Hiking Gear And Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 91.45 Billion |

| Market Size (2031) | USD 124.18 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

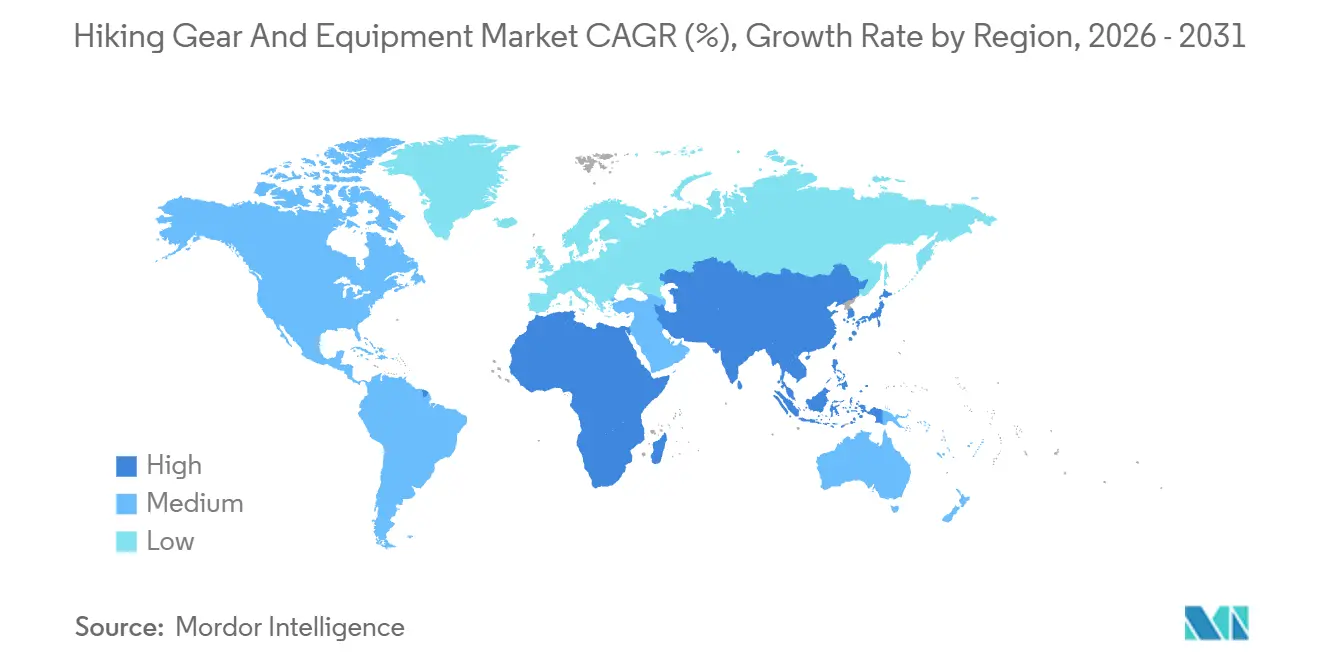

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

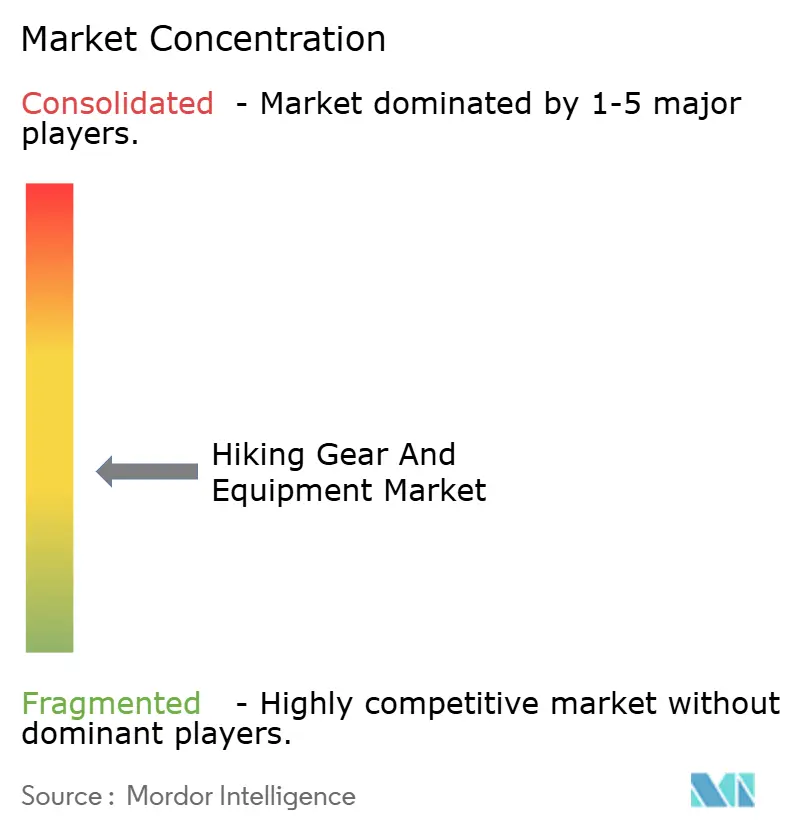

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hiking Gear And Equipment Market Analysis by Mordor Intelligence

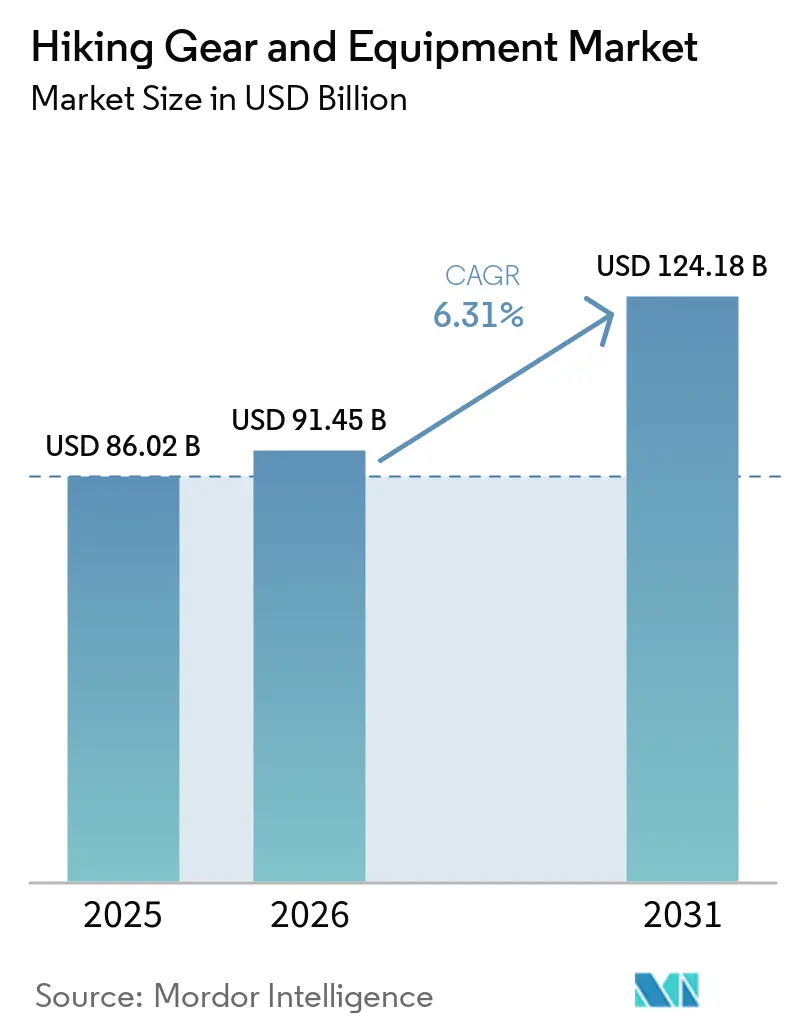

The Hiking Gear and Equipment Market size is projected to be USD 86.02 billion in 2025, USD 91.45 billion in 2026, and reach USD 124.18 billion by 2031, growing at a CAGR of 6.31% from 2026 to 2031. Record outdoor participation, swift adoption of digital retail, and ongoing material innovations, lightening packs without compromising durability, drive growth. Today's consumers prioritize gear that marries performance with environmental responsibility. This trend is bolstered by government investments in trails, enhancing access for novice hikers. Firms that adjust their product lines to reflect demographic changes, especially the increasing involvement of women and multicultural groups, maintain their pricing power despite fluctuations in raw material costs. While competition remains moderate, established brands can command premium prices, and smaller, nimble specialists are seizing niche markets with their focus on design and sustainability.

Key Report Takeaways

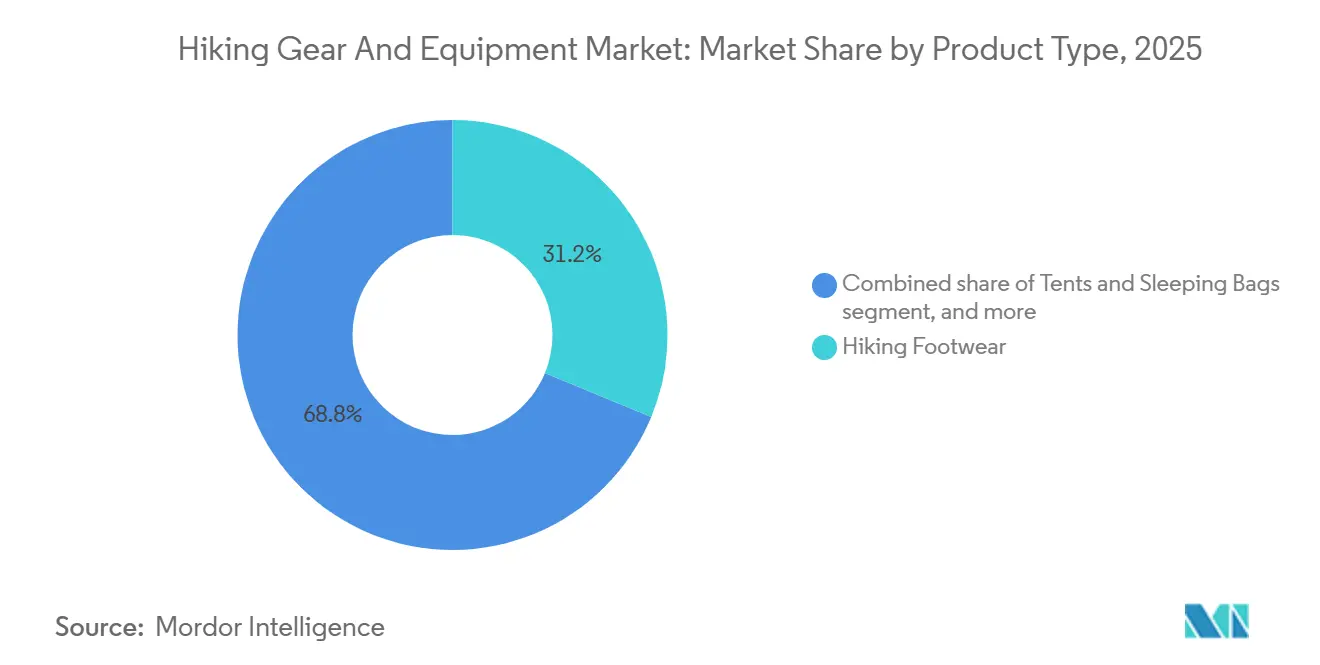

- By product type, hiking footwear led with 31.22% revenue share in 2025, while navigation and safety devices are projected to post a 7.02% CAGR through 2031.

- By end user, men accounted for 53.28% of the hiking gear equipment market share in 2025, and women are advancing at a 6.95% CAGR to 2031.

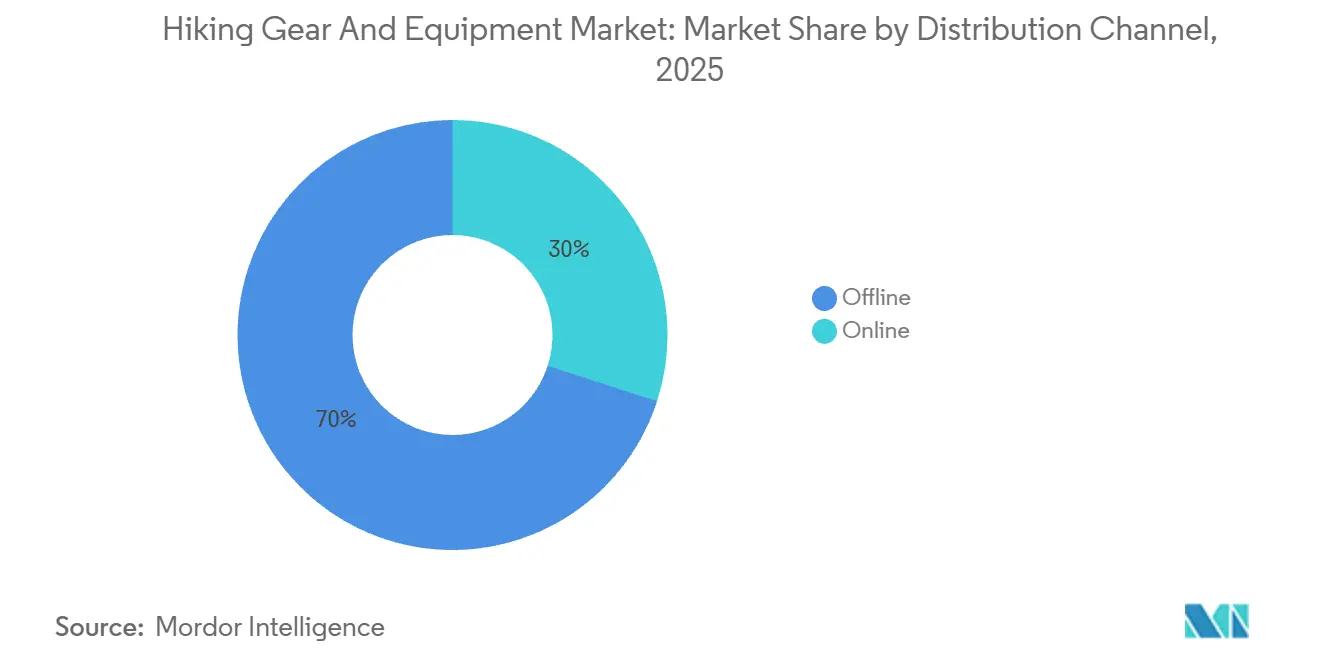

- By distribution channel, offline outlets retained 70.02% share of the hiking gear equipment market size in 2025, while online sales are expanding at a 7.52% CAGR through 2031.

- By geography, North America contributed 42.88% of 2025 global revenue, and the Asia-Pacific is forecast to grow at a 8.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hiking Gear And Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Multi-functional lightweight materials | +1.2% | North America, Europe | Medium term (2-4 years) |

| Boom in adventure tourism and government-backed eco-tourism initiatives worldwide | +0.8% | Asia-Pacific, South America | Long term (≥ 4 years) |

| Technological Innovation in Materials and Design | +0.7% | Global | Medium term (2-4 years) |

| Expansion of sustainable practices by brands focusing on ethical sourcing and production | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Wearable tech and smart safety features | +0.5% | North America, Europe | Short term (≤ 2 years) |

| Public-sector investments in trail infrastructure | +0.4% | United States, China, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Multi-functional lightweight materials

Consumer preferences are shifting towards gear that maximizes performance while minimizing weight, thanks to advancements in material engineering. This shift is fundamentally changing product development priorities across the industry. Manufacturers are increasingly turning to synthetic alternatives, with innovations in polyester and nylon achieving 30-40% weight reductions without sacrificing durability. This trend mirrors a broader change in consumer behavior: outdoor enthusiasts now prioritize versatility, leading to a surge in demand for convertible and modular gear systems. Columbia Sportswear's 2024 financials underscore this shift, highlighting growth in their technical apparel segments that champion multi-functional designs[1]Source: Columbia Sportswear Company, “Form 10-K 2024,” sec.gov. Breakthroughs in material science, such as moisture-wicking fabrics and temperature-regulating technologies, are positioning lightweight, multi-functional products as premium market differentiators. Furthermore, companies forging early partnerships with specialized textile manufacturers are gaining competitive advantages through supply chain optimizations centered around these advanced materials.

Boom in adventure tourism and government-backed eco-tourism initiatives worldwide

In emerging economies, rapid development of outdoor recreation infrastructure is fueling a significant demand for hiking equipment. This surge is largely driven by a newly affluent middle class, eager for experiential travel. Adventure tourism operators, as reported by the Adventure Travel Trade Association, cite median trip costs of USD 2,813 for 8-night excursions. Notably, 75% of this expenditure goes to local suppliers, underscoring the robust economic multiplier effects that bolster gear demand. China's ambitious outdoor sports development plan, eyeing a market value of 3 trillion yuan by 2025, showcases government-backed efforts pushing market growth beyond the confines of traditional Western markets. The Adventure Travel Trade Association highlights hiking and trekking as leading activities, with a promising 85% of tour operators forecasting enhanced profitability in 2024, a testament to the industry's unwavering confidence[2]Source: Adventure Travel Trade Association, “2024 Adventure Travel Industry Snapshot,” adventuretravel.biz. Consumers in developing markets are leaning towards value-oriented gear combinations over premium single-item purchases. This shift compels manufacturers to recalibrate their product portfolios and pricing strategies. Furthermore, geographic diversification emerges as a strategy to mitigate seasonal demand fluctuations, with markets in the Southern Hemisphere balancing out those in the Northern Hemisphere.

Technological Innovation in Materials and Design

Smart technology is revolutionizing traditional hiking gear, turning it into connected devices that boost safety, navigation, and performance monitoring. This shift is not only creating new product categories but also opening up fresh revenue streams. In a notable move, Arc'teryx teamed up with Skip to unveil the MO/GO powered exoskeleton pants. These innovative pants, thanks to electric motor assistance at the knee joint, give users the sensation of a 30-pound weight reduction, marking a significant leap in outdoor gear technology, as highlighted by The Verge. As consumers increasingly prioritize features like real-time biometric monitoring, GPS tracking, and emergency communication, the adoption of wearable technology is witnessing a sharp uptick. Material advancements are also making waves: phase-change materials are being used for better temperature regulation, antimicrobial treatments are tackling odor control, and self-repairing fabrics are extending the lifespan of products. A surge in patent filings related to outdoor gear technology in 2024 underscores the industry's robust commitment to R&D. Companies that adeptly weave technology into their offerings, all while upholding the reliability standards of traditional outdoor gear, not only command premium prices but also fortify their position against commodity manufacturers.

Expansion of sustainable practices by brands focusing on ethical sourcing and production

Driven by environmental consciousness, consumers increasingly favor brands with measurable sustainability commitments. This shift intensifies competitive pressure on brands to adopt transparent supply chain practices and utilize recycled materials. In the outdoor industry, there's a notable push for sustainability certifications. According to the Adventure Travel Trade Association, 48% of adventure travel businesses are actively pursuing environmental credentials to align with consumer expectations. As the costs of recycled polyester and organic cotton near parity with conventional materials, the price barrier to sustainable product lines diminishes, leading to accelerated adoption. Furthermore, consumers are showing a willingness to pay a premium for environmentally responsible products. This trend presents brands with an opportunity to expand their margins, especially if they can effectively communicate the value of their sustainability efforts. In response to rising demands for supply chain transparency, many companies are adopting vertical integration strategies. This shift allows them direct control over measuring and reporting their environmental impact. Additionally, regulatory pressures in major markets, notably the European Union and California, are creating a compliance edge for early adopters of sustainability. In contrast, these regulations could place traditional manufacturers at a disadvantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in high-performance material costs | -0.9% | Global, with acute impact on premium segment manufacturers | Short term (≤ 2 years) |

| Counterfeit and low-quality imports eroding brand value | -0.6% | Global, concentrated in online marketplaces and developing markets | Medium term (2-4 years) |

| Seasonal demand fluctuations | -0.4% | Northern Hemisphere markets, particularly North America and Europe | Short term (≤ 2 years) |

| Safety concerns and risk aversion | -0.3% | Global, with heightened sensitivity in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in High-performance Material Costs

In 2024, fluctuations in raw material prices exerted pressure on margins throughout the hiking gear supply chain. Synthetic fabric costs, influenced by petroleum price shifts and disruptions in the supply chain, saw a volatility of 15-20%. Sporting goods manufacturers grappled with rising input costs in both transportation and raw materials. This challenge compelled them to adopt dynamic pricing strategies and optimize inventory management. Manufacturers of premium gear felt a heightened impact; high-performance materials not only commanded steeper price premiums but also showed heightened sensitivity to supply disruptions. Companies with global supply chains, like Amer Sports, highlighted the challenges of currency exchange rate volatility, noting its influence on 2025 sales growth projections due to a strong dollar. To counteract cost volatility, companies turned to hedging strategies and diversified their suppliers. However, these risk management tactics introduced added complexity to operations and curtailed flexibility. In response to material cost pressures, manufacturers pursued vertical integration, aiming for enhanced control over supply chain economics and quality standards.

Counterfeit and Low-quality Imports Eroding Brand Value

Intellectual property infringement and product counterfeiting not only blur brand distinctions but also pose safety risks, eroding consumer trust in premium outdoor gear. The rise of online marketplaces has facilitated the widespread distribution of counterfeit products. Often, these fake hiking gears fall short of safety standards, raising liability concerns for genuine manufacturers. To counteract this, companies are ramping up investments in authentication technologies, legal measures, and consumer education, driving up brand protection costs. During economic downturns, consumers' price sensitivity makes them more susceptible to counterfeit alternatives, which promise value but often compromise on performance and safety. Furthermore, global supply chains face quality control hurdles, necessitating stricter monitoring and testing protocols, which in turn inflate operational costs and delay market entry. The surge of private and white-label products in online platforms intensifies competition for branded manufacturers and risks muddling consumer perceptions of quality and performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominance Drives Market Foundation

In 2025, hiking apparel secures a dominant 25.72% share of the market, cementing its status as the industry's cornerstone. This prominence is attributed to a blend of frequent replacements, fashion-forward influences, and avenues for technical innovations. The segment enjoys a unique crossover appeal, attracting both dedicated outdoor enthusiasts and urbanites who embrace hiking-inspired fashion. This trend broadens the market's reach, extending well beyond conventional outdoor retail channels. Meanwhile, navigation and safety devices are the standout performers, charting a robust 7.02% CAGR through 2031. This surge underscores a growing consumer emphasis on technology-driven risk mitigation and preparedness for emergencies. Backpacks continue to be in steady demand as indispensable gear. At the same time, hiking footwear sees a boost, thanks to advancements in biomechanical design and adaptations for specialized terrains.

While tents and sleeping bags grapple with competition from lightweight alternatives, they also face challenges from an expanding rental market. This trend is especially pronounced among younger consumers who increasingly value experiences over ownership. Hydration gear is riding the wave of heightened health consciousness, bolstered by technological strides in filtration and temperature control. Other accessories, such as trekking poles, headlamps, and multi-tools, exist as fragmented subcategories. Yet, they present ripe opportunities for innovation, especially in materials and the integration of smart technology. Notably, the Outdoor Industry Association's 2024 trends report highlights a significant shift in the outdoor retail market: a growing preference for casual products over traditional technical gear. This shift is reshaping product development priorities across all categories[3]Source: Outdoor Industry Association, “Explore Outdoor Retail Sales Trends,” oia.org.

By End User: Women's Segment Accelerates Market Expansion

In 2025, men hold a 53.28% share of the market, echoing longstanding trends in outdoor participation. Meanwhile, women, with a 6.95% CAGR projected through 2030, emerge as the segment with the most rapid growth, signaling a notable demographic shift in outdoor recreation. Women's gear needs to diverge from men's, emphasizing distinct fit, functionality, and aesthetic preferences. This divergence not only drives specialization in product lines but also necessitates dedicated investments in research and development. The segment's growth is further bolstered by social media's sway and community-building efforts, which have effectively diminished traditional barriers to outdoor participation.

The uptick in the kids' segment mirrors a broader family trend towards outdoor recreation and a parental push for active lifestyles. This trend paves the way for scalable and adjustable gear systems. Moreover, product development tailored to gender goes beyond mere sizing. It encompasses safety features, storage solutions, and comfort technologies, all attuned to varied usage patterns and preferences. As the market broadens its appeal to diverse demographic groups, it unveils avenues for culturally attuned product development and marketing. Companies that adeptly cater to women's needs with specialized product lines and community-centric strategies stand to gain significantly in this expanding market.

By Distribution Channel: Digital Transformation Reshapes Retail Dynamics

In 2025, offline retail commands a dominant 70.02% market share, underscoring the enduring significance of hands-on product engagement and expert advice in the purchase of hiking gear. Yet, online retail is carving out a niche, growing at a brisk 7.52% CAGR through 2031. A broader product range, competitive pricing, and advancements in digital product showcasing fuel this surge. Today's consumers often research online but may finalize purchases in-store, highlighting the need for retailers to adopt an omnichannel approach.

Manufacturers are increasingly embracing direct-to-consumer strategies, aiming for tighter control over brand narratives and customer interactions. This is especially pronounced in premium segments, where compelling brand storytelling can sway purchasing choices. E-commerce is witnessing a surge, particularly among younger, urban consumers who value convenience and price comparisons, often at the expense of in-store consultations. Meanwhile, physical retail spaces are transforming. They're shifting from mere inventory displays to experiential hubs, focusing on product trials, community gatherings, and expert consultations. Retailers that adeptly merge online and offline channels, bolstered by cohesive inventory and customer service systems, are reaping significant competitive rewards.

Geography Analysis

In 2024, North America captured 42.88% of the global revenue, driven by its vast trail networks and a robust discretionary spending culture. The USDA's allocation of USD 2 billion for recreation not only bolsters local economies but also enhances trail maintenance and accessibility, drawing in new hikers. With U.S. participation hitting 168.1 million in 2024, specialty retailers enjoyed a consistent customer flow[4]Source: USDA Forest Service, “Fiscal Year 2025 Budget Justification,” usda.gov. While Canada boosts demand for cold-weather gear, Mexico's adventure tourism hotspots drive sales of budget-friendly packs and footwear.

Asia-Pacific, with a projected CAGR of 8.04% through 2031, is the region to watch, largely due to China's ambition for a 3 trillion-yuan outdoor economy. With over 400 million Chinese participating in outdoor sports, there's a notable uptick in sales of mid-tier apparel and hydration equipment[5]Source: National Development and Reform Commission of China, “Guidance on High-Quality Outdoor Sports Destinations,” ndrc.gov.cn . Tech-savvy consumers in Japan and South Korea lean towards premium ultralight kits, while those in India and Southeast Asia, as their disposable incomes rise, gravitate towards value bundles. The region's manufacturing not only brings cost benefits but also heightens competition from emerging domestic brands.

Europe's growth narrative is deeply intertwined with sustainability. Consumers are increasingly willing to pay a premium for products made from recycled fabrics and those bearing the bluesign certification. This trend is compelling brands to not just meet but surpass EU environmental standards. The region's Alpine and Nordic hiking traditions fuel a consistent demand for year-round footwear and layering, balancing out the slower growth observed in Southern Europe. Meanwhile, South America and the Middle East & Africa, though smaller players, are carving out strategic niches, navigating seasonal sales cycles and seizing early opportunities in developing trail infrastructures.

Competitive Landscape

The hiking gear and equipment market showcases a moderate fragmentation, balancing scale advantages with opportunities for disruptors. Premium brands like The North Face, Columbia Sportswear, and Arc’teryx utilize global distribution, proprietary fabrics, and endorsements from athletes. Arc’teryx’s launch of the USD 5,000 MO/GO exoskeleton highlights the potential of hardware-software hybrids in carving out unique market positions. Columbia invests its cash flow into the PFG and SH/FT ranges, extending their appeal beyond just backcountry use.

Amer Sports, the parent company of Salomon and Arc’teryx, reported a 23% revenue growth in Q1 2025, underscoring the benefits of scale in footwear and apparel. New market entrants are tapping into eco-friendly textiles and designs tailored for women, targeting niches that have been overlooked. Tech companies are embedding GPS chips and biometric sensors into their gear, forming alliances that could pose challenges to traditional players without electronics know-how. While there's a surge in securing intellectual property through patents and trade secrets, many are also opening innovation labs, collaborating with start-ups to push the boundaries of material science.

Strategic maneuvers are increasingly leaning towards direct-to-consumer approaches, safeguarding margins and capturing detailed customer insights. Brands are deepening engagement through loyalty programs, rewarding trail usage with in-app achievements that translate to discounts. M&A talks are buzzing around vertical integration, especially with specialty fabric mills, aiming to stabilize supply fluctuations and enhance sustainability tracking. With no single entity commanding more than 15% of the revenue, the hiking gear and equipment market remains a competitive playground for nimble brands adept in design, digital strategies, and environmental considerations.

Hiking Gear And Equipment Industry Leaders

The North Face (VF Corp.)

Columbia Sportswear

Decathlon (Quechua/Forclaz)

Patagonia

Arc'teryx (Anta Sports)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Simond has introduced one of the lightest serious trekking shelters. The new Sprint Tarp Tent 2P weighs just 620g in total, using Dyneema composite fabric to deliver a combination of minimal pack weight and high durability, according to the brand.

- March 2026: Big Agnes expanded its line with the launch of its new ultralight shelter family, the VST range, designed for hikers and fastpackers chasing low pack weights without sacrificing comfort or weather protection. According to the brand, the backpacking tents use the recycled 20D HyperBead fabric, delivering a 4,000mm waterproof rating while remaining PFAS-free.

- February 2026: YETI expanded its product line with the launch of the Skala, a new line of technical hiking backpacks designed for everything from fastpacking to multi-day hikes. According to the brand, available in several capacities, including 32L, 40L, and 50L, the Skala range marks a noticeable shift in YETI’s positioning.

Global Hiking Gear And Equipment Market Report Scope

| Backpacks |

| Hiking Footwear |

| Hiking Apparel |

| Tents and Sleeping Bags |

| Navigation and Safety Devices |

| Hydration Gear |

| Other Accessories |

| Men |

| Women |

| Kids |

| Offline |

| Online |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Backpacks | |

| Hiking Footwear | ||

| Hiking Apparel | ||

| Tents and Sleeping Bags | ||

| Navigation and Safety Devices | ||

| Hydration Gear | ||

| Other Accessories | ||

| By End User | Men | |

| Women | ||

| Kids | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global hiking gear equipment market in 2026?

The hiking gear equipment market size reached USD 91.45 billion in 2026 and is set to rise to USD 124.18 billion by 2031.

Which product category is expanding the fastest?

Navigation and safety devices are projected to grow at a 7.02% CAGR through 2031 as hikers adopt tech-enabled risk-mitigation tools.

What region offers the highest growth potential?

Asia-Pacific is expected to record a 8.04% CAGR, driven by China’s 3 trillion-yuan outdoor economy push and rising middle-class adventure travel.

Why are lightweight materials critical for growth?

Advances in nylon and polyester deliver 30–40% weight savings, enhancing comfort and motivating upgrades to new multi-functional apparel.

Page last updated on: