Healthcare Computerized Maintenance Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

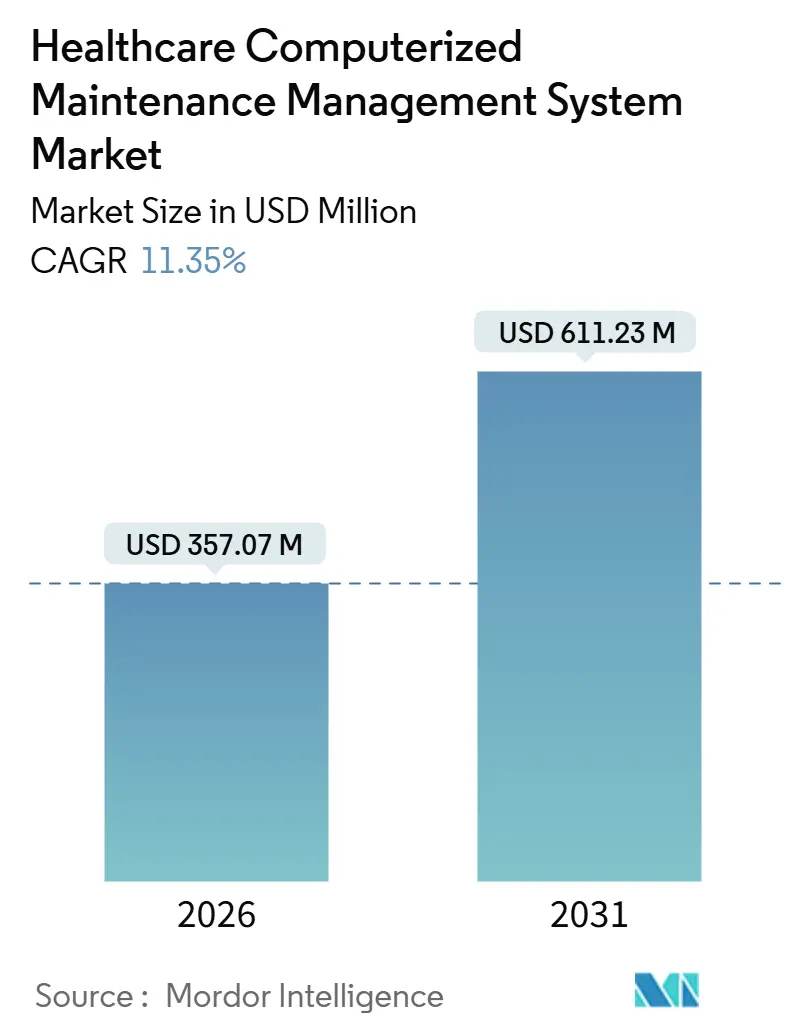

| Market Size (2026) | USD 357.07 Million |

| Market Size (2031) | USD 611.23 Million |

| Growth Rate (2026 - 2031) | 11.35% CAGR |

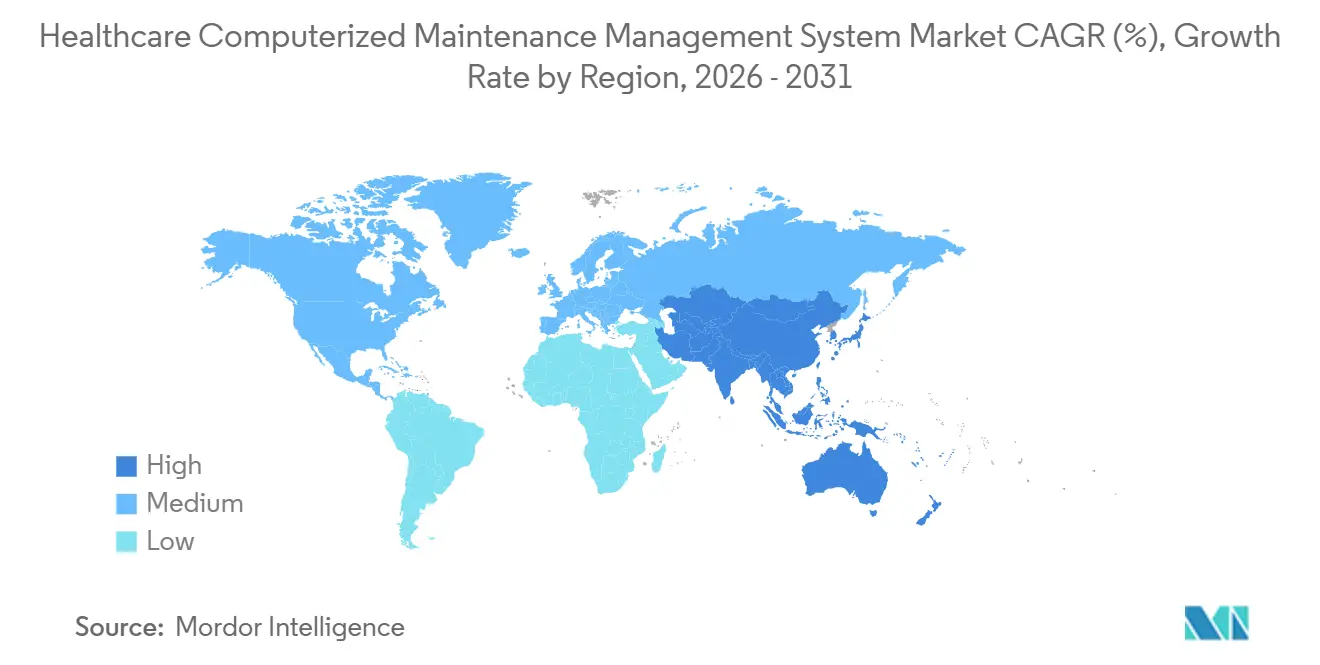

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

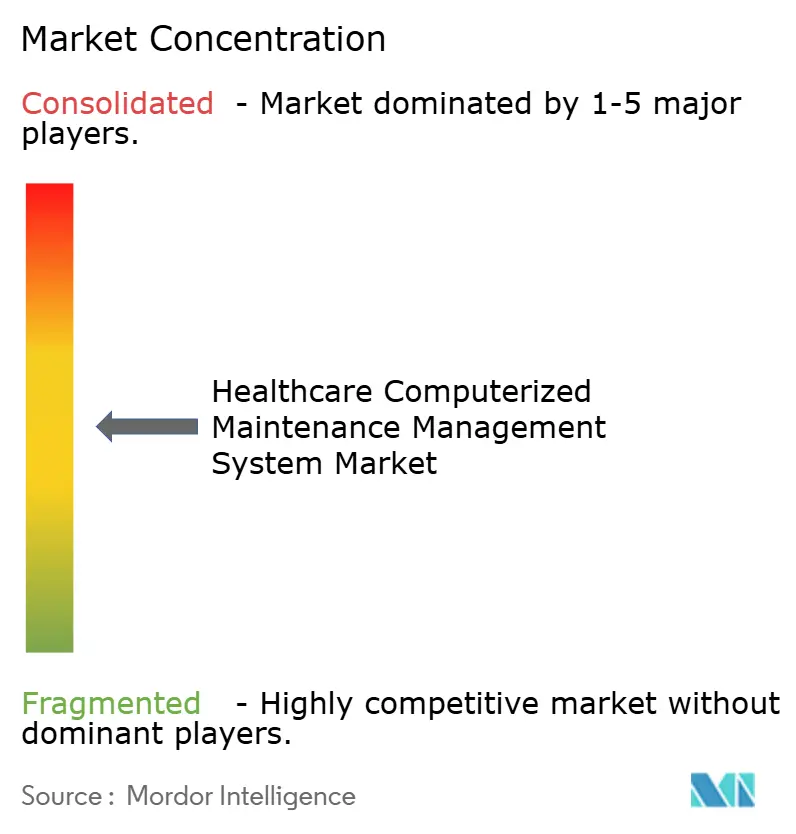

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Computerized Maintenance Management System Market Analysis by Mordor Intelligence

The Healthcare Computerized Maintenance Management System Market size is estimated at USD 357.07 million in 2026, and is expected to reach USD 611.23 million by 2031, at a CAGR of 11.35% during the forecast period (2026-2031).

The expansion is driven by the migration from paper logs to auditable digital systems needed to satisfy CMS Conditions of Participation, FDA 21 CFR Part 11 audit trails, and Joint Commission accreditation requirements. Regulatory pressure aligns with the growing preference for software-as-a-service models, especially among multi-site health systems that seek centralized visibility at lower capital cost. Facilities also value predictive analytics that minimize downtime, and vendors that can integrate with electronic health records and building automation systems are gaining an edge. Mergers between device manufacturers and software providers point to a future in which maintenance data flows bidirectionally between the healthcare computerized maintenance management system market and connected-device ecosystems.

Key Report Takeaways

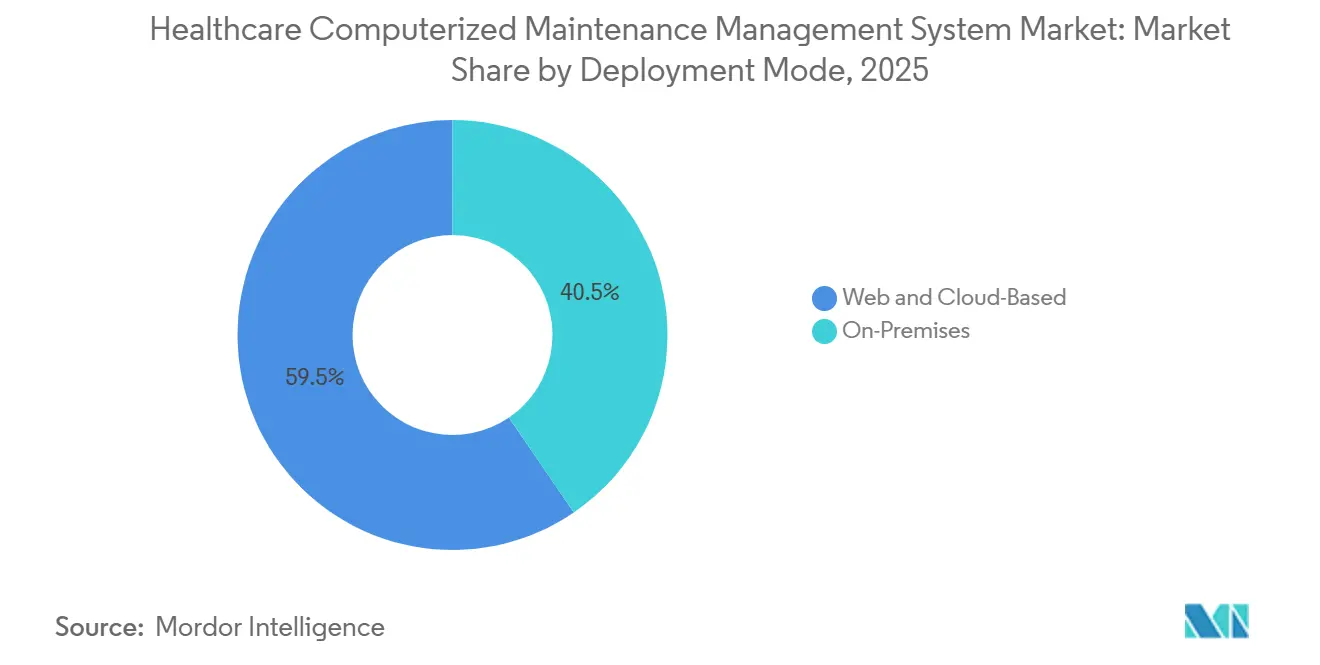

- By deployment mode, web and cloud platforms led with 59.54% healthcare computerized maintenance management system market share in 2025; the same segment is forecast to expand at an 11.45% CAGR through 2031.

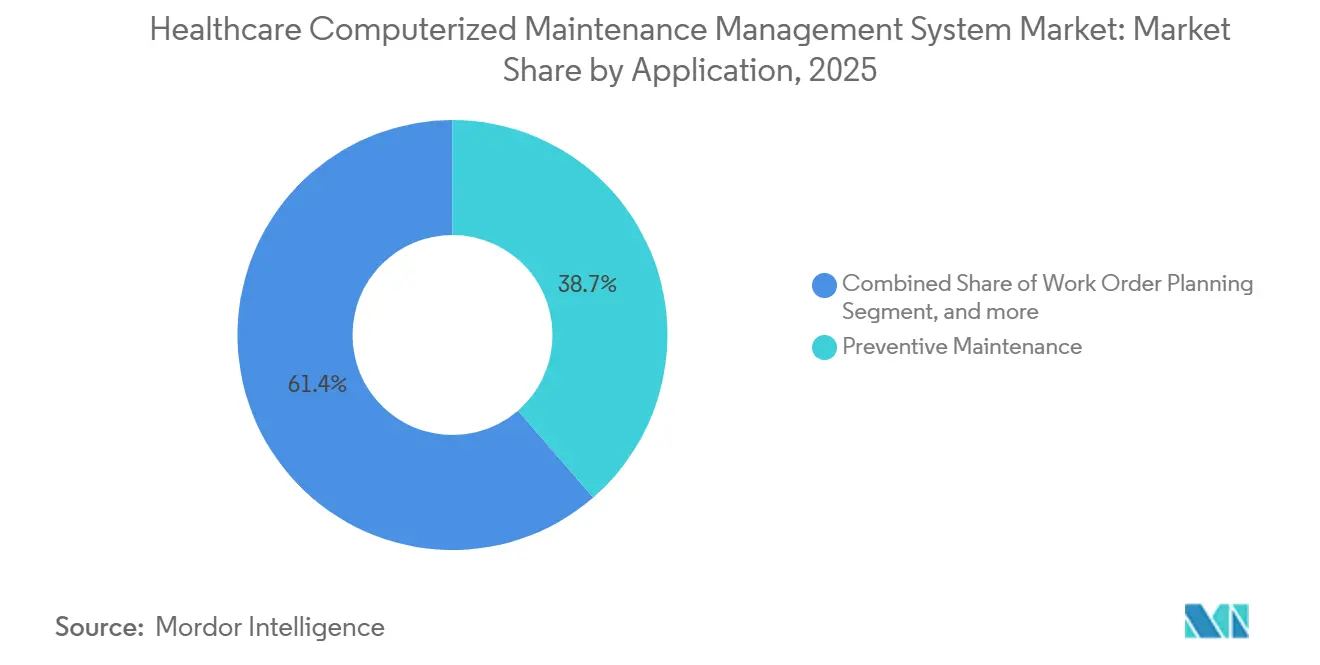

- By application, preventive maintenance commanded 38.65% share of the healthcare computerized maintenance management system market size in 2025, while predictive maintenance is advancing at an 11.65% CAGR through 2031.

- By end user, hospitals held 71.37% of the healthcare computerized maintenance management system market in 2025; diagnostic laboratories are growing the fastest, with a 12.65% CAGR to 2031.

- By geography, North America held 43.12% of the healthcare computerized maintenance management system market in 2025; diagnostic laboratories are growing the fastest, with a 10.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Computerized Maintenance Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Cloud-Based CMMS Solutions | +2.1% | Global, stronger in North America and Asia-Pacific | Medium term (2-4 years) |

| Need for Efficient Maintenance Management | +1.8% | Global | Long term (≥4 years) |

| Stringent Regulatory & Accreditation Mandates | +2.3% | North America and Europe, spreading to Asia-Pacific | Short term (≤2 years) |

| Digital Transformation & Smart Facility Initiatives | +1.9% | Asia-Pacific core, Middle East spillover | Medium term (2-4 years) |

| Predictive Maintenance via AI & IoT | +1.7% | North America and Europe | Medium term (2-4 years) |

| Infrastructure Expansion in Emerging Markets | +1.6% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Cloud-Based CMMS Solutions

Cloud deployment enables real-time synchronization of work orders, inventory, and vendor metrics across dispersed campuses, a capability that paper or client-server systems cannot match[1]Australian Digital Health Agency, “National Digital Health Strategy 2023–2028,” digitalhealth.gov.au. The healthcare computerized maintenance management system market benefits from subscription pricing, which replaces large capital investments and shortens rollouts to weeks. HIPAA-compliant virtual private clouds with encryption at rest and in transit ease historic security concerns. As a result, cloud platforms are the default choice for new hospital projects and retrofits, accelerating revenue growth for vendors that offer seamless updates and elastic scalability. The model also facilitates analytics modules that benchmark performance across facilities, further increasing stickiness for the healthcare computerized maintenance management system market.

Growing Need for Efficient Maintenance Management Across Healthcare Facilities

Hospitals operate thousands of devices that must be inspected, calibrated, and documented. Unplanned downtime costs U.S. providers USD 1,200 per hour on average, and up to USD 5,000 per hour for critical-care modalities[2]American Hospital Association, “Hospital Downtime Cost Study 2024,” aha.org. CMMS software automates scheduling, sends alerts before deadlines, and stores inspection evidence needed for audits. In the healthcare computerized maintenance management system market, return on investment is heightened for rural and resource-constrained hospitals that cannot afford redundant equipment. The resulting efficiency gains turn maintenance from a compliance box-tick into a lever for throughput and patient safety, strengthening long-term demand.

Stringent Regulatory and Accreditation Compliance Mandates

The Joint Commission demands evidence of maintenance aligned with manufacturer guidelines or risk assessments. CMS reimbursement hinges on meeting similar standards, while 21 CFR Part 11 of the FDA requires tamper-proof electronic records. European Medical Device Regulation adds post-market surveillance obligations. Vendors embed checklists, audit logs, and electronic signatures directly into workflows, making regulatory readiness a built-in feature rather than an add-on. The healthcare computerized maintenance management system market thus expands as compliance shifts from optional to obligatory for revenue integrity.

Rapid Digital Transformation of Hospital Infrastructure and Smart Facility Initiatives

Asia-Pacific governments fund greenfield smart hospitals that converge building automation, clinical engineering, and supply-chain systems. India’s Ayushman Bharat Digital Mission and Saudi Arabia’s Vision 2030 mandate integrated digital platforms. CMMS vendors with robust APIs and multilingual interfaces capture early-stage contracts, accelerating the healthcare computerized maintenance management system market in high-growth regions. Projects require interoperability with IoT sensors and electronic health records, fostering ecosystems rather than siloed point solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation & Integration Costs | −1.4% | Global, acute for small facilities | Short term (≤2 years) |

| Data Security & Patient Privacy Concerns | −0.9% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Limited Technical Expertise & Change Management | −1.1% | Emerging markets, rural facilities | Long term (≥4 years) |

| Interoperability Issues With Legacy IT | −1.2% | Global, especially legacy-heavy North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Implementation and Integration Costs

A 200-bed U.S. hospital spends USD 150,000–500,000 over five years to deploy an enterprise CMMS, with integration accounting for up to 40% of the cost. Small hospitals delay purchases despite demonstrable ROI. Consumption-based pricing is emerging but not yet mainstream, tempering short-term growth in the healthcare computerized maintenance management system market.

Data Security and Patient Privacy Concerns

CMMS records can reveal patterns that attackers exploit. A 2025 cyber incident showed how equipment schedules helped time ransomware attacks. NIST now recommends zero-trust architecture for non-clinical systems[3]National Institute of Standards and Technology, “Zero-Trust Architecture for Healthcare Operational Technology,” nist.gov. Until such safeguards become ubiquitous, security fears will restrain parts of the healthcare computerized maintenance management system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Reshapes IT Infrastructure

The cloud segment captured 59.54% of the healthcare computerized maintenance management system market share in 2025 and is forecast to expand at an 11.45% CAGR through 2031, making it the largest contributor to the healthcare computerized maintenance management system market size for deployment modes. Subscription models eliminate server procurement, accelerate roll-outs, and include continuous updates that keep pace with security threats. Multi-site health systems value a single-tenant solution for asset data and analytics, while smaller providers leverage elastic pricing to avoid overbuying capacity.

On-premises solutions persist where data sovereignty, military cybersecurity controls, or air-gapped networks are mandatory. Veterans Affairs and certain defense hospitals choose hybrid configurations, running core CMMS locally while analytics sit in government-approved clouds. Vendor roadmaps, however, increasingly prioritize cloud-first codebases, signaling that the healthcare computerized maintenance management system market will continue tilting toward hosted delivery over the forecast period.

By Application: Predictive Maintenance Gains Ground

Preventive maintenance accounted for 38.65% of the healthcare computerized maintenance management system market in 2025, underscoring regulatory obligations for scheduled inspections. Predictive maintenance, though smaller, is the fastest-growing application, with a 11.65% CAGR, driven by AI-enabled failure forecasts and IoT sensor data. Hospitals adopt blended strategies, pairing time-based checklists with condition-based triggers to optimize technician workloads and spare-parts stocking.

Work-order planning and inventory management modules round out demand. Facilities prefer integrated suites that eliminate double data entry, ensuring that a predictive alert automatically opens a work order, reserves parts, and schedules staff. Vendors offering modular expansion paths retain clients as needs mature, reinforcing stickiness in the healthcare computerized maintenance management system market.

By End User: Diagnostic Laboratories Accelerate Adoption

Hospitals accounted for 71.37% of the healthcare computerized maintenance management system market size in 2025, reflecting the sheer volume and diversity of assets within inpatient settings. Academic centers run thousands of devices across campuses, creating economies of scale for enterprise implementations. Diagnostic laboratories, however, are growing at a 12.65% CAGR as automated analyzers and molecular platforms demand rigorous calibration and reagent tracking to meet CLIA standards.

Clinics and ambulatory surgery centers look to lightweight, mobile-first tools that align with smaller device fleets and limited IT resources. Vendors like UpKeep and Limble win here by offering per-user pricing and barcode scanning for quick adoption. Long-term care, imaging centers, and blood banks represent additional niches where dedicated workflows—such as refrigeration monitoring—help suppliers differentiate in the competitive healthcare computerized maintenance management system market.

Geography Analysis

North America retained 43.12% of the healthcare computerized maintenance management system market share in 2025, anchored by compliance requirements under CMS Conditions of Participation, FDA electronic records rules, and Joint Commission audits. Canada enforces similar asset-tracking through Accreditation Canada, while Mexico’s private hospital chains invest ahead of slower-moving public institutions. The region now sees replacement cycles rather than first-time roll-outs, so growth hinges on predictive analytics and broader platform integration rather than raw penetration.

Asia-Pacific is the fastest-growing region, with a 10.65% CAGR, driven by large-scale hospital construction in India and China and by policy mandates for interoperable digital health infrastructure. Australia’s Digital Health Blueprint mandates CMMS-EHR-registry connectivity and creates procurement templates for neighboring countries. Japan and South Korea focus on legacy replacement, while Southeast Asian medical tourism hubs demand multilingual, cloud-ready solutions. Suppliers capable of navigating data-residency rules and providing local-language support are gaining ground in this phase of the expansion of the healthcare computerized maintenance management system market.

Europe advances under the Medical Device Regulation, with Germany, the United Kingdom, and France modernizing hospital IT through dedicated funds such as Germany’s Hospital Future Act. The Gulf Cooperation Council invests heavily in smart hospitals as part of diversification strategies, exemplified by Burjeel Healthcare’s Oracle Health EMR deployment that links clinical and facilities data. Latin America’s growth centers on Brazil and Argentina but is tempered by fiscal volatility. Across all regions, greenfield projects embed CMMS from inception, while mature markets emphasize integration depth and analytics in shaping demand for the healthcare computerized maintenance management system market.

Competitive Landscape

Competition is moderate and stratified. Enterprise software majors—ServiceNow, IBM Maximo, and Infor—leverage existing footprints to upsell asset-management modules, but their complexity and cost spur mid-tier players to flourish. Specialist vendors such as Nuvolo, Accruent, Brightly, and TRIMEDX pre-load compliance workflows and boast biomedical expertise, traits valued by regulated providers. Lightweight cloud entrants UpKeep, Limble, and Hippo CMMS serve clinics and small hospitals with mobile-first interfaces and usage-based pricing.

Medical device manufacturers blur traditional lines by embedding maintenance dashboards into scanners and monitors. Philips HealthSuite and GE HealthCare OnWatch Predict export real-time performance data via HL7 FHIR APIs, allowing third-party CMMS to trigger proactive service events. Such alliances offer hospitals predictive insights yet risk vendor lock-in if data remains proprietary. White-space opportunities abound in diagnostic laboratories, ambulatory surgery centers, and emerging markets where greenfield hospitals prefer cloud-native, multilingual products, highlighting continued fragmentation and innovation in the healthcare computerized maintenance management system market.

Healthcare Computerized Maintenance Management System Industry Leaders

Accruent

IBM

Fluke Corp.

Facilio Inc.

Eptura

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Maintainly, the modern computerized maintenance management system (CMMS) built for today’s maintenance teams launched its newly redesigned user interface, marking the beginning of a new era for the platform and reinforcing its commitment to usability, performance, and operational clarity. It serves many industries with physical assets, like manufacturing, hospitality, energy, healthcare, and education.

- June 2025: PartsSource launched the industry’s first multi-vendor Asset Health Record that aggregates imaging and biomedical data across manufacturers to boost clinical uptime.

- February 2025: Burjeel Healthcare rolled out one of the Middle East’s largest Oracle Health EMR platforms, integrating facilities-management analytics with clinical records.

Global Healthcare Computerized Maintenance Management System Market Report Scope

As per the scope of the report, a healthcare computerized maintenance management system (CMMS) is software that helps healthcare facilities manage and track the maintenance of medical equipment and infrastructure. It schedules preventive maintenance, records repair histories, and ensures equipment safety and compliance. This system improves operational efficiency and reduces downtime of critical healthcare assets.

The Healthcare Computerized Maintenance Management System Market Report is Segmented by Deployment Mode (Web & Cloud-Based and On-Premises), Application (Preventive Maintenance, Work Order Planning, Inventory Management, Predictive Maintenance, and Other Applications), End-User (Hospitals, Diagnostic Laboratories, Clinics, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Web & Cloud-Based |

| On-Premises |

| Preventive Maintenance |

| Work Order Planning |

| Inventory Management |

| Predictive Maintenance |

| Other Applications |

| Hospitals |

| Diagnostic Laboratories |

| Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Deployment Mode | Web & Cloud-Based | |

| On-Premises | ||

| By Application | Preventive Maintenance | |

| Work Order Planning | ||

| Inventory Management | ||

| Predictive Maintenance | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Diagnostic Laboratories | ||

| Clinics | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the expected value of the Healthcare CMMS market in 2031?

The sector is projected to reach USD 611.23 million by 2031, growing at an 11.35% CAGR.

Which deployment model leads adoption?

Web and cloud platforms held 59.54% share in 2025 and remain the fastest-growing approach through 2031.

Why are diagnostic laboratories adopting CMMS rapidly?

High-throughput analyzers and stringent calibration requirements drive labs toward digital asset tracking, producing a 12.65% CAGR.

How does predictive maintenance differ from preventive maintenance?

Predictive models use sensor data and AI to forecast failures in advance, cutting unnecessary inspections and reducing downtime.

Which region shows the fastest growth?

Asia-Pacific leads with a 10.65% CAGR, propelled by large-scale hospital construction and digital-health mandates.

What factors restrain smaller hospitals from adopting CMMS?

High upfront costs, limited IT expertise, and concerns about data security slow adoption among small and rural facilities.

Page last updated on: