Healthcare Equipment Leasing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

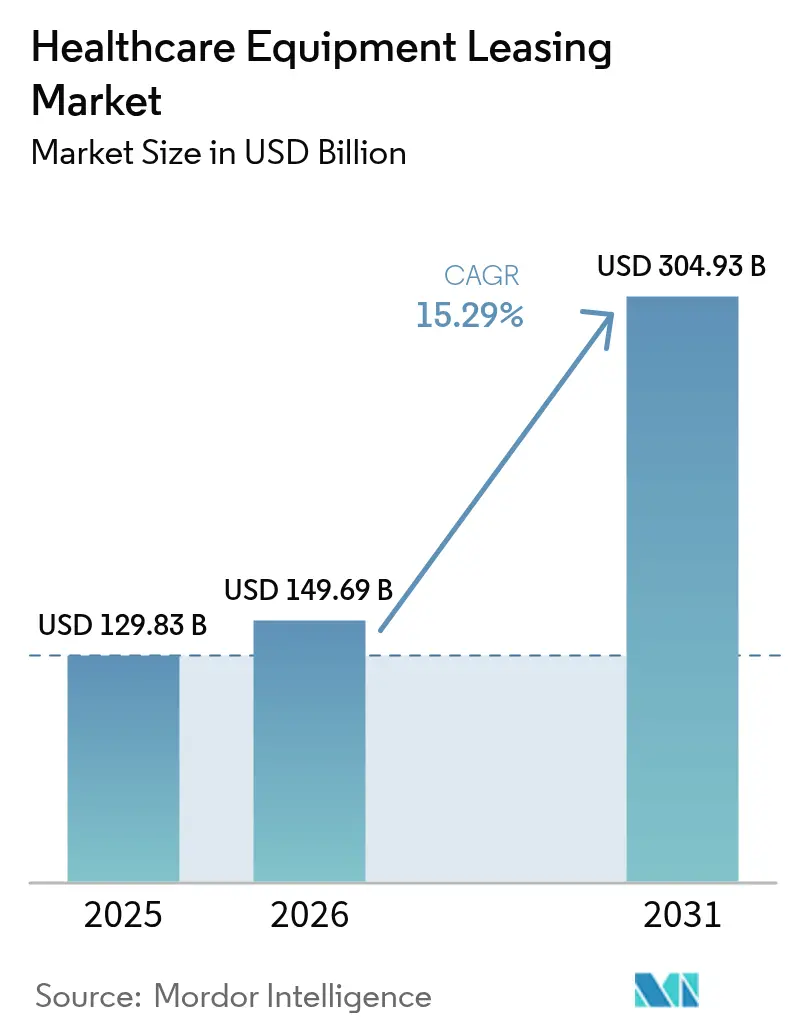

| Market Size (2026) | USD 149.69 Billion |

| Market Size (2031) | USD 304.93 Billion |

| Growth Rate (2026 - 2031) | 15.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Equipment Leasing Market Analysis by Mordor Intelligence

The Healthcare Equipment Leasing Market size is expected to grow from USD 129.83 billion in 2025 to USD 149.69 billion in 2026 and is forecast to reach USD 304.93 billion by 2031 at 15.29% CAGR over 2026-2031.

The expansion is anchored in hospitals’ preference for asset-light models that preserve liquidity, shorten technology refresh cycles, and align capital outlays with revenue generation. Providers leverage leasing to secure AI-enabled imaging, connected monitoring, and digitally integrated surgical systems without depleting cash reserves, while lessors assume obsolescence and resale risk. Intensified pressure on operating margins, heightened regulatory focus on outcomes, and the emergence of managed service contracts further accelerate demand. Simultaneously, demographic changes and the shift of care to outpatient and home settings expand the addressable base for portable, remotely monitored devices, reinforcing the long-run growth path of the healthcare equipment leasing market.

Key Report Takeaways

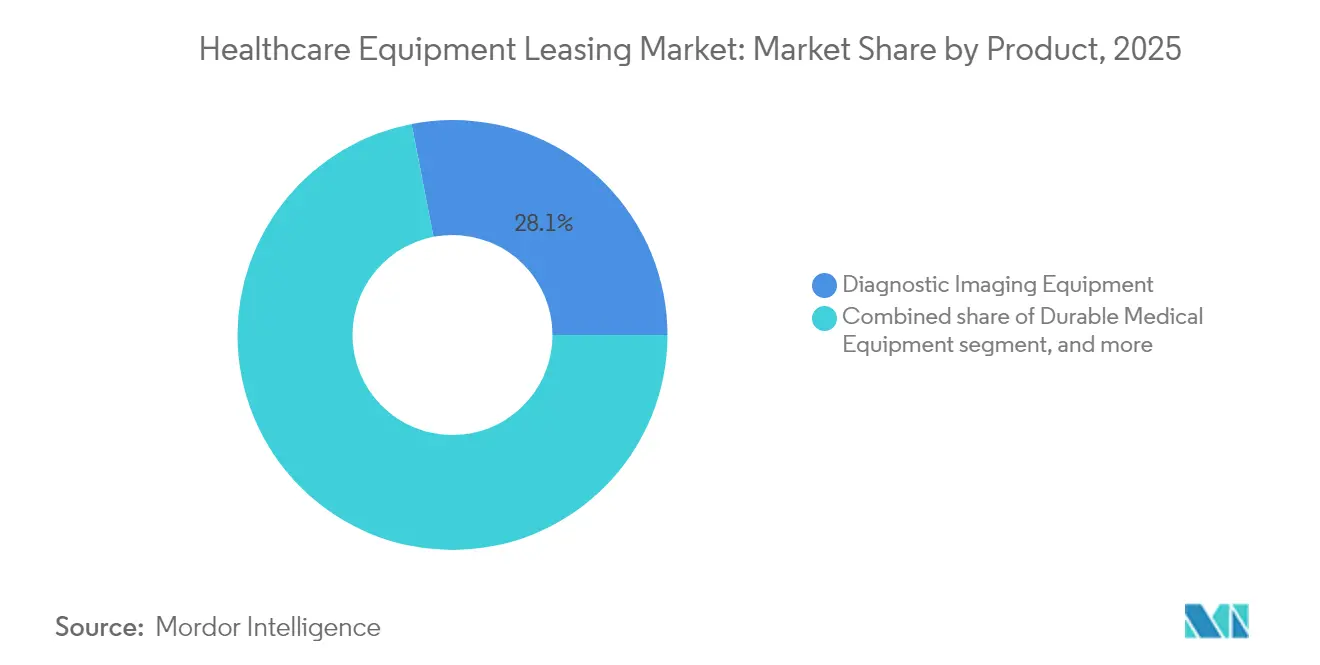

- By product type, diagnostic imaging equipment captured 28.05% of 2025 revenue, while digital and electronic equipment is forecast to grow at 17.12% CAGR through 2031.

- By lease type, operating leases held 63.68% of 2025 demand, whereas managed equipment service agreements are set to expand at 17.24% CAGR to 2031.

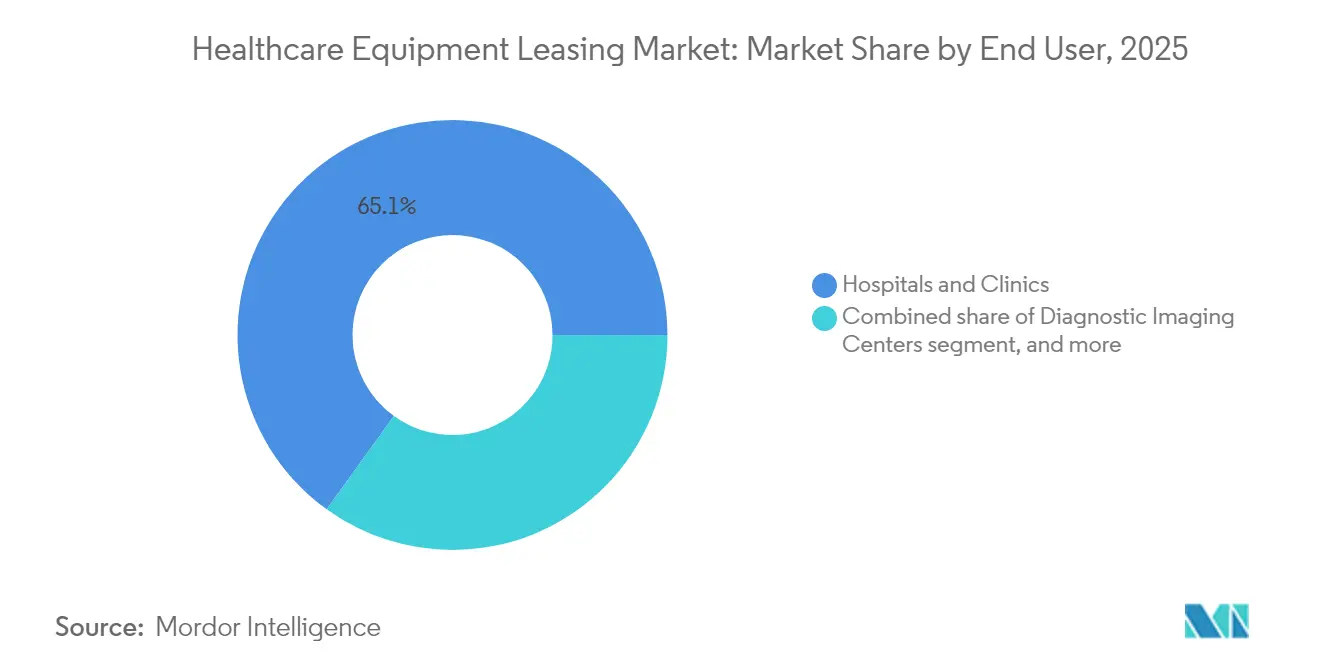

- By end user, hospitals and clinics commanded 65.05% of 2025 activity, while home healthcare providers are advancing at 17.95% CAGR over the outlook period.

- By duration, short-term contracts under 12 months accounted for 45.12% of 2025 transactions, and long-term arrangements exceeding three years are projected to climb at 17.02% CAGR.

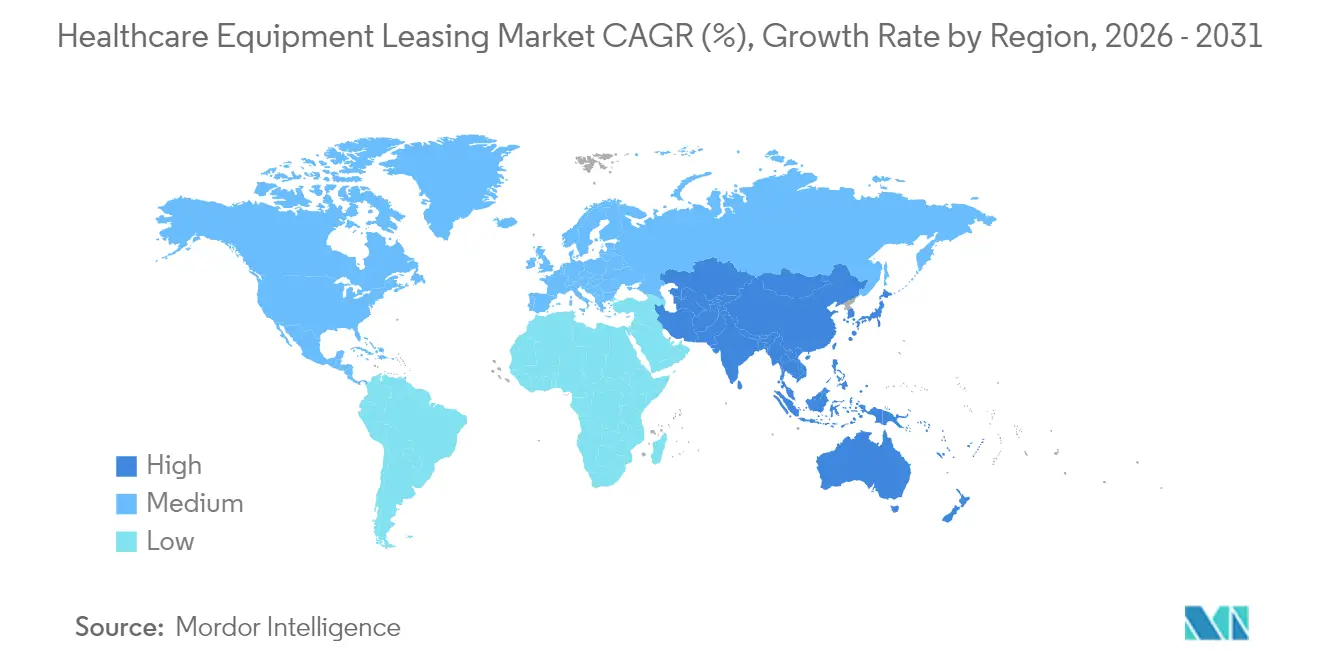

- By geography, North America led with 41.25% share in 2025, yet Asia-Pacific is on track for a 16.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Equipment Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Capital Expenditure For Medical Technology | +3.2% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Shift Toward Asset-Light Operating Models In Healthcare | +2.8% | Global, led by North America, expanding to APAC | Long term (≥4 years) |

| Expansion Of Diagnostic Imaging And Surgical Infrastructure | +2.1% | APAC core, spill-over to MEA & Latin America | Long term (≥4 years) |

| Growing Preference For Operational Flexibility And Cash-Flow Management | +2.4% | Global, particularly acute in post-pandemic markets | Medium term (2-4 years) |

| Acceleration Of Technology Refresh Cycles In Medtech | +1.9% | Global, with early adoption in developed markets | Short term (≤2 years) |

| Rise Of Outcome-Based Managed Equipment Service Contracts | +1.6% | North America & EU, broadening into APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Capital Expenditure for Medical Technology

Hospitals face capital allocation stress as MRI, CT, and robotic surgery platforms exceed multi-million-dollar price points while reimbursement schedules tighten. Leasing shifts these costs from balance sheets to predictable operating lines, freeing cash for clinical programs. Siemens Healthineers’ 10-year value partnership with Tower Health illustrates the model, bundling equipment, lifecycle management, and upgrades to mitigate obsolescence. Providers redirect preserved capital toward patient-centric initiatives yet still secure leading-edge technology. As high-spec imaging and therapy systems evolve every two to three years, the healthcare equipment leasing market becomes the preferred pathway for modernization without large-scale capex spikes.

Shift Toward Asset-Light Operating Models in Healthcare

Health systems adopt asset-light strategies to concentrate on clinical outcomes rather than equipment ownership. Everything-as-a-Service arrangements replace lump-sum purchases with performance-linked monthly fees, aligning technology use with value delivered. The model improves leverage metrics, reduces depreciation pressure, and enhances agility in uncertain economic climates. Providers allocate freed capital to telehealth, workforce retention, and digital front-door initiatives while lessors specialize in depreciation management. The widening gap between brisk innovation cycles and limited budgets cements leasing as a core pillar of financial resilience across the healthcare equipment leasing market.

Expansion of Diagnostic Imaging and Surgical Infrastructure

Emerging markets race to install MRI suites, hybrid ORs, and ambulatory imaging centers as urbanization and middle-class growth raise diagnostic demand. Leasing allows rapid deployment without upfront capital drains, enabling mid-sized hospitals in India, Indonesia, and Brazil to offer advanced scans sooner than equity financing would permit. GE HealthCare’s collaboration with Sutter Health, which cut MRI scan times by 40%, signals how AI-ready equipment can be procured through lease structures that spare capex budgets[1]GE HealthCare, “Sutter Health Accelerates MRI Throughput With AI-Enabled Scanning,” gehealthcare.com. The healthcare equipment leasing market thus serves as a catalyst for capacity build-out and quality improvement in fast-growing regions.

Rise of Outcome-Based Managed Equipment Service Contracts

Hospitals negotiate contracts that tie lease payments to uptime, image quality, or procedure throughput, ensuring technology contributes directly to patient care metrics. OEM-linked lessors bundle training, predictive maintenance, and AI analytics, guaranteeing performance while sharing operational risk. Academic studies show such models improve equipment utilization and cost predictability[2]ScienceDirect, G. Selviaridis and J. van der Valk, “Outcome-Based Healthcare Equipment Contracts,” sciencedirect.com. As value-based care expands, the healthcare equipment leasing market shifts from commodity financing toward integrated, outcome-oriented partnerships.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent accounting standards increasing on-balance-sheet liabilities | -1.8% | Global, acute in public entities & regulated providers | Medium term (2-4 years) |

| Availability of refurbished and second-life equipment alternatives | -1.2% | Global, pronounced in cost-sensitive markets | Long term (≥4 years) |

| Rising cybersecurity and data-privacy compliance costs | -1.5% | North America & EU, spreading worldwide | Short term (≤2 years) |

| Limited awareness of leasing benefits among small healthcare providers | -0.9% | Emerging markets and rural settings globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Accounting Standards Increasing On-Balance-Sheet Liabilities

ASC 842 and IFRS 16 oblige health systems to record lease liabilities, reducing prior off-balance-sheet advantages. The change raises reported leverage, complicates debt-covenant compliance, and forces CFOs to revisit purchase-versus-lease models. Operating leases now appear alongside finance leases, narrowing the gap to loan financing. U.S. Bank’s advisory notes that proper classification remains vital for rating reviews. Although transparency improves, the rule tempers aggressive growth in the healthcare equipment leasing market for organizations sensitive to headline debt metrics.

Availability of Refurbished and Second-Life Equipment Alternatives

A mature global refurbishing ecosystem offers MRI, CT, and ultrasound systems at discounts of 30–50% relative to new leases. DirectMed Imaging’s inventory demonstrates ready access to certified parts and extended warranties at lower cost. Price-constrained community clinics in Latin America and Africa often favor refurbished units over new leased gear. Lessors must therefore differentiate through service guarantees, uptime commitments, and built-in upgrade paths to defend share in the healthcare equipment leasing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostic Imaging Leads Digital Transformation

Diagnostic imaging held 28.05% of 2025 revenue, underscoring its critical role in treatment pathways and its sizable capital requirements. MRI, CT, and ultrasound systems command premium lease rates, and providers rely on these arrangements to avoid aging fleets that hinder clinical throughput. The healthcare equipment market share for imaging remains stable as demand for precision diagnostics and minimally invasive interventions rises in oncology and cardiology.

Digital and electronic equipment is advancing at 17.12% CAGR, the highest among product categories, propelled by AI-integrated monitors, connected ventilators, and smart IV pumps. Short technology cycles encourage two- to three-year terms with mid-cycle upgrades. The healthcare equipment market size for connected devices widens as interoperability mandates push hospitals toward platform overhaul. Patient monitoring, life-support, and surgical robotics follow with steady gains, each supported by leasing programs that bundle training and analytics support. Durable medical equipment and laboratory analyzers sustain predictable replacement schedules, while portable home-care devices open a new frontier for the healthcare equipment leasing market among aging populations.

By Lease Type: Operating Models Dominate Service Evolution

Operating leases represented 63.68% of 2025 transactions, favored for their flexible end-of-term options and off-setting of obsolescence risk. Hospitals align these structures with budget cycles, often embedding variable usage clauses to match seasonal procedure volumes. The healthcare equipment leasing market size tied to operating agreements benefits from predictable monthly payments that preserve credit lines.

Managed equipment service agreements are expanding at 17.24% CAGR, reflecting demand for turnkey solutions that combine hardware, software, and managed services. Lessors assume maintenance, compliance, and performance metrics, easing the operational burden on providers. Capital leases appeal to institutions targeting eventual ownership for long-life assets such as radiotherapy vaults, while sale-leaseback structures monetize legacy fleets to fund digital upgrades. The growing appeal of full-service models demonstrates the healthcare equipment leasing market progression from financing tool to integrated performance partnership.

By End User: Hospitals Anchor Home Care Acceleration

Hospitals and clinics generated 65.05% of 2025 leasing volume, driven by multi-disciplinary equipment needs across inpatient, outpatient, and emergency settings. High-acuity environments demand constant technology refresh, especially in imaging, surgery, and critical care units. The healthcare equipment market share held by hospitals stays dominant as integrated delivery networks consolidate purchasing.

Home healthcare providers are expanding at 17.95% CAGR, mirroring policy moves that reimburse hospital-at-home programs and remote vital-sign monitoring. Portable oxygen concentrators, tele-ECG kits, and connected infusion pumps rank among high-demand assets. The healthcare equipment market size attributable to home-based care grows as payers reward reduced readmissions and patient satisfaction. Diagnostic imaging centers and ambulatory surgical centers follow with robust uptake, leveraging leasing to match rising outpatient procedure volumes without inflating capex burdens. Long-term care and rehabilitation facilities maintain steady participation, updating mobility aids and rehabilitation robotics to improve outcomes for aging cohorts.

By Duration: Short-Term Flexibility Yields to Strategic Partnerships

Short-term leases under 12 months accounted for 45.12% of 2025 volume, reflecting pandemic-era urgency and the need to trial AI-ready devices before rolling out system-wide. The healthcare equipment leasing market share linked to short-term contracts remains sizable as providers cope with unpredictable demand surges.

Long-term arrangements above three years are rising at 17.02% CAGR, signaling confidence in integrated partnerships that stabilize costs and secure multiyear upgrade paths. FDA’s forthcoming Quality Management System Regulation will heighten documentation requirements, favoring lessors with robust compliance support. Medium-term leases between one and three years bridge flexibility and cost efficiency for equipment with moderate obsolescence risk. As lifecycle management disciplines mature, providers align lease tenors with clinical road maps, solidifying the healthcare equipment leasing market’s role in strategic capital planning.

Geography Analysis

North America contributed 41.25% of 2025 revenue, supported by sophisticated reimbursement models, established leasing infrastructure, and regulators that value operational flexibility. Providers replace capital-intensive imaging suites and surgical robots via service contracts that ensure uptime and continuous updates. The healthcare equipment market size in the region benefits from tight hospital margins and competitive technology benchmarks.

Europe posts steady growth as modernization programs and cross-border procurement initiatives standardize leasing frameworks. Aging populations and digital health directives create recurring replacement cycles for imaging, infusion, and monitoring systems. Asia-Pacific, the fastest-growing territory at 16.08% CAGR, witnesses rapid infrastructure build-out across China, India, and ASEAN states. Public-private partnerships, rising middle-class demand, and clinical capacity shortages make leasing integral to timely facility expansion. Middle East and Africa add incremental demand as government projects in the Gulf integrate turnkey leasing packages for new specialty centers. South America experiences cyclical uptake tied to economic stability, with private payers in Brazil and Chile emphasizing AI-enhanced diagnostics. The geographic spread underscores that the healthcare equipment leasing market scales across maturity levels by tailoring contract terms to regulatory, fiscal, and clinical nuances.

Competitive Landscape

The healthcare equipment leasing market remains moderately fragmented. Captive finance units of Siemens Healthineers, GE HealthCare, and Philips combine OEM knowledge with tailored funding, gaining share in outcome-based contracts. Independent lessors such as CHG-MERIDIAN excel in multi-vendor portfolios and niche modalities, while Med One Group focuses on short-term flexibility for infusion, respiratory, and monitoring equipment.

Strategic maneuvers pivot toward value partnerships. Siemens Healthineers opened mega depots in New York and California to boost 30% additional parts inventory, reinforcing uptime guarantees[3]Siemens Healthineers, “Mega Depot Expansion Boosts Parts Availability,” siemens-healthineers.com. GE HealthCare’s AI-enabled imaging deal with Sutter Health exemplifies technology-plus-service bundling. Private equity interest remains high: Frazier Healthcare Partners’ acquisition of DirectMed Imaging aims to deepen access to aftermarket parts for radiology fleets.

Technology integration differentiates competitors. AI analytics, IoT telemetry, and predictive maintenance portals improve asset utilization and reduce unplanned downtime. Lessors able to document compliance under upcoming FDA QMSR earn preference among large health systems. White-space opportunities include financing for home-based care devices, digital therapeutics, and emerging-market mobile clinics, indicating ample room for specialized entrants.

Healthcare Equipment Leasing Industry Leaders

Agiliti Health, Inc

Getinge AB

Koninklijke Philips NV

US Med-Equip

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Siemens Healthineers signed a 10-year partnership with Tower Health to manage imaging equipment lifecycles and introduce digital workflow tools.

- March 2025: Baxter International debuted the Voalte Linq voice-activated communication device to streamline clinical workflows, expecting U.S. rollout in H2 2025.

- February 2025: Siemens Healthineers opened mega depots in New York and California, boosting parts inventory by 30% and enhancing delivery flexibility.

- January 2025: Sutter Health entered a seven-year agreement with GE HealthCare to acquire AI-enabled imaging systems that cut MRI scan times by 40%.

- December 2024: CHG-MERIDIAN acquired Meridian Leasing Corporation, enlarging its North American healthcare footprint.

- October 2024: Frazier Healthcare Partners bought DirectMed Imaging to strengthen aftermarket radiology parts and repair capabilities.

Global Healthcare Equipment Leasing Market Report Scope

As per the scope of the report, healthcare equipment lessors and lessees enter into an arrangement in which the lessor permits the lessee to use the equipment for a set amount of time in exchange for lease rentals. Leasing businesses can finance costly medical equipment such as MRI machines, X-Ray machines, and ventilators without having to put up big sums of money upfront. At the end of the lease term, the equipment can be returned to the lessor or acquired at the current market price.

The healthcare equipment leasing market is segmented by product, end-user, and geography. By product, the market is segmented by durable medical equipment, surgical and therapy equipment, personal and home-care equipment, digital and electronic equipment, storage and transport equipment. By end user, the market is segmented by hospitals and clinics, diagnostic centers, and others. The other end users include ambulatory surgery centers and at-home care centers. By geography, the market is segmented by North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Diagnostic Imaging Equipment |

| Durable Medical Equipment |

| Surgical & Therapy Equipment |

| Patient Monitoring & Life-support |

| Digital & Electronic Equipment |

| Storage & Transport Equipment |

| Home-care Equipment |

| Laboratory & Analytical Equipment |

| Operating Lease |

| Capital/Finance Lease |

| Sale-Leaseback |

| Managed Equipment Service Agreement |

| Hospitals & Clinics |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Home Healthcare Providers |

| Long-term Care & Rehabilitation Facilities |

| Short-term (< 12 months) |

| Medium-term (1-3 years) |

| Long-term (> 3 years) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostic Imaging Equipment | |

| Durable Medical Equipment | ||

| Surgical & Therapy Equipment | ||

| Patient Monitoring & Life-support | ||

| Digital & Electronic Equipment | ||

| Storage & Transport Equipment | ||

| Home-care Equipment | ||

| Laboratory & Analytical Equipment | ||

| By Lease Type | Operating Lease | |

| Capital/Finance Lease | ||

| Sale-Leaseback | ||

| Managed Equipment Service Agreement | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Home Healthcare Providers | ||

| Long-term Care & Rehabilitation Facilities | ||

| By Duration | Short-term (< 12 months) | |

| Medium-term (1-3 years) | ||

| Long-term (> 3 years) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the healthcare equipment leasing market?

The healthcare equipment leasing market stands at USD 149.69 billion in 2026.

How fast is the sector projected to grow over the next five years?

Market value is forecast to reach USD 304.93 billion by 2031, advancing at a 15.29% CAGR.

Which product category commands the highest share of leased assets?

Diagnostic imaging equipment leads with 28.05% share in 2025.

Which end-user segment is growing the quickest?

Home healthcare providers are expanding at 17.95% CAGR through 2031.

Why are managed equipment service agreements gaining traction?

They bundle hardware, software, maintenance, and performance guarantees, rising at 17.24% CAGR.

Which region offers the strongest growth opportunity?

Asia-Pacific is projected to expand at 16.08% CAGR, driven by rapid infrastructure build-out.

Page last updated on: