Europe Medical Equipment Maintenance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

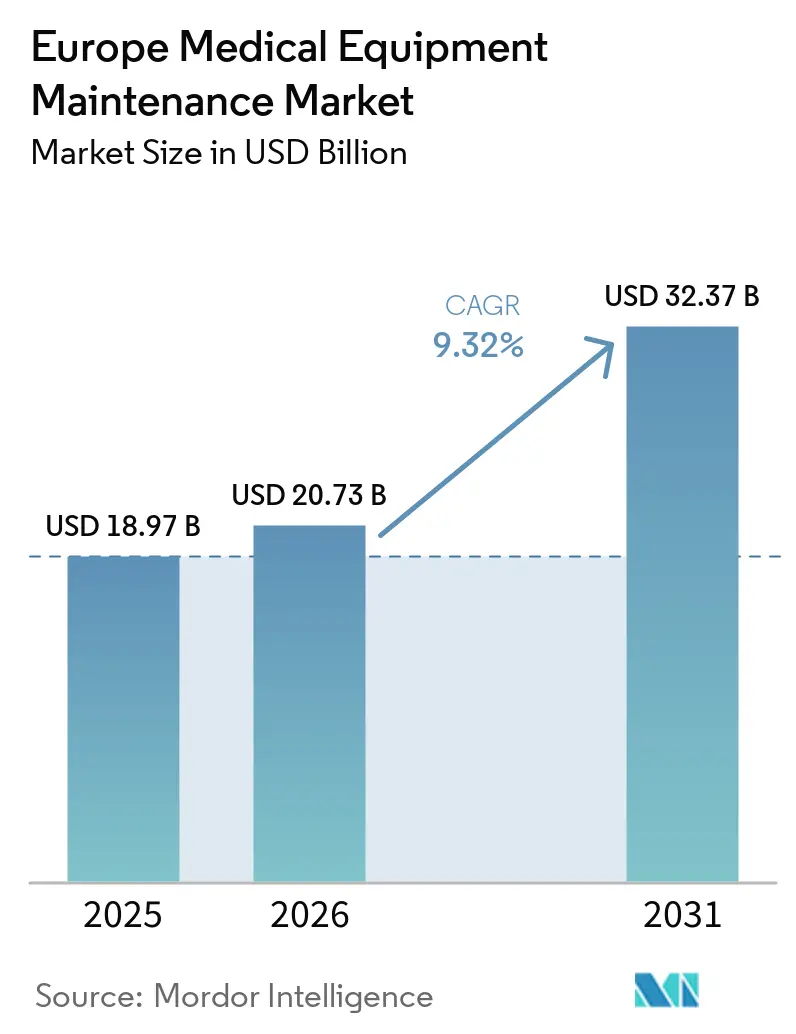

| Base Year Market Size (2025) | USD 18.97 Billion |

| Market Size (2026) | USD 20.73 Billion |

| Market Size (2031) | USD 32.37 Billion |

| Growth Rate (2026 - 2031) | 9.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medical Equipment Maintenance Market Analysis by Mordor Intelligence

The Europe Medical Equipment Maintenance Market size is expected to increase from USD 18.97 billion in 2025 to USD 20.73 billion in 2026 and reach USD 32.37 billion by 2031, growing at a CAGR of 9.32% over 2026-2031.

Hospitals in Europe are managing a growing base of imaging, surgical, and life-support systems, with many aging assets requiring more frequent servicing. Software-driven services are also increasing due to the rising importance of remote diagnostics, firmware updates, and condition monitoring under EU medical device compliance and cybersecurity requirements. OEMs dominate service delivery by controlling proprietary parts, firmware access, and remote connectivity. However, independent providers are gaining traction as hospitals adopt multi-vendor coverage for non-imaging assets and older equipment. Regulatory demands, budget constraints, digital service adoption, and outpatient care expansion are driving sustained growth in the Europe medical equipment maintenance market.

Key Report Takeaways

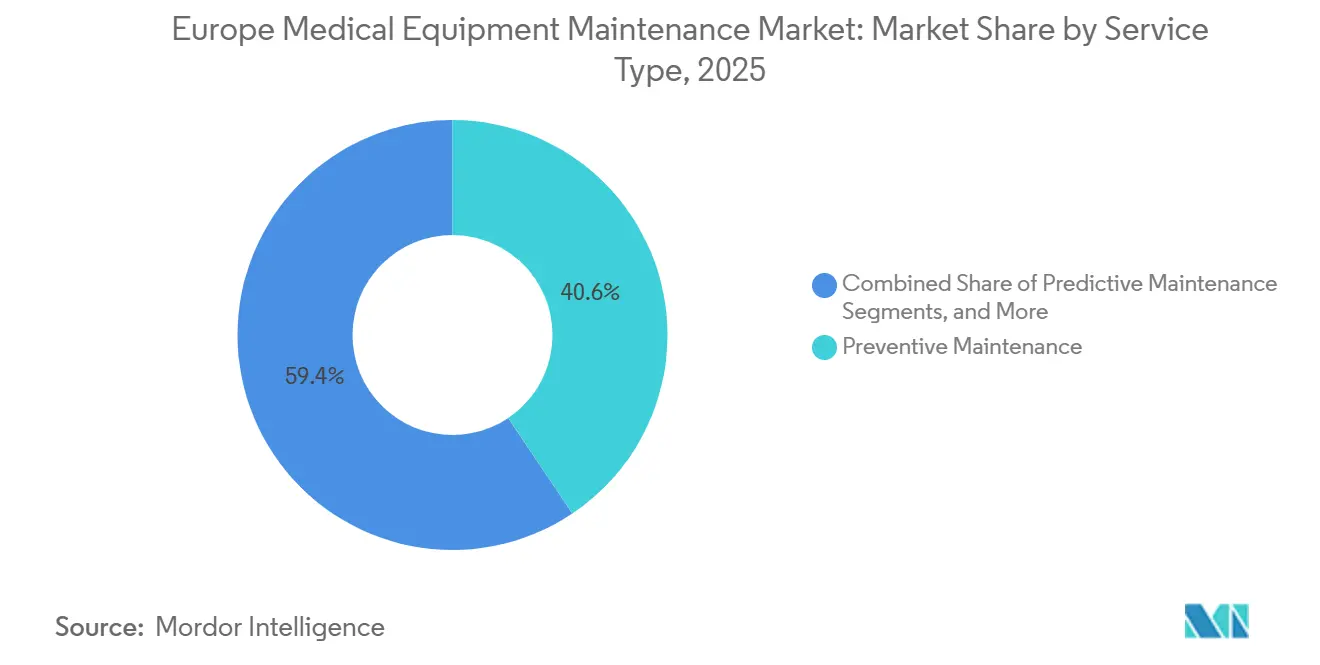

- By service type, preventive maintenance held 40.56% revenue share in 2025, while predictive maintenance is projected to expand at 12.25% CAGR through 2031.

- By contract model, full-service agreements held 47.53% revenue share in 2025, while multi-vendor contracts are projected to grow at 11.85% CAGR through 2031.

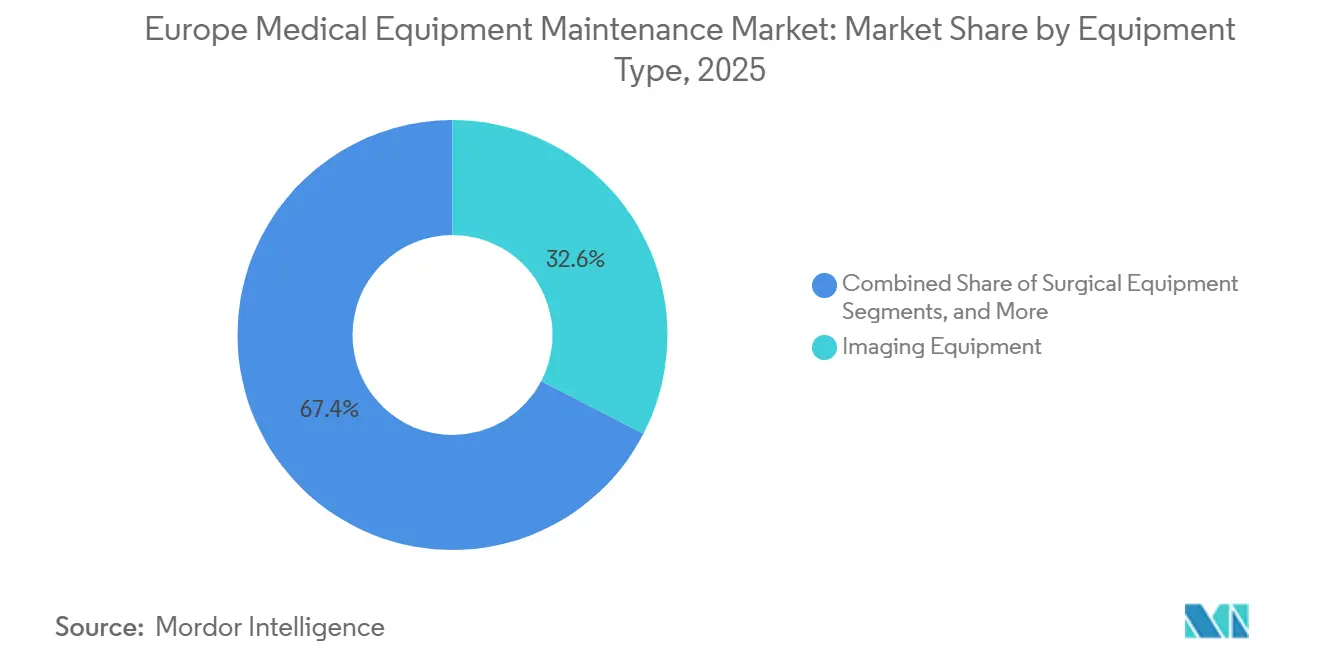

- By equipment type, imaging equipment accounted for 32.62% of the Europe medical equipment maintenance market size in 2025, while surgical equipment is projected to grow at 13.56% CAGR through 2031.

- By service provider, OEMs held 51.78% revenue share in 2025, while ISOs are projected to grow at 13.7% CAGR through 2031.

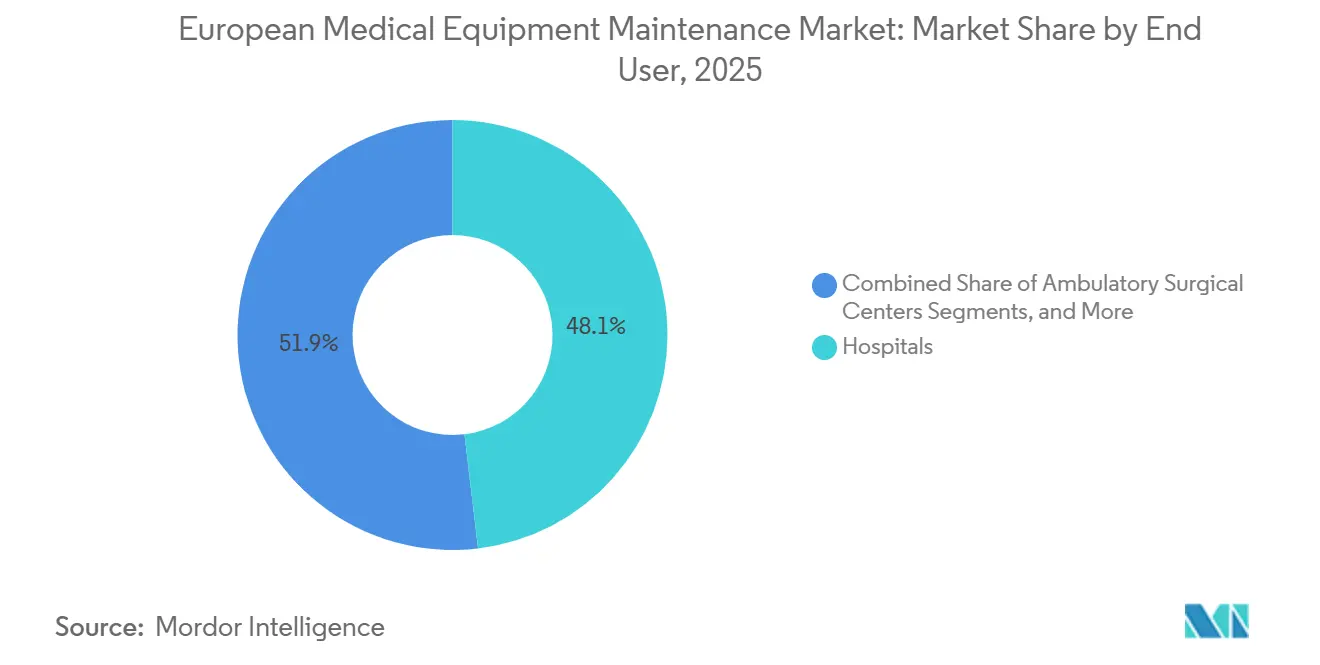

- By end user, hospitals accounted for 48.13% revenue share in 2025, while ambulatory surgical centers are projected to grow at 12.51% CAGR through 2031.

- By geography, Germany held 24.54% revenue share in 2025, while the United Kingdom is projected to grow at 14.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Medical Equipment Maintenance Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EU MDR and post-market documentation requirements | +1.5% | EU-wide mandatory compliance | Short term (≤ 2 years) |

| Rising installed base of high-uptime diagnostic equipment | +1.8% | Germany, France, Benelux, Nordics, with secondary relevance in Italy and Spain | Medium term (2-4 years) |

| Shift toward predictive and condition-based maintenance | +1.4% | DACH, the United Kingdom, and the Netherlands, with spillover to Eastern Europe | Medium term (2-4 years) |

| Hospital cost pressure supporting multi-vendor contracts | +1.2% | Spain, Italy, France, and the United Kingdom | Short term (≤ 2 years) |

| Aging equipment fleets increasing reactive service demand | +1.1% | Eastern Europe, Southern Europe, and secondary hospitals in the United Kingdom | Medium term (2-4 years) |

| Cross-border standardization of service quality | +0.9% | EU-wide, with earlier gains in Germany, France, and the Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU MDR and Post-Market Documentation Requirements

Under the EU MDR, post-market surveillance has turned routine equipment servicing into a documented compliance task across Europe's medical equipment maintenance market. Hospitals and manufacturers must maintain service histories, corrective action records, and device-level evidence to support ongoing safety and quality reviews. MDCG 2025-10 emphasizes integrating this continuous work into a formal quality management process. A December 2025 proposal adding Article 87a includes cybersecurity vulnerabilities in the reporting process, highlighting the importance of patching, firmware validation, and remote software support.[1] EUR-Lex, “Regulation (EU) 2017/745, Consolidated Text As of 1 January 2026 (CELEX 02017R0745-20260101),” EUR-Lex, eur-lex.europa.eu Hospitals are increasingly adopting structured service contracts to ensure timely compliance documentation and reduce administrative burdens, especially for higher-risk connected devices where maintenance quality and documentation are equally critical.

Shift Toward Predictive and Condition-Based Maintenance

Predictive maintenance is projected to grow at a 12.25% CAGR through 2031, making it the fastest-growing service type in Europe's medical equipment maintenance market. This growth is driven by remote monitoring, sensor data, and software tools that identify faults before they cause downtime. Siemens Healthineers reports resolving 60% of service requests remotely, reducing the need for fieldwork. Early fault detection is crucial for high-utilization systems like MRI and CT, where downtime impacts operations. Telemetry-based services also enhance provider retention, making predictive maintenance a technical and commercial advantage.

Rising Installed Base of High-Uptime Diagnostic Equipment

Europe's medical equipment maintenance market benefits from a growing installed base of advanced diagnostic systems like MRI, CT, and PET/CT, which require regular servicing. GE HealthCare operates over 3,000 specialized field service technicians across Europe, reflecting the scale of service demand. As imaging systems become more software-intensive, service requirements per device increase. Periodic validations and safety checks are essential in regions with strict biomedical standards. Robotic surgeries further drive maintenance budgets, ensuring the market's growth despite varying equipment purchasing cycles.

Aging Equipment Fleets Increasing Reactive Service Demand

Aging device fleets support Europe's medical equipment maintenance market, particularly in public systems and secondary hospitals with limited budgets. Independent firms like MIDES specialize in complex electro-medical repairs and ISO 13485-certified ultrasound probe repairs, meeting demand beyond standard OEM support. Providers like MEDSER focus on legacy Siemens CT systems, helping hospitals extend the life of older imaging assets. Selective replacement spending ensures continued demand for reactive repairs and life-extension services, supporting both emergency repairs and long-tail service opportunities outside standard OEM packages.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shortage of skilled biomedical service engineers | -1.3% | EU-wide, with stronger pressure in Eastern Europe, Spain, Italy, and the United Kingdom | Short term (≤ 2 years) |

| Cybersecurity exposure in remote diagnostics | -0.7% | EU-wide, with broader relevance across connected device environments | Medium term (2-4 years) |

| OEM lock-in and proprietary parts restrictions | -1.0% | EU-wide, strongest in DACH and the Nordics | Medium term (2-4 years) |

| Fragmented public procurement and tendering processes | -0.8% | Spain, Italy, and parts of Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Biomedical Service Engineers

The shortage of trained biomedical engineers continues to challenge the Europe medical equipment maintenance market. Servicing advanced systems like MRI, CT, and robotics requires specialized technical expertise, but the labor pool is not growing in line with the expanding installed base. Conworx reports conducting over 6,000 annual field service deployments across Germany, Switzerland, Austria, and the Benelux region, yet technician availability remains a limiting factor. This shortage drives hospitals to prioritize providers with multi-vendor management, centralized dispatch, and comprehensive training programs over cost-focused options. Larger OEM service networks, such as Siemens Healthineers, benefit from their established training infrastructure and remote support capabilities. Until the staffing pipeline improves, labor constraints will continue to restrict service coverage expansion in the region.

Cybersecurity Exposure in Remote Diagnostics

Remote diagnostics enhance equipment uptime but expose hospital networks to cybersecurity risks, posing a significant challenge in the Europe medical equipment maintenance market. Recent regulations emphasize the need for robust security measures, requiring providers to manage vulnerability reporting, secure access, and software updates effectively. Smaller ISOs, while technically proficient, often lack the necessary cybersecurity processes and documentation. Hospitals must balance the need for broader remote access with stricter network safety controls, which may delay contract decisions and raise qualification standards across the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Preventive Maintenance Holds the Base While Predictive Maintenance Expands Faster

In 2025, preventive maintenance accounted for 40.56% of service-type revenue, maintaining its position as the leading service category in Europe's medical equipment maintenance market. This reflects its role in routine calibrations, inspections, electrical safety checks, and scheduled component replacements, which align with audit-ready workflows and compliance requirements. Scheduled services offer predictable budgeting for hospitals and provide service providers with a stable renewal base compared to reactive repairs.

Predictive maintenance is projected to grow at a 12.25% CAGR through 2031, making it the fastest-growing segment in the market. Remote diagnostics and data-driven fault detection enable earlier interventions, particularly for high-utilization imaging and life-support assets. Software and firmware servicing are also gaining importance as newer devices require regular updates and performance monitoring. As hospitals adopt connected platforms, software-led service revenue is expected to grow faster than traditional repair services.

By Contract Model: Full-Service Agreements Lead While Multi-Vendor Contracts Gain Traction

Full-service agreements held 47.53% of contract-model revenue in 2025, making them the preferred structure in the market. Hospitals favor this model for high-value imaging systems due to its cost visibility, uptime commitments, and simplified compliance tracking. It is particularly effective for facilities with limited internal biomedical teams, as it consolidates parts, labor, software updates, and documentation under one contract.

Multi-vendor contracts are projected to grow at an 11.85% CAGR through 2031, reflecting hospitals' increasing preference for consolidating services across diverse device estates. These contracts simplify procurement with a single invoice, unified reporting, and consistent service levels. Time-and-material contracts remain in use for niche assets but are less attractive for larger hospitals seeking tighter budget control. Shared-service arrangements are also gaining traction in smaller regions to cover less frequently used equipment.

By Equipment Type: Imaging Equipment Leads Revenue While Surgical Equipment Grows Faster

Imaging equipment accounted for 32.62% of revenue in 2025, making it the largest category in the market. Systems like MRI, CT, PET/CT, X-ray, and fluoroscopy require regular calibration, software validation, and high-value replacement parts, ensuring consistent service demand. Maintenance for legacy X-ray and fluoroscopy systems remains significant in regions with extended replacement cycles. Life-support equipment, including ventilators and anesthesia systems, continues to require regular safety checks and planned service intervals.

Surgical equipment is expected to grow at a 13.56% CAGR through 2031, driven by the adoption of robotic surgery systems, which create ongoing maintenance needs. Contracts for robotic surgery systems highlight the recurring service requirements associated with these installations. Other categories, such as endoscopy, monitoring, and dialysis, also contribute to consistent service demand across OEM and independent channels. The market is diversifying beyond its traditional imaging-heavy focus.

By Service Provider: OEMs Still Lead While ISOs Scale Through Consolidation

OEMs held 51.78% of the market share in 2025, maintaining their leadership due to access to proprietary parts, firmware, and manufacturer-specific service protocols. Their dominance is strongest in advanced imaging and connected systems, where software control and documentation are critical. In-house biomedical teams often outsource complex tasks, reinforcing OEMs' position as trusted service providers.

ISOs are projected to grow at a 13.7% CAGR through 2031, making them the fastest-growing provider segment. Hospitals increasingly rely on ISOs for non-imaging assets, mixed fleets, and out-of-warranty equipment due to cost advantages. Larger ISO groups are scaling effectively, leveraging technician training, parts sourcing, and national coverage. As consolidation continues, procurement decisions are shifting toward commercial terms, service breadth, and contract simplicity.

By End User: Hospitals Provide the Largest Base While Ambulatory Surgical Centers Grow Faster

Hospitals accounted for 48.13% of end-user revenue in 2025, making them the largest demand center in the market. Their broad device portfolios create consistent demand for maintenance, corrective services, software updates, and documentation support. Hospitals face significant pressures around uptime and compliance, making service outsourcing a practical choice.

Ambulatory surgical centers are projected to grow at a 12.51% CAGR through 2031, driven by the shift of procedures to outpatient settings. These centers increasingly require dependable equipment uptime for advanced systems like endoscopy, digital imaging, and robotics. Diagnostic imaging centers and dialysis facilities remain stable segments, while laboratories and specialty clinics contribute to a diverse demand base, often opting for smaller service plans.

Geography Analysis

In 2025, Germany accounted for 24.54% of Europe's medical equipment maintenance market, maintaining its position as the largest national market in the region. This dominance is driven by a substantial installed base of imaging equipment and a regulatory framework prioritizing documented and scheduled maintenance activities. Germany also serves as a key testing ground for multi-vendor service structures, as hospitals manage diverse fleets from various manufacturers and emphasize traceable service processes.

The United Kingdom is projected to grow at a 14.20% CAGR through 2031, making it the fastest-growing market in Europe's medical equipment maintenance sector. NHS procurement frameworks streamline the process from specification to contract award, enabling faster execution and consistent multi-year service coverage. GE HealthCare’s January 2024 agreement with Nuffield Health, valued at GBP 200 million (approximately USD 254 million), covers around 800 devices across the UK private hospital network, showcasing the scale of managed equipment service models.

Spain and Italy remain significant mid-sized markets in Europe's medical equipment maintenance sector, despite fragmented public procurement structures. Budget pressures are prompting hospitals in both countries to explore a mix of OEM contracts, multi-vendor arrangements, and ISO-supported services for non-imaging assets. Medisolve’s expansion in Southern Europe reflects this trend, as independent players aim to build larger regional platforms to handle increased diagnostic imaging workloads. Beyond major Western European markets, the rest of Europe offers additional growth opportunities as hospitals modernize equipment and adopt service models prevalent in Germany and the UK. Growth is expected from newer connected devices, support for older fleets, and a shift toward contract-based maintenance over one-off interventions.

Competitive Landscape

In the Europe medical equipment maintenance market, no single company holds a dominant position, even though the top tier remains moderately concentrated. Major OEMs, such as Siemens Healthineers and GE HealthCare Deutschland, leverage their control over original parts, firmware access, and remote diagnostics infrastructure. This control is particularly crucial for connected imaging and surgical platforms. Meanwhile, a diverse array of regional and national ISOs populates the market's long tail, competing primarily on price, flexibility, and multi-vendor coverage. As a result, competition has evolved, emphasizing contract scope and service integration over break-fix repairs. This shift highlights a growing focus on lifecycle management, documentation support, and digital uptime tools within the Europe medical equipment maintenance landscape.

Technology is a key differentiator in Europe's medical equipment maintenance market. Siemens Healthineers resolves approximately 60% of service requests remotely through its service infrastructure, reducing site visits and accelerating hospital response times. Similarly, GE HealthCare employs tiered service structures to enhance uptime commitments and monitoring across varied equipment environments. Hospitals relying on device telemetry and remote support are less likely to switch providers quickly. Regulatory documentation and cybersecurity requirements further strengthen this advantage, making software control as critical as field engineering in ensuring service quality.

Independent providers are scaling operations to compete effectively. Medisolve's acquisition of CEDYT in Spain in March 2026 followed earlier moves, including Sincronis's September 2025 acquisition of Logic S.r.l. and Polygon Group's October 2025 majority stake in HCE, reflecting rapid consolidation within the ISO layer. Additionally, GE HealthCare's January 2024 agreement with Nuffield Health and Siemens Healthineers' June 2026 fluoroscopy maintenance contract in Hull demonstrate how leading companies secure recurring service revenue through long-term contracts. Opportunities remain in out-of-warranty imaging support, software compliance, and outpatient service bundles, where standardized OEM offerings may lack cost-effectiveness or specificity. This leaves the Europe medical equipment maintenance market with a strong top tier, yet open to challenges from focused independent players in niche segments.

Europe Medical Equipment Maintenance Industry Leaders

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Medtronic plc

FUJIFILM Holdings Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Siemens Healthineers secured a 10-year, GBP 331,632 (USD 444,980.50) maintenance contract for the Artis Zee Multipurpose Fluoroscopy Imaging System at Castle Hill Hospital, effective June 2026 to June 2036.

- March 2026: Medisolve acquired a majority stake in Spain's CEDYT S.A., expanding its maintenance portfolio to over 3,600 diagnostic imaging devices and achieving group revenues of EUR 180 million (USD 173 million).

- December 2025: The Medical Device Coordination Group issued MDCG 2025-10, emphasizing evidence-based maintenance documentation and post-market surveillance for medical devices and in vitro diagnostics.

- October 2025: Polygon Group acquires a majority stake in HCE, strengthening its position in high-tech imaging equipment maintenance in Southern Europe.

Europe Medical Equipment Maintenance Market Report Scope

As per the scope of the report, medical equipment maintenance is the routine care, safety checks, and repairs done on healthcare machines (like X-ray machines or heart monitors). It keeps them working well. This prevents sudden breakages, ensures accurate test results, and keeps patients safe.

The Europe medical equipment maintenance market is segmented by service type, contract model, equipment type, service provider, end-user, and geography. By service type, the market includes preventive maintenance, corrective maintenance, operational maintenance, predictive maintenance, and software and firmware updates. By contract model, the market is segmented into full-service agreements, shared-service agreements, time and material contracts, and multi-vendor contracts. By equipment type, the market is categorized into imaging equipment (magnetic resonance imaging (MRI), computed tomography (CT), X-ray and fluoroscopy systems, ultrasound systems, and nuclear medicine and PET systems), surgical equipment (electrosurgical devices, robotic surgical systems, and minimally invasive surgical devices), life-support equipment (ventilators and anesthesia machines), and other medical equipment (endoscopic devices, patient monitoring systems, and dialysis equipment). By service provider, the market is segmented into original equipment manufacturers, independent service organizations, and in-house biomedical teams. By end-user, the market is segmented into hospitals, diagnostic imaging centers, ambulatory surgical centers, dialysis centers, laboratories, dental and specialty clinics, and others. By geography, the market is analyzed across Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Preventive Maintenance |

| Corrective Maintenance |

| Operational Maintenance |

| Predictive Maintenance |

| Software and Firmware Updates |

| Full-Service Agreements |

| Shared-Service Agreements |

| Time and Material Contracts |

| Multi-Vendor Contracts |

| Imaging Equipment | Magnetic Resonance Imaging (MRI) |

| Computed Tomography (CT) | |

| X-Ray and Fluoroscopy Systems | |

| Ultrasound Systems | |

| Nuclear Medicine and PET Systems | |

| Surgical Equipment | Electrosurgical Devices |

| Robotic Surgical Systems | |

| Minimally Invasive Surgical Devices | |

| Life-Support Equipment | Ventilators |

| Anesthesia Machines | |

| Other Medical Equipment | Endoscopic Devices |

| Patient Monitoring Systems | |

| Dialysis Equipment |

| Original Equipment Manufacturers |

| Independent Service Organizations |

| In-House Biomedical Teams |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Dialysis Centers |

| Laboratories |

| Dental and Specialty Clinics |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Service Type | Preventive Maintenance | |

| Corrective Maintenance | ||

| Operational Maintenance | ||

| Predictive Maintenance | ||

| Software and Firmware Updates | ||

| By Contract Model | Full-Service Agreements | |

| Shared-Service Agreements | ||

| Time and Material Contracts | ||

| Multi-Vendor Contracts | ||

| By Equipment Type | Imaging Equipment | Magnetic Resonance Imaging (MRI) |

| Computed Tomography (CT) | ||

| X-Ray and Fluoroscopy Systems | ||

| Ultrasound Systems | ||

| Nuclear Medicine and PET Systems | ||

| Surgical Equipment | Electrosurgical Devices | |

| Robotic Surgical Systems | ||

| Minimally Invasive Surgical Devices | ||

| Life-Support Equipment | Ventilators | |

| Anesthesia Machines | ||

| Other Medical Equipment | Endoscopic Devices | |

| Patient Monitoring Systems | ||

| Dialysis Equipment | ||

| By Service Provider | Original Equipment Manufacturers | |

| Independent Service Organizations | ||

| In-House Biomedical Teams | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Dialysis Centers | ||

| Laboratories | ||

| Dental and Specialty Clinics | ||

| Others | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the 2031 outlook for medical equipment maintenance in Europe?

The sector is projected to reach USD 32.37 billion by 2031 from USD 20.73 billion in 2026, growing at a CAGR of 9.32%.

Which service type currently leads revenue in Europe?

Preventive maintenance led with 40.56% of service-type revenue in 2025 because hospitals still rely on planned servicing, safety checks, and compliance documentation.

Which part of the region is expanding the fastest?

The United Kingdom is forecast to grow at 14.20% CAGR through 2031, supported by framework-led procurement and multi-year service contracts.

Why are OEMs still ahead of independent service providers?

OEMs held 51.78% revenue share in 2025 because they control proprietary parts, firmware access, remote diagnostics, and service documentation support.

What is driving faster growth in surgical equipment maintenance?

Surgical equipment is projected to grow at 13.56% CAGR through 2031 as robotic surgery systems create recurring maintenance demand from installation onward.

Which end users are creating the strongest future demand?

Hospitals remained the largest end-user group with 48.13% revenue share in 2025, while ambulatory surgical centers are growing fastest at 12.51% CAGR through 2031.

Page last updated on: