Market Overview

| Study Period | 2020 - 2031 |

|---|---|

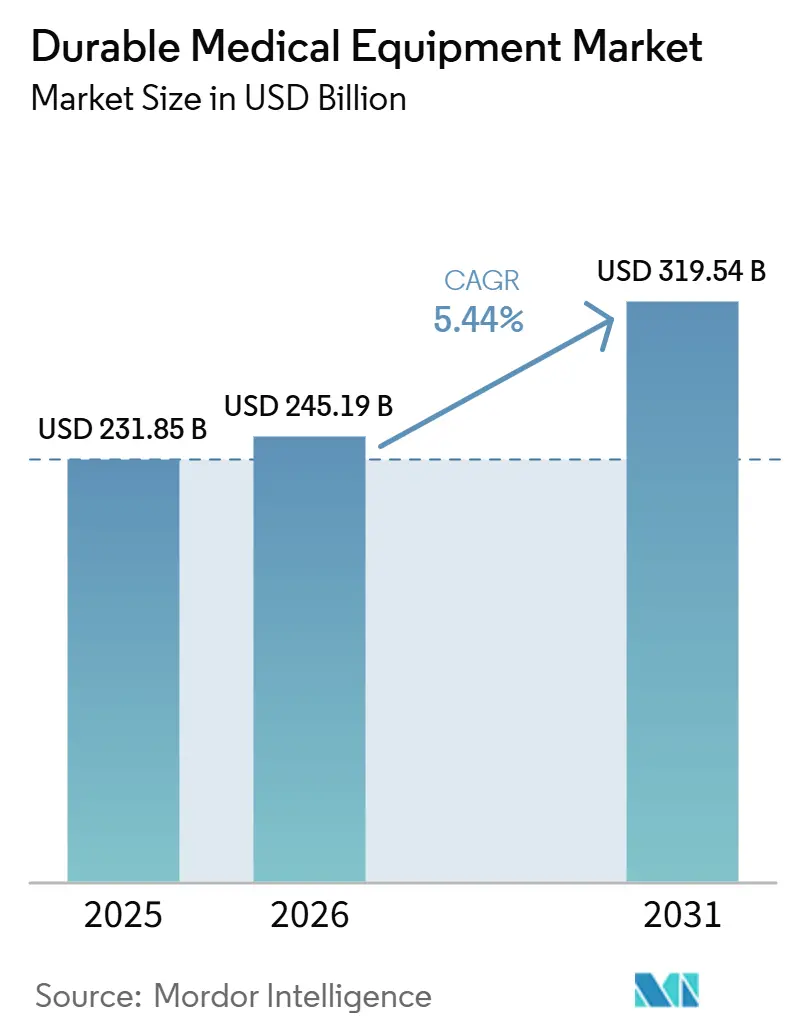

| Market Size (2026) | USD 245.19 Billion |

| Market Size (2031) | USD 319.54 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Durable Medical Equipment Market Analysis by Mordor Intelligence

The Durable Medical Equipment Market size was valued at USD 231.85 billion in 2025 and is estimated to grow from USD 245.19 billion in 2026 to reach USD 319.54 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

The durable medical equipment market is transitioning toward home-based chronic-care delivery as reimbursement lifts, IoT connectivity embeds in everyday devices, and predictive software lowers ownership costs. North American payers led by Medicare are rewarding technology-assisted rehabilitation over labor-intensive visits, while Japan and several European systems expand coverage for wheelchairs, hospital beds, and oxygen solutions. Hospital procurement strategies now prize energy-efficient and service-bundled hardware, spurring vendors to add predictive maintenance and remote firmware updates. Online and direct-to-patient fulfillment further compresses channel costs, letting consumers receive equipment within hours in major U.S. metros. Competitive positioning hinges on integrating device hardware with analytics platforms, accelerating acquisitions of niche software firms and sparking new subscription models that align cash flow with utilization.

Key Report Takeaways

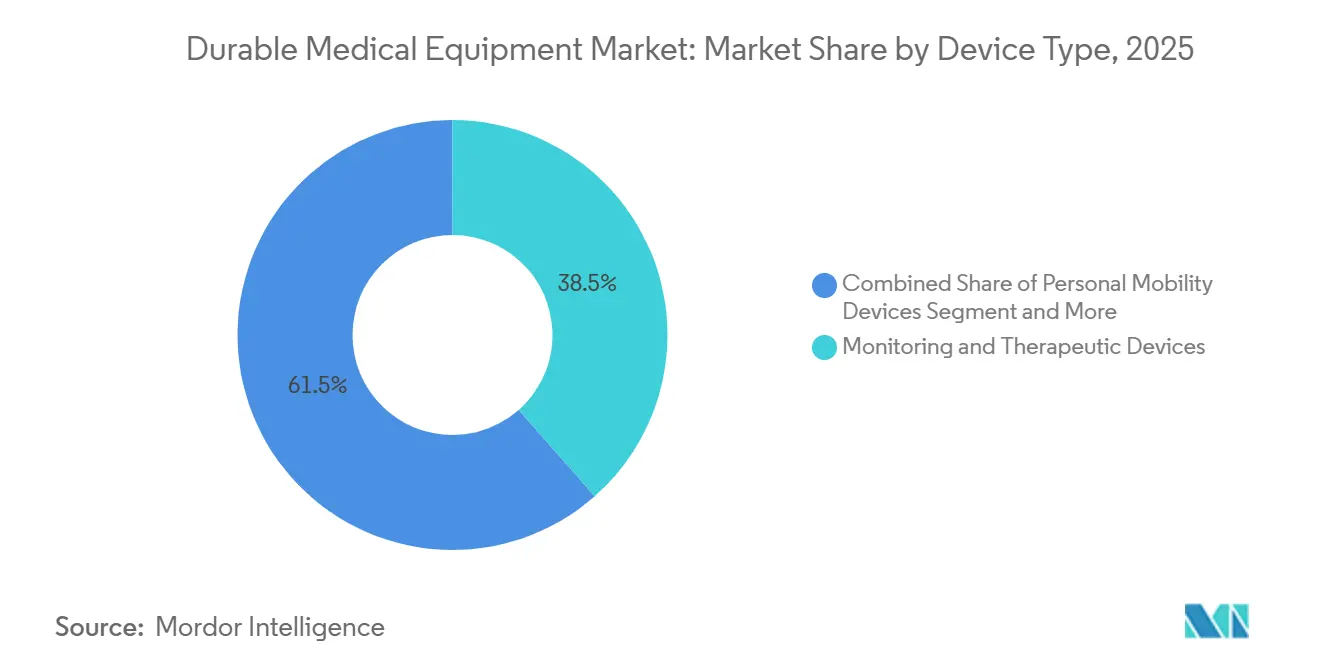

- By device type, monitoring and therapeutic devices commanded 38.55% of durable medical equipment market share in 2025; the same segment is forecast to accelerate at an 8.25% CAGR to 2031.

- By end-user, hospitals and clinics accounted for 53.53% of the durable medical equipment market size in 2025, whereas home-healthcare settings are projected to expand at a 9.85% CAGR through 2031.

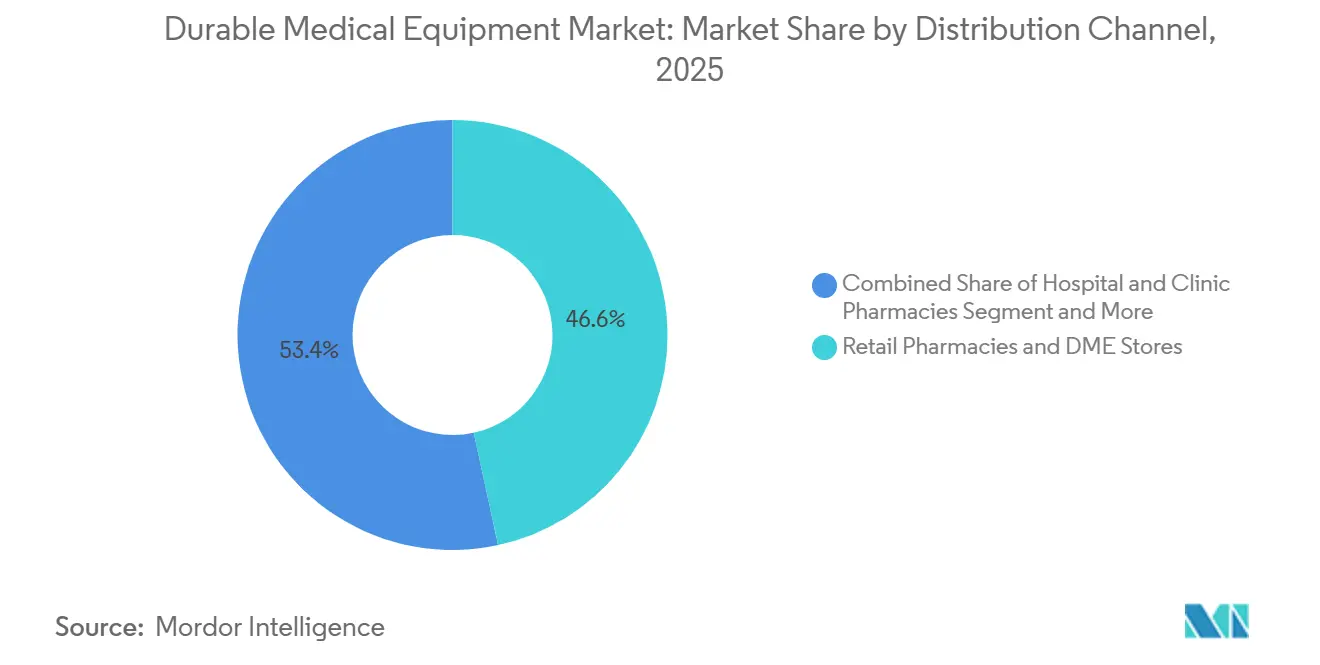

- By distribution channel, retail pharmacies and durable medical equipment stores led with 46.63% revenue share in 2025, while online and direct-to-patient channels are advancing at an 11.87% CAGR through 2031.

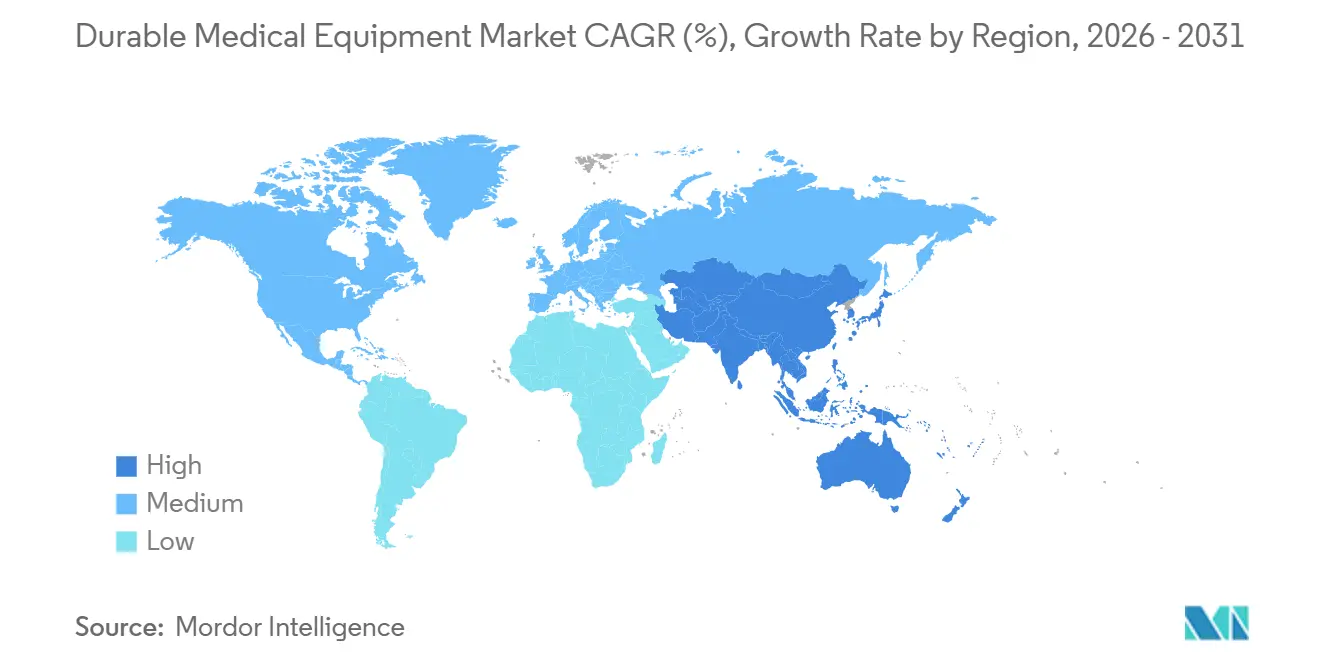

- By geography, North America held a 41.13% share of the durable medical equipment market in 2025, whereas Asia-Pacific is registering the highest regional CAGR at 8.51% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Durable Medical Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly ageing population sustaining mobility & respiratory demand | +1.8% | Global, peak impact in Japan, Europe, North America | Long term (≥ 4 years) |

| IoT-enabled device ecosystems improving adherence & data monetisation | +1.2% | North America & EU, early adoption in urban APAC | Medium term (2-4 years) |

| Shift to home-based chronic-care supported by reimbursement expansion | +1.5% | North America, Japan, Australia; emerging in China, India | Medium term (2-4 years) |

| AI-driven predictive maintenance lowering TCO for providers | +0.6% | North America & EU hospitals, spill-over to APAC | Long term (≥ 4 years) |

| E-commerce & DTP fulfilment compressing channel costs | +0.9% | North America, UK; nascent in urban China, India | Short term (≤ 2 years) |

| ESG-linked hospital cap-ex boosting energy-efficient equipment refresh | +0.5% | EU (NHS England, Germany), North America (select systems) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Ageing Population Sustaining Mobility and Respiratory Demand

Japan’s share of citizens aged 75 years and older surpassed 15% in 2025, pushing purchases of wheelchairs, walkers, and oxygen concentrators covered by the long-term care insurance program that reimburses up to 90% of device costs [1]Ministry of Health, Labour and Welfare, “Long-Term Care Insurance Statistics,” mhlw.go.jp. Eurostat forecasts Europe’s population aged 65 and above to reach 30% by 2050, prompting national payers to subsidize home-based respiratory therapy and mobility aides. CMS projects Medicare enrollment to rise to 80 million by 2030, enlarging the addressable base for powered wheelchairs and CPAP systems. Germany allocated EUR 450 billion in 2024 health spending, with a rising share earmarked for assistive technology under social insurance rules. Safety standards such as ISO 7176 and IEC 60601 help ensure devices supplied to seniors meet durability and electrical requirements, reducing liability for providers.

IoT-Enabled Device Ecosystems Improving Adherence and Data Monetization

Connected glucose monitors, pulse oximeters, and portable ventilators increasingly pair with smartphones, transmitting real-time readings to cloud dashboards. Abbott’s FreeStyle Libre 2 Plus transmits glucose data directly to Apple Health, allowing physicians to adjust dosing without clinic visits. ResMed’s AirSense 11 CPAP streams usage metrics to clinicians, cutting 30-day readmissions for obstructive sleep apnea by 18% in a 2024 multi-site study. The FDA’s TEMPO model grants automatic Medicare coverage for breakthrough connected devices within two days of approval, slashing time-to-reimbursement and encouraging rapid commercial launches. However, heterogeneous data standards slow cross-platform analytics, motivating adoption of HL7 FHIR for interoperability across vendor ecosystems.

Shift to Home-Based Chronic Care Supported by Reimbursement Expansion

The 2025 Medicare Home Health Prospective Payment System boosted the base payment rate by 2.6% and introduced therapy thresholds favoring equipment-assisted rehabilitation over staff-heavy visits. Japan expects home medical care recipients to top 1.6 million by 2029, catalyzed by reimbursement for beds and wheelchairs. China earmarked subsidies for fall-detection sensors and smart vitals monitors under its 14th Five-Year Plan for aging services. The NHS “hospital at home” program deploys portable infusion pumps and connected vitals monitors, reducing acute-bed use by 12% in 2024. Risk-management standards such as ISO 14971 and privacy regulations like GDPR govern the roll-out of home-use equipment, protecting patient safety and data.

AI-Driven Predictive Maintenance Lowering TCO for Providers

GE HealthCare’s Asset Performance Management analyzes vibration and temperature data from imaging and monitoring fleets, predicting failures up to two weeks in advance and reducing unplanned outages by 25% across early-adopter hospitals. Philips HealthSuite automates service tickets and parts ordering for 15,000 connected devices, lifting uptime by roughly 20% across European clients. Siemens Healthineers trains neural networks on tens of millions of service events to recommend optimal maintenance windows, trimming mean repair times to 18 hours. Draft FDA guidance on predetermined change-control plans lets manufacturers update AI algorithms without fresh 510(k) submissions, accelerating roll-outs of self-learning maintenance software. Compliance with IEC 62304 keeps cybersecurity and software lifecycle processes in check.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront & lifecycle service costs | -0.9% | Global, acute in emerging markets with limited financing | Medium term (2-4 years) |

| Uptake of GLP-1 obesity drugs reducing mobility-aid volumes | -0.7% | North America, EU; emerging in urban APAC | Short term (≤ 2 years) |

| Skilled biomedical-tech labour shortages lengthening service cycles | -0.4% | North America, EU, Australia; spill-over to urban APAC | Long term (≥ 4 years) |

| Fragmented post-sale data standards hampering interoperability | -0.3% | Global, most acute in North America & EU multi-vendor sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Service Costs

Advanced power wheelchairs with IoT sensors list between USD 15,000 and USD 40,000, while smart hospital beds range from USD 8,000 to USD 25,000, challenging budgets where third-party reimbursement is thin. Preventive maintenance and software updates frequently add 20% to ownership expenses over five years, extending replacement cycles and increasing downtime risk. Biomedical technician shortages keep hourly service rates high across mature markets, with the U.S. Bureau of Labor Statistics expecting only 5% employment growth through 2032. Subscription bundles from equipment-as-a-service vendors absorb the upfront hit by spreading costs over monthly invoices. In Europe, MDR post-market surveillance updates every two years add EUR 50,000–200,000 per product line, expenses generally passed to buyers.

Uptake of GLP-1 Obesity Drugs Reducing Mobility-Aid Volumes

Prescriptions for semaglutide and tirzepatide climbed sharply through 2024, helping patients shed weight and regain mobility, thereby tempering demand for wheelchairs and walkers. Insulin-pump sales are also expected to slow as Type 2 diabetes prevalence eases in treated populations; manufacturers are pivoting toward smart-home integration and fall-detection to reposition mobility platforms as preventive-care hubs. CPAP volumes face similar headwinds where weight loss alleviates obstructive sleep apnea, pushing vendors to enhance adherence analytics and cloud services to retain value. Mobility-equipment makers showcased sensor-rich devices with gait analysis and telehealth integration at the 2024 Medtrade conference, underscoring the strategic pivot toward proactive monitoring.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring and Therapeutic Equipment Dominates

Monitoring and therapeutic devices held a 38.55% share of the durable medical equipment market in 2025 and are on track to expand at an 8.25% CAGR to 2031, outperforming mobility aids and bathroom-safety products. OTC glucose monitors like Abbott FreeStyle Libre 2 Plus and Dexcom Stelo remove finger-stick calibration and sync to mobile health apps, spurring double-digit unit growth across North America [2]Abbott Laboratories, “FreeStyle Libre 2 Plus Now Available,” abbott.com. Philips Respironics’ multi-year recall shifted sleep-apnea demand to ResMed, whose cellular-enabled AirSense 11 helped reduce hospital readmissions by 18% in pilot programs, strengthening its foothold.

Growth momentum continues as payers reimburse remote vital-sign monitors used in home-health programs, helping the durable medical equipment market size for monitoring devices widen. Yet insulin-pump volumes face pressure from obesity-drug uptake, pushing pump makers to concentrate on pediatric and Type 1 diabetes niches. Oxygen concentrators and CPAP systems benefit from mHealth connectivity that supports remote adherence tracking. In contrast, personal mobility devices confront slower growth; to offset volume headwinds, power-chair vendors now embed fall-detection sensors and posture-adjustment algorithms that collect usable clinical data, reinforcing their role in value-based care pathways.

By End-User: Hospitals Remain Core, but Home Health Scales Faster

Hospitals and clinics represented 53.53% of durable medical equipment market share in 2025, underpinned by complex ventilators, high-acuity beds, and advanced imaging systems. However, home-healthcare agencies are expanding revenue at a 9.85% CAGR as reimbursement incentives shift chronic care outside the hospital walls. Japan’s long-term care insurance and China’s provincial subsidies blaze a path that normalizes hospital-grade equipment in living rooms, thereby enlarging the durable medical equipment market size devoted to residential settings.

Hospital demand remains resilient for intensive-care ventilators and surgical navigation platforms, yet ambulatory surgery centers are deploying mobile C-arms and compact ultrasounds to support same-day procedures. Nursing homes and hospices abide by value-based contracts penalizing readmissions, so they procure IoT beds and remote monitoring mats to detect deterioration early. The dual-track demand pattern - high acuity in facilities, growing acuity at home - forces suppliers to design modular devices that meet diverse power, service, and data requirements across settings.

By Distribution Channel: Digital Fulfillment Gains Pace

Retail pharmacies and brick-and-mortar DME stores captured 46.63% of 2025 revenue, but online and direct-to-patient channels are sprinting at an 11.87% CAGR. Amazon Pharmacy covers same-day equipment delivery for nearly half of U.S. households, raising consumer expectations for immediate access. CVS Health now embeds DME ordering in its mobile experience, shrinking discharge delays for hospitals that need home-bound patients equipped rapidly. European regulators enforce ISO 13485 and GDPR in e-commerce sales, safeguarding product quality and data privacy while enabling cross-border transactions that enlarge the durable medical equipment market.

High-touch products such as custom wheelchairs still rely on physical fittings, but pharmacies counter e-commerce pressure by installing in-store clinics for training and same-day setup. Delivery partners like DoorDash and Uber partner with national chains to meet four-hour fulfillment targets in urban corridors, further tightening the logistics race. The FDA’s rapid-coverage TEMPO model accelerates OTC launches for connected monitors, accelerating direct-to-consumer demand.

Geography Analysis

North America remains the largest regional contributor at 41.13% share in 2025, buoyed by rising Medicare enrollment and CMS policy that lifts home-health reimbursement. The FDA’s expedited coverage for breakthrough devices shrinks commercialization timelines, accelerating adoption of IoT monitors and AI-enhanced oxygen concentrators. Amazon Pharmacy’s logistics backbone supports rapid equipment delivery, helping online sales climb, while Canada’s Assistive Devices Program funds up to 75% of eligible product costs, expanding access. Mexico’s social insurance pilots portable oxygen services in rural areas, cutting hospital admissions.

Asia-Pacific is the fastest-growing arena at an 8.51% CAGR to 2031, propelled by Japan’s “2025 problem” demographic shift and China’s preference for aging in place. India’s Ayushman Bharat Digital Mission created unique health IDs for half a billion citizens, smoothing telemedicine prescriptions for home-use monitors. South Korea reimburses up to 80% of portable oxygen rentals, while Australia’s National Disability Insurance Scheme funds assistive technology for more than 600,000 participants.

Europe carries substantial weight behind aging demographics and ESG procurement goals. Germany channels social insurance toward assistive devices, the NHS commits to net-zero procurement, and France’s Silver Economy initiative subsidizes home-medical kits, pushing lifecycle-low-carbon equipment into mainstream demand. EU-wide medical device regulation mandates post-market surveillance that raises compliance barriers but uplifts safety, reinforcing buyer confidence in long-lasting equipment that anchors the durable medical equipment market.

Competitive Landscape

The top vendors, Abbott, Medtronic, ResMed, Philips, Stryker, Baxter, GE HealthCare, Siemens Healthineers, Invacare, and Masimo collectively control a meaningful yet not dominant slice of the durable medical equipment market, with many niche players filling gaps in mobility, bathroom safety, and home-monitoring lines. Integration of software layers drives M&A: Abbott folded Bigfoot Biomedical’s insulin-dosing algorithms into its Libre ecosystem in 2024, while Medtronic bought Cardiovascular Systems to deepen its vascular catalog. ResMed’s 2023 pickup of Brightree secures recurring SaaS fees from DME suppliers, boosting stickiness[3]ResMed Inc., “ResMed Acquires Brightree,” resmed.com.

Philips Respironics’ recall opened a USD 1.1 billion liability and redirected sleep-apnea demand toward ResMed and regional makers. Invacare’s 2023 Chapter 11 exit ceded share to Drive DeVilbiss and Sunrise Medical in manual mobility equipment, highlighting the market’s susceptibility to supply disruptions. Vendors differentiate by embedding AI-assisted maintenance and subscription financing; GE HealthCare and Philips roll predictive-maintenance dashboards that guarantee uptime in leasing models, while Masimo enters consumer wearables with sensor-rich baby and temperature monitors. Remanufactured systems gain ground as the NHS and other buyers chase carbon-reduction targets, favoring fleets with 30–50% lower embodied emissions.

Durable Medical Equipment Industry Leaders

Getinge AB

Medtronic PLC

Compass Health Brands

GE Healthcare

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Quipt Home Medical acquired a full-service DME provider from Ballad Health, strengthening its U.S. respiratory-care footprint.

- February 2025: NYC Health + Hospitals’ NYC Care program launched a benefit that lets eligible patients obtain low- or no-cost durable medical equipment across all system facilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the durable medical equipment (DME) market as the worldwide sale of reusable, non-implantable devices, mobility aids, therapeutic and monitoring equipment, and bathroom safety furniture that are prescribed for chronic or post-acute care and withstand repeated home or clinical use. The 2025 baseline size is USD 232.54 billion, with value tracked across all major geographies and primary distribution channels.

Scope Exclusions: Single-use disposables, implantable devices, and purely diagnostic consumables sit outside this assessment.

Segmentation Overview

- By Device Type

- Personal Mobility Devices

- Wheelchairs

- Crutches & Canes

- Walkers & Rollators

- Other Personal Mobility Devices

- Bathroom Safety Devices & Medical Furniture

- Medical Beds & Mattresses

- Commodes & Toilets

- Other Bathroom Safety & Medical Furniture

- Monitoring & Therapeutic Devices

- Blood Glucose Monitors

- Oxygen Equipment

- Vital-sign Monitors

- Other Monitoring & Therapeutic Devices

- Personal Mobility Devices

- By End-User

- Hospitals & Clinics

- Home-Healthcare Settings

- Ambulatory Surgical Centres

- Other End-Users

- By Distribution Channel

- Hospital & Clinic Pharmacies / DME Suppliers

- Retail Pharmacies & DME Stores

- Online & Direct-to-Patient Channels

- Business-to-business (B2B)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed purchasing managers at hospital groups, home-care providers, and regional distributors in North America, Europe, and six high-growth Asian economies. Follow-up surveys with respiratory therapists and physiatrists verified utilization shifts and average replacement cycles, enabling us to tighten assumptions that secondary sources left ambiguous.

Desk Research

We began by mapping official statistics from bodies such as the Centers for Medicare & Medicaid Services, Eurostat, Japan's MHLW, and the World Bank, which clarify patient pools, healthcare spend, and reimbursement ceilings. Trade associations, including AAHomecare and Medtech Europe, offered shipment trends, while customs databases and patent analytics (Questel) helped us flag technology diffusion. Company 10-Ks, investor decks, and Factiva news archives then anchored typical average selling prices (ASP) and competitive moves. The desk-research sources quoted here are illustrative; numerous additional publications and datasets informed our evidence base.

Market-Sizing & Forecasting

A top-down construct, rooted in national health-expenditure tables and import-export reconciliations, established the total demand pool, which was subsequently cross-checked through selective bottom-up roll-ups of leading suppliers' revenue disclosures. Key variables include: (1) population aged 65 and older, (2) prevalence of diabetes and COPD, (3) mix shift toward home-based care, (4) reimbursement coverage ratios, and (5) median ASP evolution across mobility, respiratory, and wound-care device clusters. Forecasts rely on multivariate regression coupled with scenario analysis to capture reimbursement reforms and technology adoption curves; gaps in bottom-up input are bridged by regional channel checks and median ASP imputation.

Data Validation & Update Cycle

Outputs undergo variance tests against external market signals, peer ratios, and historical series before senior analyst sign-off. Reports refresh annually, and mid-cycle updates are triggered when material policy or recall events change demand indicators.

Why Mordor's Durable Medical Equipment Baseline Earns Trust

Published estimates often diverge because analysts select dissimilar product baskets, price conventions, and refresh cadences. Mordor's disciplined scope alignment and dual-path modeling keep our baseline reproducible and balanced for strategic planning.

These comparisons show that scope breadth, ASP inputs, and validation rigor materially steer results; our blended top-down corroborated by field insights gives decision-makers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 232.54 B (2025) | Mordor Intelligence | - |

| USD 221.35 B (2023) | Global Consultancy A | Excludes bathroom safety furniture; infers totals from hospital procurement only |

| USD 232.33 B (2024) | Trade Journal B | Adds rental-service revenue and consumables, inflating base |

| USD 241.50 B (2024) | Industry Data Service C | Assumes rapid smart-device uptake, limited primary validation |

These comparisons show that scope breadth, ASP inputs, and validation rigor materially steer results; our blended top-down corroborated by field insights gives decision-makers a dependable starting point.

Key Questions Answered in the Report

How large will the durable medical equipment market be by 2031?

It is projected to reach USD 319.54 billion, supported by a 5.44% CAGR driven by home-based chronic-care expansion.

Which device category leads sales?

Monitoring and therapeutic devices held 38.55% revenue share in 2025 and maintain the fastest 8.25% CAGR.

Which region shows the highest growth momentum?

Asia-Pacific posts the fastest 8.51% CAGR through 2031 as Japan's aging demographics and China's home-care subsidies expand demand.

How are recalls reshaping competition?

Philips Respironics' recall shifted sleep-apnea patients to ResMed and smaller rivals, altering share positions and accelerating investment in connected CPAP analytics.

What role do online channels play?

Same-day and next-day fulfillment services from Amazon Pharmacy and pharmacy chains push e-commerce revenue, particularly for OTC monitors and mobility aids.

Page last updated on: