Europe Irrigation Pumps Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.30 Billion |

| Market Size (2026) | USD 2.5 Billion |

| Market Size (2031) | USD 3.80 Billion |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

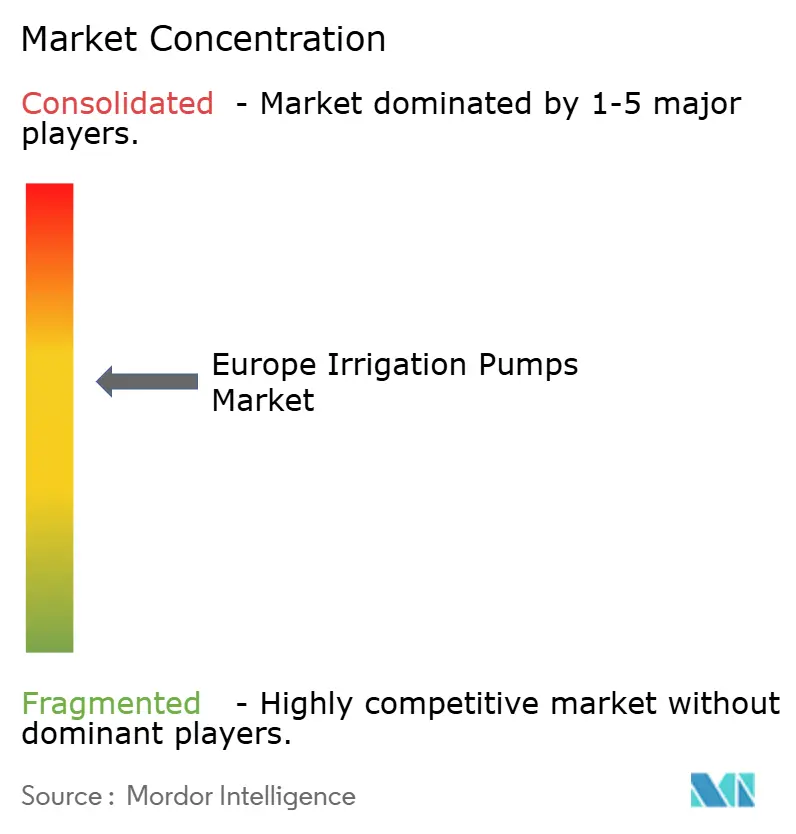

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Irrigation Pumps Market Analysis by Mordor Intelligence

The Europe irrigation pumps market size is projected to be USD 2.30 billion in 2025, USD 2.5 billion in 2026, and reach USD 3.80 billion by 2031, growing at a CAGR of 8.80% from 2026 to 2031. This expansion reflects a reset in farm-water infrastructure rather than a short replacement cycle, as growers and irrigation bodies move away from older fixed-speed systems toward efficient and monitored pump sets. Planned support under the Common Agricultural Policy 2021 to 2027 directed EUR 31.4 billion (USD 33.9 billion) toward farm investment programs that include irrigation modernization, and water metering remains a key condition for support in many cases[1]Source: European Parliament and Council, “Regulation (EU) 2021/2115 Establishing Rules on Support for CAP Strategic Plans,” ndfr.nl. The Europe irrigation pumps market is also being shaped by stronger pressure in southern basins, rising interest in solar and hybrid pumping, and greater use of digital controls that cut power use and improve compliance. Demand remains uneven across the region because southern countries carry the heaviest irrigation dependence, while northern and eastern countries are modernizing from a lower installed base. The main risk is that efficiency upgrades can still support more irrigated acreage instead of lower abstraction, while small and mid-size farms can still struggle with the remaining co-payment after subsidy support.

Key Report Takeaways

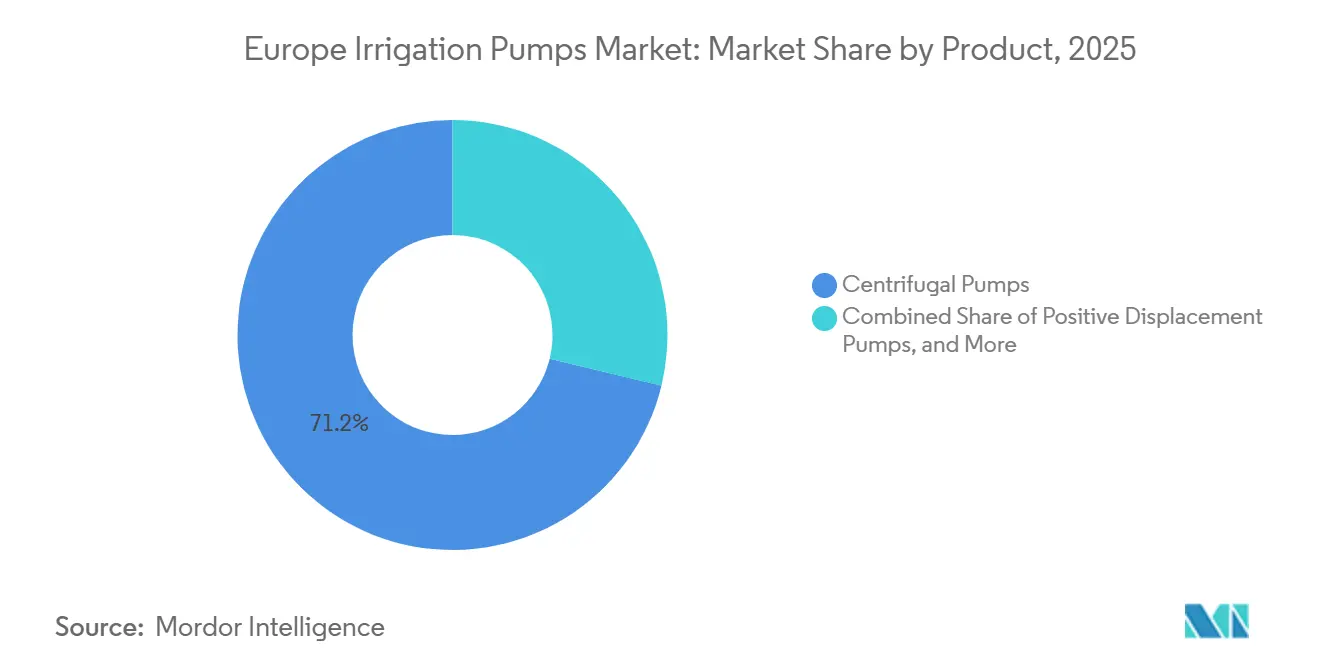

- By product type, centrifugal pumps were the largest segment and held 71.2% of Europe irrigation pumps market share in 2025, while positive displacement pumps are the fastest segment and are forecast to expand at an 8.2% CAGR from 2026 to 2031.

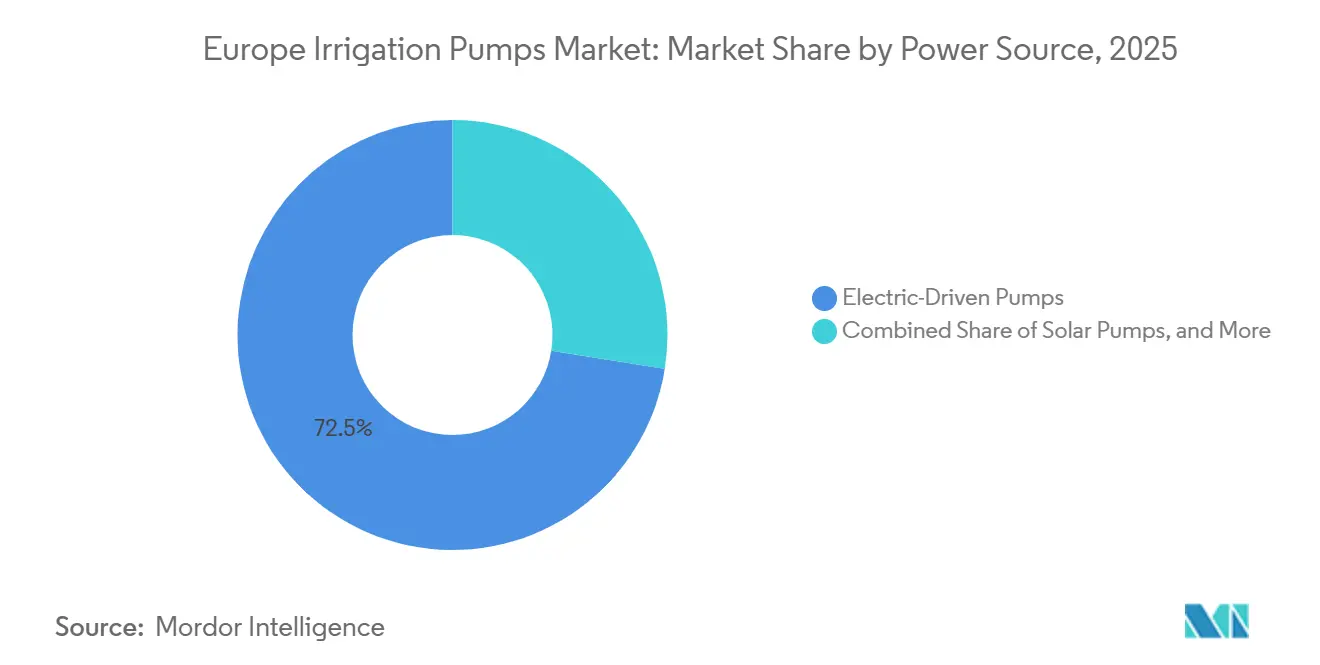

- By power source, grid-electric pumps were the largest segment and held 72.5% of Europe irrigation pumps market size in 2025, while solar pumps are the fastest segment and are forecast to grow at a 7.4% CAGR from 2026 to 2031.

- By geography, Germany was the largest country segment and held 25.7% of revenue in 2025, and Germany is also the fastest country segment with a 7.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Irrigation Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-scarcity-driven retrofit of legacy irrigation pumps | +2.0% | Spain, Italy, France, and Germany | Short term (≤ 2 years) |

| CAP-backed irrigation modernization spending | +1.8% | Europe-wide, concentrated in France, Germany, Spain, and Italy | Medium term (2-4 years) |

| Precision irrigation and variable frequency drive-linked pump automation | +1.5% | Germany, Netherlands, France, and Italy | Medium term (2-4 years) |

| Solar and hybrid pumping economics improving | +1.2% | Spain, Italy, Portugal, with spillover to France and Germany | Medium term (2-4 years) |

| Reclaimed-water irrigation creates retrofit demand | +0.9% | Spain, Italy, and France | Long term (≥ 4 years) |

| Vineyard, orchard, and greenhouse irrigation intensity | +0.7% | Spain, Italy, France, and Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Water-Scarcity-Driven Retrofit of Legacy Irrigation Pumps

Water stress is no longer treated as a seasonal operating issue in the Europe irrigation pumps market. It is becoming an administrative trigger for equipment renewal in basins where abstraction is already under pressure. The Joint Research Centre reported in February 2026 that human activity appropriates 10% to 50% of renewable freshwater in most European regions, while southern and Mediterranean areas face the greatest overuse pressure[2]Source: Joint Research Centre, European Commission, “Europe’s Renewable Freshwater, in Majority of Regions, Up to Half Appropriated by Humans,” joint-research-centre.ec.europa.eu. These conditions favor replacement of older fixed-speed assets that lack metering and cannot easily meet current monitoring needs. In practice, growers are not just buying a new pump. They are replacing an older irrigation setup with a system that can track flow, support control functions, and fit within stricter basin management rules.

Common Agricultural Policy (CAP)-Backed Irrigation Modernization Spending

The Common Agricultural Policy spending cycle remains one of the clearest supports for the Europe irrigation pumps market. Planned investment under the 2021 to 2027 framework reached EUR 31.4 billion (USD 33.9 billion), covering European Union and national co-financing for farm and irrigation projects under Articles 73 and 74. The 2025 proposal also kept water management and soil health visible in the next policy cycle, signaling continuity rather than a one-period support window. France, Spain, Germany, and Italy remain the most active national funding centers because they are the largest recipients of Common Agricultural Policy support and also run sizable irrigation modernization pipelines. A key point is that metering is often required before subsidy approval. That rule pushes older pump fleets onto a regulatory replacement schedule rather than a purely voluntary spending cycle.

Precision Irrigation and Variable Frequency Drive-Linked Pump Automation

Precision control is giving the Europe irrigation pumps market a stronger operating case even when subsidy access is limited. Variable frequency drives reduce power draw by matching motor speed to actual irrigation demand instead of forcing a pump to run at a constant rate. Franklin Electric Co., Inc. stated in 2024 that variable speed integration can cut electricity use by 20% to 60% in irrigation pump applications, which changes the payback case for growers with large seasonal pumping loads[3]Source: Franklin Electric Co., Inc., “Cost-Efficient and Flexible Irrigation with the Latest Well Pump Technology,” franklinwater.eu. Emotron AB also documented field use of its drives in German irrigation through installations deployed by Porsch Irrigation, showing that energy control and pressure stability matter together in precision systems. This matters most in Germany, the Netherlands, France, and Italy, where higher-specification farming systems can justify advanced controls more quickly. It also changes competition because suppliers with remote diagnostics, speed control, and system monitoring can capture more value than firms that only sell pump hardware.

Solar and Hybrid Pumping Economics Improving

Solar and hybrid economics are widening the customer base of the Europe irrigation pumps market. Photovoltaic module prices fell 15% to 20% between 2023 and 2025, while grid electricity costs rose sharply in several countries over the same period, improving the economics of solar-powered irrigation. Studies have reported that energy cost savings from solar-powered irrigation can reach 40% to 70% in southern Europe, with Spain and Portugal at the higher end because of stronger irradiance. The fastest adoption is not limited to pure solar. Hybrid solar-battery and solar-diesel setups are also gaining popularity because energy security matters as much as cost in regions where peak-season grid reliability is a production issue. National strategic plans in countries such as France, Italy, Romania, and Portugal also support on-farm solar investment under the Common Agricultural Policy framework. That support shortens payback periods and makes solar-compatible pump purchases easier to justify for high-value crop systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront pump-system capital expenditure for small and mid-size farms | -1.3% | Europe-wide, most acute in Eastern and Central Europe | Short term (≤ 2 years) |

| Groundwater permitting and abstraction caps | -0.8% | Spain, Italy, Belgium, Czech Republic, and England | Medium term (2-4 years) |

| Country-by-country grid and hybrid-system compliance complexity | -0.6% | Europe-wide, most pronounced in Eastern Europe | Medium term (2-4 years) |

| Water-savings rebound limits net pumping-volume growth | -0.5% | Spain, Italy, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Pump-System Capital Expenditure for Small and Mid-Size Farms

Capital cost remains the clearest demand restraint in the Europe irrigation pumps market. A full system upgrade that includes the pump, variable frequency drive, metering hardware, and installation can still place a heavy burden on farms that operate with tight seasonal cash flow. Regulation (European Union) 2021/2115 allows support for eligible investment costs, but the remaining co-payment still stretches practical machinery budgets in many small and mid-size farms, especially in central and eastern member states. The timing of reimbursement is part of the problem because support can arrive well after installation decisions must be made. Suppliers have responded with modular pump station formats, but the cost reduction has not yet been enough to bring turnkey upgrades within easy reach for the smallest operators. As a result, adoption is strongest where larger growers, cooperatives, and irrigation bodies can spread capital costs across more hectares or more users.

Groundwater Permitting and Abstraction Caps

Permitting pressure is also narrowing the easier growth pockets of the Europe irrigation pumps market. Water-stressed regions still need efficient pumping, but new groundwater withdrawals face more scrutiny, and that can delay or reduce expansion projects. Spain’s Royal Decree 1085/2024 connected reclaimed water use, sustainability assessments, and authorization procedures more closely, which adds procedural steps for projects that depend on new abstraction rights or water source changes. The same policy direction means that demand can shift from new capacity toward retrofit work, especially where reclaimed water schemes or replacement programs become the preferred path. Large installations in stressed basins can also face longer review periods under Water Framework Directive principles. This does not eliminate demand, but it changes its mix and makes planning more administrative than in the past.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Centrifugal Pumps Remain The Largest Base, While Positive Displacement Gains Speed

Centrifugal pumps held the largest market share and accounted for 71.2% of the Europe irrigation pumps market share in 2025. Their position reflects broad utility across surface abstraction, open-channel irrigation, and borehole-linked farm systems in both field crops and horticulture. Demand is strongest where operators need a familiar and flexible solution that can serve different heads and flow conditions without narrowing use to one crop system. Large public and consortium irrigation schemes also continue to rely on centrifugal formats, especially vertical turbine and split-case designs. Caprari S.p.A. illustrated this role in 2024 through its Scigliati plant project in Italy, which lifted basin irrigation flow capacity by more than 50% with 5 customized vertical lineshaft units.

The Europe irrigation pumps market size for positive displacement pumps is projected to expand at an 8.2% CAGR from 2026 to 2031. This growth is tied to uses that are more specialized than the main centrifugal category. Precision fertigation in vineyards, berry crops, orchards, and greenhouse systems needs controlled low-volume dosing, and that favors diaphragm and progressive cavity pump formats. The Europe irrigation pumps market is also seeing wider interest in reclaimed-water irrigation, and that supports niche use cases for vortex and solids-tolerant applications where standard impeller systems can wear faster. Submersible pumps remain a stable second-tier category because deep-well irrigation still matters in Spain and Italy, even as replacement demand shifts toward higher-efficiency and better-protected units. Taken together, product demand is separating into a high-volume mainstream centrifugal base and a faster specialty layer built around precision dosing, reclaimed water, and protected cultivation.

By Power Source: Grid-Electric Stays Largest, While Solar Changes The Upgrade Case

Grid-electric pumps held the largest market share at 72.5% in 2025, which kept them as the largest power-source segment in the Europe irrigation pumps market. Their lead comes from dense rural electrification, long-established electric pump infrastructure, and steady efficiency gains under motor and system upgrade programs. For many farms, grid connection still offers the simplest operating model, especially where irrigation seasons are predictable and system sizing is already aligned with local water demand. European manufacturers continue to invest in this category because efficiency upgrades can still unlock replacement sales without changing the whole irrigation layout. That keeps grid-electric pumping central to the installed base even as other energy options improve.

The Europe irrigation pumps market size for solar pumps is projected to expand at a 7.4% CAGR from 2026 to 2031. Cost improvement in photovoltaic modules and stronger support for on-farm renewable systems are moving solar from a niche option into a viable mainstream choice in selected geographies. Franklin Electric Co., Inc. reinforced this shift in early 2026 through launches aimed at agricultural, irrigation, and fertigation use, including the NCV Series and MHp Series for multistage applications. Hybrid systems are also expanding because growers in some markets value reliability and energy independence over pure cost savings. Italy’s agrivoltaics support structure added another push by aligning solar deployment with continued farm use of the land. As a result, power-source competition is no longer only about energy cost. It is also about resilience, subsidy fit, and the ability to pair pumps with precise water delivery.

Geography Analysis

Germany held the largest market share in 2025, accounting for 25.7% of the Europe irrigation pumps market. Germany is also the fastest-growing national segment, with the Europe irrigation pumps market size in the country projected to expand at a 7.9% CAGR from 2026 to 2031. This dual position reflects a deep installed base and a high replacement value per hectare, as growers and irrigation users favor precision-grade upgrades, digital controls, and premium, compliance-ready equipment. The local presence of KSB SE & Co. KGaA and Wilo SE also supports channel strength, product familiarity, and faster deployment of advanced pump solutions suited to data-led farming systems.

Spain and Italy continue to anchor the largest installed irrigation base by volume, making them central to the Europe irrigation pumps market. Their role is tied to climate-dependent supplemental irrigation, a broad mix of crop systems, and the continued need for deep-well, surface abstraction, and precision fertigation solutions. Spain is also moving more actively toward reclaimed water use under the new regulatory framework, which is driving demand for compatible pumping equipment and materials in reuse schemes. Italy remains highly tiered, with consortium-scale pumping, individual farm-borehole systems, and specialized positive-displacement pumps for vineyards, olives, and premium horticulture all present in one country. France adds another strong layer because it is a major Common Agricultural Policy beneficiary and therefore maintains an active pipeline for irrigation and related energy-efficiency upgrades.

The United Kingdom market is moving under tighter abstraction oversight, which supports demand for metered and compliant replacement systems while making new capacity additions harder to approve. Russia remains part of the regional scope but follows a separate investment logic because its agricultural modernization path is not tied to European Union policy structures. The Rest of Europe cluster, including Poland, Romania, the Netherlands, and Portugal, is gaining momentum as drought pressure and access to co-financing bring irrigation modernization further into the farm investment agenda. This means the Europe irrigation pumps market still leans on southern demand today, but the next layer of growth is spreading across central and eastern parts of the region from a smaller installed base.

Competitive Landscape

The Europe irrigation pumps market shows moderate concentration, with a premium tier led by Grundfos Holding A/S, KSB SE & Co. KGaA, Franklin Electric Co., Inc., Caprari S.p.A., and Xylem Inc., while Italian specialists remain highly active in the country and application niches. The leading companies hold their positions through broad centrifugal and submersible portfolios, strong distributor coverage, and a track record of meeting energy and compliance needs across different irrigation settings. Caprari S.p.A., Pedrollo S.p.A., DAB Pumps S.p.A., and SAER Elettropompe S.p.A. remain especially relevant in southern agricultural regions where local application knowledge and product familiarity matter. That keeps competition balanced between scale advantages and regional specialization.

Strategy in the Europe irrigation pumps market is moving beyond pump hardware alone. Xylem Inc. strengthened its digital position in 2024 by acquiring a majority stake in Spain-based Idrica and building the Xylem Vue platform around remote control, water index monitoring, and pump diagnostics. Franklin Electric Co., Inc. added another service-oriented layer in October 2025 through the Smart Control Box, which supports protection, control, and remote monitoring for irrigation and water applications. Grundfos Holding A/S expanded its broader service footprint in 2024 by acquiring Culligan’s commercial and industrial water treatment operations in Italy, France, and the United Kingdom, adding adjacent capabilities in water quality and service delivery. These moves show that suppliers increasingly compete on system intelligence, service depth, and lifecycle support rather than on initial equipment price alone.

Open space remains strongest where small and mid-size farms need simpler solar-hybrid packages and lower-cost digital retrofits for older installed assets. That is important because many growers still cannot justify full system replacement even when regulation and operating costs favor modernization. Firms that can retrofit monitoring, protection, and energy control onto legacy pumps may reach a wider part of the installed base than firms that focus only on full premium replacements. At the same time, application-specific engineering still matters in the agricultural irrigation pumps industry, especially in sand-laden groundwater, reclaimed water circuits, and high-value fertigation systems where generic designs can wear faster or lose dosing precision. This is why European specialists continue to matter even while larger multinationals build software and service layers around their pump portfolios.

Europe Irrigation Pumps Industry Leaders

Grundfos Holding A/S

Xylem Inc.

KSB SE & Co. KGaA

Franklin Electric Co., Inc.

Caprari S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Franklin Electric Co., Inc. launched the NCV Series vertical multistage pumps for agricultural, industrial, and residential water applications including irrigation, offering maximum flow rates up to 18 m3/h and heads up to 180 m with a multiple-mounting design for simplified maintenance.

- January 2026: KSB SE & Co. KGaA launched the Omega 2 series, a next-generation axially split volute casing pump with optimized hydraulics, double-entry impellers, and a self-centering rotor system for waterworks, distribution, and irrigation canal applications across Europe.

- July 2025: Franklin Electric Co., Inc. deployed a horizontal pond irrigation installation in a European agricultural operation, incorporating a 10-inch VSI submersible pump delivering up to 350 m3/h with a stainless-steel cooling shroud and PT100 temperature sensor.

Europe Irrigation Pumps Market Report Scope

An irrigation pump is a mechanical device used to draw water from a source, such as a well, river, or pond, and move it under pressure to agricultural fields. It powers watering systems like sprinklers, drips, or canals to provide crops with a controlled and consistent water supply.

The Europe irrigation pumps market report is segmented by product type, including centrifugal pumps, submersible pumps, positive displacement pumps, and vortex pumps, by power source, including grid-electric, diesel, solar, and hybrid solar-diesel and solar-battery, and by geography, including Germany, United Kingdom, France, Spain, Italy, Russia, and rest of Europe. The market forecasts are provided in terms of value in USD.

| Centrifugal Pumps | End-suction Surface Pumps |

| Split-case Pumps | |

| Vertical Turbine Pumps | |

| Submersible Pumps | Borehole Pumps |

| Submersible Multistage Pumps | |

| Positive Displacement Pumps | Diaphragm Pumps |

| Progressive Cavity Pumps | |

| Vortex Pumps |

| Grid-electric Pumps |

| Diesel Pumps |

| Solar Pumps |

| Hybrid Solar-Diesel and Solar-Battery Pumps |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Russia |

| Rest of Europe |

| By Product Type | Centrifugal Pumps | End-suction Surface Pumps |

| Split-case Pumps | ||

| Vertical Turbine Pumps | ||

| Submersible Pumps | Borehole Pumps | |

| Submersible Multistage Pumps | ||

| Positive Displacement Pumps | Diaphragm Pumps | |

| Progressive Cavity Pumps | ||

| Vortex Pumps | ||

| By Power Source | Grid-electric Pumps | |

| Diesel Pumps | ||

| Solar Pumps | ||

| Hybrid Solar-Diesel and Solar-Battery Pumps | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is driving demand for irrigation pumps in Europe?

Demand is being supported by water-scarcity-led replacement of older pump fleets, Common Agricultural Policy modernization funding, and stronger adoption of monitored and energy-efficient systems.

What is the projected size of the Europe irrigation pumps market by 2031?

The Europe irrigation pumps market is forecast to reach USD 3.80 billion by 2031 from USD 2.5 billion in 2026, advancing at an 8.80% CAGR over 2026 to 2031.

Which product category leads revenue across Europe?

Centrifugal pumps are the largest product segment and held 71.2% share in 2025 because they fit a wide range of irrigation tasks across surface, open-channel, and borehole use.

Which power source is growing fastest in farm irrigation pumping?

Solar pumps are the fastest power-source segment with a 7.4% CAGR from 2026 to 2031, supported by better solar economics and policy support for on-farm renewable investment.

Which country is the largest and fastest-growing within the region?

Germany is both the largest country segment with 25.7% share in 2025 and the fastest-growing one with a 7.9% CAGR through 2031, supported by high replacement values and precision-oriented upgrades.

What is the biggest barrier for smaller farms?

The largest barrier is upfront system cost, because even after subsidy support the remaining co-payment can still exceed practical machinery budgets for many small and mid-size operators.

Page last updated on: