Predictive Maintenance For MedTech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

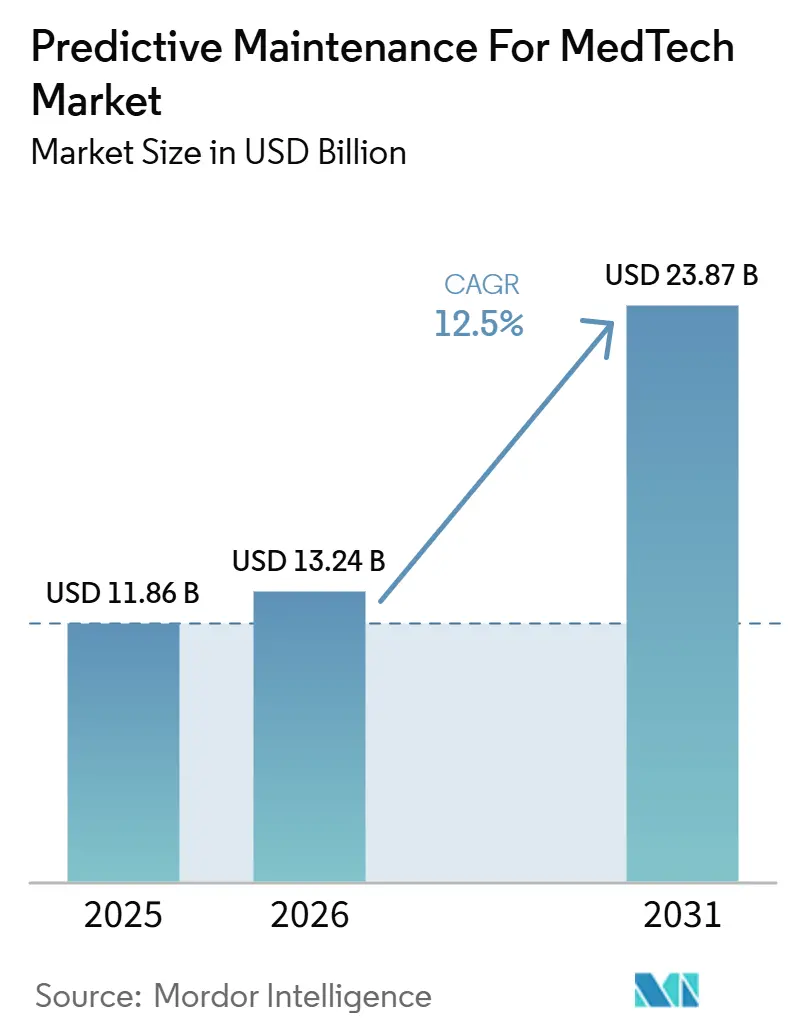

| Market Size (2026) | USD 13.24 Billion |

| Market Size (2031) | USD 23.87 Billion |

| Growth Rate (2026 - 2031) | 12.50% CAGR |

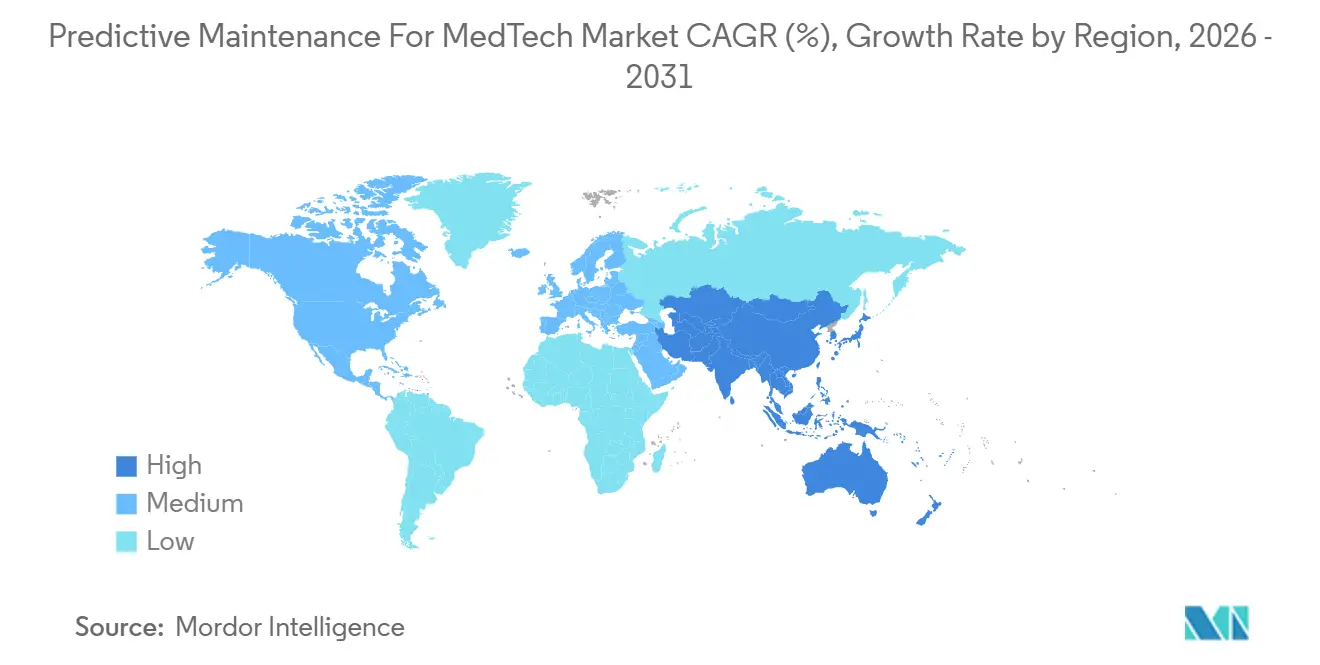

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

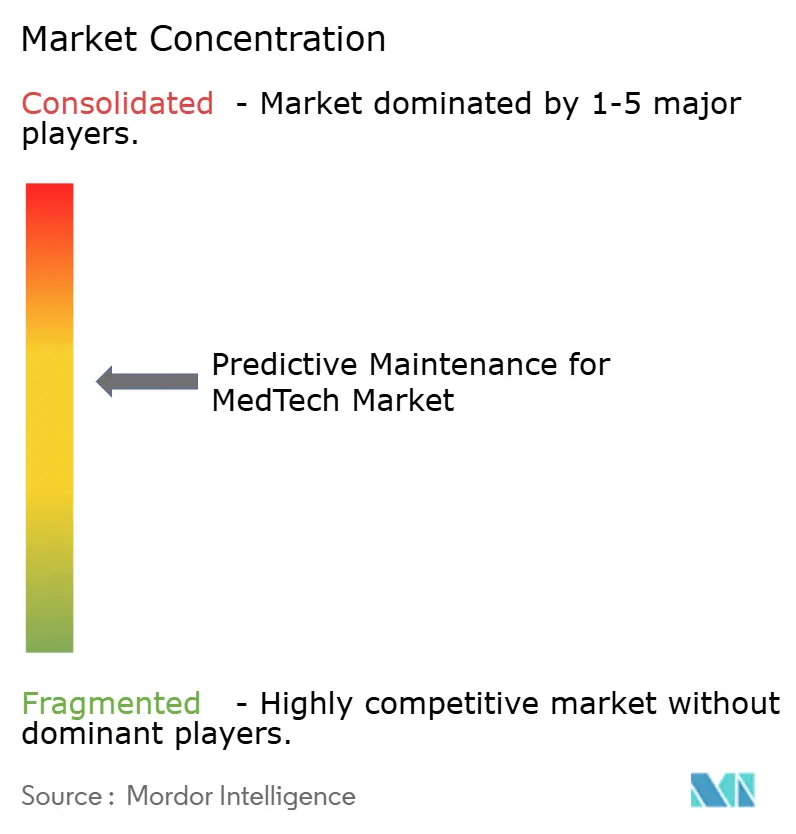

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Predictive Maintenance For MedTech Market Analysis by Mordor Intelligence

The Predictive maintenance for MedTech market is projected to expand from USD 11.86 billion in 2025 and USD 13.24 billion in 2026 to USD 23.87 billion by 2031, registering a CAGR of 12.50% between 2026 to 2031. The market is moving away from calendar-based maintenance because hospitals now manage large fleets of connected assets that generate enough operating data for condition-based intervention. That shift is becoming more urgent as biomedical engineering teams face heavy workloads and must maintain larger numbers of devices across imaging, monitoring, laboratory, and therapy settings, which raises the value of automated prioritization and early fault detection. Competitive activity is also broadening because OEMs, cloud platforms, independent service providers, and focused analytics vendors each control different parts of the service stack, from raw telemetry to workflow integration. North America remains the largest demand center because health systems there have dense connected infrastructure and mature service ecosystems, while Asia-Pacific is expanding faster as hospital digitization creates demand for fleet-level equipment intelligence. The growth path for the market remains favorable, but the pace at which vendors solve interoperability and deployment economics will continue to shape how much value each player captures.

Key Report Takeaways

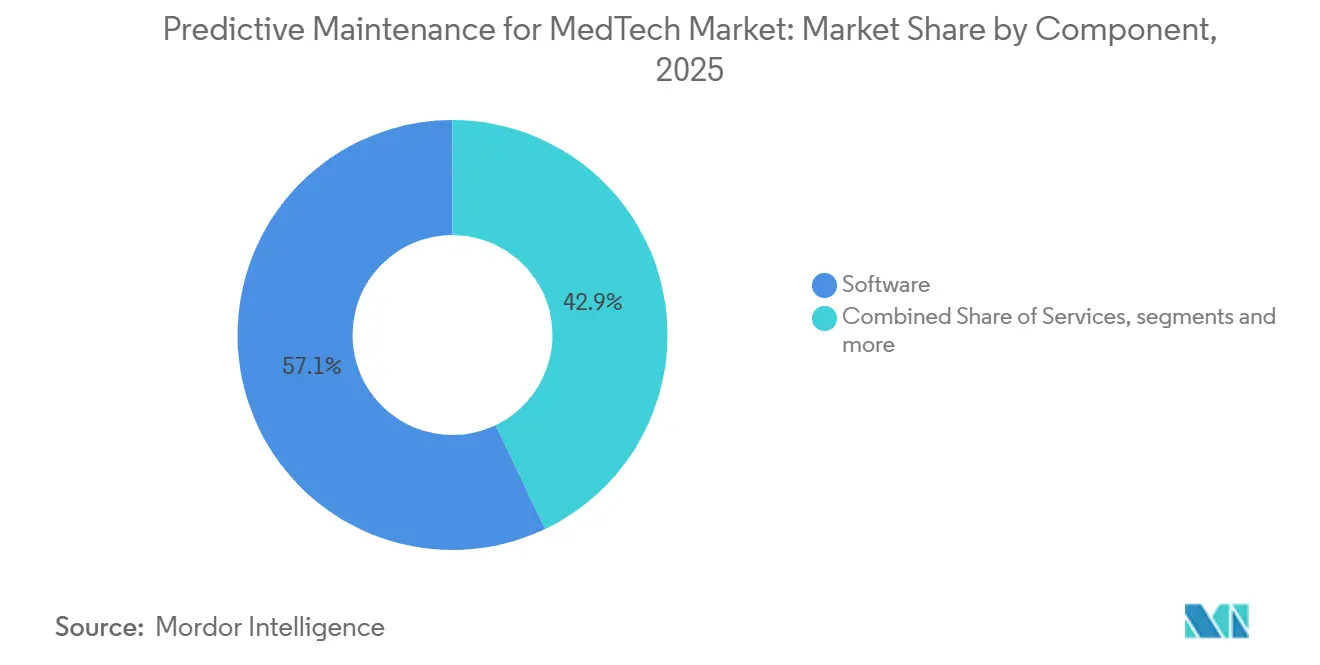

- By component, software led with 57.11% revenue share in 2025, while services recorded the highest projected CAGR at 12.93% through 2031.

- By deployment mode, cloud-based deployment held 58.71% market share in 2025, while hybrid deployment mode is expected to be the fastest-growing segment with a projected CAGR at 12.86% through 2031.

- By organization size, large enterprises held 61.17% revenue share in 2025, while small and medium enterprises posted the highest projected CAGR at 13.28% through 2031.

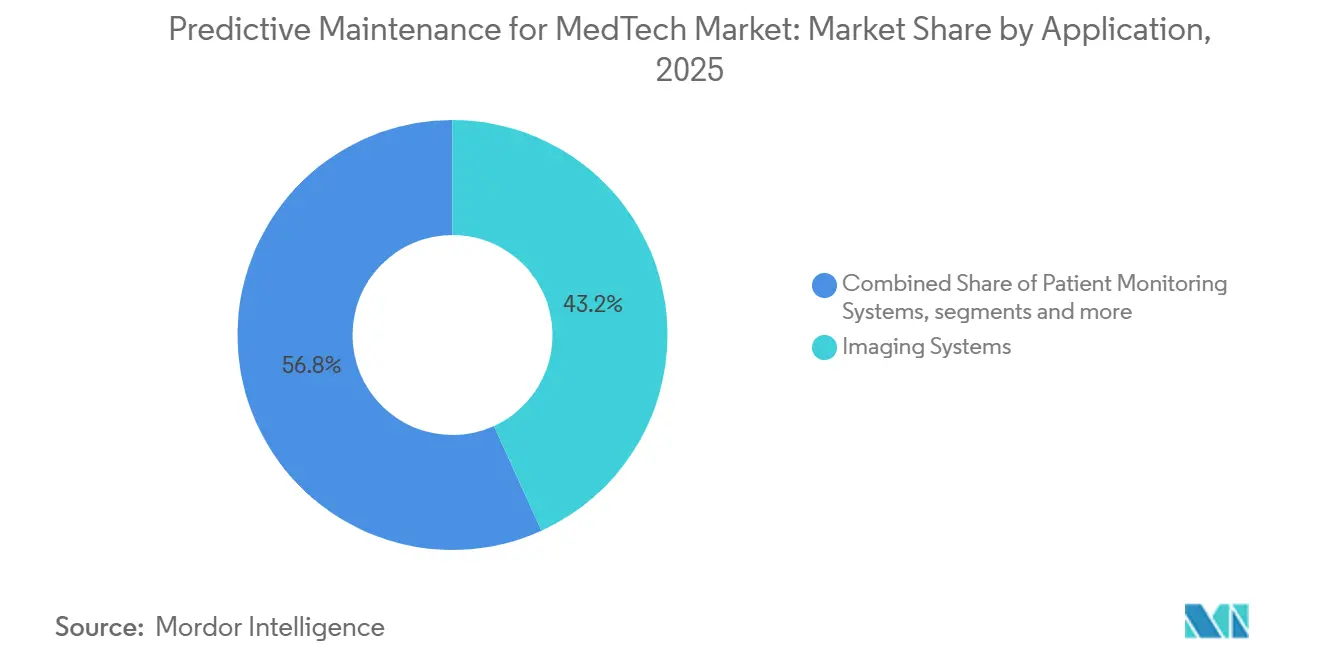

- By application, imaging systems accounted for 43.17% revenue share in 2025, while patient monitoring systems are forecasted to expand at a 13.37% CAGR through 2031.

- By end-user, hospitals held 45.21% revenue share in 2025, while clinics and specialty centers recorded the highest projected CAGR at 13.33% through 2031.

- By geography, North America held 49.35% share in 2025, while the Asia-Pacific is forecasted to grow at a 14.48% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Predictive Maintenance For MedTech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Installed Base of Connected Medical Equipment | +2.8% | Global, led by North America and APAC | Medium term (2-4 years) |

| Escalating Downtime Cost and Service-Level Pressure in Hospitals | +2.3% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Expansion of Remote Device Monitoring and Cloud-Connected Service Models | +2.1% | North America & Europe, spill-over to APAC | Medium term (2-4 years) |

| AI Model Maturation for Anomaly Detection on Medical Assets | +1.9% | Global, concentrated in North America | Medium term (2-4 years) |

| Underused Service Telemetry from Multi-Vendor Fleets | +1.6% | North America & Europe | Long term (≥ 4 years) |

| Cyber-Resilient Edge Analytics for Regulated Device Environments | +1.4% | Global, with regulatory push concentrated in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Installed Base of Connected Medical Equipment

The predictive maintenance for MedTech market is gaining momentum because connected clinical assets now produce a steady stream of operating data instead of isolated fault codes, which makes failure detection more precise and more useful in daily service planning. A 500-bed hospital in 2026 operates 15,000 to 20,000 connected medical devices, and that scale has changed maintenance from an equipment task into a fleet management problem that requires constant prioritization.[1]GE HealthCare, “Beyond Downtime, Redefining Predictive Medical Equipment Maintenance,” GE HealthCare Insights, gehealthcare.comStaffing constraints add more pressure because the same source notes that the U.S. labor pipeline remains far smaller than projected biomedical equipment technician demand, which makes predictive automation more relevant in routine operations. Procurement patterns are also helping adoption because new medical equipment increasingly ships with embedded sensors and cloud connectivity as standard features instead of optional upgrades. That change means newer hospitals can launch the predictive maintenance for MedTech market from a stronger starting point, with cleaner telemetry and fewer retrofit projects than older facilities had to manage.

Escalating Downtime Cost and Service-Level Pressure in Hospitals

The predictive maintenance for MedTech market is also being lifted by the direct financial cost of equipment failure, which has become easier for hospital leadership to measure and link to revenue disruption. One day of unplanned MRI downtime can cost more than USD 41,000 at hospitals averaging 380 MRI procedures per month in the United States, and that loss can represent more than 15 canceled scan sessions. GE HealthCare reported that its OnWatch Predict platform reduced unplanned downtime by up to 60% and lowered customer-initiated service requests by 35%, which translated into 2.5 additional operating days per MRI system each year across 1,500 EMEA installations. This matters more as hospital groups negotiate broader service contracts with uptime commitments, because availability is no longer treated as a service aspiration and is now tied more closely to contract performance. As these expectations spread across larger care networks, the predictive maintenance for MedTech market benefits vendors that can show measurable uptime gains and connect those gains to service-level outcomes.

Expansion of Remote Device Monitoring and Cloud-Connected Service Models

The predictive maintenance for MedTech market is expanding through remote monitoring because cloud-connected service models shorten the time between anomaly detection and corrective action. Microsoft Azure Health Data Services provides standards-based infrastructure that uses FHIR and DICOM to bring different health data streams together for analytics at cloud scale, which supports broader fleet visibility in multi-device environments. As remote monitoring becomes more common, vendors can build maintenance contracts around uptime delivered instead of site visits performed, and that changes how financial risk is shared between buyer and provider. In that setting, the predictive maintenance for MedTech market tends to favor vendors with larger failure datasets and better model precision because weak models raise false alerts and increase service friction.

AI Model Maturation for Anomaly Detection on Medical Assets

The predictive maintenance for MedTech market is moving into a more advanced phase because failure prediction models are shifting from fixed thresholds to architectures that detect component degradation well before clinical disruption occurs. A 2025 framework validated on CT equipment at West China Hospital used IoMT telemetry and deep learning on millions of X-ray tube exposures to predict tube failures with actionable lead time.[2]Ran Peng et al., “AI-Driven Predictive Maintenance for Medical Imaging Equipment, A Deep Learning Framework Based on the IoMT Data,” Reliability Engineering & System Safety, sciencedirect.comThe FDA finalized its Predetermined Change Control Plan guidance in December 2024, which gives manufacturers a clearer path to pre-authorize defined future algorithm modifications within the original submission and reduces the limits that once slowed model updates. That regulatory shift matters because predictive performance improves when models can be refreshed and refined against new operating conditions instead of remaining static in the field. As vendors widen failure signature libraries across broader installed bases, the predictive maintenance for MedTech market should see more reliable alerts and more consistent performance across different device categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented OEM Data Access and Limited Interoperability | -1.8% | Global, most acute in multi-vendor hospital environments in North America and Europe | Long term (≥ 4 years) |

| High Validation Burden for Clinical-Grade Predictive Models | -1.5% | North America & EU | Medium term (2-4 years) |

| Cybersecurity and Patient-Data Governance Complexity | -1.3% | Global, compliance-driven in North America and EU | Medium term (2-4 years) |

| Long Hospital Procurement and Integration Cycles | -1.0% | Global, most pronounced in government-funded health systems in Europe and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented OEM Data Access and Limited Interoperability

The predictive maintenance for MedTech market still faces a major barrier because multi-vendor hospitals receive telemetry in proprietary formats that were built for OEM service portals rather than neutral analytics environments. A hospital that manages equipment from 5 or more manufacturers may need separate integration work for each vendor before a cross-fleet model can operate in a useful way, which extends deployment time and raises project cost. Even when access is contractually available, the most maintenance-relevant fields, including wear counters, drift indicators, and detailed error histories, are not always exposed in a complete form to third-party systems. HL7 FHIR R6 has introduced the DeviceAlert resource, which creates a formal path for device alert data inside a standardized framework, but adoption across large legacy fleets will take time.[3]HL7 International, “Medical Device Integration with FHIR, IoMT, IEEE 11073, and the New R6 DeviceAlert Resource,” FHIR R6 Implementation Guide, fhir.org Until interoperability improves further, the predictive maintenance for MedTech market will remain easier for OEM-linked solutions to scale than for independent vendors that must normalize data across competing device ecosystems.

High Validation Burden for Clinical-Grade Predictive Models

The predictive maintenance for MedTech market also grows more slowly because model development in healthcare requires more validation, traceability, and documentation than comparable industrial maintenance programs. A pilot using Microsoft Azure Databricks and SAP HANA in a regulated medical device manufacturing setting delivered a 28% reduction in unplanned downtime and a 40% improvement in audit preparation efficiency, yet the compliance architecture required for FDA CFR Part 11 deployment added substantial operational complexity. Quality management expectations under ISO 13485 and related design-control practices mean vendors must document how models are built, updated, monitored, and reviewed over time. Continuous-learning systems add another layer of burden because each retraining cycle can trigger new documentation work and slower release cycles. That burden makes it harder for smaller suppliers to scale in the predictive maintenance for MedTech market, especially when they lack the regulatory teams and established compliance workflows that larger OEM service organizations already maintain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Maintains Dominance, Services Model Restructuring

Software held 57.11% of the predictive maintenance for MedTech market share in 2025, which confirms that buyers still place the highest value on analytics layers that can sit over installed device fleets without forcing hardware replacement. In the predictive maintenance for MedTech market, software remains attractive because health systems can extend one analytics environment across imaging, patient monitoring, laboratory systems, and infusion equipment under a recurring subscription model. Hardware is the smallest revenue component because gateways, edge nodes, and connected sensors are becoming more standardized and less differentiated in price. In the predictive maintenance for MedTech industry, value is shifting toward how data is interpreted and operationalized rather than toward the physical devices that collect it.

Services are expanding faster than the overall market, with a projected 12.93% CAGR from 2026 to 2031, because many health systems prefer outsourced analytics management instead of building internal capabilities from the ground up. The predictive maintenance for MedTech market is therefore seeing services move away from one-time implementation work and toward recurring managed support tied to uptime, intervention planning, and workflow execution. As more service value becomes linked to data ownership and model performance, the predictive maintenance for MedTech market may become harder for smaller service firms to penetrate unless they can partner for telemetry access or narrow their focus to selected device classes.

By Deployment Mode: Cloud Leads, Hybrid Architecture Gaining Ground

Cloud-based deployment held 58.71% market share in 2025, which reflects strong buyer preference for elastic compute capacity, centralized model updates, and subscription pricing that converts capital spending into operating cost. The predictive maintenance for MedTech market has favored cloud adoption because high-fidelity model training needs large volumes of historical device data that many hospital-owned systems cannot process efficiently on local infrastructure. Cloud delivery also makes it easier for vendors to push model improvements, software fixes, and workflow changes across distributed fleets without waiting for site-by-site intervention.

Hybrid architecture is the fastest-growing deployment mode with an anticipated CAGR at 12.86%, because it addresses a practical gap between local control and centralized analysis in the predictive maintenance for the MedTech market. In this setup, sensitive or time-critical telemetry can be processed at the edge, while model training and fleet-wide benchmarking can still occur in the cloud. On-premise systems will continue to hold a place in locations with strict data residency expectations, but the predictive maintenance for MedTech market is increasingly moving toward architectures that combine local processing with cloud-based learning and oversight.

By Organization Size: Large Enterprises Anchor Revenue, SMEs Accelerating

Large enterprises held 61.17% of revenue in 2025 because integrated delivery networks and academic medical centers manage broad device fleets, support in-house biomedical teams, and have the procurement structure needed for long multi-year contracts. The predictive maintenance for MedTech market remains anchored by these organizations because they produce enough service and utilization data to support stronger models and more reliable fleet benchmarking. Large providers also tend to work directly with OEMs or cloud vendors on customized deployments, which gives them earlier access to integration support and more tailored workflow design.

Small and medium enterprises are projected to grow at 13.28% CAGR through 2031, the fastest among organization sizes, because subscription economics and pre-trained models have lowered the entry threshold for facilities with smaller fleets. The predictive maintenance for MedTech market is becoming more reachable for community hospitals, ambulatory surgery centers, independent imaging centers, and specialty clinics that manage fewer than 500 devices. As a result, the predictive maintenance for MedTech market is gaining another demand layer in which operational simplicity matters as much as model sophistication.

By Application: Imaging Anchors Revenue, Patient Monitoring Accelerating

Imaging systems captured 43.17% revenue share in 2025, which gave them the largest application position because these assets carry high capital value and generate direct procedure revenue that is quickly lost during downtime. In the predictive maintenance for MedTech market, imaging therefore stays central because the financial and clinical consequences of failure are immediate, visible, and easy for hospital leadership to quantify. The application also benefits from mature telemetry and long service histories, which make model training more practical than in less standardized device categories.

Patient monitoring systems are forecasted to grow at 13.37% CAGR through 2031, making them the fastest-growing application in the predictive maintenance for MedTech market. Demand is rising because connected monitors are spreading across ICU, step-down, ambulatory, and outpatient settings, which expands the installed base that requires ongoing performance oversight. Predictive approaches are useful here because they help distinguish actual equipment degradation from nuisance alarms caused by contact wear, battery decline, or firmware drift. Surgical, therapy, and sterilization equipment remain smaller categories, yet the predictive maintenance for MedTech market is gradually widening in these areas as automated tracking and documentation expectations become more demanding.

By End-User: Hospitals Anchor Market, Outpatient Settings Driving New Growth

Hospitals held 45.21% of end-user revenue in 2025 because they manage the broadest mix of clinical assets, maintain internal biomedical engineering functions, and possess the scale to negotiate long managed service agreements. The predictive maintenance for MedTech market remains centered on hospitals because they can combine fleet size, capital exposure, and compliance demands in a way that supports full enterprise deployment. Their equipment portfolios include imaging, monitoring, laboratory, therapy, and support devices, which makes a cross-fleet maintenance platform more valuable than isolated point solutions.

Clinics and specialty centers are forecasted to grow at 13.33% CAGR through 2031, making them the fastest-growing end-user group as outpatient providers formalize maintenance governance that was previously managed more informally. Diagnostic imaging centers are especially compelling because they rely on expensive imaging assets but often lack large in-house service teams, which makes subscription-based predictive support easier to justify. Ambulatory surgery centers also stand out because the consequences of device failure during a procedure create a stronger willingness to invest in uptime protection. Home healthcare remains earlier in its development, but portable ventilators, infusion pumps, and remote monitoring tools are starting to create new service needs beyond institutional facilities. That broader end-user mix gives the predictive maintenance for MedTech market a larger runway, with adoption no longer limited to the largest hospital systems.

Geography Analysis

North America held 49.35% of the predictive maintenance for MedTech market share in 2025, supported by dense connected hospital infrastructure, mature third-party service organizations, and health systems with strong multi-site procurement capacity. The United States remains the main revenue center because large hospital networks are already managing complex fleets and are under pressure to standardize documentation, uptime, and maintenance governance across many facilities.

Europe remains the second-largest regional market, with Germany, the United Kingdom, and France serving as the main demand centers because they combine large hospital systems, strict governance expectations, and strong OEM presence. Germany stands out because university hospital networks operate broad multi-modality fleets and sit close to major OEM service organizations, which creates a demanding home environment for predictive service capability. Siemens Healthineers has used its digital health platform to combine equipment utilization analytics, remote diagnostics, and protocol optimization, showing how deeply maintenance intelligence can be integrated into broader care delivery software. The United Kingdom, France, Italy, the Nordics, Poland, and the Netherlands are also advancing as procurement programs push larger care networks toward more standardized equipment management models.

Asia-Pacific is forecasted to grow at 14.48% CAGR from 2026 to 2031, which makes it the fastest-growing regional segment in the predictive maintenance for MedTech market. China, India, Japan, and South Korea are creating new demand because government-backed hospital digitization is improving the data foundation needed for fleet-level equipment intelligence. Japan also presents a strong case for predictive service adoption because the pressure to keep devices available is rising alongside the need to control maintenance costs in a mature health system. China is adding momentum as more networked medical devices move under tighter cybersecurity and maintenance governance expectations, which pushes hospitals toward more formal monitoring practices. South America and the Middle East and Africa remain smaller today, but connected hospital buildouts in Brazil, the GCC, and South Africa are setting better conditions for future adoption because telemetry capability is being specified earlier in the equipment lifecycle.

Competitive Landscape

The predictive maintenance for MedTech market is moderately concentrated because OEMs such as GE HealthCare, Siemens Healthineers, and Koninklijke Philips hold strong telemetry advantages through long device-to-cloud relationships and large installed service bases. In the predictive maintenance for MedTech market, these companies benefit from direct access to failure histories, firmware behavior, component wear patterns, and service workflows that independent vendors often cannot see at the same level of detail.

Hyperscale technology vendors, including Microsoft, IBM, Oracle, and SAP, compete from a different angle in the predictive maintenance for MedTech market because their strength lies in cloud infrastructure, data integration, regulatory tooling, and model development speed rather than in device-specific fault intelligence. Microsoft’s Azure Health Data Services supports standardized health data handling through FHIR and DICOM, which is valuable when hospitals want to unify information from many systems before applying analytics. These platform players become more relevant when buyers need broad interoperability, scalable governance, and enterprise-level compliance support across mixed device fleets.

Independent service organizations and focused analytics vendors still have room to compete, especially in interoperability, service workflow design, and lower-friction offerings for providers that do not want full OEM dependence. Their best opportunity lies in multi-vendor environments where hospitals want one operational layer across several manufacturers and care sites. This space remains difficult because data access is uneven, but it also remains important because many providers will continue to manage mixed fleets rather than single-brand infrastructures. Philips also deepened its position through the 2026 WellSpan alliance, which shows that large OEMs are expanding from equipment supply into longer-term AI-linked operating relationships. The result is a tiered market where OEM telemetry strength, cloud platform breadth, and workflow integration capability all matter, but no single group fully controls every layer of the value chain.

Predictive Maintenance For MedTech Industry Leaders

IBM

Siemens Healthineers AG

GE HealthCare

Koninklijke Philips N.V.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Siemens Healthineers and MEDIOT AI (a subsidiary of ABA Life) announced a strategic collaboration to advance AI-powered healthcare infrastructure across Africa and emerging markets, with predictive biomedical maintenance identified as a primary focus alongside smart hospital interoperability and connected care. The partnership combines Siemens Healthineers' imaging and diagnostics expertise with MEDIOT AI's sovereign AI platforms through the MEDIFUS Health Operating System.

- March 2026: Koninklijke Philips unveiled the Rembra CT system at ECR 2026 in Vienna, a next-generation radiology platform designed for acute and high-demand imaging environments, alongside the Verida spectral CT, the world's first detector-based spectral CT powered by AI across the full imaging chain, first introduced at RSNA 2025.

- February 2026: GE HealthCare launched ReadyFix in the United States, a remote fleet management solution enabling real-time device diagnostics, remote software deployment, and standardized clinical configuration management for cardiac device fleets, expanding the DeviceReady portfolio. Hospitals averaging 10-15 connected devices per bed represent the primary target environment.

Global Predictive Maintenance For MedTech Market Report Scope

According to the report’s scope, predictive maintenance for MedTech market refers to the market for software, analytics platforms, sensors, and services that use artificial intelligence (AI), machine learning, Internet of Things (IoT) data, and advanced diagnostics to predict equipment failures and maintenance needs in medical devices before they occur. These solutions help healthcare providers and MedTech companies reduce downtime, optimize asset performance, extend equipment lifespan, improve patient safety, and lower maintenance costs across medical equipment such as imaging systems, patient monitoring devices, laboratory instruments, and surgical equipment.

The predictive maintenance for MedTech market is segmented into component, deployment mode, organization size, application, end-user, and geography. By component, the market is segmented into software, services, and hardware. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By organization size, the market is segmented into large enterprises and small and medium enterprises. By application, the market is segmented into imaging systems, patient monitoring systems, laboratory diagnostics equipment, surgical and therapy devices, and sterilization and support equipment. By end-user, the market is segmented into hospitals, ambulatory surgery centers, diagnostic imaging centers, clinics and specialty centers, and home healthcare providers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Hardware |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Imaging Systems |

| Patient Monitoring Systems |

| Laboratory Diagnostics Equipment |

| Surgical and Therapy Devices |

| Sterilization and Support Equipment |

| Hospitals |

| Ambulatory Surgery Centers |

| Diagnostic Imaging Centers |

| Clinics and Specialty Centers |

| Home Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Imaging Systems | |

| Patient Monitoring Systems | ||

| Laboratory Diagnostics Equipment | ||

| Surgical and Therapy Devices | ||

| Sterilization and Support Equipment | ||

| By End-User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Diagnostic Imaging Centers | ||

| Clinics and Specialty Centers | ||

| Home Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of predictive maintenance for MedTech?

The predictive maintenance for MedTech market stands at USD 13.24 billion in 2026 and is projected to reach USD 23.87 billion by 2031 at a 12.50% CAGR.

Which component category leads revenue today?

Software leads the mix with 57.11% of revenue in 2025 because providers can add analytics across installed device fleets without replacing hardware.

Which application is growing the fastest?

Patient monitoring is the fastest-growing application, with a projected 13.37% CAGR through 2031, supported by wider deployment of connected monitors across acute and ambulatory settings.

Why is North America the largest regional contributor?

North America held 49.35% share in 2025 because it has a dense, connected hospital infrastructure, mature service ecosystems, and health systems that are already scaling centralized equipment governance.

Page last updated on: