Europe Organic Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

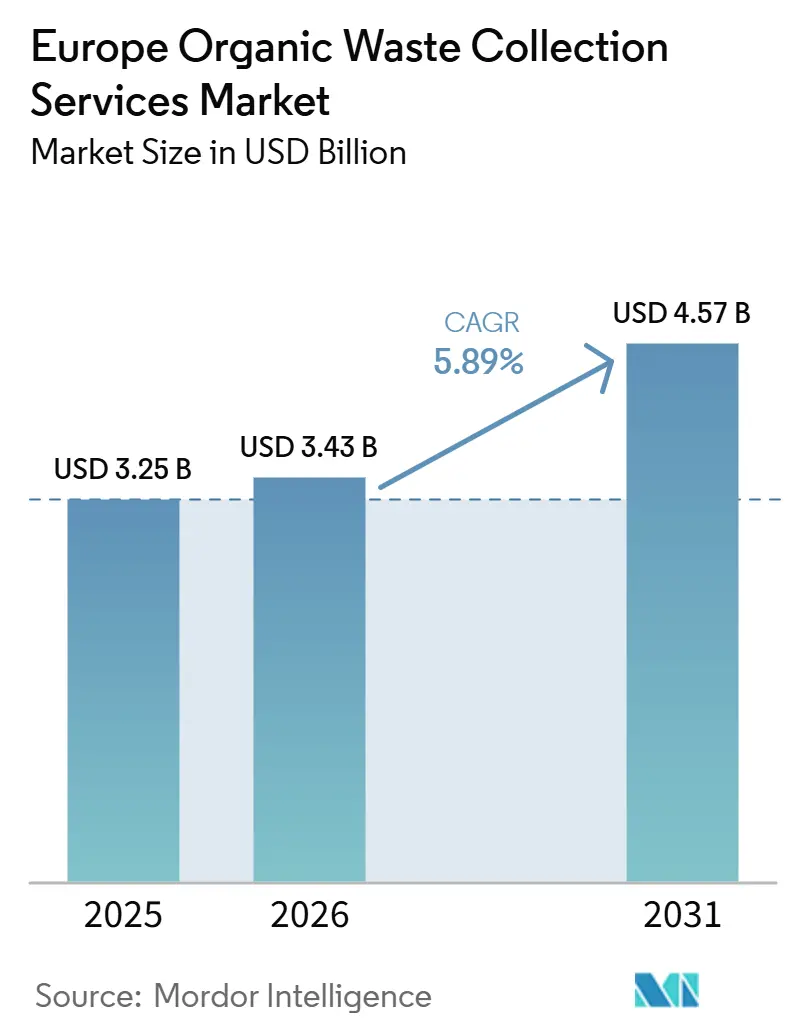

| Base Year Market Size (2025) | USD 3.25 Billion |

| Market Size (2026) | USD 3.43 Billion |

| Market Size (2031) | USD 4.57 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

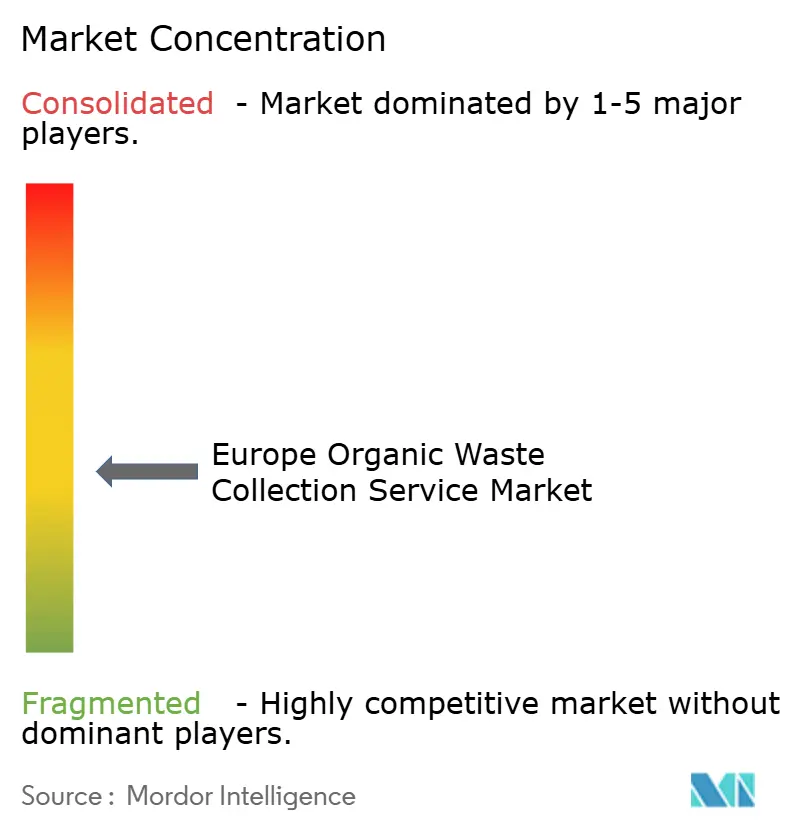

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Organic Waste Collection Services Market Analysis by Mordor Intelligence

The Europe Organic Waste Collection Services Market size is projected to be USD 3.25 billion in 2025, USD 3.43 billion in 2026, and reach USD 4.57 billion by 2031, growing at a CAGR of 5.89% from 2026 to 2031.

Policy pressure from the EU Waste Framework Directive’s separate bio-waste collection mandate and rising landfill taxes is anchoring near-term demand as municipalities scale structured door-to-door programs and quality controls to meet circularity targets. REPowerEU’s biomethane push reframes organic waste as a strategic energy feedstock, which elevates the role of dependable collection and contamination management across both residential and commercial routes. Competitive strategies prioritize vertical integration, digital tracking through RFID-linked bins, and fleet electrification to manage fuel and maintenance costs under emerging zero-emission urban zones. Capital access for biomethane grid-injection and municipal infrastructure is improving through EU-level lenders, which favors operators capable of aligning collection flows with downstream upgrading capacity. These shifts position the Europe organic waste collection service market to benefit from regulatory timelines, technology maturity, and grid-injection incentives concentrated in markets with consistent policy frameworks.

Key Report Takeaways

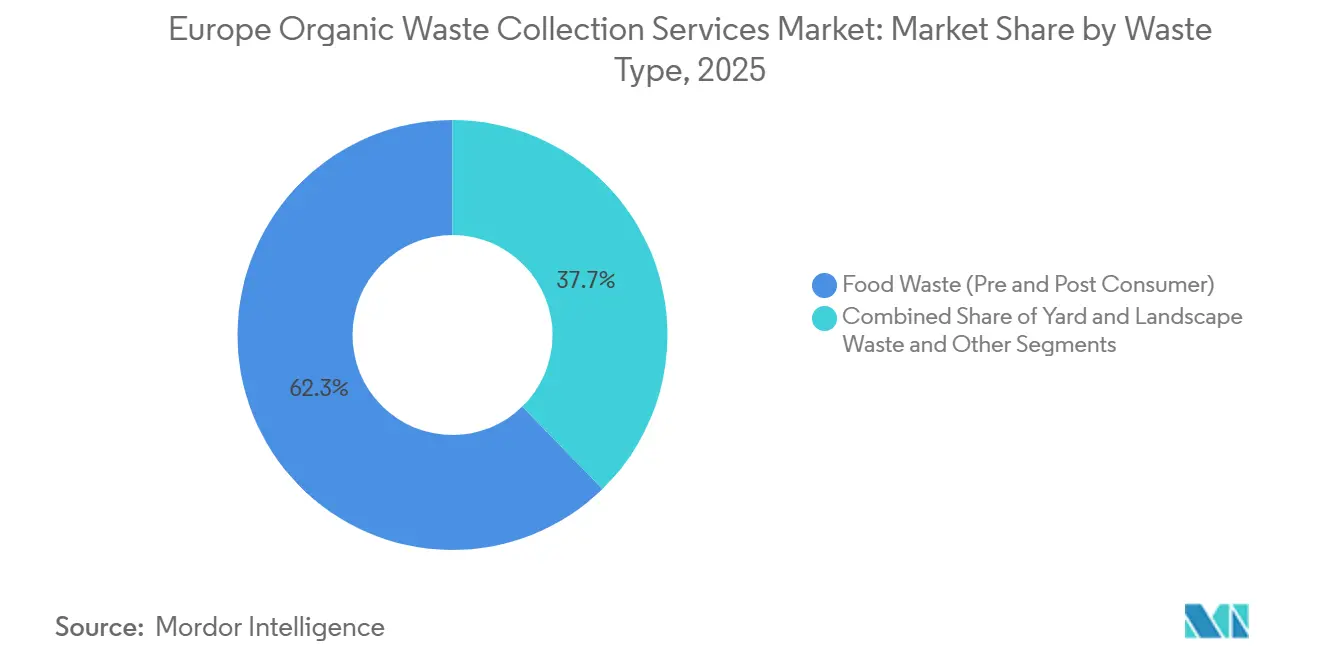

- By waste type, food waste captured 62.3% share of the Europe organic waste collection service market size in 2025 and is advancing at a 6.89% CAGR through 2031.

- By end-user, the residential segment held 54.8% of the Europe organic waste collection service market share in 2025, while commercial food service is projected to expand at a 7.62% CAGR to 2031.

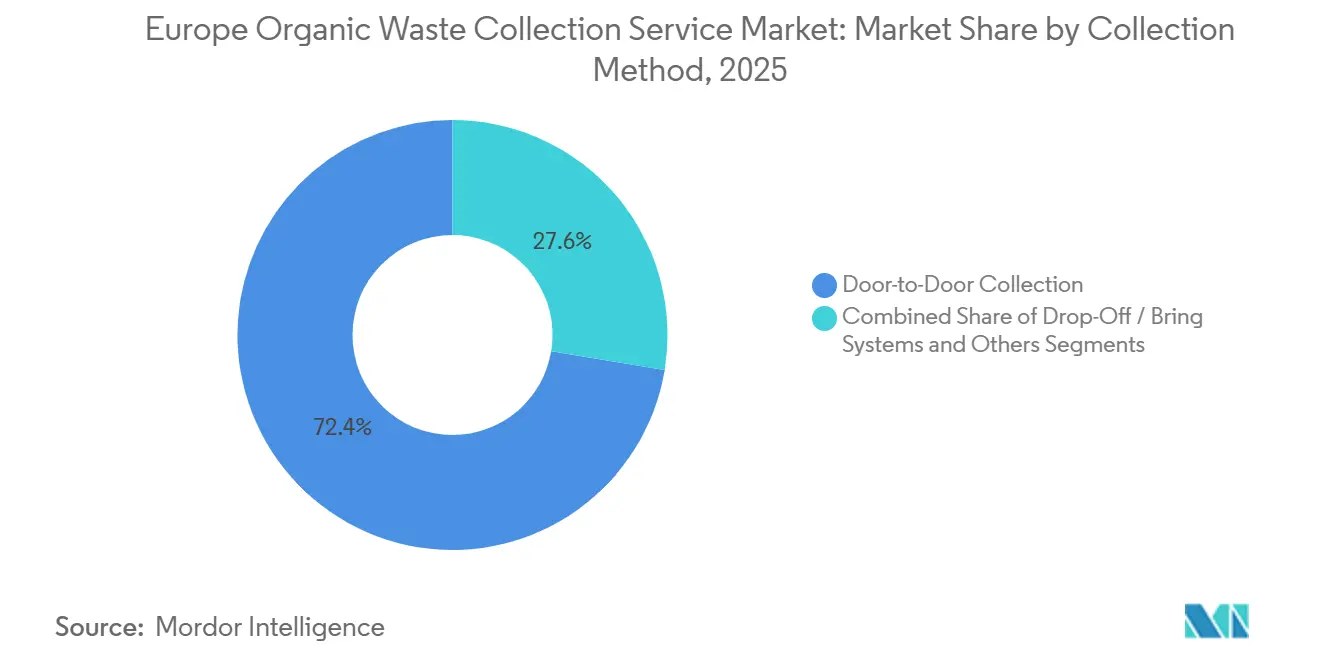

- By collection method, door-to-door led with a 72.4% revenue share in 2025, and fully automated systems are forecast to grow at an 8.49% CAGR to 2031.

- By technology and equipment, semi-automated systems accounted for a 64.7% share in 2025, while fully automated variants are set to post the fastest growth at 8.49% CAGR through 2031.

- By geography, Germany commanded 24.2% share in 2025, while Spain is projected to record the highest growth at 7.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Organic Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Landfill Directive restrictions and escalating landfill taxes across member states | +1.8% | EU-27, particularly Greece (€35-45/tonne from 2026), Portugal, Romania | Medium term (2-4 years) |

| Growing biogas and biomethane demand aligned with REPowerEU energy security goals | +1.5% | EU-27 core; Germany, France, Italy lead; spill-over to Iberia and Eastern Europe | Medium term (2-4 years) |

| Farm to Fork Strategy promoting food waste reduction and resource recovery | +1.2% | EU-27, with 30% per capita reduction targets by 2030 for retail, restaurants, and households | Long term (≥ 4 years) |

| Extended Producer Responsibility schemes expanding to organic waste streams | +0.7% | EU-27, with Flanders mandatory separate collection by January 2026 and similar moves in NL and BE | Medium term (2-4 years) |

| Municipal commitments to climate neutrality and methane reduction | +0.6% | EU-27 national and city-level, concentrated in Germany and the Netherlands | Long term (≥ 4 years) |

| Technological innovation in collection systems and digitalization | +0.6% | EU innovation hubs; examples in Slovakia and Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Landfill Directive Restrictions and Escalating Landfill Taxes Across Member States

The EU’s requirement for separate bio-waste collection has created uneven enforcement timelines, resulting in staggered procurement windows and early-mover advantages for operators who invested ahead of local deadlines in countries such as Greece, Portugal, and Romania, and in regions like Flanders, where the January 2026 cutover is accelerating municipal contracting decisions[1]European Commission, “Revised Waste Framework Directive Enters Into Force,” European Commission, environment.ec.europa.eu. Greece’s landfill tax progression to a EUR 35-45 per tonne range from 2026 shifts the cost parity toward digestion pathways even when accounting for significant upgrading investments per integrated facility, which strengthens the business case for route optimization and quality-controlled collection. Implementation gaps in some member states sustain residual flows and undercut separate collection growth, as modest landfill levies and enforcement limits are linked to informal transfers that reduce predictable feedstock supply for biomethane value chains. Early Warning Reports identified a need to improve bio-waste performance in most member states, and specific country-level capacity shortages and delays show that collection contracts must be sequenced with facility readiness to avoid underutilization or stranded equipment. Portugal’s tight landfill capacity window emphasizes the role of integrated operators that can divert flows to composting or digestion while maintaining contamination control under separate collection schemes. A scheduled 2027 EU review of targets introduces planning uncertainty that can delay capital commitments, so operators that can flex capacity arrangements and stage investments are better positioned to weather policy recalibration while continuing growth in the Europe organic waste collection service market

Growing Biogas and Biomethane Demand Aligned with REPowerEU Energy Security Goals

REPowerEU’s 35 bcm biomethane goal redefines organics as energy feedstock, yet capacity additions remain constrained by collection bottlenecks as current production is far below potential, with association data showing installed biomethane capacity that outpaces output by a notable margin due to feedstock procurement gaps. Across key countries, policy models determine momentum more than legacy plant count, with auction frameworks and certificate obligations in France lifting output despite many small units, while regulatory volatility in Germany slows investments even with a large installed base and long-standing expertise. Denmark’s high biomethane penetration is supported by long-duration support schemes and emerging CCUS incentives, indicating that yields on collection investments grow when paired with long-term offtake stability. Southern Europe’s pipeline is expanding from a low base, with Spain and Portugal setting targets and mobilizing funding tools, though permitting gaps and execution delays show that reliable separate collection flows must develop in parallel with upgrading assets to synchronize supply with grid-injection plans. EU-level lenders are underwriting grid-injection readiness to de-risk pipeline connections, exemplified by loans that extend to national transmission infrastructure and regional projects that create predictable pathways from bins to biomethane offtake. These linkages reinforce how cohesive policies and financing shorten the distance between separate collection performance and sustained growth in the Europe organic waste collection service market.

Farm to Fork Strategy Promoting Food Waste Reduction and Resource Recovery

The 2025 entry into force of the revised Waste Framework Directive, with binding 2030 food waste reduction targets, creates a dual mandate that elevates prevention while maintaining strong recycling goals, encouraging municipalities to expand separate collection and align tariffs with sorting quality. Parliamentary data estimates that total EU food waste remains significant across households, retail, and hospitality, so the scale of reduction needed implies that collection routes must be resilient to variability in set-outs and sensitive to contamination risks if organics are to reliably supply anaerobic digestion. Member states will incorporate prevention programs into national law, creating space for contract designs that directly reward improved sorting behavior and document-quality outcomes through digital tools at the container level. Precedents like pay-as-you-throw schemes for non-household users and their subsequent rollout to households are set to influence commercial and municipal pricing systems that reflect both waste generation and contamination levels, favoring operators with RFID-based verification and auditable reporting systems. The policy hierarchy prioritizes donation over energy recovery, yet energy incentives can still attract surplus food into digestion when donation logistics are weak, which means municipalities and operators need to coordinate with social organizations to uphold prevention intent while keeping collection economics viable. Member states with landfill bans for certain sectors have catalyzed quick steps toward compliance, but where collection infrastructure lags the minimization of residual waste is often limited to the lowest viable threshold, which underscores why investments in container networks and education affect both volumes and quality for the Europe organic waste collection service market

Extended Producer Responsibility Schemes Expanding to Organic Waste Streams

In Europe, the European Commission's revisions to the Waste Framework Directive, along with regional circular economy policies, are broadening the scope of Extended Producer Responsibility (EPR) schemes. These schemes are moving beyond just packaging and textiles to encompass a wider range of municipal and organic waste streams. Regions like Flanders and the Netherlands are tightening their mandates, requiring separate collections for bio-waste and food waste. This shift underscores a growing demand for specialized services in organic waste collection and treatment. Starting January 2026, Flanders will ramp up its mandatory bio-waste collection. Concurrently, Belgium and the Netherlands are witnessing a surge in investments, driven by similar policy shifts. These investments span organic waste logistics, curbside collection infrastructure, and composting and anaerobic digestion networks. As a result, municipalities and waste management operators are broadening their services to include dedicated collections for food and green waste.

With the expansion of EPR-linked waste management duties, the Europe Organic Waste Collection Service market is poised for medium-term growth over the next 2–4 years. This is largely due to mounting regulatory pressures on municipalities, businesses, and food producers to enhance their organic waste segregation and recycling efforts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory frameworks and implementation gaps across EU member states | -1.2% | EU-27, especially cross-border operations and certificate interoperability | Medium term (2-4 years) |

| High infrastructure investment needs for vehicles and facilities | -0.9% | EU-wide, more acute in Eastern and Southern Europe | Long term (≥ 4 years) |

| Contamination in organic streams affecting downstream processing quality | -0.6% | EU-27, where physical impurities >5% degrade compost value | Short term (≤ 2 years) |

| Limited processing capacity in Eastern and Southern regions | -0.5% | Bulgaria, Romania, Croatia, Cyprus, Türkiye | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Frameworks and Implementation Gaps Across EU Member States

The coexistence of different biomethane guarantee-of-origin schemes and non-interoperable registries blocks seamless cross-border certificate flows, which reduces the ability to match waste-rich regions with offtake markets and complicates regional consolidation strategies for operators working across multiple member states. Some national rules require that biomethane for blending originate domestically, which narrows market access for tradable certificates and sustains smaller local ecosystems that may not reach optimal scale for operations and financing. Countries have set widely differing biomethane targets with varied support instruments, and these asymmetries create regulatory arbitrage that tends to shift capital and fleet investments toward jurisdictions with more reliable support and clearer contract models. The 20-month window to transpose the revised Waste Framework Directive puts early movers at an advantage, while lagging regions will need to compress planning, procurement, and rollout, potentially raising contractor premiums and execution risk for separate collection systems. Differences in definitions and calculation methods reduce comparability of recycling rates and performance metrics, which complicates benchmarking and can distort the perceived success of collection strategies.

High Infrastructure Investment Needs for Vehicles and Facilities

European circular economy and municipal waste management initiatives highlight that the Europe Organic Waste Collection Service market grapples with significant infrastructure challenges. These challenges stem from the hefty capital investments needed for specialized collection vehicles, transfer stations, composting plants, anaerobic digestion facilities, and sorting infrastructure. Such investments weigh heavily on municipalities and private operators, especially in Eastern and Southern Europe, where waste management systems are underdeveloped.

As EU member states move towards mandatory separate bio-waste collection, demand for dedicated organic waste-handling infrastructure surges. This includes the need for temperature-controlled vehicles, smart collection systems, and decentralized treatment facilities. However, smaller municipalities and regional operators often grapple with funding constraints, hindering the pace of infrastructure deployment and service expansion.

Moreover, escalating equipment costs, limited land availability, and prolonged permitting timelines for waste treatment facilities pose significant hurdles for newcomers and limit capacity growth. Consequently, these infrastructure investment challenges are poised to be a persistent restraint on the Europe Organic Waste Collection Service market for the foreseeable future.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Pre-Consumer Food Waste Drives Dual Generation and Diversion

Food waste accounts for the largest portion of collected organics at 62.3% and is advancing at a 6.89% CAGR, which reflects how regulatory targets and biomethane economics align to prioritize high-moisture streams for digestion within the Europe organic waste collection service market[2]HyFuelUp Consortium, “State of Play of Biogas & Biomethane in Europe,” HyFuelUp, hyfuelup.eu. The household share of EU food waste remains elevated, so municipalities need to maintain route flexibility and contamination control even as targets drive prevention programs, since collections must still capture residuals at high quality for downstream processing. Member-state adaptations will blend donation incentives with energy recovery structures, yet reliable collection remains central to energy targets tied to REPowerEU, which tightens links between bins, trucks, and biomethane capacity planning. Yard and landscape waste tends to follow seasonal patterns and often routes to composting, while emerging projects demonstrate potential for advanced pre-treatment to boost gas yields where digestion is selected. Agricultural residues continue to expand as digestion substrates, yet many of these flows are captured by farm-scale assets that sit outside municipal contracts, which moderates the influence of these streams on urban collection routes tied to the Europe organic waste collection service market.

Within food waste, pre-consumer fractions from processing and manufacturing can be more concentrated and predictable, which reduces contamination risk and aligns with offtake planning for digestion and composting under strict quality standards. Member-state moves toward pay-as-you-throw for non-households build incentives for pre-consumer generators to adopt quality controls at the source, which supports higher yields and fewer rejects across the chain. Municipalities are testing transparent labeling and citizen-facing digital tools to guide correct set-outs, which is essential to maintain marketability of compost and biogas products that depend on low impurity levels. Policy debates continue on the balance between donation and energy recovery, and operators need to align collection contracts with prevention targets to avoid unintended shifts that send edible food into digestion pathways. The Europe organic waste collection service market size linked to food waste is supported by the intersection of regulation, infrastructure rollout, and the growing monetization opportunities in biomethane and compost streams under quality-first programs.

By End-User: Commercial Food Service Growth Outpaces Residential Base

Residential users held 54.8% share in 2025 as municipalities expanded door-to-door programs, while commercial food service is projected to post a 7.62% CAGR as retail and hospitality adapt to reduction targets and strengthen participation in separate collection across the Europe organic waste collection service market. The residential base requires sustained education and contamination management since households generate much of the EU’s food waste, and performance depends on easy-to-use containers, reliable schedules, and clear feedback that corrects sorting behavior. Municipalities are rolling out updated labeling and online dashboards that record set-out quality and share images from operator inspections, which improves trust and gives citizens the tools to adjust practices in real time. In the commercial food service segment, integrated bins with RFID and dynamic weighing support pay-as-you-throw tariffs and strengthen compliance, while enabling auditors to map contamination to particular sites or shifts. Under Extended Producer Responsibility frameworks, related waste streams are being aligned to broader circular initiatives, and operators that offer integrated compliance services can capture more wallet share across categories for the Europe organic waste collection service market.

Industrial facilities contribute to pre-consumer organic outputs and often require tailored logistics and contamination controls, so operators serving these sites are embedding verification tools and reporting modules that integrate with client environmental management systems. On-site processing technologies that reduce volume and stabilize organic matter are gaining attention as complements to off-site collection, and cases show reductions in handled volume and greenhouse gas footprints when biodigesters are deployed correctly. Regional differences persist in participation and readiness, with lagging separate collection rates tied to financial and administrative constraints that limit the speed of high-quality rollout. Service models that combine route reliability with clean bin programs and responsive citizen feedback loops are proving essential to narrowing the gap between policy ambition and day-to-day set-out behavior, which directly supports growth in the Europe organic waste collection service market.

By Collection Method: Door-to-Door Dominance Faces Automation Pressure

Door-to-door accounted for 72.4% share and is growing at a 7.91% CAGR, supported by the separate bio-waste collection requirement and the move toward punctual tariffs that reward correct sorting within the Europe organic waste collection service market. Vehicle bodies with integrated RFID and dynamic weighing capture container-level data and automate billing, which is especially useful for dense urban zones and narrow streets where smaller electric trucks are entering service. Bring systems remain critical for low-density areas and are enhanced by a network of civic amenity sites where residents can deliver organics and related materials on flexible schedules, though coverage gaps correlate with low composting rates in some countries. Smart solar-compacting bins and monitored semi-underground containers allow high-traffic locations to be serviced less frequently without risking overflows, and integration with route software reduces fleet miles and emissions. European municipal contracts are also piloting mixed-fleet rollouts that combine conventional refuse trucks with electric units tailored for city centers, aligning with net-zero objectives while preserving reliability on outer routes.

Container-level RFID deployment at large scale is proving that predictive routing supported by sensor data reduces driving distance and improves service verification, helping municipalities enforce contamination rules and optimize cost-to-serve. Route engineering based on academic algorithms is demonstrating potential to eliminate daily vehicles by smoothing route loads across rear- and side-loader fleets, which further supports decarbonization goals under electrified fleets. Automated alerting through container trackers has allowed some operators to shift from fixed schedules to on-demand collection for specific streams like glass, which consolidates trips and raises truck utilization. Bringing these elements together, door-to-door remains the anchor of municipal service while sensor-enabled bring systems, dynamic route design, and specialized electric vehicles create a blended model that can defend share against automation constraints and labor scarcity in the Europe organic waste collection service market.

By Technology & Equipment: Semi-Automated Systems Dominate Amid Automation Transition

Semi-automated systems held 64.7% share in 2025 as operators balance labor flexibility with efficient loading through rear- and side-loader bodies, while the fully automated category is growing at 8.49% CAGR as labor markets tighten and safety considerations gain weight in procurement. Electric refuse trucks are being configured with varied bodies to handle household and commercial routes, and procurement waves in leading cities show that emission-reduction timelines are pulling forward total cost of ownership inflection points under predictable densities. Operators are integrating electronic identification, dynamic weighing, and real-time telemetry to build reliable billing and compliance records, which help municipalities manage pay-as-you-throw models and contamination penalties. Access control platforms with card and smartphone logins are also advancing, enabling tailored tariffs by property type and tracking container-level interactions across large service footprints. Together, these technologies support predictable flows and lower unit costs, which stabilize the Europe organic waste collection service market as volumes shift under prevention and recycling targets.

At the same time, on-site biodigesters are gaining traction as complements in commercial and industrial settings where volume reduction can sharply reduce off-site collection needs, enabling operators to focus fleets on areas with the greatest route density while still managing organics responsibly. Mixed-order fleet rollouts remain common in procurement programs that must maintain service reliability through transition, and recent orders demonstrate continued momentum for battery-electric chassis designed for city operations. Municipalities are also establishing depot charging capacity and energy management systems to support electric fleets, and these investments are converging with vehicle deliveries due from 2026 onward under multi-year programs that will influence route design and maintenance practices. As these technologies diffuse, the Europe organic waste collection service industry will see continued upgrades in identification, weighing, and access control, which underpin pricing reforms and quality enforcement that are key to downstream digestion and compost performance.

Geography Analysis

Germany led with a 24.2% share in 2025, supported by extensive biogas expertise and numerous upgrading plants, although policy instability has slowed momentum compared with other countries that have adopted clearer procurement and certification models for biomethane[3]European Biogas Association, “European Biomethane Capacity Hits 7 Bcm,” European Biogas Association, europeanbiogas.eu. France’s policy model and certificate obligations have boosted biomethane output and plant counts, reinforcing organic collection growth within a framework that supports long-term offtake certainty. Italy’s rapid expansion from a low base and the scale of support mobilized through national and EU channels has encouraged grid-injection investments that improve route monetization prospects when quality standards are met. The Europe organic waste collection service market size connected to these core geographies is benefiting from clear linkages between separate collection obligations, biomethane offtake, and grid readiness, supported by targeted financing.

In the United Kingdom, municipal electrification pilots and large-scale investments by leading operators signal an aggressive shift toward low-emission fleets and integrated treatment capacity, with recent project announcements indicating multi-year timelines through 2028 and beyond for operational readiness. Denmark’s high biomethane grid penetration and large average plant size anchor confidence in feedstock procurement where separate collection has matured, which encourages steady investments in routes and contamination control. The Netherlands continues to digitize container identification and route telemetry in support of pay-as-you-throw and granular service verification, while national certificate limits for imports reinforce the need to maintain dependable domestic organics flows. Spain is positioned for faster growth with plants in development, and grid-injection financing indicates longer-term support to align collection improvements with offtake targets for biomethane.

Eastern and Southern Europe are addressing significant capacity deficits and participation gaps in separate collection, with Bulgaria, Cyprus, and Croatia showing limited organics treatment and high landfill shares that constrain biomethane scale-up linked to municipal routes. Romania’s policymaking still needs to advance to unlock biomethane deployment and guarantee-of-origin systems that support cross-border trade, and this affects investor confidence in collection route expansions that depend on predictable offtake contracts. Portugal has set biomethane replacement targets and mobilized capital through recovery plans, yet operational grid-injection remains nascent, which explains why collection improvements must be paced with facility completion and commissioning. Ukraine’s early steps on biomethane deployment and EU partnership signals show emerging regional potential in the long term, though near-term implications for municipal organics remain limited by broader infrastructure and geopolitical constraints. These geographic patterns underscore that the Europe organic waste collection service market share and growth trajectory are bound to national transposition timelines, financing access, and the readiness of grid-injection and treatment assets to absorb high-quality organics at scale.

Competitive Landscape

Competition reflects national policy asymmetries, with regional oligopolies forming around countries that have consistent support frameworks, reliable certificate systems, and clear transposition schedules for separate bio-waste collection. Vertically integrated players that combine collection with sorting, digestion, composting, and energy recovery capture more value per ton and defend margins by internalizing quality and contamination controls within their own chains. Operators are also differentiating through digital platforms that automate compliance documentation, integrate with sensors to trigger automatic pick-up requests, and create customer interfaces that reduce manual errors in scheduling and reporting. Together, these models show that the Europe organic waste collection service market is defined by a blend of asset-heavy integrated chains and asset-light digital specialists who enable municipalities and enterprises to meet policy-driven milestones.

Technology suppliers and municipal operators are expanding pilot deployments into full-scale programs, such as citywide RFID-tagging of bins and monitored networks of semi-underground containers, which tighten feedback loops between set-out behavior, service, and tariffs. Strategic investments by industry players in waste-to-energy, biomethane integration, and advanced recycling platforms broaden the value capture beyond municipal organics, which increases resilience against policy shifts or seasonal variations in feedstock. Structured financing from EU-level banks into grid-injection and biomethane plant portfolios signals that lenders are comfortable underwriting proven technologies and integrated portfolios, a trend that is constructive for operators who can demonstrate quality-controlled collection inputs. These moves, coupled with municipal electrification and digital route optimization, favor companies that align route economics to downstream energy revenues in the Europe organic waste collection service market.

Examples of strategic moves include Rotterdam’s 2026-bound deployment of 32 electric refuse trucks to support zero-emission goals, which sets a benchmark for fleet transition planning and depot readiness in dense urban markets. In Greece, large municipal orders for specialized electric chassis with integrated weighing and RFID systems reflect the push to modernize operations and harmonize quality enforcement with decarbonization objectives. In Sweden, a leading operator’s multi-depot charging plan and additional electric truck procurement underscore the momentum for city-optimized electric platforms custom-built for waste collection duty cycles. These developments exemplify how technology, financing, and policy combine to shape competitive positioning across the Europe organic waste collection service market.

Europe Organic Waste Collection Services Industry Leaders

AEB Amsterdam

Afvalzorg

ALBA Group

Attero

Avalex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Contarina updated its door-to-door collection reporting system with new adhesive labels and an IT portal that allows citizens to view detailed set-out quality reports and images to improve sorting practices and service outcomes.

- November 2025: Interzero expanded its all-in-one service for CENTERSHOP in Austria, managing EPR licensing and installing presses to reduce waste volume, transport frequency, and create additional revenue from recyclable fractions.

- October 2025: Interzero’s Waste Platform won the Golden Innovation Award for full BDO integration and logistics automation features like 24/7 remote pickup ordering, reducing manual errors and saving significant staff time for users.

- September 2025: Indaver launched its Plastics2Chemicals installation in Antwerp with 26 kT annual capacity using thermal depolymerization, broadening circular feedstock coverage beyond organics and deepening portfolio resilience.

Europe Organic Waste Collection Services Market Report Scope

| Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste |

| Agricultural Residues |

| Others |

| Residential |

| Commercial (HoReCa, Retail) |

| Industrial (Food Processing & Manufacturing) |

| Others (Agri-waste) |

| Door-to-Door Collection |

| Drop-Off / Bring Systems |

| Others |

| Manual Collection Systems |

| Semi-Automated Systems |

| Fully Automated Systems |

| Others |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Waste Type | Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste | |

| Agricultural Residues | |

| Others | |

| By End-User | Residential |

| Commercial (HoReCa, Retail) | |

| Industrial (Food Processing & Manufacturing) | |

| Others (Agri-waste) | |

| By Collection Method | Door-to-Door Collection |

| Drop-Off / Bring Systems | |

| Others | |

| By Technology & Equipment | Manual Collection Systems |

| Semi-Automated Systems | |

| Fully Automated Systems | |

| Others | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe organic waste collection service market size and growth outlook to 2031?

The Europe organic waste collection service market size was USD 3.25 billion in 2025 and is projected to reach USD 4.57 billion by 2031 at a 5.89% CAGR.

Which collection method leads in Europe and how fast is it growing?

Door-to-door collection leads with a 72.4% share and is growing at a 7.91% CAGR, driven by the separate bio-waste collection mandate and quality-linked tariffs.

Which end-user segments are most important for organic waste collection growth?

Residential remains the base with 54.8% share, while commercial food service shows the fastest growth with a 7.62% CAGR due to 2030 reduction targets.

What role does biomethane policy play in Europe’s organic waste collection?

REPowerEU’s biomethane goals and certificate frameworks connect high-quality organics collection to grid-injection investments and long-term offtake stability.

Which technologies are changing route economics in organics collection?

RFID-enabled bins, container sensors, access control, dynamic weighing, and battery-electric refuse trucks are reducing kilometers, improving compliance, and lowering lifecycle costs.

Where are the strongest growth opportunities by country?

Germany leads by share, while Spain and parts of Southern Europe hold higher growth potential as targets, financing, and permitting pipelines align with new collection capacity.

Page last updated on: