 23.45% of 2025's sales. Western Europe, with its premium market inclination, saw Germany, the United Kingdom, and France together account for a hefty 60% of the full-frame mirrorless volume. Economic fluctuations and steep import duties have dampened South America's market, with Brazil's hefty 60% electronics tariff nudging demand towards refurbished products. In the United Arab Emirates and South Africa, growth is buoyed by tourism and upscale commercial photography services, offering some insulation from the encroachment of smartphone alternatives.

Regulatory Landscape

Photography equipment sold into major consumer markets is shaped by product-safety rules, export controls, and customs and tariff administration. In the European Union, Regulation (EU) 2023/988 on general product safety creates broad safety obligations for consumer products placed on the market, supported by the European Commission updating harmonized standards via Commission Implementing Decision (EU) 2026/901 (adopted April 17, 2026). For accessory categories that overlap with photography workflows, photobiological safety requirements for LED lighting are also relevant; EN IEC 62471:2026 is referenced in 2026 enforcement updates for commercial LED lighting used in setups such as ring lights and backdrop lighting, which increases compliance attention around blue-light and exposure thresholds.

Trade and technology controls add further constraints for higher-end and specialized camera systems. In the United States, the Department of Commerce Bureau of Industry and Security revised Export Administration Regulations licensing requirements for certain cameras, systems, or related components (Federal Register action dated February 2024), which can affect cross-border availability of advanced imaging hardware. Import treatment and tariff exposure still depend on product classification and enforcement through the Harmonized Tariff Schedule (USITC) and U.S. Customs and Border Protection processes, which becomes a material issue for vendors and retailers managing price points in tariff-sensitive segments.

Competitive Landscape

The Photography Equipment Market is moderately concentrated, with players like Canon, Sony, and Nikon collectively accounting for a major market share from interchangeable-lens cameras. Despite this dominance, competition remains intense as each brand leverages its technological strengths. Canon leads the professional segment with its flagship EOS R1 and an ecosystem of over 40 RF lenses. Its dual-gain-output sensor architecture provides 13 stops of dynamic range at ISO 3200, enabling wedding and event photographers to handle mixed lighting without bracketing exposures. Sony, a pioneer in mirrorless technology with its Alpha 1 and Alpha 7R V models, benefits from vertical integration. With a 53% share of the global CMOS sensor market through Sony Semiconductor, the company reserves its most advanced stacked sensors for its own cameras, creating a significant performance advantage. Nikon, in April 2024, acquired RED Digital Cinema, signaling its entry into the professional cinema camera market. By combining its Z-mount optics with RED's REDCODE RAW compression and color science, Nikon aims to compete with Sony's FX6 and Canon's Cinema EOS series. Fujifilm, on the other hand, occupies a niche with its X-series APS-C and GFX medium-format cameras, appealing to street and commercial photographers through film-simulation modes like Velvia, Provia, and Acros, which replicate analog color science for in-camera aesthetics.

White-space opportunities exist in the rental and subscription models, which remain underdeveloped outside North America and Europe, and in the action-camera segment. DJI's Osmo Action 5 Pro has gained market share from GoPro by offering superior low-light performance and variable-aperture sensors. Meanwhile, Chinese sensor manufacturers such as OmniVision and Will Semiconductor are disrupting the market by eroding Sony's 53% CMOS market share. These companies provide lower-cost alternatives, appealing to camera manufacturers looking to reduce bill-of-material costs. AI-powered computational workflows have emerged as a critical battleground for market-share gains. Canon's Deep Learning AF, Sony's AI-based Real-time Recognition AF, and Nikon's 3D-tracking algorithm highlight the growing importance of autofocus speed and accuracy over megapixel count in influencing purchase decisions among professional and prosumer buyers.

The long-term competitive landscape will favor companies that integrate AI processing units directly into camera bodies. This integration enables real-time features such as subject recognition, noise reduction, and horizon leveling, reducing reliance on post-production software. These advancements are particularly advantageous for event photographers and photojournalists who operate under tight deadlines, as they shorten the time from capture to delivery. As the market evolves, players that can deliver these AI-driven capabilities will gain a significant edge, meeting the growing demand for faster and more efficient workflows in professional photography.

Photography Equipment Industry Leaders

Canon Inc.

Nikon Corporation

Fujifilm Holdings Corp.

Panasonic Holdings Corp.

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is monetizing the market shift from entry-level ownership toward higher-value creator and professional workflows by packaging capability upgrades into camera bodies and lenses that reduce production time. The direction is visible in recent 2026 launches, where Canon introduced the EOS R6 V alongside the RF20-50mm F4 L IS USM PZ power-zoom lens (May 2026), and Sony introduced the Alpha 7R VI with a high-resolution sensor and updated processing (May 2026). These releases track the report context of demand concentrating around mirrorless systems optimized for vlogging and advanced video, where AI autofocus, stabilization, and integrated computational workflows support premium ASPs.

Another whitespace centers on expanding access models and channel strategies around specialty and online demand signals. Online accounted for 55.82% of 2025 turnover in the report context, and rentals and subscriptions are already being used by specialty retailers and brands to reduce upfront barriers for premium kits. The shipment mix also supports targeted portfolio planning, with CIPA-reported 2025 digital camera shipments reaching 9,438,876 units (+11.2% YoY), interchangeable-lens cameras at 74.18% of shipments, and mirrorless at 90.13% of interchangeable-lens volume. In parallel, built-in lens (compact) shipments grew 29.6% in 2025, reinforcing room for premium compacts and compact creator kits where availability and assortment have been constrained for certain models.

Recent Industry Developments

- July 2026: Sony announced the RX10 V, the fifth generation of its all-in-one super zoom camera line, continuing the 24-600mm class positioning for travel, wildlife, and sports. The update maintains a differentiated bridge-camera option in a market where smartphones pressure entry-level dedicated cameras and where vendors defend margins through specialized form factors.

- December 2025: Sony launched the Alpha 7 V and the FE 28-70mm f/3.5-5.6 OSS II lens. The release broadened Sony's full-frame mirrorless line and supported system attach rates by pairing a new body with an updated standard zoom for mainstream full-frame buyers.

- July 2024: Canon launched the EOS R5 Mark II full-frame mirrorless camera, positioned around high-resolution hybrid capture with in-body stabilization and 8K video capabilities. It reinforced Canon's focus on professional and creator workloads, where advanced autofocus and video features support sustained premium pricing and lens ecosystem pull-through.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue generated from the sale of photography equipment used to capture still and video images, counted at the point of equipment sale. Under this scope, the focus stays on dedicated devices used for photography and video creation across major global regions.

Scope exclusions: We exclude smartphone handsets, standalone editing software, printing services, and general consumer electronics that are not primarily sold as photography equipment.

Segmentation Overview

- Product Type

- Cameras

- Cam Corder

- Category

- Mass

- Premium

- End User

- Professional

- Personal

- Distribution Channel

- Online Channel

- Offline Channel

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Peru

- Colombia

- Chile

- Rest of South America

- Middle East and Africa

- South Africa

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on camera and related device demand, pricing direction, and channel shifts before any calculations are locked. We rely on public sources such as national statistics offices for electronics output and trade, UN Comtrade for import and export trends, World Bank macro indicators, and USITC-style tariff schedules to understand price pressure and supply movement.

To keep the sizing practical, we also review sources like company annual reports and investor decks, product launch notes, and association websites relevant to imaging and consumer electronics. A paid subscription for company financials and intelligence is used selectively to normalize reported revenue lines across regions and to separate imaging-related sales from adjacent electronics. Patent databases are also used to check feature-cycle timing that affects replacement demand. These examples are illustrative, and other public sources were also referred to for data collection, validation, and clarification during research.

Primary Interviews and Surveys

Primary work is used to stress test the desk assumptions on replacement cycles, average selling price movement, and channel mix, then to narrow any gaps left by public data. We speak with manufacturers, distributors, retailers, and photography professionals across APAC, EMEA, and the Americas so the model captures both supply behavior and buyer adoption patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 40% |

| Mid tier: 43% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 22% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing is built using a top-down approach where global and regional demand pools are reconstructed from category level shipment direction, trade flows, and price realization patterns, and then mapped back to equipment revenue. The totals are then corroborated with selective bottom-up checks, such as sampled camera and camcorder price points multiplied by observed unit movement across key channels, followed by adjustments when the checks indicate an over or under count.

Inputs that matter in this market include camera and camcorder shipment trends, the mirrorless shift versus DSLR decline, replacement cycle timing for pros and enthusiasts, online versus offline mix, and average selling price movement tied to feature upgrades like autofocus and stabilization. Where unit visibility is weaker for smaller geographies, gap handling uses proxy indicators like import intensity, income bands, and retailer assortment depth, and then is aligned back to the regional total so the rollup stays consistent.

For forecasting, we use scenario analysis with a light multivariate regression layer on the stable drivers, including disposable income and consumer electronics spend indicators, and then apply expert-led adjustments for category-specific events like product refresh timing and creator economy demand swings. The final forecast is reviewed to ensure it remains consistent with the slow-growth nature of dedicated equipment and the pace of substitution from smartphones at the entry level.

Data Validation & Update Cycle

Validation is done by comparing the model output against independent signals like trade values, publicly discussed shipment direction, and the implied price per unit movement, which helps catch sudden jumps that do not fit real buying behavior. When variances are found, we revisit the assumptions, re-check the arithmetic, and in some cases reconnect with interviewees to confirm what changed in channel discounts, mix, or product availability.

Before sign-off, the work goes through multi-step analyst reviews where key inputs, conversion logic, and region splits are checked again, and any outliers are documented with a clear reason. Reports are refreshed annually, and interim updates are triggered when material events occur, such as tariff changes, large supply disruptions, or major category shifts. Right before delivery, a fresh pass is done so clients receive the most current view available.

Mordor Intelligence's Photography Equipment Market Size Measured Against Other Published Estimates

Published market sizes for photography equipment can look inconsistent because each source chooses its own product boundary, base year, and pricing logic. Differences also come from how quickly assumptions are refreshed when demand shifts between dedicated cameras and adjacent imaging products.

The gap usually traces back to what is counted as photography equipment, how lenses and accessories are treated, and whether the estimate leans on shipments, retail sell-through, or company revenue mapping. Currency timing and the way average selling prices are stepped forward also matter, since premium mirrorless models can lift value even when units are flat.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.74 B (2026) | |

| Global Consultancy A | USD 9.90 B (2026) | Uses a wider product basket that explicitly includes lenses, lighting, and tripods, which can lift the value even if the camera body market is steady. |

| Industry Publisher B | USD 9.52 B (2025) | Anchored on a different base year and product grouping, and may treat category transition effects (such as mirrorless mix) with a slower ASP update, which can keep the value lower. |

The table shows a tight spread around the mid to high single-digit billions, and the main separation is what gets counted as equipment versus adjacent add-ons. In Mordor Intelligence's model, the value is centered on cameras and camcorders, which avoids blending in accessory-heavy categories that can move differently by channel and promotion. With those scope choices kept clear and then checked against trade and pricing signals, the final number stays easier to reproduce and explain when buyers compare it across regions and years.

Key Questions Answered in the Report

How big is the photography equipment market?

The photography equipment market size is expected to grow from USD 9.72 billion in 2025 to USD 9.74 billion in 2026 and is forecast to reach USD 9.91 billion by 2031 at 0.35% CAGR over 2026-2031.

Which region is growing fastest for photography gear sales?

Asia-Pacific shows the strongest momentum, projected to expand at a 1.12% CAGR through 2031 on the back of surging creator demand in China and India.

What product category holds the largest revenue share?

Cameras dominate with 83.96% of 2025 sales, supported by ongoing mirrorless innovation.

Why are premium bodies gaining traction?

Professionals and advanced amateurs seek AI autofocus, in-body stabilization, and robust weather sealing, lifting the premium tier to 42.82% of 2025 revenue.

Which companies lead the competitive landscape?

Canon, Sony, and Nikon collectively control roughly 70% of global interchangeable-lens camera revenue, while Fujifilm, Panasonic, and DJI lead niche segments.

Page last updated on: