Fish Hunting Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

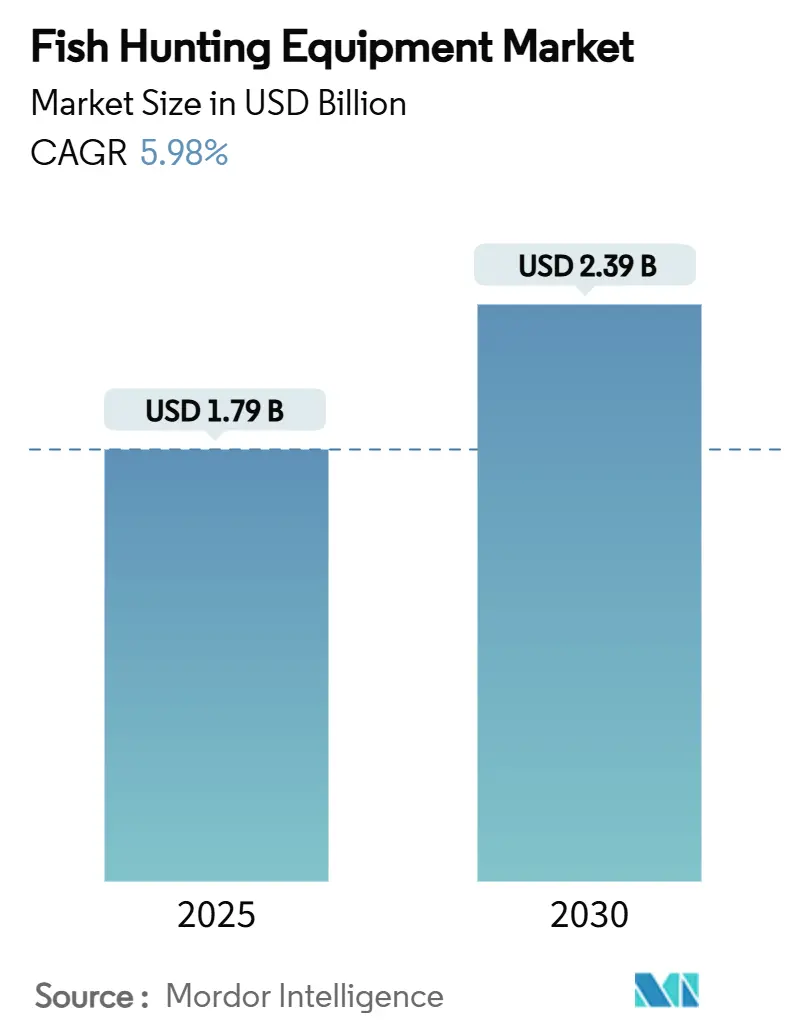

| Market Size (2025) | USD 1.79 Billion |

| Market Size (2030) | USD 2.39 Billion |

| Growth Rate (2025 - 2030) | 5.98% CAGR |

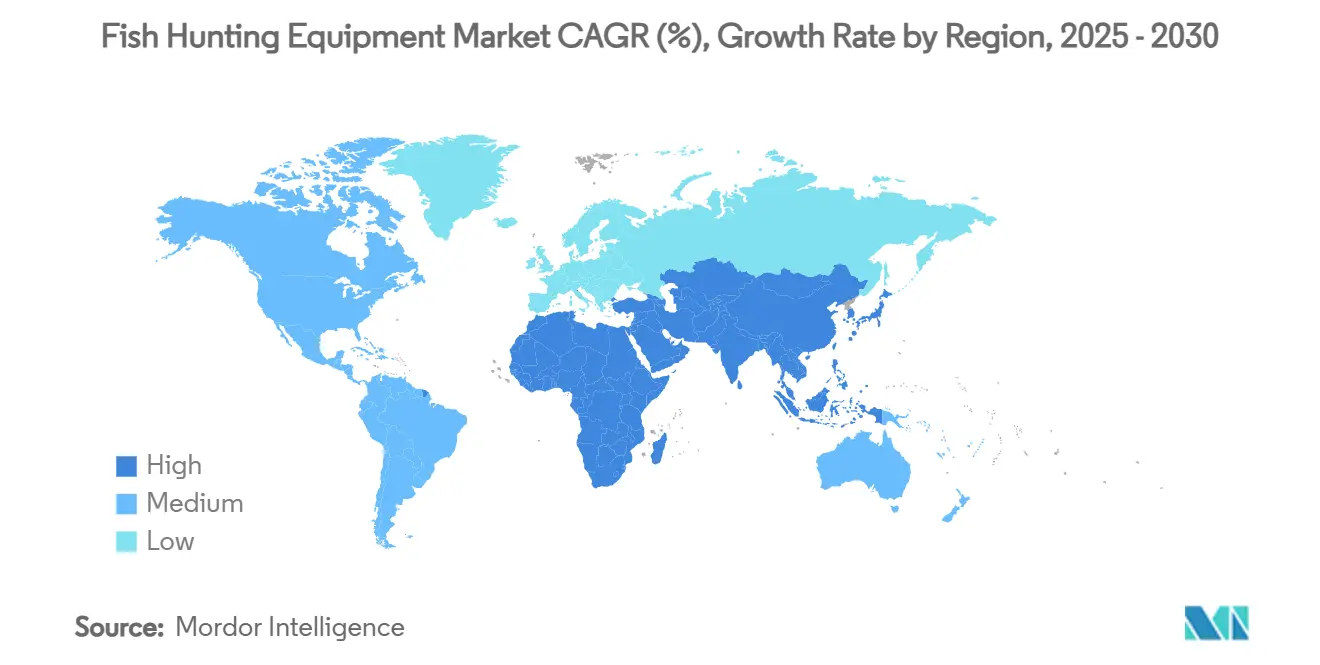

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fish Hunting Equipment Market Analysis by Mordor Intelligence

The fish hunting equipment market size stands at USD 1.79 billion in 2025 and is forecast to climb to USD 2.39 billion by 2030, advancing at a 5.98% CAGR over the period. Driven by robust participation trends, rising disposable incomes, and continuous product innovation, the expansion of the angling market is evident. Upgrades to products, especially those integrating smart electronics, are not only appealing to a broader demographic of anglers but are also diversifying revenue streams. While North America, with its deep-rooted angling culture and established retail infrastructure, maintains its leadership, the Asia-Pacific region is witnessing the most significant incremental gains. Here, urban consumers are increasingly allocating their growing leisure budgets to outdoor recreation. The rise of digital commerce is transforming purchasing behaviors, with online platforms outpacing physical stores in growth. However, industry players face challenges, contending with fluctuations in raw material prices and stricter sustainability regulations. These pressures are hastening the shift towards eco-certified designs, even as they strain profit margins.

Key Report Takeaways

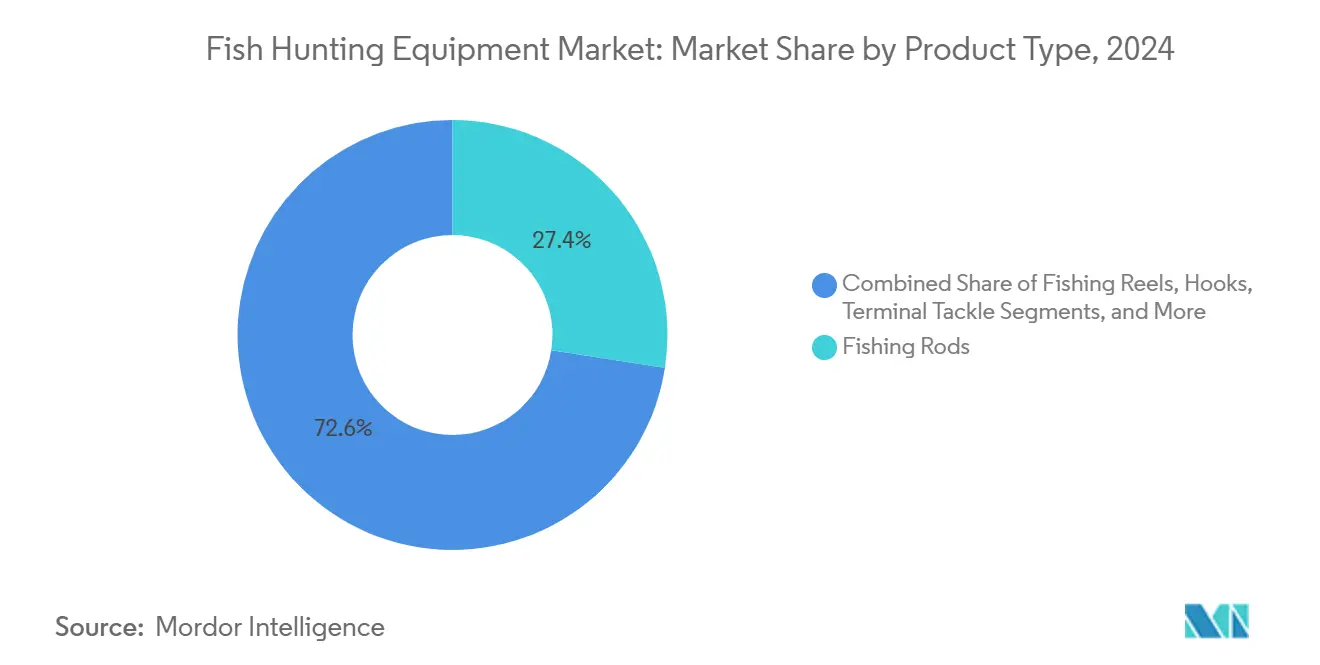

- By product type, Smart Electronic Devices recorded the quickest trajectory at a 10.28% CAGR between 2025 and 2030, while Fishing Rods retained the largest 27.44% share of the Fish Hunting Equipment market size in 2024.

- By end user, Recreational/Leisure Fishing led with 61.23% of the Fish Hunting Equipment market share in 2024; Professional Sport Fishing is projected to move ahead at a brisk 7.25% CAGR through 2030.

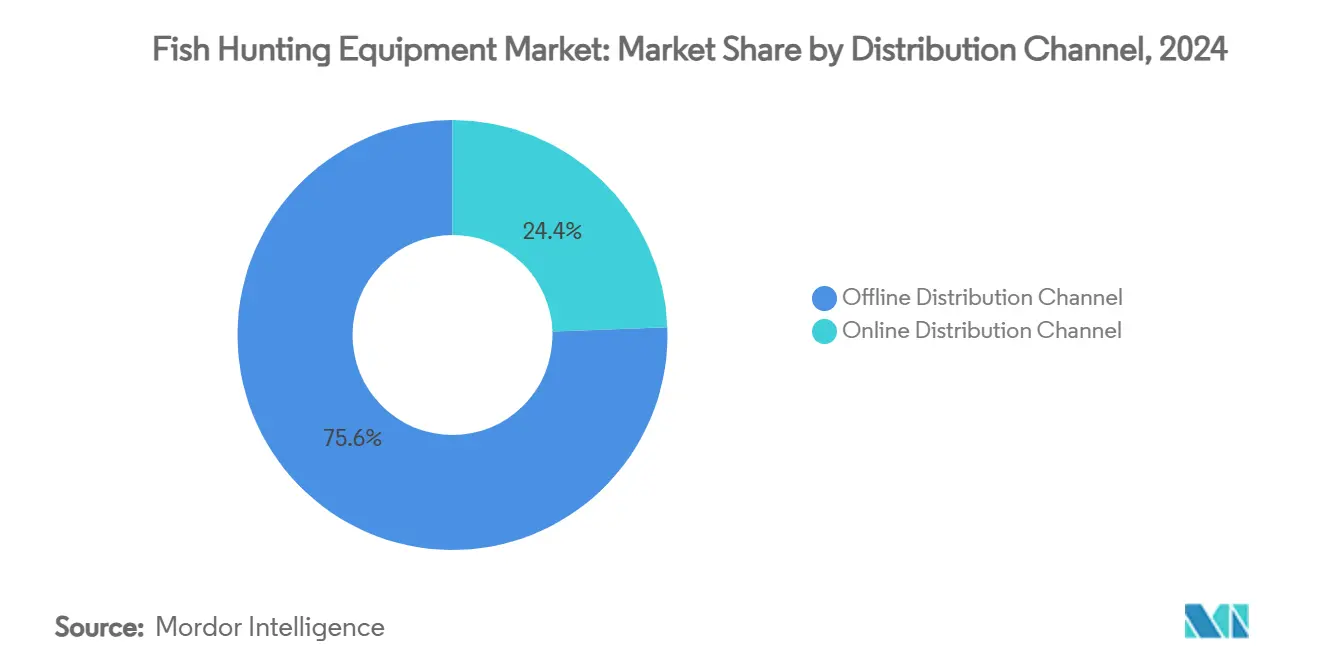

- By distribution channel, the Offline segment accounted for 75.57% of revenues in 2024, whereas Online platforms are forecast to expand at a 9.36% CAGR to 2030.

- By geography, North America accounted for 34.18% of the Fish Hunting Equipment market share in 2024. Asia-Pacific is forecast to register the quickest expansion with a 7.13% CAGR through 2030.

Global Fish Hunting Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing participation in recreational angling | +1.8% | Global, strongest in North America and APAC | Medium term (2-4 years) |

| Technological advances in smart fish-finders and sonar | +2.2% | North America and EU leading, expanding to APAC | Long term (≥ 4 years) |

| Product customization and high-performance materials | +1.5% | Global, premium markets in developed regions | Medium term (2-4 years) |

| Growth of outdoor and adventure tourism | +0.8% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Community networks and social influences | +0.5% | Global, accelerated by digital platforms | Short term (≤ 2 years) |

| Eco-certified gear commanding premium pricing | +0.7% | North America and EU primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Participation in Recreational Angling

Recreational fishing is witnessing a notable uptick in participation, signaling a shift in outdoor recreation trends, largely fueled by a diversifying demographic. In 2023, female anglers numbered 21.3 million, and Hispanic American participation has seen a near doubling in the last decade, leading to the emergence of new consumer segments with unique equipment preferences, as highlighted by Tackle Trade World[1]Source: Recreational Boating & Fishing Foundation, “Record Numbers of People Go Fishing in the USA,” tackletradeworld.com. Furthermore, 2023 saw 4.2 million Americans casting their lines for the first time, underscoring a robust growth pipeline for equipment manufacturers. This trend, bolstered by a pandemic-induced emphasis on wellness and nature-centric activities, is gaining traction. According to NOAA Fisheries, recreational fishing accounted for 201 million trips in 2022, translating to a USD 73.8 billion economic impact and supporting 487,000 jobs nationwide[2]Source: NOAA Fisheries, “Recreational Fishing,” fisheries.noaa.gov. As participation swells, there's a consistent demand for entry-level equipment, but as novices hone their skills, there's a noticeable shift towards premium, specialized gear.

Technological Advances in Smart Fish-Finders and Sonar

Smart electronic devices are reshaping fishing equipment by integrating artificial intelligence, GPS mapping, and real-time data analytics, significantly boosting angling success rates. Today's fish-finders blend sonar technology with smartphone connectivity, enabling anglers to share data and tap into crowd-sourced fishing insights via cloud platforms. The segment's impressive 10.28% CAGR highlights the swift adoption of technologies, once reserved for commercial fishing, now democratized for recreational users thanks to miniaturization and cost-efficiency. Patent activity in sonar and fish-finding tech has surged, with firms crafting proprietary algorithms for fish identification and underwater terrain mapping. These advancements go beyond conventional sonar, incorporating underwater cameras, temperature sensors, and water quality monitors into unified device ecosystems. This technological convergence paves the way for subscription services and data monetization, shifting equipment sales from one-off transactions to a model of recurring revenue.

Product Customization and High-Performance Materials

Manufacturers are increasingly turning to advanced materials engineering, utilizing carbon-fiber composites, titanium alloys, and nano-coatings to boost equipment performance and longevity. Anglers now have the ability to customize their gear, from rod actions and reel gear ratios to lure configurations, tailored to specific fishing conditions and target species. This level of personalization commands a price premium of 25-40% over standard offerings. Such trends underscore a broader consumer shift towards personalized products and a preference for professional-grade equipment, especially among dedicated recreational anglers. Innovations in manufacturing, particularly modular designs and 3D printing technologies, are facilitating mass customization, slashing lead times without compromising on quality. Furthermore, high-performance materials are meeting environmental durability standards; for instance, saltwater-resistant coatings and corrosion-proof components are significantly prolonging equipment lifespan, even in challenging conditions. This trend of customization not only offers manufacturers a chance to stand out in a competitive market but also fosters customer loyalty through tailored product experiences.

Growth of Outdoor and Adventure Tourism

As adventure tourism expands, the demand for fishing equipment surges, fueled by destination fishing experiences and guided angling services that rely on specialized gear tailored for diverse environments. International fishing tourism not only drives substantial equipment sales but also sees travelers purchasing location-specific gear and upgrading their equipment to tackle the challenges of exotic destinations. This trend is further amplified by social media, where shared fishing adventures online not only inspire equipment purchases but also entice followers to travel to those destinations. According to the Australian Government Department of Agriculture, outdoor recreation, with fishing tourism at its helm, plays a pivotal role in bolstering regional economies, supporting local equipment retailers and guiding services[3]Source: Australian Government Department of Agriculture, “Recreational Fishing,” agriculture.gov.au. Given the need for versatility and portability in destination fishing, there's a growing demand for multi-purpose gear and travel-friendly designs that excel in varied fishing environments. This intertwining of tourism and fishing also paves the way for equipment rental services and curated destination-specific gear packages, alleviating travel burdens while ensuring the right equipment is always at hand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter catch quotas and fishing-license regulations | -0.5% | Global, with varying regional intensity | Medium term (2-4 years) |

| Volatile carbon-fiber and alloy input costs | -0.3% | Global manufacturing, premium segment impact | Short term (≤ 2 years) |

| Stringent environmental regulations and compliance | -0.4% | EU and North America leading, expanding globally | Long term (≥ 4 years) |

| Seasonality and weather dependency | -0.3% | Regional variations, temperate climate zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Catch Quotas and Fishing-License Regulations

Regulatory tightening across major fishing jurisdictions is constraining market growth. These regulations are reducing fishing opportunities and increasing compliance costs, which in turn discourage participation. The European Union's 2025 fishing regulations have set reduced total allowable catches for several species. Notably, the European Commission has significantly cut Baltic Sea cod quotas due to concerns over low biomass[4]Source: European Commission, “Fishing Opportunities in the Baltic Sea 2025,” eur-lex.europa.eu. In Massachusetts, the Division of Marine Fisheries reports that 2025 will see substantial quota reductions, with Atlantic herring quotas hitting their lowest levels ever. This directly jeopardizes commercial fishing viability and diminishes demand for related equipment. Furthermore, rising license fees and intricate permitting processes pose challenges for new anglers and impose continuous costs on seasoned participants. To safeguard vulnerable species, recreational fishing is facing heightened restrictions, including seasonal closures and gear limitations. These measures not only curtail equipment utilization but also diminish the frequency of purchases. While this regulatory trend underscores global conservation priorities, it casts a shadow of uncertainty over equipment manufacturers, raising questions about the sustainability of long-term demand.

Volatile Carbon-Fiber and Alloy Input Costs

Premium fishing equipment manufacturers, reliant on advanced composites and specialized alloys, grapple with margin pressures and pricing uncertainties due to material cost volatility. Prices of carbon fiber, swayed by demand cycles in the aerospace and automotive sectors, disrupt supply chains and impact the production schedules of fishing rods and reels. Johnson Outdoors, in recent quarters, highlighted margin compression, attributing it to unfavorable overhead absorption and heightened promotional pricing pressures, mirroring broader industry challenges. Costs of titanium and specialized alloys exhibit similar fluctuations, notably impacting high-end reel components and hardware applications, where the material's performance commands a premium price. Manufacturers are caught in a dilemma: absorb rising costs to safeguard market share or transfer these costs to consumers, who might delay purchases or opt for cheaper alternatives. While supply chain diversification and long-term material contracts offer some relief, smaller fishing equipment manufacturers find themselves at a disadvantage, lacking the negotiating clout of their larger industrial counterparts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Electronics Drive Innovation

Smart Electronic Devices are set to grow at a brisk pace of 10.28% CAGR through 2030. In contrast, Fishing Rods, while leading the market with a 27.44% share in 2024, are witnessing a more tempered growth. The electronics segment is riding the wave of rapid technological advancements, seamlessly integrating features that revolutionize traditional fishing methods. These innovations harness real-time data analytics and connectivity, enhancing the angling experience. Fishing Reels, a staple in the market, enjoy steady demand, buoyed by regular replacement cycles and performance upgrades. Meanwhile, Hooks and Terminal Tackle are on a consistent upward trajectory, thanks to their consumable nature and ongoing innovations in materials and designs. Fishing Lines, leveraging advanced polymer technologies, are witnessing moderate growth, especially with specialized applications tailored for diverse fishing conditions and target species.

Lures and Baits are holding their ground, driven by relentless product innovation and seasonal demand patterns that prompt regular purchases among dedicated anglers. Nets and Traps cater to both commercial and recreational segments, with their growth closely linked to regulatory compliance and enhanced efficiency in fishing operations. Accessories, ranging from apparel to coolers and bags, are capitalizing on lifestyle branding. These items are not just limited to fishing but are expanding into the broader outdoor recreation realm, thanks to cross-selling opportunities. This diverse segment landscape empowers manufacturers, offering them multiple revenue streams and a buffer against fluctuating demand cycles and varied consumer preferences across different fishing applications and skill levels.

By End User: Recreational Dominance with Professional Growth

In 2024, Recreational/Leisure Fishing commands a dominant 61.23% market share, buoyed by record participation levels and a demographic expansion fueling equipment demand across all price tiers. This segment reaps benefits from social media trends and a growing outdoor lifestyle, prompting enthusiasts to upgrade their gear and make specialized purchases tailored to diverse fishing environments and techniques. Meanwhile, Professional Sport Fishing is the fastest-growing segment, boasting a 7.25% CAGR. Its growth is spurred by rising tournament participation and lucrative sponsorships, leading to heightened demand for high-performance gear and state-of-the-art technology. This segment not only commands premium pricing but also spearheads innovation, which subsequently permeates the recreational market.

Commercial Fishing stands as a stable yet mature segment. Here, equipment demand hinges more on fleet modernization and regulatory compliance than on participation growth. Prioritizing durability and operational efficiency over consumer-centric features, this segment carves out unique product development and distribution pathways. Professional anglers, through endorsements and showcasing advanced techniques, shape recreational equipment choices. Their influence cultivates an aspirational demand, propelling premiumization trends in the broader market. The end-user segmentation underscores varied value propositions and purchasing behaviors, necessitating bespoke marketing strategies and product development approaches.

By Distribution Channel: Digital Transformation Accelerates

Online distribution channels are projected to grow at a 9.36% CAGR through 2030. In contrast, offline channels are set to dominate with a 75.57% share in 2024. This trend underscores the ongoing digital transformation in the retail of fishing equipment. A broader product selection, competitive pricing, and the convenience of shopping fuel E-commerce's ascent. These factors resonate with consumers pressed for time, especially those in search of specialized equipment often absent from local stores. Online platforms not only facilitate direct-to-consumer sales, enhancing manufacturer margins, but also offer detailed product information and customer reviews, aiding informed purchasing decisions. Furthermore, digital channels champion subscription services for consumables like lures and lines, fostering recurring revenue streams.

Conversely, traditional retail holds its ground with advantages like product demonstrations, immediate availability, and expert advice. These elements prove invaluable, especially for complex equipment purchases and first-time buyers in need of guidance. Hybrid retail models, which meld online ordering with in-store pickups or demonstrations, are emerging as the gold standard. They promise an optimal customer experience while deftly managing inventory costs and logistical challenges. This evolving landscape presents a unique opportunity for specialized fishing equipment retailers. By emphasizing expertise and service, they can carve out a niche, even amidst competition from general sporting goods chains and vast online marketplaces. For manufacturers, honing a distribution channel strategy is paramount. It's a key lever in optimizing reach and profitability, catering to a diverse array of customer segments and geographic markets.

Geography Analysis

In 2024, North America commands a robust 34.18% share of the fishing revenue landscape, underscoring its established yet vibrant ecosystem of anglers, waterways, and specialized retail. According to NOAA Fisheries, the U.S. alone recorded 201 million fishing outings, translating to a significant USD 73.8 billion economic impact. This not only underscores the industry's heft but also fuels innovation in fishing equipment. Meanwhile, Canada capitalizes on its pristine wilderness, drawing in eco-tourists and boosting sales of cold-water gear and fly-fishing outfits. Mexico's coastal charters maintain a steady demand for saltwater rods, braided lines, and offshore electronics. However, with tightening catch quotas and habitat concerns, there's a shift: manufacturers are increasingly gravitating towards low-impact materials and designs, aligning with a growing conservation ethos.

Asia-Pacific is on a rapid ascent, boasting the highest growth rate at a 7.13% CAGR. As urbanization surges and middle-class incomes rise, discretionary spending on leisure activities sees fishing emerge as a favored, affordable escape. China's e-commerce platforms are breaking barriers, granting access to premium international brands, while domestic factories are elevating quality, bridging the perception gap. In India, state-led angling festivals and reservoir stocking programs are not only cultivating participation but also boosting downstream equipment sales. Australia presents a unique blend of maturity and innovation: one in five adults engage in recreational fishing, and there's a swift adoption of blue-water electronics. The region's diverse habitats demand localized SKUs, leading to the emergence of micro-segments within the expansive Fish Hunting Equipment market.

Europe finds itself at the crossroads of tradition and modern regulation. In response to stringent environmental directives, there's a noticeable shift towards biodegradable baits and lead-free weights. Suppliers who can swiftly certify compliance, as per the European Environment Agency, stand to gain a significant early-mover advantage. While quota reductions in the Baltic and Mediterranean seas tighten commercial volumes, they haven't immediately dampened recreational participation, which often leans towards catch-and-release practices. Meanwhile, South America and the Middle East & Africa, though still in their infancy, show immense promise. Brazil's Amazon basin and Argentina's Patagonia beckon adventure seekers, and Gulf states are pouring investments into marina infrastructure, setting the stage for a burgeoning sport-fishing tourism. Yet, challenges like political stability, customs duties, and infrastructure gaps loom large. However, as these barriers diminish, they pave the way for deeper penetration into the Fish Hunting Equipment market.

Competitive Landscape

Competition remains moderate, with no single player dominating the landscape. Leading the charge are Shimano, Pure Fishing, Globeride, Inc, Rapala VMC, and Johnson Outdoors, each bolstering their position through robust R&D, expansive distribution, and strong brand equity. Shimano's flagship reel technologies seamlessly transition to its mainstream series, allowing it to dominate both premium and entry-level markets. Pure Fishing employs a savvy multi-brand strategy, using Abu Garcia for reels and Berkley for baits, to cater to diverse price points and angler tastes. Meanwhile, Daiwa innovates with carbon-fiber blanks and optimizes global logistics to manage costs.

Despite a Q1 2025 fishing revenue dip to USD 107.6 million, Johnson Outdoors swiftly adapted, tightening cost controls and boosting digital engagement, leading to a rebound in Q2 profitability at USD 9.5 million. Rapala VMC, leveraging its proprietary hook technology and strategic distribution deals, is expanding its European dominance into North America. New entrants, often rooted in digital, are aggressively pursuing market share through direct-to-consumer strategies, bypassing traditional dealer margins. Their adeptness at leveraging social media for visibility presents a swift route to market, albeit with significant investment for scalability.

Technology collaborations are gaining traction, with electronics behemoths teaming up with tackle manufacturers. Together, they're embedding sonar chips into rod butts and reel seats, crafting cohesive ecosystems and ensuring recurring revenue through firmware updates. Sustainability is emerging as a competitive edge; brands adopting recyclable nylon nets and bio-based plastics are reaping rewards in eco-aware markets. The surge in patents, particularly in sensor fusion and AI-driven fish detection, underscores a burgeoning technological race within the Fish Hunting Equipment sector.

Fish Hunting Equipment Industry Leaders

Shimano Inc.

Pure Fishing

Globeride, Inc

Johnson Outdoors

Rapala VMC Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Shimano unveiled nine new offshore fishing rods, featuring the OCEA Blade, OCEA Jigger Infinity Motive, Game Type J Full Bend, Soare Limited, Sephia SS Tip Eging, Coltsniper Limited Big Game, Nessa SS, and Dialuna models.

- January 2024: Kerfil introduced a diverse lineup of products spanning reels, rods, lures, and various accessories. Their new range features 8 rods tailored for sea fishing, accommodating weights from 3.5 to 200 g, catering to needs from delicate scraping to robust vertical fishing.

- March 2023: Okuma has unveiled its latest innovation: a high-end bass fishing rod. Melding state-of-the-art technology with top-tier performance, the X-Series Bass Rods cater to the exacting standards of dedicated anglers. These rods promise to redefine the bass fishing landscape.

Global Fish Hunting Equipment Market Report Scope

| Fishing Rods |

| Fishing Reels |

| Hooks and Terminal Tackle |

| Fishing Lines |

| Lures and Baits |

| Nets and Traps |

| Accessories (apparel, coolers, bags, etc.) |

| Smart Electronic Devices |

| Others |

| Commercial Fishing |

| Recreational/Leisure Fishing |

| Professional Sport Fishing |

| Offline Distribution Channel |

| Online Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Fishing Rods | |

| Fishing Reels | ||

| Hooks and Terminal Tackle | ||

| Fishing Lines | ||

| Lures and Baits | ||

| Nets and Traps | ||

| Accessories (apparel, coolers, bags, etc.) | ||

| Smart Electronic Devices | ||

| Others | ||

| By End User | Commercial Fishing | |

| Recreational/Leisure Fishing | ||

| Professional Sport Fishing | ||

| By Distribution Channel | Offline Distribution Channel | |

| Online Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Fish Hunting Equipment sector in 2025?

Sales total USD 1.79 billion in 2025 and are forecast to climb to USD 2.39 billion by 2030 at a 5.98% CAGR.

Which product category is expanding the fastest?

Smart Electronic Devices, such as wireless sonar and GPS-linked fish-finders, are advancing at a 10.28% CAGR.

Which region presents the highest near-term growth?

Asia-Pacific is set to outpace other regions with a 7.13% CAGR, driven by rising disposable incomes and booming outdoor tourism.

What share does Recreational Fishing command?

Recreational and leisure anglers generated 61.23% of 2024 revenues, making it the dominant end-user segment.

Page last updated on: