Ornamental Fish Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

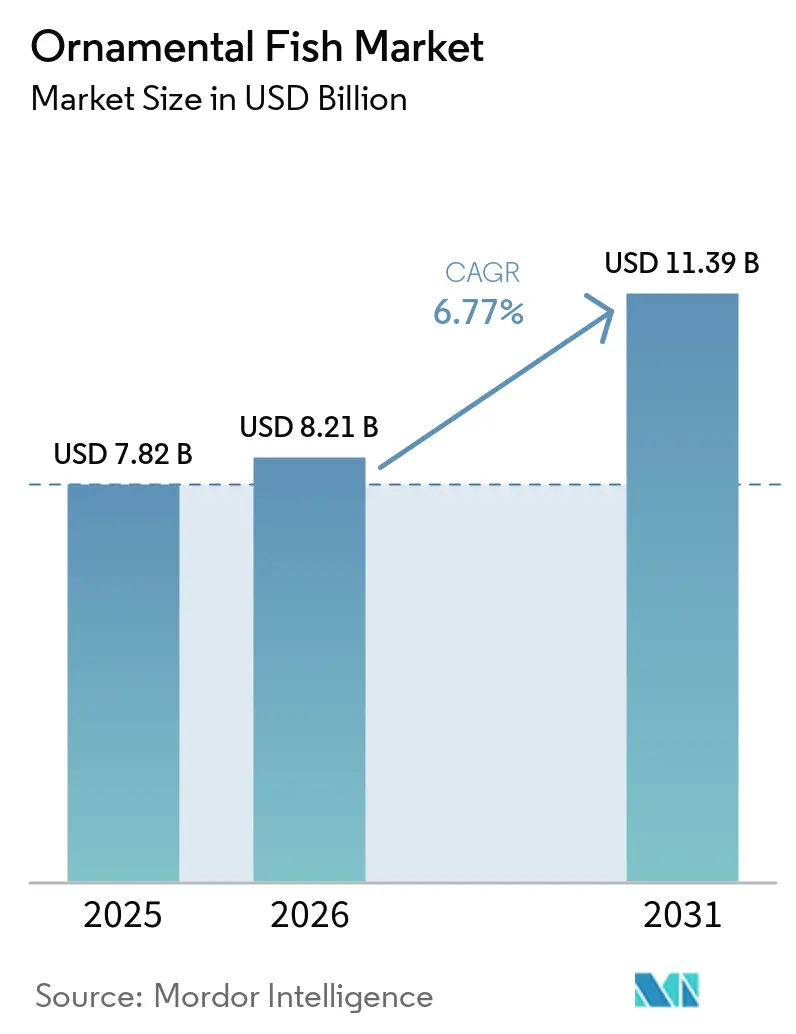

| Market Size (2026) | USD 8.21 Billion |

| Market Size (2031) | USD 11.39 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ornamental Fish Market Analysis by Mordor Intelligence

The global ornamental fish market was valued at USD 7.82 billion in 2025 and stands at USD 8.21 billion in 2026, on a trajectory to reach USD 11.39 billion by 2031, registering a CAGR of 6.77%. Tropical freshwater fish continue to dominate demand due to their affordability, ease of maintenance, and broad availability through Southeast Asian breeding networks. Meanwhile, marine ornamental fish are gaining traction as advances in captive-breeding technologies improve the commercial availability of species previously reliant on wild capture. For instance, Biota Group announced stable commercial-scale production of captive-bred Blue Tangs in January 2025, highlighting the industry's shift toward sustainable aquaculture. Asia-Pacific remains the largest and fastest-growing regional market, supported by its dual role as a major production hub and expanding consumer base. Industry development is further reinforced by government initiatives, such as South Korea's Third Comprehensive Plan for the Ornamental Fish Industry, launched in 2026, which aims to expand the national market through AI- and IoT-enabled fishkeeping solutions. Supply-chain modernization is also strengthening market growth; Thailand Post partnered with the Thai Department of Fisheries to introduce international ornamental fish express shipping services in October 2025. Additionally, a landmark structural shift occurred in April 2026 when Phillips Pet Food & Supplies and Central Garden & Pet Company formed a joint venture, consolidating key live-fish distribution and aquarium product assets.

Key Report Takeaways

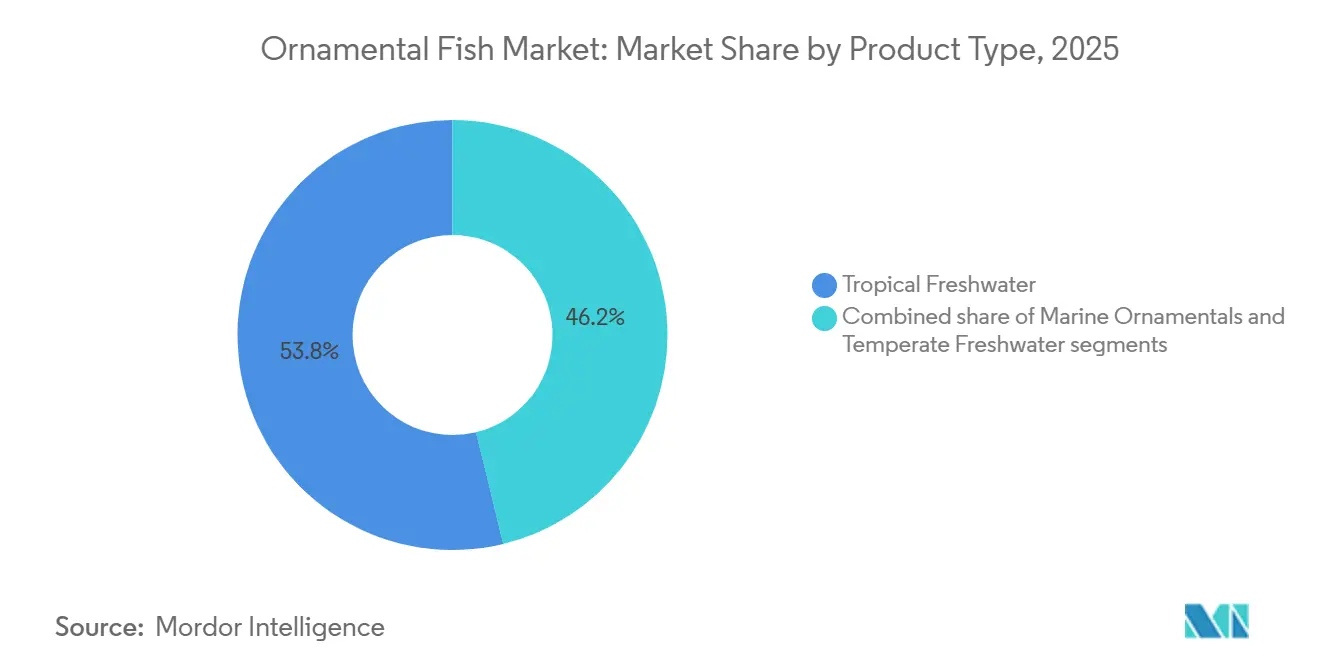

- By product type, Tropical Freshwater held 53.79% of revenue in 2025, while Marine Ornamentals are forecast to record the fastest 7.96% CAGR through 2031.

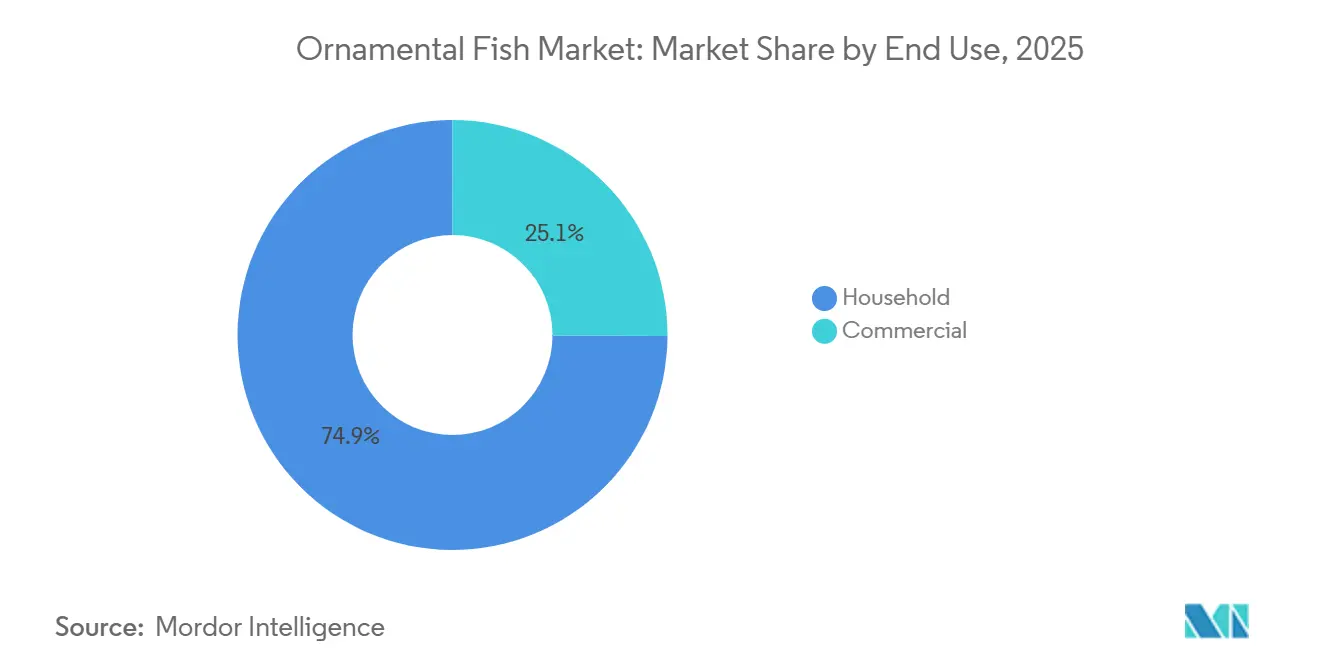

- By end use, Household accounted for 74.92% of revenue in 2025, while Commercial is projected to grow at the fastest 7.81% CAGR through 2031.

- By distribution channel, Specialty Aquatic Stores captured 53.13% of revenue in 2025, while Online Retail Stores are expected to advance at the fastest 8.01% CAGR through 2031.

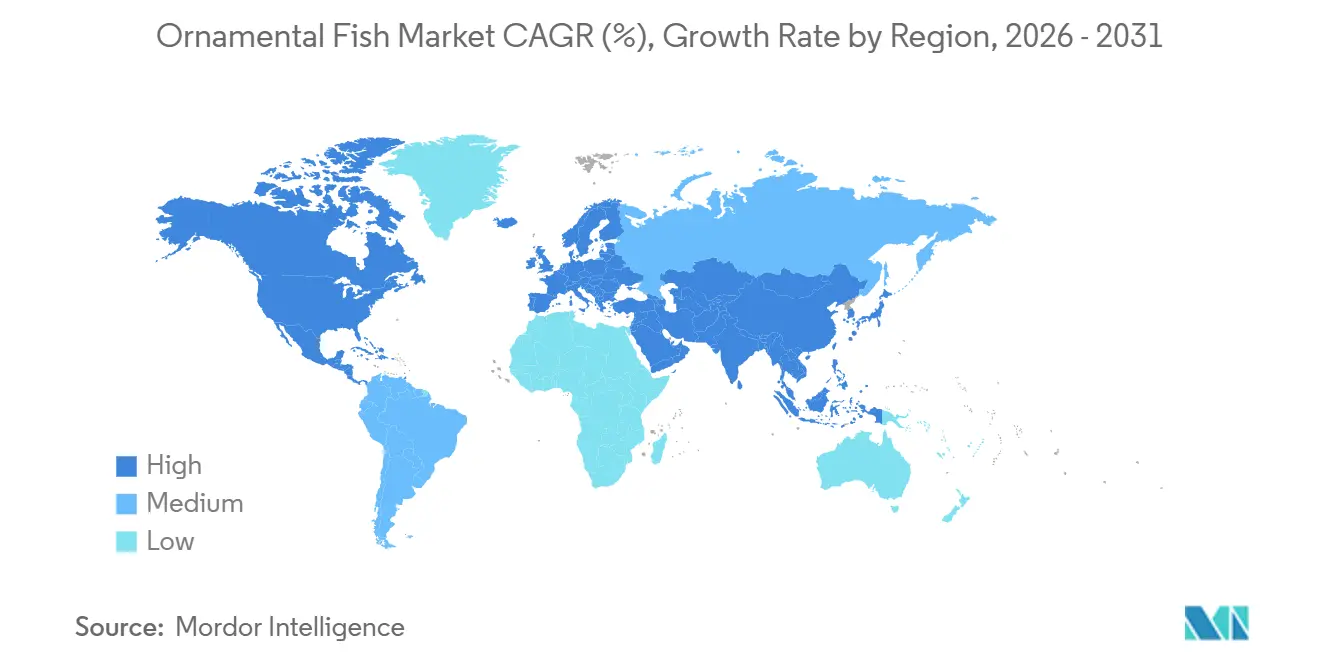

- By geography, Asia-Pacific represented 44.82% of revenue in 2025 and is also forecast to post the fastest 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ornamental Fish Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for low-maintenance aesthetic home aquariums | +1.8% | Global, concentrated in North America, Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Growth of quarantine-ready e-commerce fish fulfillment | +1.2% | North America, Europe, Asia-Pacific ; early adoption in South America | Short term (≤ 2 years) |

| Rising adoption of aquarium displays in hospitality and workplace design | +0.9% | Global, particularly GCC, Southeast Asia, North America | Medium term (2–4 years) |

| Improved captive-breeding and biosecurity reducing wild-capture dependence | +0.8% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Premiumization through rare, designer, and color-variant strains | +0.7% | North America, Europe, East Asia | Medium term (2–4 years) |

| Growing demand for traceable and certified ornamental fish supply | +0.5% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for low-maintenance aesthetic home aquariums

Aquarium keeping is evolving from a niche hobby into a mainstream home wellness trend, broadening its appeal to a wider audience. According to the American Pet Products Association's 2025 State of the Industry Report, Gen Z made up 20% of US pet-owning households in 2024, marking a significant 43.5% surge from the previous year[1]Source: American Pet Products Association, “2025 State of the Industry Report,” APPA, americanpetproducts.org. This generation views visual shareability on social media not just as an influence, but as a direct trigger for purchases. For established brands, this shift in demographics means that choices in species, packaging designs, and app-based support are now pivotal in driving conversions, alongside the traditional focus on product quality. Brands that overlook the platforms favored by younger consumers risk losing the upcoming decade's hobbyist market to more digitally savvy distributors. In response to this trend, Spectrum Brands introduced the GloFish Electric Green Angelfish at the Global Pet Expo in March 2025, ensuring its availability through major national retailers by August 2025, with a design emphasis on fluorescent colors tailored for social media appeal[2]Source: Spectrum Brands, “GloFish Electric Green Angelfish Launch,” Spectrum Brands, spectrumbrands.com.

Growth of quarantine-ready e-commerce fish fulfilment

Online retail is reshaping the ornamental fish supply chain, introducing a specialized logistics tier for live aquatic animals. This new tier mandates species-specific quarantine protocols, temperature-controlled packaging, and regulatory documentation, requirements that many traditional distributors have historically overlooked. Singapore-based exporters, in collaboration with FedEx, have set a precedent with a 48-hour delivery from Southeast Asian farms directly to US homes. They've achieved this with an average transit mortality rate of about 5% per shipment, a benchmark that's now setting global buyer expectations. This underscores a pivotal point: logistics capabilities are becoming a significant barrier to entry in the online retail space. Operators who can't guarantee live arrivals or source certified species find themselves sidelined from this rapidly expanding distribution channel. Furthermore, compliance with regulations, such as the US Lacey Act, CITES permits for certain species, and platform-specific restrictions on live animals, adds a layer of documentation complexity. This burden isn't evenly distributed across the supply chain. Meanwhile, Central Garden & Pet's Aqueon BlueIQ smart aquarium app, accessible on both iOS and Android, showcases the industry's evolution, enhancing digital customer engagement and integrating equipment functionalities well beyond the initial purchase.

Improved captive-breeding and biosecurity reduce wild-capture dependence

Breakthroughs in captive breeding are steadily closing the price gap between wild-caught and tank-bred marine specimens. This shift is allowing marine species, once the domain of specialist collectors, to flow into mainstream retail channels. In January 2025, Biota Group celebrated a milestone, announcing the stable commercial-scale production of captive-bred Pacific Blue Tangs after a dedicated five-year development program. Surge Marine Life followed suit in August 2025, unveiling the first commercially available captive-bred Rose Anthias (Odontanthias katayamai). This species, previously fetching between USD 17,000 and 20,000 in the wild, was introduced at a retail price of USD 5,999, underscoring aquaculture's potential to make ultra-premium marine life more accessible. In May 2025, De Jong Aquaculture, Europe's largest marine aquaculture hub located in the Netherlands, revealed its pioneering efforts[3]Source: De Jong Aquaculture, “Marine Ornamental Breeding Updates,” De Jong Aquaculture, dejongaquaculture.nl. They are employing IVF protocols on teleost species that have never been bred in captivity before, a move that could pave the way for lucrative new supply channels. Meanwhile, the University of Florida IFAS, with backing from Rising Tide Conservation and the SeaWorld Conservation Fund, has successfully achieved large-scale captive production of Blue Tangs and is ramping up its commercial aquaculture output. As these tank-bred species become more prevalent in retail, the premiums traditionally associated with wild-collection supply chains are set to diminish. This shift promises to reshape the economic landscape for exporters hailing from Indonesia, Sri Lanka, and the Philippines.

Premiumization through rare, designer, and color-variant strains

The ornamental fish market is carving out a premium tier, featuring rare deep-sea species, genetically enhanced color morphs, and artisan-bred regional varieties. This premium segment is generating revenues that far outstrip its contribution in unit volume. In 2024, Thailand's Betta fish, which was named the nation's aquatic emblem in May 2025, boasted an export value of around THB 400 million. This figure accounted for nearly 40% of the nation's total ornamental fish export revenues. Meanwhile, Japan's medaka, or rice fish, is at the heart of a commercial push. Traditionally used in aquascaping and known for their precision-bred color variants, these fish are now being marketed globally under a "ZEN style" branding. This approach marries artisan breeding with a focus on experiential design. The collector's market is heating up, especially for ultra-premium species. Take the Asian arowana's Super Red variety, which can fetch prices north of GBP 250,000 in select luxury circles. For market players, this trend signals a shift: it's no longer just about volume and price competition. Instead, there's a pressing need to curate a premium line alongside traditional commodity species to optimize margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mortality risk during transport and acclimatization | -0.8% | Global, most acute in long-haul export corridors (Asia-Pacific to North America/EU) | Short term (≤ 2 years) |

| Tight import controls and invasive-species compliance burden | -0.6% | North America, Australia, the EU | Medium term (2–4 years) |

| Water-quality expertise gap among first-time hobbyists | -0.4% | Global | Short term (≤ 2 years) |

| Fragmented cold-chain and quarantine infrastructure in export corridors | -0.5% | Southeast Asia, South America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mortality risk during transport and acclimatization

Transport-related mortality poses a significant challenge for the ornamental fish market. Studies from "Fish Welfare in the Ornamental Trade" reveal that, in 2025, mortality rates in the global ornamental fish supply chain could fluctuate between 2% and 73%. These rates hinge on factors like species, handling conditions, and transportation distances. According to "Ornamental Fish International", major exporters noted that in 2025, consistent mortalities exceeding 0.5% per shipment prompted buyers to reconsider their sourcing. This underscores that the repercussions of inadequate logistics stretch beyond mere per-unit losses, impacting customer loyalty. As air freight costs increasingly dominate the per-unit landed price, the stakes rise, especially for marine species. Here, individual specimens command higher values, yet their tolerance to physiological stress during transit is notably lower. In 2025, new intermodal container solutions are emerging for live marine transport. Notably, Ocean Perfect, in collaboration with UNIT45, introduced a 40-ft reefer container featuring integrated saltwater tanks. However, these innovations find their primary commercial application in food-fish logistics, sidelining ornamental trade routes.

Tight import controls and invasive-species compliance burden

Regulatory scrutiny on ornamental fish imports has intensified across all three major Western markets, creating compliance costs that disproportionately burden small-scale importers and independent specialty retailers. A 2025 USGS study published in Biological Conservation identified nine freshwater ornamental fish species as high invasion risks for US ecosystems; the US Fish & Wildlife Service is actively using the findings to assess potential injurious wildlife listings that could restrict or prohibit future imports of affected species. In Australia, DAFF's June 2026 revised draft of the marine ornamental import policy proposes species-specific biosecurity conditions linked to Megalocytivirus pagrus1 susceptibility for four genera, introducing batch-testing requirements for certain exports into an already tightly controlled gateway market. The UK's Ornamental Aquatic Trade Association has flagged that post-Brexit duplication of CITES Non-Detrimental Findings, requiring both exporting-country and UK Scientific Authority assessments for stony corals and other regulated taxa, imposes high bureaucratic cost without proportionate conservation benefit, a structural friction that affects every CITES-listed species trade. Collectively, these pressures mean regulatory compliance overhead will function as a fixed operating cost for importers across all three markets, with no near-term prospect of simplification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tropical Freshwater Anchors Volume; Marine Gain Is Strategic

In 2025, Tropical Freshwater fish captured 53.79% of product-type revenues, bolstered by affordable pricing, a diverse species range from established Southeast Asian farms, and their appeal to novice hobbyists with nano and planted aquascapes. Globally, tetras, cichlids, guppies, and goldfish dominate retail inventories in both specialty and mass-market channels. Meanwhile, discus, bettas, and premium show-quality koi command a distinct sub-layer, generating outsized revenue relative to their unit volume. Notably, Japanese koi breeders are releasing hand-selected show-grade specimens, fetching collector premiums on the international stage. Temperate Freshwater fish, while catering to a geographically concentrated niche, see ecosystems in Japan, Germany, the UK, and China breeding goldfish and koi, supporting both domestic hobbyists and competitive exhibitions.

Marine Ornamentals, the sector's fastest-growing segment, is on track for a 7.96% CAGR through 2031. This growth is fueled by a pivotal supply shift: species once only available in the wild are now being commercially bred and entering retail. A landmark moment arrived in January 2025 when Biota Group made the Blue Tang, a species with historically high demand, available on a commercial scale. In the Netherlands, De Jong Aquaculture achieved a first by breeding the Blue-Spotted Jawfish in captivity and is now scaling up for commercial release. Spectrum Brands' GloFish underscores the commercial viability of color innovations in Tropical Freshwater. With the Electric Green Angelfish hitting the shelves in August 2025, the brand is broadening its fluorescent species lineup across various retail formats. In a significant move, Australia's biosecurity review is considering allowing imports of captive-bred marine ornamentals, contingent on disease screenings. This could unlock a lucrative market for qualified exporters, previously deemed off-limits.

By End Use: Household Retains Scale; Commercial Accelerates on Experience Economy Tailwinds

Commercial end use is projected to grow at a 7.81% CAGR through 2031, outpacing the Household segment. Interior designers, hospitality operators, and corporate facility managers are increasingly viewing custom aquascape installations as experiential amenities rather than mere decorative extras. As of 2026, office design trends in the UK, GCC, and Southeast Asia are placing a premium on employee wellness and talent-attraction features. Bespoke aquariums are now being specified alongside biophilic design elements in new commercial and residential developments. The economic profile of the commercial segment starkly contrasts with that of household retail. An installation in a single hotel lobby or corporate headquarters can feature live species valued in the tens of thousands of dollars. Coupled with multi-year maintenance contracts, this positions commercial buyers as high-lifetime-value accounts, often leaning towards specialized service providers over mass-market retailers.

In 2025, the Household segment accounted for 74.92% of end-use revenues, solidifying its role as the foundational demand layer. Growth is emerging from two distinct poles: beginner starter kits, marketed through mass-market and online channels, are targeting Gen Z's first-time buyers. Meanwhile, experienced hobbyists are gravitating towards sophisticated multi-species reef setups. Spectrum Brands, in collaboration with Aperture Pet & Life, is exemplifying this trend. They've bundled GloFish species with Neptune Systems' IoT aquarium controllers and EcoTech Marine hardware in all-in-one starter kits. This move underscores how established brands are facilitating the transition from beginner to advanced hobbyist through strategic product bundling. Premium commercial installations, especially in large public aquariums, healthcare settings, and hotel lobbies, are increasingly referencing ISO 9001-aligned quality management frameworks. These frameworks serve as a compliance baseline for installers vying for institutional contracts.

By Distribution Channel: Specialty Stores Hold Share; Online Retail Drives Structural Change

In 2025, Specialty Aquatic Stores commanded a 53.13% share of distribution revenues, underscoring hobbyists' enduring preference for face-to-face expert advice. This is especially true when selecting livestock, be it marine species, rare freshwater varieties, or intricate multi-species setups where guidance on compatibility and acclimatization is invaluable. Beyond just selling live fish, these stores offer water testing, species-specific consultations, and locally acclimatized stock. Such services remain structurally unmatched by their online-only counterparts. Meanwhile, Pet Stores act as the gateway for novice aquarists, providing standard freshwater species and branded starter kits from Aqueon, Fluval, and Tetra in a mass-retail setting. Other Distribution Channels, such as wholesale distributors, direct farm-to-buyer platforms, and aquarium club networks, cater to specialist buyers in search of species not typically found in standard retail.

Online Retail Stores are emerging as the fastest-growing channel, boasting a projected CAGR of 8.01% through 2031. The recent bankruptcy of CIS International Holdings, the parent company of LiveAquaria and once the leading US online ornamental fish retailer, has shaken up the online market landscape. This upheaval has paved the way for regional platforms and captive-breeding specialists to step in and capture the audience left behind. Highlighting the trend, Central Garden & Pet's Aqueon BlueIQ app offers features like equipment compatibility alerts and automated maintenance reminders. This move showcases how established brands are leveraging digital services to deepen customer engagement beyond the initial sale. Furthermore, the landscape remains complex: certified online retailers navigate a maze of compliance requirements, from live-animal shipping permits and CITES documentation to marketplace restrictions on regulated species. This expertise sets them apart from informal peer-to-peer sellers, giving a structural advantage to those with dedicated regulatory and logistics know-how.

Geography Analysis

Asia-Pacific, holding a 44.82% revenue share in 2025, is projected to grow at a 7.98% CAGR through 2031. The region's strong production capabilities and growing domestic consumption set it apart. In 2024, Indonesia captured 11.4% of the global export market, earning USD 39.06 million from ornamental fish exports, while domestic transactions reached IDR 6.71 trillion (~USD 424 million), with 99% occurring locally, highlighting untapped export potential (Dewan Ikan Hias Indonesia). Thailand's ornamental fish exports exceeded THB 1,000 million (~USD 28.6 million) in 2024, with a live ornamental fish express logistics service launched in October 2025 to expand international market access (Thai Department of Fisheries). South Korea's Third Comprehensive Plan for the Ornamental Fish Industry (2026–2030) focuses on AI and IoT integration, professional certifications, and digital content expansion (Ministry of Oceans and Fisheries). India, under the Pradhan Mantri Matsya Sampada Yojana (PMMSY), supported 1,986 backyard ornamental fish rearing units and a brood bank in Raigad, Maharashtra, producing 7.7 lakh fish annually across 20 species, with exports estimated at INR 41 crore (~USD 4.9 million).

North America and Europe dominate consumer demand due to high discretionary spending and mature hobbyist communities. The US ornamental fish market, valued at USD 1.68 billion in 2024, is expected to exceed USD 1.8 billion in 2025, growing at 9% annually. Premiumization trends are evident as live freshwater ornamental fish import values rose 18.13% to USD 43.78 million in the first seven months of 2025, despite a 2.3% volume decline, with average prices up 21% to USD 22.27K per ton. UK saltwater ornamental fish imports fell 5.7% in value by October 2025, but Indonesia increased its market share by 16.2% YoY. Germany remains Europe's largest market, with Interzoo 2026 hosting 2,300+ exhibitors across 150,000 square meters, a 10,000-square-meter expansion from 2024. European import markets adhere to CITES compliance and EU wildlife trade regulations.

South America, the Middle East, and Africa show distinct demand profiles. South America benefits from Brazil and Colombia's retail markets and exports of wild-collected Amazonian species, facing sustainability pressures. The GCC market, led by the UAE, Saudi Arabia, and Qatar, is driven by luxury residential and hospitality spending, with custom aquascapes becoming standard in new developments. In Africa, South Africa and Nigeria dominate retail demand, with imports managed through wholesale networks. Regulatory compliance, including CITES permits and GCC biosecurity certifications, shapes trade in these regions.

Competitive Landscape

The live-fish distribution layer of the ornamental fish market remains moderately fragmented, while notable consolidation has taken place in branded accessories, equipment, and nutrition. A significant vertical integration move in recent years is the April 2026 joint venture between Phillips Pet Food & Supplies and Central Garden & Pet. This venture merges Segrest Farms' live-fish operations and Aqueon/Coralife brand assets with Phillips' exclusive Fluval distribution rights. This move is poised to limit the operational flexibility of independent distributors managing both brand families. In Q4 FY2025, Spectrum Brands' aquatics segment achieved high-single-digit net sales growth in North America and EMEA, fueled by distribution gains and the robust performance of the GloFish brand. Concurrently, the company lodged a 2024 patent application for an innovative modular back-panel aquarium filtration system, underscoring its commitment to product innovation amidst a broader revenue dip in the pet category.

Tetra, celebrating its 75-year anniversary at Interzoo 2026, showcased a live aquascaping workshop and a branded experience area, signaling its dedication to penetrating the professional channel beyond just mass retail. Strategic differentiation in the competitive landscape hinges on three main pillars: captive-breeding prowess, digital-platform integration, and ownership of logistics infrastructure. De Jong Aquaculture's IVF-assisted marine fish breeding and Surge Marine Life's focus on rare deep-water species aquaculture underscore a long-term capability that outpaces incumbents reliant on wild-collection supplies. Spectrum Brands' 2024 collaboration with Aperture Pet & Life, which melds GloFish species with Neptune Systems and EcoTech Marine's IoT hardware, crafts a connected-device ecosystem. This integration not only enhances user experience but also establishes switching costs for loyal hobbyists.

There's an untapped opportunity in the realm of certified sustainable sourcing: no single entity currently dominates marine ornamental fish certification, unlike the Marine Stewardship Council's stronghold in food fish. This presents a potential avenue for a resourceful retailer or standards body. Emerging disruptors include specialists in captive-breeding, e-commerce platforms sourcing directly from farms in Southeast Asia, and AI-driven services monitoring fish health in tandem with IoT aquarium hardware.

Ornamental Fish Industry Leaders

LiveAquaria

PetSmart LLC

Petco Health and Wellness Company, Inc.

Rolf C. Hagen Inc.

Tetra GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: In a move set to transform the landscape of wholesale ornamental fish distribution in the U.S., Phillips Pet Food and Supplies and Central Garden & Pet Company have forged a strategic joint venture. Operating under the Phillips brand, the venture melds Central's Segrest Farms live-fish operations and Aqueon/Coralife brand assets with Phillips' exclusive distribution rights to the Fluval brand.

- October 2025: Thailand Post and the Thai Department of Fisheries launched the country's first international express shipping service for live ornamental fish, with Phase 1 covering the US, China, Japan, Taiwan, and Indonesia; domestic ornamental fish shipments via Thailand Post totaled over 110,000 pieces between February and August 2025.

- September 2025: Surge Marine Life (Florida, US) began shipping the world's first commercially available captive-bred Rose Anthias (Odontanthias katayamai) at affordable prices, compared to wild-specimen retail prices, marking a significant cost-accessibility threshold in marine ornamental aquaculture

Global Ornamental Fish Market Report Scope

Ornamental fish refers to any aquatic species reared or marketed for their aesthetic beauty, color, or exotic characteristics rather than for food or sport. The global ornamental fish market is segmented by product type, end use, distribution channel, and geography. By product type, the market is segmented into tropical freshwater, temperate freshwater, and marine ornamentals. By end use, the market is segmented into household and commercial. By distribution channel, the market is segmented into specialty aquatic stores, pet stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Tropical Freshwater |

| Temperate Freshwater |

| Marine Ornamentals |

| Household |

| Commercial |

| Specialty Aquatic Stores |

| Pet Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Tropical Freshwater | |

| Temperate Freshwater | ||

| Marine Ornamentals | ||

| End Use | Household | |

| Commercial | ||

| Distribution Channel | Specialty Aquatic Stores | |

| Pet Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for the ornamental fish market?

The ornamental fish market is valued at USD 8.21 billion in 2026 and is projected to reach USD 11.39 billion by 2031, growing at a 6.8% CAGR.

Which product category leads ornamental fish sales?

Tropical Freshwater leads the category with 53.79% of revenue in 2025 because it combines lower prices, broad species choice, and strong beginner appeal.

Which channel is growing fastest for ornamental fish sales?

Online Retail Stores are projected to grow at 8.01% CAGR through 2031, supported by better live-animal logistics, quarantine handling, and digital customer support.

Why is captive breeding important for marine ornamental fish?

Captive breeding improves supply stability, lowers dependence on wild collection, and makes high-demand species such as Blue Tang more commercially available.

Page last updated on: