Europe Orthopedic Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.21 Billion |

| Market Size (2026) | USD 14.74 Billion |

| Market Size (2031) | USD 17.69 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Orthopedic Devices Market Analysis by Mordor Intelligence

The Europe orthopedic devices market size in 2026 is estimated at USD 14.74 billion, growing from 2025 value of USD 14.21 billion with 2031 projections showing USD 17.69 billion, growing at 3.72% CAGR over 2026-2031. Surging procedure volumes linked to aging demographics, a return to elective surgeries after COVID-19, and the rapid uptake of smart implants that comply with EU-MDR traceability rules underpin this steady expansion. Material shifts toward bioabsorbable composites, broader adoption of 3-D printing for patient-specific parts, and the growing role of ambulatory surgical centers (ASCs) help manufacturers differentiate offerings. Meanwhile, supply-chain uncertainty around titanium and rare-earth inputs keeps procurement teams focused on dual sourcing, and divergent reimbursement reforms place margin pressure on high-innovation devices. Competitive strategies now hinge on platform robotics, in-house additive manufacturing, and sustainability credentials, keeping the Europe orthopedic devices market in a state of disciplined but active investment.

Key Report Takeaways

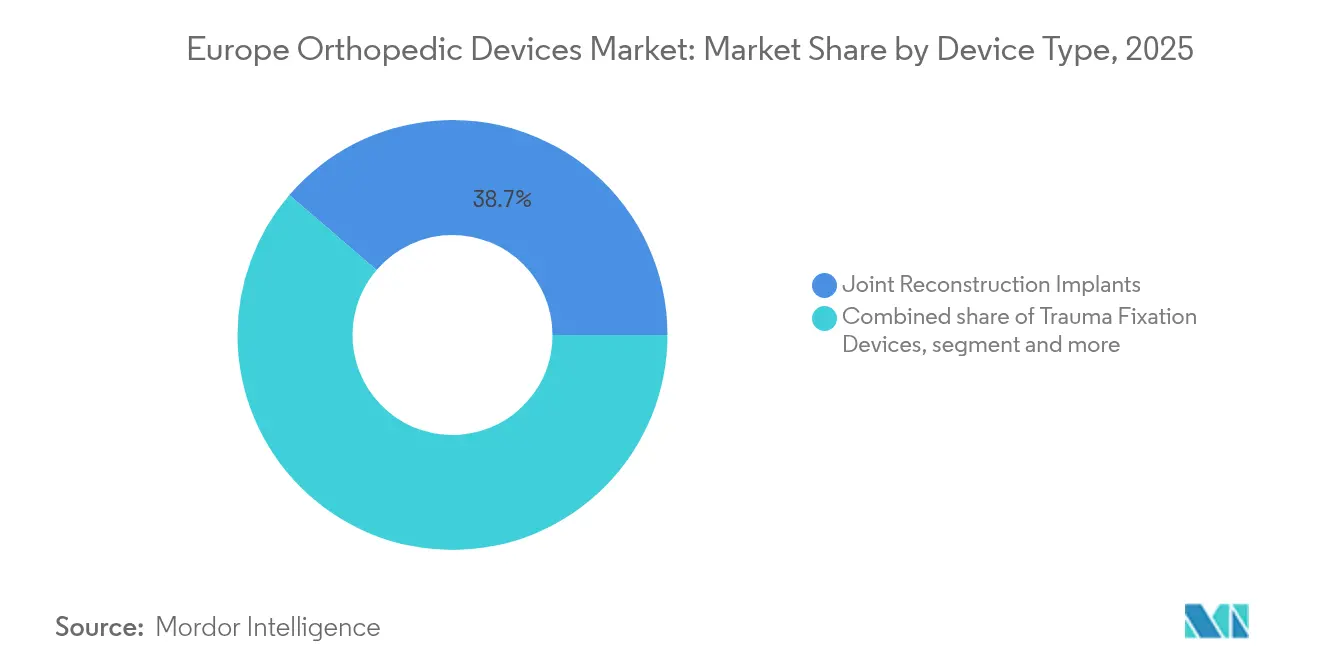

- By device type, joint reconstruction implants held 38.72% of Europe orthopedic devices market share in 2025; orthobiologics are projected to grow at a 4.28% CAGR through 2031.

- By material, titanium and titanium alloys commanded 39.65% share of the Europe orthopedic devices market size in 2025, while bioabsorbable and composite materials are set to expand at a 5.12% CAGR by 2031.

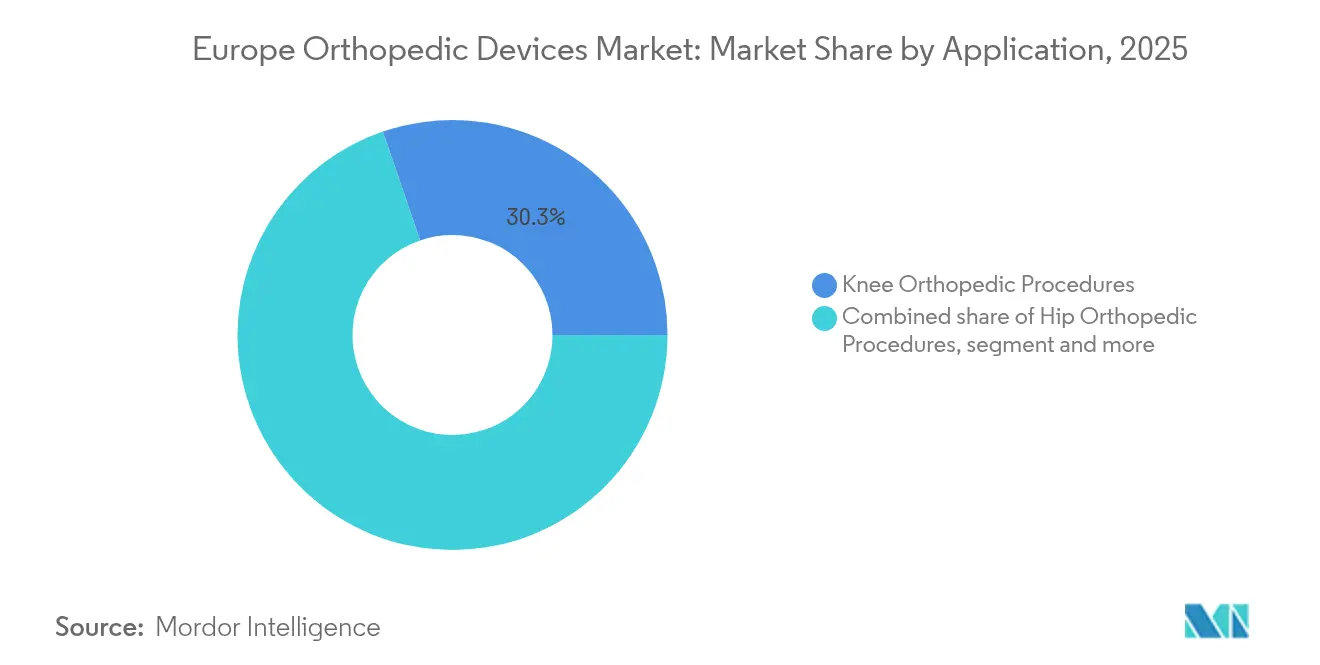

- By application, knee procedures accounted for 30.25% of the Europe orthopedic devices market size in 2025; spine procedures are forecast to accelerate at a 4.73% CAGR over 2026-2031.

- By end user, hospitals led with 59.12% revenue share in 2025, whereas ASCs represent the fastest-growing setting at 5.56% CAGR.

- By geography, Germany retained 23.15% market share in 2025; the United Kingdom is poised for the highest growth at a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Orthopedic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-related surge in joint reconstruction | +1.2% | Germany, Italy, France | Long term (≥ 4 years) |

| Shift toward outpatient & day-case care | +0.8% | UK, Netherlands, Germany | Medium term (2-4 years) |

| 3-D printed patient-specific implants | +0.6% | Germany, UK, France | Medium term (2-4 years) |

| EU-MDR traceability fuels smart implants | +0.4% | EU-wide | Short term (≤ 2 years) |

| Robotic-assisted surgery adoption | +0.5% | Germany, France, UK | Medium term (2-4 years) |

| Green rules boost bioabsorbable materials | +0.3% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-related surge in joint reconstruction procedures

Germany expects total knee arthroplasty incidence to climb from 245 to 379 per 100,000 inhabitants by 2040, a 55% jump that exemplifies region-wide demographic strain. The volume spike is most pronounced among patients aged 40-69 for knees and 80-89 for hips, forcing designers to extend implant durability and enable higher post-surgery activity levels. Growing awareness of periprosthetic joint infection costs stimulates interest in antimicrobial surfaces, while longer life expectancy pushes payers to reward devices with proven survivorship. Collectively, these shifts channel funding toward technologies that minimize revision risk and lower lifetime treatment costs.

Shift toward outpatient & day-case orthopedics

Enhanced recovery after surgery protocols have reduced average length of stay for total knee arthroplasty from 8.17 days to 5.92 days in multicenter European studies.[1]BMC, “Enhanced Recovery After Knee Arthroplasty,” bmcemery.com ASCs help clear pandemic-era backlogs, especially in the United Kingdom where waiting lists top 7.6 million cases. Device makers that can prove faster mobilization—through cementless fixation or tailored instrumentation—gain a contracting edge as hospitals benchmark throughput. Payers now track same-day discharge and 30-day readmission rates, cementing outpatient suitability as a core buying criterion across the Europe orthopedic devices market.

Rapid adoption of 3-D printed patient-specific implants

Point-of-care printing moves production from central warehouses to hospital basements, trimming inventory and customizing geometry. Platforms such as Arburg Plastic Freeforming enable biodegradable lattice structures that mimic cancellous bone, lowering stress shielding and improving osseointegration. Venture funding, evidenced by OSSTEC’s GBP 2.5 million raise in April 2025, validates the commercial case. EU-MDR pathways for custom devices favor firms with robust quality systems, which may consolidate share among larger incumbents able to absorb certification costs.

EU-MDR traceability driving smart implants

Extended transition deadlines to December 2027 for Class III devices temporarily reduce pressure, yet unique device identification and post-market surveillance rules still require integrated sensors or RFID chips for ease of tracking.[2]EUR-Lex, “EU Medical Device Regulation Transition Deadlines,” eur-lex.europa.eu Smart implants that automatically log performance data appeal to notified bodies and surgeons alike, helping companies justify premium pricing even as reimbursement tightens. Early adopters build proprietary data lakes that could evolve into predictive maintenance models, adding service revenue on top of hardware sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented reimbursement limits access | -0.9% | France, Germany, Italy | Medium term (2-4 years) |

| Stringent & costly EU-MDR conformity | -0.7% | EU-wide | Short term (≤ 2 years) |

| Titanium & rare-earth supply volatility | -0.5% | Global | Short term (≤ 2 years) |

| Limited orthopedic surgery workforce capacity | -0.4% | Netherlands, Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented reimbursement across the EU

France cut prosthesis tariffs by 25%, with a further 5.7% reduction planned by 2025, prompting some manufacturers to restrict portfolio breadth.[3]MedTech News, “France Cuts Prosthesis Reimbursement Tariffs,” medtechnews.comHealth technology assessment (HTA) timelines vary; evidence packs that pass German reference pricing may still face 12-month delays in Italy. The administrative load squeezes small enterprises, nudging them to license innovations rather than commercialize independently, thereby slowing product rotation in the Europe orthopedic devices market.

Limited orthopedic surgery workforce capacity

Several Eastern European regions operate with fewer than 6 orthopedic surgeons per 100,000 residents, compared with 15-plus in Germany. Training bottlenecks slow operating-room throughput, constraining procedure volumes that would otherwise be driven by demographic demand. Robotics and AI decision support partially mitigate the skill gap, yet staffing shortages remain a structural drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Joint Reconstruction Dominance Amid Orthobiologics Surge

Joint reconstruction implants held 38.72% Europe orthopedic devices market share in 2025, underlining their entrenched role in treating advanced osteoarthritis. At the same time orthobiologics posted the highest 4.28% CAGR, powered by platelet-rich fibrin and 3-D printed scaffolds that encourage bone regeneration. Demand for patient-specific knees and hips dovetails with surgeon interest in biologic augmentation, positioning integrated mechanical-biologic solutions as the next competitive frontier. Trauma fixation remains resilient, fueled by sports injuries and an aging yet active population. Spine devices advance on the back of navigation systems that limit soft tissue disruption and speed recovery.Orthobiologics uptake accelerates as aging but active Europeans seek grafts that restore function without metal hardware.

Clinical trials showing 100% union in complex hindfoot cases reinforce surgeon confidence. Meanwhile, craniomaxillofacial applications exploit additive manufacturing to tailor plates that match each patient’s contour, reducing OR time and improving cosmetic outcomes. Sports medicine implants extend durability through hybrid polymer-fiber constructs, anchoring the Europe orthopedic devices market in a trajectory that blends repair with regeneration.

By Material: Titanium Leadership Challenged by Bioabsorbable Innovation

Titanium held 39.65% Europe orthopedic devices market size in 2025. The alloy’s modulus and proven biocompatibility sustain its primacy in load-bearing roles; however, biodegradable PLGA and PEEK-fiber hybrids recorded a 5.12% CAGR, boosted by mandates to cut procedure-related waste. Hospitals appreciate the avoidance of second surgeries for screw removal in pediatric cases, a benefit translating directly into lower total treatment cost. Stainless steel continues in budget-sensitive trauma indications, while carbon-fiber-reinforced polymers win share in imaging-critical spine cages.

Supply risk drives interest in composites that reduce titanium content by 30%-plus without compromising fatigue life. Researchers demonstrate femoral stems in PEEK-ceramic matrices that lower stress shielding and distribute load more evenly along the shaft. Procurement teams now score bids on life-cycle CO₂ emissions, nudging OEMs to re-engineer packaging and sterilization processes. These seen-but-not-felt shifts add cumulative momentum to sustainable materials within the Europe orthopedic devices market.

By Application: Knee Procedures Lead While Spine Growth Accelerates

Knee procedures delivered 30.25% of the Europe orthopedic devices market size in 2025 as osteoarthritis prevalence climbed. Yet spine surgeries posted the fastest 4.73% CAGR, leveraging endoscopic techniques and expandable cages that shorten recovery. Hip arthroplasty maintains volume but increasingly features dual-mobility cups to curb dislocation. Trauma fixation grows at par with road-traffic patterns and sports activity, while extremities benefit from 3-D printed scaffolds that tackle complex revisions.

Spine’s momentum reflects better navigation suites that enhance pedicle screw precision even in osteoporotic bone. Surgeons now choose minimally invasive lateral approaches to reduce muscle trauma, enabling same-day discharge in select centers. Knee segment innovation focuses on kinematic alignment and patient-matched instrumentation, aided by AI planning tools that cut operative time. Collectively, these innovations sustain procedure diversity across the Europe orthopedic devices market.

By End User: Hospital Dominance Faces ASC Disruption

Hospitals captured 59.12% revenue in 2025, anchored by complex revision work and multi-disciplinary care. ASCs, however, clock a 5.56% CAGR on the strength of streamlined workflows and payer incentives that reward site neutral payments. Orthopedic specialty clinics carve niches in sports and limb reconstruction, supported by imaging suites and rehabilitation gyms co-located for convenience.

Public health systems increasingly steer low-risk joints and trauma cases to ASCs to clear tertiary centers for oncology and polytrauma. Implant vendors tailor product kitting for outpatient efficiency—supplying pre-sterilized single-use trays that cut turnover time by 25%. Remote monitoring apps feed data back to hospital command centers, reinforcing value-based metrics that shape implant formulary decisions within the Europe orthopedic devices market.

Geography Analysis

Germany accounted for 23.15% of the Europe orthopedic devices market in 2025 thanks to high surgeon density, robust insurance coverage, and a domestic manufacturing backbone that insulates against logistics shocks. Procedure volumes will climb further as the over-65 cohort expands, with primary knee replacements forecast to rise 55% by 2040. Reference pricing policies control costs yet still reimburse premium implants that deliver measurable quality-of-life gains, sustaining innovation flow.

The United Kingdom is set to post a 5.92% CAGR through 2031. UKCA marking offers an alternative route to market that can shave months off approval times, encouraging early launch of robotics and patient-specific knees. NHS capital budgets emphasize theatres capable of 23-hour stays, marrying throughput targets with patient satisfaction goals. Cutting waiting lists from 142 days toward the European average focuses political attention on surgical capacity and technology adoption.

France continues to purchase high volumes but faces 25% tariff cuts on prostheses that squeeze hospital budgets. Despite reimbursement pressure, centers of excellence in Lyon and Strasbourg adopt smart implants that self-report kinematics, justifying higher upfront spend with lower readmission risk. Italy and Spain lag on total spend yet demonstrate quick HTA turnaround for devices backed by strong real-world evidence. Eastern European markets such as Poland and Romania promise longer-run upside but must address surgeon scarcity before volumes surge. Overall, regional heterogeneity obliges suppliers to tailor access plans while they scale the Europe orthopedic devices market.

Competitive Landscape

The competitive profile is moderately consolidated. Zimmer Biomet, Stryker, and DePuy Synthes dominate core joints, together exceeding 50% of reconstruction revenue. Each pairs flagship implants with proprietary robotics, supporting lock-in through integrated pre-op planning and analytics. Stryker’s Mako suite now includes shoulder capabilities, widening addressable procedures. Zimmer Biomet’s 2025 CE marks for Persona® Revision and RibFix Advantage® underscore iterative expansion of recognized brands.

Mid-tier challengers pursue breadth through M&A. Enovis paid EUR 800 million for LimaCorporate in 2024, securing trabecular titanium know-how for complex recon work. Smith & Nephew buys AI navigation startups to leapfrog planning software gaps. Arthrex broadens sports medicine while investing in bioabsorbables that align with EU greening rules. Start-ups such as OSSTEC leverage hospital-based printing cells, offering two-week turnaround on custom femoral condyles—far faster than global logistics can move finished goods.

Supply chain vigilance remains central. OEMs dual source titanium billet, build additive powder stockpiles, and qualify alternate alloy chemistries. Regulatory compliance acts as both moat and hurdle: large players fund internal notified-body liaison teams, whereas small innovators often partner with contract manufacturers that already hold MDR certifications. Taken together, these forces sustain dynamic rivalry yet keep overall structure disciplined within the Europe orthopedic devices market.

Europe Orthopedic Devices Industry Leaders

Zimmer Biomet Holdings Inc.

Stryker Corporation

DePuy Synthes (Johnson & Johnson)

B. Braun SE

Arthrex Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OSSTEC raised GBP 2.5 million to commercialize 3-D printed joint replacements for hospital-based production.

- March 2025: Johnson & Johnson MedTech obtained CE marking for the VOLT Plating System ahead of European rollout.

- February 2025: Zimmer Biomet reported USD 7.679 billion FY 2024 sales and secured CE marks for the Persona Revision Knee and RibFix Advantage systems.

- October 2024: Zimmer Biomet completed the acquisition of OrthoGrid Systems Inc. to enhance AI guidance in hip replacement.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the Europe orthopedic devices market as all manufactured implants, fixation systems, orthobiologic preparations, and powered tools that are permanently or temporarily introduced inside the human body to replace, restore, or stabilize bones and joints following trauma, degenerative disease, or congenital deformity.

Scope Exclusions: Non-implant consumables such as surgical gowns, external braces, and imaging capital equipment are outside our scope.

Segmentation Overview

- By Device Type

- Joint Reconstruction Implants

- Trauma Fixation Devices

- Spine Surgery Devices

- Craniomaxillofacial Devices

- Sports Medicine & Arthroscopy Devices

- Orthobiologics

- Other Orthopedic Devices

- By Material

- Titanium & Titanium Alloys

- Stainless Steel

- Polymeric Biomaterials

- Bioabsorbable & Composite Materials

- Others

- By Application

- Hip Orthopedic Procedures

- Knee Orthopedic Procedures

- Spine Orthopedic Procedures

- Trauma Fixation

- Other Applications

- By End User

- Hospitals

- Orthopedic & Specialty Clinics

- Ambulatory Surgical Centers (ASCs)

- Others

- By Geography

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed European orthopedic surgeons, procurement managers at hospitals and ambulatory surgical centers, notified-body consultants, and material suppliers across Germany, the UK, France, Italy, Spain, and the Nordics. These discussions validated implant mix shifts, ASP movements, and MDR-driven product sunset timelines, filling data gaps left by public sources.

Desk Research

We began with public datasets from Eurostat, OECD Health Statistics, the European Federation of National Associations of Orthopaedics and Traumatology, and national procedure registries such as the UK National Joint Registry. These quantified replacement and fixation volumes and pricing baselines. Company 10-Ks, CE-mark approval databases, and reputable trade journals supplied average selling price (ASP) trends and upcoming product launches. Where deeper financial or shipment splits were needed, our analysts accessed D&B Hoovers, Dow Jones Factiva, and Questel patent analytics to benchmark competitive intensity. This list is illustrative, and many additional sources were consulted for triangulation.

Market-Sizing & Forecasting

A blended top-down reconstruction of the demand pool, built from annual hip, knee, spine, and trauma procedure counts multiplied by weighted ASPs, served as the starting point. Results were cross-checked through sampled supplier roll-ups and channel checks to refine totals. Key variables in the model include elective surgery rebound rates, average implant-per-procedure ratios, titanium price trends, EU-MDR compliance costs, and penetration of robot-assisted arthroplasty. A multivariate regression atop these indicators projected revenue through 2030, while scenario analysis adjusted for currency shifts and reimbursement reforms.

Data Validation & Update Cycle

Outputs pass variance and outlier screens, followed by multi-analyst peer review. We refresh each model annually and trigger interim updates when regulatory, pricing, or merger events materially skew baselines. A final analyst pass occurs before every client delivery.

Why Mordor's Europe Orthopedic Devices Baseline Earns Trust

Published estimates rarely match because publishers choose different device mixes, ASP assumptions, and refresh cadences.

Our disciplined definition, annual update rhythm, and dual-path modeling keep the baseline dependable for decision makers.

Key gap drivers include: some firms fold external braces into revenue pools, others apply global ASPs without EU MDR mark-up, and a few model future volumes on aggressive robotic uptake scenarios rather than the balanced adoption rates our surgeons reported.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.21 B (2025) | Mordor Intelligence | - |

| USD 12.89 B (2024) | Regional Consultancy A | Uses broader product basket yet older procedure counts, inflating unit volumes while understating ASP progress |

| USD 15.80 B (2024) | Trade Journal B | Includes accessories such as screws and sutures that fall outside implant definition |

| USD 13.49 B (2025) | Global Consultancy C | Applies uniform 5.4 % CAGR from 2019 without revising for post-COVID elective backlog normalization |

In summary, our transparent variable selection, balanced scenario work, and constant validation deliver a market view that clients can reproduce and confidently use as a strategic baseline.

Key Questions Answered in the Report

What is the current size of the Europe orthopedic devices market?

The Europe orthopedic devices market is valued at USD 14.74 billion in 2026 and is projected to reach USD 17.69 billion by 2031.

Which segment is expanding fastest?

Orthobiologics lead growth with a 4.28% CAGR as surgeons adopt regenerative approaches for younger, active patients.

How big is Germany’s share of the market?

Germany accounts for 23.15% of regional revenue, reflecting high procedure volumes and robust healthcare funding.

Why are ambulatory surgical centers important?

ASCs post a 5.56% CAGR because enhanced recovery protocols allow same-day discharge, relieving hospital capacity constraints.

Page last updated on: